Trader's DFA Marc Wildi - Statistician and Economist Kent Hoxsey - Programmer and Trader

32

Trader's DFA Marc Wildi - Statistician and Economist Kent Hoxsey - Programmer and Trader A Practioner's Introduction to the Direct Filter Approach

-

Upload

nina-barlow -

Category

Documents

-

view

42 -

download

0

description

Trader's DFA Marc Wildi - Statistician and Economist Kent Hoxsey - Programmer and Trader. A Practioner's Introduction to the Direct Filter Approach. Signalextraction. Noise Filter Signal. Signal. Eurostoxx50, MA(200) Equal-Weights (Faber 2009). Real-Time Signalextraction. - PowerPoint PPT Presentation

Transcript of Trader's DFA Marc Wildi - Statistician and Economist Kent Hoxsey - Programmer and Trader

Trader's DFA

Marc Wildi - Statistician and EconomistKent Hoxsey - Programmer and Trader

A Practioner's Introductionto the Direct Filter Approach

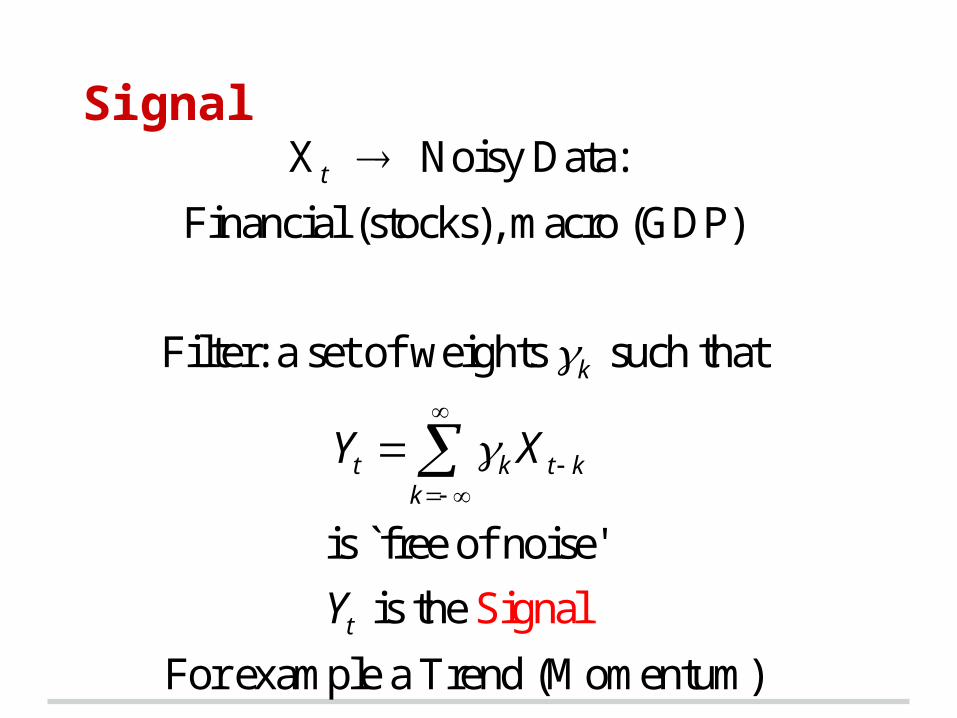

Signalextraction

• Noise

• Filter

• Signal

SignalX Noisy Data:

Financial (stocks), macro (GDP)

Filter: a set of weights such that

is `free of noise'

is Signal the

For example a Trend (Mom

entum)

t

k

t k t kk

t

Y X

Y

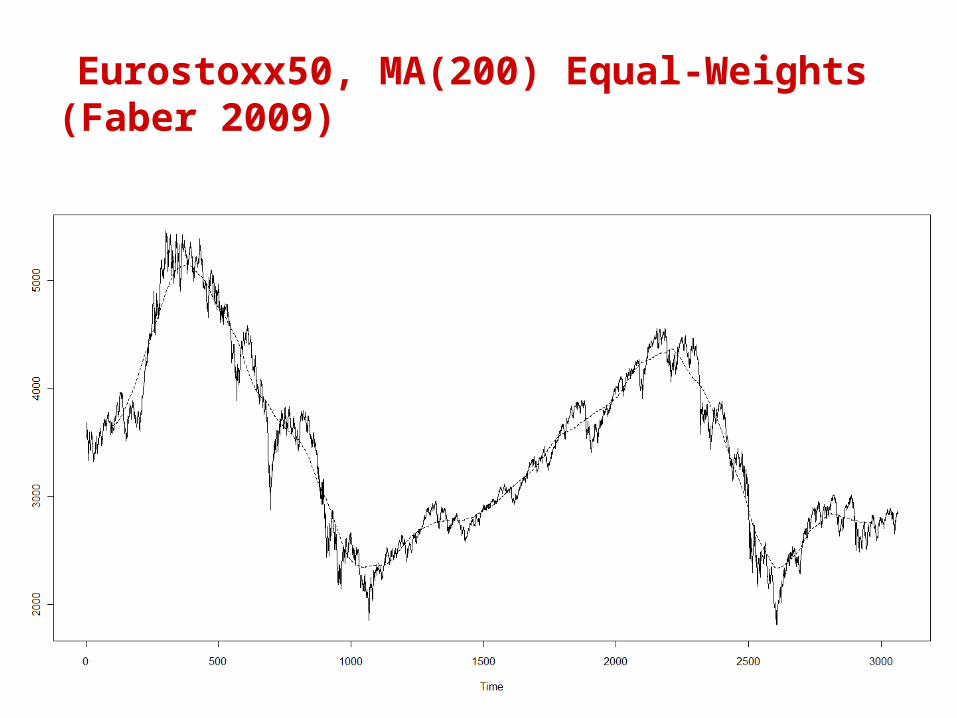

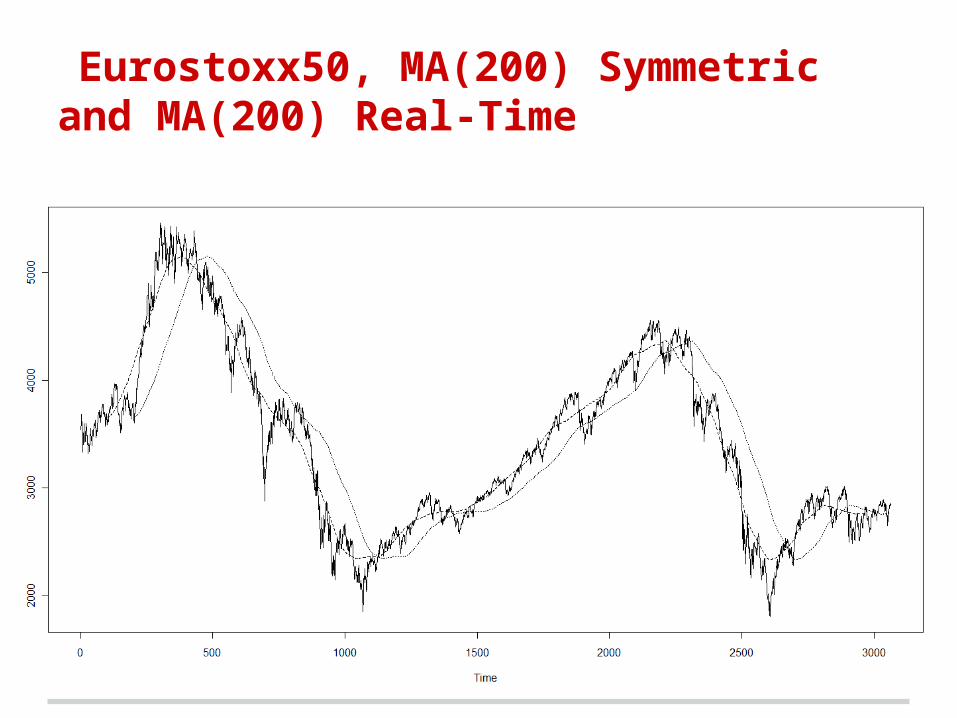

Eurostoxx50, MA(200) Equal-Weights (Faber 2009)

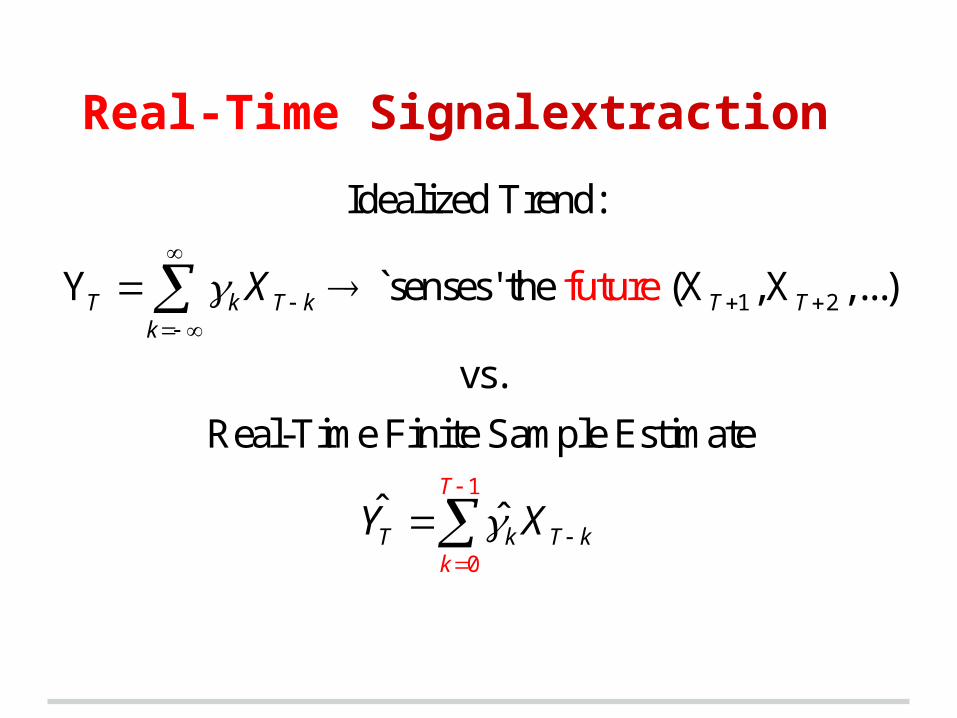

Real-Time Signalextraction

1

1 2

0

future

Idealized Trend:

Y `senses' the (X ,X ,...)

vs.

Real-Time Finite Sample Estima

ˆ ˆ

te

T k T k T Tk

T

kT k T k

X

Y X

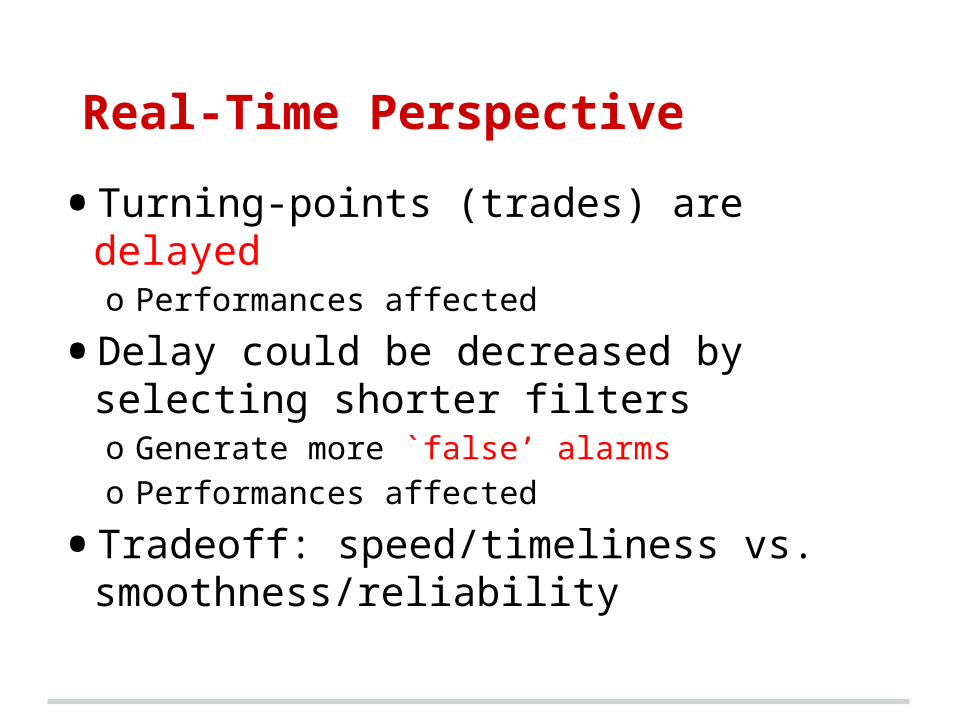

Eurostoxx50, MA(200) Symmetric and MA(200) Real-Time

Real-Time Perspective

• Turning-points (trades) are delayedo Performances affected

• Delay could be decreased by selecting shorter filterso Generate more `false’ alarmso Performances affected

• Tradeoff: speed/timeliness vs. smoothness/reliability

Frequency Domain

• Timeliness

• Reliability

• Both!

Real-Time SignalextractionFrequency Domain

1

0

1

0

Idealized Target: Y

ˆ ˆReal-Time Estimate:

Transferfunctions

( ):= exp( ) ( if symmetric)

ˆ ˆ( ):= exp( )

T k T kk

T k T k

kk

T

k

T

kk

X

Y X

ik

ik

Optimization Criterion: Mean-Square

2ˆFILTERWEIGHTS

2

ˆ

ˆFilter error:

Criterion: E[ ] min

Frequency Domain

ˆˆ( ) ( ) S( ) min

k

t t t

t

k k kk

r Y Y

r

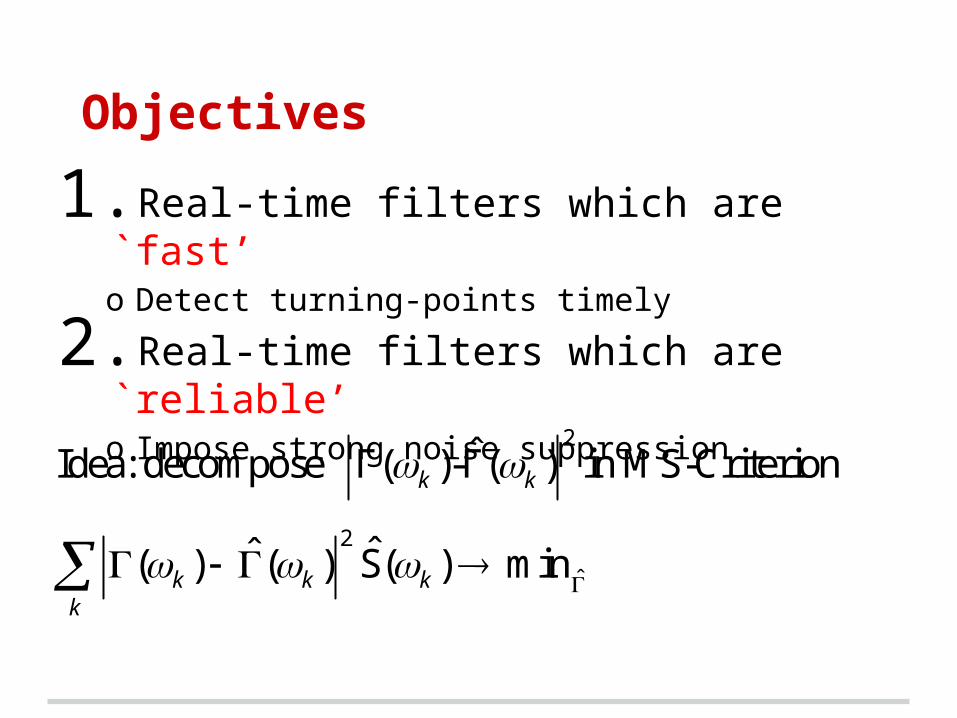

Objectives

1.Real-time filters which are `fast’o Detect turning-points timely

2.Real-time filters which are `reliable’o Impose strong noise suppression

2

2

ˆ

ˆIdea: decompose Γ( )-Γ( ) in MS-Criterion

ˆˆ( ) ( ) S( ) min

k k

k k kk

Cosine Law applied to

ˆ ( )

ˆ( ) ( )

ˆ ( )

( )

2

2

ˆ( ) ( )

ˆ ˆ ˆ( ) ( ) 2 ( ) ( ) 1 cos( ( ))

2ˆ( ) ( )

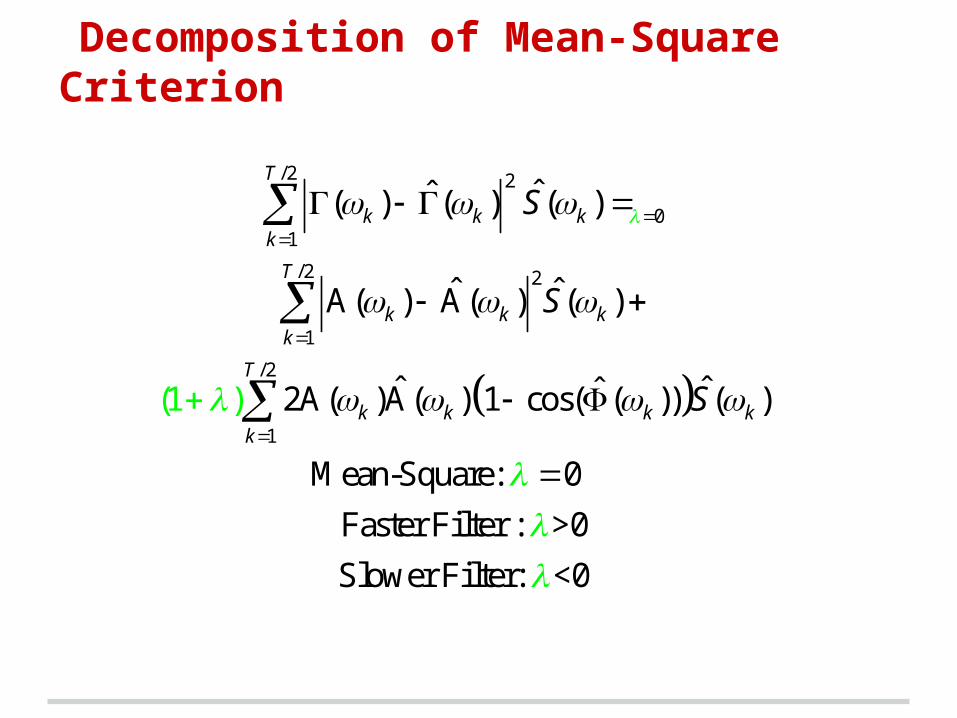

Decomposition of Mean-Square Criterion

/2 2

01

/2 2

1

/2

1

ˆˆ( ) ( ) ( )

ˆ ˆA( ) A( ) ( )

ˆ ˆˆ2A( )A( ) 1 cos( ( )) ( )

Mean-Squ

(

are: 0

Faster Filter : >0

Slower Filter:

1

<0

)

T

k k kk

T

k k kk

T

k k k kk

S

S

S

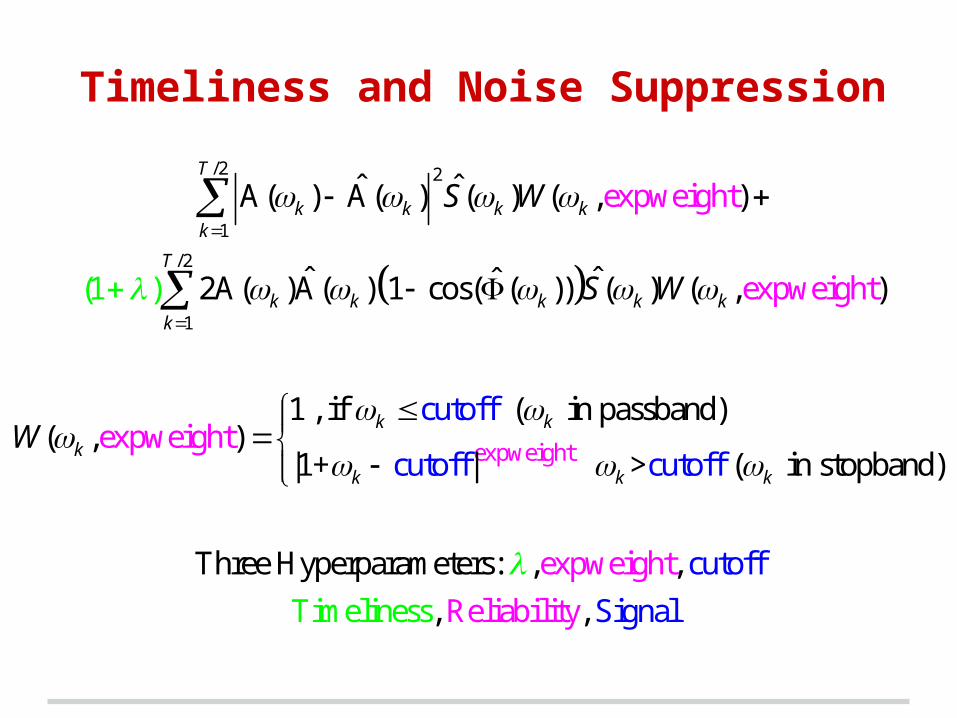

Timeliness and Noise Suppression

/2 2

1

/2

1

expweight

expweight

expw

ˆ ˆA( ) A( ) ( ) ( , )

ˆ ˆˆ2A( )A( ) 1 cos( ( )) ( ) ( , )

1 , if ( in passband)( , )

|1+ | > ( in st

cutoff

cuto opbff cutoff

eight

e

(1

xpweia

ghnd)

)

t

T

k k k kk

T

k k k k kk

k k

k

k k k

S W

S W

W

Three Hyperparameters: , ,

Timelines

expw

, s

cutoff

Si

eight

Reliabilit gnaly,

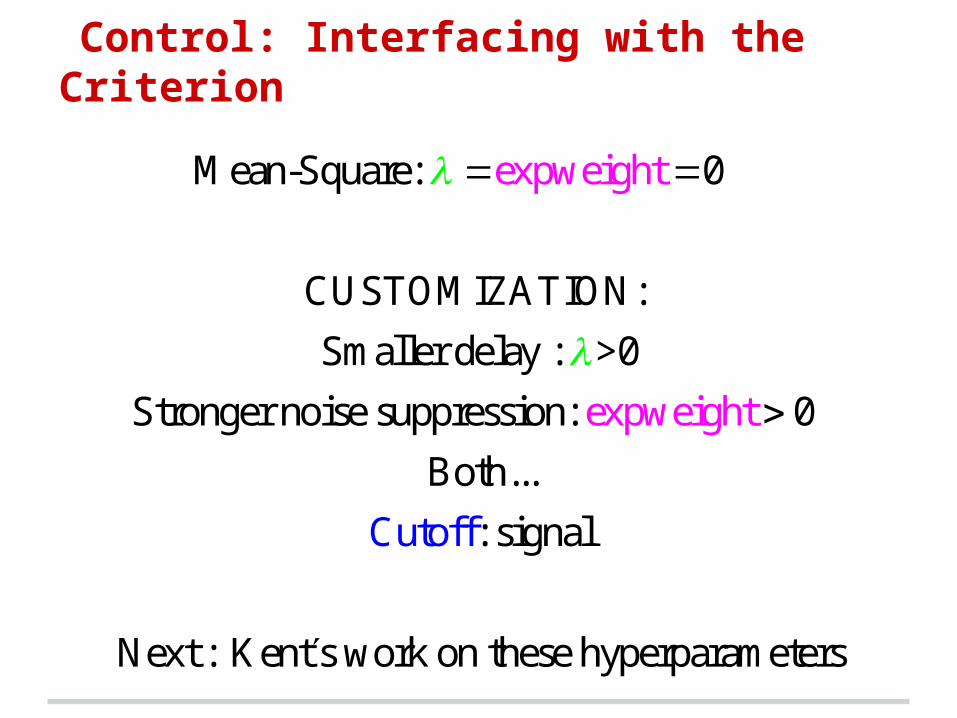

Control: Interfacing with the Criterion

Mean-Square: 0

CUSTOMIZATION:

Smaller delay : >0

Stronger noise suppression: 0

Both...

: signal

Next : Kent s

expwe

work

ight

on t

expw

hese

Cu

eigh

h

toff

yper

t

parameters

Latest Developments (2011,2012)

• Fast closed-form solutionso I-MDFA

• Generic Approacho Replicate model-based approaches, HP-designs, CF-

designs (see http://blog.zhaw.ch/idp/sefblog)o Customize traditional mean-square approaches

• Alleviate/control overfittingo Regularizationo Rmetrics-2012

Background

• SEFBlog:o http://blog.zhaw.ch/idp/sefblogo Articles, books, applications, R-code, tutorials

• Recent Articles:o Wildi/McElroy (2012)

http://blog.zhaw.ch/idp/sefblog/index.php?/archives/263-On-a-Trilemma-Between-Accuracy,-Timeliness-and-Smoothness-in-Real-Time-Forecasting-and-Signal-Extraction.html

o Wildi (2012) http://blog.zhaw.ch/idp/sefblog/index.php?/

archives/262-Up-Dated-I-MDFA-Code-and-Working-Paper.html

Background

• R-Code/tutorialso Check the categories `I-MDFA code repository’ or

`tutorial’ on SEFBlog

• Macro-indicators o http://www.idp.zhaw.ch/usrio http://www.idp.zhaw.ch/euri

• Tradingo http://www.idp.zhaw.ch/MDFA-XTo http://blog.zhaw.ch/idp/sefblog/index.php?/

archives/157-A-Generalization-of-the-GARCH-in-Mean-Model-Vola-in-I-MDFA-filter.html

A Hybrid Approach

• iMetricao Access to State Space, ARIMA, I-MDFA, Stochastic

Volatility, Hybrido Chris Blakely: www.cd-blakely.com

Vola in I-MDFA

Described in a blog post, and then in more detail later in a conference presentation.

http://blog.zhaw.ch/idp/sefblog/index.php?/archives/157-A-Generalization-of-the-GARCH-in-Mean-Model-Vola-in-I-MDFA-filter.html

Exercise: Reproduce the Example

Code available on SEF-Blog at:

http://blog.zhaw.ch/idp/sefblog/uploads/Vola_in_I-MDFA_prototype1.r

Runs as-is, but you need a "trading" function

Zero-crossing function:start with your filter weights and data series

create a vector of NAs as long as your index to be your signal

set signal to 1 where filtered data > 0

set signal to 0 where filtered data < 0

fill your NAs - na.locf() is your best friend

Not sophisticated, but tricky: watch your lagsVeddy importante: signal *today* means returns *tomorrow*

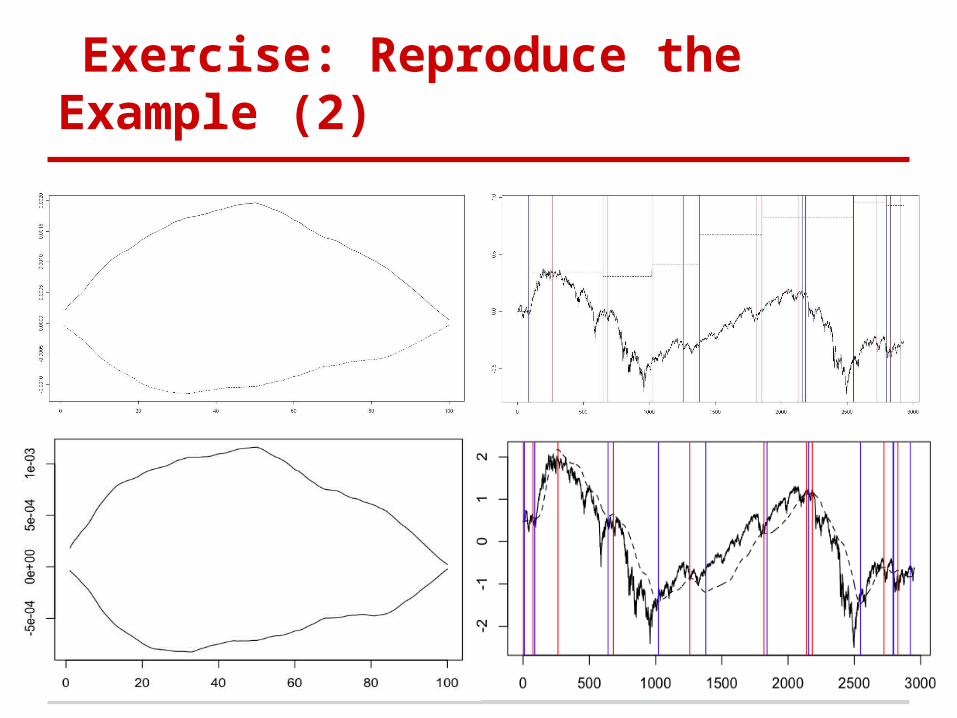

Exercise: Reproduce the Example (2)

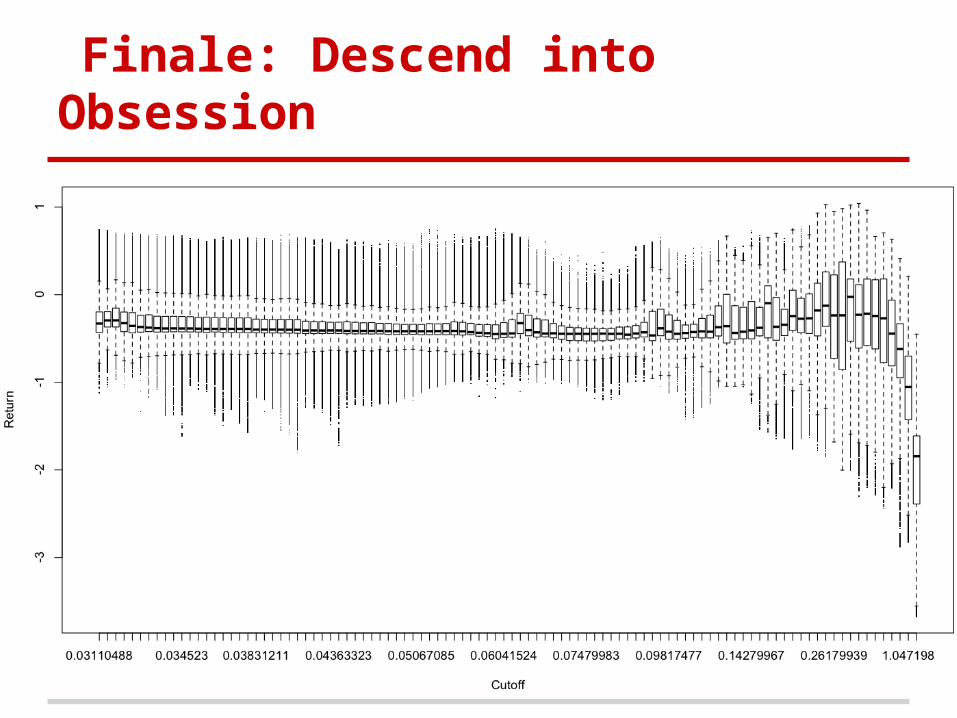

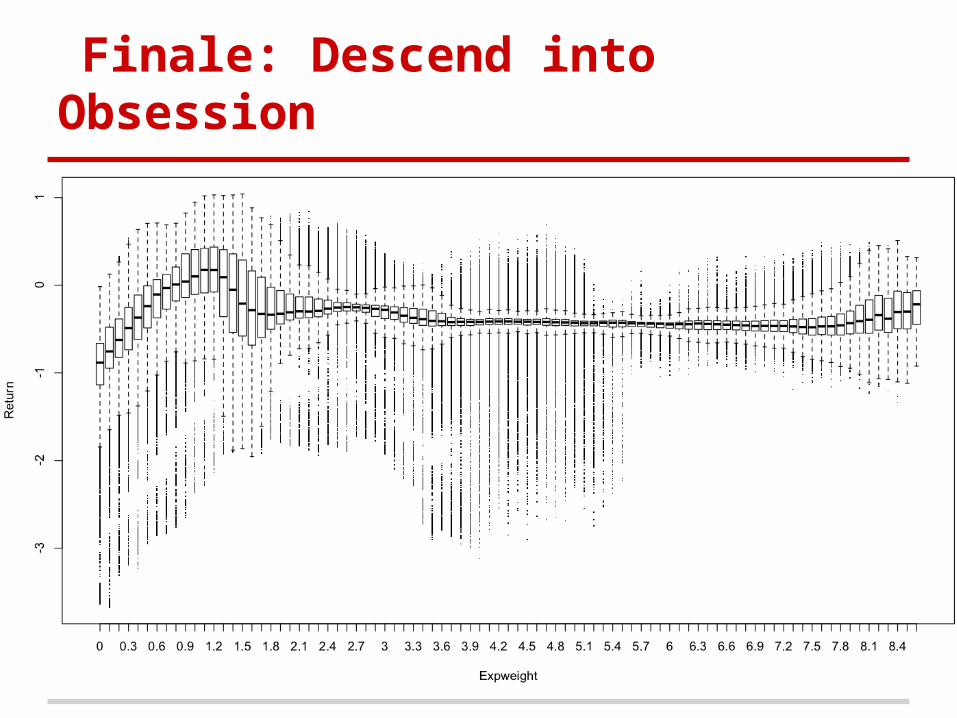

Corollary: Understand the Behavior

Reference code runs a multi-stage loopcalculates filters for combinations of params

runs an optimizer over the param space

Effective, but not illuminating for meparameter changes not intuitive (for me)

needed a feel for sensitivity

And I just happen to have a lot of machines...easy code changes: expand.grid and foreach

lots of cpu time

eventually, lots of results

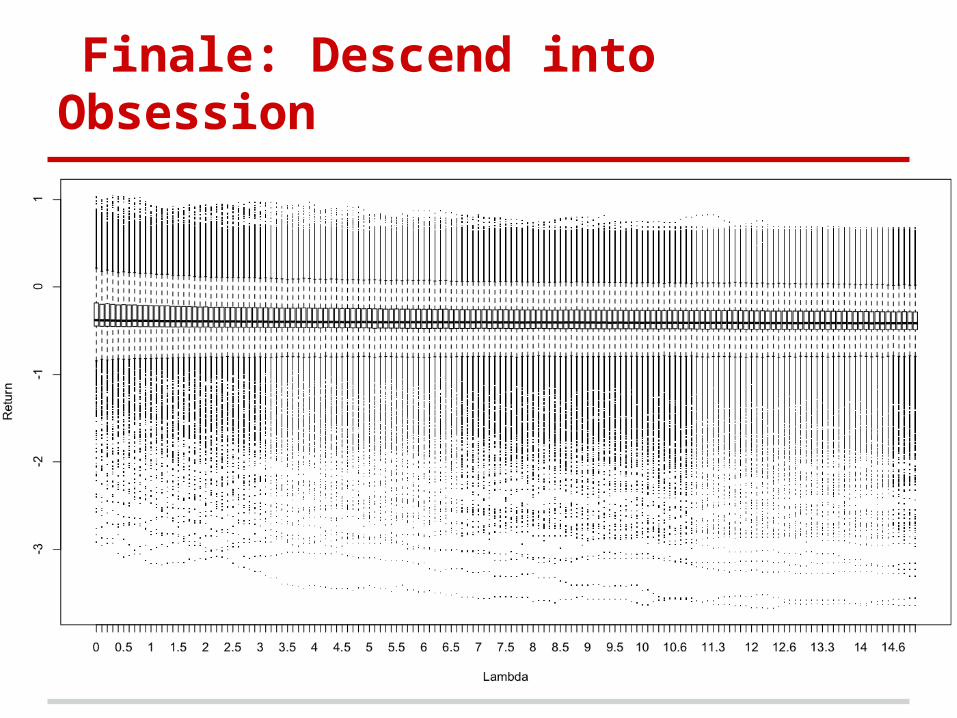

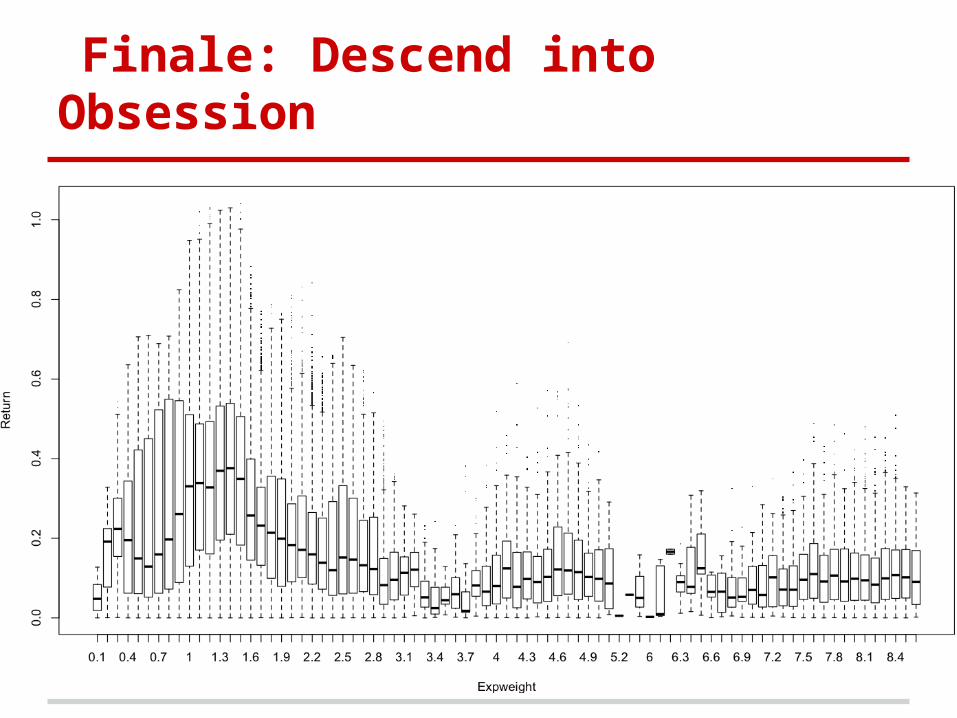

Finale: Descend into Obsession

Finale: Descend into Obsession

Finale: Descend into Obsession

Finale: Descend into Obsession

Finale: Descend into Obsession

Finale: Descend into Obsession

Finale: Descend into Obsession

Results: Qualitative Analysis of M/S

Results: Qualitative Analysis of M/S

![[THEODORE WILDI] ELECTROTECHNIQUE - 4 edition.pdf](https://static.fdocuments.in/doc/165x107/5695d1e11a28ab9b02984728/theodore-wildi-electrotechnique-4-editionpdf.jpg)

![[Theodore Wildi] Electrical Machines, Drives and P(Bookos.org)](https://static.fdocuments.in/doc/165x107/55cf99e0550346d0339f9b9a/theodore-wildi-electrical-machines-drives-and-pbookosorg.jpg)