Theory of Contracts Lecture : Incomplete Contracting

63

Theory of Contracts Lecture : Incomplete Contracting Patrick Legros 1 / 63

Transcript of Theory of Contracts Lecture : Incomplete Contracting

Theory of ContractsLecture : Incomplete Contracting

Patrick Legros

1 / 63

Outline

Grossman-Hart

Optimality of Null Contracts

Financial Contracting

2 / 63

Outline

Grossman-Hart

Optimality of Null Contracts

Financial Contracting

3 / 63

Outline

Grossman-Hart

Optimality of Null Contracts

Financial Contracting

4 / 63

Grossman-Hart (1986), The costs and benefits of owership, JPE

Hart (1995), Firms, contracts and financial structures, ClarendonPress

Hart-Moore (1990), property rights and hte nature of the firm, JPE

Review of Economic studies, special issue (1999): articles byMaskin-Tirole, Segal, Hart-Moore

5 / 63

Grossman-Hart 1986

agent:asset:

M2

a2→ M1

a1→ output

I M1 invests i → change revenue R

I M2 : invests e → change cost C

I i , e are not contractable: price cannot depend on (i , e) evenif i and e are jointly observed at the time of the exchange.

I Can contract on ownership: who owns the asset, gives theright to exclude the other party from using the asset.

6 / 63

Grossman-Hart 1986Timing

Contract{A1,A2}

Invest(i , e)

M1 and M2

observe(i , e)

Negotiateprice p

R(i)− pp − C (e)

r(i ,A1)− pp − C (e,A2)

I “Relation specific investments”: i an de have a lower value(r < R, c > C ) outside the relationship

I p : competitive price (for a “standardized good”)

I Both c and r depend on which assets each manager controls.

7 / 63

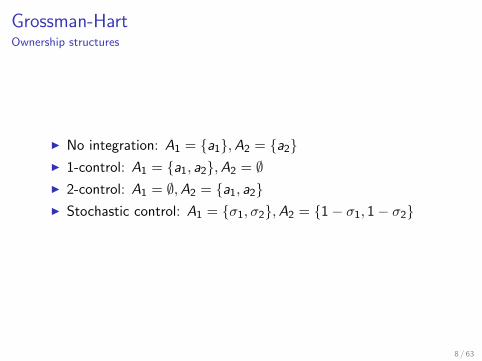

Grossman-HartOwnership structures

I No integration: A1 = {a1},A2 = {a2}I 1-control: A1 = {a1, a2},A2 = ∅I 2-control: A1 = ∅,A2 = {a1, a2}I Stochastic control: A1 = {σ1, σ2},A2 = {1− σ1, 1− σ2}

8 / 63

Grossman-HartNash Bargaining

I Bargaining set is B = {v1, v2|∃d : vi = vi (d)}I Threat point: (v1, v2)I Nash: maxv∈B(v1 − v1)(v2 − v2)

v1

v2

v1

v2

B

(v1 − v1)(v2 − v2)

Nash

9 / 63

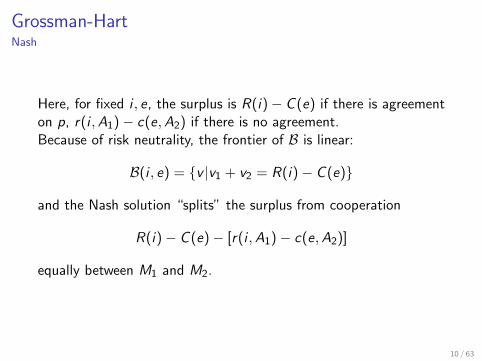

Grossman-HartNash

Here, for fixed i , e, the surplus is R(i)− C (e) if there is agreementon p, r(i ,A1)− c(e,A2) if there is no agreement.Because of risk neutrality, the frontier of B is linear:

B(i , e) = {v |v1 + v2 = R(i)− C (e)}

and the Nash solution “splits” the surplus from cooperation

R(i)− C (e)− [r(i ,A1)− c(e,A2)]

equally between M1 and M2.

10 / 63

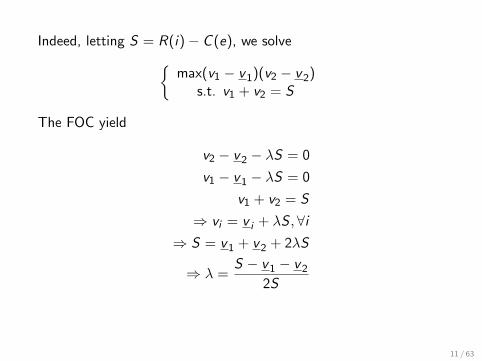

Indeed, letting S = R(i)− C (e), we solve{max(v1 − v1)(v2 − v2)

s.t. v1 + v2 = S

The FOC yield

v2 − v2 − λS = 0

v1 − v1 − λS = 0

v1 + v2 = S

⇒ vi = v i + λS ,∀i⇒ S = v1 + v2 + 2λS

⇒ λ =S − v1 − v2

2S

11 / 63

Grossman-HartEffects of ownership

First effect of ownership (ex-post)

I For fixed (i , e), changes the threat point since c(e,A2) andr(i ,A1) may vary with A1,A2.

I SInce the threat point changes, the Nash bargaining outcomechanges

Second effect of ownership (ex-ante)

I At the ex-ante stage (when i , e are chosen) the game hasdifferent payoffs

I hence there is likely a different ex-ante equilibrium in i , e.

12 / 63

The first effect is a simple redistributional effect (total payoff isstill R(i)− C (e)

The second effect can be distortionnary because by changing htemarginal returns from investment it may lead to inefficientinvestments

13 / 63

Fix (i , e) and (A1,A2) and find Nash outcome:

N1(i , e,A1,A2) = r(i ,A1)− p +1

2[R(i)− C (e)− r(i ,A1) + c(e,A2)]

N2(i , e,A1,A2) = p − c(e,A2 +1

2[R(i)− C (e)− r(i ,A1) + c(e,A2)]

Fix (A1,A2), find equilibrim (i , e) of game with payoffs

v1(i , e,A1,A2) = N1(i , e,A1,A2)− i

v2(i , e,A1,A2) = N2(i , e,A1,A2)− e

14 / 63

Grossman-Hart“Efficient ownership”

Total surplus is

W ∗(A1,A2) = R(i∗(A1,A2))− C (e∗(A1,A2))− i∗(A1,A2)− e∗(A1,A2)

The efficient ownership structure is (A1,A2) that maximizesW ∗(A1,A2)

What does this mean?

I Must assume either a large amount of wealth (or ability toborrow at no cost) in order to implement the needed transferof assets

I For instance, suppose initially the ownership structureA1 = {a1},A2 = {a2} but that the “optimal” ownershipstructure is 1-control: A∗1 = {a1, a2},A∗2 = ∅

I Hence W ∗(A) < W ∗(A∗), but because of non-transferability(Nash bargaining), this does not imply that both agents preferA∗ to A.

15 / 63

Grossman-HartWealth effects

v1

v2

W ∗(A)

W ∗(A∗)

minimum price of asset 2

16 / 63

Grossman-HartWealth effects

v1

v2

W ∗(A)

W ∗(A∗)

minimum price of asset 2

17 / 63

Grossman-HartWealth effects

I Hence if agents have finite wealth, there is no reason to focuson the “efficient” ownership structure. But then, what can wesay about vertical integration or control structures?

I Corporate finance (only one side has wealth and can purchaseassets)

I Models with wealth effects and general equilibrium effects.

18 / 63

Grossman-HartSome results

H0:C ′ < 0,C” > 0,R ′ > 0,R” < 0

H1:

R(i)− C (e) > r(i ,A1)− c(e,A2) ≥ 0,∀i , eA1 ∩ A2 = ∅A1 ∪ A2 = {a1, a2}

H2:

R ′(i) > r ′(i , {a1, a2}) > r ′(i , {a1} ≥ r ′(i , ∅|C ′(e)| > |c ′(e, {a1, a2}| > |c ′(e, a2| ≥ |c ′(e, ∅)|

(marginal return from investment is larger inside than outside andis increasing in ownership.)

19 / 63

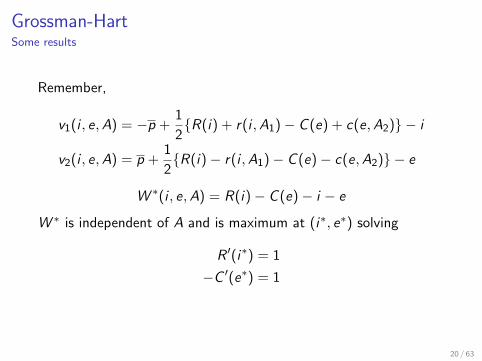

Grossman-HartSome results

Remember,

v1(i , e,A) = −p +1

2{R(i) + r(i ,A1)− C (e) + c(e,A2)} − i

v2(i , e,A) = p +1

2{R(i)− r(i ,A1)− C (e)− c(e,A2)} − e

W ∗(i , e,A) = R(i)− C (e)− i − e

W ∗ is independent of A and is maximum at (i∗, e∗) solving

R ′(i∗) = 1

−C ′(e∗) = 1

20 / 63

However, when i , e are chosen non-cooperatively,

∂v1

∂i=

1

2[R ′(i) + r ′(i ,A1]− 1

∂v2

∂e= −1

2[C ′(e) + c ′(e,A2)]− 1

and by H1-H2, at the second-best optimum i , e

0 =∂v1

∂i< R ′(i)− 1

0 =∂v2

∂e< −C ′(e)− 1

therefore,

R ′(i) > 1 ⇒ i < i∗

−C ′(e) > 1 ⇒ e < e∗

21 / 63

I Result 1: under-investmentwell known (Williamson, Cournot); not robust (Tirole if othertypes of negotiation processes).

I Result 2: complementary assetsshould be owned together; integration is optimal(r ′(i , {a1}) = r ′(i , ∅), c ′(e, {a2}) = c ′(e, ∅)

I Result 3: independent assetsshould not be owned together; integration is not optimal(r ′(i , {a1, a2}) = r ′(i , {a1}), c ′(e, {a1, a2}) = c ′(e, {a2}))

22 / 63

Grossman-HartMajor insights

I Definition of ownership: residual right of control over assets

I Distribution of ownership rights has real effects because itmodifies the expected marginal returns from investment

I In GH 1986,: ownership can modify the threat point even if allquasi-rent is appropriable, ie:; if there is a constant outsideoption: ex-post decisions have to be made and ownership onan asset gives the owner the right to choose the decision

I if no integration, decisions are chosen in a Cournot fashionI if integration, decisions are chosen in a “dictatorial” fashionI renegotiation: contract on decisions taking as threat points the

decisions corresponding to the ownership structure.

23 / 63

Grossman-HartMajor insights

I Definition of ownership: residual right of control over assets

I Distribution of ownership rights has real effects because itmodifies the expected marginal returns from investment

I In GH 1986,: ownership can modify the threat point even if allquasi-rent is appropriable, ie:; if there is a constant outsideoption: ex-post decisions have to be made and ownership onan asset gives the owner the right to choose the decision

I if no integration, decisions are chosen in a Cournot fashionI if integration, decisions are chosen in a “dictatorial” fashionI renegotiation: contract on decisions taking as threat points the

decisions corresponding to the ownership structure.

24 / 63

Grossman-HartMajor insights

I Definition of ownership: residual right of control over assets

I Distribution of ownership rights has real effects because itmodifies the expected marginal returns from investment

I In GH 1986,: ownership can modify the threat point even if allquasi-rent is appropriable, ie:; if there is a constant outsideoption: ex-post decisions have to be made and ownership onan asset gives the owner the right to choose the decision

I if no integration, decisions are chosen in a Cournot fashionI if integration, decisions are chosen in a “dictatorial” fashionI renegotiation: contract on decisions taking as threat points the

decisions corresponding to the ownership structure.

25 / 63

Grossman-HartMajor criticisms

I “Incomplete contracting” and dynamic programmingif anticipate that (i , e) will be observed by both agents andthat renegotiation takes place under symmetric information; itis simple to design - at the contracting stage - a “mechanism”that will be played after (i , e) is observed and that will lead toan efficient outcome (Maskin-Tirole).

I Does not explain why contracts are limited in scope (source ofincompleteness)

I Assume away wealth effects and focus on normative analysisof the “efficient” ownership structure

I GH identified with hold-up problem (ex-ante investments) andrelation specific investments. Not needed actually: e.g. ifnegotiation ex-post is not efficient.

I The fact that a “null” contract is signed ex-ante – while itmay be possible to commit to a mechanism – can berationalized (Che-Hausch, Segal).

26 / 63

Grossman-HartMajor criticisms

I “Incomplete contracting” and dynamic programmingif anticipate that (i , e) will be observed by both agents andthat renegotiation takes place under symmetric information; itis simple to design - at the contracting stage - a “mechanism”that will be played after (i , e) is observed and that will lead toan efficient outcome (Maskin-Tirole).

I Does not explain why contracts are limited in scope (source ofincompleteness)

I Assume away wealth effects and focus on normative analysisof the “efficient” ownership structure

I GH identified with hold-up problem (ex-ante investments) andrelation specific investments. Not needed actually: e.g. ifnegotiation ex-post is not efficient.

I The fact that a “null” contract is signed ex-ante – while itmay be possible to commit to a mechanism – can berationalized (Che-Hausch, Segal).

27 / 63

Grossman-HartMajor criticisms

I “Incomplete contracting” and dynamic programmingif anticipate that (i , e) will be observed by both agents andthat renegotiation takes place under symmetric information; itis simple to design - at the contracting stage - a “mechanism”that will be played after (i , e) is observed and that will lead toan efficient outcome (Maskin-Tirole).

I Does not explain why contracts are limited in scope (source ofincompleteness)

I Assume away wealth effects and focus on normative analysisof the “efficient” ownership structure

I GH identified with hold-up problem (ex-ante investments) andrelation specific investments. Not needed actually: e.g. ifnegotiation ex-post is not efficient.

I The fact that a “null” contract is signed ex-ante – while itmay be possible to commit to a mechanism – can berationalized (Che-Hausch, Segal).

28 / 63

Grossman-HartMajor criticisms

I “Incomplete contracting” and dynamic programmingif anticipate that (i , e) will be observed by both agents andthat renegotiation takes place under symmetric information; itis simple to design - at the contracting stage - a “mechanism”that will be played after (i , e) is observed and that will lead toan efficient outcome (Maskin-Tirole).

I Does not explain why contracts are limited in scope (source ofincompleteness)

I Assume away wealth effects and focus on normative analysisof the “efficient” ownership structure

I GH identified with hold-up problem (ex-ante investments) andrelation specific investments. Not needed actually: e.g. ifnegotiation ex-post is not efficient.

I The fact that a “null” contract is signed ex-ante – while itmay be possible to commit to a mechanism – can berationalized (Che-Hausch, Segal).

29 / 63

Optimality of null contracts

Che and Hausch (1999) (see also Tirole) consider a simple ex-anteinvestment trading situation and show that if the investment ofone party affects directly the welfare of the other party, then theoptimal ex-ante contract when there is renegotiation is the “nullcontract” (do not specify anything at all).

This situation of “cooperative investment” should be contrastedwith the GH situation where each party benefits from his owninvestment only.

30 / 63

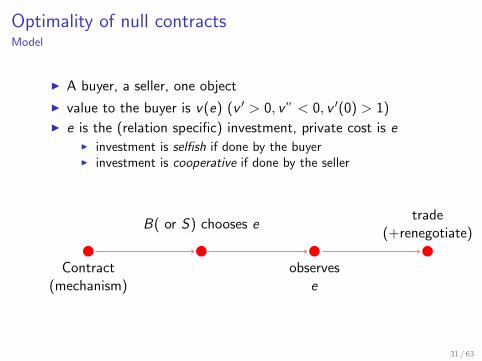

Optimality of null contractsModel

I A buyer, a seller, one object

I value to the buyer is v(e) (v ′ > 0, v” < 0, v ′(0) > 1)I e is the (relation specific) investment, private cost is e

I investment is selfish if done by the buyerI investment is cooperative if done by the seller

Contract(mechanism)

B( or S) chooses e

observese

trade(+renegotiate)

31 / 63

The first best:e∗ : max

ev(e)− e

ore∗ : v ′(e∗) = 1

If there is no contract, parties observe e and negotiate the price.Assuming Nash bargaining, the price is set at p = v(e)/2(investment is specific, hence outside options are zero).

The agent making the investment anticipates this and choosesenull to maximize 1

2v(e)− e leading to

enull : v ′(enull) = 2

.this is independent of whether the investment is selfish orcooperative.

32 / 63

Can the parties do better with an ex-ante contract?

Always yes if there is no renegotiation.

With renegotiation the answer is yes only if there is selfishinvestment; with cooperative investment the parties cannotimprove on the “null contract”.

33 / 63

Che-HauschSelfish investment

Selfish investment Consider an initial contract where the partiesagree to trade at price p ∈ [0, v(e∗)− e∗]. Since the buyer ismaking the investment, his payoff is v(e)− p − e which ismaximized at e = e∗: the first best is achieved.

Note that this initial contract is immune to renegotiation. Indeed,renegotiation can happen if both parties agree to it. For any valueof e, since the total surplus is v(e)− e, either the buyer or theseller will be hurt by renegotiating to a price different from theinitial price.

34 / 63

Che-HauschCooperative investment

Cooperative investment With a fixed price initial contract theseller’s payoff is p − e which is maximized at e = 0, hence thiscontract cannot achieve the first best. However the first best canstill be achieved when there is no renegotiation, but twe need touse more sophisticated contracts like “option contracts”.(Noldeke-Schmidt, Edlin-Rubinstein).

Option contract The buyer has the option of buying the good atprice p = v(e∗).

If v(e) > v(e∗), the buyer will exert the option; if v(e) < v(e∗) hewill refuse to buy. This creates a discontinuity in the payoff to theseller: if e ≥ e∗ his payoff is v(e∗)− e and if e < e∗ his payoff is 0.It is then optimal for the seller to choose e = e∗.

35 / 63

Che-HauschRenegotiation

The option contract leads to the first best only if the partiesbelieve that the “no trade” outcome cannot be renegotiated.

Let p be the option price. If the buyer rejects the trade at thisprice, renegotiation will lead to a price of v(e)/2: hence as long asv(e) < 2p the buyer will prefer to refuse to exert the option andengage in renegotiation. This is the hold-up problem.

The seller chooses e to maximize

min{1

2v(e), p} − e

and the solution is either 0 or enull . In either case, the bestoutcome is what is achieved without an ex-ante contract!

36 / 63

Financial contracting

In financial contract instruments like debt or equity, the rights todecide on the assets and the rights to the monetary profits are“bundled”:

I With debt, the shareholders have control rights on decisionson the assets unless she cannot repay the debt, in which casethe creditor gets control of the decisions. In general thedecision is whether the firm can continue to operate orwhether the asset should be liquidated (e.g. through abankruptcy procedure).

I Hence (with equity) the shareholders have a residual right onthe monetary profits and the decisions as long as debt isrepaid, otherwise the rights go to the debt holder.

37 / 63

The fundamental insight of GH that ownership should be definedwith respect to residual rights of control has had a profound impacton the way researchers have approached financial contracting.

It is now well understood that it is important to separate the waymonetary rights from the way control rights over decisions areallocated.

EX: Kaplan-Stromberg and venture capital contracts.

The literature (starting with Aghion-Bolton) has initially usedmodels based on the IC paradigm, partly because completecontracts may make the issue of “ownership” somewhat irrelevant.At the same time it became clear that the key issue was whetherthe parties could prevent renegotiation, for then, the rights given inthe initial contract will have an effect on the way renegotiation willdevelop.

38 / 63

Financial contracting

The IC approach to financial contracting has initiated withAghion-Bolton (1992), and we will give a simple example of thismodel. We will then consider a “complete contracting” examplewith Dewatripont-Tirole (1994)

39 / 63

Financial contractingAghion-Bolton 1992

K borroweddecision,

cash flow,rights allocated

State θrevealed

Actionis takenby owner

negotiation

Output,payment,realized

I Output is verifiable, and shares x(π, θi ) can be signed.

I Action is C (continue) or L (liquidate) is not contractible

I Entrepreneur has private benefit B only if action C

I Entrepreneur has limited liability

I Contracts can allocate “ownership” (who decides) and profits

I Monetary payoffs are state and action dependent

40 / 63

Financial contractingAB: assumptions

Monetary payoffs are state and action dependent:

Action L → πL, for all θ,

Action C →

πC if θ1,

πC if θ2,

πC if θ3.

Assume

H1:

{πC + B < πL < πC + B < πC + B

πC < πL < πC

H2: Pr(θi ) = 1/3

H3:1

3(πL + πC + πC ) > K

41 / 63

Financial contractingAB: first best

From H1-H3, the first best would require a state contingentdecision

if θ1 → L

if θ2, θ3 → C

However since the decision is not contractible, choice depends onwho has ownership. Below we will ignore renegotiation (does notaffect the qualitative results).

42 / 63

Financial contractingAB: is the FB attainable by control allocation?

Case: E has controlIf θ1, chooses L only if

x(πC , θ1) + B < x(πL, θ1)

⇒ x(πL, θ1) > B

Therefore, if E chooses efficiently, the investor gets

if θ1 : πL − x(πL, θ1) ≤ πL − B

if θ2 : πC − x(πC , θ2) ≤ πC

if θ3 : πC − x(πC , θ3) ≤ πC

But then the expected payoff of the investor is at most13(πL + πC + πC )− 1

3B which could be less than K if B is largeenough.

43 / 63

Financial contracting

Case: I has controlIf θ2, I will decide on C only if πC − x(πC , θ2) ≥ πL − x(πL, θ2). IfE does not have cash flow rights, the condition cannot be satisfiedsince πC < πL.

Hence if I has decision rights, it is important that E has cash flowrights in state θ2.

However since by limited liability the maximum payoff to I in stateθ2 is πC , the expected payoff to I is 1

3(2πC + πC ) which could beless than K since πC − πL < 0

44 / 63

Financial contractingAB: wrapping up

Aghion and Bolton show that the investor should have control, andcash flow rights, in states where value maximization is efficient butthat the entrepreneur should have control, or possibly cash flowrights, when value maximization is not efficient.

While Kaplan-Stromberg seem to comfort these conclusions, oneelement is crucially missing from Aghion-Bolton: the fact that avariation in cash-flows and decisions will probably have an effect onincentives.

45 / 63

Financial contractingDewatripont and Tirole 1994

I Two periods

I Complete contract approach: allocation of decision rights canbe contingent (ex-ante) on interim realizations

I Intuition: create classes of investors (debt-holder, shareholder)who have different risk attitudes.

I to simplify assume that the entrepreneur cares only about hisprivate benefit.

46 / 63

Financial contractingDT: timing

K borroweddecision rights

Efforte ∈ {e, e}

Profitsπ1 ∈ {π1, π1}

signal u

DecisionC or L

Profitsπ2

I Pr(π1 = π1|e) = p > p = Pr(π1 = π1|e)

I π2 ∼ hA(π2, u) where A ∈ {C , L},I Cost of effort: 0 if e, K if e

I Private benefit B only if A = C

I Investor payoff is π1 + π2.

47 / 63

Financial contractingDT: assumptions

Two assumptions:

H1:E (π2|C , u)− E (π2|L, u) is increasing in u and is zero at u = u,

H2: C is riskier than L for each u.

48 / 63

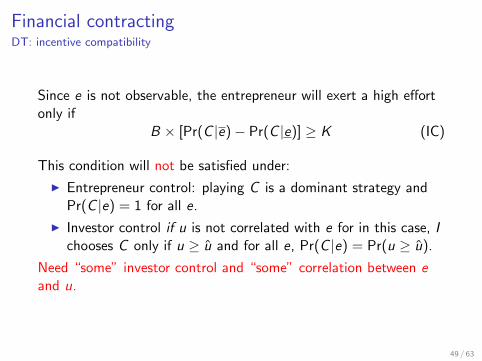

Financial contractingDT: incentive compatibility

Since e is not observable, the entrepreneur will exert a high effortonly if

B × [Pr(C |e)− Pr(C |e)] ≥ K (IC)

This condition will not be satisfied under:

I Entrepreneur control: playing C is a dominant strategy andPr(C |e) = 1 for all e.

I Investor control if u is not correlated with e for in this case, Ichooses C only if u ≥ u and for all e, Pr(C |e) = Pr(u ≥ u).

Need “some” investor control and “some” correlation between eand u.

49 / 63

Financial contractingDT: creation of incentives

As a benchmark, suppose that u is contractible. A contract canimpose an action as a function of (π1, u).

Since π1 is“good news” about e, moral hazard logic implies thatthe entrepreneur should be rewarded: this takes the form of agreater likelihood of having C chosen. By the same logic, if π1 isobserved, should choose L more often.

Hence under contractibility of u, think of two cutoff values, u∗ > uif π1 is realized and u∗∗ < u if π1 is realized. For values to the leftof the cutoff action L is taken.

if π1: u u u∗u∗∗

if π1:u u u∗u∗∗

L C

50 / 63

Financial contractingDT: creation of incentives

As a benchmark, suppose that u is contractible. A contract canimpose an action as a function of (π1, u).

Since π1 is“good news” about e, moral hazard logic implies thatthe entrepreneur should be rewarded: this takes the form of agreater likelihood of having C chosen. By the same logic, if π1 isobserved, should choose L more often.

Hence under contractibility of u, think of two cutoff values, u∗ > uif π1 is realized and u∗∗ < u if π1 is realized. For values to the leftof the cutoff action L is taken.

if π1: u u u∗u∗∗

if π1:u u u∗u∗∗

L

C

51 / 63

Financial contractingDT: creation of incentives

As a benchmark, suppose that u is contractible. A contract canimpose an action as a function of (π1, u).

Since π1 is“good news” about e, moral hazard logic implies thatthe entrepreneur should be rewarded: this takes the form of agreater likelihood of having C chosen. By the same logic, if π1 isobserved, should choose L more often.

Hence under contractibility of u, think of two cutoff values, u∗ > uif π1 is realized and u∗∗ < u if π1 is realized. For values to the leftof the cutoff action L is taken.

if π1: u u u∗u∗∗

if π1:u u u∗u∗∗

L C

52 / 63

Financial contractingDT: u not contractible

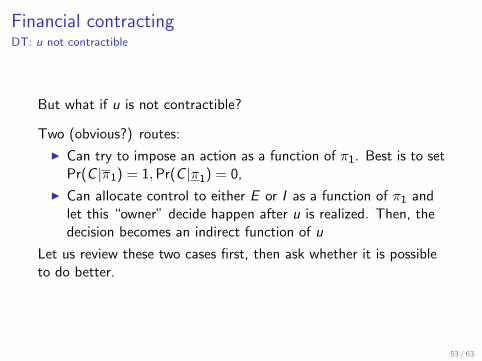

But what if u is not contractible?

Two (obvious?) routes:

I Can try to impose an action as a function of π1. Best is to setPr(C |π1) = 1,Pr(C |π1) = 0,

I Can allocate control to either E or I as a function of π1 andlet this “owner” decide happen after u is realized. Then, thedecision becomes an indirect function of u

Let us review these two cases first, then ask whether it is possibleto do better.

53 / 63

Financial contractingAT: decision a function of π1

If Pr(C |π1) = 1,Pr(C |π1) = 0, the probability margin in (IC)becomes

Pr(C |e)− Pr(C |e) = Pr(C |π1)× Pr(π1|e)− Pr(C |π1)× Pr(π1|e)

= p − p

Therefore if p − p ≥ KB , (IC) holds. The payoff of the investor is

pE (π2|C ) + (1− p)E (π2|S) = E (π2|S) + p[E (π2|C )− E (π2|S)]

54 / 63

Financial contractingAT: ownership

Give control to I when first period profit is π1 and give control toE if π1. By H1, I chooses C only if u > u while E always choosesC . Hence,

Pr(C |e)− Pr(C |e) = (p − p)(1− Pr(u ≥ u))

and incentives are weakened with respect to the previouspossibility. However, the investor’s payoff is now equal to

pE (π2|C ) + (1− p)

{∫u≤u

E (π2|S , u)du +

∫u≥u

E (π2|C , u)du

}= E (π2|S) + p[E (π2|C )− E (π2|S)]

+ (1− p)

∫u≥u

[E (π2|C , u)− E (π2|S , u)]du

Hence both investor and entrepreneur payoffs can be greater in thissolution if (IC) can be satisfied.

55 / 63

Financial contractingAT: two classes of investors

The ownership allocation in the previous case leads to cutoff valuesfor decisions that are independent of u if there is E ownership.Hence there is C “too often.” A better solution would be toallocate ownership in such a way that we can replicate the“benchmark rule” with cutoffs u∗ and u∗∗.

Intuitively to do so, in state π1, the agent who has the right todecide must be willing to use u∗∗ < u as a cutoff: hence he mustevaluate payoffs as a “risk loving” agent. By contrast in state π1,the agent in control must use u∗ > u and must evaluate payoffs asa “risk averse” agent.

56 / 63

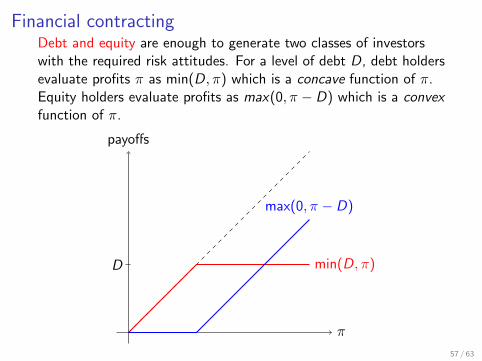

Financial contractingDebt and equity are enough to generate two classes of investorswith the required risk attitudes. For a level of debt D, debt holdersevaluate profits π as min(D, π) which is a concave function of π.Equity holders evaluate profits as max(0, π − D) which is a convexfunction of π.

π

payoffs

min(D, π)

max(0, π − D)

D

57 / 63

Financial contracting

Hence, giving control to a debt holder after π1 will lead to a cutoffgreater than u and giving control to an equity holder after π1 willlead to a cutoff smaller than u. This should lead to higher payoffsfor the investors and the entrepreneur. It is still the case howeverthat incentives are weakened with respect to the first solution(where control is allocated to risk neutral investor if π1.

Let us work through an example

58 / 63

Financial contractingAT: an example

Payoffs:

L ⇒π2 =

{L with probability γ

0 with probability 1− γ

C ⇒π2 =

{1 with probability u

0 with probability 1− u

where 0 < L < 1, u ∈ [u, u], γ > u.

Then, a risk neutral agent will choose C for all u greater than thecutoff value

u = γ × L

59 / 63

Financial contractingAT: example

If the debt is D, the equity holder chooses C only when

u(1− D) ≥ γ(L− D)

⇔ u ≥ γL− D

1− D.= ueq(D)

note that ueq(D) ∈ (0, γL) since L < 1.

If D < L, the debt holder always chooses S since γ > u impliesthat γD > uD for all u. The equity holder is willing to pay thedebt holder who has control in order to have C chosen (like a riskpremium).

60 / 63

Financial contracting

The equity holder is willing to pay R (in exchange for reducing thedebt to D − R) if

u(1− D + R)− R ≥ γ(L− D)

note that the equity holder may be willing to repay all the debt(R = D) if

u − D ≥ γ(L− D)

⇔ u ≥ γL + (1− γ)D

which is impossible if γL + (1− γ)D > u. in this case there existsa maximum transfer R that the equity holders are willing to pay inorder to induce the debt holder not to liquidate the firm.

61 / 63

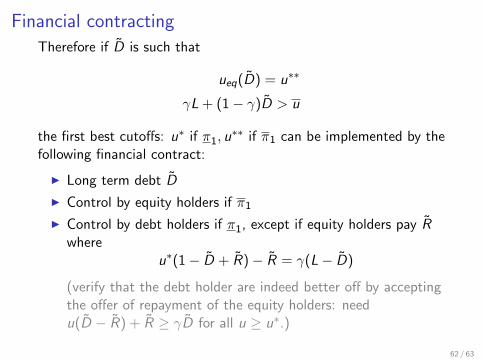

Financial contracting

Therefore if D is such that

ueq(D) = u∗∗

γL + (1− γ)D > u

the first best cutoffs: u∗ if π1, u∗∗ if π1 can be implemented by the

following financial contract:

I Long term debt D

I Control by equity holders if π1

I Control by debt holders if π1, except if equity holders pay Rwhere

u∗(1− D + R)− R = γ(L− D)

(verify that the debt holder are indeed better off by acceptingthe offer of repayment of the equity holders: needu(D − R) + R ≥ γD for all u ≥ u∗.)

62 / 63

Financial contractingSome conclusions

1. When actions are not contractible, capital structure is a wayto discipline managers and is also an incentive scheme forinvestors.

2. “Outsiders” play an efficiency-enhancing role only when thereis a “well designed” correlation between the income flow andthe control rights.

3. In general need multiple instruments in order to avoid a moralhazard in teams problem (effort of entrepreneur, decision ofowners)

4. Incentives for managers are linked to outside intervention:I strong intervention if weak performanceI weak intervention if strong performance

63 / 63