TradeGuide - Commonwealth Bank

83

Welcome to the Commonwealth Bank TradeGuide

Transcript of TradeGuide - Commonwealth Bank

Welcome to the Commonwealth Bank

TradeGuide

Dear Trade Participant,

Whether you are new to the business or an experienced trader, the Commonwealth Bank Trade Services TradeGuide is designed to assist you in your importing and exporting activities.

To make it easy for you to fi nd the information that is relevant to your operation, we have packaged the TradeGuide onto this CD, which is an interactive disk. This means you can click on links in the Contents page to fast track you to where you want to go. You can also use the link buttons at the bottom left of each page to move backward or forward between sections or return to the Contents.

As you will see, this comprehensive guide provides in-depth information on a range of topics, from documentation of shipments to government regulations and methods of payment.

Of course, the TradeGuide does not replace one-to-one advice that you can receive from our trade fi nancing professionals, but it may help answer some of the questions you have. The Commonwealth Bank plays a leading role in facilitating trade and offers a range of trade services and products to help you. Please do not hesitate to contact us to discuss your needs.

I hope you fi nd this interactive CD useful, and I would like to take this opportunity to congratulate you on choosing to participate in Australia’s vibrant trading market and wish you every success in your endeavours.

Yours sincerely,

Mike ReidyExecutive Manager, Trade ServicesCommonwealth Bank

Welcome

1

How to navigate

Skip to previous section

Previous page

Content page

Next page

Skip to next section

Welcome letter 1

Trade Services Helpdesk 3

Preface 4

About the Commonwealth Bank of Australia 5

Introduction 6

Risks in international trade 7

■ Foreign exchange – introduction 10

■ Foreign exchange – risk management 13

Documentation of shipments 18

■ Bills of exchange 18

■ Documentation of shipments 20

Methods of payment 24

■ Methods of payment – operations 24

■ Methods of payment – risks 42

Finance 47

■ Finance for importers and exporters 47

■ Post-shipment fi nance for exporters 51

■ Associated fi nancial instruments 54

Complementary trade information 56

■ Complementary services for importersand exporters 56

■ Government regulations 62

■ Checklist for exporters 64

Glossary 66

Appendices 68

■ Sample exchange rate schedule 68

■ Sample completed application for issuance of an Import Documentary Credit 69

■ Sample Documentary Credit transmittedby S.W.I.F.T. 71

■ Sample Documentary Credit issued by mail 72

■ Sample shipping documents 73

■ Application for forward exchange contract 79

■ Lodgement authority for Export Shipping Documents 80

Click on the bold chapter headings to link directly to that chapter.

Click to print all document

Content

2

3

For technical or general import/export assistance, 8:30am to 8:00pm (EST).

Phone: 1300 654 112 (Toll Free)

Fax: 1300 654 115 (Toll Free)

Email: [email protected]

Enquiry: SWIFT: CTBAAU2SITS

Trade Services Helpdesk

To visit our trade web-site, click here

4

Eighth edition 2006With the volatile economic and market conditions prevalent in the international fi nancial markets in recent years, banking techniques, through necessity, have undergone considerable change. This is no less the case in fi nancing of import and export transactions.

Factors such as the deregulation of the Australian fi nancial markets have resulted in the development of innovative fi nancing techniques suitable to both importers and exporters. Availability of appropriate fi nancing can be integral to a trader’s ability to quote a competitive price for goods and to minimise the total cost of any goods purchased.

Accordingly, this publication has been written as a guide for new and inexperienced traders who are seeking an overview of international trade and appropriate fi nancing tools. We have endeavoured to structure the publication to be read from cover to cover and so to build upon the information included in previous chapters.

The publication should not be regarded as a textbook nor as the sole source of reference for international trade enquiries.

Requests to reproduce any part of this publication are to be referred to:

Commonwealth Bank of AustraliaInternational Trade ProductsGPO Box 2719Sydney NSW 1155

Important note

This CD is published as an information service only. Although every effort has been made to ensure that the information contained in this CD is correct at the time of publication, neither the Commonwealth Bank of Australia nor its employees are responsible for any loss occasioned to any person acting or refraining from acting as a result of the contents of this CD, or for any error in or omission from this CD.

First edition: 1986

Reprinted: 1987

Second edition: 1988

Third edition: 1991

Fourth edition: 1992

Fifth edition: 1993

Sixth edition: 1997

Seventh edition: 2005

Eighth edition: 2006

Full terms and conditions for the accounts/facilities mentioned in this CD are available on application. Bank and Government charges may apply. Applications for fi nance are subject to the Bank’s normal credit approval.

Preface

5

The Commonwealth Bank of Australia was established by an Act of Parliament in 1911 to conduct banking business and opened for business on 15 July 1912.

The Bank’s functions were later expanded to encompass those of a central bank. Subsequent legislative amendment in 1959 created a separate Reserve Bank of Australia to take over the central bank functions.

Since then the Bank has progressed to the point where it is one of Australia’s largest fi nancial institutions.

In recent times the Bank has undergone signifi cant restructuring to meet the challenges of a rapidly evolving fi nancial market place.

These challenges are being presented through substantial breakthroughs in technology, emergence of other ‘niche’ fi nancial providers and increased expectations from consumers of fi nancial products.

The international trade arena is not isolated from these challenges.

The Bank has been, and continues to be, active in catering for the requirements of importers and exporters. We have resources available for use by traders including fl exible fi nance packages, access to global payment systems and, of course, appropriate skilled personnel to help and assist customers in their import and export transactions.

The assistance available from our personnel will assist a trader in determining the most effi cient fi nancing structure, identifying risks, methods of mitigating some of these risks and to determine the most appropriate payment method in light of the individual transaction.

To contact one of our experts to discuss your individual trade fi nance requirements, simply call 1300 654 112 or visit commbank.com.au

About the Commonwealth Bank of Australia

6

Since earliest times, people have been trading surplus goods for profi t or in exchange for other goods or services. This basic principle continues to guide international trade today. Certainly, today’s mechanisms for payment, shipment methods, and the global economy make for a far more sophisticated market place than those of historical times, however, the ‘raison d’être’ remains.

This sophistication has been accompanied by growth in the variety of goods available, numbers of buyers and sellers, channels of delivery and methods of payment. Inevitably, the risks encountered by both buyers and sellers have increased also.

Today’s traders need to have access to information and specialist services to ensure that all payment, fi nance and risk mitigation options are explored and all risks are evaluated before committing to a deal.

The Commonwealth Bank assists traders on many of these issues. The areas of expertise for the banking industry are fi nance, method of payment and management of credit, transfer and foreign exchange risks. The international banking system also provides a complete means of settling trade debts between buyer and seller.

The Commonwealth Bank provides both exporters and importers with strong support through a range of services specifi cally tailored to meet the requirements of each individual trader.

As the proceeds from export sales are integral to Australia’s income, the support offered by the Commonwealth Bank to Australian exporters brings benefi ts to all Australians. The income derived from export sales leads to improved balance of trade fi gures, lower interest rates, more business investment and employment, etc.

In the following chapters we examine some of the more common risks found in international trade, and the methods of payment available to traders. We also explain the processes of the different methods of payment through the banking system and focus on the risks that each of these methods of payment brings. Additional chapters discuss the documentation and fi nancing aspects of trade.To further assist traders we have included a separate section on complementary services available from the Commonwealth Bank and other organisations.

Introduction

7

Dealing with buyers and/or sellers in other countries brings with it complexity that is unlikely to be found in local trading. The diversity of trade opportunities and the constant changes in economic circumstances make it impossible to generalise which is the most signifi cant risk faced by traders. This chapter describes the more common commercial risks that a trader will encounter and also includes a brief commentary on the prevalence of fraudulent activity in international trade.

For new or inexperienced traders, it is strongly recommended that you discuss any transactions with your bankers prior to entering into negotiations with unknown parties.

Fraudulent activityTrading goods has been a regular process throughout the ages. As with other endeavours, this has come to the attention of unscrupulous persons. There is an almost infi nite variety of frauds that are practiced on inexperienced and experienced traders alike. A key rule of thumb is to transact deals only with reputable parties that have a proven record in trading the particular goods in question.

The modern age, despite the ease of communications and the improvement in technology, has not seen any reduction in fraudulent trade and accordingly all traders are cautioned against immediately accepting offers that seem ‘too good to be true’, because, more often than not, they are.

Some of the common attributes of recent frauds are very large amounts, lack of any substantial evidence of the existence of the goods, a plethora of offi cial looking documents and lack of a track history for the buyers and sellers in their international trade dealings.

Any negotiations with unknown suppliers, buyers or third party agents should always be treated with care and diligence and no commitment given until the bona fi des of all parties are established.

Any reservations that traders may have about any deal should be discussed with their bankers. Banks by the nature of their role in facilitating paymentfor trade transactions are in a position to view many of the frauds that are attempted and perpetrated. Accordingly, a discussion with your bankers may bring to light any risks that may have been overlooked at the time of negotiation.

Commercial risksThere are a variety of commercial risks in international trade and the following describes some of the more common of these risks and their mitigants that should be considered during your negotiations. When, how and to what extent these risks apply is discussed more fully in the chapter ‘Methods of payment, risks’ (page 42).

EXCHANGE RISK

All traders should evaluate the profi tability of sales and purchases prior to agreeing to a contract.

Transactions which are to be denominated in currencies other than the trader’s local currency (being the currency in which costs, etc. are incurred), will require the foreign currency amount that is to be paid or received to be converted to local currency equivalent.

Exchange Risk, sometimes also referred to as Currency Risk, describes the risk that after exchange of the foreign currency amount the resultant local currency equivalent will vary from the local currency amount that was calculated before agreeing to the contract.

Exchange Risk arises due to variations in exchange rates for the currencies concerned and the delay between the time of entering into the contract and making or receiving the payment.

Given the constantly fl uctuating nature of exchange rates, management of foreign exchange exposuresis vitally important to the profi tability of any trader.

Mitigants

Exchange Risk plays a very large role in international trade. Accordingly, a separate chapter, ‘Foreign exchange’ (page 10), has been devoted to discuss the many and varied methods of mitigating this risk.

NON-DELIVERY/PERFORMANCE

When dealing with suppliers there is a risk that they may not be able to perform in accordance with the sales contract.

Risks in international trade

8

Non-performance may be an inability to deliver the requested goods, delivering inferior goods or simply being unable to deliver on time. Such non-performance may or may not be as a result of events outside the supplier’s control. However, the result of non-performance by the supplier will have an impact on the ability of the buyer to meet their commitments or to maintain their manufacturing output.

The adage ‘caveat emptor’ (‘let the buyer beware’) is especially true in international trade.

For an exporter, this risk may manifest itself in the importer not honouring the sales contract and wilfully not making payment. Any subsequent efforts made by the exporter to enforce the contract will represent costs that will detract from the profi t originally forecast.

Mitigants

There are no guaranteed methods of eliminatingthis risk. It may, however, be mitigated by making enquiries and seeking trade references prior to dealing with any new trading partners.

A secondary source of quality goods should always be available to limit economic damage caused by non-performance of the supplier.

For exporters, the risk of repudiation of the sales contract may be insured through export insurance entities such as Atradius Credit Insurance NV or QBE Trade Indemnity (page 59).

CREDIT RISK

The creditworthiness (being the ability and willingness to make payment) of the buyer should be of paramount importance for any exporter. Obviously, contracts should not be entered into and shipments should not be made unless payment is reasonably assured of being received.

Therefore, at a minimum, credit and trade references should be obtained before committing to any sale. For exporters who have agreed to extended credit terms with the buyer, it may be prudent for the exporter to obtain updated credit references on a regular basis or to examine the buyer’s annual reports to ensure their ongoing creditworthiness.

Credit Risk should not be considered solely as the risk of insolvency of the buyer. Any party involvedin the payment chain, including banks, must be included when considering this risk.

For an importer, the risk of insolvency of the seller needs consideration. If payment is made and the seller becomes insolvent, the importer may fi nd that their payment will not be returned. Similarly, if the seller is unable to effect shipment due to their insolvency the importer will need to quickly locate a new supplier.

The method of payment chosen may support the extension of some credit terms to the buyer.

Traders should also consider the impact of any default in relation to any exchange risk mitigant arrangements that may have been made.

Mitigants

For an exporter, these risks may be insured through entities such as Atradius Credit Insurance NV and QBE Trade Indemnity (refer page 59). Further options for mitigation of this risk are discussed in the section ‘Without Recourse Export Finance (WREF)’ (refer page 52).

An importer will need to be confi dent that the supplier is and will be able to fulfi ll their side of the sales contract before committing themselves to the transaction.

TRANSFER RISK

Payment Transfer Risk is the risk that due to a change in governmental regulations, the importer is prohibited or restricted in making payment or obtaining foreign currency to settle debts. Conversely an exporter may also be restricted in receiving payments from certain sources or exchanging foreign currency.

Many countries have laws and regulations relating to the outward transfer of money and the conversion of foreign currency receipts. Where these regulations are suddenly or unexpectedly changed, import and export transactions previously agreed to and not yet settled may suddenly be thwarted.

Accordingly, the ability of an importer or exporter to fulfi ll their obligations is subject to stable political environments. Equally, the broader political climate

9

in the trader’s counterpart’s country may be impacted by international actions such as economic embargoes and sanctions which may preclude settlement of transactions.

These changes may be brought about by war, natural events, etc. or a change in political power and a consequent change in governmental regulations.

Mitigants

For an exporter, some of these risks may be insured through entities such as Atradius Credit Insurance NV and QBE Trade Indemnity (refer page 59).

Country riskMost countries have regulations that govern the import and export of goods. Where these regulations are suddenly and unexpectedly changed, import and export transactions already agreed to and not completed may suddenly become invalid.

Additionally, an exporter should consider the integrity of business laws and the legal system in the country they are selling to as well as the level of compatibility of these laws with Australian laws.

Accordingly, the ability of an importer or exporter to fulfi ll their obligations is subject to stable political environments.

Any change in the relevant governmental regulations may have an effect on either the payment and receipt of money or the acceptability of the goods for import or export. These changes may be brought about by war, natural events, etc. or more generally a change in political power and a consequent change in governmental regulations.

Country Risk is the risk that, due to a change in governmental regulations, the importer is prohibited or restricted from receiving the shipment. Conversely, an exporter may be restricted in effecting the shipment due to cancellation of export licences, permits, etc.

Mitigants

For an exporter, some of these risks may be insured through entities such as Atradius Credit Insurance NV and QBE Trade Indemnity (refer page 59).

Transport risksTransport risks include the risks of theft, pilferage and damage to the goods whilst in transit from the seller to the buyer.

Additional losses over and above the cost of the goods may also be incurred as a result of damage to the goods. These additional costs and losses will range from freight costs, to the loss of any profi t that would have been made on the onselling of the goods, etc.

Mitigants

These risks are normally insured through commercial marine insurance agencies.

10

The buying and selling of goods internationally will usually mean that one party will be either receiving or paying a foreign currency, that is, a currency other than the currency used domestically. In some cases, it may be that both parties will be dealing in a foreign currency.

Accordingly, the issue of foreign exchange is of prime importance to both importers and exporters who are making or receiving payments in a foreign currency.

In this chapter, we discuss some background to exchange rates and in the following chapter, Foreign exchange (risk management), a commentary is provided on the various methods available to traders to manage their exposure to movements in exchange rates.

What is an exchange rate?The simple answer is that it is the price expressedin one currency to exchange that currency for another. The way a rate, or price, is quoted in Australia is the amount of foreign currency that willbe received or provided by the customer for one Australian Dollar (AUD).

The exchange rate is determined by a numberof factors including the amount of currency for saleor purchase, comparative interest rates, the number of buyers and sellers and their expectations on the future worth of the currency, which in turn is determined by the perceived economic health of the country.

Exchange rates are always quoted from the perspective of the bank. Therefore, when a bank quotes a selling rate, it is the rate at which the bank is prepared to offer the foreign currency in exchange for AUD. The foreign currency will be paid to the customer in accordance with their instructions, e.g. includes remittances to suppliers and payments due under documentary collections and documentary credits, etc. Conversely, in the case where a buying rate is quoted, the customer will pay the foreign currency to the bank and receive an appropriate amount of Australian Dollars in return.

For example...

A bank selling rate is quoted for United States Dollars (USD) at 0.7108.

Therefore, as this exchange rate is in terms of one Australian Dollar, the importer will receive 71.08 US cents for each Australian Dollar.

Accordingly, if a payment due to an overseas supplier is USD10,000, this amount is to be divided by the exchange rate to calculate the amount in Australian Dollars that is required to be paid by the importer to the bank:

USD10,000 divided by 0.7108 = AUD14,068.66

On the other hand, a bank buying rate is quoted for United States Dollars at 0.7198 that is an exporter will receive one Australian Dollar for each 71.98 US cents.

Accordingly, if the payment received by the exporter is USD15,000, this amount is to be divided by the exchange rate to calculate the amount of Australian Dollars that will be received from the bank:

USD15,000 divided by 0.7198 = AUD20,839.12

The use of rates and the difference between buying and selling rates may sometimes be confusing. However, two simple rules will help traders to use quoted rates correctly. These rules are:

◆ If the customer pays AUD to the bank, the bank will use the selling rate. If the customer receives AUD from the bank, the bank will use a buying rate, and;

◆ To arrive at an AUD equivalent, divide the foreign currency amount by the rate quoted. To arrive at a foreign currency equivalent multiply the AUD amount by the rate quoted.

Excesses and shortfalls of those currencies bought and sold by banks are cleared through domestic and international fi nancial markets. The Commonwealth Bank participates actively in these markets in order to provide up to the moment rates to its customers.

Exchange rates fall into two main categories:

◆ spot or value today exchange rates (buying and selling), and;

◆ forward exchange rates (buying and selling).

Foreign exchange – introduction

11

Spot and value todayexchange ratesIn the international fi nancial markets, foreign exchange deals agreed today will generally be settled two working days hence. Two day settlement is referred to as ‘spot value’. As Australian banks settle their excess or shortfall of foreign currencies in fi nancial markets, Australian banks encourage their major foreign exchange customers to conform to this practice and fi x exchange rates two days ahead of when the funds are required or expected.

Traditionally, however, Australian traders have usually sought ‘value today’ transactions, where the currencies are exchanged that same day. Accordingly, the rates available in the international market are adjusted to refl ect the timing difference between the internationally accepted two day ‘spot value’ transactions and the Australian practice of ‘value today’ transactions.

A sample Daily Exchange Rates schedule is shown on page 68. Although all these rates are quoted on a ‘value today’ basis, further timing differences can intrude in the calculation of a buying rate. Therefore there will be up to 3 buying rates quoted for each currency whilst only one selling rate.

There is only one rate quoted for the selling of each currency as there is not a timing difference for selling rates. This is because the bank will receive AUD immediately from its customer whilst

simultaneously delivering the foreign currency in accordance with the customer’s instructions.

Foreign exchange buying ratesIn calculating a buying rate of exchange, the Bank takes into account any lapse in time between the date of purchasing the foreign currency from a customer and the date on which the foreign currency concerned is actually received by the bank in an immediately tradable form. It should be noted that foreign cash is not viewed as immediately tradable.

As can be seen from the Daily Exchange Rates schedule on page 68, the Bank quotes three buying rates. These are T/T (Telegraphic Transfer), O/D Air Cheques and Notes (cash).

The T/T rate is used in those cases where the bank buying the currency has received the foreign currency in one of its foreign currency accounts conducted with banks overseas.

Where the bank has received foreign currency to such an account before it pays the AUD equivalent to the customer, the bank is able to immediately use those funds in its foreign currency dealings. Accordingly, the bank is able to pass on that benefi t to the customer by way of an exchange rate which will generate more AUD for the customer than would be the case if the O/D or Note buying rates had been used.

The O/D rate is used where the bank buying the currency has not yet received the foreign currency, however is able to set about claiming the amount due by clearance of a cheque, etc.

For example, where a customer presents a cheque in a foreign currency and requests that it be immediately exchanged for AUD, and if the bank (negotiating bank) agrees to do so, it will generally use the O/D rate to calculate the amount of AUD due to the customer.

However, the bank has not received the foreign currency, it has simply received a cheque in that foreign currency. The cheque gives the negotiating bank the right to receive the foreign currency, however the cheque must fi rst be presented to the bank that it is drawn on (drawee bank) for payment. As the drawee bank is generally overseas, there will be a considerable delay until the foreign currency amount is actually received by the negotiating bank. Accordingly the O/D rate includes an interest factor for the period that the negotiating bank expects it will be out of pocket. Accordingly the rate is not as favourable to the customer as the T/T rate as it generates less AUD per unit of foreign currency.

The note buying rate is used where the bank purchases foreign currency presented in the form of cash. This rate attempts to recompense the bank for the holding costs, the risk of holding foreign cash, the value of which is subject to exchange rate fl uctuations, the small transaction amounts involved and the fact that the bank is out

12

of pocket until a buyer is found, if at all. Therefore, of the three buying rates, the note buying rate will yield the least amount of AUD to the customer per unit of foreign currency.

Forward exchange ratesA forward exchange rate is a rate that is quoted to buy or sell a particular currency at a future date. The date will generally be between 3 and 185 days in the future.

In International trade, as soon as an Australian exporter or importer agrees to a sale or purchase of goods in a foreign currency, an exchange risk arises. If the exchange rate moves, the amount of Australian currency to be received or paid will be affected.

Accordingly, if an exporter or importer knows the exchange rate at which these transactions will be converted when payment is received or made, they will be able to trade with confi dence knowing that the amount of local currency received or paid will ensure the transaction is profi table. A forward exchange rate meets this requirement. Forward exchange rates are not estimates of what the exchange rate for the currency will be at the future date. Rather they are rates that are based on current exchange rates adjusted to refl ect the differences between the interest rates for the two currencies concerned for the period nominated. This aspect is explained more fully in the following chapter.

Forward exchanges rates may also be quoted between two foreign currencies, e.g. a bank agrees to buy Japanese Yen from a customer in exchange for USD.

13

We briefl y discussed exchange risk in the earlier chapter, ‘Risks in international trade’. In this chapter, we will discuss mechanisms by which this risk can be managed.

Exchange risk can, of course, be avoided by importers and exporters simply contracting for purchases and sales in their local currency only. Such an approach, however, is likely to lead to a loss of trade opportunities due to a more fl exible approach being adopted by their competitors. For exporters, they may also be denying themselves the opportunity of fi nancing their export contracts in lower interest rate currencies.

It has become commonplace, since the deregulation of the Australian fi nancial markets in the early 1980s, that fi nancial news, both press and television, make mention of foreign currency exchange rates. This has certainly raised the consciousness of the Australian public and, of course importers and exporters, to the volatility of exchange rates.

Any movement in the exchange rate will affect the amount of domestic currency that an exporter receives, or an importer pays. For an exporter there are costs to be met from domestic currency, e.g. wages, rents, utilities, and therefore the profi tability or otherwise of any sale where payment is received in a foreign currency is contingent upon a favourable exchange rate. On the other hand, an importer who purchases goods where payment is effected in a foreign currency, will generally receive payment from local buyers in their domestic currency, thus also

creating an exposure to exchange rate movements.

Accordingly, a trader needs to be acquainted with the many and varied methods available to manage the risk of adverse movements in exchange rates.

The Commonwealth Bank offers a number of methods of managing these risks.

These methods include Forward Exchange Contracts, Flexible Forward Exchange Contracts, 24 Hour Market Watch, Foreign Currency Accounts, Foreign Currency Overdrafts and Foreign Currency Options.

It is sound practice for all traders to consider their exposure to foreign exchange movements and to develop a policy for the management of such risks. As movements in exchange rates are continual and have the potential to have a profound and wide ranging effect on a trader’s fi nancial viability, it is important to have a set policy so that these movements do not encourage speculation or complacency.

Each of the risk management methods discussed in the following pages have different features and meet different needs and market conditions. Accordingly, some methods may not be appropriate to a trader’s particular circumstance. The features vary from nullifying any exposure to exchange rate movements to allowing for some movements both adverse or benefi cial or to simply covering a worst case scenario. Of course, the cost of each of the options available will vary along with the complexity

of the risk management strategy agreed upon.

Due to the complex and volatile nature of some of the risk management methods, it is recommended that discussions are sought with your bankers prior to committing to any transaction that will involve an exchange of foreign currency.

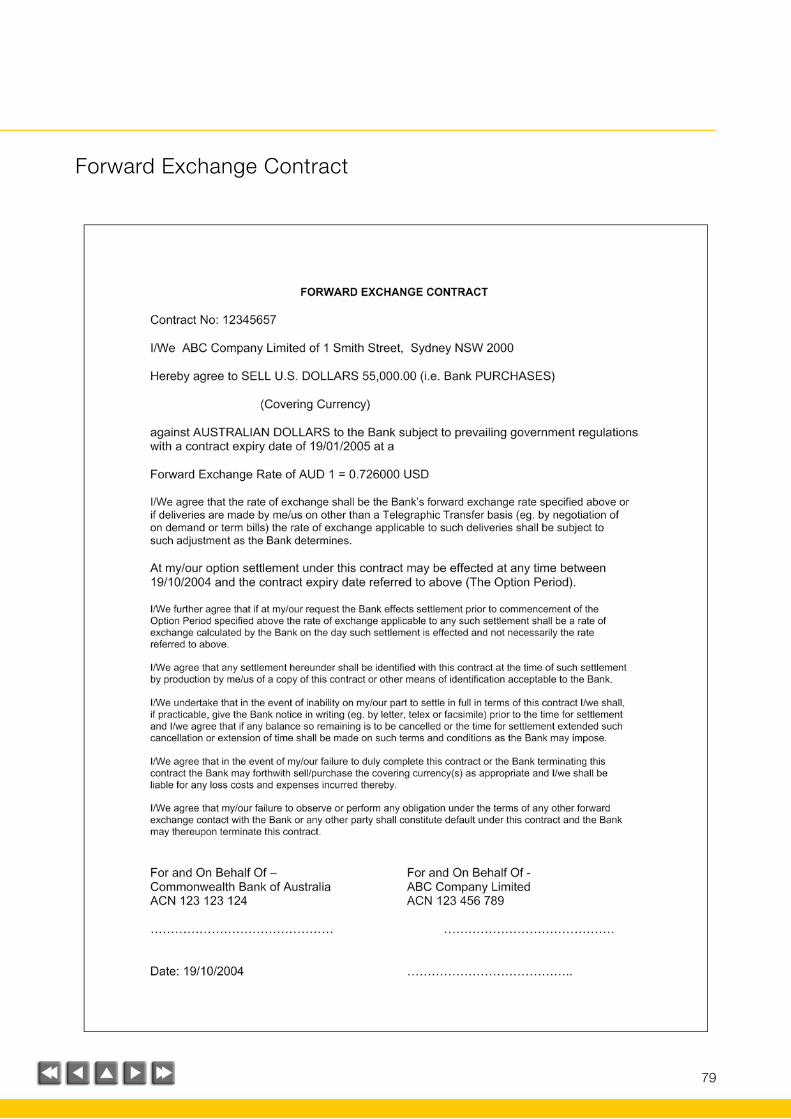

Forward exchange contractsAs discussed in the previous chapter (Foreign exchange, introduction) a customer may request the bank to quote a forward exchange rate. If the bank agrees to do so, a rate will be agreed and a forward exchange contract will be signed by both the bank and the customer. A forward exchange contract simply documents the agreement to buy or sell a foreign currency at a fi xed rate upon or within certain dates. Traders wishing to arrange facilities for the dealing of forward exchange contracts should discuss their requirements with their bankers.

A sample of the Commonwealth Bank’s Standard Forward Exchange Contract is shown on page 79.

The forward exchange contract will stipulate whether the bank is to buy or sell the foreign currency, the amount of foreign currency involved, the agreed exchange rate and the date or period of time on or during which delivery of the currencies is to take place.

A forward exchange contract may be arranged

Foreign exchange – risk management

14

so that delivery of the currencies at the agreed exchange rate is to occur on one particular, fi xed date. This is known as a ‘fi xed’ forward exchange contract. Alternatively, delivery of the currencies at the agreed exchange rate may be agreed to take place between two dates. The period between these two dates is known as an ‘optional period’. These contracts are known as ‘optional’ forward exchange contracts.

Optional forward exchange contracts are primarily used where the customer is not sure of the shipping timetable of the goods and thus the subsequent date of payment or receipt of the foreign currency amount.

Both these types of forward exchange contracts are available for buying and selling foreign currencies. Where a forward exchange contract is entered into for the bank to buy a foreign currency, the rate quoted is on the basis that the foreign currency is provided to the bank on a ‘T/T’ basis. That is, the foreign currency must be received by the bank in one of its foreign currency accounts conducted with banks overseas on the date or within the optional period nominated in the forward exchange contract. Therefore, if a cheque is presented to the bank for conversion at the forward exchange contract rate, the contract rate will be adjusted to take into account the time delay that will be encountered in receiving payment from the bank that the cheque is drawn on. (See comments in the previous chapter under ‘Foreign exchange buying rates’ on page 11.)

Calculation of forwardexchange ratesA forward exchange rate does not represent a forecast by the bank of what the buying or selling rate of exchange for the relative currency will be in the future. Instead, the bank will calculate the forward exchange rate based on the differential between the respective interest rates of the two currencies involved.

It may seem unusual to base exchange rates around interest rates, however by way of example, consider an importer with a commitment to pay USD25,000 in 90 days time.

The importer may eliminate the risk of exchange rate movements by simply buying USD25,000 at the time of commitment to purchase the goods and investing this amount for 90 days until the payment is due. To buy the USD, the importer will spend AUD and accordingly will need to borrow or recall from an investment the appropriate amount. Therefore, the net exchange rate received at the end of 90 days will be the total USD available (USD25,000 plus interest earned) divided by the total AUD expended (the principal amount plus interest paid or foregone).

Although this example is simplified, banks will calculate forward exchange rates using much the same rationale.

24 Hour Market Watch Service

The 24 Hour Market Watch Service allows a trader the fl exibility of protecting a minimum acceptable foreign exchange rate whilst allowing for possible benefi cial movements in the relevant foreign exchange rate.

The mechanics of its operation are as follows.

A trader will agree with the Commonwealth Bank a minimum exchange rate that is acceptable to the trader. This rate is known as the ‘Stop Loss Rate’. From that time, the Bank will monitor exchange rate movements 24 hours a day through its international network of foreign exchange dealing rooms. If the market rate reaches the Stop Loss Rate, the Bank will buy or sell the relevant currency in accordance with the customer’s instructions.

If the foreign exchange rate moves materially in favour of the customer, the Bank will contact the customer to discuss the possibility of adjusting the Stop Loss Rate to take advantage of favourable movements in the exchange rate.

In currencies where the exchange rate is trending in favour of the customer, a 24 Hour Market Watch may prove more benefi cial to the customer than locking into a forward exchange contract where the exchange rate is fi xed.

Due to the complexity and variety of methods available to a trader to manage their exposure to movements in exchange rates, it is suggested that discussions be held with the Bank’s foreign exchange personnel prior to undertaking any foreign exchange dealings.

15

Foreign Currency OptionsA Foreign Currency Option (FCO) is available to exporters and importers as another mechanism to manage their foreign exchange risks.

A customer, in buying an option from the Commonwealth Bank, acquires the right but not the obligation to buy or sell an agreed amount of foreign currency at a predetermined exchange rate on, or up to, the specifi ed expiry date of the option.

In entering into an option contract, only the seller (generally the bank) of the contract is obliged to perform, and then only if the buyer exercises their right, or option, to buy or sell the foreign currency.

This contrasts to the forward exchange contract where both parties have an obligation to receive or deliver against the contract.

In purchasing an option, a customer will pay a premium to the seller of the option. The amount of the premium is determined by the seller considering a number of factors. These factors include the current exchange rate, the required option rate (or strike rate), volatility of the two currencies involved, the term of the option contract and whether the option may be called at maturity only or at any time during its term.

Flexible forward contractsIn a competitive environment, traders will want to be able to take advantage of favourable movements in

exchange rates. While a forward exchange contract allows importers and exporters to protect themselves against adverse exchange rate movements, it does not allow a trader to benefi t from any potential favourable exchange rate movements.

A fl exible forward contract combines the protectionof a forward exchange contract with the fl exibilityof a foreign currency option. By utilising the appropriate fl exible forward contract, importers and exporters will have:

◆ the security of knowing that whatever happens to the currency rate, their foreign exchange exposure remains protected. Importers and exporters are able to choose the level of required protection at the start, so the worst case is always known,

◆ the potential to benefi t from favourable currency rate movements.

Strategies that help traders manage their foreign exchange exposures will need to take into consideration three elements:

◆ the exchange rate level that needs to be protected;

◆ how long the exposure needs to be covered;

◆ the customer’s exchange rate outlook, that is their perception of the direction or trend of the relevant currency’s exchange rate and that currency’s volatility.

The Commonwealth Bank offers many variations of a fl exible forward contract, and each of these caters

to different market conditions and customers’ individual strategies.

The three fl exible forward contracts are described as:

◆ Flexible Forward Collar;

◆ Flexible Forward Convertible, and;

◆ Flexible Forward Bonus.

The most suitable contract will depend on the market conditions at the time of setting the contract and the customer’s strategy or policy of managing foreign currency exposures.

Flexible Forward Collar is designed for those customers who have a view that exchange rate movements will not be signifi cant. They do, however, wish to benefi t from potentially favourable exchange rate movements within a defi ned range. The Collar provides the customer with the comfort of knowing their worst case while enabling the customer to take some advantage of any favourable exchange rate movements.

The Collar is structured by setting two rates at the start of the contract – a fl oor rate and a ceiling rate.

The customer will select a level of required protection (for an importer a fl oor rate and for an exporter a ceiling rate) and the Bank will set a corresponding ceiling or fl oor rate.

At maturity of the Collar, there are three possible scenarios that will determine the exchange rate used by the customer at such a time. These are:

16

◆ The prevailing spot rate is at or below the fl oor rate – the customer is obliged to deal at the agreed fl oor rate;

◆ The prevailing spot rate is at or above the ceiling rate – the customer is obliged to deal at the agreed ceiling rate, or;

◆ The prevailing spot rate is between the fl oor and ceiling rate – the customer may deal at that prevailing spot rate.

As can be seen, the exchange rate used by the customer at maturity of the Collar will always be within the range that was agreed upon at commencement of the Collar, even if the prevailing spot rate at maturity falls outside the agreed range.

Flexible Forward Convertible is designed for those customers who require short term exchange rate protection and anticipate low exchange rate volatility. The Convertible is structured by setting two rates at the start of the Convertible, a contract rate and a Trigger rate. The contract rate is the guaranteed rate at which the customer’s foreign exchange exposure will remain protected. The customer will select the level of protection required, (contract rate) and the Bank will set the corresponding Trigger rate.

If the prevailing spot exchange rate reaches the Trigger rate at any time during the Convertible, the Convertible reverts to a forward exchange contract where the customer is locked in to dealing at the contract rate, and the Bank will issue a Trigger

notice. If the Trigger rate is not reached during the period of the Convertible and the prevailing spot rate at maturity of the Convertible is more favourable than the contract rate, there is no obligation to deal under the Convertible. Note: The customer is obliged to deal at the contract rate if the prevailing spot exchange rate reaches the Trigger rate at any time over the period of the Convertible.

Accordingly, at maturity of the Convertible there are two possible scenarios that will determine the exchange rate used by the customer at such a time. These are:

◆ The Trigger rate has not been reached during the term of the Convertible. In such a case the customer may deal at the more favourable of the following rates:

• The prevailing spot exchange rate; or • The Convertible contract rate.

◆ The Trigger rate has been reached during the term of the Convertible. In such a case the customer is obliged to deal at the contract rate, regardless of the prevailing spot exchange rate at maturity.

The worst case for the customer is that the Trigger rate is reached during the term of the Convertible. However if the Trigger rate is not reached then the customer is able to take advantage of any favourable movements in the exchange rate.

Flexible Forward Bonus is designed for those

customers who require longer term exchange rate protection and anticipate exchange rate volatility.The Bonus is structured through the setting of two exchange rates at the start of the contract; a contract rate and a Trigger rate.

The contract rate is the guaranteed rate at which the customer’s exposure will remain protected.

The customer will select the level of protection required, (contract rate), and the Bank will set the corresponding Trigger rate.

At maturity of the Bonus, there are two possible scenarios that will determine the exchange rate used by the customer. These are:

◆ The Trigger rate has been reached during the term of the Bonus. In such event, the customer may deal at the more favourable of the following rates:

• The prevailing spot exchange rate; or • The Bonus contract rate.

◆ The Trigger rate has not been reached during the term of the Bonus. In such a case, the customer is obliged to deal at the contract rate, regardless of the prevailing spot exchange rate at maturity.

In effect, the Bonus starts life as a forward exchange contract at the contract rate. The Trigger rate defi nes the level of the exchange rate at which the customer is no longer required to deal at the contract rate. If at any time over the life of the Bonus the exchange rate reaches the Trigger rate,

17

the Bank will notify the customer who immediately has the potential to benefi t from exchange rate movements below or above the contract rate. Note: the customer is obliged to deal at the contract rate unless the exchange rate reaches the Trigger rate at any time over the contract period.

Key features of all of the fl exible forward variants:

◆ Minimum transaction amount of the foreign currency equivalent of AUD25,000;

◆ Maturity periods from 1 week to 2 years.Other periods will be considered on request;

◆ Contracts are available against both the Australian Dollar and US Dollar for:

◆ Japanese Yen, Great British Pounds, Swiss Franc and Euros;

◆ Hong Kong Dollars, Singapore Dollars and New Zealand Dollars;

◆ Other currency pairs will be considered on request.

Foreign currency account

A foreign currency account is an account conducted in a currency other than Australian dollars.

The trader who receives and makes payments in the same foreign currency may choose to use this account as a method of minimising their exposure to exchange rate movements.

Simply, a trader may lodge foreign currency receipts into the account, hold them in that currency, and then use those funds to meet payments for their import commitments as they fall due.

The Commonwealth Bank offers foreign currency accounts in most freely negotiable currencies. As these accounts are domiciled within Australia, traders are able to manage the account in a more effi cient manner than would be the case in attempting to manage an account conducted with a fi nancial institution overseas.

Foreign currency overdraft

A foreign currency overdraft operates on a foreign currency account with the added fl exibility of allowing overdrawings up to an agreed limit. It allows a trader another option in managing their foreign exchange risk by enabling them to manage foreign currency cash fl ows.

Consider an exporter who requires some working capital to manufacture goods for export.

As the payment, when received, for the exported goods will be in a foreign currency, the exporter may elect to borrow that same currency to fi nance the manufacture of the goods. Accordingly, by converting the foreign currency to pay wages and local suppliers the exporter now has a debt in the same currency as that of the payment to be received. Therefore, provided the buyer makes payment, the exporter is no longer exposed to movements in exchange rates.

Foreign currency overdrafts are especially useful to customers when short term accommodation in foreign currency is required.

18

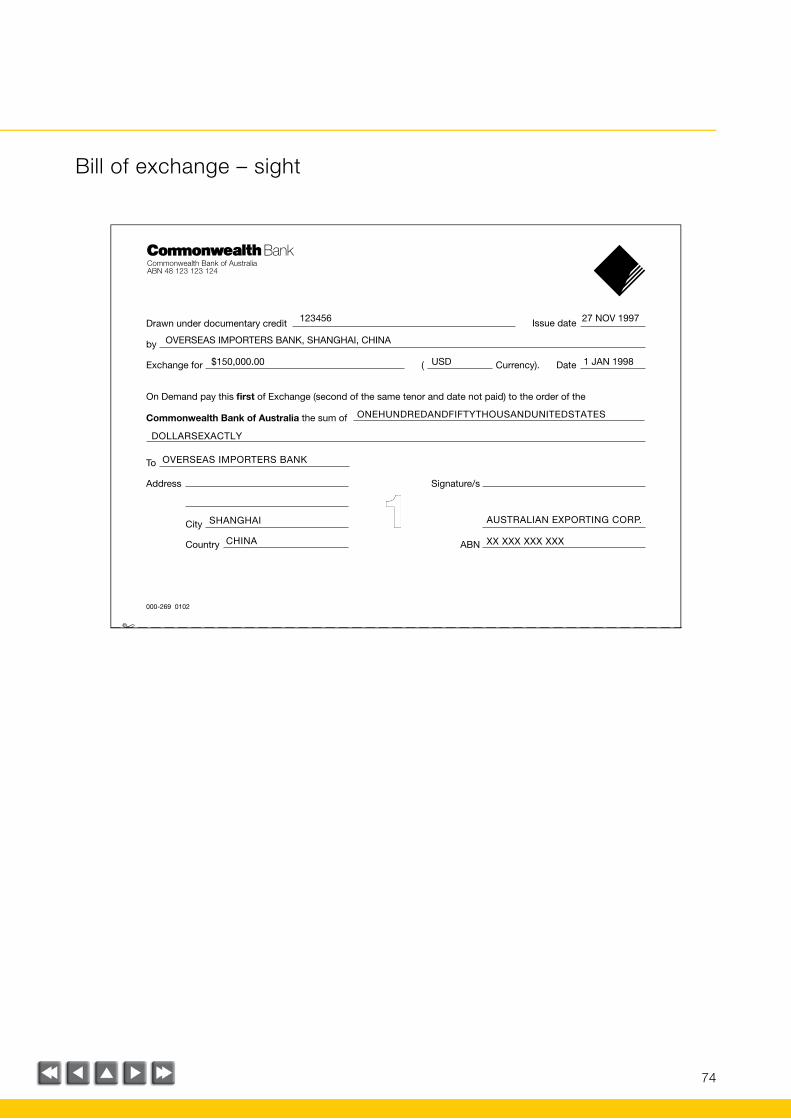

A primary document used in the settlement of many trade transactions is a ‘bill of exchange’, commonly referred to as a ‘draft’.

Bills of exchange have been used for many years and have reached an almost universal acceptability in the fi nancing and settlement of trade transactions.

A bill of exchange is simply a demand for payment issued by one party, generally the seller, on another party, generally the buyer. It is a legal document, governed in Australia by the Australian Bills of Exchange Act 1909. International conventions also support the basic rights and obligations of the various parties to a bill.

The Act defi nes a bill of exchange as ‘...an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay on demand, or at a fi xed or determinable future time, a sum certain in money to or to the order of a specifi ed person, or to bearer.’

A valid bill of exchange facilitates payment of trade transactions and, perhaps more importantly, provides a more straightforward means of undertaking recovery action in the event of default than relying on the underlying commercial contract.

Two of the more usual of bills of exchange used in international trade are illustrated on the following page.

The party issuing, or drawing, the bill of exchange is referred to as the ‘drawer’ or ‘principal’. This is the party to whom payment is owed, i.e. the exporter. The person to whom the bill of exchange is addressed, or drawn on, is the ‘drawee’. The drawee is the party who is required to make payment, i.e. the importer.

The examples show the Commonwealth Bank of Australia as the payee. The Bank will be the payee in those cases where bills are drawn under documentary credits or documentary collections.

In these circumstances, the Bank acts on the instructions of the exporter, and the documentary credit as appropriate, to receive and process payments. This is necessary as the importer will not be paying the exporter direct, but the intermediary banks.

Bills of exchange will be a demand for either immediate payment, ‘at sight’, or for future payment on a determinable date. The means of determining the maturity date of a bill of exchange is called ‘Tenor’ or ‘Usance’ of the draft, e.g. 90 days after

shipment or some other defi ned event. The tenor is determined during negotiations between buyer and seller as it stipulates when payment is to be made.

The drawee becomes legally liable for payment only after they have ‘accepted’ the bill of exchange, i.e. agreed to make payment according to the tenor of the bill. This agreement is evidenced by the drawee’s endorsement of the bill of exchange. Once accepted, the drawee is legally obliged to make payment in accordance with the tenor of the bill of exchange.

It should be noted that although a legal obligation is in place, the bill of exchange is not the same as a guarantee of payment. Instead, it allows for legal recourse against the acceptor of the bill if payment is not forthcoming.

The section ‘Methods of payment’ (page 24), illustrates the role of the bill of exchange in the settlement of trade transactions. Methods of using a bill of exchange as a fi nancing medium are discussed in the chapters ‘Finance for importers and exporters’ (page 47).

Documentation of shipment – bills of exchange

19

000-269 0102

Exchange for ( Currency.

To

Signature/s

ABN

Drawn under documentary credit Issue date

by

Address

City

Country

On Demand pay this first of Exchange (second of the same tenor and date not paid) to the order of the

Commonwealth Bank of Australia the sum of

1

Date

000-270 0102

DateExchange for ( Currency.

To

Signature/s

ABN

after pay this first

Drawn under documentary credit Issue date

by

Address

City

Country

of Exchange (second of the same tenor and date not paid) to the order of the Commonwealth Bank of Australia

the sum of

1

Tenor of bill, in this case“On Demand” that is, sight.

Amount and currency due.

Drawee, the party who is to make the payment.

Drawer, the party to whom the payment is owed.

Payee, the party to receive payment if not the drawer.

Tenor of bill, that is a number of days aftera determinable event that payment is due.

Amount and currency due.

Drawee, the party who is to make the payment.

Drawer, the party to whom the payment is owed.

Payee, the party to receive payment if not the drawer.

20

As documentation of a shipment plays a role in protecting the interests of all parties to a shipment it behoves a trader to have a basic understanding of the many documents that will be encountered.

In international trade, shipments traverse national boundaries, encountering varying legal, customs and other governmental requirements. Failure to comply with these regulations will delay shipments or payment and could prove costly to traders. Compliance with many of these regulations usually requires presentation of certain documents.

It is therefore wise for the importer to clarify with various authorities exactly what documentation is necessary to quickly clear a shipment, and to convey these requirements clearly to the exporter.

It is also prudent for the exporter to clarify these details independently to ensure that there are no avoidable delays. In Australia, this information may be obtained from the Australian Customs Service, Australian Quarantine and Inspection Service or through the services of a customs agent.

Generally, there are four types of documents used in international trade, namely:

◆ commercial;

◆ transport;

◆ insurance; and

◆ offi cial.

Commercial documents

Commercial invoices

A commercial invoice is a document that describes the transaction between the buyer and seller. While it primarily concerns these two parties, a third party such as a bank, customs or an insurance company may be interested in the document.

Invoices should contain data that is correct in all respects. While sellers may consider buyers’ requirements for detail on invoices as onerous, it should be remembered that these details may be required to comply with exchange control, import licence or customs duties legislation in the buyer’s country.

Invoices should include a full and accurate description of the transaction, these are:

◆ the full names and addresses of all parties to the transaction;

◆ any reference/invoice/order/sale numbers;

◆ transport details – departure date and time, point of dispatch and destination, shipping marks, mode of transport;

◆ a clear and accurate description of the goods;

◆ details of weight and measurement of packages;

◆ the total and unit value of the goods;

◆ the appropriate Incoterm (CIF, FOB etc.); and

◆ the method of payment.

An example of a commercial invoice is shown on page 73.

Other invoices

Exchange control and import/export regulations in many countries are such that, what may appear to be excessive demands by the buyer for documentation, may in fact be forced by these regulations.

Accordingly, the following variants to a commercial invoice may be required by the buyer.

Invoices combined with a certifi cate of origin and value are sometimes required for differing tariffs and customs duty based on the country of origin.

Consular invoices are invoices attested, in the county of dispatch, by the consulate of the importing country.

Commercial invoices certifi ed by a Chamber of Commerce or Chamber of Manufacturers.

These particular requirements will be determined by the customs or laws of the trading nations. They will vary between countries and, very often, between products.

Packing list

This document is usually required by the buyer when the shipment consists of a large number of cartons or packages. The packing list will itemise the items that are to be found in each of the cartons or packages and will assist the buyer to quickly locate required stock lines. It will also assist the seller in ensuring that the shipment is as ordered.

Documentation of shipments

21

Bill of exchange

The bill of exchange is discussed in detail in a separate chapter (page 18).

A bill of exchange or draft is used when paymentis to be made by either a documentary collectionor a documentary credit.

An example of a bill of exchange is shown on page 19.

Transport documents

To assist traders understand transport documents the following terms should be kept in mind:

Consignee The party shown on the transport document as the recipient of the goods (buyer, importer).

Consignor or shipper

The party shown on the transport document as the sender of the goods (seller, exporter).

Carrier The party who operates the carrying vessel or aircraft.

Freight Forwarder

The party who acts as an agent for the consignor in arranging shipment through a carrier.

Bill of lading

Where shipment is effected by sea, a document called a ‘bill of lading’ would normally be issued.

A commonly used transport document, its importance lies in three of its characteristics.

Firstly, it is a contract of carriage. Secondly, it is a receipt for goods and, thirdly, it is a transferable document of title. It is this third characteristic that enables exporters to ship goods without payment but continue to control the goods through control of the bill of lading until payment is received or a promise to pay is obtained.

As a contract of carriage, the bill of lading sets out the conditions of transport. Many of these clauses, particularly those common to most goods, have been standardised by international agreements. A bill of lading may also be subject to various laws depending on the countries that are involved. While the clauses on the reverse of a bill of lading may be considered lengthy and detailed, it is nevertheless worth a trader’s time to read through these clauses to ensure that there is nothing contrary to their particular interests.

At many major ports, goods will only be released upon presentation of an original bill of lading. Therefore, they are usually issued in three or more originals to guard against loss through mail or courier services.

Bills of lading should include the following details:

◆ a description of the goods including identifying marks and numbers;

◆ the name of the carrying vessel;

◆ the place of departure and destination;

◆ the names of shipper and consignee and, if required, the party to be notifi ed on arrival of carrying vessel at the port of destination;

◆ the terms of shipment – i.e. whether freight has been paid prior to dispatch or if it is to be collected at the port of destination;

◆ the date that the goods were loaded on board;

◆ the number of original bills of lading issued, and;

◆ the date the bill of lading is issued.

An example of a bill of lading is shown on pages 77-78.

There are a number of varying types of bills of lading that are commonly referred to in international trade. Some of the more common are detailed below:

Short bill of lading

Short bills of lading are generally used by shippers when they are required to issue bills of lading due to specifi c arrangements with the carrier at the port of dispatch.

It is an abbreviated bill of lading and in its standard form has the approval of the Council of Shipping.

On board or shipped bill of lading

These bills of lading simply carry an additional specifi c statement that the goods have been shipped on board a particular vessel.

22

Received for shipment bill of lading

A received for shipment bill of lading does not provide the additional assurance that the relative goods have actually been shipped. As its name suggests, it simply acknowledges that the relative goods have been ‘received for shipment’ by the carrier.

Claused bill of lading

When goods are received for shipment and the merchandise or the packaging is obviously defective, the carrier will, for their own protection, include or superimpose a clause on the bill of lading advising of the defect.

Charter party bill of lading

A charter party bill of lading is used in those situations where a shipper will hire/lease a vessel for a particular shipment. These situations are normally for the shipment of bulk materials e.g. grains, oil, livestock, etc.

The ‘charter party’ is a document setting out the full leasing details of the vessel leased for specifi c voyages or periods. Any bill of lading issued in these circumstances is subject to the specifi c individual conditions of that charter.

Freight forwarders bill of lading

This is simply a bill of lading that has been issued by a freight forwarder and not the actual carrier of the shipment. It is common practice for shippers

to have a freight forwarder arrange shipment with the carrier and accept the freight forwarder’s bill of lading in lieu of that of the carrier’s.

A trader should seek advice as to the different rights that they may have under a freight forwarder’s bill of lading to those available under a bill of lading issued by the carrier.

Combined transport document

A combined transport document allows the shipper to arrange shipment through the one carrier for a number of different modes of transport without the additional problems of arranging a different transport document for each differing transport mode.

Through transport document

A through transport document completes the same function as the combined transport document, however the carrier does not act as the principal through the entire journey. In the portions of the voyage where carriage is completed using other than the carrier’s vessels, the carrier acts only as an agent and not the principal. Accordingly, traders will need to examine the terms and conditions of such a document to ascertain their rights.

Sea waybill

A sea waybill is a transport document used for sea shipments. It differs to a bill of lading in that it does not act as a document of title but is a receipt for goods and a contract for carriage. Additionally, different

rights and obligations are accorded to all parties for shipments under sea waybills as compared to the rights and obligations due under bills of lading. Advice should be sought from your shipping agent to ensure that your interests are protected.

As the sea waybill is not a document of title, the goods may be released without presentation of an original sea waybill. In this respect the sea waybill operates in a similar fashion to that for air waybills in that the goods are released to the consignee, as shown on the waybill, without the need for the provision of an original transport document.

Accordingly, this particular document would not be appropriate in those situations where the exporter wishes to retain control of the goods by a document of title which in turn would only be made available to the importer upon payment, or promise to pay, for the shipment.

Air waybill

In the case of an air shipment an air waybill is the relative transport document that will be required.

An air waybill, like a bill of lading, is a document issued by the carrier acknowledging receipt of the goods. Similar to a sea waybill, an air waybill does not convey title to the goods, instead the shipment is consigned to a particular party. The consignee may obtain access to the goods without presentation of an air waybill.

Accordingly, as the shipper does not control the goods after the goods have been tendered to the

23

carrier for shipment, this can present problems when a bill of exchange is involved and the exporter wishes to retain control of the shipment until payment is made.

To overcome this the goods may be consigned by the shipper to a trusted third party who will release the goods after payment or a promise of payment has been made. However, there is no standard practice to meet the requirements of the shipper in this situation.

It will be up to the shipper in each case to satisfy themselves as to the creditworthiness of the consignee before agreeing to a sale where possession of the goods will be obtained by the buyer prior to payment.

Insurance documents

Depending on when payment is to be made, either the importer or the exporter will have a fi nancial interest in the safe arrival of the goods. Accordingly, the goods should be insured against damage or loss whilst in transit.

There are many types of risks that may be insured against and each of these should be considered at time of shipment. These risks may include strikes, war, riots, civil commotion, theft, pilferage, etc. Other risks pertinent to a particular shipment should also be considered, e.g. if goods are frozen food stuffs, insurance against the malfunction of a refrigerated container will be appropriate.

Responsibility for insurance

The responsibility for arranging insurance will largely depend on the terms agreed to between the buyer and the seller. Either party may arrange the insurance. However, depending on the timing of the payment, the party not arranging the insurance may require evidence that goods are insured prior to making shipment or payment. This aspect is further discussed in ‘Methods of payment, risks’ (page 42).

Offi cial documents

A variety of offi cial documents may be required to meet both the exporting and importing countries’ customs and or foreign exchange regulations.

Documents relating to origin, quality, fumigation, phytosanitary, Halal, health, weight, inspection and import and export licences, are some examples of offi cial documents that may be required. The documentation required to ensure prompt clearance through customs will vary between country, buyer and goods traded. Traders should, therefore, familiarise themselves with the respective import/export regulations in their country.

24

The matter of payment for goods is, appropriately, a point of focus for both importers and exporters.

The two parties involved in negotiations will have confl icting cash fl ow and risk management issues arising from the timing of the proposed payment.

Exporters will seek to receive the highest price for their goods and to receive payment as soon as possible, preferably before the manufacture and shipment of those goods. Importers, on the other hand, will seek the lowest overall costs and deferment of payment for as long as possible, preferably until the goods have been consumed or on-sold.

To further complicate negotiations, exporters will prefer to have control over the goods until after payment is received while importers will prefer to have received, examined and even on sold the goods before making payment.

The negotiations will, therefore, need to balance these confl icting demands to arrive at an acceptable outcome for all parties. Each party’s ability to access fi nance, their preparedness to accept some commercial risk, the trading relationship between the two parties, market forces and exchange control regulations in each party’s country will all play a part in determining the relative strengths of each party in negotiating the timing and method of payment.

To achieve an agreement, both the buyer and seller will need to accept some commercial

risk. It is up to each party to determine what are acceptable commercial risks in the overall transaction and thereby come to an agreement on the timing and method of payment to be used.

As each of the methods of payment, discussed in the following pages, have different types and graduations of risk for both buyer and seller, the risks may be shared between the buyer and seller in a variety of ways. Thus the available methods of payment allow for most negotiations to reach an acceptable compromise.

The methods of payment that are available are as follows:

◆ clean payment/open account;

◆ documentary collection; and

◆ documentary credit.

The following pages examine these three methods of payment. Firstly we defi ne each method of payment and then discuss the initiation of such a payment and the mechanics of its operation within the banking system.

It is important to understand the processes used so that the risks inherent in each payment method are better understood. The more common risks, as defi ned in the earlier chapter, ‘risks in international trade’, are then discussed as they pertain to an importer or exporter for each payment method.

Clean payment/open account

Defi nition

A ‘clean’ payment is a remittance made through a bank by International Money Transfer (i.e. telegraphically) or by the purchase from a bank of a bank draft. (A bank draft should not be confused with a bill of exchange; a bank draft is a cheque issued by a bank usually drawn on an overseas bank. It may be described as an ‘international bank cheque’.)

The International Money Transfer is more frequently used to settle trade debts than bank draft due to its speed of transmission, reliability and that funds, when received by the exporter, are immediately available.

The primary benefi t of a clean payment is that it is a relatively cheap and uncomplicated method of payment for both importers and exporters alike.

Open account is not so much a method of payment as an agreement between the importer and exporter as to the timing of payments.

Open account terms provide simplicity for both buyer and seller in that the buyer is able to place orders for any number of shipments up to an agreed value during an agreed period of time, say USD250,000 per month. The terms of the open account arrangement will also specify when payment for the shipments will be made, e.g. at end of month. A variation on this may be that the importer is

Methods of payments – operations

25

allowed say, 30 days after month’s end to make the payment. As you will appreciate, the existence of a long trouble-free trading history and relationship is an essential requirement for such terms.

Open account transactions are generally settledby a clean payment.

Similarly, prepayments describe the situation where the importer is required to make a clean payment to the exporter prior to the goods/services being shipped or received.

Initiation/implementation

A clean payment is initiated by a request from the importer to their bank. The request, if for an International Money Transfer, will include the seller’s name and bank account details, amount and currency of payment. The importer will also authorise the bank to debit their account for the payment. The importer’s bank will then telegraphically remit the payment to the seller in accordance with the details provided previously by the seller.

The purchase of a bank draft requires a request from the buyer including the exporter’s name and amount and currency of the payment. The importer will also authorise the bank to debit their account for the payment.

The bank draft is then provided to the buyer who will forward it to the seller.

Process within the banking system

In those cases where funds are to be remitted by International Money Transfer, the importer’s bank will remit the funds through its correspondent banks overseas for credit, as clear funds, to the exporter’s account. The exporter, as benefi ciary of the payment, will, in the normal course of business, receive the payment in their account some 2 to 3 days later. However, as the transit time is dependent on the currency remitted, time zones in the relevant countries, the Remitting Bank’s correspondent arrangements, sophistication of communications in the exporters country and the domicile of the exporter’s account, e.g. at a capital offi ce or at a remote branch, delays beyond this period may be encountered.

If the importer requests a Bank Draft, the Bank Draft is prepared by the bank and given to the importer who may post or otherwise arrange for the item to be forwarded to the exporter. The exporter will then be required to deposit the draft into their account and, unless otherwise allowed by their bank, await an appropriate clearance time before being allowed to draw against the item.

Documentary collection

Defi nition

A documentary collection allows the shipping documents to be presented to the buyer through the banking system against the buyer’s payment,

or their promise to pay at a future date, before such shipping documents are released to them.

A documentary collection consists of a bill of exchange and a variety of shipping documents. The shipping documents will usually consist of an invoice, a transport document, possibly an insurance policy, and any other documents required by the buyer or other parties to aid clearance of the goods

If shipping documents are to be released to the buyer against their payment, this is called a sight documentary collection, or documents against payment (D/P).

If shipping documents are to be released to the buyer against their promise of future payment, this is called a term documentary collection, or documents against acceptance (D/A). In these cases, the date for payment is determined by the tenor of the bill of exchange, e.g. 90 days after bill of lading date, and should agree with the terms of sale previously agreed between the buyer and seller.

The promise by the buyer to pay at a future date is obtained by the buyer accepting the bill of exchange upon presentation. The acceptance is evidenced by the buyer endorsing the bill of exchange.

An accepted bill of exchange does not guarantee payment. The buyer may refuse, or be unable, to make payment at maturity. Accordingly, the creditworthiness of the buyer and the country/ transfer risks are points for consideration by the exporter before agreeing to such payment terms.

26

Documentary collections are a widely used payment method and have gained almost universal acceptance. The operations of a documentary collection are governed by the Uniform Rules for Collections (URC) which have been published by the International Chamber of Commerce (ICC). The URC establish the various parties’ rights and obligations under documentary collections and provide a framework for resolving some problems which may arise. The Commonwealth Bank recommends that traders become familiar with the requirements of the URC before transacting business under documentary collections.

The ICC may be contacted on (03) 8608 2261.

Initiation/implementation

A documentary collection whether it be sight or term is initiated by the exporter.

After the buyer and seller have agreed that payment is to be effected by documentary collection, the exporter dispatches the shipment in accordance with the sales contract.

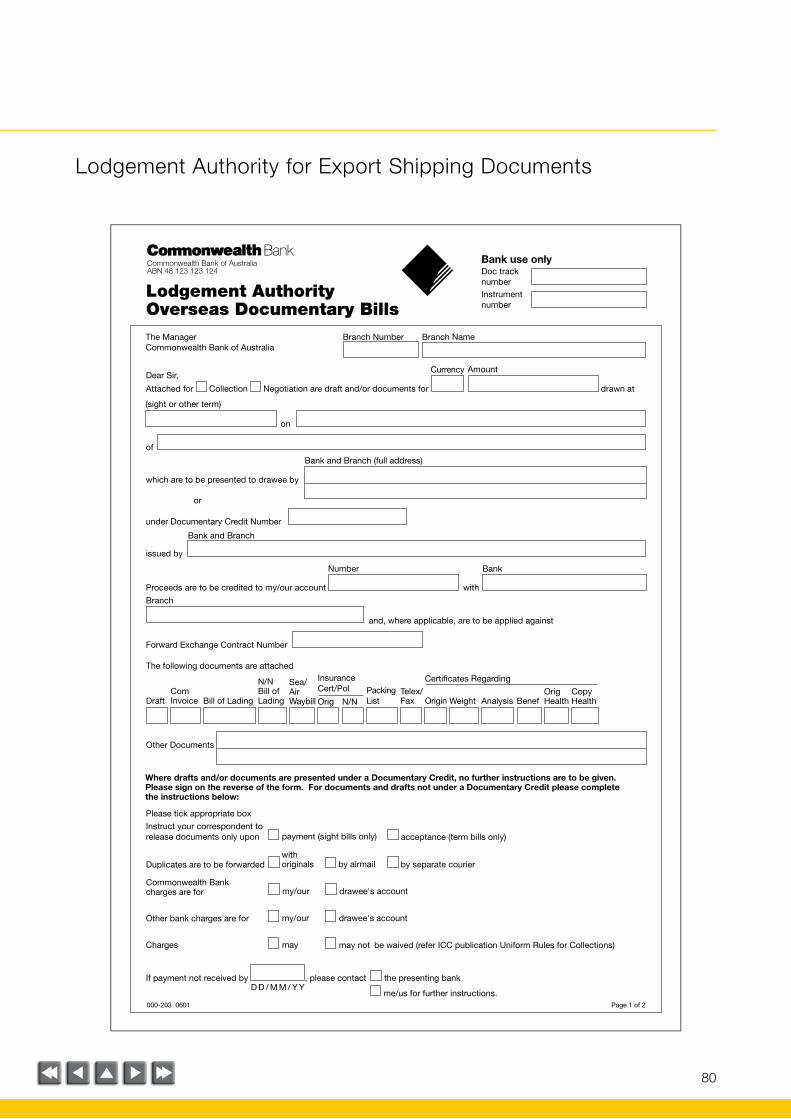

The relative shipping documents accompanied by a completed bill of exchange are lodged by the exporter with their bank. A suitable authority is also submitted with the documents to the bank detailing the exporter’s wishes in regards to the forwarding and release of shipping documents and where proceeds, if received, are to be credited (Fig. 1 page 27).

A copy of the Bank’s standard lodgement authority for documentary collections is shown on pages 80-81.

Importers will await an advice from their bank as to the arrival of the relative documentary collection containing the shipping documents and will respond at that time.

Process within the banking system

After receipt of the shipping documents and the exporter’s instructions by the exporter’s bank (the ‘remitting bank’), they are forwarded to the buyer’s bank (the ‘presenting bank’) in accordance with the exporter’s instructions.

Upon receipt, the presenting bank will act in accordance with the remitting bank’s instructions contained in the schedule prepared by the remitting bank that accompanies the shipping documents.

Accordingly, if the documentary collection is to be paid at sight (D/P), the documents will be presented to the importer for their acceptance and payment (see Fig. 2 page 28). If payment is made, the presenting bank will remit the funds to the remitting bank for fi nal payment to the exporter whilst the shipping documents are released to the importer (see Fig. 3 page 29).

If payment is refused by the importer, the presenting bank will retain the documents and act in accordance with the instructions received from

the remitting bank. The remitting bank will in turn seek instructions from the exporter as to what action is to be taken to collect the amount due. Instructions regarding the storage, insurance, etc. of the goods may also be obtained.

In the case where the documentary collection is term (D/A), the shipping documents will be released to the importer upon their acceptance of the bill of exchange. Acceptance of the bill of exchange serves as an acknowledgment of the debt owing by the importer to the exporter and an undertaking to make payment at the relative maturity date of the bill of exchange. Advice of acceptance, and the maturity date for payment, will be conveyed by the presenting bank to the remitting bank who, in turn, will convey this information to the exporter.

If the importer refuses to accept the bill of exchange the presenting bank will retain the documents and act in accordance with the instructions received from the remitting bank.

At maturity date the presenting bank will re-present the bill of exchange to the importer for payment.

If payment is made, the presenting bank will remit the funds to the remitting bank for payment to the exporter.

If the importer refuses to make payment the presenting bank will retain the bill of exchange and act in accordance with the instructions received from the remitting bank.

27

2. Shipment

1. Contract of sale

1. LODGEMENT OF SHIPPING DOCUMENTS

Buyer (importer) 3. Seller (exporter)

Presenting bank Remitting bank

4. Lodgement of shipping documents

1. Contract of sale as negotiated between the buyer and seller to determine price, quantity, shipment (how, when and where), trading terms, method of payment etc.