Trade Credit Insurance Products - Aman Union · Whole Turnover vs. Selected Cover vs. XoL 12 •...

38

Trade Credit Insurance Products Robert Nijhout 1

Transcript of Trade Credit Insurance Products - Aman Union · Whole Turnover vs. Selected Cover vs. XoL 12 •...

Trade Credit Insurance Products

Robert Nijhout

1

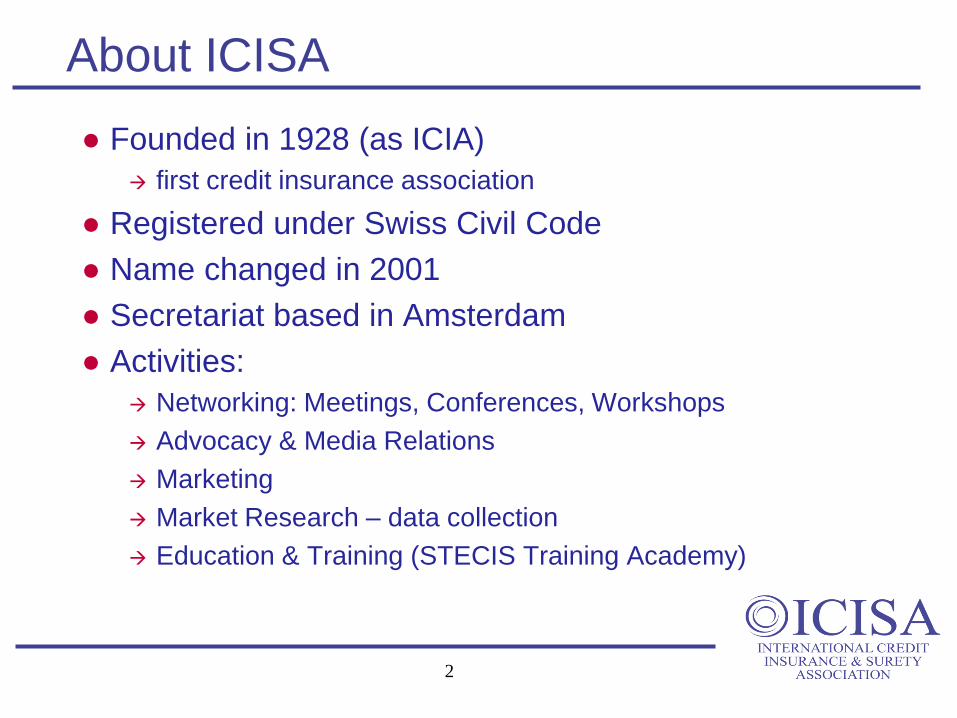

About ICISA

● Founded in 1928 (as ICIA)

first credit insurance association

● Registered under Swiss Civil Code

● Name changed in 2001

● Secretariat based in Amsterdam

● Activities:

Networking: Meetings, Conferences, Workshops

Advocacy & Media Relations

Marketing

Market Research – data collection

Education & Training (STECIS Training Academy)

2

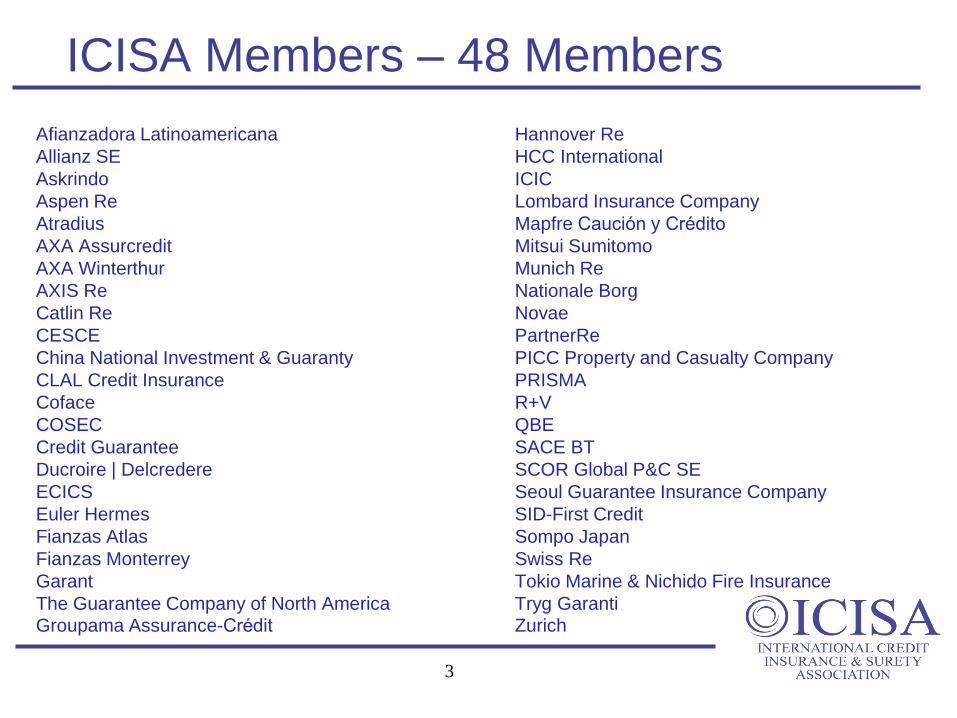

ICISA Members – 48 Members

Afianzadora Latinoamericana Hannover Re

Allianz SE HCC International

Askrindo ICIC

Aspen Re Lombard Insurance Company

Atradius Mapfre Caución y Crédito

AXA Assurcredit Mitsui Sumitomo

AXA Winterthur Munich Re

AXIS Re Nationale Borg

Catlin Re Novae

CESCE PartnerRe

China National Investment & Guaranty PICC Property and Casualty Company

CLAL Credit Insurance PRISMA

Coface R+V

COSEC QBE

Credit Guarantee SACE BT

Ducroire | Delcredere SCOR Global P&C SE

ECICS Seoul Guarantee Insurance Company

Euler Hermes SID-First Credit

Fianzas Atlas Sompo Japan

Fianzas Monterrey Swiss Re

Garant Tokio Marine & Nichido Fire Insurance

The Guarantee Company of North America Tryg Garanti Groupama Assurance-Crédit Zurich

3

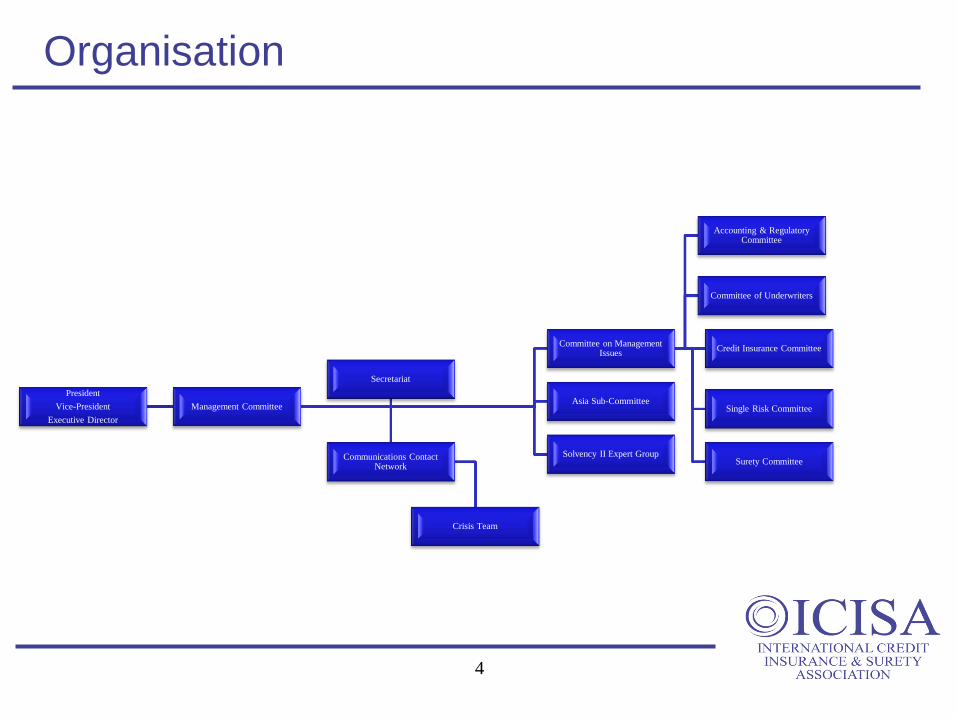

Organisation

4

President

Vice-President

Executive Director

Management Committee

Committee on Management Issues

Accounting & Regulatory Committee

Committee of Underwriters

Credit Insurance Committee

Single Risk Committee

Surety Committee

Asia Sub-Committee

Solvency II Expert Group

Secretariat

Communications Contact Network

Crisis Team

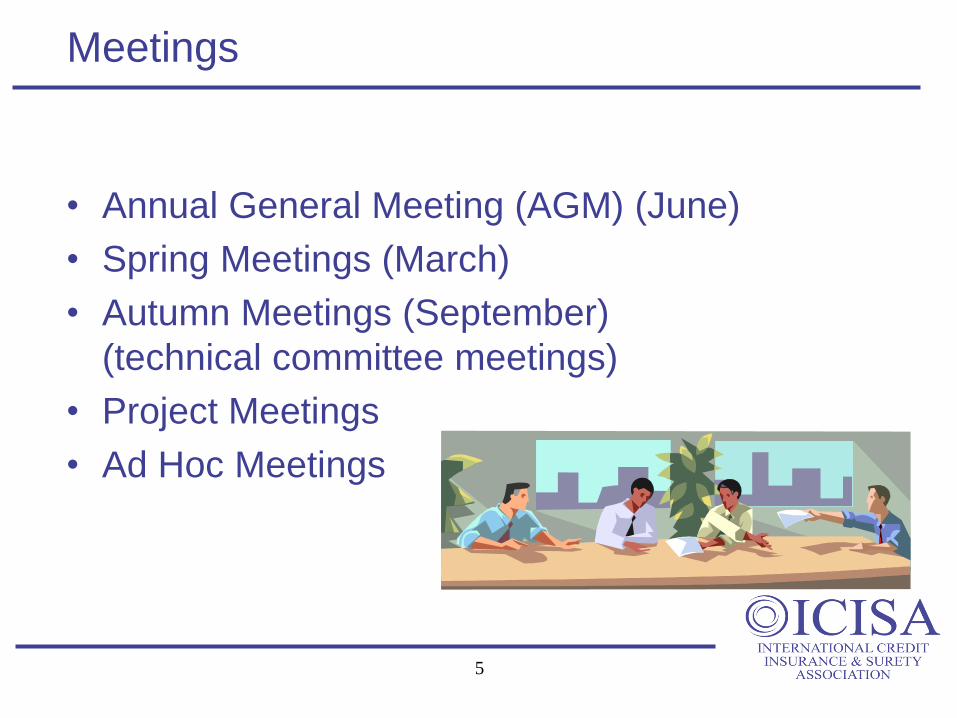

Meetings

• Annual General Meeting (AGM) (June)

• Spring Meetings (March)

• Autumn Meetings (September)

(technical committee meetings)

• Project Meetings

• Ad Hoc Meetings

5

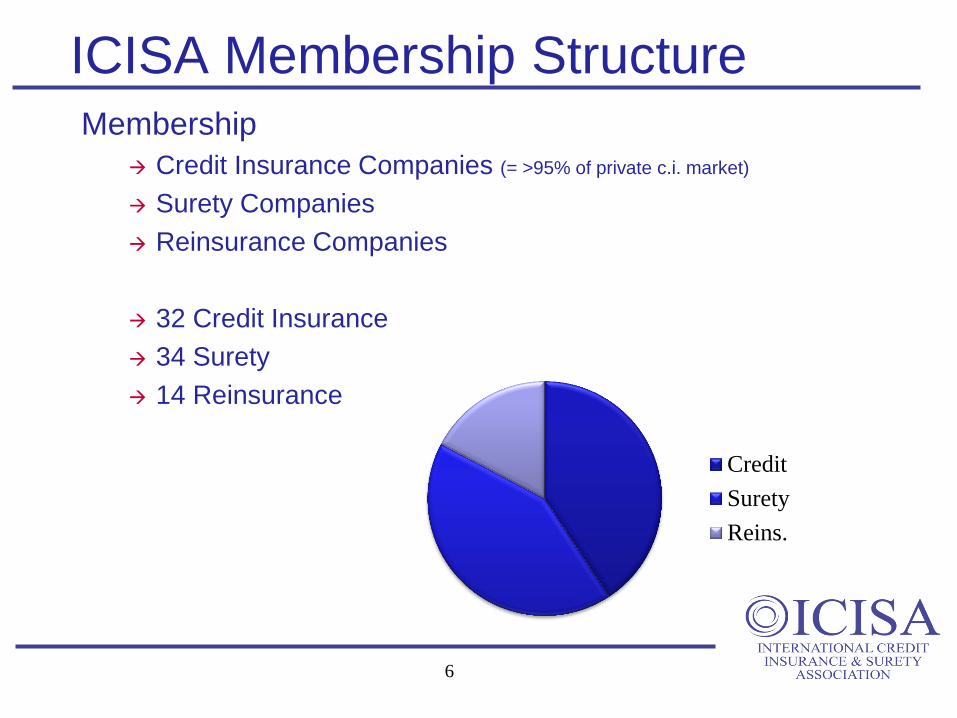

ICISA Membership Structure Membership

Credit Insurance Companies (= >95% of private c.i. market)

Surety Companies

Reinsurance Companies

32 Credit Insurance

34 Surety

14 Reinsurance

Credit

Surety

Reins.

6

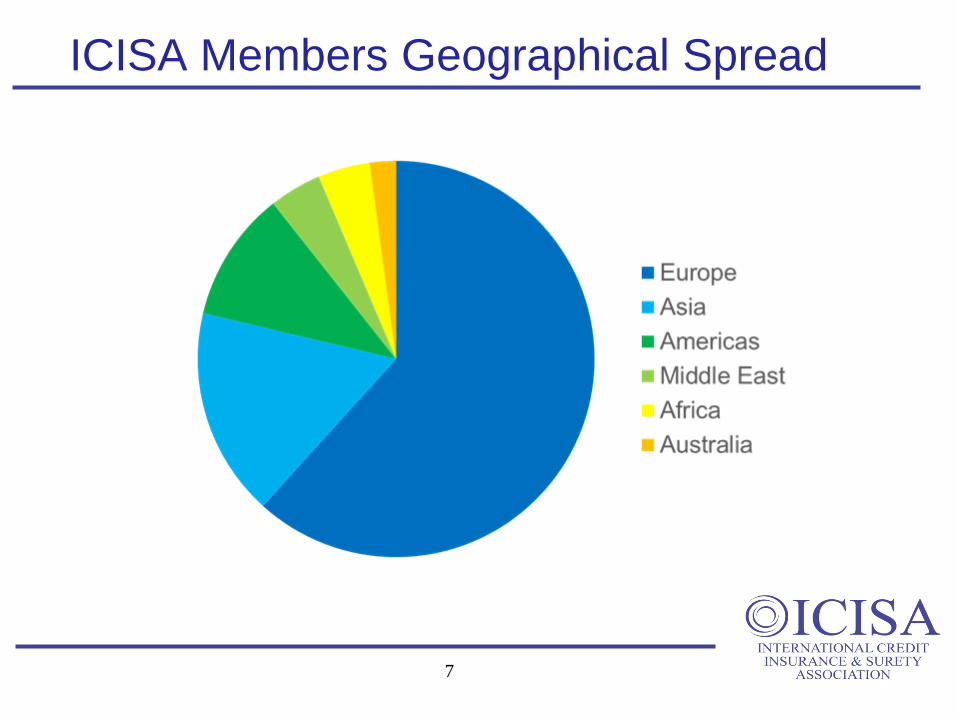

ICISA Members Geographical Spread

7

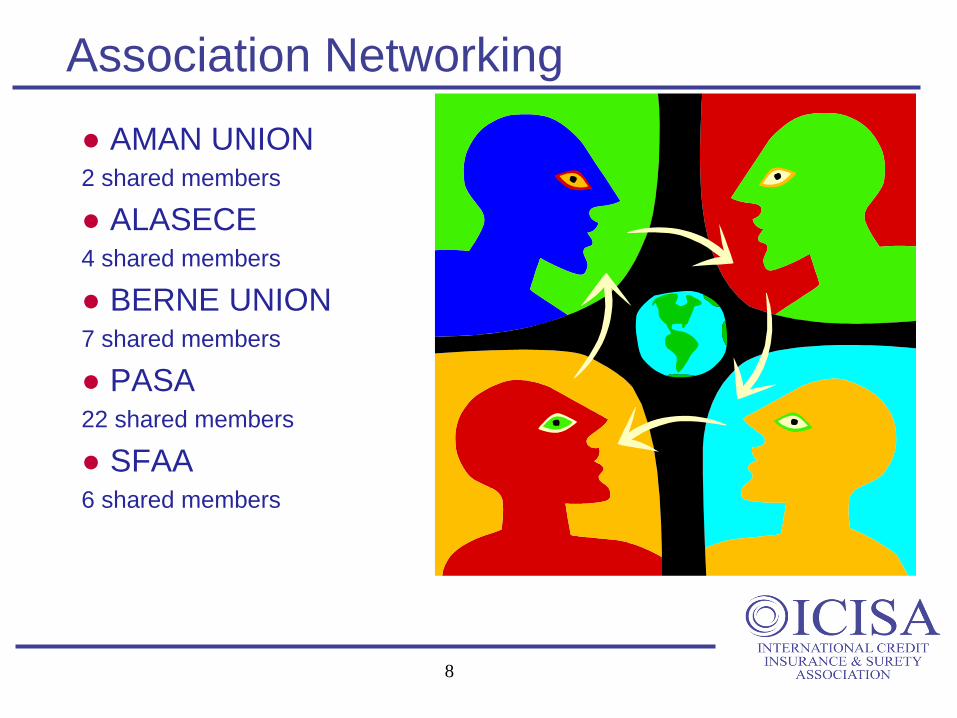

Association Networking

● AMAN UNION 2 shared members

● ALASECE 4 shared members

● BERNE UNION 7 shared members

● PASA 22 shared members

● SFAA 6 shared members

8

Advocacy Partners

• European Union:

• European Commission

• EIOPA

• ECB

• Insurers of Europe

• IASB

• ICC

• OECD

• World Bank

• UNCITRAL

• Media

9

Types of Cover

10

Types of Cover

• “Domestic” is just another country

• Commercial vs. Political Risk

• Whole Turnover vs. Single Risk Cover vs. XoL

• Credit Risk vs. Pre-Credit Risk

• Short-Term vs. Medium Term

11

Whole Turnover vs. Selected Cover vs. XoL

12

• Whole turnover policy

Covers seller’s total credit sales

Cover usually for 80-90%

• Single Risk Cover (single buyer cover)

Cover for all sales to one debtor

or

Cover for a single contract with one debtor

• Excess of Loss (XoL)

Cover in excess of amount of first loss borne by the

insured

First loss / threshold

• Prospecting

• Negotiation about payment condition

• Risk assessment of buyer

• Monitoring of buyer

• Debt collection on buyer

• Loss minimising

13

Additional Services

Trade Credit Insurance

vs.

Financial Guarantee

14

A Financial Guarantee is understood as comprising any bond,

guarantee, indemnity or insurance, covering financial obligations in

respect of any type of loan, personal loan and leasing facility, granted

by a bank/ credit institution, financial institution or financier or issued or

executed in favour of any person or legal entity in respect of the

payment or repayment of borrowed money or any contract transaction

or arrangement – the primary purpose of which is to raise finance or

secure sums due in respect of borrowed money.

By way of explanation, the purpose of this definition is the avoidance of insurance cover for any financial obligation which does not arise from or relates to a trade transaction defined as the supply of goods and/or rendering of services.

15

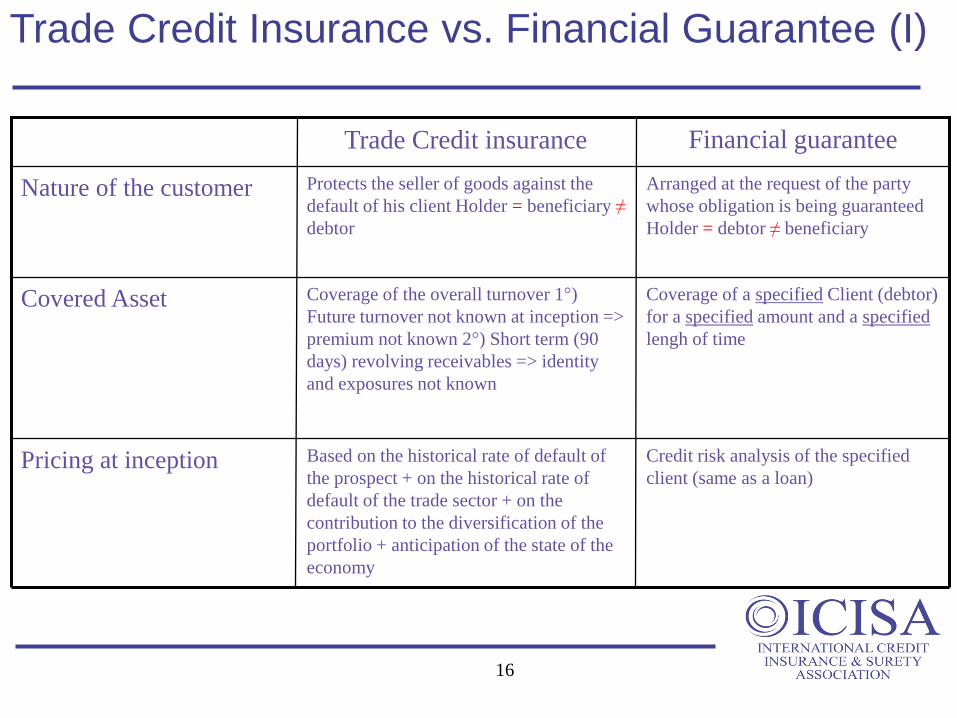

Official ICISA Definition - Financial Guarantee

16

Credit risk analysis of the specified

client (same as a loan)

Based on the historical rate of default of

the prospect + on the historical rate of

default of the trade sector + on the

contribution to the diversification of the

portfolio + anticipation of the state of the

economy

Pricing at inception

Coverage of a specified Client (debtor)

for a specified amount and a specified

lengh of time

Coverage of the overall turnover 1°)

Future turnover not known at inception =>

premium not known 2°) Short term (90

days) revolving receivables => identity

and exposures not known

Covered Asset

Arranged at the request of the party

whose obligation is being guaranteed

Holder = debtor ≠ beneficiary

Protects the seller of goods against the

default of his client Holder = beneficiary ≠

debtor

Nature of the customer

Financial guarantee Trade Credit insurance

Trade Credit Insurance vs. Financial Guarantee (I)

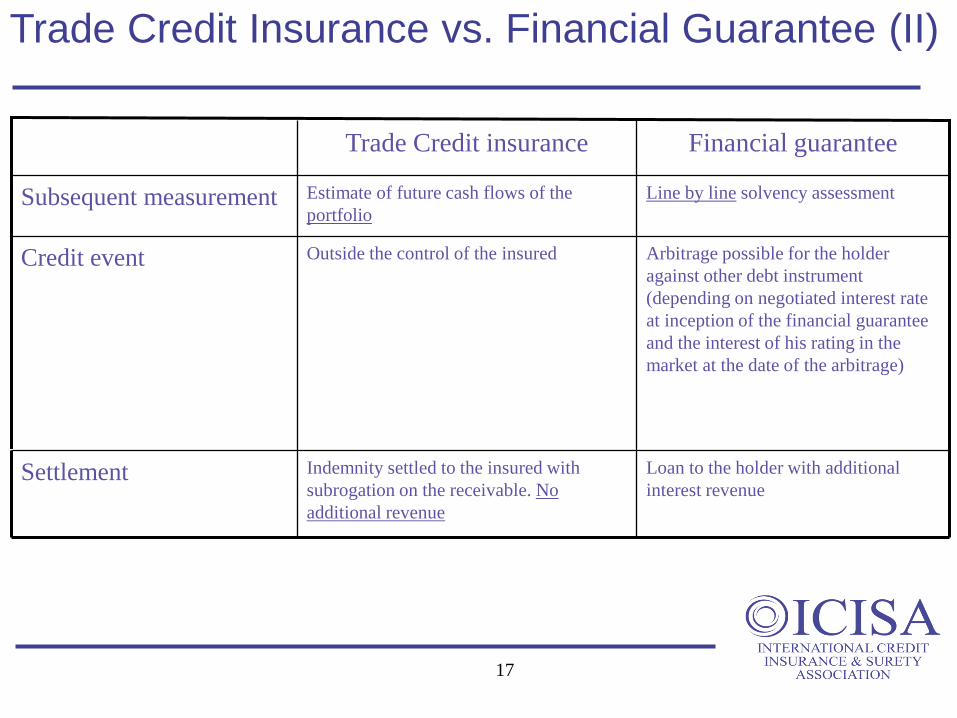

Loan to the holder with additional

interest revenue

Indemnity settled to the insured with

subrogation on the receivable. No

additional revenue

Settlement

Arbitrage possible for the holder

against other debt instrument

(depending on negotiated interest rate

at inception of the financial guarantee

and the interest of his rating in the

market at the date of the arbitrage)

Outside the control of the insured Credit event

Line by line solvency assessment Estimate of future cash flows of the

portfolio Subsequent measurement

Financial guarantee Trade Credit insurance

Trade Credit Insurance vs. Financial Guarantee (II)

17

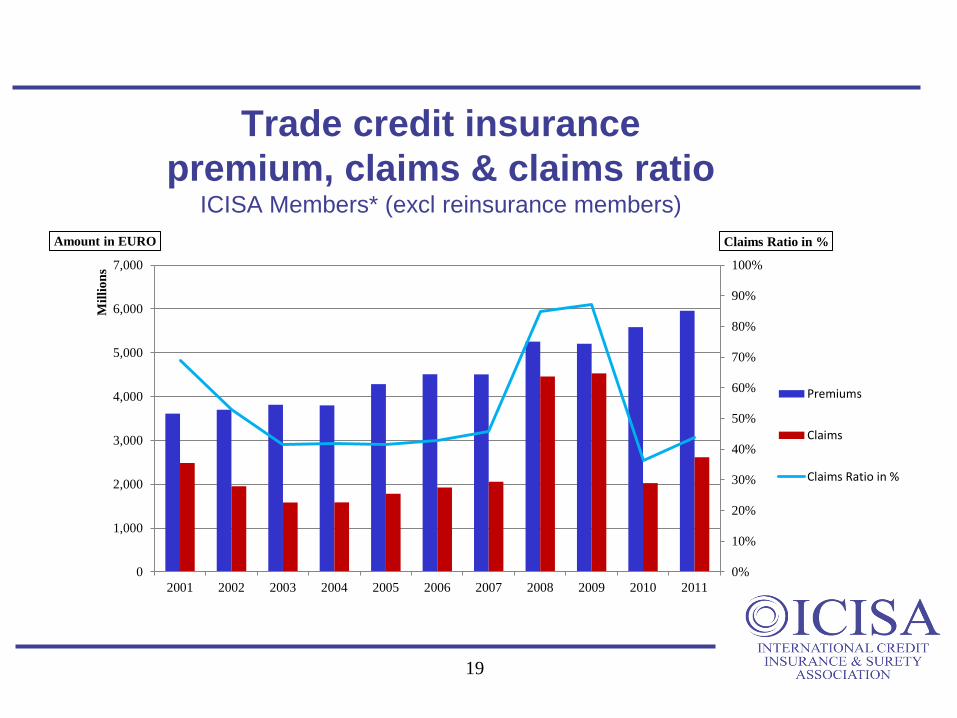

ICISA Trade Credit Insurance Members Results 2011

• Premium: € 5.961 million

• Claims: € 2.615 million

• Claims Ratio: 43.9%

• Insured Exposure: € 1.658 billion

18

Trade credit insurance

premium, claims & claims ratio ICISA Members* (excl reinsurance members)

19

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Claims Ratio in % Amount in EURO

Mil

lio

ns

Premiums

Claims

Claims Ratio in %

Trade credit insurance

Insured Exposure ICISA Members* (excl reinsurance members)

20

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2005 2006 2007 2008 2009 2010 2011

Bill

ion

s

Insured ExposureTrade Credit Insurance

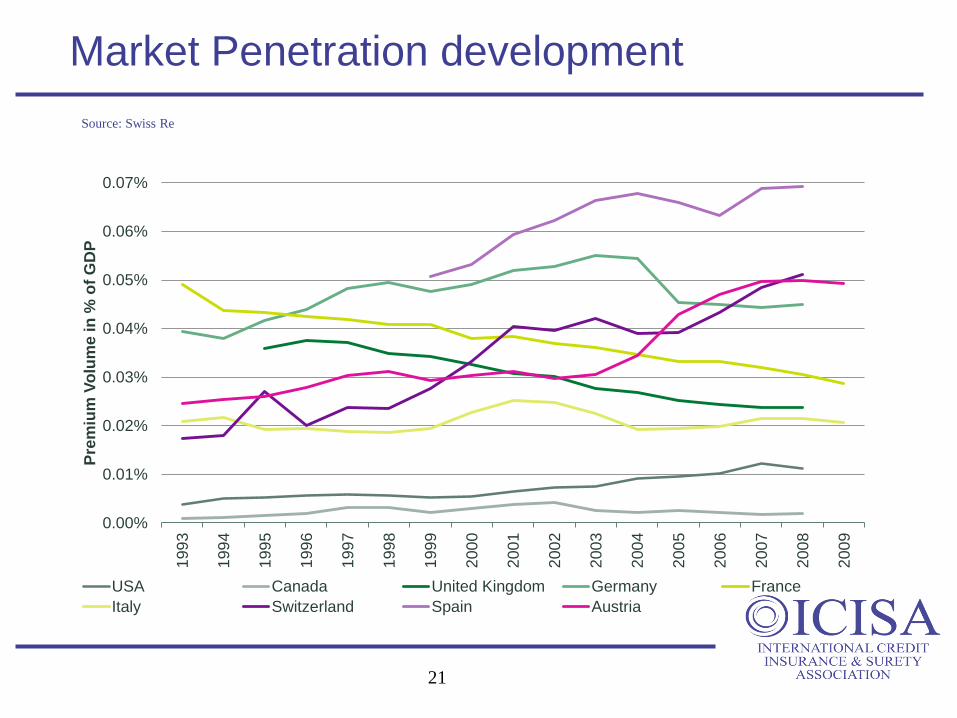

Market Penetration development

Source: Swiss Re

0.00%

0.01%

0.02%

0.03%

0.04%

0.05%

0.06%

0.07%1

99

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

Pre

miu

m V

olu

me

in

% o

f G

DP

USA Canada United Kingdom Germany France

Italy Switzerland Spain Austria

21

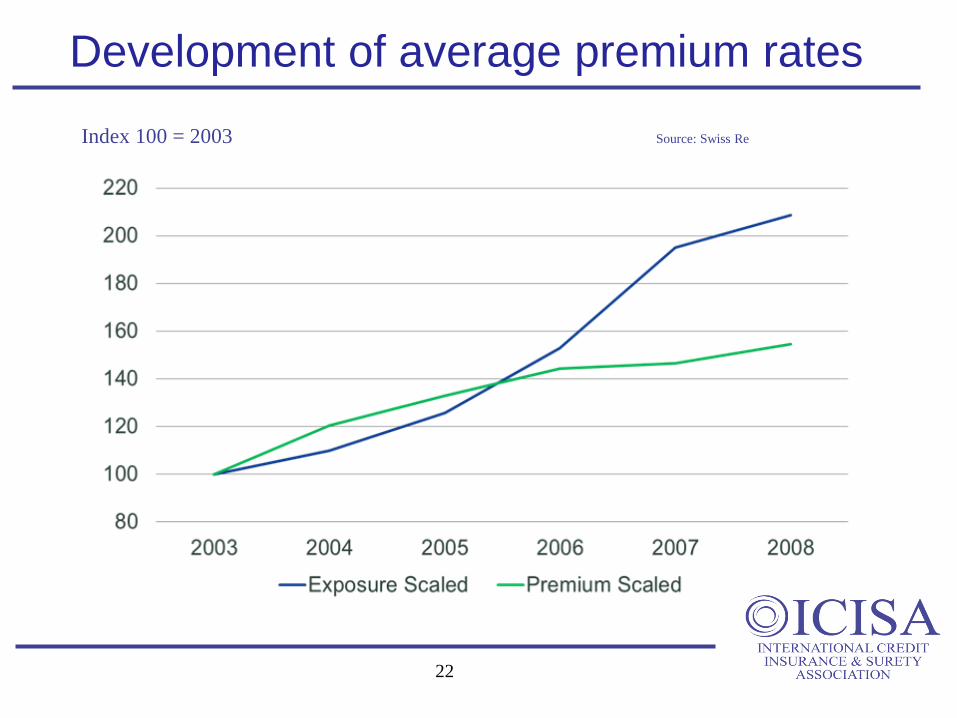

Development of average premium rates

Index 100 = 2003 Source: Swiss Re

22

Lessons learned from the crisis

● Trade credit insurance is cyclical, driven by the economic environment

● Mitigate negative impact when cycle turns - policy terms/conditions and active monitoring

● Diversified portfolios are less vulnerable

● Identify a potential down-turn timely and take appropriate measures both on the risk and policy side

● For 2013, measures should have been taken in 2012

● Premium rates need to be risk adjusted to be able to absorb higher loss in bad years

● Alignment of interest between policy holder and underwriter; retentions (>15%), aggregate limits and deductibles

● Make the cake bigger, through e.g. product innovation

● Transparency

● Consultancy role – “much more than insurance”

23

Single Risk Cover and the crisis

• The market fared well during the 2008-2009 global slump:

passed the stress test despite higher claims severity one player withdrew

PRI market uptrend resilient showing rapid premium growth

ample capacity available two years later

• The last crisis recognized as largest loss occurrence met by the

private market since its development

• “Pure” Political Risk coverage hardly affected

• Single Risk Debtor coverage remains bulk of major claims.

• Unclear overall picture total claims during the period: • est. between 1.5 and 3 billion USD.

24

Lessons learned from claims

Recovery potential is at the heart of the PRI private market

• One of the most important aspect of PRI underwriting is about

determining if there is a basis for securities and potential recovery.

• Claims related to Single Risk private Debtor raised several issues

after crisis:

conflicts of local jurisdictions, notably with the emerging

countries;

hard time for the Insurers in being entitled to exercise their

rights belonging to the Insured in foreign jurisdictions;

narrow border between Sovereign Buyer / Private Buyer;

convergence of interests between private operators and ECAs

in claim management still existing but limited common

approach.

25

Bite the bullet

In the wake of the crisis, there is momentum forward-thinking on our

business practices and reviewing the concrete and legal issues that we have

to deal with:

• Refocus on definition and scope of PRI products. What about emerging

non-trade related issue?

• Pursue innovation in products to meet new clients’ expectations as banks

growing needs.

• Improve policy wordings with regard to law and jurisprudence evolution

and market practices.

• Enforce recovery process (subrogation clause).

• Principle of a separate treatment of commercial debt and financial debt

towards multilaterals?

26

The ICISA initiative

To better assess the efficiency of our industry, we should improve our market standards and practices, enhance data transparency and better structure the market to address the major challenges the PRI has to deal with.

• In June 2009, ICISA sets up a new committee for “non-traditional credit insurance

business” launched under the influence of single risk insurance providers, members

of ICISA.

• The ICISA Single Risk Committee organizes an annual meeting with Lloyds’s,

ECAs and market political risk insurers that are not members of ICISA. Broadest

representation of the Single Risk Market.

• The SRC has launched a number of important initiatives such as a market survey, a

classification on product types as well as the terminology catalogue.

• Current concern: the principle of separate treatment of commercial debt vs.

financial debt with the view that UNCTAD, the UN and the ICC acknowledge this

principle in their standards in conformity with current practices.

27

The Current Market

Where are we now?

Hardening market

Ample reinsurance capacity

Premium income rising

Insolvencies increasing

Claims increasing: frequency – average claims size

Current crisis political (EU/USA)

Sovereign risk – ability to support

Trade Finance: lack of trust + Basle II & III

Growth in Asia & L America

Clients’ expectations

28

The Current Market

What are the consequences?

Mismatch between risk and premium

Reliability

Transparency

29

The Current Market

What is the role of a private trade credit insurer?

Support the economy?

Support its clients?

Protect its shareholders?

Job security?

All of the above?

30

The future of Trade Credit Insurance

● Internal:

Entry-level for new players is high

Differing risk perception: low rates vs. high risks

Shareholders changing demands

● External:

Effects of the crisis (euro? inflation? recovery?)

Solvency II favours diversified insurers

Ample reinsurance capacity

31

New Products

● Do we need new products?

● Excess of loss

● Cancellable/non-cancellable limits

● Benchmark:

Risk syndication

New risks – identify market concerns:

Environment

Sovereign/Political

32

New Players, New Challenges

● New underwriters – New reinsurers - Driver:

Ability

Capacity

Opportunity

● Negative economic outlook

Country risk concerns

Crunch in trade finance

Increasing claims - soft market

● New territories:

BRICs

Eastern Europe

Asia

33

Current Issues and Concerns

● Advocacy

Solvency II / CAT Risk

Accounting Standards (IFRS4)

Marketable Risks in the E.U.

Shadow Banking in the E.U.

Lack of financial information - E.U. and China

India: restrictions on underwriting trade credit

● Media & Communication:

Communication Contacts Network

Crisis Team

Asia Team

34

ICISA Media & Communication

Press

Press conference calls

Press releases

Press meetings/ Press tour

Publications

Newsletter

Yearbook

Catalogue of Terms

Positioning papers

Book on trade credit insurance

Social Media

Communication Contacts Network

Crisis Team

Asia Team

One Pagers

35

ICISA / JAN 2012 / General

Education and Training

Training Seminars:

– Two-Day Seminars: Basic + Advanced

– Open Standard Seminars

– In-House customised Seminars

– One-Day Fly-In-Fly-Out

36

ICISA / JAN 2012 / General

Training Seminars 2013

20 – 22 March 2013

• Credit Insurance – Basic

• Surety – Basic

12 – 14 June 2013:

• Credit Insurance – Advanced

• Surety - Advanced

37