UGANDA 2013 FinScope III SURVEY REPORT FINDINGS · PDF fileUGANDA 2013 FinScope III SURVEY...

112

UGANDA 2013 FinScope III SURVEY REPORT FINDINGS Unlocking Barriers to Financial Inclusion November 2013 ECONOMIC POLICY RESEARCH CENTRE

Transcript of UGANDA 2013 FinScope III SURVEY REPORT FINDINGS · PDF fileUGANDA 2013 FinScope III SURVEY...

UGANDA 2013 FinScope III SURVEY REPORT FINDINGS

Unlocking Barriers to Financial Inclusion

November 2013

ECONOMIC POLICY RESEARCH CENTRE

ECONOMIC POLICY RESEARCH CENTRE

MINISTRY OF FINANCE, PLANNING AND ECONOMIC DEVELOPMENT

REEV CONSULT INTERNATIONAL

UGANDA 2013 FinScope III SURVEY REPORT FINDINGS

Unlocking Barriers to Financial Inclusion

November 2013

i

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

ACKNOWLEDGEMENTS

This report was prepared by the Econom-ic Policy Research Centre (EPRC) as the Implementing Institution for FinScope

III based on the 2013 FinScope III survey data collected by REEV Consult International dur-ing the period June - July 2013. EPRC worked under the guidance of the FinScope III (2013) Steering Committee, which had a Secretariat at the Bank of Uganda. The Steering Com-mittee had a membership drawn from the Ministry of Finance, Planning and Economic Development, Bank of Uganda, Uganda Insur-ance Commission, Capital Markets Authority, Uganda Bankers’ Association, Uganda Insur-ers Association, the Association of Microfi-nance Institutions of Uganda, Uganda Bureau of Statistics (UBOS), Private Sector Founda-tion of Uganda and Development Partners notably UKaid from the Department for Inter-national Development (DFID).

EPRC wishes to extend gratitude to DFID for entirely funding the FinScope III project. Without their financial support this project could not have been implemented as suc-cessfully as it was.

EPRC acknowledges with thanks the contri-butions made by all members of the Steering Committee. We particularly wish to single out for mention the role played by the Uganda Bureau of Statistics (UBOS), which went be-yond the membership of the Steering Com-mittee to other additional responsibilities. UBOS spearheaded the FinScope III survey design and undertook quality assurance of

the work of the Research House. The efforts of UBOS helped FinScope III to collect and an-alyze high quality data on which this report is based. We also acknowledge the role played by the Capital Markets Authority in chairing and providing the necessary stewardship.

Much gratitude is also extended to the Bank of Uganda and in particular the FinScope Sec-retariat for efficiently organizing meetings and coordinating activities.

Ms. Annette Altvater of Development Pio-neer Consultants in Dar es Salaam, Tanzania provided guidance on the development of FinScope III questionnaire between Decem-ber 2012 and January 2013. Her significant contribution is very much appreciated.

FINMARK Trust of South Africa and Founder of FinScope surveys gave us guidance and insight into the FinScope III study especially with regard to generating comparable results with other African countries undertaking Fin-Scope surveys.

Finally, special thanks go to the team of EPRC researchers namely, Musa Mayanja Lwanga, Ezra Munyambonera, Xavier Mugisha, Ibra-him Kasirye and Lawrence Bategeka; and Vi-cent Fred Sennono, Stephen Baryahirwa and Byron Twesigye of the Uganda Bureau of Sta-tistics who meticulously analysed and com-piled the information for this report.

SARAH N. SSEWANYANA, PHDEXECUTIVE DIRECTOR, ECONOMIC POLICY RESEARCH CENTRENovember 2013

iii

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

TABLE OF CONTENTS

ACKNOWLEDGEMENTS iEXECUTIVE SUMMARY viii1. INTRODUCTION AND BACKGROUND 11.1 An overview of the Uganda’s financial sector landscape 11.2 Data Sources 31.3 Methodology 41.4 Organisation of the Report 5

2. BACKGROUND CHARACTERISTICS OF THE ADULT POPULATION 62.1 Demographics 62.2 Socio-economic characteristics 62.3 Physical access to financial institutions (supply side) 8

3. FINANCIAL INCLUSION 93.1 Overall financial usage 93.2 Financial access strand 93.3 Comparison with other African countries 143.4 Concluding remarks 15

4. FORMAL Products and services PENETRATION 164.1 Having a bank account with a financial institution 164.2 Nature of transactions conducted at various banking points 184.3 Barriers to having a bank account 194.4 Concluding remarks 21

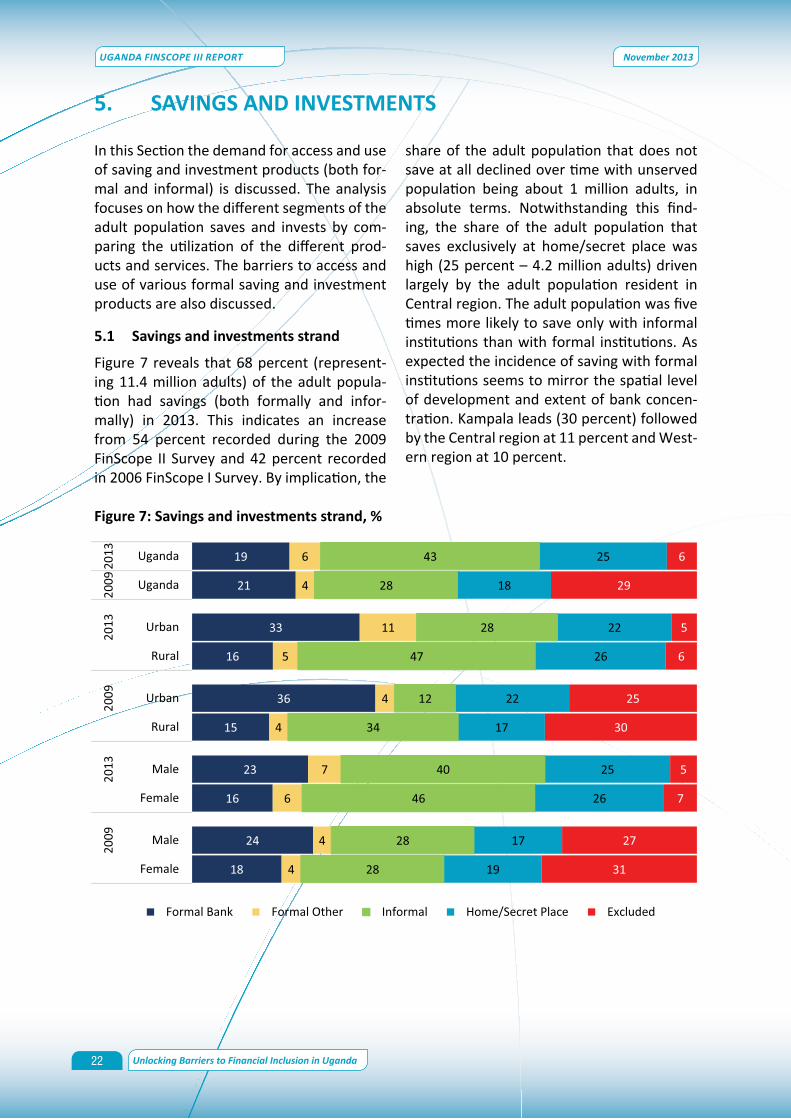

5. SAVINGS AND INVESTMENTS 225.1 Savings and investments strand 225.2 Knowledge of savings and practice 255.3 Savings mechanisms 275.4 Investment activities/products 305.5 Barriers to saving/investing 325.6 Concluding remarks 33

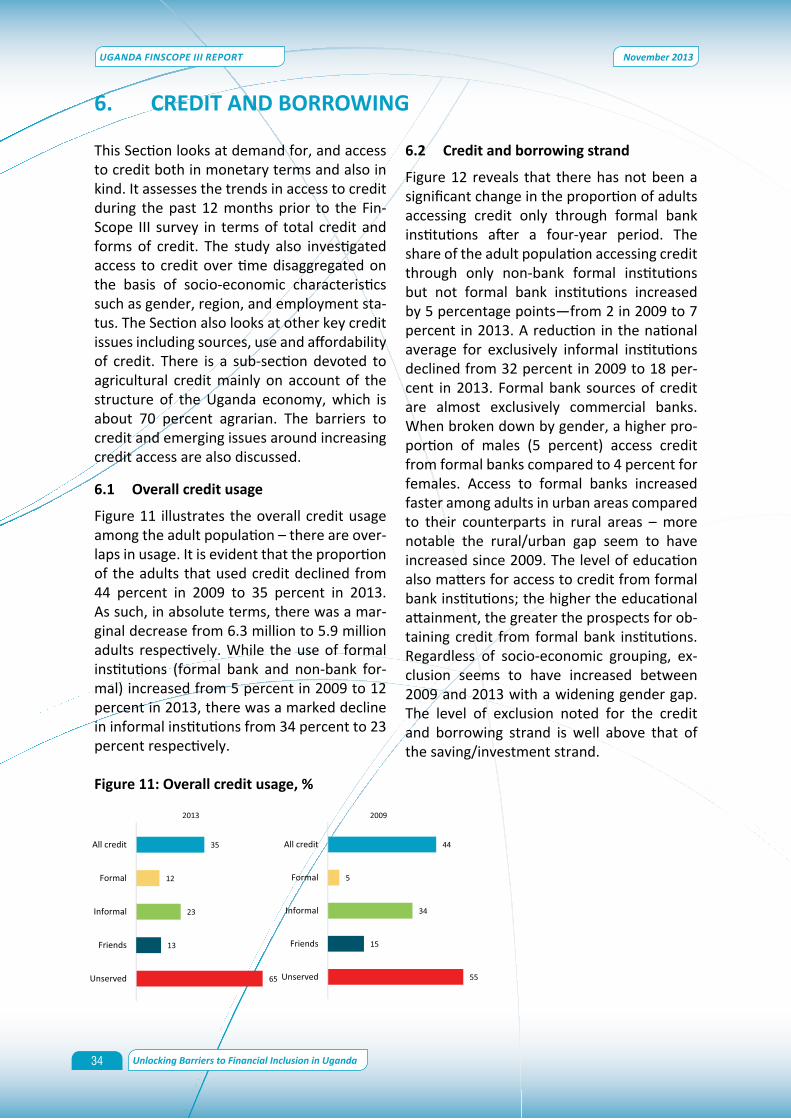

6. CREDIT AND BORROWING 346.1 Overall credit usage 346.2 Credit and borrowing strand 346.3 Types of credit 376.4 Uses of credit 396.5 Perceptions on credit and borrowing 416.6 Loan size and collateral requirements 426.7 Barriers to credit 436.8 Concluding remarks 44

iv

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

7. RISK MANAGEMENT AND INSURANCE 457.1 Risks profile 457.2 Access to and utilisation of insurance services 477.3 Risk management profile 497.4 Barriers to the use of insurance 517.5 Concluding remarks 54

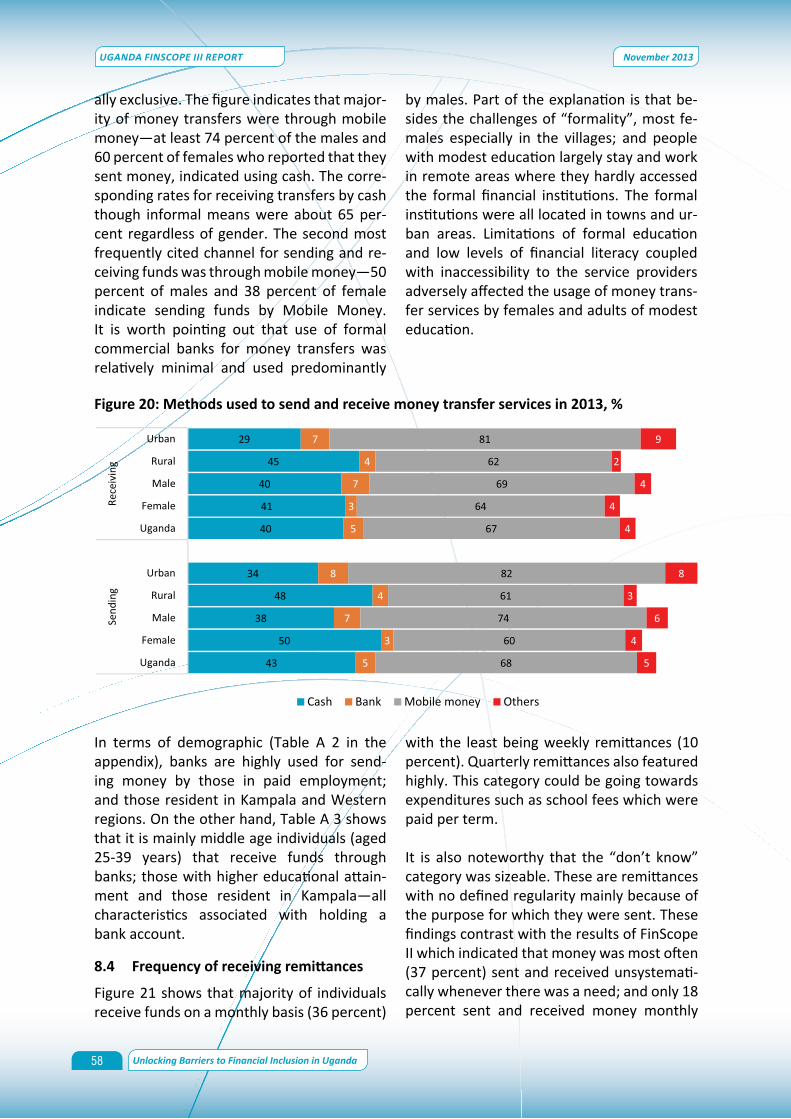

8. REMITTANCES AND MONEY TRANSFER 558.1 Remittances Strand 558.2 Frequency of use of money transfer services 568.3 Channels used to send and receive money transfers 578.4 Frequency of receiving remittances 588.5 Origin of money transfers 598.6 Uses of funds received 608.7 Receiving funds on behalf of others 618.8 Concluding remarks 62

9. ACCESS TO AND UTILISATION OF MOBILE MONEY SERVICE 639.1 Comparison of use of mobile money relative to other financial services 639.2 Knowledge and use of mobile money services 639.3 Utilization of different products 649.4 Utilization of mobile money services by service provider 669.5 Barriers to mobile money services use 679.6 Concluding remarks 68

10. FINANCIAL LITERACY AND CONSUMER PROTECTION 6910.1 Main sources of information 6910.2 Knowledge on the basics of financial literacy 7210.3 Perceptions on loan repayment 7410.4 Consumer Protection 7510.5 Budgeting 7810.6 Concluding remarks 78

11. CONCLUSIONS AND EMERGING POLICY IMPLICATIONS 79REFERENCES 83

v

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

LIST OF TABLES

Table 1: Adult population characteristics by location in 2013, % 7Table 2: Distance to the nearest financial institution by location in 2013, % 8Table 3: Use of financial services (mutually exclusive) by adult characteristics in 2013, % 13Table 4: Product and services penetration by adult characteristics in 2013, % 17Table 5: Nature of transactions by socio-economic characteristics and location in 2013, % 18Table 6: Reasons for not having a formal bank account in 2013, % 20Table 7: Savings and investments strand by adult characteristics in 2013, % 24Table 8: Preference for savings and practice by adult characteristics in 2013, % 26Table 9: Savings mechanisms by adult characteristics in 2013, % 28Table 10: Reasons for currently saving/investing by adult characteristics in 2013, % 29Table 11: Investment mechanisms in 2013, % 31Table 12: Reasons for never saving or investing by adult characteristics in 2013, % 32Table 13: Credit and borrowing strand by socio-economic characteristics, % 36Table 14: Forms of borrowing during the last 12 months in 2013, % 38Table 15: Main reasons for utilizing credit services in 2013, % 39Table 16: Form of collateral security required by institution in 2013, % 43Table 17: Reasons for not taking loans by gender and location in 2013, % 43Table 18: Risk encountered in the last 12 months in 2013, % 46Table 19: Overall usage of formal and informal insurance, % 48Table 20: Reasons why the adults preferred informal insurance in 2013, % 49Table 21: Risk management mechanisms by adult characteristics in 2013, % 50Table 22: Barriers to formal insurance products and services in 2013, % 52Table 23: Remittances and transfers, % 56Table 24: Knowledge and use of mobile money services in 2013, % 64Table 25: Transactions done with mobile money in 2013, % 65Table 26: Utilisation of mobile money services by service provider in 2013, % 66Table 27: Reasons for not using mobile money services in 2013, % 67Table 28: The most important sources of financial information in 2013, % 70Table 29: Areas where further financial information is required in 2013, % 71Table 30: Testing knowledge of basic financial literacy in 2013, % 73Table 31: Self-reported perceptions on implications of failure to pay back a loan in 2013, % 74Table 32: Preferred options for dispute settlement in 2013, % 76

List of Appendix Tables

Table A 1: Enumeration areas and households 84Table A 2: Remittances and transfers - Sent, 2013 (%) 87Table A 3: Remittances and transfers – receipts, 2013 (%) 88Table A 4: Use of funds received and recipient in 2013, % 89

vi

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

LIST OF FIGURES

Figure 1: Households most important source of income in 2013, % 8Figure 2: Overall usage of financial services, % 9Figure 3: Mutually exclusive use of financial services by institutions, % 10Figure 4: Financial access strand with mobile money services in 2013, % 11Figure 5: Financial inclusion by selected African countries 2009-2012, % 15Figure 6: Operating an account with financial institutions, % 16Figure 7: Savings and Investments strand, % 22Figure 8: Private time and savings deposits (UShs billion) 23Figure 9: Perception on the single most definition of saving in 2013, % 25Figure 10: Means of planning for retirement/old age (mutually inclusive) in 2013, % 30Figure 11: Overall credit usage, % 34Figure 12: Credit and borrowing strand by gender and location, % 35Figure 13: Main reasons for accessing agricultural credit in 2013, % 40Figure 14: Perceptions on whether access to financial institutions improved since 2009, retrospectively % 41Figure 15: Borrowers’ perception on the affordability of their recent loan in 2013, % 42Figure 16: Understanding of the terms and conditions of loan/credit in 2013, % 42Figure 17: Loan size by gender and location in 2013, UShs (‘000), % 42Figure 18: Barriers to informal services use in 2013, % 51Figure 19: Use of money transfer services in 2013, % 57Figure 20: Methods used to send and receive money transfer services in 2013, % 58Figure 21: Regularity of receiving remittances in 2013, % 59Figure 22: Receipt of transfers from within and outside Uganda in 2013, % 60Figure 23: Uses of remittances and transfers by location in 2013, % 61Figure 24: Transparency and fairness of financial institutions in 2013, % 77

APPENDIX 1: SURVEY DESIGN 84

vii

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

ACRONYMS AND ABBREVIATIONS

ACSA Accumulating Savings and Credit AssociationsATM Automatic Teller MachineBoU Bank of UgandaCS Pro Census and Survey Processing SystemCV Coefficient of VariationDfID Department for International Development EAs Enumeration AreasEPRC Economic Policy Research CentreGDP Gross Domestic ProductGoU Government of UgandaGPS Geographical Positioning SystemIRA Insurance Regulatory AuthorityLCs Local CouncilsMDIs Micro-Deposit taking InstitutionsMFIs Microfinance Institutions MoFPED Ministry of Finance Planning and Economic Development MTN Mobile Telephone NetworkNDP National Development PlanNGOs Non-governmental OrganisationsNSSF National Social Security FundOPM Office of the Prime MinisterPPS Probability proportion to sizePSU Primary Sampling Unit ROSCAs Rotating, Savings and Credit Associations SACCOs Savings and Credit Cooperative OrganizationsUBoS Uganda Bureau of StatisticsUIA Uganda Insurance AssociationUDHS Uganda Demographic and Health SurveysUNHS Uganda National Household SurveysUSD United States DollarsUShs Uganda ShillingsVSLAs Village Savings and Lending Associations

viii

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

EXECUTIVE SUMMARY

I. Introduction

Overtime, Uganda’s financial sector has continued to record some positive changes such as the level of financial development, increased competition and improved efficiency in the financial system. There have also been deliberate efforts by government to strengthen financial inclusion in Uganda since 2001. With these developments in the financial sector, it is important that regular assessments are done to explore the extent to which such developments have translated into improved demand, access to and usage of financial products and services by the Ugandan adult population. As such, regular nationally representative FinScope surveys have been carried out in Uganda and other African countries to provide a basis for monitoring such progress – in terms of demand, access to and use of financial products and services.

To date, FinScope surveys have been carried out in 18 African countries including Uganda. The main objective of these surveys is to determine the levels of access to and use of financial products and services by the adult population. The 2013 FinScope III survey for Uganda follows two previous surveys—FinScope I and II surveys carried out in 2006 and 2009 respectively. Like the earlier surveys, FinScope III sought to establish the level of financial inclusion by looking at access to and usage of financial products and services through four major access strands namely: saving and investment; credit and borrowing; remittances and money transfer; and insurance. Additionally, the survey sought to establish the level of financial literacy amongst the adult population and their perception of consumer protection offered by financial institutions.

I.1 Data Sources

The analysis in the report is based on the 2013 FinScope III survey conducted by REEV

Consult International during June – July 2013. This survey builds on the previous nationally representative FinScope I and II conducted in 2006 and 2009 respectively. However, unlike the previous surveys, FinScope III survey presents an opportunity to track households in future surveys to monitor progress made by the same individuals over time. The survey was also expanded to include mobile money services and a refinement of some questions. It was based on a two stage stratified random sampling design and covered 3,401 households.

The report adopts the financial inclusion framework developed by FinMark Trust, which considers four financial access strands – credit and borrowing; remittances and transfer; savings and investments; and insurance. Within each strand, access to and use of the various products and services (formal and informal) by the adult population (16 years and above) is analysed across gender, life cycle (age), educational attainment, employment status, wealth quintile and spatially. Similar analysis is done based on the self-reported barriers to access and usage of the various financial products and services. At the aggregate level, all the four strands are combined to generate a single indicator – financial access strand.

I.2 Approach

In terms of access and use of financial services through institutions, the report constructs the 2013 financial access strand that is in line with the structure and framework of 2009 FinScope II survey as follows: Formal banks (Regulated by Bank of

Uganda –BoU): commercial banks, microfinance-deposit taking institutions (MDIs) and Credit institutions);

Non-bank formal (other formal) other microfinance institutions (MFIs), Savings and credit cooperative organisations (SACCOs), Insurance

ix

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

companies, cell phone mobile money, non-banking financial institutions like foreign exchange bureau, money transfer services like Western Union;

Informal —all other institutions including village savings and rotating groups – Rotating, Savings and Credit Associations (ROSCAs), Village Savings and Lending Associations (VSLAs), Accumulating Savings and Credit Associations (ACSA), Non-government organisations (NGOs), investment clubs, savings clubs, services by employers and other village groups like burial societies and welfare funds. Others informal services include shops and investing through property like houses for rent, livestock and crop produce to be sold later or farm inputs to use at a later date. FinScope III also considers borrowing such as credit from a shop, school, health centre and individuals as informal access; and

Financially excluded (unserved) are non-users of formal banks, non-bank formal or informal institutions. Products and services under financially excluded include saving in a secret place, shops or with friends/relatives; borrowing from friends or family members; or money transfers using individuals.

The analysis is done at individual level for the entire adult population aged 16 years and above, unless stated otherwise. The estimates are weighted to reflect the total adult population. To shed light on financial inclusion of the adult population, the results in 2013 are compared with those based on 2009 FinScope II, where possible.

II. Key Findings

II.1 UseofFinancialInstitutions

Overall usage of financial products and services: Broadly speaking, the Ugandan adult population financial usage was from diverse financial institutions. The share of the adult

population that cited to have accessed formal institutions (banked and non-bank formal) increased by almost two fold from 28 percent in 2009 to 54 percent in 2013. The growth was driven by the increase in the non-bank formal from 20 percent in 2009 to 52 percent in 2013. On the other hand, the increase in the share of the adult population using informal financial institutions (60 percent in 2009 to 74 percent in 2013) was not as fast as that observed for formal financial institutions.

Financial access strand (mutually exclusive): Overall, 85 percent of the adult population had access to and usage of financial services in 2013 while 15 percent were financially excluded. This compares with 70 percent in 2009, with those excluded being 30 percent. The results revealed that in 2013, 20 percent of the adult population (representing 3.4 million adults) were using a formal regulated financial intermediation service, and nearly 34 percent were using only the non-bank formal but not the formal banks, and 31 percent (representing estimated 5.1 million adults) were using only informal institutions but not the formal financial products and services. An estimated 2.6 million adult population were financially excluded in 2013 – contributing about 15 percent of the total adult population. This marks a reduction in financially excluded adult population, from 30 percent (4.3 million adults) in 2009.

In comparison to 2009, use of formal banking institutions remained the same while the share using only non-bank formal institutions but not formal banking institutions increased from 7 percent in 2009 to 34 percent in 2013. This increase was mainly driven by the surge in use of mobile money services between 2009 and 2013.

There were marked variations in access and usage of financial products and services across social groups and spatially. For example, the gender gap observed in financial exclusion in 2009 had diminished in 2013; although

x

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

there was a growing gender gap in terms of those who accessed only informal financial products and services – 7 percentage points. While there was a marked decline in the rural/urban divide, use of informal products and services remained higher among adults in rural areas compared to their counterparts in urban areas. The gap declined from 22 percentage points in 2009 to 19 percentage points in 2013. Formal employment, wealth status and educational attainment were the biggest differentiators in the use of formal banking institutions. The adults in the top most quintile were five times more likely to access banks compared to those in the bottom wealth quintile (gap growing over time); and there was a marked decline in use of formal banking institution by those in self-employment.

II.2 Formal Product and Service Penetration

Usage: One in every 5 adults (representing 3.3 million adults) had a formal account of some nature in formal banks or non-bank formal institutions in 2013. This marks a marginal increase from 18 percent (representing 2.5 million) in 2009. There was a significant reduction in the share of the population that operated an account with commercial banks from 74 percent in 2009 to 50 percent in 2013. It is evident that the SACCOs which were legally constituted, but not controlled by BoU had become an option of choice second to commercial banks – the share of the adult population that operated an account increased from 5 percent in 2009 to 21 percent in 2013.

Barriers to having a bank account: The most cited barriers were income/employment related (lack of income (47 percent) and no job (17 percent) and lack of knowledge on how a bank account works (18 percent); supply side constraints included cost of operating an account (22 percent) and distance to bank (13 percent). While the share was low, some 3 percent did not trust the financial

institutions.

II.3 Savings and Investments

Savings and investments strand: The results from the survey revealed that 68 percent of the adult population was saving (both formally and informally) in 2013 indicating an increase from 54 percent in 2009 and 42 percent recorded in 2006 – based on FinScope surveys. By implication, the share of financially excluded but not using home/secret place adult population declined over time—from 29 percent in 2009 to 6 percent by 2013. Ugandans were about twice more likely to save exclusively with informal institutions than with formal institutions. At national level, use of informal institutions increased by 15 percentage points but was marked with a growing gender and rural/urban divide gap. The likelihood to save/invest with a formal banking institution increased with educational attainment and wealth quintile. The youth were more than three times less likely to save/invest with formal banks compared to the middle aged adult population. Despite the developments in the financial sector, a significant proportion of the adult population used home/secret place for saving – the share increased from 18 percent in 2009 to 25 percent in 2013.

Savings mechanisms: Only focused on the adult population that saved in the past 12 months prior to the FinScope III survey. The most cited mechanisms in order of frequency included: home (51 percent), VSLAs/ROSCAs (29 percent) and buying of livestock/assets (18 percent). The practise of using home/secret place exclusively reduces with increasing educational attainment and wealth quintile status. Saving/investing with the bank/MDI was cited by only 19 percent of the adult population. These were mainly the adults who were males, better educated, formally employed and residing in relatively well developed regions.

What drives savings: Those who reported to

xi

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

have been saving at the time of the survey indicated multiple reasons why they did so. These included, in order of popularity: meeting basic needs (67 percent), emergencies (41 percent), education (33 percent) and livestock (22 percent). Saving for emergencies reduced but savings for business start-up/expansion increased by wealth quintile status and educational attainment. There was a gender gap with females more likely to save for emergencies while their male counterparts were more likely to save for acquisition of land.

Investment products/activities: One in every 10 adults invested through formal financial institutions (formal bank and non-bank formal) emphasizing low financial penetration. This share increases with educational attainment, wealth quintile status, level of development of the local economy and employment security. On the other hand, investment in informal financial institutions was cited by 47 percent of the adult population. It is evident that females were more likely to invest in informal institutions whereas their male counterparts were more likely to invest in formal ones.

The majority of adult population invested in agriculture and related activities. Specifically, 53 percent of the adult population that indicated to have invested at the time of the survey, most of them cited such investments in farm land (53 percent), 41 percent in livestock, and 39 percent reported investing through an informal group and 24 percent invested in starting up/expanding an existing business. Vulnerable groups i.e. females, the less educated, the unemployed and the poor were more excluded from investment activities compared to their less vulnerable counterparts.

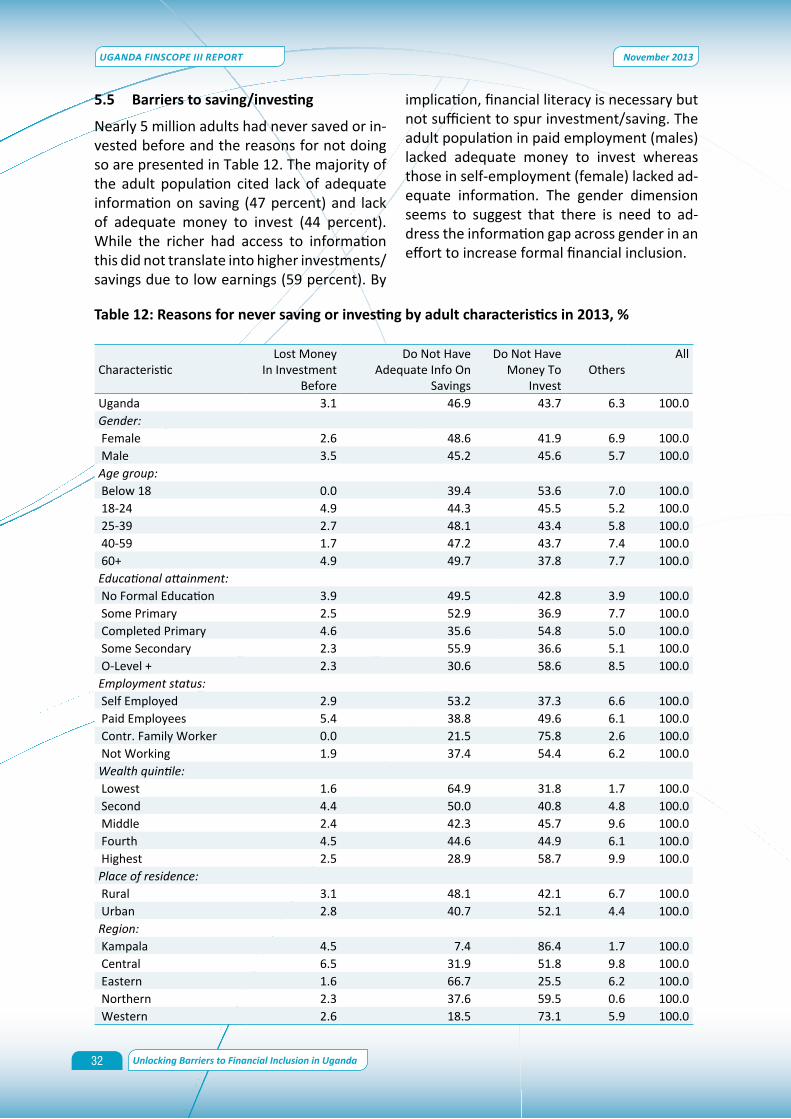

Barriers to savings/investments: The cited barriers seem to point to lack of income and lack of knowledge as reasons for exclusions from savings/investment activities. Citing of

lack of money to save/invest increases with the life cycle. While only 7 percent of adults resident in Kampala cited lack of information on savings, a significant share (66 percent) reported the same in Eastern region. This is a wide spatial variation that needs to be addressed.

II.4 Credit and borrowing

Credit and borrowing strand: The results revealed that access to credit and borrowing was very low in Uganda with only 4 percent of the adult population accessing credit from formal bank institutions. A similar rate (4 percent) accessed credit from non-bank formal financial institutions while 20 percent accessed credit from informal sources.

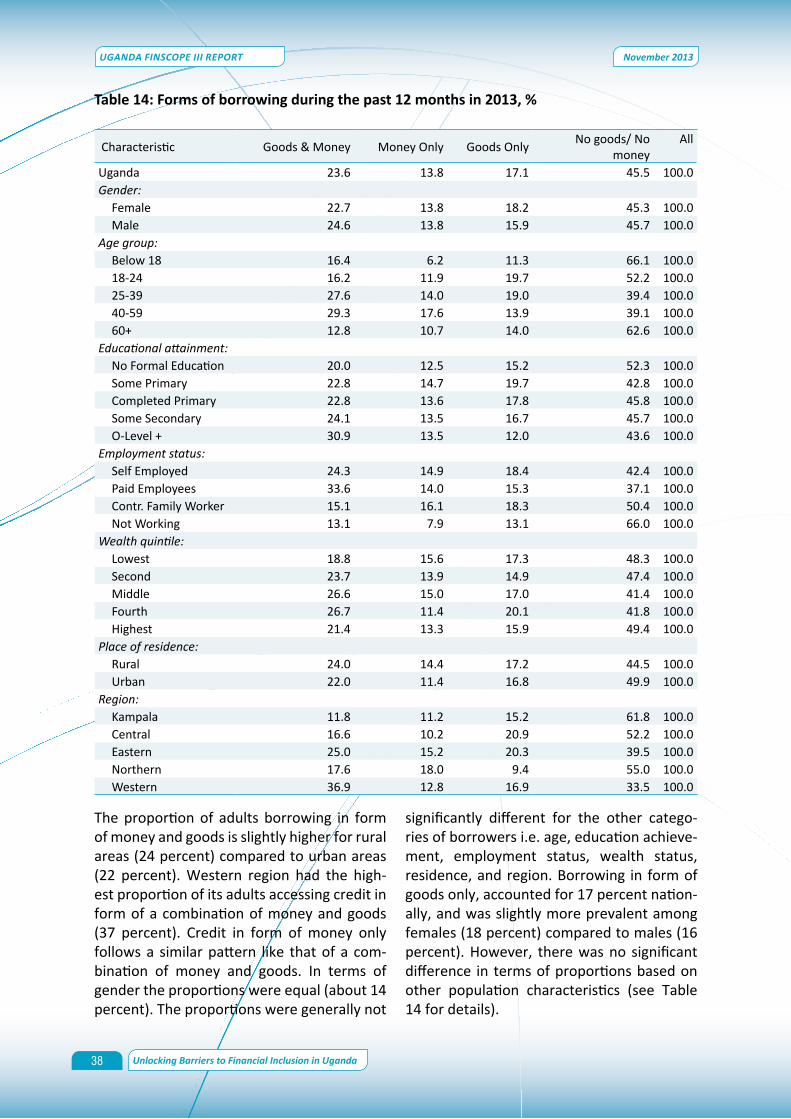

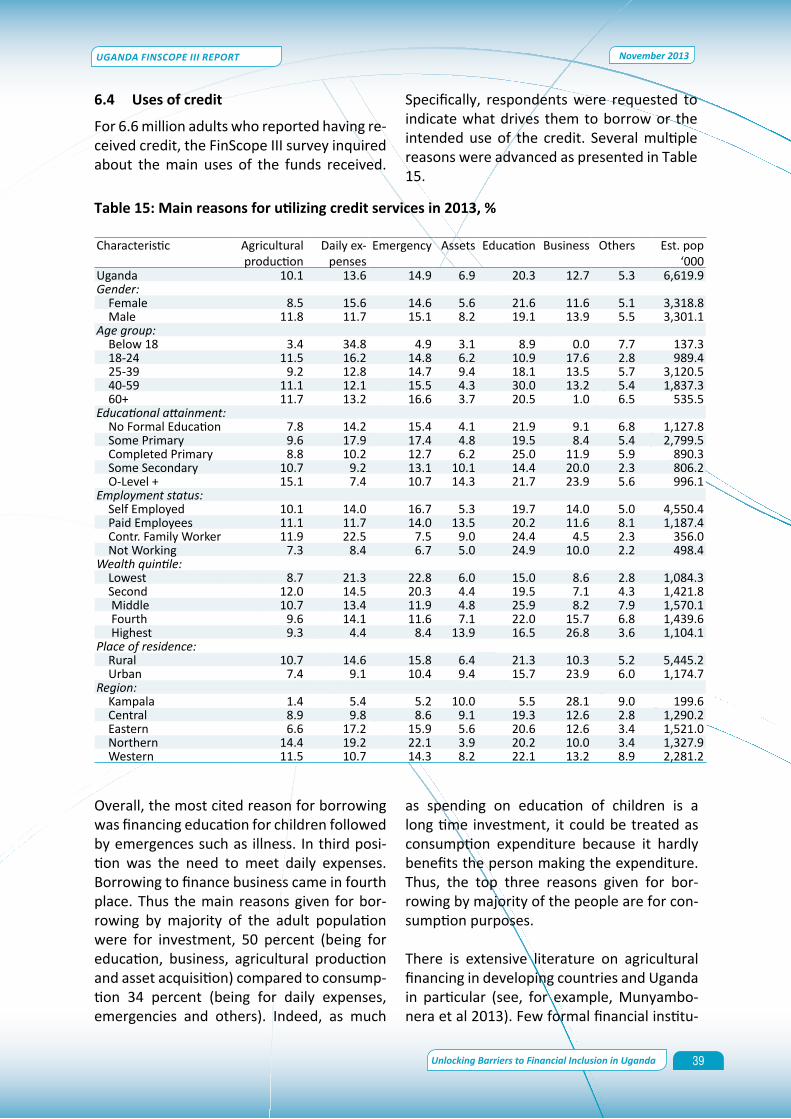

What drives borrowing: The majority that borrowed did so to finance education of children (20 percent) and to cater for emergencies (15 percent). Only 10 percent of the borrowers borrowed for agricultural production yet majority of Uganda’s population derive their sustenance from agriculture. The biggest proportion of people borrowing to finance agricultural production does so for purchase of inputs (54 percent), followed by hiring farm labour (29 percent). There is a regional dimension – with adults in Northern region more likely to borrow for agricultural production and emergencies whereas those adults resident in Kampala were more likely to borrow for business purposes and acquisition of assets compared to their counterparts in other regions. As noted under savings/investments, borrowing for emergencies reduces with wealth quintile status, educational attainment and level of development of the local economy. A significant share of the youth (18-24 years) cited borrowing for business start-up/expansion compared to their other counterparts.

Terms and conditions, and size of loan: Regarding understanding loan conditions and cost of credit, nearly all the adult borrowers

xii

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

understood the terms and conditions before taking a loan. The majority of the borrowers (52 percent) indicated that the loan was affordable against 5 percent that indicated that it was very expensive. The average loan size was relatively small, with 73 percent of borrowers indicating taking small loans that did not exceed UShs 500,000. Male borrowers were almost two times likely to take a loan in excess of UShs1 million (18 percent) compared to their female counterparts (8 percent).

Barriers to credit and borrowing: Some 31 percent of the adult population that never accessed a loan during the past 12 months cited fearing debts as a reason for not doing so. The high cost of loans is the second most frequently cited reason for not accessing credit (14 percent) followed by lack of security (13 percent).

II.5 Insurance and Risk Management

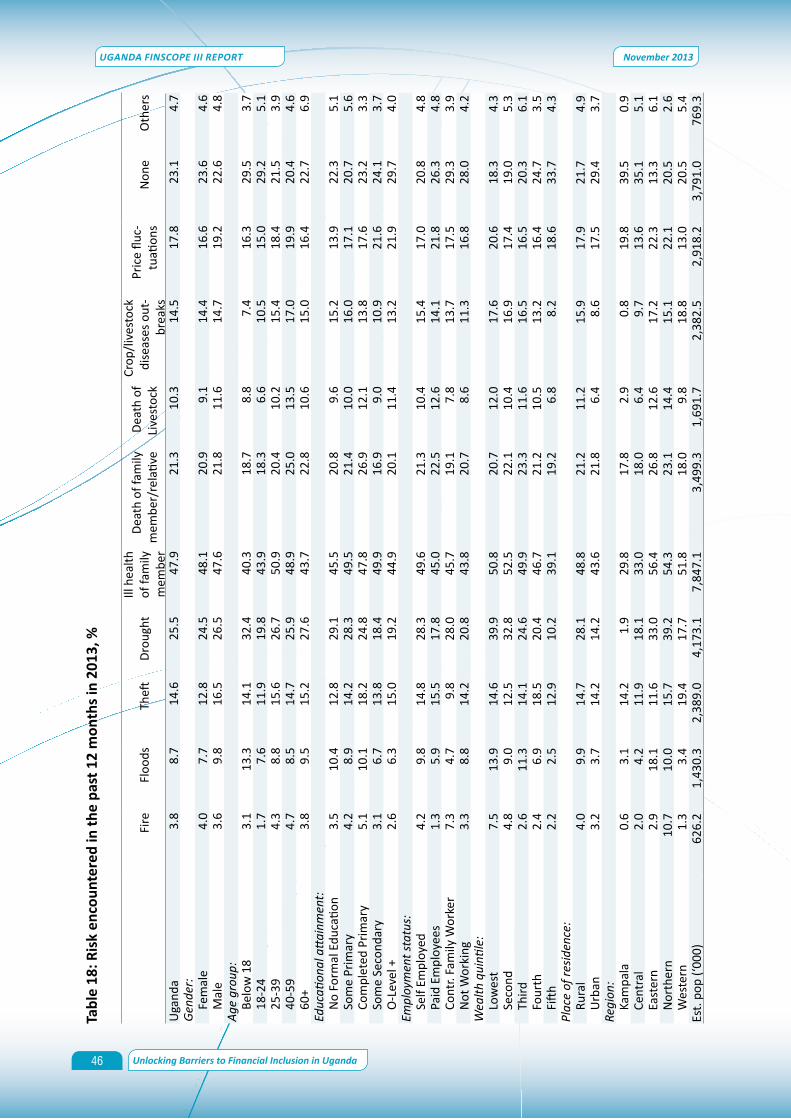

Risk profile: The survey requested the respondents to indicate whether their households experienced shocks in the past 12 months prior to the survey that might have, in turn, negatively impacted on their incomes at individual level. The responses were not mutually exclusive. The most common risks included, in order of frequency: illness of family member (48 percent), drought (26 percent) and death of a family member/relatives (21 percent), price fluctuations (18 percent) and theft (15 percent). The likelihood of citing drought, crop/livestock diseases and ill-health reduced with wealth quintile status. This is expected since the better-off are less likely to be engaged in agriculture-related activities. Furthermore, the self-employed were more likely to cite drought compared to their counterparts in paid employment, whereas the reverse is true for price fluctuations.

Insurance access strand: Use of formal insurance services in Uganda remained low with only 2 percent of adult population

reporting use of these services in 2013 marking a reduction from 3 percent in 2009. Overall usage of informal insurance groups grew between 2009 and 2013. Nearly 44 percent of those using informal groups indicated that it was easier to join such groups; 15 percent said that formal insurance was beyond their means and 11 percent had never heard about formal insurance companies.

Risk management profile: The majority of adult Ugandans (45 percent in 2013) dealt with these risks largely through informal means, such as: borrowing from friends and family, asking for donations from neighbours, relatives and friends, and sale of assets such as land (15 percent). Borrowing from friend/relatives, seeking for donations, reduction in consumption reduces with wealth status. The adult population resident in rural areas was more likely to report sale of assets, borrow from friends/relative and seeking for donations compared to their counterparts in urban areas. A slightly higher share of the youth cited sale of assets compared to their counterparts in other age groups.

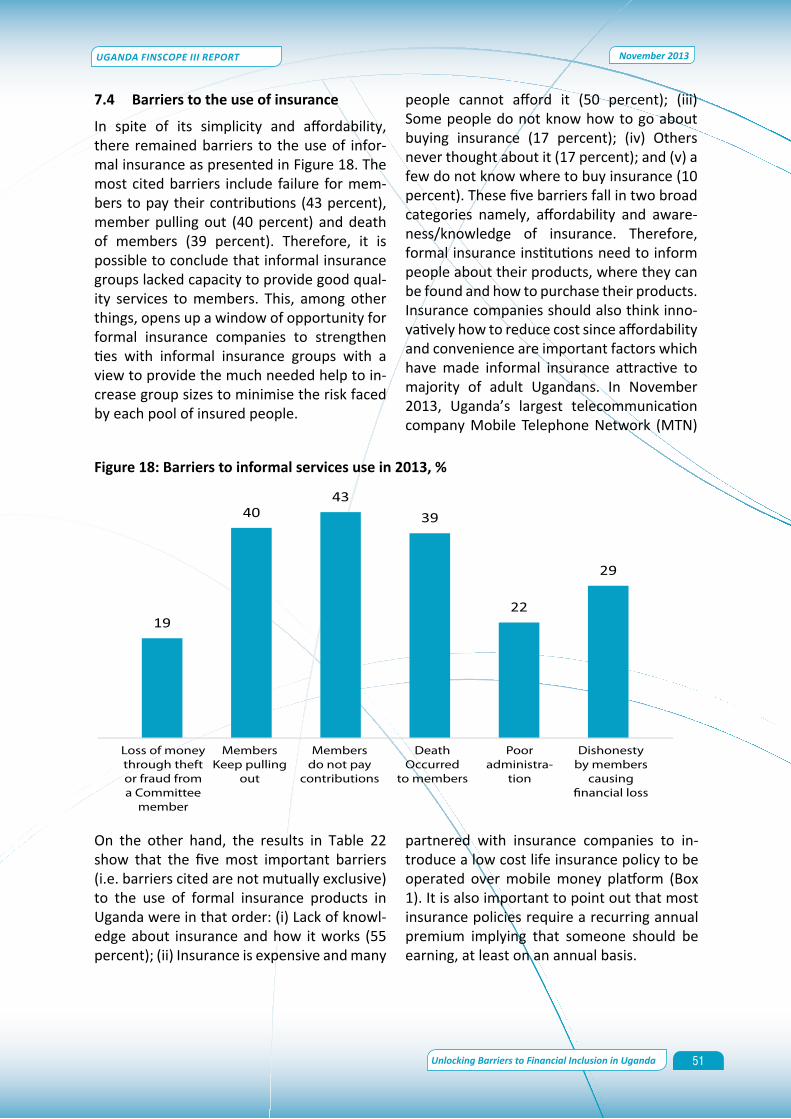

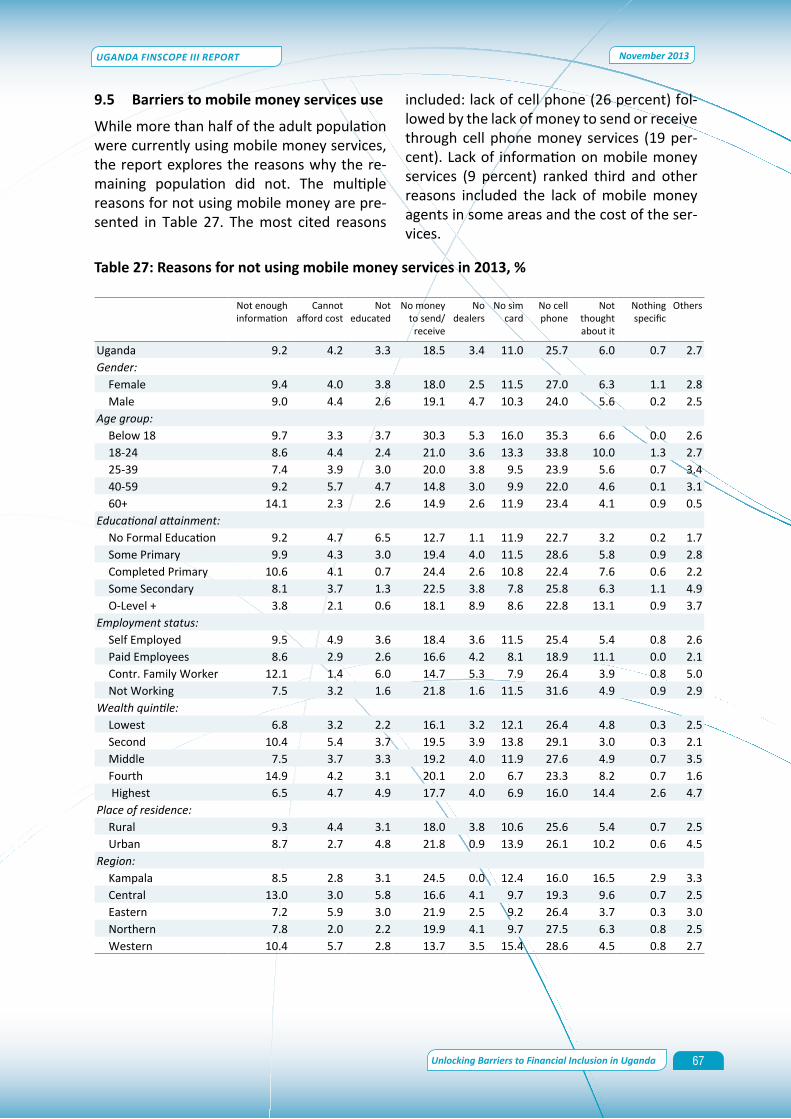

Barriers to insurance: While there is a growing usage of informal insurance groups by the adult population, these groups have their own weaknesses. These weaknesses are of governance, institutional development and accountability in nature. On the other hand, there remains multiple barriers to accessing formal insurance. Surprisingly, more than half of the adult population that was not currently using formal insurance products and services at the time of the survey, cited lack of knowledge on how formal insurance work. The other common barriers to formal insurance included high cost cited by 50 percent, others were aware of formal insurance services but did not have knowledge on how it works (17 percent) or even never thought of having one (17 percent).

xiii

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

II.6 RemittancesandMoneyTransferservices

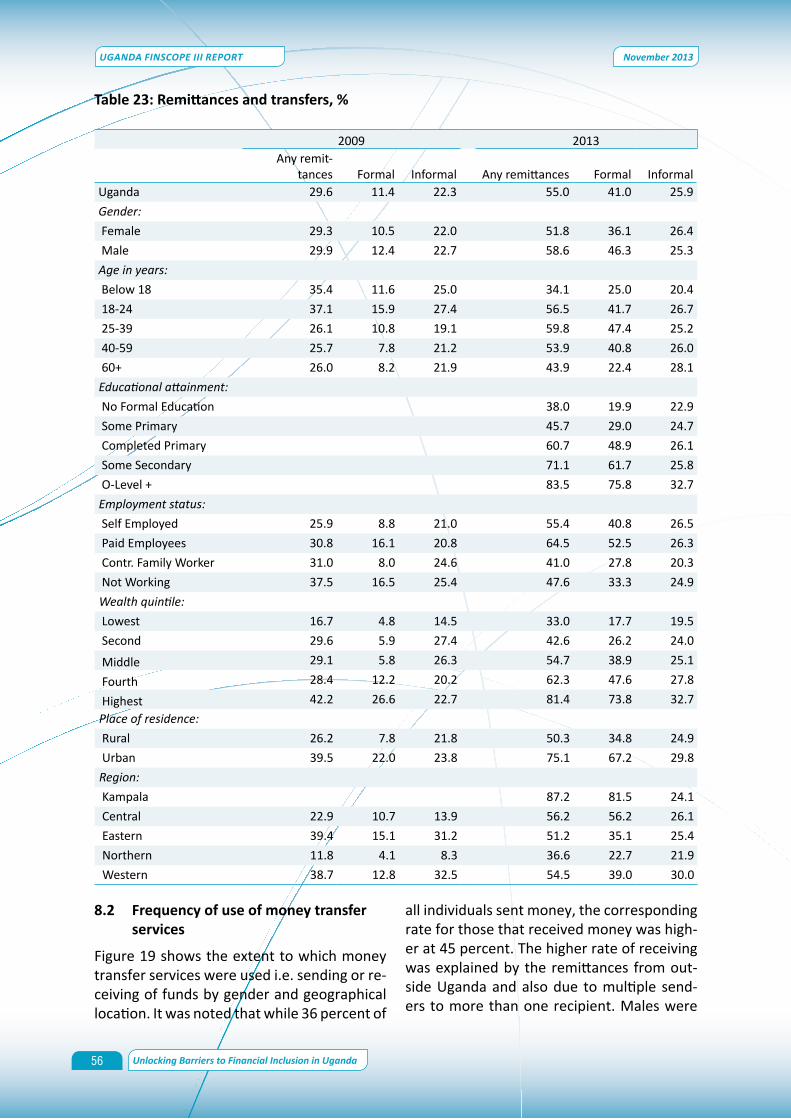

The frequency of reporting receiving remittances and transfers by Ugandans increased from 30 percent in 2009 to 55 percent by 2013. The above changes were driven by increase in receiving formal (non-bank) transfers—whose rate increased from 11 percent to 41 percent during this period. Majority of money transfers in Uganda were informal—by way of cash through relatives or friends. In terms of origin of funds, the frequency of receiving remittances from outside Uganda declined from 16 percent in 2009 to 8 percent by 2013. In comparison to the previous FinScope (2009) findings, FinScope (2013) shows that mobile money services were increasingly becoming the most popular formal means of transferring money in Uganda. Regarding uses, about 62 percent of remittances were devoted to home consumption.

II.7 Use of Mobile Money Services

The survey established that 56 percent of adults were currently using mobile services though only 34 percent were formally registered with the service providers. As such, a significant proportion of the mobile money users accessed the services through a third party account. Utilization of mobile money was higher amongst males than females and higher in urban than in rural areas. The survey results revealed that the majority of Ugandans mainly use mobile money services for cash withdraws (56 percent), followed by cash deposits (27 percent). Usage of mobile money services for other services like payment for utilities, school fees, and purchase of airtime remained low.

II.8 Financial Literacy and Consumer Protection

The level of financial literacy remained low. This was particularly demonstrated when it came to solving simple financial related arithmetic problems.

There is therefore, a need to link the development of financial educational products and services to the currently most important sources of financial information. The sources cited included: through radios and TVs, while a small proportion received information through newspapers and informal sources such as friends and relatives—especially in rural areas.

In terms of consumer protection, of the adults that indicated to have used financial service providers, they were requested to indicate their degree of satisfaction with the services provided. The findings revealed that 11 percent of the adult population remained unsatisfied with their financial providers across all the population groups; with the urban, the more educated and the richer ones being the most dissatisfied with financial service providers. On complaint handling, majority of the adult population preferred that an independent institution be set up.

III. Emerging Issues

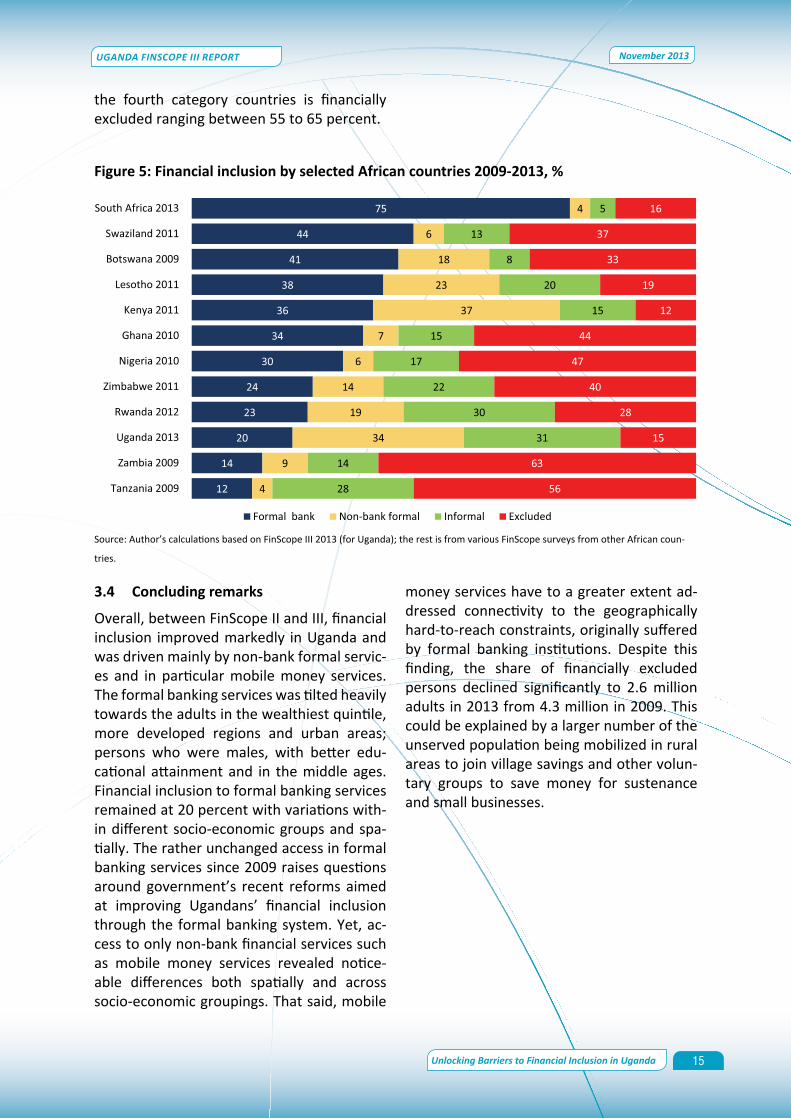

Overall there has been remarkable improvement in financial inclusion in Uganda since 2009. However, this improvement was registered mainly in the non-bank formal sector largely driven by the introduction and growth of mobile money services. With the exclusion of mobile money which is largely used for money transfers and not for financial intermediation, formal financial inclusion in Uganda remains low when compared with other countries like South Africa, Namibia, Swaziland and Kenya where similar FinScope studies have been carried out.

Financial inclusion through formal banking by the adult population remained unchanged after the four-year period. Yet, Uganda realised growth in the number of commercial banks and commercial bank branches. Access to and use of formal banking services was skewed heavily towards the adult population in the top 20 percent of the wealth distribution, in the more developed regions

xiv

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

and in urban areas; as well as towards persons who were males, with better educational attainment and middle aged contributing further to inequalities across and within these categories.

Although a lot has been done to address the supply side constraints of formal financial services among the adult population, much more needs to be done differently to spur demand and access. Below are some of the key policy actions.

III.1 Maintaining macroeconomic stability

The results of FinScope 2013 suggest that macroeconomic instability has an effect on the utilisation of financial products and services (as illustrated in section 5.1). High inflation adversely affects the demand for credit and the cost of borrowing. It also adversely affects savings as well as investment decisions of firms and households. There is therefore a need to maintain macroeconomic stability at all times in order to accelerate the growth of the financial sector.

III.2 Spatialtargetingtopromotefinancialinclusion

From the results it is clear that access to and use of financial products and services were skewed toward the urban population and better developed regions. Northern Uganda registered the highest level of exclusion—partly due to the lingering effects of the civil war. Hence there is need to consolidate government’s efforts to prioritize development of road infrastructure and energy in the region. The private sector should also be encouraged and/or supported to increase its broad-based investment activities to compliment government efforts.

III.3 Promote broad-based growth

While Uganda has been able to meet the millennium development goals (MDGs) of halving income poverty—from 56 percent in 1992 to 22 percent in 2013 (preliminary estimates)—not every Ugandan has benefited

from this growth. The study findings have revealed that development of the financial sector has not benefited all socio-economic groups. There are notable gender gaps; rural/urban gaps; and gaps across educational attainment. There is need to promote pro-poor growth policies that will lift the majority of the population from poverty and reduce income inequality.

III.4 Promotingbroad-basedlong-termsavings and investment to support sustainable growth

The study revealed that most of the financial services available were of a short-term nature, and therefore suitable for supporting short-term consumption. There is a major gap in the provision of long-term savings mobilisation to support long-term investment efforts. Policies aimed at eradicating slack capacity in long-term savings mobilisation and investment remain critical and paramount.

III.5 Financialeducationandinformationdissemination

One of the barriers for financial exclusion—especially in the strands of savings/investments, credit, and insurance was due to lack of knowledge about these services. This is exacerbated by the low levels of literacy and numeracy among the Ugandan population. The results showed that lack of financial knowledge and information was one of the barriers to the use of financial products and services. This calls for intervention from both the private sector and government to design programs that will improve financial literacy as well as increase information of the financial products and services. This is especially important for the insurance sector—given the increasing vulnerabilities faced by the adult population. There should be a policy on training in entrepreneurship and financial literacy, which should go hand in hand for sustainability purposes.

xv

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

III.6 Technologicalinnovationandutilisation

There is no doubt that the use of technology has led to improvement in access to non-bank formal financial services although this segment is dominated by mobile money transfer services. As such, other strands such as insurance should develop appropriate products—in line with Uganda’s risk profile. The survey has provided evidence which shows that new financial products like mobile money can improve the access and use of financial services in Uganda. However, the use of this mobile phone technology is still limited to only money transfer services. There is therefore need to adopt and extend this technology to the provision of other products and services like savings mobilisation as well as credit extension through mobile money banking, agent banking and micro banking. This will enable the services to reach the population not only in urban areas but also in rural and hard-to-reach areas.

III.7 Productdifferentiationandmarketsegmentation

From the survey results it is clear that the supply of formal financial services especially insurance is lower than the demand due to lack of access to and the complexity of the services. There is need for financial institutions to creatively introduce products and services and marketing techniques that are better tailored to the needs and development of individuals in view of the population differences in terms of location, age, gender, and economic status. For example, insurance products required for the urban population are quite different from those needed in rural due to differences in risks encountered.

III.8 Legal,Institutionalandregulatoryframework

The results also revealed increased access to and usage of SACCOs and other MFIs (Tier 4 institutions). Some of these institutions are dependent on government through the Microfinance Support Centre. On the other

hand, the extent of mobilization of savings has remained very low since 2005 and as such rely heavily on government. As such sustainability is unlikely to be achieved for institutions that receive public support. This calls for a well-thought through exit strategy. Specifically, the government has to put in place mechanisms that will strengthen the institutional infrastructure of the SACCOs and other MFIs to increase their mobilization of savings and deposits in order to sustainably extend loans to members.

Likewise, the survey results have demonstrated increasing use of ICT in enhancing financial inclusion. This calls for well-coordinated institutional arrangement among the key stakeholders in the financial sector when refining the existing laws and regulations.

1

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

Uganda’s Vision 2040 highlights access to fi-nance as one of the barriers among others that are affecting the competitiveness of the economy. Most individuals and firms access credit from informal sources. One of the rea-sons for the limited access to credit is the low level of domestic savings which affects the ability by institutions to offer long term finance. As such, the Government of Uganda (GoU) intends to increase gross national sav-ings from the current level of 14.5 percent to about 35 percent of GDP by 2040, as a means to accelerate structural transformation (Na-tional Planning Authority, 2013).

Uganda has made significant progress in im-proving the welfare of its citizens. During the past 10 years, the incidence of income pover-ty has declined from 38 percent in 2002/3 to 22 percent in 2013 (preliminary estimate). On the other hand, GDP grew, on average, over 5 percent during the same period while the agricultural sector performed dismally—with annual growth rates of less than 3 percent on average, during 2002/3-2012/13.

1.1 AnoverviewoftheUganda’sfinancialsector landscape

After independence in 1962 like many devel-oping countries at the time, Uganda pursued financially repressive policies that allowed government to intervene in the financial/banking system. Government intervention was in form of setting up state owned banks, interest rate controls, partial nationalisation of foreign banks and the establishment of a variety of administered lending programmes (Brownbridge 1996). This era of financial repression led to the deterioration in the performance of Uganda´s financial/banking sector. By the early 1990s Uganda´s banking system was among the weakest in Sub-Saha-ran Africa. Its liabilities comprised less than 10 percent of GDP. Domestic credit to the pri-vate sector as a percentage of GDP had fallen from about 9 percent in 1967 to about 4 per-

cent in 1992 (World Bank 2013). The number of commercial bank branches had gradually reduced from 290 in 1970 to only 84 by 1987, of which 70 percent of branches were oper-ated by public sector banks.

1.1.1 Financial sector reforms

After decades of financial repression, the gov-ernment embarked on a programme to liber-alise the financial sector with the intention of improving efficiency in resource allocation, lowering the cost of credit, increasing the ac-cess to banking services by the general popu-lation, and mobilisation of savings, all geared towards financial and economic develop-ment (Kasekende & Atingi-Ego 2003). These reforms that started in the late 1980s, were aimed at removing controls and letting the market forces determine the various prices in the banking/financial sector. The reforms included interest rate liberalisation, reduc-tion in direct credit provided by government, prudent regulation (legal and regulatory re-forms), privatisation of financial institutions, capital account liberalisation, and foreign exchange liberalisation, among others (Bat-egeka & Okumu 2010)

1.1.2Currentfinanciallandscape

Following the reforms, there has been an im-provement in the performance of Uganda’s financial sector. For instance, financial deep-ening as proxied by domestic credit provided by banking sector to GDP increased from 4 percent in 1995 to 17 percent in 2010, lending interest rates fell from 39 percent in 1990 to 20 percent in 2010. The level of non-perform-ing loans in respect to total loans has fallen from above 10 percent in 2000 to about 4 percent by June 2013 (Bank of Uganda 2013). The number of commercial bank branches per 100,000 adults increased from about 1.1 in 2004 to about 2.5 in 2010. Depositors with commercial banks per 1,000 adults increased from 87.1 in 2004 to 191.8 in 2010. These de-velopments point to some level of financial

1. INTRODUCTION AND BACKGROUND

2

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

development, increased competition and im-proved efficiency in the financial system in Uganda (Lwanga et al. 2013).

Currently there are 24 commercial banks with a total of over 400 branches, MDIs and credit institutions with over 100 branches. There are three credit institutions and four MDIs, which are complementing commercial banks in the provision of financial products and ser-vices to the population. In addition, 20 insur-ance companies are licensed and regulated by the Insurance Regulatory Authority (IRA). The financial structure also comprises of the microfinance institutions (MFI) which include SACCOs of Tier 41 by grading, providing finan-cial services to people in peri-urban and rural areas. Since 2009, there has been a tremen-dous evolution in mobile money services that has changed Uganda’s financial landscape to include a large proportion of the population that was formerly excluded from the financial services sector.

Despite the noted improvements, financial deepening in Uganda is still very low and the financial system remains underdeveloped in a number of respects. The banking sector is still highly concentrated with 3 out of 24 commercial banks accounting for approxi-mately 50 percent of the total market share i.e. assets, deposits and number of branches (Lwanga et al. 2013). Most commercial bank branches are concentrated in the capital, Kampala, and other urban centres leaving the rural population with no access to commer-cial bank services. The cost of credit in Ugan-da is still very high with prime lending rates averaging 15 percent. Interest rate spreads—one of the measures of the efficiency of the banking sector and therefore instrumental in the mobilization of investible resources—are large about 11 percent between 1992 and

1 In Uganda, financial institutions are graded in tiers based on the minimum capital requirements. Tier 1 are commercial banks with a minimum capi-tal of UShs 25 billion (about US$ 10 million). Tier 2 are credit institutions with a minimum capital of UShs 1 billion (about US$ 400,000). Tier 3 are MDIs with a minimum capital requirement of UShs 500 million (about US$ 200,000). Tier 4 are un-regulated financial institutions not authorized to receive deposits from the public.

2010, on average. As such, the large interest rate spreads discourage potential savers due to low returns on deposits and thus limits fi-nancing for potential borrowers (Lwanga et al. 2013).

1.1.3StrengtheningfinancialinclusioninUganda

In view of the above challenges and weak-nesses, on the supply side, the GoU has undertaken a number of initiatives geared towards enhancing financial inclusion. The most recent ones include: • Establishment of the Microfinance Sup-

port Centre Ltd in 2001. The Centre is funded by GoU, African Development Bank and Islamic Development Bank to facilitate access to affordable, sus-tainable and convenient financial and business development services to ac-tive and productive Ugandans through SACCOs, Unions, other MFIs and SMEs;

• Lifting the moratorium on licensing new banks in July 2007. As a result of this, eight new banks have since been li-censed.2. The period has also witnessed an accelerated branch expansion ei-ther through mergers and acquisitions or through new branch openings. The mergers resulted in less branches or at the most the same number; and

• Establishment of a credit reference bu-reau in 2008, to minimise information asymmetry between lenders and bor-rowers.

With the noted developments in the financial sector, it is imperative that an assessment is done to explore the extent to which such developments have translated into improved financial access to the Ugandan adult popula-tion. As such, regular nationally representa-tive FinScope surveys have been carried out in 18 African countries including Uganda; to provide a basis for monitoring progress in terms of demand, access to, and use of finan-

2 The specific commercial banks licensed since 2007 are Kenya Commercial Bank, Equity Bank, Fina Bank, Global Trust Bank, United Bank for Africa, Eco bank, Housing Finance Bank, ABC Bank (Kenya).

3

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

cial products and services. This information collected through the surveys provide guid-ance to the key players (including policy mak-ers, regulators and financial services provid-ers) in the financial sector on the extent of use of different services. More importantly, evidence from such surveys in Uganda can in-form the BoU’s financial inclusion initiatives – as articulated in its Strategic Plan 2012-2017.

The overall objective of the FinScope III survey was to provide data to be used to measure and to profile the levels of access to and use of financial services by adult Ugandans, rich and poor, whether located in rural or urban areas together with gender considerations. The analysis based on such data allows stake-holders to assess progress in usage patterns across all types of providers in the formal and informal sector, and across the four access strands: credit and borrowing, savings and investments, remittances and transfers, and insurance. Further still, unlike the previous FinScope surveys in Uganda, the current Fin-Scope III survey will act as a baseline to form a panel for the upcoming surveys.

More specifically this report, first, explores the extent to which the above developments in the financial sector have translated to im-proved financial access and use by the Ugan-dan adult population, i.e. to examine finan-cial access to all forms of financial products and services. Second, it provides evidence that would be used to determine access to and use of financial products and services by the Ugandan adult population on a consoli-dated basis rather than specific segments.

1.2 Data Sources

FinScope III survey builds on the previous na-tionally representative FinScope I and II con-ducted in 2006 and 2009 respectively. The three surveys provide cross-sectional data for monitoring financial inclusion in Uganda. However, there is a new development in Fin-Scope III—of tracking households—that will enable future surveys to monitor progress

based on the same individuals over time. These data will provide a richer basis for un-derstanding the dynamics in the financial sec-tor in terms of inclusion. The survey was con-ducted by REEV Consult International during June-July 2013 with technical support from the Uganda Bureau of Statistics (UBoS), Fin-Mark Trust and the Economic Policy Research Centre (EPRC).

Sample design: FinScope III survey was based on a two-stage stratified random sampling design. In the first stage the selection was based on a region and by a stratum (urban/ rural). In each stratum, the primary sample unit (PSU) was the enumeration area (EA) and was selected systematically using the probability proportion to size (PPS) mecha-nism within each stratum. Prior to the first sampling stage, it was ideal to order the sampling frame of EAs within each stratum geographically in order to provide implicit stratification and obtain a sample that was geographically representative within each region. In order to increase the efficiency of the sample design for the FinScope III survey, the sampling frame was divided into strata which were as homogeneous as possible. The first level of stratification corresponded to the geographic domains of analysis, which are the national, five regions – with Kampala as a region of its own - and rural/urban. The second stage of stratification was the EA, which was the ultimate sampling unit. A total of 4,032 households were selected using the 2012 Uganda Population and Housing Census mapping frame. Enumeration areas were al-located into the five regions (rural/urban) al-luded above. At EA level, the target was eight households. The households were selected using simple random sampling. Thereafter, one adult person (aged 16 years and above) from a list of all adults in a selected house-hold was selected using KISH grid method.

Sample size: In determining the sample size, the degree of precision (reliability) desired for the survey estimates, cost and opera-

4

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

tional limitations, and efficiency of the design were taken into consideration. The actual sampled households with complete informa-tion were 3,401, which translates to a com-pletion rate of 84 percent and response rate of 85 percent. The sample for the FinScope III was designed to provide financial indicator estimates for the country as a whole and for urban and rural areas separately; and for the five regions including Kampala.

Scope of the survey: Like the previous Fin-Scope I and II surveys, FinScope III gathered detailed demographic information of the adult population (individuals aged 16 years and above), socio-economic characteristics and use and non-use of financial services. Particular information collected included: fi-nancial and risk management strategies; fi-nancial discipline and knowledge; attitudes and perceptions of, as well as preference for, financial service providers; usage and atti-tude to mobile money technology; rural and agriculture issues; remittances; and asset ac-cumulation patterns. However, unlike earlier FinScope surveys, FinScope III included a spe-cific section on mobile money as well as ad-ditional questions to reflect the new changes in the financial landscape. The details of the sample design are provided in Appendix 1.

1.3 Methodology

1.3.1 ApproachThe report adopted the financial inclusion framework developed by FinMark Trust, which considers four financial access strands – credit and borrowing; remittances and transfer; savings and investments; and insur-ance. Within each strand, access to and use of the various products and services (formal and informal) was analysed across the adult population segments and spatially. Similar analysis was done based on the self-reported barriers to access and usage of the various products and services. At the aggregate level, all the four strands are combined to generate a single indicator.

1.3.2 Description of key variables used in the analysis

i) Financial access strand: The 2013 fi-nancial access strand is constructed in line with the structure and framework of 2009 FinScope II survey as follows:a. Formal banks regulated by the Central

Bank – Tiers 1-3: This category includes financial institutions that are directly supervised and regulated by BoU. They include: commercial banks, credit insti-tutions and MDIs;

b. Non-bank formal other: includes insti-tutions like the SACCOs and other MFIs, insurance companies and the non-banking financial institutions like for-eign exchange bureau, money transfer services like Western Union, and cell phone money services;

c. Informal includes money lenders, ROS-CAs, ASCAs, VSLAs, (NGOs), investment clubs, saving clubs, services by employ-ers and other village groups like burial societies and welfare funds. It is impor-tant to note that whoever belongs to ROSCAs or Nigiina groups is assumed to be saving informally. Others include shops and investing through property like houses for rent, livestock and crop produce to be sold later or farm inputs to use at a later date. FinScope III also considers borrowing such as credit from a shop, school, health centre and individuals as informal access. How-ever, it is important to note that such kind of borrowing is used as an alterna-tive to borrowing from formal financial institutions and informal institutions or groups; and

d. Financially excluded (unserved): these are non-users of either formal banks, non-bank formal or informal institu-tions. Products and services under fi-nancially excluded include saving in secret place, shops or friends/relatives; borrowing from friends or family mem-bers; or money transfers using individu-als.

5

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

ii) Employment categories: The main employment status is categorised as follows: selfemployed; paid employed (full time, part-time and casuals both in private and public institutions); contributing family workers (unpaid for household work) and not work-ing (including still in school, unemployed, and retired/pensioners).

iii) Highest educational attainment: In-formation was gathered on the respondents’ highest level of educational attainment. In the analysis, this variable is categorised into five (5): no formal education (never went to school); some primary (completed primary six and below); completed primary educa-tion; some secondary (completed senior three and below); and ordinary level educa-tion and above (includes all those that com-pleted ordinary secondary level and beyond).

iv) Life cycle: The life cycle of the adult population was captured through age in completed years by the time of conducting the survey. Information on age was captured as a continuous variable but as a categorical variable for the analysis. The life cycle is di-vided into five age groups. This categorisa-tion is done in such a way that the analysis could provide insights into financial inclu-sion segmentation by youth (16-17; 18-24), middle age (25-39; 40-59) and elderly (60 plus). These distinctions do reveal significant differences in both the adult population de-mographic roles and extent of financial inclu-sion.

v) Wealth index: The previous poverty studies on Uganda use consumption expendi-ture as a proxy for measuring the living stan-dards. However, unlike the Uganda National Household Surveys (UNHS), the FinScope sur-veys do not gather information on consump-tion expenditure. Instead, the study con-structed a wealth index that is similar to that commonly used in the Uganda Demographic and Health Surveys (UDHS) reports. The de-tails of how this indicator was constructed is available upon request.

vi) Regional variable: The report uses five regions instead of the usual UBoS statistical administrative regions – Central, Northern, Eastern and Western. The analysis treats Kampala as a separate region from the rest of Central region unless stated otherwise.

It is worth pointing out that the survey ques-tionnaire included the would-be useful policy categories (e.g employment, income sources, among others), some of these categories were collapsed into broader categories so as to generate statistically useful policy-orient-ed analysis. This process was guided by the level of the coefficient of variation (CV). The analysis was done at individual level for the adult population aged 16 years and above, unless stated otherwise. The estimates were weighted to reflect the total adult popula-tion composition. To shed light on financial inclusion of the adult population, the results in 2013 were compared with those based on FinScope II, where possible.

1.4 OrganisationoftheReport

The subsequent sections present the key find-ings based on the FinScope III survey data, and where possible comparisons are made with FinScope II of 2009. More specifically, Section 2 describes the Ugandan adult popu-lation by the most important socioeconomic characteristics and spatially. The section also provides insights into the supply side of the financial sector. Section 3, provides overall insights into the financial access strands and how they relate to key adult population char-acteristics. In the next sections 4-8, discus-sion focuses on the different financial strands – saving and investment; credit and borrow-ing; insurance and risk management, and re-mittances and transfers respectively. Section 9 discusses in-depth findings on access and utilisation of mobile money services prior to the discussion on financial literacy and con-sumer protection in Section 10. Section 11 concludes with implications and concrete key actions for strengthening financial inclusion for state and non-state actors.

6

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

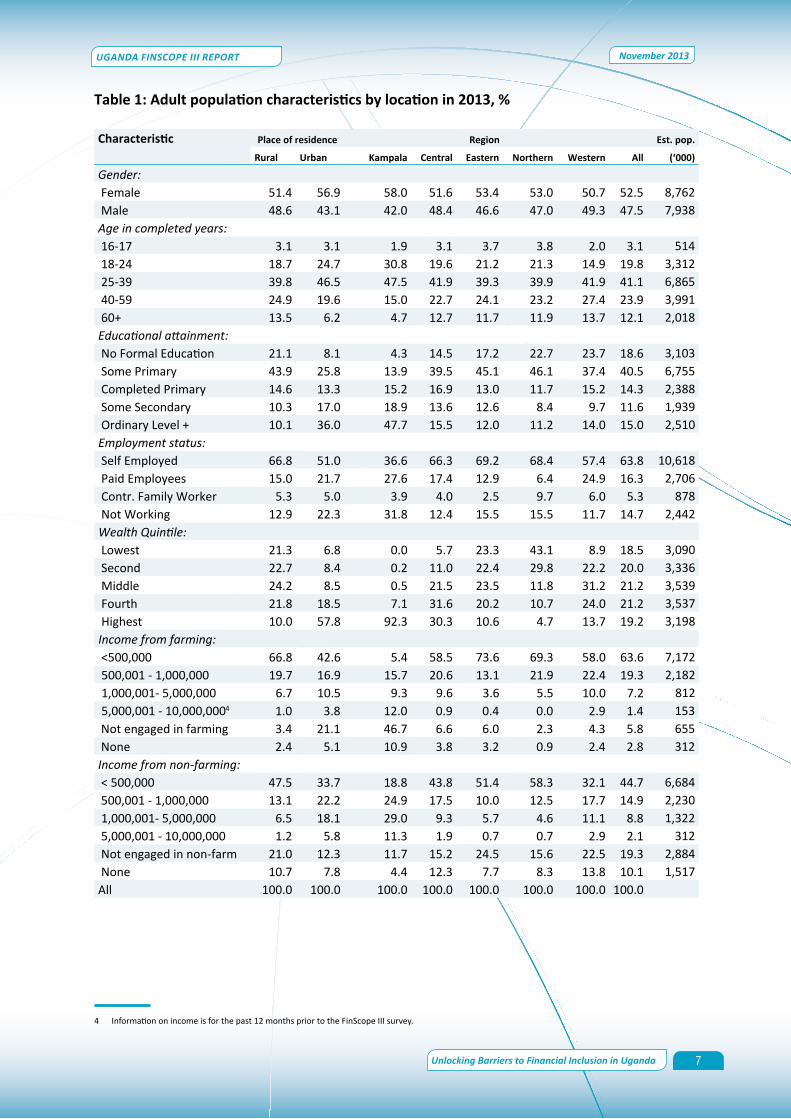

2.1 Demographics

This section presents demographics and so-cio-economic profile of the target adult pop-ulation. The results are presented in Table 1. The total adult population is estimated at 16.7 million persons, with nearly 48 percent of the adult population being males. In terms of life cycle, 23 percent were below 25 years and 40 percent of the adult population were aged between 25 – 39 years.

2.2 Socio-economiccharacteristics

At the national level, nearly two fifth of the adult population had attained some pri-mary education driven largely by individu-als resident in rural areas, and Eastern and Western regions. The adults in urban areas were more likely to have completed second-ary education and above compared to their counterparts in rural areas. Nearly 48 percent of Kampala adults had completed secondary education and above, a share well above the national average of 15 percent. Throughout the report, it was not possible to make com-parison by educational attainment over time. The variable was not captured in the same way in both previous surveys.

Nationally, 19 percent of the adult popula-tion fall in the lowest wealth quintile. The corresponding estimate for Northern region was 43 percent followed by Eastern region at 23 percent. In Kampala, 92 percent of the adult population was in the top 20 percent of the wealth distribution compared to about 5 percent in Northern region. The poverty profile based on the wealth quintile by geo-graphic location mirrors similar patterns as those based on the monetary poverty profile (see Ssewanyana & Kasirye, 2012/2013).

Turning to livelihood, the results in Table 1 confirm the importance of agriculture as the main source of employment and income. Nearly 64 percent of the adult population were self-employed. As expected the share of self-employed adults in rural areas was 67 percent, was well above the national average. Residents in Kampala were more likely to be in paid employment relative to their counter-parts in other regions. Some 15 percent of the adult population did not work in the past 12 months prior to the survey. In terms of source of income, the results suggest that the majority of the adult population (64 percent) earned less than UShs 500,0003 in a year. The particular activities engaged in (in order of importance) included: sale of produce from own food crop production; running own busi-ness; working on other people’s farms; and sale of produce from own cash crop produc-tion.

3 This income level is equivalent to USD200 at the exchange rate of USD1=Shs2,580.

II RESULTS OF THE SURVEY

2. BackgroundCharacteristicsoftheAdultPopulation

7

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

Table1:Adultpopulationcharacteristicsbylocationin2013,%

Characteristic Place of residence Region Est. pop.

Rural Urban Kampala Central Eastern Northern Western All (‘000)

Gender: Female 51.4 56.9 58.0 51.6 53.4 53.0 50.7 52.5 8,762 Male 48.6 43.1 42.0 48.4 46.6 47.0 49.3 47.5 7,938Age in completed years: 16-17 3.1 3.1 1.9 3.1 3.7 3.8 2.0 3.1 514 18-24 18.7 24.7 30.8 19.6 21.2 21.3 14.9 19.8 3,312 25-39 39.8 46.5 47.5 41.9 39.3 39.9 41.9 41.1 6,865 40-59 24.9 19.6 15.0 22.7 24.1 23.2 27.4 23.9 3,991 60+ 13.5 6.2 4.7 12.7 11.7 11.9 13.7 12.1 2,018Educational attainment: No Formal Education 21.1 8.1 4.3 14.5 17.2 22.7 23.7 18.6 3,103 Some Primary 43.9 25.8 13.9 39.5 45.1 46.1 37.4 40.5 6,755 Completed Primary 14.6 13.3 15.2 16.9 13.0 11.7 15.2 14.3 2,388 Some Secondary 10.3 17.0 18.9 13.6 12.6 8.4 9.7 11.6 1,939 Ordinary Level + 10.1 36.0 47.7 15.5 12.0 11.2 14.0 15.0 2,510Employment status: Self Employed 66.8 51.0 36.6 66.3 69.2 68.4 57.4 63.8 10,618 Paid Employees 15.0 21.7 27.6 17.4 12.9 6.4 24.9 16.3 2,706 Contr. Family Worker 5.3 5.0 3.9 4.0 2.5 9.7 6.0 5.3 878 Not Working 12.9 22.3 31.8 12.4 15.5 15.5 11.7 14.7 2,442Wealth Quintile: Lowest 21.3 6.8 0.0 5.7 23.3 43.1 8.9 18.5 3,090 Second 22.7 8.4 0.2 11.0 22.4 29.8 22.2 20.0 3,336 Middle 24.2 8.5 0.5 21.5 23.5 11.8 31.2 21.2 3,539 Fourth 21.8 18.5 7.1 31.6 20.2 10.7 24.0 21.2 3,537 Highest 10.0 57.8 92.3 30.3 10.6 4.7 13.7 19.2 3,198Income from farming: <500,000 66.8 42.6 5.4 58.5 73.6 69.3 58.0 63.6 7,172 500,001 - 1,000,000 19.7 16.9 15.7 20.6 13.1 21.9 22.4 19.3 2,182 1,000,001- 5,000,000 6.7 10.5 9.3 9.6 3.6 5.5 10.0 7.2 812 5,000,001 - 10,000,0004 1.0 3.8 12.0 0.9 0.4 0.0 2.9 1.4 153 Not engaged in farming 3.4 21.1 46.7 6.6 6.0 2.3 4.3 5.8 655 None 2.4 5.1 10.9 3.8 3.2 0.9 2.4 2.8 312Income from non-farming: < 500,000 47.5 33.7 18.8 43.8 51.4 58.3 32.1 44.7 6,684 500,001 - 1,000,000 13.1 22.2 24.9 17.5 10.0 12.5 17.7 14.9 2,230 1,000,001- 5,000,000 6.5 18.1 29.0 9.3 5.7 4.6 11.1 8.8 1,322 5,000,001 - 10,000,000 1.2 5.8 11.3 1.9 0.7 0.7 2.9 2.1 312 Not engaged in non-farm 21.0 12.3 11.7 15.2 24.5 15.6 22.5 19.3 2,884 None 10.7 7.8 4.4 12.3 7.7 8.3 13.8 10.1 1,517All 100.0 100.0 100.0 100.0 100.0 100.0 100.0 100.0

4

4 Information on income is for the past 12 months prior to the FinScope III survey.

8

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

2.3 Physicalaccesstofinancialinstitutions(supply side)

In terms of physical access to financial insti-tutions, Table 2 reveals that access varied by type of institution and location. The adult population resident in urban areas and in par-ticular Kampala had better access to financial institutions relative to their counterparts in other regions. The gap (based on share of the

Figure1:Householdsmostimportantsourceofincomein2013,%

adult population) between rural and urban areas was least with informal institutions – 10 percentage points. It is also evident that adults resident in Central and Western re-gions had better access to commercial banks than Eastern and Northern regions. These findings have implications for financial inclu-sion as discussed in the subsequent sections.

Table2:Distancetothenearestfinancialinstitutionbylocationin2013,%

Location Commercial bank Semi-formal Informalinstitution

<5 km > 5 km <5 km > 5 km <5 km > 5 kmPlace of residenceRural 21.5 78.5 44.9 55.1 84.3 15.7Urban 57.7 42.3 81.4 18.6 94.2 5.8Region:Kampala 93.3 6.7 96.9 3.1 100.0 0.0Central 36.5 63.5 50.5 49.5 86.9 13.1Eastern 22.9 77.1 43.9 56.1 84.6 15.5Northern 12.7 87.3 43.7 56.4 85.1 14.9Western 32.5 67.6 60.3 39.7 85.9 14.1Uganda 28.5 71.5 51.0 49.0 85.9 14.1

9

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

3. Financial Inclusion

This Section presents the status of Uganda fi-nancial inclusion consolidated for all the four access strands as described in Section 1 – sav-ings and investment, credit and borrowing, remittance and transfers, and insurance. The Section discusses the overall usage of finan-cial institutions as a first step in understand-ing the financial access strand. The analysis is done across the socio-economic characteris-tics of the adult population and spatially.

3.1 Overallfinancialusage

Broadly speaking, the adult population ac-cessed multiple source of diverse financial service institutions. Figure 2 presents the overall usage of financial services by the adult population. The share of the adult population that accessed formal institutions (banked and non-bank formal) increased by almost two fold from 28 percent in 2009 to 54 percent in 2013. The growth was driven by the increase in the non-bank formal from 20 percent in 2009 to 52 percent in 2013. On the other hand, the increase in the adult population using informal institutions was not as fast as that observed for formal financial institu-tions. Although not presented in Figure 2, 15 percent of the adult population (representing 2.6 million adults) accessed both formal and informal financial institutions.

3.2 Financial access strand

As noted in section 3.1, there are overlaps in the financial products and services usage. In this section, these overlaps are removed. Figure 3 ranks the adult population’s financial access strands based on financial tiers by BoU - mutually exclusive use of financial services. Nearly 85 percent of the adult population had access to financial institutions in 2013 compared to 70 percent in 2009. The results reveal that in 2013, 20 percent of the adult population (translates into an estimated 3.4 million adults) were using formal regulated fi-nancial intermediation service, and nearly 34 percent were using only non-bank formal in-stitutions, and 31 percent (translates into an estimated 5.1 million adults) were using only informal institutions financial products and services. About 2.6 million adults were finan-cially excluded in 2013 – contributing about 15 percent of the total adult population. This marks a reduction from 30 percent (4.3 mil-lion adults) in 2009.

Figure 3 further presents a comparison with estimates based on the previous FinScope II survey. Clearly, there are no significant dif-ferences between the proportion of the adult population accessing formal bank institu-tions between 2009 and 2013. Yet, in abso-lute terms, there was an increase of 400,000 adults over a four-year period. This finding

Figure2:Overallusageoffinancialservices,%

10

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

suggests a rather slow improvement in the usage of products and services from formal bank institutions. This raises policy concerns of the slow demand for formal bank financial services given the reforms and developments in the financial sector as articulated in Sec-tion 1.

There was a significant reduction in informal inclusion from 42 percent in 2009 to 31 per-cent in 2013 whereas only non-bank formal inclusion increased by 27 percentage points. This could be explained by the movement of a proportion of the population from usage of the informal to non-bank formal products and services especially mobile money services. The rather high incidence of access to infor-mal services by the adult population is partly explained by the emerging rural and commu-nity based savings groups such as VSLAs and ASCAs as channels saving and borrowing.

Of special interest was the significant increase in non-bank formal inclusion to 34 percent in 2013 from 7 percent in 2009 (Figure 3). This drastic change was driven mainly by provision of mobile money services (see Figure 4). In-depth analysis reveals that 5.1 million adults used mobile money services, accounting for more than 90 percent of the non-bank formal services. The usage of mobile money services was three times that of the other non-bank services. As such the non-bank formal ser-vices excluding mobile money accounted for about 3 percent whereas the mobile money services accounted for 31 percent. These findings imply that the contribution of non-bank institutions excluding mobile money services to the provision of financial services remained very low. This finding seem to sug-gest a faster uptake of mobile money services relative to SACCOs and other forms of MFIs. The share of the urban adult population using mobile money services (38 percent) was well

Figure3:Mutuallyexclusiveuseoffinancialservicesbyinstitutions,%

Source: Author’s calculations based on FinScope II and III.

11

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

above the national average, and there were observed rural/urban and gender differences. The financial inclusion through mobile mon-ey is attributed to the product innovation of mobile money introduced by the mobile tele-phone networks in 2009. This phenomenon is discussed in detail in Section 9.

the demand for financial services depends on the level of development of the local econo-mies. It is anticipated that the current focus by GoU on infrastructure – notably roads and energy – will partly encourage the financial service providers to move to underserved re-gions.

Figure4:Financialaccessstrandwithmobilemoneyservicesin2013,%

Next the report explores how the above na-tional estimates relate to financial access strands by socio-economic characteristics. Table 3 shows that the patterns and trends observed at national level were similar to those observed by disaggregated characteris-tics. Specifically, the Western region had the least proportion of the financially excluded, whereas the adult population resident in Northern region was more likely to be in-formally included compared to counterparts in other regions. The very low formal finan-cial inclusion in Northern region is partly ex-plained by the high income poverty levels and the low bank concentration as a result of the 20-year civil war experienced in this part of the country. This finding seems to cor-roborate the low physical access to financial institutions as illustrated in Table 2 in section 2.3. As expected, residents of Kampala had the highest proportion of the adult popula-tion using formal banking institutions—49 percent. This is explained by the high concen-tration of financial institutions in Kampala. At least 28 percent of residents in Western region used formal banking institutions, fol-lowed by those in the Central region at 21 percent. Overall, these findings suggest that

Compared to FinScope II in 2009, There was a decline in the use of formal banks in east-ern region, there was a significant increase in Western region in the share of the adult pop-ulation with access to formal banking from 18 percent to 28 percent in 2013. While adults resident in Northern and Eastern regions reg-istered 10 percentage points reduction in the use of informal services over a four year peri-od, the incidence of usage of informal servic-es remained well above the national average – with four in every 10 adults using informal services.

Turning to the rural/urban divide, there are marked differences as shown in Figure 4. The results reveal that 2.2 million adults resident in rural areas had access to formal banking institutions whereas 2.2 million adults were financially excluded in 2013. The rather high incidence of formal banking in urban areas (36 percent) is partly due to the fact that for-mal banking institutions target where there is good customer catchment to transact prof-itable businesses with banks. On the other hand, the adult population in rural areas reg-istered high accessibility to financial services through only informal institutions. The ease

12

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

of access to such informal financial services in terms of cost and flexible terms of payment of the loans advanced, partly explains this find-ing. There was a marginal decrease in access to formal banking from 39 percent in 2009 to 36 percent in 2013 among the adult popula-tion in urban areas. This decrease, although, marginal needs policy attention in line with the reforms and developments in the finan-cial sector. Noteworthy, is the seemingly widening rural/urban gap in the share of the adult population accessing non-bank formal financial services and the high incidence of financial exclusion. On the other hand, there are no noticeable gaps in the level of informal and formal banking.

Considering gender, it is clear that access through the formal banking system was more pronounced in males than in females (Fig-ure 4), but the gender gap remained almost the same after a four-year period. The gen-der gap in formal banking could be indicative of the fact that formal financial institutions’ terms and conditions favour males over fe-males, although this should not be inter-preted as deliberate discrimination. While females were more likely to report use of

only informal financial services, their male counterparts were more likely to report use of only formal banking services. Whether the higher likelihood to access and usage of in-formal financial institutions among the adult females was due to easy access and flexible terms is debatable. More importantly, there is a growing gender gap in use of informal financial services. The financial exclusion by gender declined between 2009 and 2013 as well as the gender gap.

Financial inclusion depicts a life cycle dimen-sion (Table 3). In terms of formal banking services, there are noticeable differences between the youth population (18-24 years) with their middle aged (25-39 and those aged 40-59 years) counterparts. Among the youth population only 15 percent were formally in-cluded in the formal banking, well below the national average. The rather high access to non-bank formal services is partly driven by the mobile money services. Both the youth and elderly persons were more likely to be financially excluded at about 19 percent and 23 percent respectively. The levels of exclu-sion were well above the national average.

13

UGANDA FiNScope iii RepoRT

Unlocking Barriers to Financial inclusion in Uganda

November 2013

Table3:Useoffi

nancialservices(m

utua

llyexclusive)b

yad

ultp

opulati

oncha

racteristicsin

201

3,%

2009

2013

Char

acte

ristic

s F

orm

al B

ank

Non

-ban

k fo

rmal

Info

rmal

Exc

lude

d F

orm

al B