TV2007 Finance and growth - Antonio Ciccone · Long-Run Equilibrium (Perfect Financial Markets),,...

77

Finance and Growth

Transcript of TV2007 Finance and growth - Antonio Ciccone · Long-Run Equilibrium (Perfect Financial Markets),,...

Finance and Growth

2

INTRODUCTION

What are the effect of the quality of the financial system oneconomic growth?

Theory (Levine, Finance and Growth, Handbook of EconomicGrowth, 2005)

3

4

5

6

7

Empirical CROSS-COUNTRY studies on finance and growth

How is “Finance” measured?

-- SIZE MEASURES

(1) BANK CREDITGDP

CORPORATE BONDSGDP

(2)

STOCK MARKET CAPITALIZATIONGDP

(3)

And, most importantly, (1)+(2)+(3)

8

-- STRUCTURE MEASURES

(1) Measures of bank competition

(2) Measures of efficiency of contract enforcement

(3) Measures of protection of minority shareholders

(4) Measures of “informativeness” of stock market

9

Empirical CROSS-COUNTRY studies on finance and growth (1)

Cross-country work linking size measures of financial markets to (subsequent) growth (many studies, see Levine’s review)

,1996 1960

1 ,1960

2

3 ,1960 1960 4 1960

log log*100

36

log log

c c

c

c

c c c

y y

FD

X

FD y y

β

β

β β

−

= +

+

+ +

10

Empirical CROSS-COUNTRY studies on finance and growth (2)

Cross-country before-after studies linking financial liberalization to growth

( ), , 1

1 , 2 , 4 , 1

log log

log

c t c t

c t c t c t

y y

FD X yβ β β

−

−

−

= + +

e.g. Bekaert, Harvey, and Lundblad, “Does Financial Liberalization Spur Growth,” Journal of Financial

Economics, forthcoming.

11

Empirical CROSS-COUNTRY studies on finance and growth (3)

Cross-country empirical work on how FINANCE improvesthe country-level response to “growth opportunities”

e.g. Bekaert, Harvey, and Lundblad, “Global growth opportunities and market integration,” Journal of Finance,

forthcoming.

12

Hypothesis:Financial system mobilized funds when they can be productively employed (when there is a growth opportunity)

“Growth opportunity for the country”?

1 21 1

...

ct

ct ct Ictt t It

GrowthOpportunity

P P PE E E

ω ω ω⎛ ⎞ ⎛ ⎞ ⎛ ⎞= + + +⎜ ⎟ ⎜ ⎟ ⎜ ⎟⎝ ⎠ ⎝ ⎠ ⎝ ⎠

Global sectoralprice-earningsratios

Country-sector-specific weights

13

PE ratio: Measure the value of a stock relative to currentearnings. High values are seen to proxy for high futurerelative to current earnings.

Value Production(1)Total Production

ictict

ct

ω =

Stock Market Cap(2)Total Stock Market Cap

ictict

ct

ω =

Weights:

14

( ), , 1 1 , 1 2 ,log logc t c t c t c ty y GrOpp Xβ β− −− = +

( ), , 1

1 , , 1 2 , 4 , 1

log log

log

c t c t

c t c t c t c t

y y

FD GrOpp X yβ β β

−

− −

−

= + +

EMPIRICAL SPECIFICATIONS:

(1)

(2)

15

Do Growth Opportunities Affect Economic Growth?

16

“OPENNESS MEASURES”

17

18

19

“STRUCTURAL MEASURES”

20

21

22

CHANNEL ANALYSIS USING

DISAGGREGATE,

INDUSTRY ANALYSIS

23

More disaggregate studies of “channels” through which finance potentially impacts growth

ONE AGGREGATE CHANNEL:Lowers cost of capital. More capital productivity.

DISAGGREGATE, INDUSTRY STUDY:

Lower cost of capital should be more important for

industries relying more heavily on external capital

24

Analyzing channels using industry data

Rajan and Zingales, AER, 1998

Does greater financial development have dis-proportionate growth effecton industries that are finance dependent?

25

(COMPUSTAT) Finance dependence industry i?

, ,,

,

i U S i U Si i U S

i U S

I C A S H F L O WE X T F I N E X T F I N

I−

= =

26

Dis-proportionate growth effect?

, , , ,ln i c i c i US c i c i cY EXTFIN FD SHARE uη τ α γ⎡ ⎤∆ = + + + +⎣ ⎦

, , , ,ln i c i c iUS c i c i cY EXTFIN FD SHARE uη τ α γ⎡ ⎤∆ = + + + +⎣ ⎦

PERSPECTIVE 1

PERSPECTIVE 2

27

28

29

30

31

32

Questions

RZ-1-- Rybczynski effect?

FD up Cost of (external) capital down Shift towards external capital intensive industries?

THEN should it not be?: ,c i USFD EXTFIN∆ ×

33

QuestionsRZ-2

-- Heckscher-OhlinGreater FD Lower cost of (external) capital Greater production in (external) capital intensive industries?

& -- transition dynamics after shock that took economy out of steady state?

THEN Why should production structure return to steady state? E.g. shock to cost of capital.

34

Questions

RZ-3

-- Cost of external capital would seem to affect industries through entire debt, not just externally funded investment

-- Interest rate affects more capital intensive industries more; must be controlled for

35

Questions

RZ-4

--

-- I could be proxy for growth opportunities

, ,,

,

i U S i U Si i U S

i U S

I C A S H F L O WE X T F I N E X T F I N

I−

= =

36

“Channels” through which finance potentially impacts growth

Reallocates capital more quickly to where it is most productive

37

Analyzing channels using industry data

Fisman & Love, JF, 2004; NBER, 2004Does greater financial development speed up resource reallocation to industries that have good growth opportunities?

(COMPUSTAT) Growth opportunity industry i

Speed up resource reallocation?

, ,ln ...i c i c i US cY GROWTHOPP FDη τ β∆ = + + +

, ,i i US i USGROWTHOPP GROWTHOPP SALESGROWTH= =

38

39

40

41

42

43

, ,i US i i USEXTFIN EXTFIN ε= +

Questions

RZ-FL

--

-- , ,i US i i USGROWTHOPP GROWTHOPP ν= +

Measurement error bias really necessarilydownwards?

44

FURTHER WORK ON FINANCE INTERSECTORAL REALLOCATION in response to “Growth Opportunities”

-- Theoretical framework to study link between finance and speed of capital reallocation-- Analysis of the consequences of measurement error due to “country idiosyncratics”-- Deal with bias due to country idiosyncratics

45

Overview

1. Theoretical framework 2. Model estimation issues

1. Bias when employing US (or any other country) data to construct global industry characteristics

2. Dealing with measurement error bias 3. Data4. Results

1. Using US-based proxy only2. Accounting for measurement error

46

Theoretical Framework: Perfect Financial Markets

Shifts (country; industry; country-industry)in productivity and preferences

Industry-country optimal capital if financial markets were perfect (target)

Industry value added growth

Theoretical Framework – Estimation – Data - Results

47

Theoretical Framework: Financial Development as an ADJUSTMENT MECHANISM

Shifts (country; industry; country-industry)in productivity and preferences

Industry-country optimal capital if financial markets were perfect (target)

Industry value added growth

FinancialDevelopment

Actual capital growth

Theoretical Framework – Estimation – Data - Results

48

Model Set-Up

, ,

, , , ,

1

1, ,

0 0

(1 )11

, , (1 ), , , , , ,

, , , 0

, , , , , ,

Preferences

ln 0 1

Demand

Supply

i c t

i c t i c t

I C

t i c t

Ci c tt

i c t i c t i c ti t i c t

i c t i c t i c t

U x B dc

pMx B P p B dcP P

Z A K

ρρ ρ

ρρ ρρ

ρ

ρ−

− −− − −−

⎛ ⎞= < ≤⎜ ⎟

⎝ ⎠

⎛ ⎞ ⎛ ⎞= =⎜ ⎟ ⎜ ⎟⎜ ⎟ ⎝ ⎠⎝ ⎠

=

∫ ∫

∫

Theoretical Framework – Estimation – Data - Results

Industries Countries

49

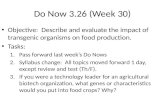

Long-Run Equilibrium (Perfect Financial Markets)

, , , ,

* * *, ,

, ,

*, , , , , , , , , ,

1, ,*

, ,, , ,

or

ln ln ln Country-effect ln

i c t i c t

ti c t t

i c t

i c i c T i c T i c S i c S i c

i c t ti c t t

t i c t i t

rA p r p MCA

Y p Z p Z K

B rK Mr A P

ρρ− −

= = =

∆ = − = + ∆

⎛ ⎞= ⎜ ⎟⎜ ⎟

⎝ ⎠

Theoretical Framework – Estimation – Data - Results

Target capital increases reflect anticipated future industry growth opportunities (due to technical change, demand shifts, and

changing prices of international competitors)

50

Financial Development and Target Capital Adjustment

cφ

*,ln i cK∆

( ) *, ,ln 1 ln 0 1i c c i c cK Kλ λφ φ∆ = − + ∆ ≤ ≤⎡ ⎤⎣ ⎦

Theoretical Framework – Estimation – Data - Results

,ln i cK∆

1

λ

0

51

Financial Development and Target Capital Adjustment

Target capital increases translate into faster value added growth in countries with high levels of financial development

( )

( )

* *, , , ,

*, ,

Price adjustment:

ln (1 ) ln ln ln

Value added and target capital growth:

ln 1 ln ln

i c i c i c i c

i c c i c t

p K K MC

Y K r

ρ

θ θφ θ λρ

∆ = − ∆ −∆ + ∆

∆ = − + ∆ + ∆ =⎡ ⎤⎣ ⎦

Theoretical Framework – Estimation – Data - Results

52

Technology & preference shifts, and target capital

, , , ,

* * *, ,

, , ,

ln ; ln

ln ln ln

/(1 )

i c c i i c i c c i i c

i c c i i c

i c i c i c

A a a a B b b b

K K K

b a

ε

ε ρ ρ

∆ = + + ∆ = + +

∆ = ∆ + ∆ +

= + −

Theoretical Framework – Estimation – Data - Results

Global industry investment

opportunity

“Country Indiosyncratics”

Country effect

53

Value added growth andglobal industry investment opportunities

*, ,ln Country-effects [(1 ) ] ln [(1 ) ]i c c i c i cY Kθ φ θ θ φ θ ε∆ = + − + ∆ + − +

Theoretical Framework – Estimation – Data - Results

54

Effect of financial development on value added growth

cφ

Theoretical Framework – Estimation – Data - Results

0

1

1

(1 ) cθ φ θ− +

θ

55

Model Estimating Equation:

Theoretical Framework – Estimation – Data - Results

*, ,

* *, ,

ln Country-effects [(1 ) ] ln [(1 ) ]

Target capital growth=Actual capital growth in US

ln ln ln

i c c i c i c

i US US i i US

Y K

K K K

θ φ θ θ φ θ ε

ε

∆ = + − + ∆ + − +

∆ = ∆ + ∆ +

56

Classical measurement error:

Theoretical Framework – Estimation – Data - Results

*, ,

* *, ,

, ,

(1) ln Country-effects [(1 ) ] ln [(1 ) ]

(2) ln ln ln

and are independent

i c c i c i c

i US US i i US

i c i US

Y K

K K K

θ φ θ θ φ θ ε

ε

ε ε

∆ = + − + ∆ + − +

∆ = ∆ + ∆ +

57

Downward bias due to classical measurement error:

[ ]*

,

( )(1 )( )

ic

i US

Var KVar K

θ φ θ⎛ ⎞

− + ⎜ ⎟⎜ ⎟⎝ ⎠

cφ

Theoretical Framework – Estimation – Data - Results

0

1

1

(1 ) cθ φ θ− +

58

Upward bias due to measurement error:

Theoretical Framework – Estimation – Data - Results

( ), , , ,

, ,

(2) in (1) yields US-proxy ESTIMATING EQUATION

ln Country-effects [(1 ) ] ln [(1 ) ]

TWO GROUPS OF COUNTRIES

Group 1--HIGH Financial Development:

Group 1--LOW Finan

i c c i US c i c i US

i c i US

Y Kθ φθ θ φθ ε ε

ε ε

∆ = + − + ∆ + − + −

=

, ,cial Development: and are independenti c i USε ε

59

Upward bias due to measurement error:

[(1 ) ]HIGHθ φ θ− +

LOWφ HIGHφ

Theoretical Framework – Estimation – Data - Results

[(1 ) ]LOWθ φ θ− +

True values

Least squaresestimates

0

1

60

Accounting for measurement error:

*, ,

,

* *,

*,

(1) ln Country-effects [(1 ) ] ln [(1 ) ]

Ignore for a moment

ln Country-effects (1 ) ln ln

ln Country-effects Industry-effects ln

i c c i c i c

i c

i c i c i

i c c i

Y K

Y K K

Y K

θ φ θ θ φ θ ε

ε

θ φ θ

φ θ

∆ = + − + ∆ + − +

∆ = + − ∆ + ∆

∆ = + + ∆

Theoretical Framework – Estimation – Data - Results

,

,

ln Country-effect

ln

i c i c i

PREDICTED EST ESTi US i US i

Y

Y

φ

φ

∆ = +Θ + Λ

∆ = Θ + Λ

61

Accounting for measurement error:

( )

( )

, , , ,

, , , ,

(2) in (1) yields US-proxy EQUATION

ln Country-effects [(1 ) ] ln [(1 ) ]

ln Country-effects Industry-effects ln [(1 ) ]

i c c i US c i c i US

i c c i US c i c i US

Y K

Y K

θ φ θ θ φ θ ε ε

θφ θ φ θ ε ε

∆ = + − + ∆ + − + −

∆ = + + ∆ + − + −

Theoretical Framework – Estimation – Data - Results

,

,

Instrument for ln :

ln

i US

PREDICTED EST ESTi US i US i

K

Y φ

∆

∆ = Θ + Λ

62

Data1. Country-Industry level (from UNIDO)

• Value added growth in the eighties• 66 countries; 28 manufacturing industries

2. Country-level• FD: main measure is private credit to GDP (PRIVC)• Other control variables: GDP, institutions, human capital

3. Industry-levelExploit the NBER-Manufacturing database. In contrast to COMPUSTAT more

representative (key for international comparisons)• Capital growth• Other proxies of sector growth opportunities, employed in the literature

Theoretical Framework – Estimation – Data - Results

63

Least squares approach

Theoretical Framework – Estimation – Data - Results

, , ,

LEAST-SQUARES ESTIMATION OF

ln Country-effects Industry-effects lni c c i US i cY FD K uα∆ = + + ∆ +

64

Least squares approach: Opportunities and RZ financedependence

(1) (2) (3) (4) (5) (6)

SHARE80i,c -0.1900 -0.1981 -0.1955 -0.0724 -0.0809 -0.0803(3.75) (3.83) (3.79) (3.12) (3.49) (3.47)

Finance X Investment Opportunities 0.3485 0.2905 0.3433 0.2261[PRIVCR X CAPGR ] (3.35) (2.34) (5.22) (3.22)

Finance X External Finance Dependence 0.0179 0.0109 0.0228 0.0146[PRIVCR X EXTFIN ] (2.25) (1.28) (5.17) (3.09)

Adjusted R2 0.2986 0.2962 0.2991 0.4489 0.4565 0.4540Countries 66 66 66 66 66 66Observations 1589 1589 1589 1589 1589 1589Industry Fixed-Effects Yes Yes Yes Yes Yes YesCountry Fixed-Effects Yes Yes Yes Yes Yes Yes

OLS Robust Estimation

Theoretical Framework – Estimation – Data - Results

65

Least squares approach: Alternative proxies of opportunities

Theoretical Framework – Estimation – Data - Results

,( )i i USGROWTHOPP Fisman Love SALESGROWTH− =

= Anticipated Growth Opportunity

+

Effect of Unanticipated Demand Shifts on Sales

66

Least squares approach: Alternative proxies of opportunities

(1) (2) (3) (4)

SHARE80i,c -0.1875 -0.1922 -0.1838 -0.1971(3.68) (3.81) (3.61) (3.83)

Finance X Investment Opportunities 0.5551 0.5349[PRIVCR X CAPGR ] (3.05) (3.26)

Finance X Sales Growth 0.1724 -0.2309[PRIVCR X SALESGR ] (1.77) (1.38)

Finance X Value Added Growth 0.1391 -0.1860[PRIVCR X VAGR ] (1.58) (1.37)

adj. R-squared 0.2946 0.2992 0.2944 0.2991Countries 66 66 66 66Observations 1589 1589 1589 1589Industry Fixed-Effects Yes Yes Yes YesCountry Fixed-Effects Yes Yes Yes Yes

OLS

Theoretical Framework – Estimation – Data - Results

Least squares approach: Alternative adjustment channels

(1) (2) (3) (4) (9) (10) (11) (12)

Finance X Invest. Opport. 0.3520 0.2986 0.3664 0.3026[PRIVCR X CAPGR ] (2.93) (4.11) (3.54) (4.26)

Law X Invest. Opport. -0.2141 -0.0604 -0.1977 -0.0782[LAW X CAPGR ] (2.71) (0.68) (3.26) (1.15)

Schooling X Invest. Opport. 0.0567 0.0238 0.0537 0.0327[SCH X CAPGR ] (2.36) (1.03) (3.15) (1.80)

adjusted R-squred 0.3159 0.3207 0.4758 0.4800 0.3037 0.3086 0.4559 0.4581Countries 57 57 57 57 1524 1524 1524 1524Observations 1435 1435 1435 1435 62 62 62 62Industry Fixed-Effects Yes Yes Yes Yes Yes Yes Yes YesCountry Fixed-Effects Yes Yes Yes Yes Yes Yes Yes Yes

Legal System Quality (LAW ) Schooling (SCH )OLS Robust OLS Robust

Theoretical Framework – Estimation – Data - Results

68

Least squares approach: Controlling for income

OLS Robust IV(1) IV(2) OLS Robust IV(1) IV(2)

(1) (2) (3) (4) (5) (6) (7) (8)

SHARE80i,c -0.1889 -0.0683 -0.1936 -0.1906 -0.1755 -0.0704 -0.1786 -0.1773 (3.70) (2.93) (3.70) (3.71) (3.04) (2.86) (3.05) (3.05)

Finance X Invest. Opport. 0.2162 0.1942 1.0587 0.5104 0.3528 0.3400 1.0448 0.7632[PRIVCR X CAPGR ] (1.41) (1.90) (2.78) (1.98) (3.45) (4.66) (4.61) (4.58)

Income X Invest. Opport. 0.0939 0.0936 0.2278 0.1506[Y X CAPGR ] (1.33) (1.52) (1.39) (1.16)

R-squaredCountries 0.2988 0.4516 0.3069 0.3366 0.3344 0.4889 0.3561 0.3686Observations 5.76 14.68 12.19 13.05 6.10 16.54 13.39 14.18Industry Fixed-Effects 65 65 65 65 53 53 53 53Country Fixed-Effects 1562 1562 1562 1562 1317 1317 1317 1317

All countries Dropping Low Income Countries

Theoretical Framework – Estimation – Data - Results

69

New (IV) Approach to deal with country-idiosyncratics

, , ,

INSTRUMENTAL-VARIABLES ESTIMATION OF

ln Country-effects Industry-effects lni c c i US i cY FD K uα∆ = + + ∆ +

Theoretical Framework – Estimation – Data - Results

,

,

Instrument for ln :

ln

i US

PREDICTED EST ESTi US i US i

K

Y FD

∆

∆ = Θ + Λ

Estimated across countrieswithout US

70

Predicted and Actual US Industry Growth

311313

314

321

322

323324 331

332 341

342

351

352

353

354

355

356

361

362

369

371

372

381382

383

384

385

390

-.02

0.0

2.0

4.0

6C

apita

l Gro

wth

in th

e U

nite

d St

ates

(KH

AT)

0 .02 .04 .06 .08 .1Predicted Capital-Value Added Growth in the United States (est. with OLS)

Theoretical Framework – Estimation – Data - Results

slope=0.48

t-stat=3.39

1/(reverse regressionslope)=1.62

71

Predicted and Actual US Industry Growth

311313

314

321

322

323324 331

332 341

342

351

352

353

354

355

356

361

362

369

371

372

381382

383

384

385

390

-.04

-.02

0.0

2.0

4.0

6C

apita

l Gro

wth

in th

e U

nite

d St

ates

(KH

AT)

0 .02 .04 .06 .08 .1Predicted Capital-Value Added Growth in the United States (est. with Huber)

Theoretical Framework – Estimation – Data - Results

slope=0.66

t-stat=4.69

1/(reverse regressionslope)=1.65

72

New Approach: Instrumental Variable Estimates

IV(1) IV(2)

(1) (2)

SHARE80i,c -0.1931 -0.1913(3.74) (3.75)

Finance X Investment Opportunities 1.1683 0.6872[PRIVCR X CAPGR ] (4.01) (3.72)

centered R-squared 0.3108 0.3351F-score 12.15 13.51Countries 66 66Observations 1589 1589Industry Fixed-Effects Yes YesCountry Fixed-Effects Yes Yes

Theoretical Framework – Estimation – Data - Results

73

New Approach: Other opportunities measures

Theoretical Framework – Estimation – Data - Results

,( )i i USGROWTHOPP Fisman Love SALESGROWTH− =

= Anticipated Growth Opportunity

+

Effect of Unanticipated Demand Shifts on US Sales

74

New Approach: Other opportunities measures

(1) (2) (3) (4)

SHARE80i,c -0.1812 -0.1541 -0.1851 -0.1709(3.41) (3.00) (3.53) (3.36)

Finance X Sales Growth 1.1794 0.5541[PRIVCR X SALESGR ] (2.78) (2.80)

Finance X Value Added Growth 1.0054 0.5156[PRIVCR X VAGR ] (2.75) (2.77)

centered R-squared 0.282 0.2823 0.3286 0.326Countries 66 66 66 66Observations 1589 1589 1589 1589Industry Fixed-Effects Yes Yes Yes YesCountry Fixed-Effects Yes Yes Yes Yes

IV(1) IV(2)

Theoretical Framework – Estimation – Data - Results

75

New approach: Controlling for income

OLS Robust IV(1) IV(2) OLS Robust IV(1) IV(2)

(1) (2) (3) (4) (5) (6) (7) (8)

SHARE80i,c -0.1889 -0.0683 -0.1936 -0.1906 -0.1755 -0.0704 -0.1786 -0.1773 (3.70) (2.93) (3.70) (3.71) (3.04) (2.86) (3.05) (3.05)

Finance X Invest. Opport. 0.2162 0.1942 1.0587 0.5104 0.3528 0.3400 1.0448 0.7632[PRIVCR X CAPGR ] (1.41) (1.90) (2.78) (1.98) (3.45) (4.66) (4.61) (4.58)

Income X Invest. Opport. 0.0939 0.0936 0.2278 0.1506[Y X CAPGR ] (1.33) (1.52) (1.39) (1.16)

R-squaredCountries 0.2988 0.4516 0.3069 0.3366 0.3344 0.4889 0.3561 0.3686Observations 5.76 14.68 12.19 13.05 6.10 16.54 13.39 14.18Industry Fixed-Effects 65 65 65 65 53 53 53 53Country Fixed-Effects 1562 1562 1562 1562 1317 1317 1317 1317

All countries Dropping Low Income Countries

Theoretical Framework – Estimation – Data - Results

76

Endogeneity of Financial Development and Measurement Error in US-based proxy of opportunities

Instrumental Variable Technique IV FULL IV(1) FULL IV(2)(1) (2) (3)

SHARE80i,c -0.1906 -0.1918 -0.1914(3.75) (3.76) (3.76)

Finance X Investment Opportunities 0.5194 0.8166 0.7263[PRIVCR X CAPGR ] (3.53) (2.74) (2.98)

centered R-squared 0.3388 0.3305 0.3339F-score 12.44 12.25 12.67Countries 66 66 66Observations 1589 1589 1589Industry Fixed-Effects Yes Yes YesCountry Fixed-Effects Yes Yes Yes

Theoretical Framework – Estimation – Data - Results

77

Conclusion

-- Greater financial development translates into faster growth of industries with good investment opportunities

-- This effect strengthens when mis-measurement of global investment opportunities is taken into account