Three Challenges in the U.S. Labor Market: Participation ...

31

Three Challenges in the U.S. Labor Market: Participation, Inequality, and Fluidity Jason Furman Chairman, Council of Economic Advisers World Bank Group January 28, 2016

Transcript of Three Challenges in the U.S. Labor Market: Participation ...

Three Challenges in the U.S. Labor Market:

Participation, Inequality, and Fluidity

Jason FurmanChairman, Council of Economic Advisers

World Bank GroupJanuary 28, 2016

Overview

1

1. Strength of the Labor Market Recovery

2. Three Long-Standing Challenges:a) Labor Force Participationb) Income Inequalityc) Labor Market Fluidity

3. (Brief) Policy Implications

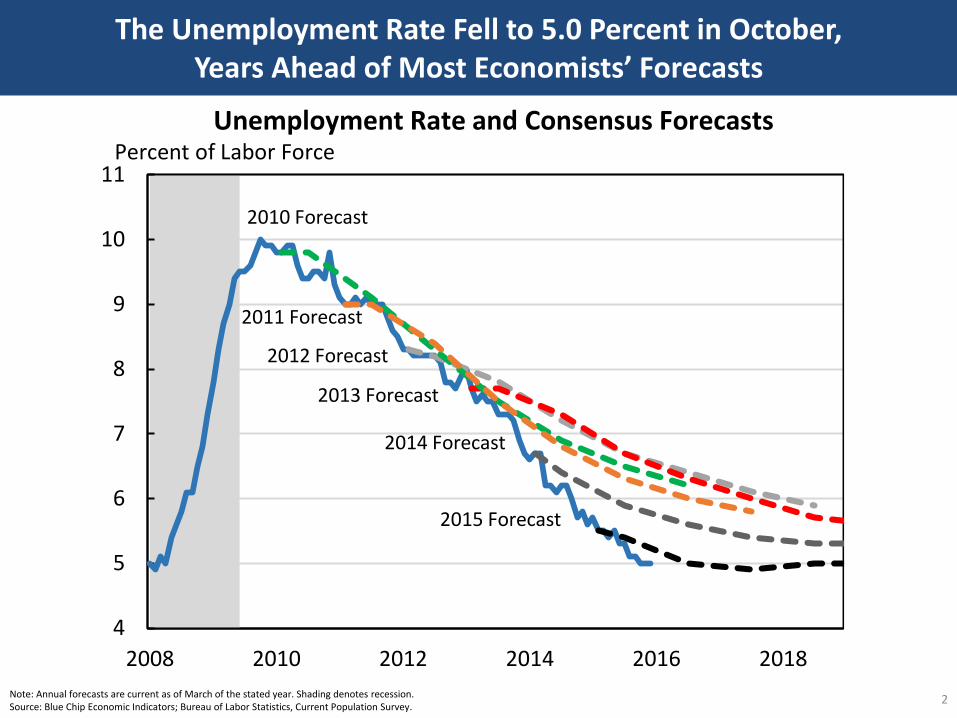

The Unemployment Rate Fell to 5.0 Percent in October,Years Ahead of Most Economists’ Forecasts

2Note: Annual forecasts are current as of March of the stated year. Shading denotes recession.Source: Blue Chip Economic Indicators; Bureau of Labor Statistics, Current Population Survey.

4

5

6

7

8

9

10

11

2008 2010 2012 2014 2016 2018

2012 Forecast

2013 Forecast

2014 Forecast

2011 Forecast

2010 Forecast

Unemployment Rate and Consensus ForecastsPercent of Labor Force

2015 Forecast

Labor Market Recovery is Broad Based, But Still Some Elevation in the Broadest Measures and Long-term Unemployment

3Note: Unemployment rates by education are for persons age 25+. All other rates for persons age 16+ unless noted. Source: Bureau of Labor Statistics; CEA calculations.

91

120

90

102

103

111

103

121

103

109

103

106

326

64

87

84

92

89

99

72

99

74

106

90

28

-13

8

-2

-2

-10

-3

-15

-3

-7

-3

-5

-50 0 50 100 150 200 250 300 350

Long-Term UR

Short-Term UR

U-6 (U-5 + Part-Time for Economic Reasons)

U-5 (U-4 + Other Marginally Attached)

U-4 (U-3 + Discouraged)

Asian UR

Hispanic UR

Black UR

White UR

Female UR

Male UR

Overall Unemployment Rate (UR)

Remaining Elevation as of December 2015 Percent Increase to Great Recession Peak Percent Recovered

Percent Change in Indicator Relative to 2001-07 Average

Tracking the Recovery Across Labor Market IndicatorsAll Data as of December 2015

Nominal Wages are Rising Somewhat Faster Than Earlier in the Recovery, and Low Inflation is Boosting Real Wage Growth

4

Average Hourly Earnings for all Private Workers (Dec-15)

2010-2014Average

Consumer Price Index - All Urban Consumers

(Nov-15)

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2011 2012 2013 2014 2015 2016

Average Hourly Earnings Growth and Consumer Inflation12-Month Percent Change

Source: Bureau of Labor Statistics; CEA calculations.

The First Challenge: Labor Force Participation

5Note: Shading denotes recession.Source: Bureau of Labor Statistics.

Employment-Population Ratio

Dec-15

Labor Force Participation Rate

55

60

65

70

1950 1960 1970 1980 1990 2000 2010

Labor Force Participation and Employment-Population RatesPercent

Four Potential Explanations of the Decline in Labor Force Participation

6

The labor force participation rate fell 3.4 percentage points from 2007-Q4 to 2015-Q4. This can be attributed to:

Structural1. Aging of the population. This is the mechanical impact of, for example, having fewer

55-59 year olds (male LFPR = 77%) and more 70-74 year olds (male LFPR = 23%).

2. Non-aging trends. Male participation rates have been declining since the early 1950s and female participation rates have been declining since the late 1990s.

Cyclical3. Normal business cycle. Historically, for every 1 percentage point elevation in the

unemployment rate, the participation rate is 0.1 to 0.2 percentage points lower.

4. Unusual business cycle. The Great Recession was unusually severe and hit a labor market that has undergone structural changes, making the cyclical impact different.

Note – CEA’s statistical analysis combines 2 and 4 as a residual.

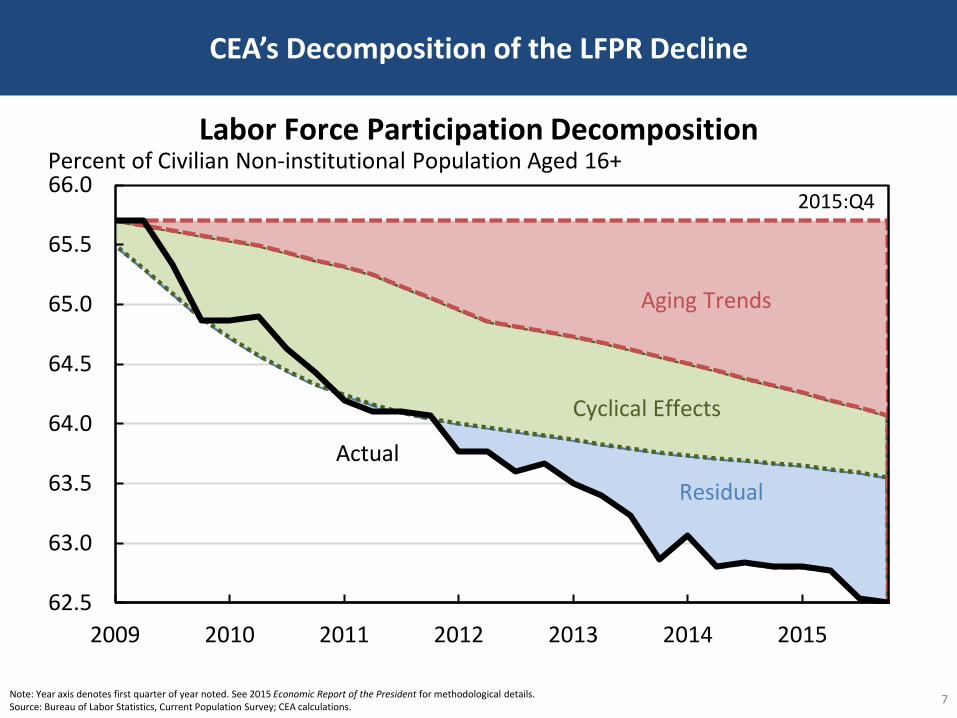

CEA’s Decomposition of the LFPR Decline

7Note: Year axis denotes first quarter of year noted. See 2015 Economic Report of the President for methodological details.Source: Bureau of Labor Statistics, Current Population Survey; CEA calculations.

62.5

63.0

63.5

64.0

64.5

65.0

65.5

66.0

2009 2010 2011 2012 2013 2014 2015

Labor Force Participation DecompositionPercent of Civilian Non-institutional Population Aged 16+

Residual

Aging Trends

Cyclical Effects

Actual

2015:Q4

The Case for the Residual Being Unusual Business Cycle (i.e. Hopefully Cyclical)

8

62.5

63.0

63.5

64.0

64.5

65.0

65.5

66.0

66.5

67.0

2009 2010 2011 2012 2013 2014

Labor Force Participation DecompositionIncluding Mean Duration of Unemployment

Percent

Remaining Residual

Other Effects

Mean Duration

Actual

Unemp.

Gap

Unemp.

Gap (t-4)

Unemp.

Gap (t-8)

Mean

Duration

Mean

Duration

(t-4)

Mean

Duration

(t-8)

-0.0330* 0.00429 0.0151 -0.00406 -0.0142* 0.00222

(0.00914) (0.0146) (0.0114) (0.00534) (0.00524) (0.00527)

Independent Variables (Year-over-Year Differences)

Regression of Quarterly Differences in Detrended Participation Rate

Note: Regression is estimated using data from 1960:Q1 to 2014:Q2. Newey-West standard errors using a maximum lag of 12 are reported in parentheses. Participation rate and unemployment gap are detrended using the procedure described in Appendix A. F-tests are joint significance tests of the disability insurance, mean duration, and schooling variables. * p<0.01.Source: Bureau of Labor Statistics; CEA calculations.

The Case for the Residual Being Non-aging Trends (i.e. Structural)

9Source: Bureau of Labor Statistics; Aaronson et al. (2006); CEA calculations.

Actual (Annual

Average)

2015

Aaronson et al. 2006 Projections Based on

Structural Trends

62

63

64

65

66

67

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Labor Force Participation vs. Pre-Crisis Structural ProjectionsPercent of Civilian Non-institutional Population Age 16+

Overall

Men

Dec-15

Female

30

40

50

60

70

80

90

1950 1960 1970 1980 1990 2000 2010

Labor Force Participation by GenderPercent of Civilian Non-institutional Population Age 16+

Structural Declines in Employment-Population Ratios

10Note: Shading denotes recession.Source: Bureau of Labor Statistics; CEA calculations.

Prime-Age (25-54) Female Employment-

Population Ratio

1948-2007Trend

Dec-15

30

40

50

60

70

80

90

1950 1960 1970 1980 1990 2000 2010

Prime-Age Female Employment-Population RatioPercent

2000-2007 Trend

Prime-Age (25-54) Male Employment-Population

Ratio

1948-2007Trend

Dec-15

80

85

90

95

100

1950 1960 1970 1980 1990 2000 2010

Prime-Age Male Employment-Population RatioPercent

Canada

France

Germany

Italy

Japan

2014

United Kingdom

United States

86

88

90

92

94

96

98

100

1990 1995 2000 2005 2010 2015

Prime-Age Male Labor Force Participation RatesPercent

CanadaFrance

2014

Germany

Italy

Japan

United Kingdom

United States

50

60

70

80

90

1990 1995 2000 2005 2010 2015

Prime-Age Female Labor Participation RatesPercent

Prime-Age LFPR Across G-7 Economies

11Source: Organisation for Economic Co-operation and Development.

30

40

50

60

70

80

90

100

Slo

ven

iaSw

eden

Icel

and

Po

rtu

gal

Swit

zerl

and

Au

stri

aN

orw

ayD

enm

ark

Fran

ceFi

nla

nd

Ge

rman

ySp

ain

Ne

the

rlan

ds

Can

ada

Esto

nia

Cze

ch R

epu

blic

Luxe

mb

ou

rgB

elgi

um

Slo

vak

Rep

ub

licU

nit

ed K

ingd

om

Po

lan

dN

ew

Ze

alan

dH

un

gary

Isra

el

Au

stra

liaG

reec

eJa

pan

Un

ited

Sta

tes

Irel

and

Ch

ileIt

aly

Ko

rea

Mex

ico

Turk

ey

Prime-Age Female Labor Force ParticipationPercent of Population

80

85

90

95

100

Cze

ch R

epu

blic

Jap

anSw

itze

rlan

dLu

xem

bo

urg

Mex

ico

Slo

vak

Rep

ub

licSw

eden

Gre

ece

Fran

ceIc

elan

dG

erm

any

Au

stri

aSl

ove

nia

Spai

nC

hile

Esto

nia

Ne

the

rlan

ds

Un

ited

Kin

gdo

mN

ew

Ze

alan

dP

ort

uga

lB

elgi

um

Ko

rea

Can

ada

Den

mar

kA

ust

ralia

Turk

ey

Po

lan

dFi

nla

nd

Irel

and

Hu

nga

ryN

orw

ayU

nit

ed S

tate

sIt

aly

Isra

el

Prime-Age Male Labor Force ParticipationPercent of Population

Prime-Age LFPR Across OECD Economies

12Source: Organisation for Economic Co-operation and Development.

U.S. Labor Market Has High Flexibility But Low Supportiveness

13Source: Organisation for Economic Co-operation and Development.

OECD Measures of Institutional Labor Market SupportUS Percentile Rank

(100=Most Supportive)

Expenditure on Active Labor Market Policies 3

Net Childcare Costs, Lone Parent 6

Implicit Rax on Returning to Work, Lone Parent 9

Unemployment Benefits (1 Year) 11

Unemployment Benefits (5 Years) 11

Number of Weeks Lost Due to Sick Leave 11

Net Childcare Costs, Couples 13

Implicit Tax on Returning to Work, 2nd Earner 13

Tax Wedge: Single Earner vs. Second-Earner Couples 25

Public Expenditure for Childcare 29

OECD Measures of Labor Market FlexibilityUS Percentile Rank

(100=Most Flexible)

Overall Labor Market Regulation 100

Employment Protection for Regular Employment 100

Scope of State Intervention 94

Minimum Cost of Labor 92

Coverage of Collective Bargaining Agreements 90

Labor Taxation 71

Barriers to Entrepreneurship 62

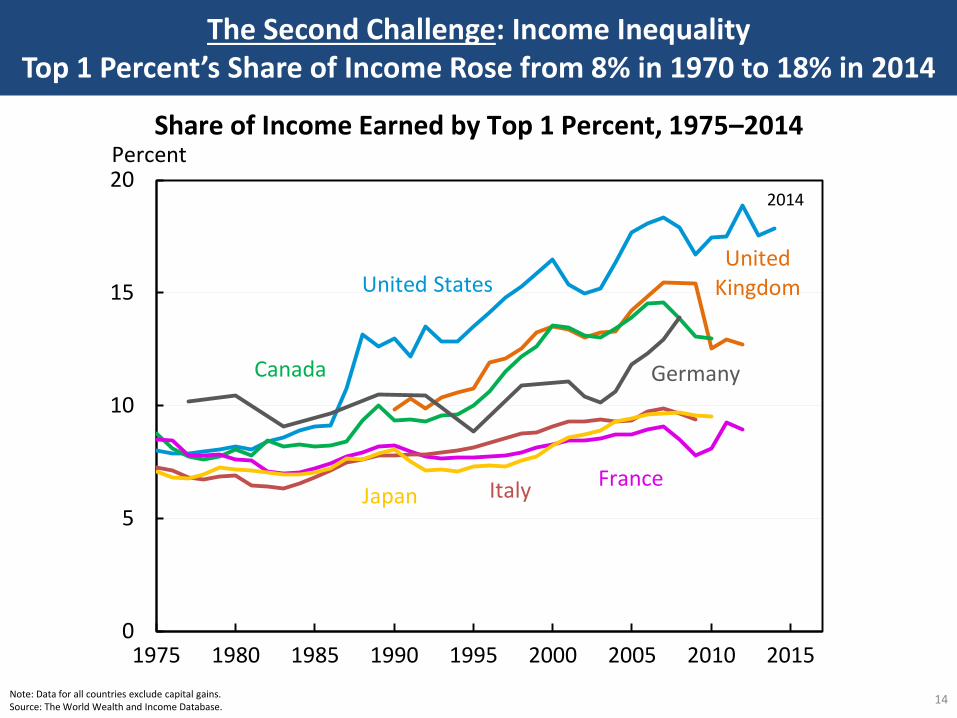

The Second Challenge: Income InequalityTop 1 Percent’s Share of Income Rose from 8% in 1970 to 18% in 2014

14Note: Data for all countries exclude capital gains. Source: The World Wealth and Income Database.

United States

2014

Canada

FranceItalyJapan

Germany

0

5

10

15

20

1975 1980 1985 1990 1995 2000 2005 2010 2015

Share of Income Earned by Top 1 Percent, 1975–2014Percent

United Kingdom

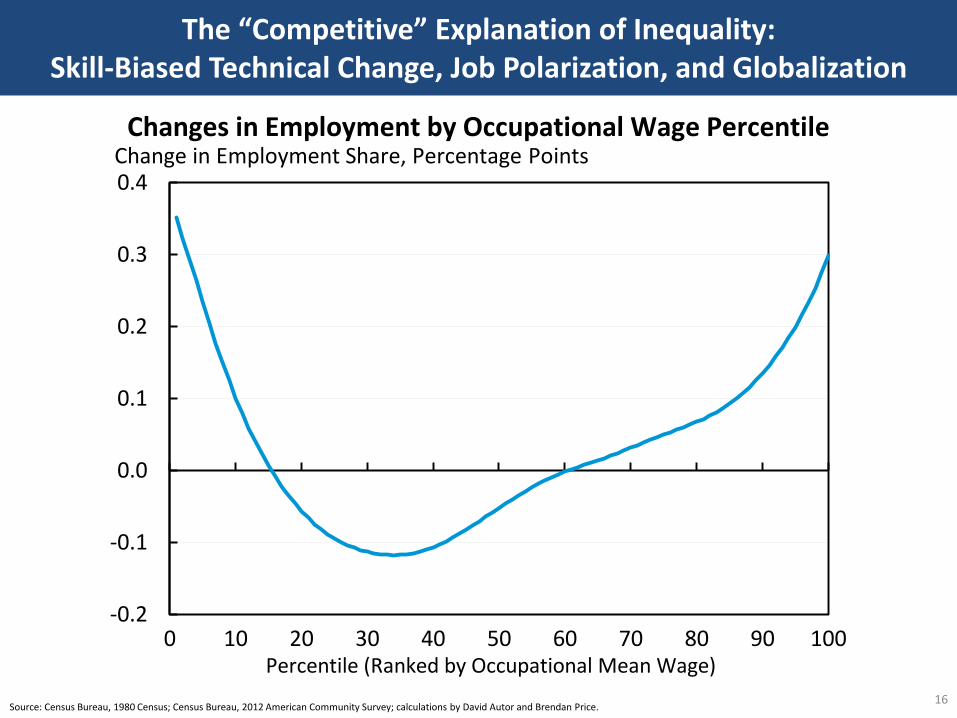

The “Competitive” Explanation of Inequality:Skill-Biased Technical Change, Job Polarization, and Globalization

15Note: Excludes five small outlier occupational categories.Source: Bureau of Labor Statistics, Current Population Survey; CEA calculations.

Machine Operators

Secretaries, Stenographers,

and Typists

Service Occupations, Except Protective

and Household

Technicians and Related Support

Occupations

Teachers, Except Postsecondary

Management-Related Occupations

Executive, Administrative, and Managerial

Occupations

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

$10 $14 $18 $22 $26 $30Average Hourly Wage, 1989 (in 2014 Dollars)

Change in Employment by Detailed Occupation, 1989–2014Change in Total Employment, Thousands

The “Competitive” Explanation of Inequality:Skill-Biased Technical Change, Job Polarization, and Globalization

16

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0 10 20 30 40 50 60 70 80 90 100Percentile (Ranked by Occupational Mean Wage)

Changes in Employment by Occupational Wage PercentileChange in Employment Share, Percentage Points

Source: Census Bureau, 1980 Census; Census Bureau, 2012 American Community Survey; calculations by David Autor and Brendan Price.

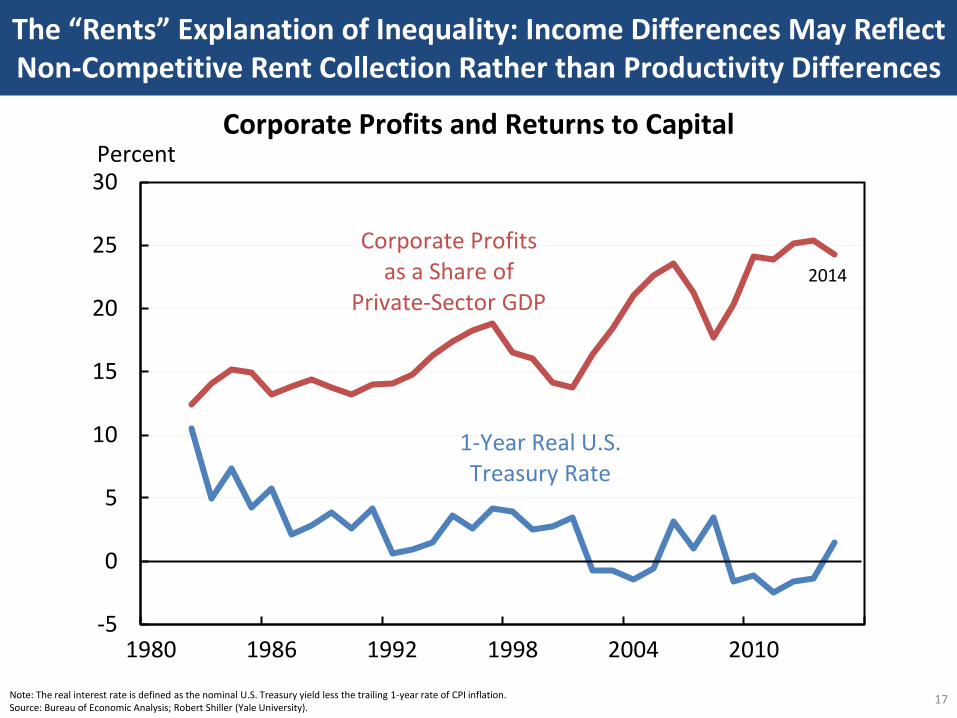

The “Rents” Explanation of Inequality: Income Differences May Reflect Non-Competitive Rent Collection Rather than Productivity Differences

17

1-Year Real U.S. Treasury Rate

Corporate Profits as a Share of

Private-Sector GDP2014

-5

0

5

10

15

20

25

30

1980 1986 1992 1998 2004 2010

Corporate Profits and Returns to CapitalPercent

Source: Bureau of Economic Analysis; Bloomberg Professional Service.Note: The real U.S. Treasury rate is defined as the nominal rate less CPI inflation.

Note: The real interest rate is defined as the nominal U.S. Treasury yield less the trailing 1-year rate of CPI inflation.Source: Bureau of Economic Analysis; Robert Shiller (Yale University).

The “Rents” Explanation of Inequality: Income Differences May Reflect Non-Competitive Rent Collection Rather than Productivity Differences

18

IndustryPercentage Point Change in Revenue Share Earned

by 50 Largest Firms, 1997-2007

Transportation and Warehousing 12.0

Retail Trade 7.6

Finance and Insurance 7.4

Real Estate Rental and Leasing 6.6

Utilities 5.6

Wholesale Trade 4.6

Educational Services 2.7

Accommodation and Food Services 2.6

Professional, Scientific and Technical Services 2.1

Administrative/Support 0.9

Other Services, Non-Public Admin -1.5

Arts, Entertainment and Recreation -2.3

Health Care and Social Assistance -3.7

Source: Census Bureau, Concentration Ratios.

The “Rents” Explanation of Inequality: Declining Union Membership May be Driven by and May Contribute to Rent-Seeking Behavior

19Note: Total employment from 1901 to 1947 is derived from estimates in Weir (1992). For 1948 to 2014, employment data are annual averages from the monthly Current Population Survey.Source: Troy and Sheflin (1985); Bureau of Labor Statistics, Current Population Survey; Weir (1992); CEA calculations.

Troy and Sheflin (1985) CPS:

Membership

2014

0

10

20

30

40

50

60

1917 1937 1957 1977 1997 2017

Union Membership as Share of Total Employment and Share of Income Accruing Top 10 Percent of Income Distrubtion

Percent

Top 10 Percent Share of Income

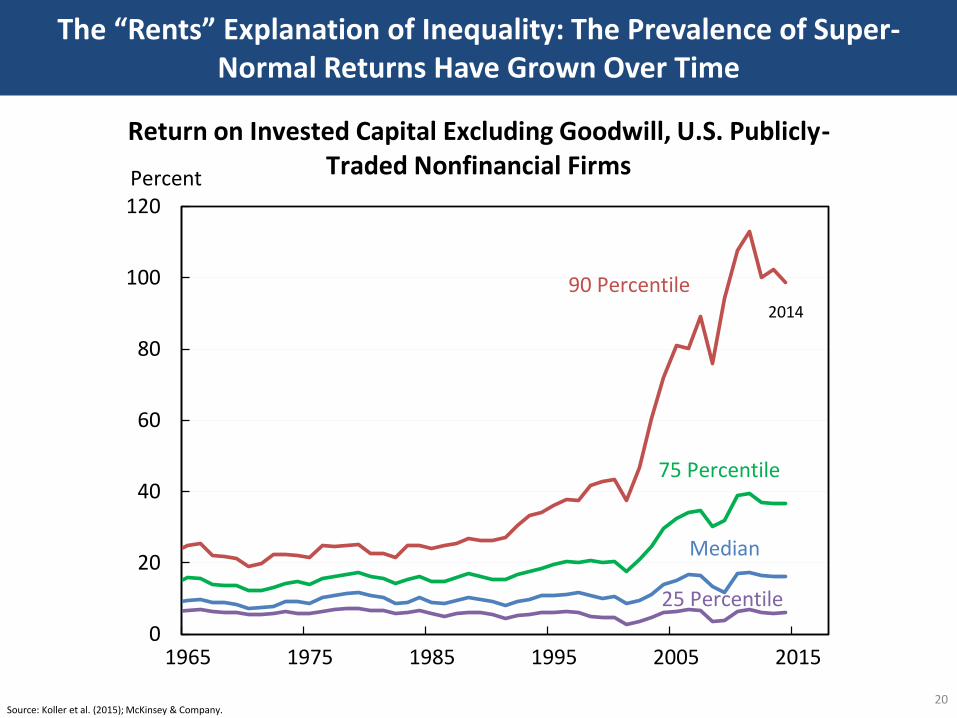

The “Rents” Explanation of Inequality: The Prevalence of Super-Normal Returns Have Grown Over Time

20Source: Koller et al. (2015); McKinsey & Company.

Median

90 Percentile2014

75 Percentile

25 Percentile

0

20

40

60

80

100

120

1965 1975 1985 1995 2005 2015

Return on Invested Capital Excluding Goodwill, U.S. Publicly-Traded Nonfinancial FirmsPercent

25th Percentile

50th Percentile

90th Percentile

Top Percentile

-0.25

0

0.25

0.5

0.75

1978 1983 1988 1993 1998 2003 2008 2013

Individual/Firm: Change in Wage Structure Since 1982Change in Log Real Annual Wage

2012

25th Percentile

50th Percentile

90th Percentile

Top Percentile

2012

-0.25

0

0.25

0.5

0.75

1978 1983 1988 1993 1998 2003 2008 2013

Firms: Change in Wage Structure Since 1982Change in Log Real Annual Wage

The “Rents” Explanation of Inequality: Virtually All of the Rise in Wage Inequality is Due to Inter-Firm as Opposed to Intra-Firm Dispersion

21Source: Song et al. (2015).

The Third Challenge: Labor Market FluidityWorker Flows have been Declining Since the 1990s

22Source: Hyatt and Spletzer (2013); Bureau of Labor Statistics, Current Population Survey; Bureau of Labor Statistics, Job Openings and Labor Turnover Survey; Census Bureau, Longitudinal Employer-Household Dynamics.

CPS Hires

JOLTS Hires

0

5

10

15

20

25

30

35

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Trends in Hires and Separations, 1995-2012

2012:Q3

Percent of Total Employment

LEHD Hires

Worker Flows have been Declining Since the 1990s

23Source: Molloy, Smith, and Wozniak (2014).

Occupation Change

Industry Change

Employer Change

2013

0

2

4

6

8

10

12

14

1980 1985 1990 1995 2000 2005 2010 2015

Percent of Total Population Age 16+Employer, Occupation, and Industry Transitions

Worker Flows have been Declining Since the 1990s

24

Number Who

Found a Job

Dec-15

Number Who

Exited Job

2.3

2.4

2.5

2.6

2.7

2.8

1991 1996 2001 2006 2011 2016

Share of Population Finding and Exiting Jobs per MonthPercent

Note: Shading denotes recession.Source: Bureau of Labor Statistics; CEA calculations.

Business Entry Rates Have Also Declined

25Source: Census Bureau, Business Dynamics Statistics; CEA calculations.

Firms

7

9

11

13

15

1975 1980 1985 1990 1995 2000 2005 2010

Firm Entry Rate, 1978-2013Percent of Total Firms

2013

Benefits from Job Switching Have Declined

26

Wage and Earnings Gains Associated with Job Switching

Data

Source Age

Group Time Period Gain to Switching

Jobs

Topel and Ward (1992) LEED 18 to 34 1957:Q1 - 1972:Q4

9%

Molloy, Smith, and Wozniak (2014)

PSID 22 to 29

1983-1994 4%

1995-2001 10%

2003-2011 2%

NLSY 22 to 29

1966-1981 7%

1979-1994 3%

2002-2011 4%

Fallick, Haltiwanger, and McEntarfer (2012)

LEHD 25 to 55

1995:Q2 8%

1999:Q2 14%

2001:Q2 6%

Note: Topel and Ward (1992) and Molloy, Smith, and Wozniak (2014) are wage regression models, while Fallick, Haltiwanger, and McEntarfer (2012) use sample earnings medians from job switchers. All regression estimates are statistically significant, except for the Molloy, Smith, and Wozniak (2014) estimates from the 2000s.

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

All Under Age 35 Age 35 or Older

Between State

Within State

Difference in Migration Rates of Workersin Most vs. Least Licensed Occupations

Percent Di fference

0

5

10

15

20

25

30

1950s 1960s 1970s 1980s 1990s 2000 2008

Share of Workers with a State Occupational License

Percent of the Workforce

Occupational Licensing Has Grown & Interstate Mobility is Much Lower for Workers in Licensed Occupations

27Source: The Council of State Governments (1952); Greene (1969); Kleiner (1990); Kleiner (2006); Kleiner and Krueger (2013), Westat data; Census Bureau, American Community Survey 2010-2013; CEA Calculations. Number on left chart is calculated from an OLS regression controlling for race, citizenship, sex, citizenship, number of children, marital status, education, income, year, and state. Ages 25 to 65 were included.

Housing Supply Constraints Slow Income Convergence

28Source: Ganong and Shoag (2015); CEA calculations.

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

1960-69 1970-79 1980-89 1990-99 2000-10

Less ConstrainedSupply

More ConstrainedSupply

Speed of Income Convergence Across States by Housing SupplyAverage Percent of Income Gap Closed Each Year

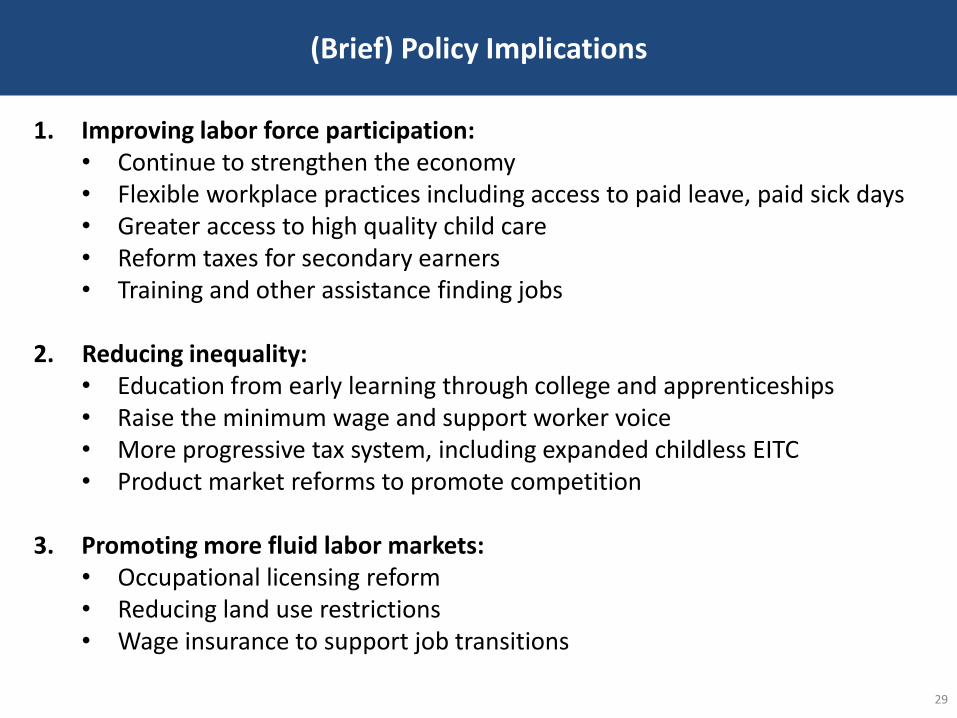

(Brief) Policy Implications

29

1. Improving labor force participation:• Continue to strengthen the economy• Flexible workplace practices including access to paid leave, paid sick days• Greater access to high quality child care• Reform taxes for secondary earners• Training and other assistance finding jobs

2. Reducing inequality:• Education from early learning through college and apprenticeships• Raise the minimum wage and support worker voice• More progressive tax system, including expanded childless EITC• Product market reforms to promote competition

3. Promoting more fluid labor markets:• Occupational licensing reform• Reducing land use restrictions• Wage insurance to support job transitions

Three Challenges in the U.S. Labor Market:

Participation, Inequality, and Fluidity

Jason FurmanChairman, Council of Economic Advisers

World Bank GroupJanuary 28, 2016