Trends In Automotive Exhaust Aftertreatment And Their ... · PGM ratios in the various types of...

14

LBMA/LPPM Precious Metals Conference 2012 12 November 2012 Session 4 – Rohr 1 Trends In Automotive Exhaust Aftertreatment And Their Impact On Future PGM Demand Dr. Friedemann Rohr Hongkong, November 12 th , 2012 Automotive Catalyst Basics Megatrends in Aftertreatment Legislation Roadmap Technology Roadmap Implications For PGM Demand Agenda

Transcript of Trends In Automotive Exhaust Aftertreatment And Their ... · PGM ratios in the various types of...

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 1

Trends In Automotive Exhaust

Aftertreatment And Their Impact On

Future PGM Demand

Dr. Friedemann Rohr

Hongkong, November 12th, 2012

Automotive Catalyst Basics

Megatrends in Aftertreatment

Legislation Roadmap

Technology Roadmap

Implications For PGM Demand

Agenda

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 2

Title and date 3

Automotive Catalysis – Basic Concepts

Title and date 4

Catalyst Architecture

precious metal

200

µm

100

: 1

oxide components

substrates

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 3

Title and date 5

Main Chemical Pathways Catalyzed By An

Automotive Aftertreatment System

NO, NO2 N2

CO CO2

Hydrocarbons CO2, H2O

Particulate matter

(mainly carbon)

CO2

Title and date 6

Megatrends In Automotive Catalysis

Shifting focus from pollution control to CO2 reduction in mature markets.

Non OECD, BRIC countries catching up fast with OECD aftertreatment

legislation.

Aftertreatment moving into new markets (heavy duty diesel, on road and non

road).

Electrification is a megatrend but has no significant impact on the PGM

demand from the automotive catalyst sector in coming years.

Heightened focus on raw material supply security, recycling.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 4

Title and date 7

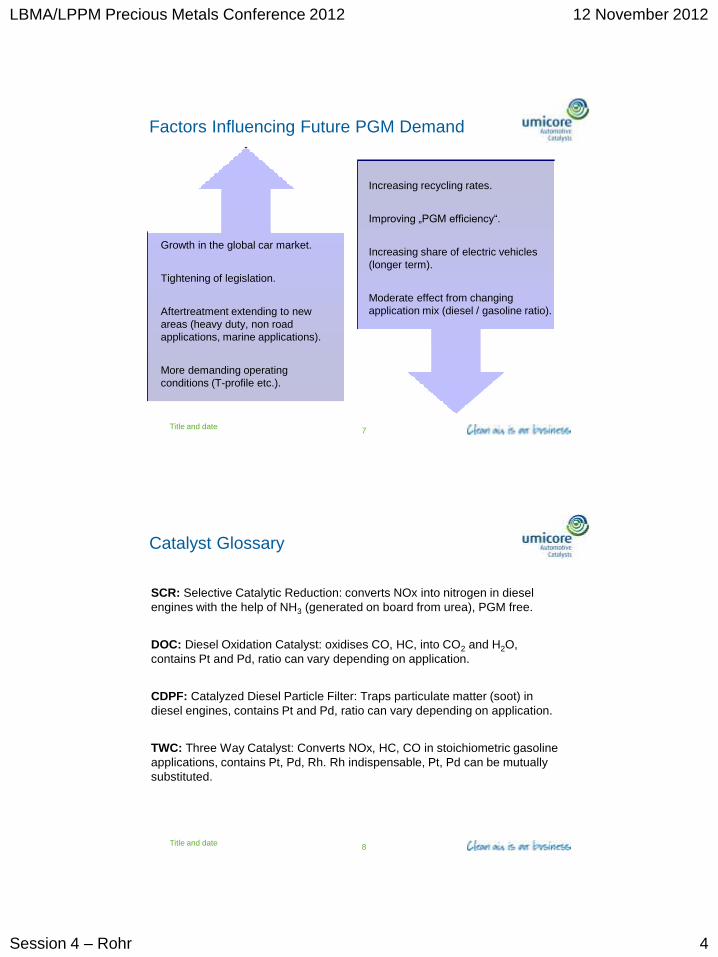

Factors Influencing Future PGM Demand

Growth in the global car market.

Tightening of legislation.

Aftertreatment extending to new

areas (heavy duty, non road

applications, marine applications).

More demanding operating

conditions (T-profile etc.).

Increasing recycling rates.

Improving „PGM efficiency“.

Increasing share of electric vehicles

(longer term).

Moderate effect from changing

application mix (diesel / gasoline ratio).

Title and date 8

Catalyst Glossary

SCR: Selective Catalytic Reduction: converts NOx into nitrogen in diesel

engines with the help of NH3 (generated on board from urea), PGM free.

DOC: Diesel Oxidation Catalyst: oxidises CO, HC, into CO2 and H2O,

contains Pt and Pd, ratio can vary depending on application.

CDPF: Catalyzed Diesel Particle Filter: Traps particulate matter (soot) in

diesel engines, contains Pt and Pd, ratio can vary depending on application.

TWC: Three Way Catalyst: Converts NOx, HC, CO in stoichiometric gasoline

applications, contains Pt, Pd, Rh. Rh indispensable, Pt, Pd can be mutually

substituted.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 5

Title and date 9

Catalyst Glossary

LNT: Lean NOx Trap: Converts NOx, HC, CO in lean burn applications (light

duty diesel and gasoline), contains Pt, Pd, Rh. Rh and Pt indispensable,

some Pt can be substituted by Pd.

Title and date 10

Application Mix And PGM Content

Lean Burn Applications ( >1)

DOC

Pt, Pd

SCR

PGM-free

LNT

Pt, Pd, Rh

Stoichiometric Applications ( =1)

CDPF

Pt, Pd

TWC

Pd, (Pt), Rh

TWC

Pd, (Pt), Rh

Gasoline

Diesel

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 6

Title and date 11

PGM Flexibility

PGM ratios in the various types of catalysts can be adjusted to some extent

as PGM price differentials change.

In TWC, Pt and Pd are mutually interchangeable, shift from Pd to Pt as a

response to 2001 price increase for Pd.

Immense pressure in 2008 to reduce Rh in LNT and TWC. Reduction

possible but some amount of Rh is essential.

In DOCs substitution of Pt with Pd is possible to some extent depending on

the application layout and the fuel quality.

Title and date 12

US

$/t

roy o

un

ce

0

500

1000

1500

2000

2500

platinum

palladium

US

$/t

roy o

un

ce

0

2000

4000

6000

8000

10000 rhodium

PGM Price Trends Encourage Mutual

Substitution And Thrifting

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 7

Title and date 13

Gasoline Vehicles Worldwide Market Share

in the Year 2011

Total worldwide car sales of

some 67 million vehicles

excluding heavy duty.

The vast majority of those were

gasoline applications (72%).

Europe is the major contributor

for the diesel segment.

„Others“ include other

propulsion (biofuel, hydrogen,

electricity etc.)

Gasoline

Diesel

Others

Title and date 14

Light Duty Application Mix Going Forward

The passenger car segment is dominated by the stoichiometric gasoline car,

the TWC is the dominant aftertreatment device.

Western Europe and India are the only large diesel passenger car markets.

LDD applications require relatively high PGM loadings and are Pt-rich.

Despite of the diesel’s superior fuel economy there is uncertainty about

growth prospects in the diesel light duty segment:

Costlier aftertreatment systems

Availability of diesel fuel (refinery output, etc.)

Continuing progress in gasoline car’s fuel efficiency

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 8

Title and date 15

Legislation Trends – OECD Countries

Some further tightening of pollutant emissions (e.g.: off cycle emissions,

gasoline particulate filters) but no major step change in PGM demand.

Increasing focus on energy efficiency / CO2.

Heavy duty and non road legislation already in place, next legislation stages

around the corner.

OECD not a major driver for future PGM demand growth per vehicle.

Title and date 16

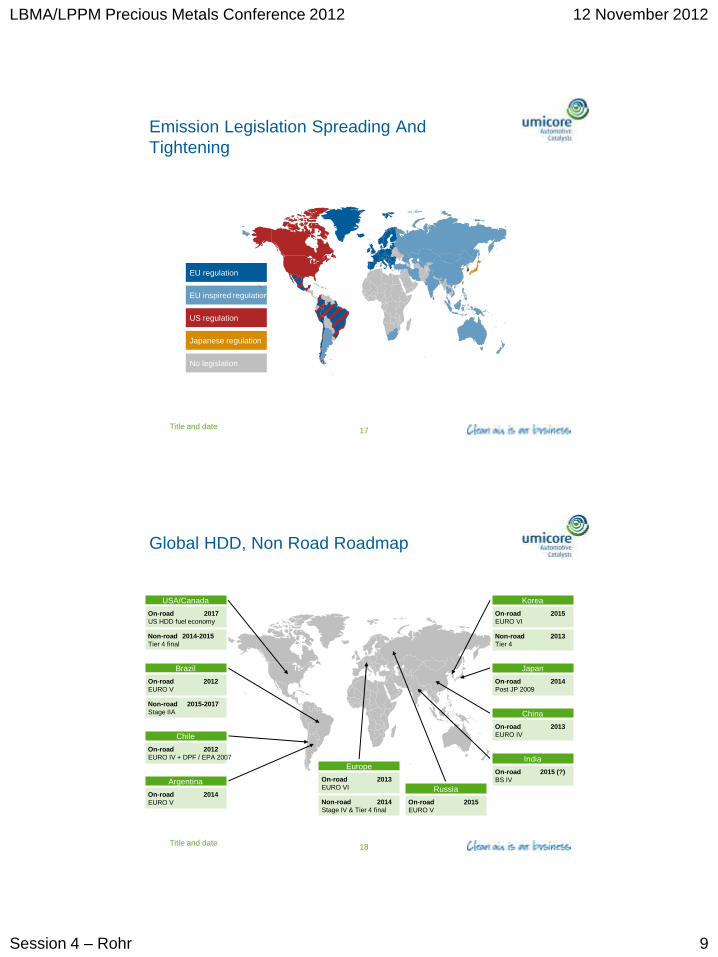

Legislation Trends – Non OECD Countries

Upcoming legislation in major non OECD countries for heavy duty and non

road segment will be the main driver for new PGM demand per vehicle.

China and India will soon implement nationwide heavy duty diesel legislation.

Non road / marine sector less clear, possibly in the 2015 – 2017 timeframe.

Catching up with EU legislation beyond EU4 in the gasoline segment will

probably not lead to a significant increase in PGM demand per vehicle.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 9

Title and date 17

Emission Legislation Spreading And

Tightening

US regulation

EU regulation

Japanese regulation

No legislation

EU inspired regulation

Title and date 18

Global HDD, Non Road Roadmap

USA/Canada

On-road 2017

US HDD fuel economy

Non-road 2014-2015

Tier 4 final

Brazil

On-road 2012

EURO IV + DPF / EPA 2007

Non-road 2015-2017

Stage IIA

On-road 2012

EURO V

Chile

On-road 2014

EURO V

Argentina

Europe

On-road 2013

EURO VI

Non-road 2014

Stage IV & Tier 4 final

On-road 2015

EURO V

Russia

On-road 2015

EURO VI

Korea

Non-road 2013

Tier 4

On-road 2014

Post JP 2009

Japan

On-road 2013

EURO IV

China

On-road 2015 (?)

BS IV

India

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 10

Title and date 19

HDD On Road, Non Road Catalyst Systems

DOC (EU III),

EU IV

Urea injection

DOC Partial

filter

DOC CDPF SCR

EU IV,

EU V,

Tier 4i,

Stage IIIB

EU VI,

Tier 4 final,

Stage IV

Urea injection

DOC (optional)

SCR

Title and date 20

New Market Segments And PGM Demand

The big new growth segments (HDD on road, non road) will require systems

based on DOCs, filters and SCRs.

On aggregate these systems require mainly Pt, especially in markets with

high sulfur fuel content (India, China etc.).

Palladium is viable in EU VI / Stage III / Tier 4 final type systems and some

degree of mutual Pt-Pd substitution is possible depending on application.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 11

Title and date 21

Focus On CO2 – Implications For PGM

Demand

Improving fuel efficiency is fast becoming the most important development focus in the car industry.

Binding CO2 legislation is in place in many markets, substantial future tightening.

Still untapped potential for improving fuel efficiency of gasoline cars (downsizing, turbo charging, VVT, direct injection…)

Impact of these technologies on TWC’s PGM loading unclear but likely not dramatic.

Catalysts’s temperature operating window may become somewhat broader requiring enhanced performance.

Operating conditions might become somewhat harsher requiring more performant catalyst formulations.

Title and date 22

Focus On CO2 - Light Duty Diesel

The diesel engine has higher fuel efficiency than the gasoline engine but light

duty diesel growth faces obstacles.

Diesel cars are more expensive, aftertreatment more complex and costly.

Availability of sufficient diesel can be an issue in some regions.

Fuel price differential in favor of diesel might disappear in some EU countries.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 12

Title and date 23

A Quick Word On PGM Recycling

Increasing recycling rates must be a common goal in the automotive catalyst

industry.

Recycling PGM is much less energy intensive compared to mining it.

Collection network / infrastructure for spent catalysts is vital.

This mechanism is not yet in place in key markets such as China.

Title and date 24

PGM Efficiency

Constant improvement in catalyst formulation has made it possible to do

more with less PGM.

Better engine calibration and engine management technologies can also help

reduce PGM loadings per catalyst.

However moving forward quantum leaps in PGM reduction per catalyst are

unlikely.

Complete substitution of PGM with base metals is an unrealistic prospect.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 13

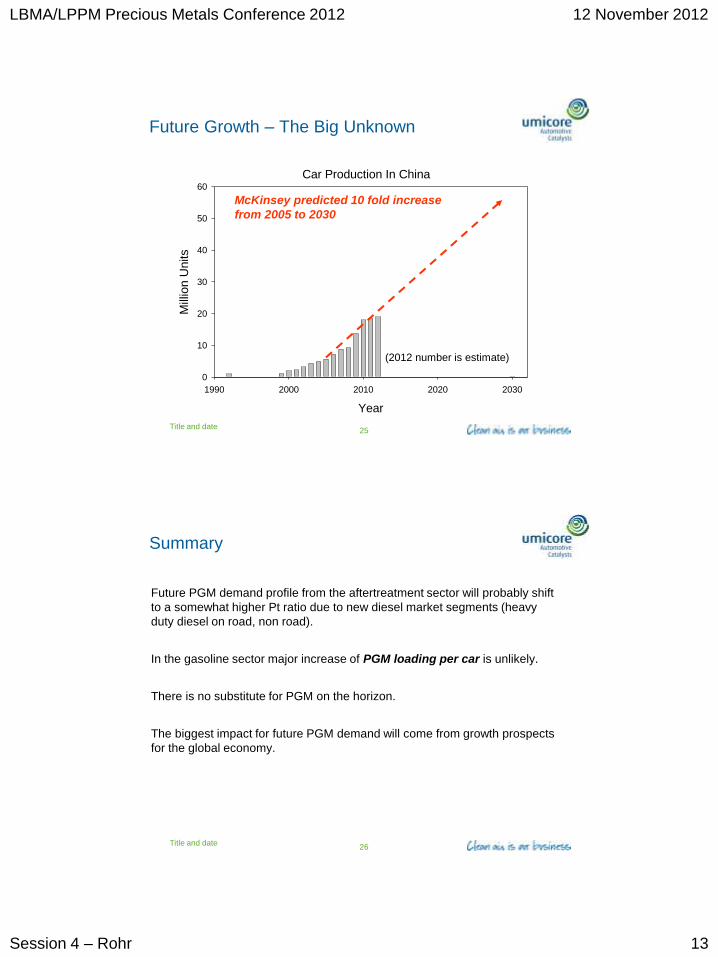

Title and date 25

Car Production In China

Year

1990 2000 2010 2020 2030

Mill

ion U

nits

0

10

20

30

40

50

60

Future Growth – The Big Unknown

McKinsey predicted 10 fold increase

from 2005 to 2030

(2012 number is estimate)

Title and date 26

Summary

Future PGM demand profile from the aftertreatment sector will probably shift

to a somewhat higher Pt ratio due to new diesel market segments (heavy

duty diesel on road, non road).

In the gasoline sector major increase of PGM loading per car is unlikely.

There is no substitute for PGM on the horizon.

The biggest impact for future PGM demand will come from growth prospects

for the global economy.

LBMA/LPPM Precious Metals Conference 2012 12 November 2012

Session 4 – Rohr 14

Thank you for your attention!