Understanding Foreign Exchange Derivatives Using Trade … · 2019-05-08 · 9-12M 5% 12M+ 2%...

9

FEATURE ARTICLE 1 HONG KONG MONETARY AUTHORITY QUARTERLY BULLETIN MARCH 2018 By Monetary Management Department Understanding Foreign Exchange Derivatives Using Trade Repository Data: The Non-deliverable Forward Market 1 Based on turnover statistics from Bank for International Settlements (BIS) (2016), Triennial Central Bank Survey – Foreign Exchange Turnover in April 2016 (www.bis.org/publ/ rpfx16fx.pdf) and internal calculations using HKTR data. 2 For more information on the data used in this article, see Box 3: Trade repositories as a data source. 1. Introduction In recent years, Hong Kong has established a regulatory framework for over-the-counter (OTC) derivatives consistent with global standards, and implemented reforms in regulatory reporting, central clearing, as well as capital and margin requirements on uncleared derivatives. These developments are in line with the G20 commitment in 2009 to enhance transparency and reduce systemic risk in the OTC derivatives market. Starting from July 2017, under the requirement of regulatory reporting, all entities supervised by the HKMA or regulated by the Securities and Futures Commission (SFC), and certain central counterparties (CCPs), have to report their OTC derivatives transactions in the five asset classes of interest rate, foreign exchange (FX), credit, equity and commodity. Among these asset classes, the mandatory reporting of interest rate swaps and FX non-deliverable forwards (NDFs) started two years earlier in July 2015. Hong Kong is a major trading centre for FX derivatives, and NDFs in particular, with an estimated 10% of global turnover of FX derivatives trading and 30% of NDF trading. 1 Similar to other FX derivatives, the NDF is a forward contract for hedging currency risk or profiting from currency volatility, albeit subject to a different settlement process that makes its use attractive for certain currencies (see Box 1 for more detail). NDFs represent an estimated 16% of the overall FX derivatives market in Hong Kong by gross notional value. This article presents a description of the NDF market as seen through the data collected in Hong Kong at the beginning of 2018, and sets out the major developments in the market over the two years of 2016–2017. The results are derived from analysis of trade-level data reported to the Hong Kong Trade Repository (HKTR). 2 In terms of market structure, the NDF market is mostly traded at very short maturities. The major non-deliverable currencies are the Taiwanese dollar, the Korean won and the renminbi. Most of the outstanding positions are held by banks and other financial entities. Over the past two years, the NDF market experienced three major changes: a marked increase in central clearing; a change in currency composition; and an increasing involvement by other financial institutions relative to banks. Box 1 NDF: What is it? The NDF is a forward contract with a different settlement process. As in a standard forward contract, two counterparties agree to buy/sell a currency at a specified future date at an agreed exchange rate. The purpose is to lock in an exchange rate for a certain period in the future. At settlement, instead of exchanging the underlying currencies, NDF counterparties settle the trade’s profit or loss in a widely traded (“deliverable”) currency, most often the US dollar. The amount settled is the difference between the exchange rate agreed in the contract and the prevailing exchange rate observed at a specified future date, multiplied by the agreed notional amount. The most prevalent non-deliverable currencies are Asian and Latin American currencies.

Transcript of Understanding Foreign Exchange Derivatives Using Trade … · 2019-05-08 · 9-12M 5% 12M+ 2%...

FEATURE ARTICLE

1 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

By Monetary Management Department

Understanding Foreign Exchange Derivatives Using Trade Repository Data: The non-deliverable Forward market

1 BasedonturnoverstatisticsfromBankforInternationalSettlements(BIS)(2016),TriennialCentralBankSurvey–ForeignExchangeTurnoverinApril2016(www.bis.org/publ/rpfx16fx.pdf)andinternalcalculationsusingHKTRdata.

2 Formoreinformationonthedatausedinthisarticle,seeBox3:Traderepositoriesasadatasource.

1. Introduction

Inrecentyears,HongKonghasestablishedaregulatoryframeworkforover-the-counter(OTC)derivativesconsistentwithglobalstandards,andimplementedreformsinregulatoryreporting,centralclearing,aswellascapitalandmarginrequirementsonunclearedderivatives.ThesedevelopmentsareinlinewiththeG20commitmentin2009toenhancetransparencyandreducesystemicriskintheOTCderivativesmarket.

StartingfromJuly2017,undertherequirementofregulatoryreporting,allentitiessupervisedbytheHKMAorregulatedbytheSecuritiesandFuturesCommission(SFC),andcertaincentralcounterparties(CCPs),havetoreporttheirOTCderivativestransactionsinthefiveassetclassesofinterestrate,foreignexchange(FX),credit,equityandcommodity.Amongtheseassetclasses,themandatoryreportingofinterestrateswapsandFXnon-deliverableforwards(NDFs)startedtwoyearsearlierinJuly2015.

HongKongisamajortradingcentreforFXderivatives,andNDFsinparticular,withanestimated10%ofglobalturnoverofFXderivativestradingand30%ofNDFtrading.1SimilartootherFXderivatives,theNDFisaforwardcontractforhedgingcurrencyriskorprofitingfromcurrencyvolatility,albeitsubjecttoadifferentsettlementprocessthatmakesitsuseattractiveforcertaincurrencies(seeBox1formoredetail).NDFsrepresentanestimated16%oftheoverallFXderivativesmarketinHongKongbygrossnotionalvalue.

ThisarticlepresentsadescriptionoftheNDFmarketasseenthroughthedatacollectedinHongKongatthebeginningof2018,andsetsoutthemajordevelopmentsinthemarketoverthetwoyearsof2016–2017.Theresultsarederivedfromanalysisoftrade-leveldatareportedtotheHongKongTradeRepository(HKTR).2Intermsofmarketstructure,theNDFmarketismostlytradedatveryshortmaturities.Themajornon-deliverablecurrenciesaretheTaiwanesedollar,theKoreanwonandtherenminbi.Mostoftheoutstandingpositionsareheldbybanksandotherfinancialentities.Overthepasttwoyears,theNDFmarketexperiencedthreemajorchanges:amarkedincreaseincentralclearing;achangeincurrencycomposition;andanincreasinginvolvementbyotherfinancialinstitutionsrelativetobanks.

Box 1

nDF: What is it?

TheNDFisaforwardcontractwithadifferentsettlementprocess.Asinastandardforwardcontract,twocounterpartiesagreetobuy/sellacurrencyataspecifiedfuturedateatanagreedexchangerate.Thepurposeistolockinanexchangerateforacertainperiodinthefuture.Atsettlement,insteadofexchangingtheunderlyingcurrencies,NDFcounterpartiessettlethetrade’sprofitorlossinawidelytraded(“deliverable”)currency,mostoftentheUSdollar.Theamountsettledisthedifferencebetweentheexchangerateagreedinthecontractandtheprevailingexchangerateobservedataspecifiedfuturedate,multipliedbytheagreednotionalamount.Themostprevalentnon-deliverablecurrenciesareAsianandLatinAmericancurrencies.

2 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLEFEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

2. StylisedfactsontheNDFmarket

a. SizeoftheNDFmarket

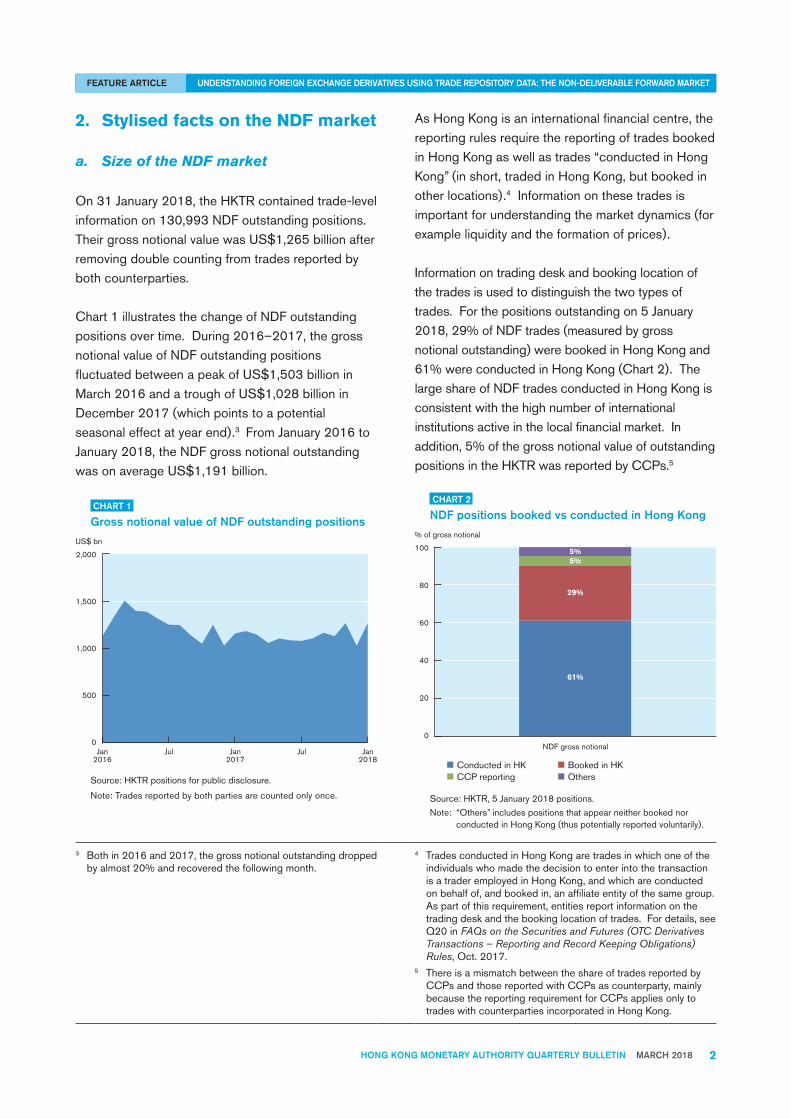

On31January2018,theHKTRcontainedtrade-levelinformationon130,993NDFoutstandingpositions.TheirgrossnotionalvaluewasUS$1,265billionafterremovingdoublecountingfromtradesreportedbybothcounterparties.

Chart1illustratesthechangeofNDFoutstandingpositionsovertime.During2016–2017,thegrossnotionalvalueofNDFoutstandingpositionsfluctuatedbetweenapeakofUS$1,503billioninMarch2016andatroughofUS$1,028billioninDecember2017(whichpointstoapotentialseasonaleffectatyearend).3FromJanuary2016toJanuary2018,theNDFgrossnotionaloutstandingwasonaverageUS$1,191billion.

CHART 1

gross notional value of nDF outstanding positions

0

500

1,000

2,000

1,500

US$ bn

Jan2016

Jul Jan2017

Jul Jan2018

Source:HKTRpositionsforpublicdisclosure.

Note:Tradesreportedbybothpartiesarecountedonlyonce.

AsHongKongisaninternationalfinancialcentre,thereportingrulesrequirethereportingoftradesbookedinHongKongaswellastrades“conductedinHongKong”(inshort,tradedinHongKong,butbookedinotherlocations).4Informationonthesetradesisimportantforunderstandingthemarketdynamics(forexampleliquidityandtheformationofprices).

Informationontradingdeskandbookinglocationofthetradesisusedtodistinguishthetwotypesoftrades.Forthepositionsoutstandingon5January2018,29%ofNDFtrades(measuredbygrossnotionaloutstanding)werebookedinHongKongand61%wereconductedinHongKong(Chart2).ThelargeshareofNDFtradesconductedinHongKongisconsistentwiththehighnumberofinternationalinstitutionsactiveinthelocalfinancialmarket.Inaddition,5%ofthegrossnotionalvalueofoutstandingpositionsintheHKTRwasreportedbyCCPs.5

CHART 2

nDF positions booked vs conducted in Hong Kong

0

20

40

60

80

100 5%

61%

29%

5%

% of gross notional

Conducted in HK Booked in HKCCP reporting Others

NDF gross notional

Source:HKTR,5January2018positions.

Note: “Others”includespositionsthatappearneitherbookednorconductedinHongKong(thuspotentiallyreportedvoluntarily).

3 Bothin2016and2017,thegrossnotionaloutstandingdroppedbyalmost20%andrecoveredthefollowingmonth.

4 TradesconductedinHongKongaretradesinwhichoneoftheindividualswhomadethedecisiontoenterintothetransactionisatraderemployedinHongKong,andwhichareconductedonbehalfof,andbookedin,anaffiliateentityofthesamegroup.Aspartofthisrequirement,entitiesreportinformationonthetradingdeskandthebookinglocationoftrades.Fordetails,seeQ20inFAQs on the Securities and Futures (OTC Derivatives Transactions – Reporting and Record Keeping Obligations) Rules,Oct.2017.

5 ThereisamismatchbetweentheshareoftradesreportedbyCCPsandthosereportedwithCCPsascounterparty,mainlybecausethereportingrequirementforCCPsappliesonlytotradeswithcounterpartiesincorporatedinHongKong.

FEATURE ARTICLE

3 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

6 Globally,LatinAmericancurrenciesrepresentanimportantclusterofnon-deliverablecurrencies,buttheyarenotheavilytradedinHongKong,likelyduetotimezonedifferences.

7 “Unidentified”entitiesarethosethatareunabletobeclassifiedintermsofsectorofactivityandcountryofincorporation.

b. Currenciesandmaturities

Unsurprisingly,Asiancurrenciesrepresentthelion’sshareofnon-deliverablecurrenciestradedinHongKong.InJanuary2018,theTaiwanesedollarwasthemostprevalentnon-deliverablecurrency,accountingfor26%oftheoutstandinggrossnotional(Chart3).Othermajornon-deliverablecurrenciesweretheKoreanwon(25%ofgrossnotional),therenminbi(23%),theIndianrupee(15%)andtheMalaysianringgit(2%).Theremaining9%ofgrossnotionalwascomprisedofaverybroadrangeofcurrencies,includinganumberofLatinAmericancurrencies,eachaccountingforlessthan2%ofthegrossnotional.6USdollarwasthesettlementcurrencyinnearlyalloftheNDFtrades(99%ofthegrossnotional).

ThematurityofNDFtradestendstoberelativelyshort.OverthreequartersoftheNDFoutstandingtrades,measuredbygrossnotionalvalue,hadaresidualmaturityofuptothreemonths(Chart3).Maturitiesbetweenthreemonthsandoneyearaccountedforanother23%.NDFtradeswitharemainingmaturityoveroneyearaccountedforlessthan2%.

CHART 3

Currency and maturity breakdown of nDF positions

0

20

40

60

80

100%

By non-deliverable currency By residual maturity

TWD 26%

KRW 25%

CNY 23%

IND 15%

MYR 2%

Others 10%

0-3M 76%

3-6M 12%

6-9M 6%9-12M 5%

12M+ 2%

Source:HKTR,5January2018positions.

Note: Percentagesdonotsumto100duetoroundingeffects.

c. Marketparticipants

InlinewiththeOTCderivativesmarketingeneral,theNDFmarketisrelativelyconcentratedaroundthetopdealers.AsshownintheHKTRdataasat5January2018,129financialentities(whichbelongto70groups)reportedNDFtradestotheHKTR.Thetopfiveinstitutionsaccountedfor48%oftheoutstandinggrossnotionalwhilethetoptenentitiesaccountedfor64%ofthegrossnotional(Chart4).

CHART 4

market participants subject to mandatory reporting

%

0

25

50

75

100

NDF gross notional

Others:36%

Top 10entities:

64%

Top 6-10entities:

16%

Top 5entities:

48%

Source:HKTR,5January2018positions.

Note:ExcludesCCPs.

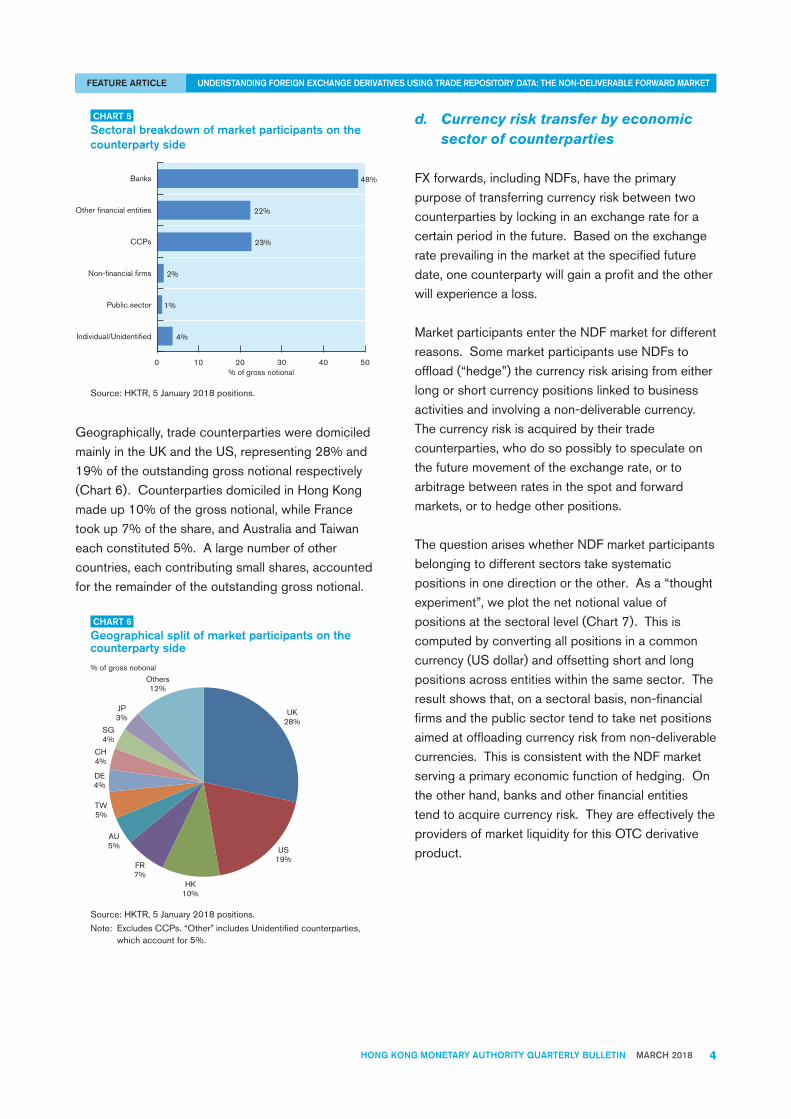

Tradecounterpartiesaresignificantlymorediverse.Asshowninthesamesetofdata,2,400distinctentities,whichbelongtoaround1,600groups,wereidentified.Chart5presentsabreakdownoftradecounterpartiesbysector.In48%ofthetrades(byoutstandinggrossnotional),bankswerethecounterparty.Thenon-bankfinancialsector(whichincludesinvestmentbanks,assetmanagers,hedgefundsandinsurers)wascounterpartyto22%oftheoutstandinggrossnotional.CCPswerecounterpartyto23%oftrades(byoutstandinggrossnotional),reflectingtheirincreasinginvolvementinprovidingcentralclearingtotheNDFmarket.Thecorporatenon-financialsectoraccountedfor2%oftheoutstandinggrossnotional,whilepublicsectorinstitutions,privateindividualsandunidentifiedentitiesaccountedfortheremaining5%.7

4 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLEFEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

CHART 5

sectoral breakdown of market participants on the counterparty side

4%

1%

2%

23%

22%

48%

0 10 20 30 40 50% of gross notional

Individual/Unidentified

Non-financial firms

Public sector

CCPs

Other financial entities

Banks

Source:HKTR,5January2018positions.

Geographically,tradecounterpartiesweredomiciledmainlyintheUKandtheUS,representing28%and19%oftheoutstandinggrossnotionalrespectively(Chart6).CounterpartiesdomiciledinHongKongmadeup10%ofthegrossnotional,whileFrancetookup7%oftheshare,andAustraliaandTaiwaneachconstituted5%.Alargenumberofothercountries,eachcontributingsmallshares,accountedfortheremainderoftheoutstandinggrossnotional.

CHART 6

geographical split of market participants on the counterparty side

UK28%

US19%

HK10%

FR7%

AU5%

TW5%

DE4%

CH4%

SG4%

JP3%

Others12%

% of gross notional

Source:HKTR,5January2018positions.

Note: ExcludesCCPs.“Other”includesUnidentifiedcounterparties,whichaccountfor5%.

d. Currencyrisktransferbyeconomicsectorofcounterparties

FXforwards,includingNDFs,havetheprimarypurposeoftransferringcurrencyriskbetweentwocounterpartiesbylockinginanexchangerateforacertainperiodinthefuture.Basedontheexchangerateprevailinginthemarketatthespecifiedfuturedate,onecounterpartywillgainaprofitandtheotherwillexperiencealoss.

MarketparticipantsentertheNDFmarketfordifferentreasons.SomemarketparticipantsuseNDFstooffload(“hedge”)thecurrencyriskarisingfromeitherlongorshortcurrencypositionslinkedtobusinessactivitiesandinvolvinganon-deliverablecurrency.Thecurrencyriskisacquiredbytheirtradecounterparties,whodosopossiblytospeculateonthefuturemovementoftheexchangerate,ortoarbitragebetweenratesinthespotandforwardmarkets,ortohedgeotherpositions.

ThequestionariseswhetherNDFmarketparticipantsbelongingtodifferentsectorstakesystematicpositionsinonedirectionortheother.Asa“thoughtexperiment”,weplotthenetnotionalvalueofpositionsatthesectorallevel(Chart7).Thisiscomputedbyconvertingallpositionsinacommoncurrency(USdollar)andoffsettingshortandlongpositionsacrossentitieswithinthesamesector.Theresultshowsthat,onasectoralbasis,non-financialfirmsandthepublicsectortendtotakenetpositionsaimedatoffloadingcurrencyriskfromnon-deliverablecurrencies.ThisisconsistentwiththeNDFmarketservingaprimaryeconomicfunctionofhedging.Ontheotherhand,banksandotherfinancialentitiestendtoacquirecurrencyrisk.TheyareeffectivelytheprovidersofmarketliquidityforthisOTCderivativeproduct.

FEATURE ARTICLE

5 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

CHART 7

Currency risk transfer in the nDF market by types of counterparty(Netnotionalpositionsinnon-deliverablecurrenciesbysector)

-20

-10

-15

-5

0

5

Sell non-deliverable currencyBuy deliverable currencySell deliverable currencyBuy non-deliverable currency

Non-financialfirms

Publicsector

Other financialentities

Unidentified

Banks

US$ bn

Source:HKTR,5January2018positions.

Notes:

1. ExcludesCCPsandIndividuals.2. Whilenetnotionalpositionscomputedacrossthewholemarketby

definitionoffseteachother,inthecharttheorangeandbluebarsdonothavetooffseteachotherinsize.EachsectorhasentitiesengaginginbothsidesofNDFtrades.Thesizeofthebarisfromoffsettinglongandshortpositionswithinthesamesector,whereasinrealitymanyNDFtradesarebetweenentitiesfromdifferentsectors.

3. ChangesinthestructureoftheNDFmarket

TheanalysisofHKTRdatasuggeststhatduring2016–2017,theNDFmarketstructurechangedalongthreedimensions:

• SharpincreaseofcentralclearingofNDFs;• ChangeinthecurrencycompositionofNDFs;

and• ShiftofsomeNDFactivitiesfrombankstoother

financialinstitutions.

a. SharpincreaseofcentralclearingofNDFs

During2016–2017,theNDFmarketexperiencedamarkedincreaseinNDFtradesbeingclearedthroughcentralcounterparties(Chart8).ThisisconsistentwithothermarketreportsanalysingCCPs’publicdisclosures.8TheriseincentralclearingintheNDFmarketisvoluntaryascentralclearingofNDFisnotmandatedinanymajorjurisdiction.

CHART 8

gross notional value of outstanding nDF positions being centrally cleared

0

500

1,500

1,000

2,000

US$ bn

NDF - intended to clearNDF - positions

NDF - not intended to clear

Jan2016

Jul Jan2017

Jul Jan2018

Source:HKTRpositionsforpublicdisclosure.

Note: “Intendedtoclear”isafieldreportedbythereportingentity.Tradesreportedbybothpartiesarecountedonlyonce.

AsshownintheHKTRdataasat31January2018,thegrossnotionaloutstandingintendedforcentralclearing(whichincludestradesthathadbeenclearedaswellasbilateraltradesthatwereexpectedtogothroughcentralclearing)wasUS$372billion,upfromUS$181billionayearearlierandfromUS$56billiontwoyearsearlier.

8 ChrisBarnes(2017),FX Clearing–The$750BNmarketthatkeepsgrowing,Clarus FT(www.clarusft.com/fx-clearing-the-750bn-market-that-keeps-growing).

6 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLEFEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

Thepercentageofnewtradesbeingclearedcentrally,whichwaspreviouslystableataround2%to4%levels,rosesharplyto12%inthefourthquarterof2016(Chart9).Itcontinuedtoriseandreached29%inthefourthquarterof2017.TakingintoaccountalloutstandingpositionsatthebeginningofJanuary2018,24%ofthetotaloutstandinggrossnotionalwascentrallycleared.

CHART 9

percentage of cleared nDF positions

24%

3%2%

4%

12%

15%

19%

22%

29%

0

35

30

25

20

15

10

5

% gross notional cleared

Cleared new tradesCleared positions

Q12016

Q2 Q3 Q4 Q2 Q3 Q4Q12017

Source:HKTR.

Note: Theredlinereferstonewtradesoriginatedin2016–2017.Thegreybarreferstooutstandingpositionson5January2018.

ClearingisnotequallycommonacrossAsiancurrencies.Inthepositionsoutstandingon5January2018,thecurrencieswiththelargestclearedvolumesweretheTaiwanesedollar,therenminbi,theIndianrupeeandtheKoreanwon(Chart10).Amongthesecurrencies,theclearingratewas27%fortheTaiwanesedollarandtheIndianrupee,22%forthe

renminbiand15%fortheKoreanwon.ThePhilippinepeso,theIndonesianrupiahandtheMalaysianringgithadsignificantlysmallerclearedvolumesandarangeofclearingrates.ThePhilippinepesohadthehighestpercentageofclearedtradesamongallAsiancurrenciesat31%.

CHART 10

Cleared nDF positions by currency

0

20

40

60

80

100

120

0

5

10

15

20

25

30

35

27%

22%

27%

15%

31%

22%

15%

US$ bn

% cleared positions (rhs)Cleared positions, gross notional outstanding (lhs)

TWD CNY INR KRW PHP IDR MYR

% gross notional

Source:HKTR,5January2018positions.

OnedriverofthevoluntaryincreaseincentralclearingofNDFsislikelytohavebeentheimplementationofreformsonmarginrequirements,whichalteredtherelativepricesofclearedandunclearedderivatives.Box2outlineshowmarginrequirementswereimplementedinmajorjurisdictionsandhow,bymakingitmorecostlytoholdunclearedOTCderivatives,thereformhascreatedincentivesforvoluntaryclearing.

FEATURE ARTICLE

7 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

Box 2

How reforms on margin requirements affected the nDF market

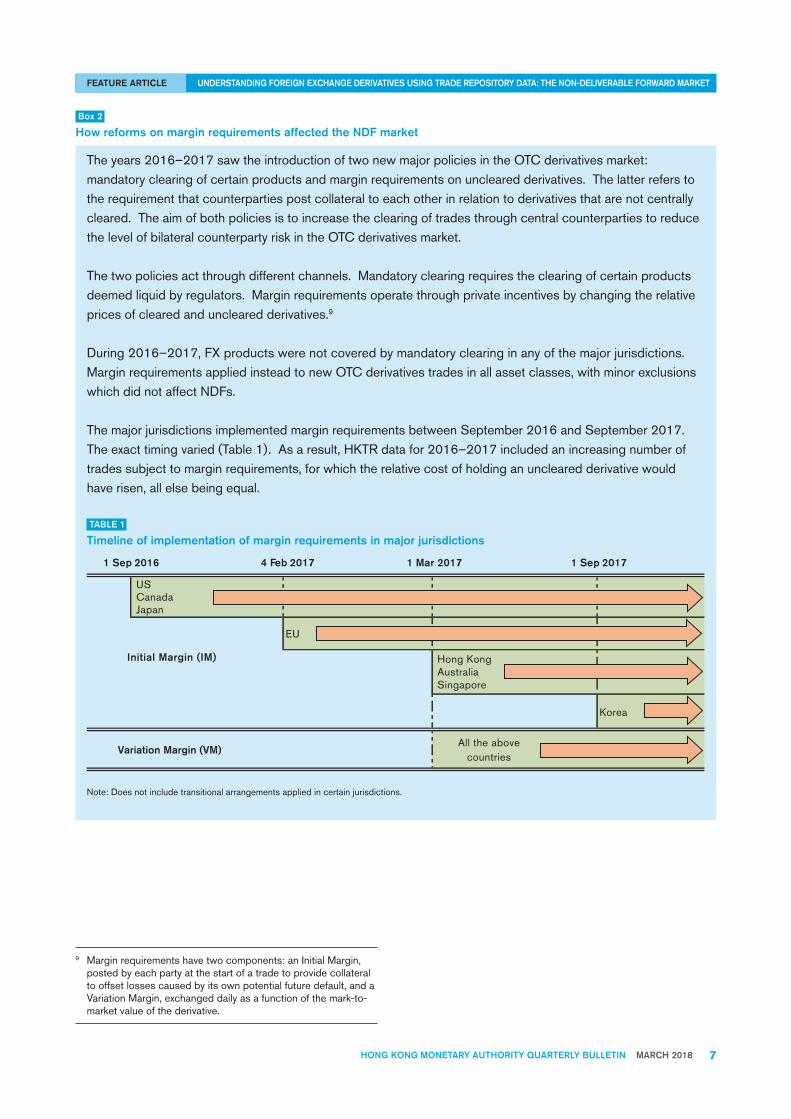

Theyears2016–2017sawtheintroductionoftwonewmajorpoliciesintheOTCderivativesmarket:mandatoryclearingofcertainproductsandmarginrequirementsonunclearedderivatives.Thelatterreferstotherequirementthatcounterpartiespostcollateraltoeachotherinrelationtoderivativesthatarenotcentrallycleared.TheaimofbothpoliciesistoincreasetheclearingoftradesthroughcentralcounterpartiestoreducethelevelofbilateralcounterpartyriskintheOTCderivativesmarket.

Thetwopoliciesactthroughdifferentchannels.Mandatoryclearingrequirestheclearingofcertainproductsdeemedliquidbyregulators.Marginrequirementsoperatethroughprivateincentivesbychangingtherelativepricesofclearedandunclearedderivatives.9

During2016–2017,FXproductswerenotcoveredbymandatoryclearinginanyofthemajorjurisdictions.MarginrequirementsappliedinsteadtonewOTCderivativestradesinallassetclasses,withminorexclusionswhichdidnotaffectNDFs.

ThemajorjurisdictionsimplementedmarginrequirementsbetweenSeptember2016andSeptember2017.Theexacttimingvaried(Table1).Asaresult,HKTRdatafor2016–2017includedanincreasingnumberoftradessubjecttomarginrequirements,forwhichtherelativecostofholdinganunclearedderivativewouldhaverisen,allelsebeingequal.

TABLE 1

Timeline of implementation of margin requirements in major jurisdictions

1 Sep 2016 4 Feb 2017 1 Mar 2017 1 Sep 2017

USCanadaJapan

EU

Initial Margin (IM)

Korea

Variation Margin (VM)All the above

countries

Hong KongAustraliaSingapore

Note:Doesnotincludetransitionalarrangementsappliedincertainjurisdictions.

9 Marginrequirementshavetwocomponents:anInitialMargin,postedbyeachpartyatthestartofatradetoprovidecollateraltooffsetlossescausedbyitsownpotentialfuturedefault,andaVariationMargin,exchangeddailyasafunctionofthemark-to-marketvalueofthederivative.

8 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLEFEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

b. ChangeincurrencycompositionofNDFs

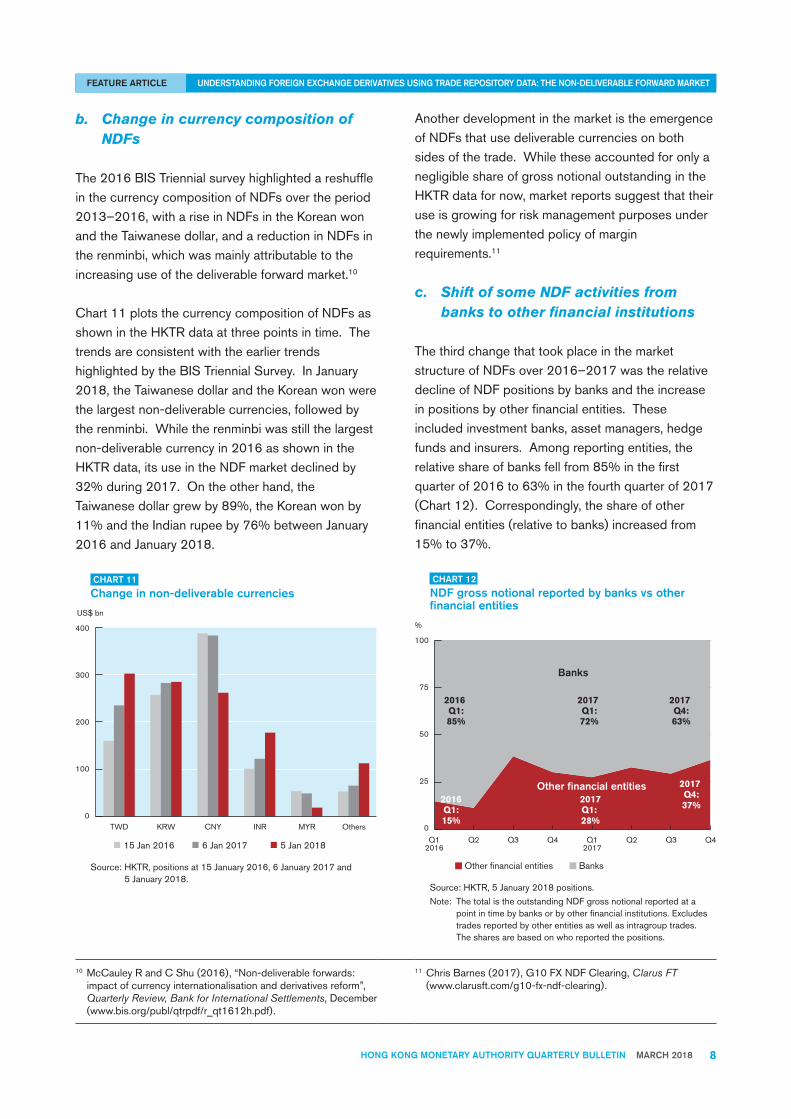

The2016BISTriennialsurveyhighlightedareshuffleinthecurrencycompositionofNDFsovertheperiod2013–2016,withariseinNDFsintheKoreanwonandtheTaiwanesedollar,andareductioninNDFsintherenminbi,whichwasmainlyattributabletotheincreasinguseofthedeliverableforwardmarket.10

Chart11plotsthecurrencycompositionofNDFsasshownintheHKTRdataatthreepointsintime.ThetrendsareconsistentwiththeearliertrendshighlightedbytheBISTriennialSurvey.InJanuary2018,theTaiwanesedollarandtheKoreanwonwerethelargestnon-deliverablecurrencies,followedbytherenminbi.Whiletherenminbiwasstillthelargestnon-deliverablecurrencyin2016asshownintheHKTRdata,itsuseintheNDFmarketdeclinedby32%during2017.Ontheotherhand,theTaiwanesedollargrewby89%,theKoreanwonby11%andtheIndianrupeeby76%betweenJanuary2016andJanuary2018.

CHART 11

Change in non-deliverable currencies

0

100

200

300

400

15 Jan 2016 6 Jan 2017 5 Jan 2018

TWD KRW CNY INR MYR Others

US$ bn

Source:HKTR,positionsat15January2016,6January2017and5January2018.

AnotherdevelopmentinthemarketistheemergenceofNDFsthatusedeliverablecurrenciesonbothsidesofthetrade.WhiletheseaccountedforonlyanegligibleshareofgrossnotionaloutstandingintheHKTRdatafornow,marketreportssuggestthattheiruseisgrowingforriskmanagementpurposesunderthenewlyimplementedpolicyofmarginrequirements.11

c. ShiftofsomeNDFactivitiesfrombankstootherfinancialinstitutions

ThethirdchangethattookplaceinthemarketstructureofNDFsover2016–2017wastherelativedeclineofNDFpositionsbybanksandtheincreaseinpositionsbyotherfinancialentities.Theseincludedinvestmentbanks,assetmanagers,hedgefundsandinsurers.Amongreportingentities,therelativeshareofbanksfellfrom85%inthefirstquarterof2016to63%inthefourthquarterof2017(Chart12).Correspondingly,theshareofotherfinancialentities(relativetobanks)increasedfrom15%to37%.

CHART 12

nDF gross notional reported by banks vs other financial entities

0

25

50

75

100

%

Q12016

Q2 Q3 Q4 Q2 Q3 Q4Q12017

2016Q1:15%

2017Q1: 28%

2017 Q4:37%

2016 Q1:85%

2017 Q1:72%

2017 Q4:63%

Banks

Other financial entities

Other financial entities Banks

Source:HKTR,5January2018positions.

Note: ThetotalistheoutstandingNDFgrossnotionalreportedatapointintimebybanksorbyotherfinancialinstitutions.Excludestradesreportedbyotherentitiesaswellasintragrouptrades.Thesharesarebasedonwhoreportedthepositions.

10McCauleyRandCShu(2016),“Non-deliverableforwards:impactofcurrencyinternationalisationandderivativesreform”,Quarterly Review, Bank for International Settlements,December(www.bis.org/publ/qtrpdf/r_qt1612h.pdf).

11ChrisBarnes(2017),G10FXNDFClearing,Clarus FT(www.clarusft.com/g10-fx-ndf-clearing).

FEATURE ARTICLE

9 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

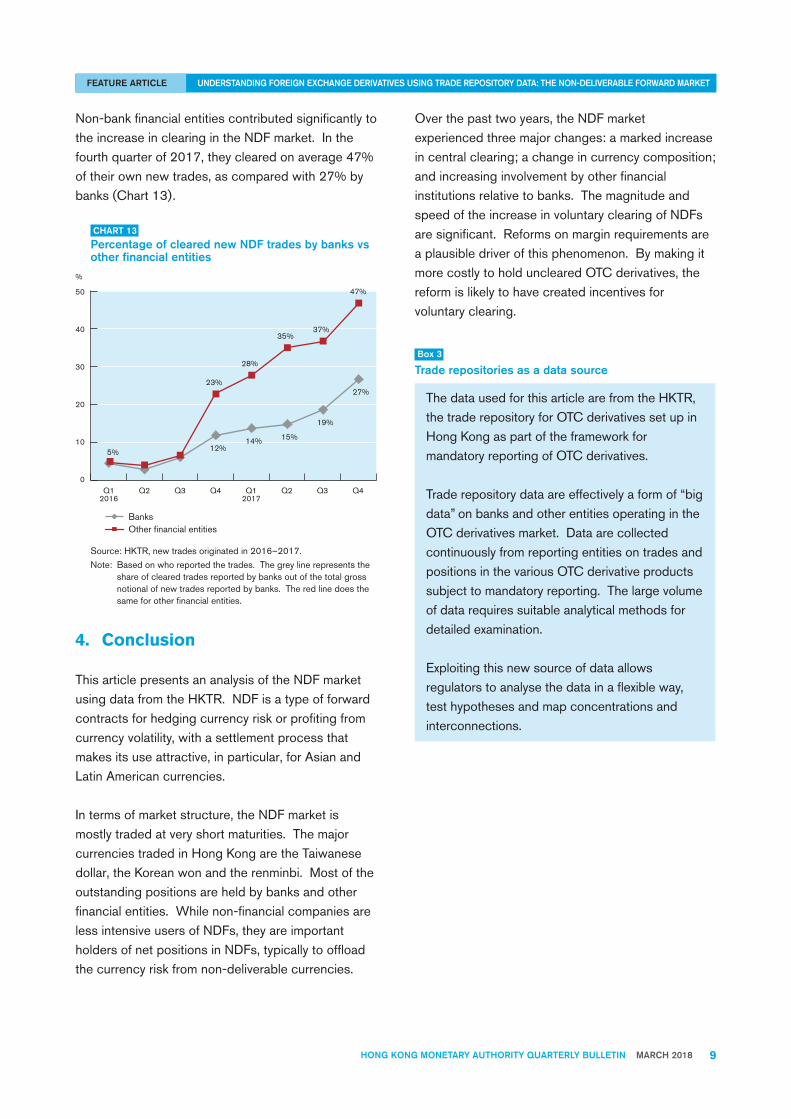

Non-bankfinancialentitiescontributedsignificantlytotheincreaseinclearingintheNDFmarket.Inthefourthquarterof2017,theyclearedonaverage47%oftheirownnewtrades,ascomparedwith27%bybanks(Chart13).

CHART 13

percentage of cleared new nDF trades by banks vs other financial entities

12%14% 15%

19%

27%

5%

23%

28%

35%37%

47%

0

50

40

30

20

10

%

Other financial entitiesBanks

Q12016

Q2 Q3 Q4 Q2 Q3 Q4Q12017

Source:HKTR,newtradesoriginatedin2016–2017.

Note: Basedonwhoreportedthetrades.Thegreylinerepresentstheshareofclearedtradesreportedbybanksoutofthetotalgrossnotionalofnewtradesreportedbybanks.Theredlinedoesthesameforotherfinancialentities.

4. Conclusion

ThisarticlepresentsananalysisoftheNDFmarketusingdatafromtheHKTR.NDFisatypeofforwardcontractsforhedgingcurrencyriskorprofitingfromcurrencyvolatility,withasettlementprocessthatmakesitsuseattractive,inparticular,forAsianandLatinAmericancurrencies.

Intermsofmarketstructure,theNDFmarketismostlytradedatveryshortmaturities.ThemajorcurrenciestradedinHongKongaretheTaiwanesedollar,theKoreanwonandtherenminbi.Mostoftheoutstandingpositionsareheldbybanksandotherfinancialentities.Whilenon-financialcompaniesarelessintensiveusersofNDFs,theyareimportantholdersofnetpositionsinNDFs,typicallytooffloadthecurrencyriskfromnon-deliverablecurrencies.

Overthepasttwoyears,theNDFmarketexperiencedthreemajorchanges:amarkedincreaseincentralclearing;achangeincurrencycomposition;andincreasinginvolvementbyotherfinancialinstitutionsrelativetobanks.ThemagnitudeandspeedoftheincreaseinvoluntaryclearingofNDFsaresignificant.Reformsonmarginrequirementsareaplausibledriverofthisphenomenon.BymakingitmorecostlytoholdunclearedOTCderivatives,thereformislikelytohavecreatedincentivesforvoluntaryclearing.

Box 3

Trade repositories as a data source

ThedatausedforthisarticlearefromtheHKTR,thetraderepositoryforOTCderivativessetupinHongKongaspartoftheframeworkformandatoryreportingofOTCderivatives.

Traderepositorydataareeffectivelyaformof“bigdata”onbanksandotherentitiesoperatingintheOTCderivativesmarket.DataarecollectedcontinuouslyfromreportingentitiesontradesandpositionsinthevariousOTCderivativeproductssubjecttomandatoryreporting.Thelargevolumeofdatarequiressuitableanalyticalmethodsfordetailedexamination.

Exploitingthisnewsourceofdataallowsregulatorstoanalysethedatainaflexibleway,testhypothesesandmapconcentrationsandinterconnections.