The Time Value of Money Module 24. Opening Why is a dollar today, worth more than a dollar a year...

14

The Time Value of Money Module 24

-

Upload

brianna-bryant -

Category

Documents

-

view

215 -

download

2

Transcript of The Time Value of Money Module 24. Opening Why is a dollar today, worth more than a dollar a year...

The Time Value of Money

Module 24

Opening

• Why is a dollar today, worth more than a dollar a year from now?

• Would you lend a friend $100 now for a repayment of $115 in 4 years?

The Time Value of Money1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

Money in the present is worth more than money in the future

The interest rate represents a payment to help compensate the lender, who would otherwise be repaid in dollars worth less than those borrowed.

Why We Charge Interest1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

Opportunity Costs– If we decide to loan a friend money, we

face the opportunity costs of what we could use that money for

– So, interest is what compensates us for the delayed gratification

The Time Value of Money1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

Purchasing Power– We know that due to inflation, the

purchasing power of the dollar will most likely decrease.

– Charging interest allows us to maintain that purchasing power

Present and Future Value1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

Present value– The value of a future sum in today’s

dollars– How much is $1 received a year from

now worth today?

Future Value– The value in the future of money

invested today– How much is $1 invested today going to

be worth in a year?

Present and Future Value1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

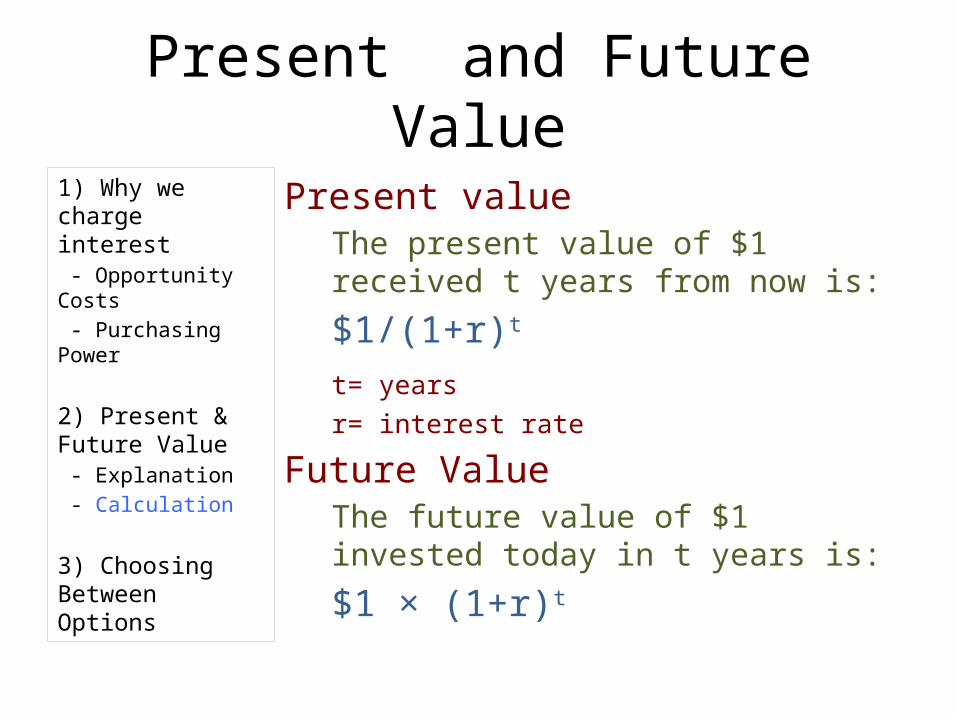

Present valueThe present value of $1 received t years from now is:

$1/(1+r)t

t= yearsr=

interest rate

Future ValueThe future value of $1 invested today in t years is:

$1 × (1+r)t

Present and Future Value1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

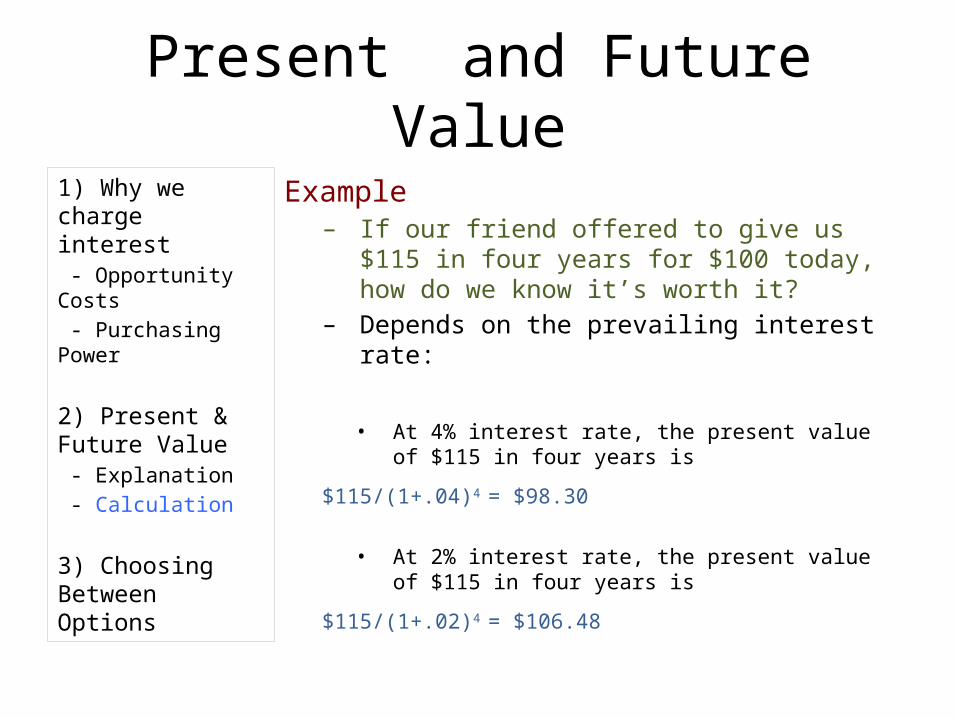

Example– If our friend offered to give us $115 in four

years for $100 today, how do we know it’s worth it?

– Depends on the prevailing interest rate:

• At 4% interest rate, the present value of $115 in four years is

$115/(1+.04)4 = $98.30

• At 2% interest rate, the present value of $115 in four years is

$115/(1+.02)4 = $106.48

Present and Future Value1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

Example– You could also compare the future value

to the $115:

• At 4% interest rate, the future value of $100 invested in four years is

$100 × (1+.04)4 = $116.99

• At 2% interest rate, the present value of $115 in four years is

$100 × (1+.02)4 = $108.24

Choosing Between Options1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present& Future Value - Explanation - Calculation

3) Choosing Between Options

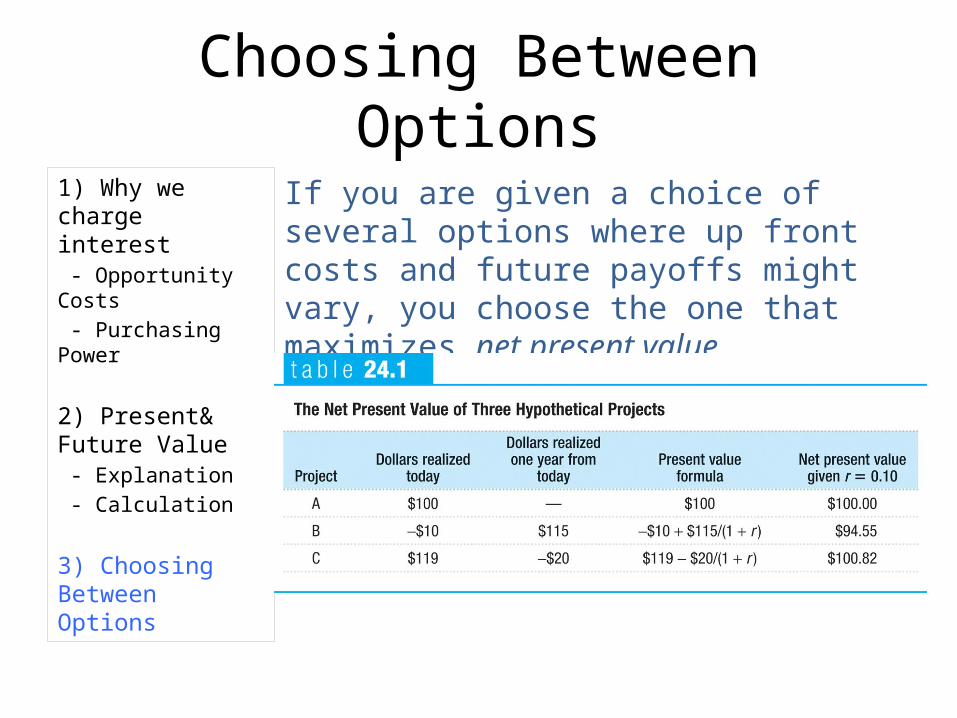

If you are given a choice of several options where up front costs and future payoffs might vary, you choose the one that maximizes net present value

Choosing Between Options1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

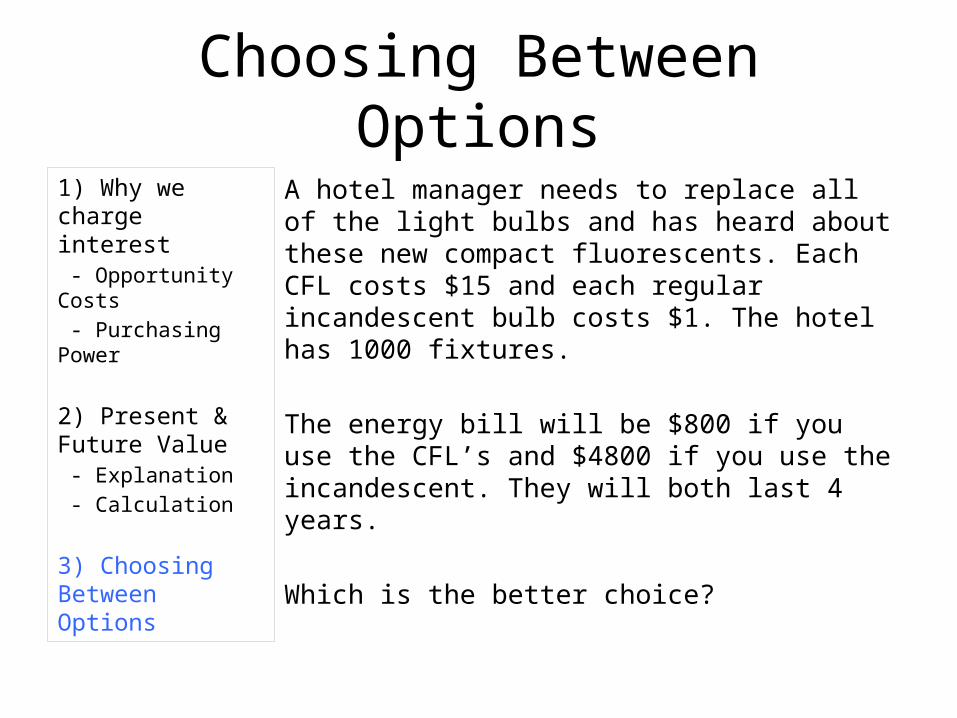

A hotel manager needs to replace all of the light bulbs and has heard about these new compact fluorescents. Each CFL costs $15 and each regular incandescent bulb costs $1. The hotel has 1000 fixtures.

The energy bill will be $800 if you use the CFL’s and $4800 if you use the incandescent. They will both last 4 years.

Which is the better choice?

Choosing Between Options1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

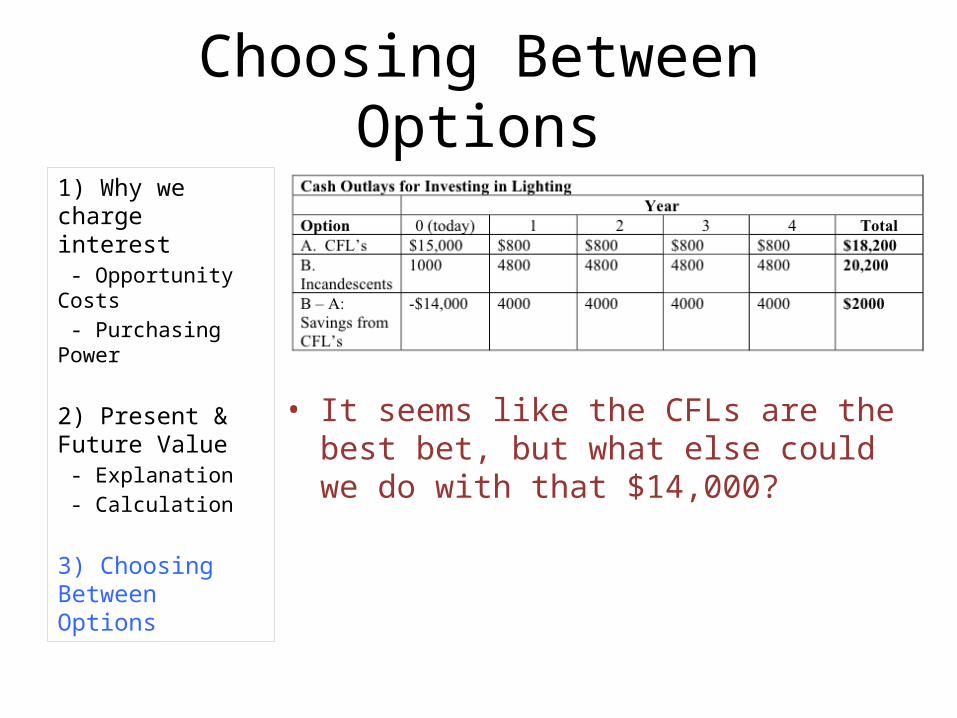

• It seems like the CFLs are the best bet, but what else could we do with that $14,000?

Choosing Between Options1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

• As interest rates get higher, the present value of the savings realized from switching to CFL’s decreases

Choosing Between Options1) Why we charge interest - Opportunity Costs - Purchasing Power

2) Present & Future Value - Explanation - Calculation

3) Choosing Between Options

Suppose that a person only lives 2 years and has 2 choices. She can go to school in next year, or go straight into the work force. If a person immediately starts working, she will earn $20,000 in both years 1 and 2. If a person goes to school in year 1, she must pay $5,000, but she would earn $47,500 in year 2. If the interest rate is 5%, calculate the present value of a person who goes to school and a person who does not.

• School:PV = -5,000/(1.05) + 47,500/(1.05)2 = $38,322.00

• Workforce:PV = 20,000/(1.05) + 20,000/(1.05)2 = $37,188.21