Truth in Lending Act Origination Claims Pre- and...

33

©National Consumer Law Center 2015 Truth in Lending Act Origination Claims Pre- and Post-Dodd Frank Empire Justice Training April 15, 2015 Alys Cohen Staff Attorney, National Consumer Law Center This session will provide an overview of TILA origination claims, focusing on post- Dodd-Frank but also pointing out some pre-Dodd-Frank angles. • General Ability to Repay Standard • Qualified Mortgages • Steering/Loan originator compensation • Higher Priced Mortgage Loan (HPML) • HOEPA/ “high-cost” loans • Disclosure 2

Transcript of Truth in Lending Act Origination Claims Pre- and...

©National Consumer Law Center 2015

Truth in Lending Act Origination ClaimsPre- and Post-Dodd Frank

Empire Justice Training April 15, 2015

Alys CohenStaff Attorney, National Consumer Law Center

This session will provide an overview of TILA origination claims, focusing on post-Dodd-Frank but also pointing out some pre-Dodd-Frank angles. • General Ability to Repay Standard

• Qualified Mortgages

• Steering/Loan originator compensation

• Higher Priced Mortgage Loan (HPML)

• HOEPA/ “high-cost” loans

• Disclosure

2

Statutes & regulations applicable to mortgage originations 2008-Forward• Truth in Lending (TILA)

– Home Ownership Equity Protection Act (HOEPA)– Higher cost mortgage loan rule (HPML)

• Escrow, Appraisal, Prepay. Penalties, Ability to Repay– Loan originator compensation rule (FRB and

Dodd-Frank LO Comp)– Mortgage disclosure improvement act (MDIA)– Dodd-Frank - Ability to repay (builds on HOEPA and

HPML)

• Real Estate Settlement Procedures Act (RESPA)-GFE/HUD-1, kickback prohibition

• Appraisal rules (TILA HPML, Independence, ECOA) 3

POLL

• Have you represented any homeowners in mortgage cases that included Truth in Lending claims, such as disclosure, high-cost (HOEPA), or higher-priced mortgage loans?

• YES

• NO

6

TILA basics--coverage

• Truth in Lending Act, 15 USC §1601 et seq(TILA) applies to loans: – By a creditor (see 15 USC §1602(f) for

details); Regulation Z, § 1026.3 (a)(17)* – To a consumer, 15 USC §1602(i)– Primarily for personal, family or

household purposes Id.

* The Consumer Financial Protection Bureau (CFPB) reissued and renumbered Regulation Z from 12 CFR Part 226 to 12 CFR Part 1026

TILA basics--contents

• Disclosure– Early and closing disclosures– HOEPA disclosures– Combines TILA/RESPA disclosure

• Substantive Rights– HOEPA– HPML– Dodd-Frank Ability to Repay/QM, and more– Escrow and Appraisal

• Remedies-which apply?– Actual, statutory and enhanced damages– Rescission– Attorneys fees

TILA disclosure basics for home secured mortgage loans

• TILA disclosure re: cost of credit: – Clear & conspicuous information– Accurate, timely and properly delivered– Material disclosures & notice of right to cancel

(NRTC)• Remedies:

– Rescission for material disclosure & NRTCviolations (if the loan is secured by the consumer’s principal dwelling & not a purchase loan)

– Statutory damages, actual damages, attorney fees

HOEPA coverage

• HOEPA applies to principal dwelling secured loans that are “high-cost” based on “triggers”

• Pre-1/10/14 closed-end, non-purchase only

• 1/10/14 – adds purchase & HELOCs (not construction, not reverse mortgage)

• Creditor = originates 2 HOEPA loans in any 12 month period, OR originates ONE HOEPA loan through a mortgage broker.

HOEPA triggers• Pre-1/10/14--2 triggers--APR and points &

fees—226.32/1026.32 – APR > comp Treas + 8 (1st lien) or +10 (sub. lien)

– P&F > 8%

• On/after 1/10/14--3 triggers—APR, points & fees, & prepayment penalty--§1026.32– APR > APOR + 6.5 (1st lien) or + 8.5

(subordinate lien or 1st lien personal property < $50K)

– P&F > 5% for loans of $20K or more; lesser of 8% or $1000 for loans under $20K

– Prepayment penalty > 2% or after 36 mos.

HOEPA violations = rescission & enhanced damages/material disclosures & prohibited

terms• Pre- and Post- D-F (1026.31, 1026.32)

– Special advance disclosure requirements– Prohibited loan terms – incl. negative amortization,

increased interest on default, prepaid escrows

• Pre-D-F prohibited loan terms (1026.32):– Certain prepayment penalty & due on demand

clauses – No short term balloon loans— < 5 year term

• Post D-F prohibited loan terms (1026.32):– NO prepayment penalties (ppp), NO balloon loans– Certain due on demand clauses

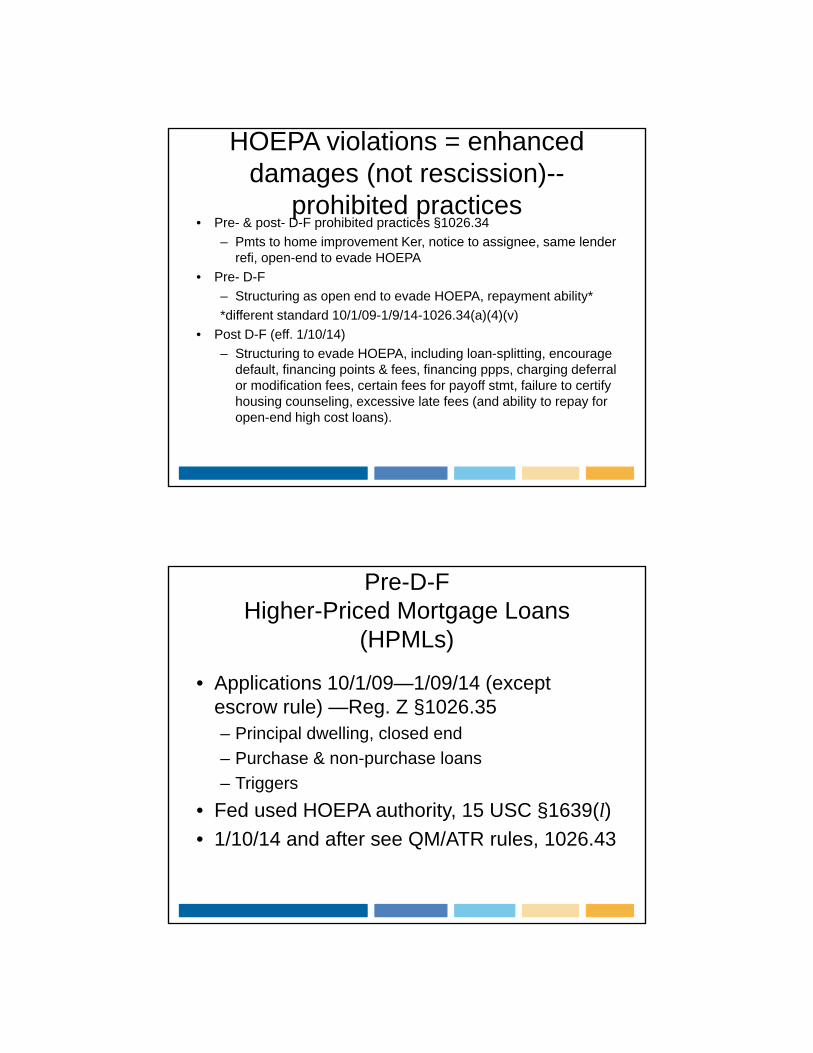

HOEPA violations = enhanced damages (not rescission)--

prohibited practices• Pre- & post- D-F prohibited practices §1026.34

– Pmts to home improvement Ker, notice to assignee, same lender refi, open-end to evade HOEPA

• Pre- D-F

– Structuring as open end to evade HOEPA, repayment ability*

*different standard 10/1/09-1/9/14-1026.34(a)(4)(v)

• Post D-F (eff. 1/10/14)

– Structuring to evade HOEPA, including loan-splitting, encourage default, financing points & fees, financing ppps, charging deferral or modification fees, certain fees for payoff stmt, failure to certify housing counseling, excessive late fees (and ability to repay for open-end high cost loans).

Pre-D-FHigher-Priced Mortgage Loans

(HPMLs)

• Applications 10/1/09—1/09/14 (except escrow rule) —Reg. Z §1026.35 – Principal dwelling, closed end

– Purchase & non-purchase loans

– Triggers

• Fed used HOEPA authority, 15 USC §1639(l)

• 1/10/14 and after see QM/ATR rules, 1026.43

Higher Priced Mortgage Loan

• What’s APOR?– The Average Prime Offer Rate

– APOR is published by the FFIEC on behalf of the FRB.

– http://www.ffiec.gov and choose Rate Spread Calculator from Consumer Compliance menu on homepage.

– http://www.ffiec.gov/ratespread/newcalc.aspx.

15

Pre- D-F HPMLs (cont’d)

• APR triggers use Average Prime Offer Rate (APOR) published by CFPB, §1026.35(a)(2)

• HPML = APR > APOR + 1.5 (1st lien);• > APOR + 3.5 (subordinate

lien).• Prohibited practices/loan terms:

– No repayment ability & ppp (sunset 1/9/14)– Using open-end to evade

• Enhanced damages & rescission for ppp

Pre-D-F HPML Escrow Requirement

• Escrow rule applies to 1st lien mortgages only: – Generally for applications from 4/1/10

– For manufactured homes effective 10/1/10

• Requires creditor to establish escrow for taxes & insurance

Compare Pre and Post D-F escrow rule for HPMLs

• Pre-D-F 226.35(b)(3)–mandatory escrow, consumer may cancel after 365 days– In general 4/1/10– Manufactured 10/1/10

D-F HPML Appraisal rules

• 1026.35—eff. 1/18/14 (Manufactured housing (MH) exempt until 7/18/15)

Appraisal independence/no coercion

• •Pre-D-F, 226.36(b)—for applications from 10/1/09-3/31/11—closed-end, principal dwelling

• •Rule implementing Dodd-Frank, 226.42 for applications starting on 4/1/11—all principal dwelling, including HELOC

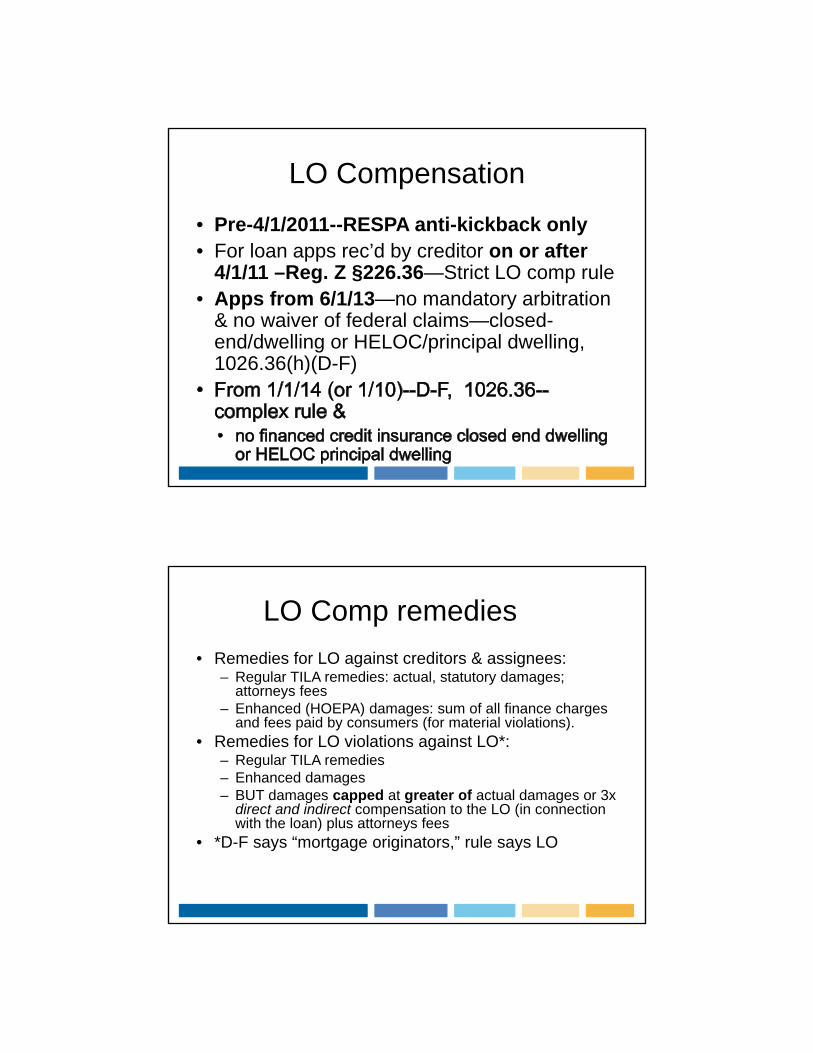

LO Compensation

• Pre-4/1/2011--RESPA anti-kickback only• For loan apps rec’d by creditor on or after

4/1/11 –Reg. Z §226.36—Strict LO comp rule • Apps from 6/1/13—no mandatory arbitration

& no waiver of federal claims—closed-end/dwelling or HELOC/principal dwelling, 1026.36(h)(D-F)

LO Comp remedies

• Remedies for LO against creditors & assignees:– Regular TILA remedies: actual, statutory damages;

attorneys fees– Enhanced (HOEPA) damages: sum of all finance charges

and fees paid by consumers (for material violations).• Remedies for LO violations against LO*:

– Regular TILA remedies– Enhanced damages – BUT damages capped at greater of actual damages or 3x

direct and indirect compensation to the LO (in connection with the loan) plus attorneys fees

• *D-F says “mortgage originators,” rule says LO

Timing of TILA Disclosures/ Advance disclosure Requirements

• MDIA early TILA disclosure requirements eff. 7/30/09 (closed end dwelling secured)– w/in 3 bus. days of application and at least 7 bus.

days before closing—Reg. Z §1026.19– Corrected redisclosure at least three business days

before closing

Format of TILA disclosures

• Classic Fed box & payment scheduler• Eff. 1/30/11 –Reg. Z §1026.18(s)--changed

format for TILA disclosures

State unfair deceptive acts and practices laws

• State UDAP, Unfair Trade Practices Acts (UTPA), Unfair competition laws (UCL)

• May be used to enforce a variety of federal laws

• Violation is a deceptive act, etc under state law for federal laws – Without a private right of action—e.g. RESPA

violations of GFE and HUD-1– To extend SOL

POLL

• Have you had clients come in with loans made in the last five years that were unaffordable when first provided to them?

• YES

• NO

26

Ability to Repay after Dodd-Frank(including for HPML & HOEPA)

• Effective 1/10/14, 15 USC 1639c and 12 CFR 1026.43

• Coverage: closed-end dwelling secured loans including manufactured housing• Does not include: HELOCs, time shares, reverse mortgages or bridge

or construction loans• Exemption for certain non-profit and government-supported lenders

(1026.43(a)(3)(iv)&(v).

• Gen’l rule—reasonable, good faith determination of ability to repay,

– Based upon verified and documented income, assets, debt

• BUT special rule for Qualified Mortgage (QM)—presumptively safer loan products

– Safe harbor/conclusively compliant for prime loans (even if in fact unaffordable)

– Rebuttable presumption for HPML & HOEPA loans

• Remedies: actual, statutory, enhanced damages+fees

27

Ability to Repay and QM: First Questions

• Where to start—Did the lender make a reasonable and good faith determination that the loan was affordable to the consumer at the time of the transaction

• Can show not reasonable or not good faith

• Based on common underwriting factors (discovery)

• Difficult claims—do your homework first.

28

Ability to Repay and QM: First Questions

• Questions:– Reasonable and good faith determination?

– If the loan was an ARM or subject to reset, did lender reasonably conclude reset payments were affordable based on financial picture at closing?

– Did consumer share information with lender that should have alerted lender to affordability problem?

• Imminent retirement, expected job loss, ongoing high medical bills, etc.?

29

Ability to Repay and QM: First Questions

• YES TO ALLLook elsewhere for solutions (does this person need a modification?).

• NOWhat is the timing/circumstances of the delinquency?– Shortly after closing? (within 6-12 months)

– Shortly after reset?

– Shortly after known event? (retirement, job loss)

30

Ability to Repay and QM: First Questions

• If delinquency was delayed, what are mitigating factors?– Used funds from previous refi cashout?

– Overdrafted accounts/cards to pay mortgage until sources ran out?

– Borrowed from family/friends?

31

Ability to repay and QM: Building your Case

• Identify which set of ATR and QM rules applies• Determine if this is a QM or non QM loan• If QM, safe harbor or rebuttable presumption?• If QM rebuttable presumption loan, can you rebut

the presumption?• If non-QM, what are general ATR requirements?• Note: only QMs have presumption of affordability;

non-QMs do NOT.• Alternatives include UDAP, unconscionability,

bankruptcy, etc.

32

Building your Case: Which set of QM rules applies?

• Investor type– Gov’t insured or guaranteed?

– GSE loan?

– Private label security or portfolio loan?

• Lender type—small creditor?

• Product type—sm cr balloon? Ppp? Refi of nonstandard loan?

33

Building your case: Determine if this is a QM loan

• Private label/general QM rules:– Loan terms (these are common to all QMs):

• No neg am or interest only• Points and fees maximum of 3% (but loans under

$100K have separate caps)• Loan term of no more than 30 years

– Underwriting payments: maximum rate for first 5 years after first payment based on fully amortizing schedule

– No more than 43% DTI (Appendix Q, which formally applies only to QM analysis but may have other applications)

34

Building your case: Determine if this is a QM loan

• Appendix Q for checking the 43% DTI is very detailed. Guidelines include:– Seasonal and self-employment– Reliance on bonuses/overtime for income– Alimony, child support, maintenance income– Rental income– Projected income (verified and within 60 days)

and obligations (only if begins within 12 mos)– Exclusions from “debt” include open accounts

with zero balance

35

Building your case: Determine if this is a QM loan

• GSE or Agency “Temporary QM” §1026.43(e)(4)– Common loan term restrictions on neg am, IO,

balloons, 30-year term and pts and fees.– Plus eligible for purchase or guarantee by GSEs,

to be insured by FHA, guaranteed by VA, guaranteed by USDA or insured by RHS

– Sunset: expires earlier of 1/10/2021 or agency regulation defining QM or if conservatorship ends

– HUD’s FHA QM effective 1/10/14.– New leverage to enforce GSE/agency

underwriting rules

36

Building your case: Determine if this is a QM loan

• How to establish eligibility for purchase, guarantee or insurance: (Commentary 43(e)(4)-4– Valid “approve/eligible” from GSE automated

underwriting program, and compliance with any conditions

– Compliance with GSE or agency guidelines– Written agreement between GSE or agency

and creditor– Individual loan waivers from GSE or agency

37

Building your case: Determine if this is a QM loan

• Small Creditor QM

– Part 1: Definition of small creditor• Assets less than $2 billion(not including affiliates)

AND

• Creditor and affiliates combined originated no more than 500 first-lien, closed-end residential mortgages subject to ATR in prior calendar year (not including subordinate liens or mortgages excluded from ATR)

38

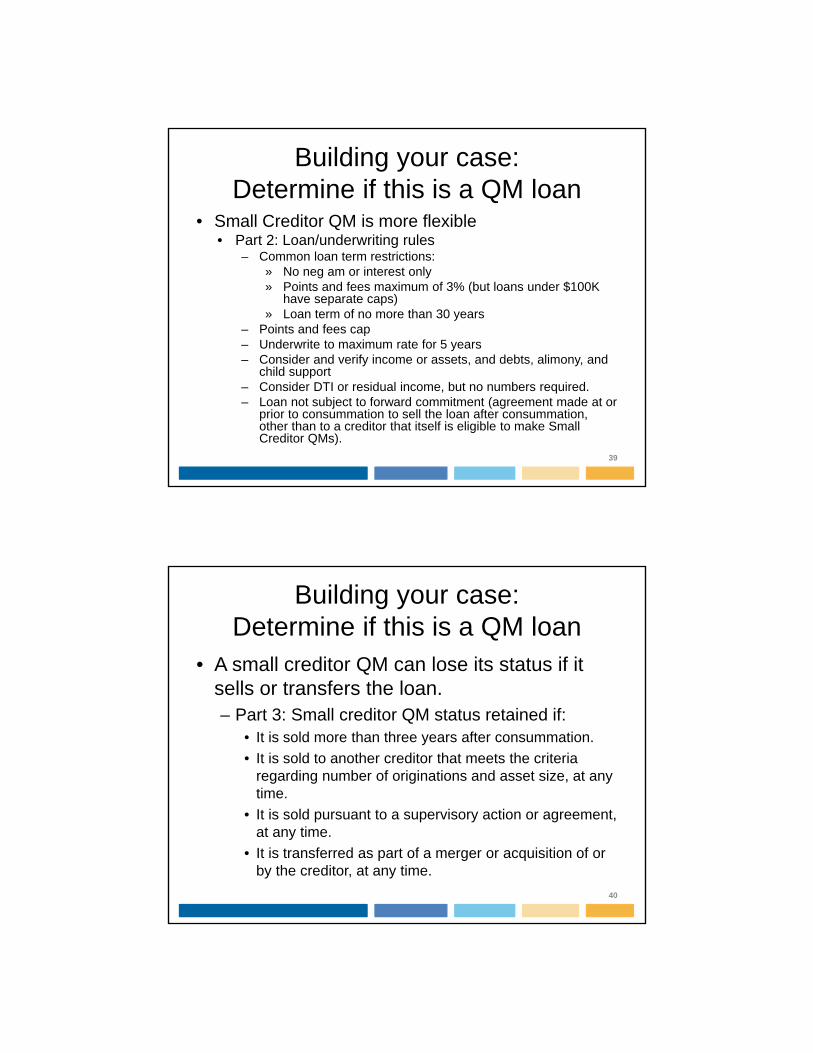

Building your case: Determine if this is a QM loan

• Small Creditor QM is more flexible• Part 2: Loan/underwriting rules

– Common loan term restrictions:» No neg am or interest only» Points and fees maximum of 3% (but loans under $100K

have separate caps)» Loan term of no more than 30 years

– Points and fees cap– Underwrite to maximum rate for 5 years– Consider and verify income or assets, and debts, alimony, and

child support– Consider DTI or residual income, but no numbers required. – Loan not subject to forward commitment (agreement made at or

prior to consummation to sell the loan after consummation, other than to a creditor that itself is eligible to make Small Creditor QMs).

39

Building your case: Determine if this is a QM loan

• A small creditor QM can lose its status if it sells or transfers the loan.– Part 3: Small creditor QM status retained if:

• It is sold more than three years after consummation.

• It is sold to another creditor that meets the criteria regarding number of originations and asset size, at any time.

• It is sold pursuant to a supervisory action or agreement, at any time.

• It is transferred as part of a merger or acquisition of or by the creditor, at any time.

40

Building your case: Determine if this is a QM loan

• Small Creditor Balloon QM– Creditor requirements—

• Until 1/9/2016 all small creditors • After 1/10/16 only small creditors operating predominantly in rural and

underserved areas (special definition)– Loan criteria

• No neg am or IO• Points and fees cap• 30 years amortization and fixed interest payments (other than balloon)• Loan term of at least 5 years• Held in portfolio (not subject to forward commitment)• Determine affordability of regular periodic payments OTHER THAN

balloon (contrast with balloon ATR rule)• Consider and verify income/assets/debts• Consider DTI or residual income (but no number required)

– Same restrictions on sale or transfer as small cred QM

41

Building your case: Determine if this is a QM loan

• QMs with PPPs– Only on fixed rate or step rate loans

– Not on higher-priced QM loans

– Otherwise permitted by applicable (state) law

– If maximum ppp pushes loan above points and fees threshold then not QM

– No PPP after first 3 years of loan

42

Building your case: Determine if this is a QM loan

• More on PPP QMs– PPP definition does not include certain bona

fide third party fees if waived at closing (in exchange for earning through interest rate), even if must be repaid upon prepayment in first three years

– Maximum PPP is 2% of UPB for year 1 and 2 and 1% for year 3.

– Must also have offered similar loan without PPP (bait and switch opportunity?)

43

Building your case: Determine if this is a QM loan

• What does the offer of a similar loan without PPP have to look like?– Consumer must also qualify for other option offered.– No PPP– Fixed rate or step-rate with same rate type– Same term as PPP loan – No deferred principal, balloon or interest-only payments, or

negative amortization • If creditor is brokering or table-funding, then additional

requirements if offer also used to comply with anti-steering rules for loan originators under § 1026.36(e):– loan with the lowest interest rate overall; – loan with the lowest interest rate with a PPP; and – the loan with the lowest total origination points or fee and

discount points

44

Certain Refis are Exempt from ATR/QM §1026.43(d)

• ATR/QM does not apply to refinancing of “non-standard” mortgage by creditor holding or servicing the non-standard mortgage.

• Not available to subservicers or third parties.• Meant to help avoid impending payment

shock.• FHA Streamline Refi subject to FHA QM• Modifications already exempt because not

new credit.

45

Certain Refis are Exempt from ATR/QM §1026.43(d)

• Eligible non-standard loans:– ARM fixed for at least one year; IO or Neg Am– Current on loan

• Maximum 1 30-day late in 12 months; no lates in prior 6 mos. (See details in Commentary)

– Written app. no later than 2 mos. after recast– New loan likely to prevent default on non-

standard loan after recast – Non-standard loan made after 1/10/14 must

comply with ATR/QM.

46

Certain Refis are Exempt from ATR/QM §1026.43(d)

• Standard loan requirements– No increase in principal balance– No cash out (except closing costs and escrow)– Monthly payment after recast materially lower--

reduced by more than 10% (not necessarily affordable long-term)

– No IO, neg am or balloon– Meets points and fees cap for QM– Loan term not greater than 40 years– Fixed rate for first 5 years

47

POLL

What proportion of your foreclosure cases (without regard to origination date) is attributable to ability to repay issues (vs. job loss, medical, divorce, etc.)?

0-5%

10-25%

25-50%

50-75%

75-100% 48

What’s Next if it is a QM?

• Qualified Mortgages have two levels of presumption:– Conclusive presumption/safe harbor IF QM

– Rebuttable presumption for “higher-priced” mortgages

A word about this dichotomy

49

50

BACK TO QM REBUTTABLE PRESUMPTION FOR HPML’S

51

Rebutting the QM Presumption

• Rebut by showing that a) income, debts, alimony, child support and PITI (including simultaneous loans of which creditor was aware) b) leave consumer with insufficient residual income or assets other than equity c)for meeting living expenses, d) including any recurring and material non-debt obligations of which the creditor was aware at consummation

52

QM or non QM

• Non-compliance with QM standard may be easier to show than rebutting QM presumption

• Unclear how courts will interpret standard for rebuttal

• And many loans get the safe harbor (despite lack of Congressional intent)

• General ATR standard has more prongs to challenge than the rebuttal

53

Not a QM: General ATR

• All loans must comply with the general Ability to Repay (ATR) requirements. A reasonable, good-faith ATR evaluation must include eight underwriting factors: 1. Current or reasonably expected income or assets (other than value of secured property) 2. Current employment status (if employment income used to assess ability to repay) 3. Monthly mortgage payment—fully indexed rate for ARMs (but may use lifetime max rate); max rate for fixed and step-rate loans; special rules for IO, neg am and balloon loans 4. Monthly payment on any simultaneous loans secured by the same property about which creditor knows or has reason to know

54

Non-QM: General ATR

5. Taxes and insurance required by creditor, plus association fees/ground

6. Debts, alimony and child support obligations(Appendix Q??)

7. Monthly back-end debt-to-income ratio (based on mortgage payment(s), current debts, alimony, and child support) or residual income (remaining income after subtracting total monthly debts from total monthly income). May consider both and may use compensating factors (and residual income may be a comp. factor).

8. Credit history

55

Non-QM Loans: General ATR

• Special monthly payment calculations include:– Balloons: maximum payment first five years

except use maximum payment in life of loan if loan is HPML

– Neg Am: assume amortizing payments after recast and assume recast is based on minimum payments prior to recast with interest rate rising as quickly as possible after consummation (note this is not worst case scenario because repayment has more time since interest is assumed to increase quickly)

56

Non-QM: General ATR

• Creditor must verify information, including income and assets, using “reasonably reliable third-party records”

– Employment status can be orally verified.

– Credit lines not reflected on a credit report used as a source need not be further verified.

– Third party sources can include: tax return or transcript, W-2s, payroll statements, bank records, employer records or third party with employer information, public benefit documentation , check cashing receipts, funds transfer receipts.

– Records can be obtained from the consumer

57

Non-QM Loans: General ATR

• Comment 43(c)(2)(i)-1• Any current or reasonably expected income for

ATR analysis includes:– Salary/wages/self-empl. Income– Military/reserve duty income– Bonuses/tips/commissions– Interest/dividends/retirement benefits or entitlements– Rental income– Royalties/trust income– Public assistance– Alimony/child support/maintenance

58

Non-QM Loans: General ATR

• Comment 43(c)(2)(vi)-1&2

• Consider current debt of ALL applicants

• Examples of current debt include– Student/car loans

– Credit cards/revolving debt

– Existing mortgages not paid off at consummation (unless contract for sale)

– Debt where forbearance or deferral expires soon (but remember 12 month rule from App. Q)

59

Non-QM Loans: General ATR

• Credit History, Comment 43(c)(2)(viii) No minimum score or specific take on how to evaluate credit history– Creditor may use rental or utility payment history where

traditional credit history is scarce (note problems with this)– Consider credit history of all applicants

• Credit report as reasonably reliable third-party record: sufficient but not where creditor knows or has reason to know it is inaccurate in whole or in part.– Fraud or similar alert; statement of dispute; other record

that contradicts– Inaccuratecan disregard without additional records but

OK to get additional records

60

No waiver of ATR claims

• Comment 1026.43(c)(1)-1(i)

– “A consumer’s statement or attestation that the consumer has the ability to repay the loan is not indicative of whether the creditor’s determination was reasonable and in good faith.”

61

ATR analysis is individual

• Comment 1026.43(c)(1)-1(i)

– Question of whether ATR determination is reasonable and in good faith “depends not only on the underwriting standards adopted by the creditor, but on the facts and circumstances of an individual extension of credit and how a creditor’s underwriting standards were applied to those facts and circumstances.”

62

Evidence that ATR determination not reasonable/good faith

• Comment 1026.43(c)(1)(ii)(B): Evidence, but not elements of a claim. 1. Default shortly after consummation or recast2. Use of underwriting standards that have historically resulted in relatively high delinquency and default rates in adverse economic conditions3. Underwriting standards applied inconsistently or used standard different from those of similar loans without reasonable justification4. Disregard of evidence that underwriting standards not effective at determining ATR5. Disregard of evidence of insufficient residual income6. Disregard of evidence that ATR relies on refinance of loan or sale of secured property(These are not requirements or prohibitions, nor elements of a claim)

63

Evidence of ATR: Facts on Continuum

• Comment 43(c)(1)-1(ii)(C)• The longer payments were made, the less likely it

is ATR assessment was unreasonable• Inconsistent underwriting could make a difference

or just be bad training with no impact• Early payment default “may even be sufficient to

establish a prima facie case” but may be caused by subsequent change of circumstances.

• Lack of early default may not preclude ATR claim if early payments were made by foregoing necessities such as food and heat

64

Contact information

• Alys Cohen, Staff Attorney

• National Consumer Law Center

• 1001 Connecticut Ave., N.W.

• Washington, D.C. 20036

• direct dial ~ (202) 595-7852

• main phone ~ (202) 452-6252 x 102

• email ~ [email protected]

• www.nclc.org65