ULIP Prospects Challenges_Group 5_Section C

26

Presented By Group – 5, Section C A mbi c a Prasad P GP / 1 4 / 1 9 2 A mit S ansi P GP / 1 4 / 1 9 3 Gopi Krishna PGP/14/196 Deepak Prasad PGP/14/210

-

Upload

amit-manohar-sansi -

Category

Documents

-

view

217 -

download

0

Transcript of ULIP Prospects Challenges_Group 5_Section C

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 1/26

Presented By

Group – 5, Section C

Ambica Prasad PGP/14/192

Amit Sansi PGP/14/193

Gopi Krishna PGP/14/196

Deepak Prasad PGP/14/210

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 2/26

Investopedia definition :• Insurance is a form of risk management in which one entity transfers the

cost of potential loss to another entity in exchange for monetarycompensation

Designed to protect the financial well-being of the individual

Important Terms in an insurance

• Insurer

• Insured

• Premium

Basically an excellent risk-management and wealth preservation tool

Required by Law in some cases

Insurance involves pooling funds from many insured entities to pay for thelosses that some may incur

Contingency contract

What is Insurance

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 3/26

Auto

Life

Health

Home

Disability

Business

Types of Insurance

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 4/26

Insurance provides security and safety

Gives you a peace of mind

Protects against mortgage payments

Eliminates dependency

Encourages saving

Means of investment

Why is Insurance needed

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 5/26

What are ULIPs?• Abbreviation for Unit Linked Insurance Policy

Provides combination of Risk cover and Investment

Investment risks may also be borne by policy holder

Life insurance monies and investments are exposed to risks

More expensive than maintaining insurance and Mutual Funds separately

Understanding ULIPs

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 6/26

Type I - a life insurance policy linked to an investment account

Type II - links life insurance to investments

Pension - links two types of benefits: life insurance and retirement income

Types of ULIPs

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 7/26

National agency based out Hyderabad

Established to protect interests of insurance holders

Also to regulate the insurance industry and to ensure order and speedygrowth

IRDA vs. SEBI spat• Who controls ULIPs

IRDA

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 8/26

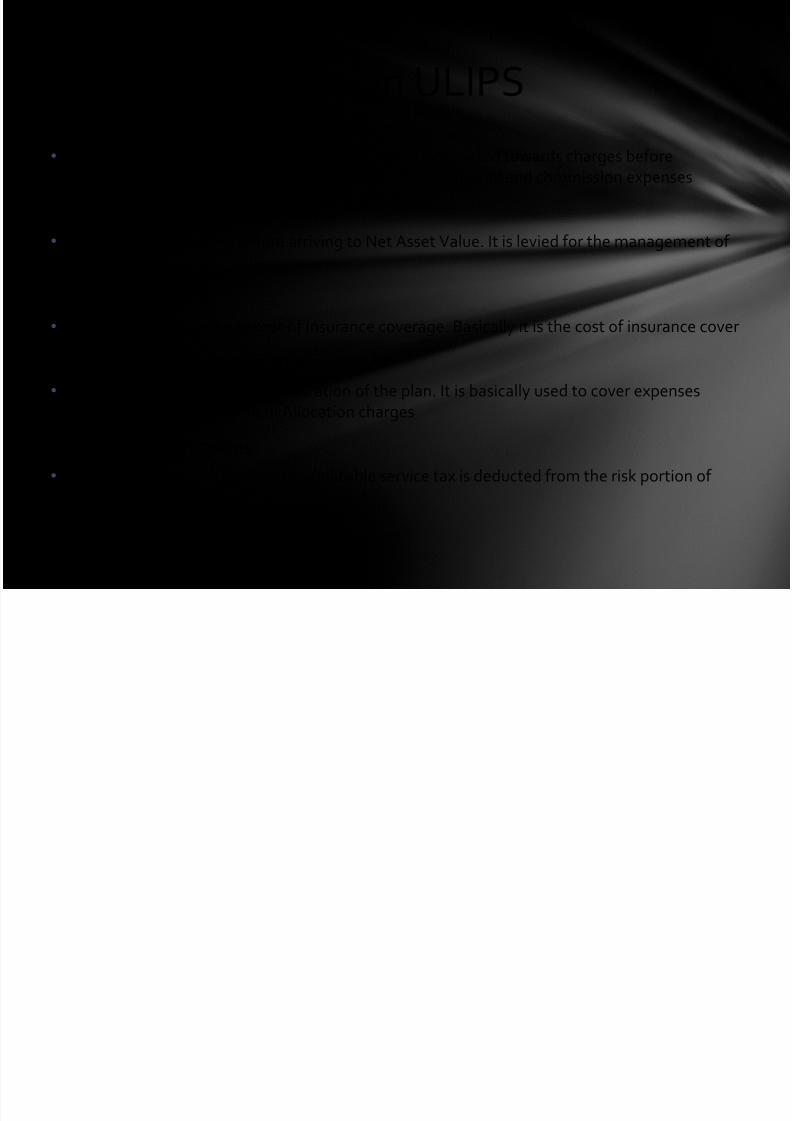

Premium Allocation Charge

• It can be defined as the percentage of premium appropriated towards charges before

allocating the unit under the policy. It includes initial/renewal and commission expenses

Fund Management Charge (FMC)

• This charge is deducted before arriving to Net Asset Value. It is levied for the management of

funds

Mortality Charges

• Mortality charges provide cost of insurance coverage. Basically it is the cost of insurance cover

Policy/Administration charges

• This is the fees levied for administration of the plan. It is basically used to cover expenses

other than FMC and Premium Allocation charges

Service Tax Deductions

• Before allotment of the units the applicable service tax is deducted from the risk portion of

the premium

Charges on ULIPS

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 9/26

Surrender Charges

• Surrender charges may be deducted on premature partial or full encashment of units as per

the policy

Switching Charge

• Within a product if you switch from one fund to another then switching charges are levied

Rider premium charge • This is the premium exclusive of expense loadings levied separately to cover the cost of rider

cover levied either by cancellation of units or by debiting the premium but not both

Partial withdrawal charge

• This is a charge levied on the unit fund at the time of part withdrawal of the fund during the

contract period

Miscellaneous charge

• This is a charge levied for any alterations within the contract, such as, increase in sum assured,

premium redirection, change in policy term etc

Charges on ULIPS

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 10/26

Mutual fund is a mechanism for pooling the resources byissuing units to the investors and investing funds in securities inaccordance with objectives as disclosed in offer document

Investments in securities are spread across a wide cross-

section of industries and sectors and thus the risk is reducedThe profits or losses are shared by the investors in proportionto their investments

A mutual fund is required to be registered with Securities and

Exchange Board of India (SEBI) which regulates securitiesmarkets before it can collect funds from the public

A Mutual Fund

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 11/26

Expense Ratio

• This basket of charges comprises the fund management fee, agentcommission, registrar fees and the selling and promotion expenses

• Front End Load

• It is associated with class “A” shares of Mutual funds. This fee is

paid when the shares are purchased. It typically goes to the brokerthat sells the fund’s shares. It is also known as “sales charge”

• No Load Fund

• It is associated with class “C” shares. In this the fund does not

charge any type of sales load• Back End Load

• It is associated with class “B” Mutual fund shares. This fee is paidwhen the shares are sold. It also goes to the broker that sells thefund’s shares

Charges in Mutual Funds

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 12/26

Purchase fee: • This fee is levied on the shareholders by some funds at the time of

purchase of shares. Difference between purchase fee and front endload is that this charge goes to the fund and not to the broker.

Redemption fee: • This fee is levied on the shareholders by some funds at the time

shares are sold. Difference between redemption fee and front endload is that this charge goes to the fund and not to the broker

Exchange fee: • This fee is levied on the shareholders by some funds at the time of

transfer of fund within the same fund family.

Transaction fees

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 13/26

Mutual Funds vs. ULIPULIPs Mutual Funds

Investment amountDetermined by the investorand can be modified as well

Minimum investmentamounts are determined by

the fund house

Expenses No upper limits, expensesdetermined by the insurance

company

Upper limits for expenseschargeable to investors have

been set by the regulator

Modifying asset allocationGenerally permitted for free

or at a nominal costEntry/exit loads have to be

borne by the investor

Tax benefits Section 80C benefits areavailable on all ULIPinvestments

Section 80C benefits areavailable only on investmentsin tax-saving funds

Portfolio disclosure Not mandatory Quarterly disclosures aremandatory

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 14/26

Advantagesof ULIP

ULIP's provide insurance cover

All ULIP's come under section 80C and can saveinvestors tax

Additional benefits like Critical illness cover,Accidental benefits can be purchased too

Premature redemption is allowed in ULIP's. It is

not allowed in MF's

Provides flexibility in investment. An investor canchoose an appropriate policy as per his risk taking

appetite. One can also shift between fundoptions

Equity and debt allocation details

Age band Equity component Debt component

0 - 25 85% 15%

26 - 35 75% 25%

36 - 45 65% 35%

46 - 55 55% 45%

56 - 65 45% 55%

66 - 75 35% 65%

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 15/26

Disadvantagesof ULIP

ULIP's come with a huge entry load. MF's do nothave any entry load

ULIP's maturity period is generally 5-20 years.Hence not suitable for short term investment

ULIP's have a compulsion of investment. They willat least make you pay the first 3 premiums

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 16/26

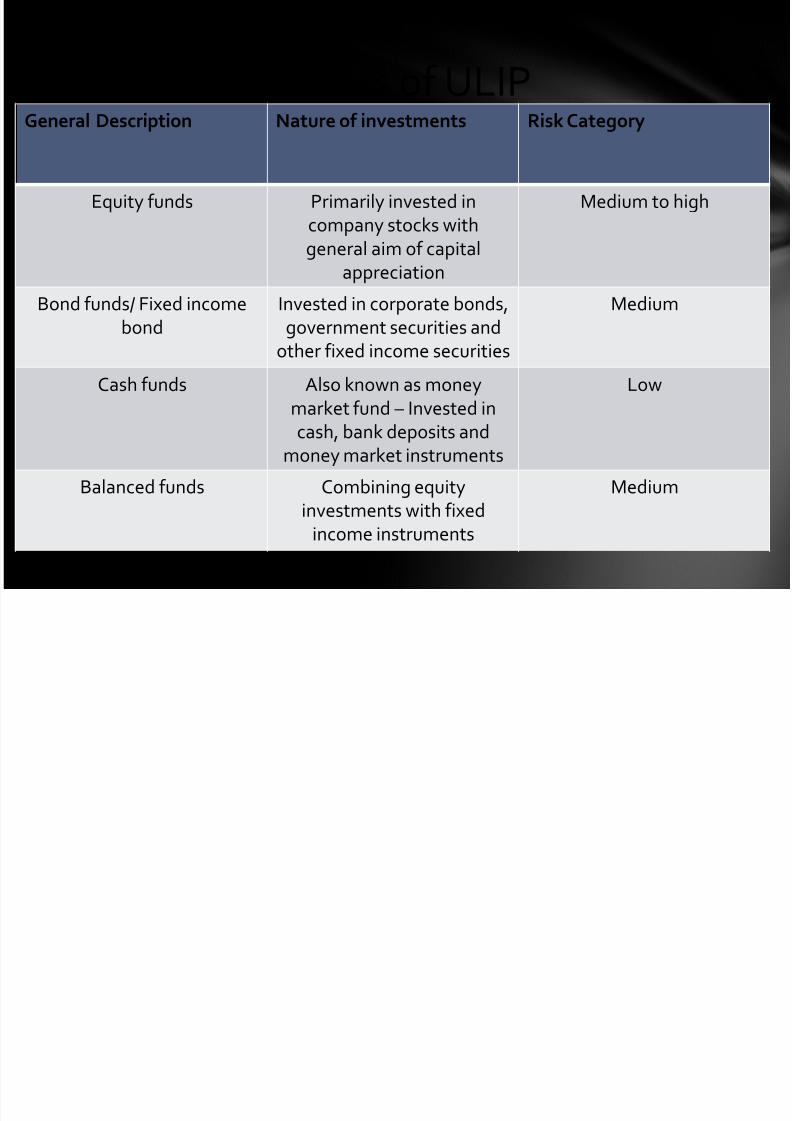

Categories of ULIPGeneral Description Nature of investments Risk Category

Equity funds Primarily invested incompany stocks withgeneral aim of capital

appreciation

Medium to high

Bond funds/ Fixed incomebond

Invested in corporate bonds,government securities and

other fixed income securities

Medium

Cash funds Also known as money

market fund – Invested incash, bank deposits andmoney market instruments

Low

Balanced funds Combining equityinvestments with fixed

income instruments

Medium

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 17/26

Performance of ULIPs

0.00

5.00

10.00

15.00

20.00

25.00

0

20

40

60

80

100

120

140

160

180

80-100%

Equity

Diversified

Plans

60-100%

Equity

Diversified

Plans

10-100%

Equity

Diversified

Plans

Index

Plans

Hybrid

Equity

Oriented

Plans

Hybrid

Debt

Oriented

Plans

Guaranteed

Plans

Debt

Plans

Gilt Plans Liquid

Plans

ULIPs and performance

No. of Plans Return Since Inception(in CAGR)

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 18/26

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

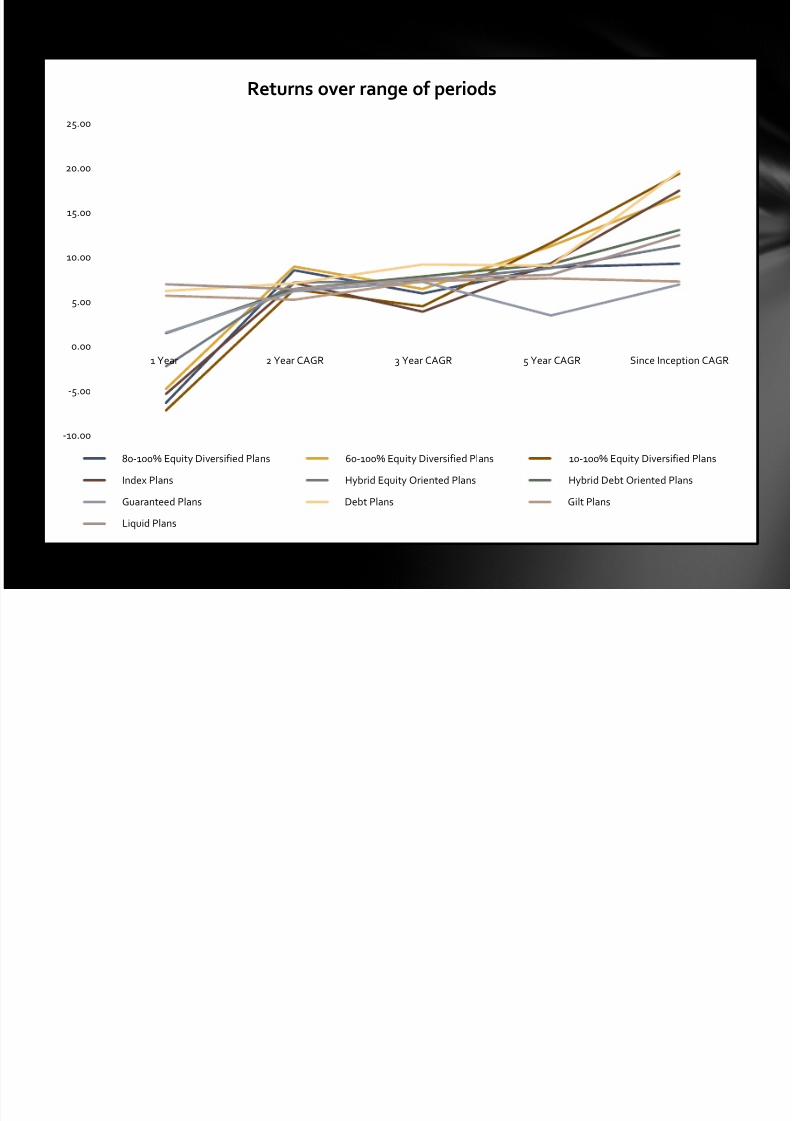

1 Year 2 Year CAGR 3 Year CAGR 5 Year CAGR Since Inception CAGR

Returns over range of periods

80-100% Equity Diversified Plans 60-100% Equity Diversified Plans 10-100% Equity Diversified Plans

Index Plans Hybrid Equity Oriented Plans Hybrid Debt Oriented Plans

Guaranteed Plans Debt Plans Gilt Plans

Liquid Plans

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 19/26

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

1 Year 2 Year CAGR 3 Year CAGR 5 Year CAGR Since Inception CAGR

S&P CNX Nifty 80-100% Equity Diversified Plans Index Plans Debt Plans Liquid Plans

Compared to Benchmark

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 20/26

ULIPs

Industry and potential purchasers love them

Most of the people who have them tend to hate

them

or

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 21/26

Accusations of mis-selling and hard-selling

Most investors admit that they don't understand how it works

It is extremely difficult to compare different Ulip products

• Have to look at not only return but also cost which varies depending upon age,

company etc.

• Companies overstate their yields

Distributors are the biggest profit makers in stead of investors

Early exit options

Creeping costs

Challenges

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 22/26

ULIP – A matter of contention between SEBI and IRDA

Finally IRDA won the battle and now ULIP is mostly an insurance product

Tightening of norms for ULIP

Recent Developments

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 23/26

•

Increase in lock in period from 3 years to 5 years• A step towards making ULIP a long term insurance product

rather than a short term product

All ULIPs, except pension, are annuity products and have to

have either a mortality cover or a health coverAll ULIP pension or annuity products will offer a minimumguaranteed return of 4.5 % annually or as specified by theIRDA from time-to-time

• protect the life time savings of pensioners from any adversemarket fluctuations at the time of maturity

New rules

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 24/26

Capping been rationalized to ensure that the difference inyield is capped from the fifth year onwards

• Frontloading of charges will reduce

• Reduces the overall charges

• Smoothens the charge structure for the policyholder

Top up on insurance premiums will be treated as a singlepremium

•

means that every top up that one makes will have to havean additional insurance cover backing it as well

No partial withdrawals allowed for pension and annuityproducts

New Rules

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 25/26

Need to bring distributors under control through regulation

Consumers need to be more aware

Making this product standardized

Stringent rules for selection of agents who mis-sell these products

Agents from third party who can advise which is the best for the investore.g. Certified Financial Planner (CFP)

Recommendations

8/3/2019 ULIP Prospects Challenges_Group 5_Section C

http://slidepdf.com/reader/full/ulip-prospects-challengesgroup-5section-c 26/26

www.sebi.gov.in

www.indg.in

www.insurancemall.in

blog.moneyraam.com

www.lifeinscouncil.org

www.rediff.com

business.mapsofindia.com

www.bajajcapital.com

References