The State Of Digital Insurance, 2016 · PDF fileas technology vendors Backbase, guidewire...

22

The State Of Digital Insurance, 2016 Landscape: The Digital Insurance Strategy Playbook by Oliwia Berdak October 17, 2016 | Updated: December 7, 2016 FOR EBUSINESS & CHANNEL STRATEGY PROFESSIONALS FORRESTER.COM Key Takeaways Digital Disruption Has Come To Insurance Consumers have embraced digital touchpoints for a range of insurance activities. Where incumbents haven’t responded with better digital experiences, a host of insurance upstarts is ready to take over. But digital technologies are changing more than just sales and service, and this is starting to impact the entire insurance value chain. There’s A Growing Chasm Between Digital Insurance Leaders And Laggards Insurers have fallen behind other industries in terms of digital maturity. But there are big differences within the industry based on product line, distribution model, and executive commitment to digital business transformation. Agent-heavy firms are least likely to explore digital opportunities. Insurers Adopt One Of Four Approaches To Digitization Most insurers are exploring the potential of digital technologies in pockets of their organization — focusing on marketing or paperless processes. Some are launching digital-only brands or making the customer life cycle digital from end to end. Few are delivering a compelling digital customer experience and building strong digital capabilities for the future. Why Read This Report Insurers have so far been shielded from digital disruption by an older demographic, underwriting expertise, and regulatory barriers. But this is about to change. This report explores how digital technologies are changing the industry’s customers, competitors, products, and operations globally. It charts the different responses that digital teams in personal and commercial insurance lines have mounted, as well as the ecosystem of vendors that are keen to aid their digital transformation efforts.

Transcript of The State Of Digital Insurance, 2016 · PDF fileas technology vendors Backbase, guidewire...

The State Of Digital Insurance, 2016Landscape: The Digital Insurance Strategy Playbook

by Oliwia BerdakOctober 17, 2016 | Updated: December 7, 2016

FOr EBUsinEss & ChannEl stratEgy PrOFEssiOnals

fOrreSTer.cOm

Key takeawaysDigital Disruption Has come To InsuranceConsumers have embraced digital touchpoints for a range of insurance activities. Where incumbents haven’t responded with better digital experiences, a host of insurance upstarts is ready to take over. But digital technologies are changing more than just sales and service, and this is starting to impact the entire insurance value chain.

There’s A Growing chasm Between Digital Insurance Leaders And Laggardsinsurers have fallen behind other industries in terms of digital maturity. But there are big differences within the industry based on product line, distribution model, and executive commitment to digital business transformation. agent-heavy firms are least likely to explore digital opportunities.

Insurers Adopt One Of four Approaches To DigitizationMost insurers are exploring the potential of digital technologies in pockets of their organization — focusing on marketing or paperless processes. some are launching digital-only brands or making the customer life cycle digital from end to end. Few are delivering a compelling digital customer experience and building strong digital capabilities for the future.

Why read this reportinsurers have so far been shielded from digital disruption by an older demographic, underwriting expertise, and regulatory barriers. But this is about to change. this report explores how digital technologies are changing the industry’s customers, competitors, products, and operations globally. it charts the different responses that digital teams in personal and commercial insurance lines have mounted, as well as the ecosystem of vendors that are keen to aid their digital transformation efforts.

2

5

9

11

13

14

© 2016 Forrester research, inc. Opinions reflect judgment at the time and are subject to change. Forrester®, technographics®, Forrester Wave, roleView, techradar, and total Economic impact are trademarks of Forrester research, inc. all other trademarks are the property of their respective companies. Unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

Forrester research, inc., 60 acorn Park Drive, Cambridge, Ma 02140 Usa+1 617-613-6000 | Fax: +1 617-613-5000 | forrester.com

table Of Contents

Customers’ Digital Interactions With Insurers Are Increasing

Customers Use a Mix Of touchpoints For insurance activities

Digitally Empowered Customers Disrupt Insurance

Digital Upstarts are targeting insurance

Digital technologies reshape insurance

Digital Insurance Strategies Are Often Too Narrow In Scope

insurers Must Embrace Digital Business transformation

Vendors That Pitch Digital Transformation Play To Their Strengths

recommendations

Digital Business Teams Must Think Beyond Digital Channels

Supplemental Material

notes & resources

Forrester interviewed insurance companies ageas, allstate insurance, aviva, the Co-operators, Cuvva, Discovery insurance, the hartford Financial services, legal & general, MaiF, nationwide Mutual insurance, next generation insurance, Policygenius, Prudential Corporation asia, shelter Mutual insurance, slice insurance technologies, and trōv, as well as technology vendors Backbase, guidewire software, hCl technologies, hearsay social, infosys, saP, and tata Consultancy services.

related research Documents

Disrupting Finance: Digital insurers

how Ecosystems Underpin Digital Business in insurance

Understand the Digital Business landscape

FOr EBUsinEss & ChannEl stratEgy PrOFEssiOnals

The State Of Digital Insurance, 2016Landscape: The Digital Insurance Strategy Playbook

by Oliwia Berdakwith Benjamin Ensor, Ellen Carney, Zhi ying ng, Martin gill, alexander Causey, and Michael Chirokas

October 17, 2016 | Updated: December 7, 2016

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

2

Landscape: The Digital Insurance Strategy Playbook

Customers’ Digital interactions With insurers are increasing

Digitally empowered customers are changing the way they shop, travel, and manage their finances.1 as a wave of digital businesses like amazon, airbnb, and spotify resets consumer expectations, digital insurance professionals are seeing their customers bring the same expectations and behaviors to insurance.

customers Use A mix Of Touchpoints for Insurance Activities

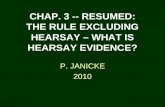

insurance distribution patterns vary substantially from country to country and by product type. But in every country, digital touchpoints are changing how customers engage with insurance companies for every type of policy. We surveyed Us and Western European online adults in Q3 2015 and Q1 2016 about their use of different touchpoints for insurance activities across the customer life cycle (see Figure 1).2 We found that (see Figure 2):

› consumers are most likely to discover insurance products offline.3 Us insurance buyers mostly learn about insurance through their friends or family, followed by an in-person or phone interaction with an insurance agent or advisor. however, digital touchpoints are not far behind. some 47% of Us online adults found out about renters’ insurance online and subsequently purchased it — almost as high as the 49% who discovered it offline.4 Even for a complex product like life insurance, some 42% found out about it online, compared with 52% for offline touchpoints. Because insurance is usually a researched rather than an impulse purchase, the most popular digital touchpoint is online search.

› Digital touchpoints dominate research. European online adults turn most frequently to insurance comparison websites (24%), followed by insurance companies’ websites (20%), to research insurance products.5 agents appear as only the third source of information (18%). the more complex the product is, the more likely consumers are to research it online. some 73% of Us consumers research life insurance online, compared with only 60% who research vehicle insurance online.

› Buying preferences differ strongly by country. agents and brokers still dominate insurance sales in countries like France and the Us; in others, like the netherlands, sweden, and the UK, direct sales dominate. as many as 55% of French insurance buyers apply for insurance policies in an agency, compared with just 7% in sweden where customers typically buy insurance online or by phone. in the Us, agents remain the leading sales channel for home, auto, and life insurance.6

› many insurance customers have embraced digital customer service. Millions of European and Us insurance customers are comfortable using their desktop or laptop computers to view their insurance policy, change their personal information, pay an insurance bill, change their coverage, or renew their policy (see Figure 3). For instance, about one-third of Us home insurance and life insurance customers interact with their insurance company by email.7 smaller numbers are starting to use mobile apps, too.

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

3

Landscape: The Digital Insurance Strategy Playbook

› customers are ready for new types of insurance products and services. Consumers aren’t only adopting digital touchpoints for routine insurance activities; they are also embracing new insurance products and services that have digital technologies at their core. For example, some 7% of smartphone-owning Us non-life insurance customers used their phones to sign up for mobile notifications, such as location-specific weather alerts, from their insurer in the past three months.8 and young Brits are embracing usage-based car insurance, with a 40% increase in the number of policies that use a tracking device to assess their driving from 2014 to 2015.9

fIGUre 1 Digital insurance teams are applying Digital technologies across the Customer life Cycle

EXPLORE

USE

ASK

ENGAGE DISCOVER

BUY

• Discover providers

• Gath

er and share data

• Find a local agen

t

• Register for digital services

• Realize insurance needs

• View and change coverage

• File claims

• Prevent claims

• Understand insurance products

• Log in easily and securely

• Change personal details

• Track claims

• Pay in the preferre

d way

• Customize coverage• Compare coverage• Get a quote• Compare price

• Ask about coverage• Get back to “normal”• Seek help

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

4

Landscape: The Digital Insurance Strategy Playbook

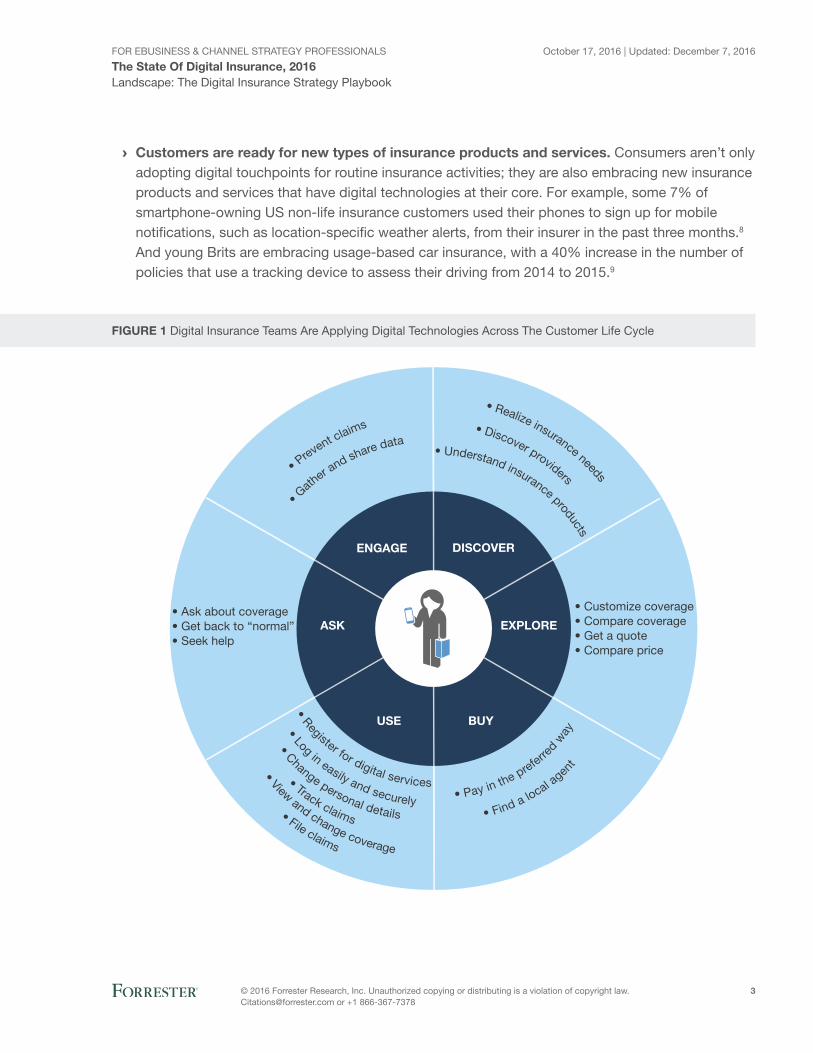

fIGUre 2 Customers Use a range Of touchpoints For their insurance activities

Comparison sitesare the most popular

way for Europeanconsumers to

research insuranceproducts, with 24%

using them.*

Insurance agents are thethird most popular wayfor European consumersto research insurance,

with 18% using them.*

11%

of US online adults use thecamera feature of their phone

to file an insurance claim.‡

Source: Forrester’s Consumer Technographics® North American Financial Services Customer Life CycleSurvey, Q2 2016 (US)

*Source: Forrester’s European Consumer Technographics Financial Services Survey 2, 2015†Source: Forrester’s Consumer Technographics North American Financial Services Online BenchmarkRecontact Survey, Q3 2016 (US)

‡Source: Forrester’s North American Consumer Technographics Financial Services Survey, 2015

The most commonway for US online

adults to interact withtheir life insurer isthrough email.

23% of USonline adults who ownlife insurance receivecustomer service via

online chat.

42%of US online adults

discover lifeinsurance

products online.

7%

of smartphone-owning US non-life-insurance customerssigned up formobilenotificationsfrom their insureron their computers.†

Base: 525 US online adults (18+) who applied for a life insurance policy in the past 36 months*Base: 569 EU-5 online adults (18+) who applied for a life insurance policy in the past 36 months†Base: 1,727 US online adults (18+) who have non-life insurance‡Base: 4,527 US online adults (18+) who have non-life insurance

18%of US onlineadults bought lifeinsurance online.

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

5

Landscape: The Digital Insurance Strategy Playbook

fIGUre 3 European and Us insurance Customers are Embracing Digital self-service

Base: 5,365 US and 5,939 European online adults (18+) who have insurance (other than life insurance) anduse a desktop or laptop computer

8%

10%

14%

16%

19%

9%

10%

12%

37%

24%

Checked the status of a claim

Changed my coverage

Changed my personal information

Paid an insurance bill

Viewed an insurance policy

“Which channels have you used to do each of the following insurance activitiesin the past three months?”(On a desktop or laptop)

Note: EU-5 includes France, Germany, Italy, Spain, and the UK.

Source: Forrester’s Consumer Technographics® North American Financial Services Online BenchmarkRecontact Survey, Q3 2016 (US) and Forrester’s European Consumer Technographics Financial ServicesSurvey 2, 2015

USEU-5

Digitally Empowered Customers Disrupt insurance

after a slow start, digital upstarts are now flooding into insurance, seeing the agent-led and paper-heavy industry as ripe for disruption. Digital technologies are reshaping the industry in more fundamental ways, and as consumers adopt new behaviors at a much faster pace — a trend that Forrester terms hyperadoption — this will affect the entire insurance value chain (see Figure 4). Digital technologies are changing the way firms can identify insurance needs, price and underwrite risk, sell policies, manage fraud and risk, provide customer support, and settle claims — and bringing in new competitors whose digital prowess can make them better at these activities.

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

6

Landscape: The Digital Insurance Strategy Playbook

fIGUre 4 Digital technology is Bringing new Competitors to all Parts Of the insurance Value Chain

Productdevelopment

& management

Riskassessment

& pricingDistribution

Policyadministration

Riskmanagement

Claimsmanagement

Marketresearch

Product design

Actuarialprocess

Productmanagement

Data analysis

Pricing

Marketing

Channelmanagement

Sales

Productselection

Accountmanagement

Billing

Claimnoti�cation

Renewal

Risk monitoring

Riskassessment

Risk advice

Claimassessment

AssistanceRisk education

Identify newtypes of assets

customerswant to protect.

Understandcustomers’

individual riskpro�les; identify

lowest-riskcustomers.

Identify themoment of

need and offerbest customer

experience.

Offer bestcustomerservice;

understandchanging

circumstances.

Analyze eventsand processinformation

quickly; offersupport and

empathy.

Monitor risk;coach

customers toreduce riskybehaviors;spot fraud.

Underwriting

Digital Upstarts Are Targeting Insurance

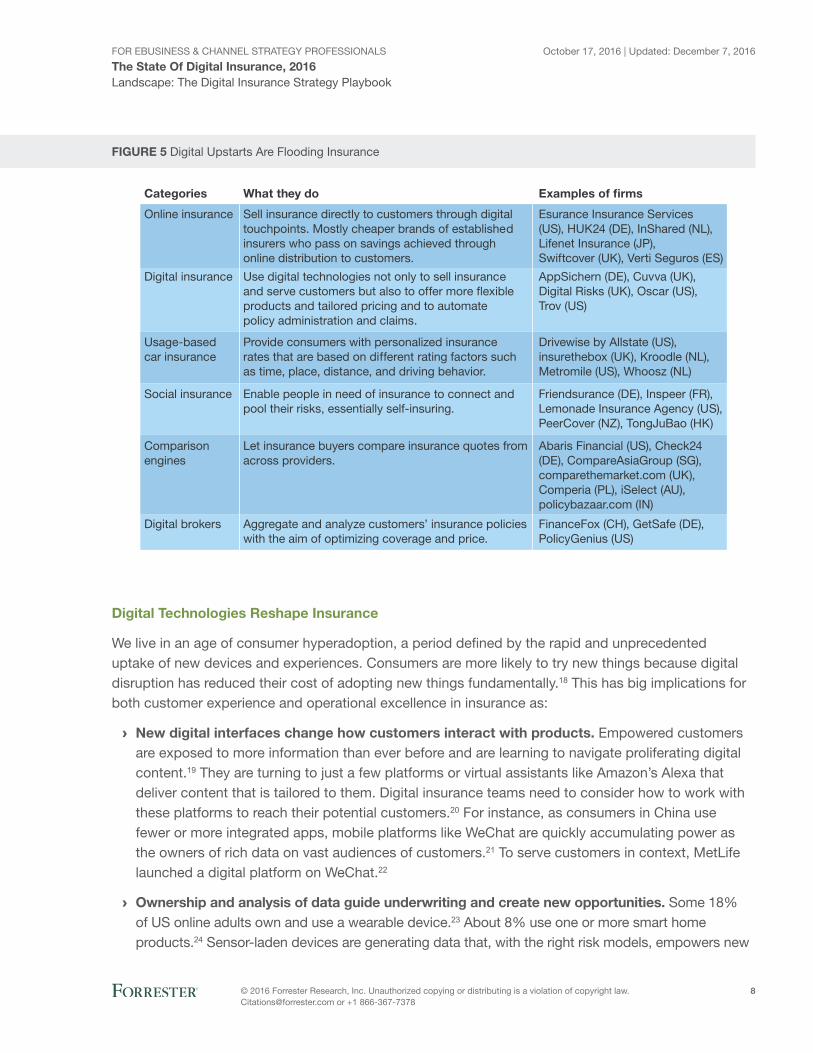

hefty capital requirements and underwriting expertise have protected parts of the insurance value chain from disruption. Because of this, many startups have chosen to focus on merchandising and distributing policies, often working with established insurers that take the risk onto their balance sheets. Disruptors are (see Figure 5):

› making it easier for customers to compare and choose insurance products. Comparison websites have given customers powerful tools to compare policies and to switch to the cheapest provider. they have also squeezed insurers’ profit margins. in the UK, 40% of online adults who bought insurance in the past three years researched that purchase through insurance comparison websites like Confused.com and comparethemarket.com.10 now a new generation of digital brokers like getsafe in germany; Esurance, FinanceFox, and Knip in switzerland; Brolly and Worry+Peace in the UK; and Policygenius in the Us aim to help customers choose and optimize their insurance coverage.

› Offering flexible coverage. Disruptors are contributing to the atomization of insurance — enabling customers to buy flexible, short-term coverage as and when needed. UK startups Cuvva and Digital risks sell flexible, pay-as-you-go car and small business insurance, respectively. Us startup

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

7

Landscape: The Digital Insurance Strategy Playbook

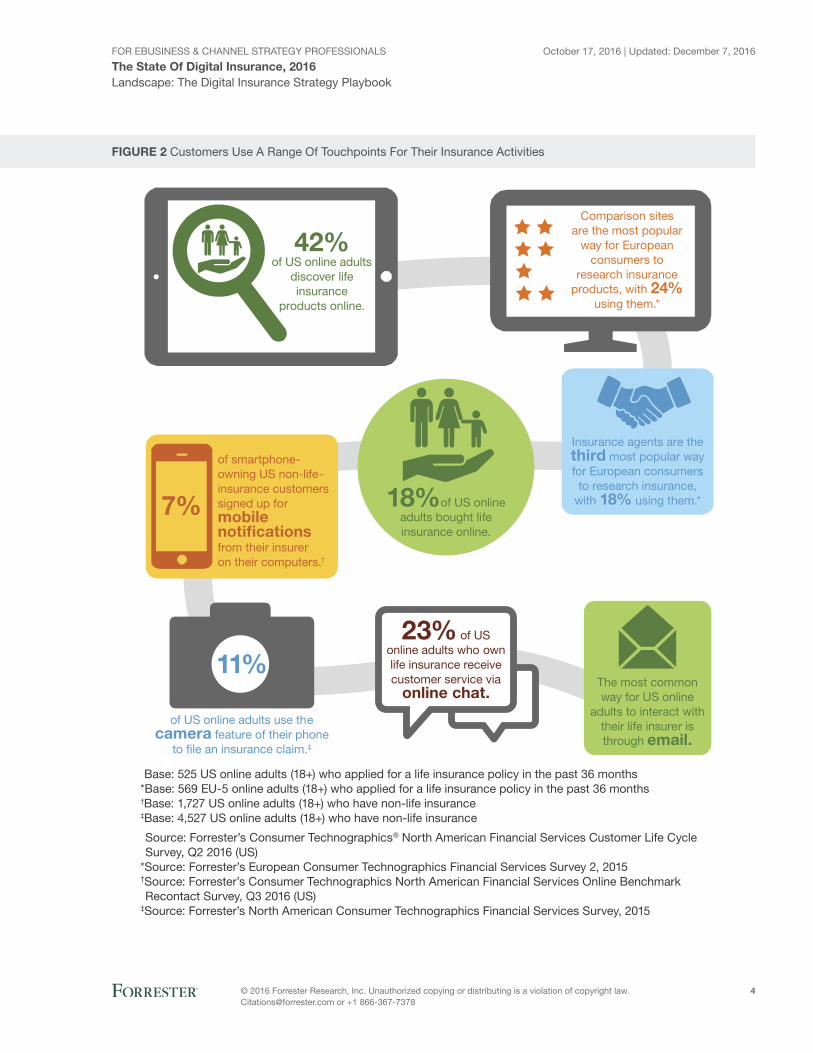

sure offers what it calls “episodic insurance,” enabling busy travelers to buy, book, and use travel accident insurance on their mobile devices.11 On-demand insurance platform trōv collects data about customers’ possessions, builds it into a personal inventory list, and lets customers turn coverage on and off for each of the items with a single swipe.12

› Using data to lower risk and develop new pricing models. While traditional car insurance pricing models assess risk and determine premiums based on group behavior and proxy variables such as credit scoring and driving records, startups like insurethebox in the UK or Whoosz in the netherlands use information about trip time of day, distance traveled, location, speed, braking and acceleration patterns, and tendency to swerve to assess drivers individually and price accordingly.13 these policies offer careful drivers discounts of up to 25% off their rate. social insurance platforms like Friendsurance in germany aim to lower the risk profile of their members by encouraging them to build their own self-insurance groups, choosing people they trust to be careful.14

› finding new distribution opportunities. Digital disruptors are helping consumers discover their insurance needs and buy relevant policies instantly. german startups massUp and simplesurance aim to make sales of low-value insurance, like smartphone coverage, profitable with insurance distribution platforms that integrate into eCommerce websites. UK startup Bought By Many connects people with complex insurance needs and approaches insurers for a quote as a group — negotiating a better price through scale. startups are also using mobile devices to distribute insurance to low-income customers. For example, sweden-based Bima offers mobile-delivered insurance and health services in emerging markets.15

› Providing end-to-end digital experiences. startups use smartphone cameras, video, and data available through application programming interfaces (aPis) to simplify and speed up the process of buying, managing, and using insurance. Cuvva’s mobile app lets new customers sign up, get a quote, and buy coverage in less than 5 minutes. instead of filling out long application forms, new customers can send a selfie and a picture of their driver’s license and the vehicle they’re about to drive. Cuvva augments this information with geolocation data collected through its app and data available from government databases.16

› Automating underwriting, claims, and customer service. Disruptors automate as many processes as possible. For example, trōv uses a chat bot to handle claims. Customers can make a claim with a single swipe, and a chat bot walks them through the claims process.17

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

8

Landscape: The Digital Insurance Strategy Playbook

fIGUre 5 Digital Upstarts are Flooding insurance

Categories What they do Examples of �rms

Online insurance Sell insurance directly to customers through digitaltouchpoints. Mostly cheaper brands of establishedinsurers who pass on savings achieved throughonline distribution to customers.

Esurance Insurance Services(US), HUK24 (DE), InShared (NL),Lifenet Insurance (JP),Swiftcover (UK), Verti Seguros (ES)

Digital insurance Use digital technologies not only to sell insuranceand serve customers but also to offer more �exibleproducts and tailored pricing and to automatepolicy administration and claims.

AppSichern (DE), Cuvva (UK),Digital Risks (UK), Oscar (US),Trov (US)

Usage-basedcar insurance

Provide consumers with personalized insurancerates that are based on different rating factors suchas time, place, distance, and driving behavior.

Drivewise by Allstate (US),insurethebox (UK), Kroodle (NL),Metromile (US), Whoosz (NL)

Social insurance Enable people in need of insurance to connect andpool their risks, essentially self-insuring.

Friendsurance (DE), Inspeer (FR),Lemonade Insurance Agency (US), PeerCover (NZ), TongJuBao (HK)

Comparisonengines

Let insurance buyers compare insurance quotes fromacross providers.

Abaris Financial (US), Check24 (DE), CompareAsiaGroup (SG),comparethemarket.com (UK),Comperia (PL), iSelect (AU), policybazaar.com (IN)

Digital brokers Aggregate and analyze customers’ insurance policieswith the aim of optimizing coverage and price.

FinanceFox (CH), GetSafe (DE),PolicyGenius (US)

Digital Technologies reshape Insurance

We live in an age of consumer hyperadoption, a period defined by the rapid and unprecedented uptake of new devices and experiences. Consumers are more likely to try new things because digital disruption has reduced their cost of adopting new things fundamentally.18 this has big implications for both customer experience and operational excellence in insurance as:

› New digital interfaces change how customers interact with products. Empowered customers are exposed to more information than ever before and are learning to navigate proliferating digital content.19 they are turning to just a few platforms or virtual assistants like amazon’s alexa that deliver content that is tailored to them. Digital insurance teams need to consider how to work with these platforms to reach their potential customers.20 For instance, as consumers in China use fewer or more integrated apps, mobile platforms like WeChat are quickly accumulating power as the owners of rich data on vast audiences of customers.21 to serve customers in context, Metlife launched a digital platform on WeChat.22

› Ownership and analysis of data guide underwriting and create new opportunities. some 18% of Us online adults own and use a wearable device.23 about 8% use one or more smart home products.24 sensor-laden devices are generating data that, with the right risk models, empowers new

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

9

Landscape: The Digital Insurance Strategy Playbook

competitors to price and underwrite risk effectively.25 Data from social media and mobile devices can also fuel new services and revenue streams. Cuvva has built a relational database of cars and their owners that the firm has used to launch a new service called “the social garage.” this lets users see which of their Facebook friends have cars available for them to borrow in their Cuvva app.26

› The shareconomy challenges risk models. as consumers seek to monetize their homes, cars, or home improvement skills, the definition of private and commercial activity — one of the variables that underwriters use to assess risk — is blurring.27 startups like Cuvva, Metromile, and slice and established insurers like axa and geico are launching policies to plug these emerging insurance gaps. For example, Metromile partners with Uber to provide insurance coverage to drivers when they’re between fares. Drivers use a telematics device to track when they’re driving “off the clock.”

› Automation changes the nature of risk. advances in cognitive technology — robots, automation, robotic process automation (rPa), smart machines, intelligent machines, and machine learning — make replacing humans with machines for some tasks increasingly possible.28 But as smart robots replace humans as drivers or doctors, underwriting models for car insurance or third-party liability will need to change. growing dependency on digital technologies makes cyber insurance, which protects business from internet-related risks including cyberattacks, a big opportunity. allianz global Corporate & specialty expects the market for cyberinsurance to grow from $2 billion today to over $20 billion in the next 10 years.29

Digital insurance strategies are Often too narrow in scope

While some insurance chief executives, like aviva’s CEO Mark Wilson and axa’s CEO thomas Buberl, are putting energy and resources into digital transformation, many other chief executives are focused on other priorities. since some insurance companies do not even have a head of eBusiness or other executive responsible for digital business, many insurance companies’ strategies depend on the determination of the CiO, CMO, and other senior executive to respond. how are digital strategy professionals at insurance companies responding to the seismic shifts affecting their industry?

› There’s strong commitment to digital business transformation. some 56% of business and technology decision-makers in insurance see accelerating their digital business as a high or critical priority over the next 12 months. this is higher than in other industries and particularly so in Europe.30 the need to accelerate digital business transformation comes from the low digital maturity of insurance when compared with other industries.31

› Insurers underestimate the impact of digitization. Most insurance executives still think of “digital” in a tactical way as relating to just touchpoints or technologies. leaders, on the other hand, are focusing their efforts on digital customer experience and digital operational excellence; they are also discovering new business models that digital technology has created.32 Discovery in

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

10

Landscape: The Digital Insurance Strategy Playbook

south africa, for example, is a fully fledged insurer in its core markets and also a partner to insurers in other geographies. the company licenses its Vitality wellness platform, including the installation of a core operating system.33

› Digital maturity varies by product line and distribution model. Property and casualty insurance is ahead in digital transformation because insurers invest where they expect to see the highest return.34 Many agent-dependent firms are still wary of upsetting their salesforce and are making only halfhearted efforts focused on digital marketing.

› executive commitment is crucial. leadership is by far the biggest determinant of a company’s digital business transformation. Digital teams that have executive support are bullish, seeing digital touchpoints and technologies as an opportunity to change their distribution model. as one European insurance executive told us: “We should be able to do 100% service and 100% sales in digital. But we need to find commercial agreements with our partners so it doesn’t matter where the sale takes place.”

Insurers must embrace Digital Business Transformation

Different understandings of the digital opportunity, combined with internal resistance due to the firm’s distribution model or costs involved in overhauling legacy systems, translate into four types of approach, each with divergent focus and impact (see Figure 6):

› Bringing digital technology to pockets of the business. Many digital insurance executives follow the path of the least resistance, focusing their digital efforts where it’s easiest or quickest to show the returns — be that investing in digital marketing or implementing paperless processes. as one digital marketing executive at a north american insurer told us: “Change is easier to embrace in digital and eCommerce than in a call center or in a large distributed agency force comprised of contractors. you also have the supply chain side of claims, where you’re dealing with body shops that are not digital at all.”

› Launching new, digital-only brands. Executives who became frustrated trying to force digital initiatives internally or who see an opportunity to target a specific customer segment like Millennials or travelers often launch separate, digital-only brands. For example, ageas launched Back Me Up, MassMutual launched haven life, and shelter insurance launched say insurance.35 these greenfield operations are a chance to start afresh — with new brands, new customer interfaces, new policy administration systems, and new marketing and billing platforms. the subsidiary might share some core systems with its mother company, which can slow it down in that part of the business.

› Digitizing the customer life cycle end-to-end. For many digital insurance teams, a fully digital customer life cycle is the holy grail. according to one head of digital engagement at a European insurer, “the opportunity is immense — not many insurers offer full, end-to-end digital experience — from product enquiry to claims and then a renewal. no one is really doing that, just a lot of smoke and mirrors.” One chief digital officer has set out a digital customer life cycle as his aim: “We absolutely think of building an end-to-end customer experience — research, buy, administer, use.”

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

11

Landscape: The Digital Insurance Strategy Playbook

› embarking on a complete digital business transformation. One chief digital officer of a European insurer is tackling the “what” and the “how” of digital business transformation simultaneously. he has a road map of digital products that he is building for his customers. the road map is underpinned by four teams needed to build the underlying capabilities: software engineering, a digital product and design team, a digital marketing center of excellence, and an innovation and new business team. he explains: “the digital capabilities — those are there in order to roll out everything else. they are the means by which we do it and work with the digital team and engineering teams in the local markets.”

fIGUre 6 insurers are adopting Four approaches in response to Digital Disruption

Impact

Single function Multiple teams Whole organization

• Digital marketing• Digital touchpoints

— web or app• Digitizing agents• Digital sales• Digital self-service

Digitizingpockets

• A new digital brandto appeal to aniche customersegment:Millennials, youngdrivers, travelers,etc.

A new digital-onlybrand

• Enabling customersto conduct theentire purchasejourney throughdigital touchpoints:discover, research,buy, engage

End-to-end digitalcustomer life cycle

• Building up digitalcapabilities to beable to respond tochanges faster

• Digitizing keycustomer journeys

• Building a singleview of thecustomer

• Evaluating andimplementingdigital technologyacross the valuechain

Digitaltransformation

Sin

gle

pur

pos

eO

ngoi

ng c

hang

e

Focu

s

Vendors that Pitch Digital transformation Play to their strengths

as insurers embark on their digital transformation journey, a wide range of partners stands ready to help. all of them define digital transformation differently but, crucially, in a way that plays to their strengths — focusing, for example, on the importance of digital experience or the absolute necessity of flexible core systems. While CiOs are the ones who will be picking their firms’ digital transformation partners, digital insurance strategy executives need to understand the different offerings coming from:

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

12

Landscape: The Digital Insurance Strategy Playbook

› Digital experience platform providers. to deliver and optimize customer experiences consistently through every phase of the customer life cycle, digital insurance teams need an array of software that supports marketing, customer insights, quotations, sales, customer service, and claims across both human and digital touchpoints. While many vendors provide components of this technology stack, some have gone on to offer these capabilities as a single digital experience platform.36 the biggest cross-industry providers are acquia, adobe, Demandware, Episerver, iBM, Oracle, saP hybris, salesforce, sDl, and sitecore.37 there are also smaller vendors like Backbase that tailor their platforms to the financial services industry, including insurance.

› Digital experience service providers. Firms like accenture interactive, Deloitte Digital, DigitaslBi, iBM interactive Experience, infosys, isobar, MrM//McCann, razorfish global, sapientnitro, VMl, and Wipro promise to deliver new or improved digital experiences designed to meet customer needs. their capabilities are centered around digital strategy, design, and development. they typically help insurers define their desired digital experience, which should match their customer needs and brand promise; design and develop cross-touchpoint customer experiences; and implement digital experience software and platforms like content management systems or eCommerce suites.38

› consulting firms. insurance strategy executives who are exploring the potential of digital technology for cutting costs, growing revenues, or changing business models are likely to turn to their traditional management and strategy consulting partners. Most of the major consultancies claim to be “end-to-end” with capabilities spanning strategy development through deployment. Consultancies are known for their strengths: McKinsey excels at strategy, tata Consultancy services stands out for its implementation, and the consulting arms of the big accounting firms like Deloitte and PwC excel at regulatory and risk-related work. however, in digital business transformations, consultancies need to demonstrate both deep industry and relevant technology expertise to deliver great customer experiences and operational agility.39

› Integration and delivery service providers. Many insurers are constrained in their digital efforts by legacy systems like policy administration, billing, or claims systems. integration service providers like accenture, Cognizant, hCl technologies, infosys, and tata Consultancy services promise to revamp customer-facing applications by improving integration with back-end systems and connecting disparate customer data stored in product-specific data siloes. Most system integrators want to deliver more than back-end integration and have been building their digital capabilities by acquiring digital agencies.40 Deep industry expertise is crucial, and the best partner is one that understands the strategic landscape of digital business integration and can determine how to apply it within your immediate context.41

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

13

Landscape: The Digital Insurance Strategy Playbook

recommendations

Digital Business teams Must think Beyond Digital Channels

While it’s OK to start small in firms where there is strong resistance to digital ambitions, digital insurance strategy professionals cannot allow this inertia to paralyze their firms. they need to elevate their firm’s digital responses and embrace digital transformation. Other chapters in this playbook will help you:

› Define a compelling digital business vision for your firm. it’s vital that you be able to describe how digitization will affect your business. you don’t need a digital strategy; you need to digitize your business strategy. Don’t just focus on digital customer experience. look at where new sources of data emerging from social media, connected devices, or government departments can drive operational agility and efficiency. think about how you can leverage the data you already hold to unlock new sources of customer value or build new revenue streams. your digital vision must encompass every aspect of how your firm does business.

› Assess your firm’s digital readiness to establish the size of the gap. Understanding the size of the gap is a vital step in planning your digital business transformation. Forrester’s digital business maturity model can help you establish your starting point by assessing your digital capabilities across your culture, organization, technology, and insight.42 it helps you identify crucial gaps and can also benchmark your position relative to your peers in insurance and in other industries. Proving that you are behind your competition can be a compelling driver for action and investment.

› Build a business case for digital transformation. to win the backing and resources needed for digital business transformation, digital insurance strategy teams will need to demonstrate potential returns on this sizable investment. they can measure the success of digital business transformation through increased revenues, reduced costs, improved time-to-market, or enhanced customer experience and differentiation.

› Think through your processes, organization, and metrics. Because digital business transformation is a journey and not a destination, much of the work involved is about embedding capabilities that will position you well for the future. rather than a one-off implementation of an agent portal or digital claims filing, for example, you need to become a more customer-focused, collaborative, and faster organization. this involves setting up new processes, governance models, or the way you measure your digital progress.

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

14

Landscape: The Digital Insurance Strategy Playbook

Engage With an analyst

gain greater confidence in your decisions by working with Forrester thought leaders to apply our research to your specific business and technology initiatives.

forrester’s research apps for iPhone® and iPad®

stay ahead of your competition no matter where you are.

Analyst Inquiry

to help you put research into practice, connect with an analyst to discuss your questions in a 30-minute phone session — or opt for a response via email.

learn more.

Analyst Advisory

translate research into action by working with an analyst on a specific engagement in the form of custom strategy sessions, workshops, or speeches.

learn more.

Webinar

Join our online sessions on the latest research affecting your business. Each call includes analyst Q&a and slides and is available on-demand.

learn more.

supplemental Material

Survey methodology

Forrester’s Consumer technographics® north american Financial services Customer life Cycle survey, Q2 2016 (Us) was fielded in april 2016. this online survey included 4,623 respondents in the Us between the ages of 18 and 88. For results based on a randomly chosen sample of this size, there is 95% confidence that the results have a statistical precision of plus or minus 1.4% of what they would be if the entire population of Us online adults (defined as those online weekly or more often) had been surveyed. Forrester weighted the data by age, gender, broadband, income, and region to demographically represent the Us online adult population. the survey sample size, when weighted, was 4,623. (note: Weighted sample sizes can be different from the actual number of respondents to account for individuals generally underrepresented in online panels.) gMi fielded this survey on behalf of Forrester.

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

15

Landscape: The Digital Insurance Strategy Playbook

Forrester conducted its European Consumer technographics Financial services survey 2, 2015, an online survey in august 2015 of 17,000 European individuals ages 16 to 99. For results based on a randomly chosen sample of this size, there is 95% confidence that results have a statistical precision of plus or minus 0.75% of what they would be if the entire population of European online adults (those online weekly or more often) had been surveyed.

Forrester conducted its north american Consumer technographics Financial services survey, 2015, an online survey fielded in september 2015 of 4,533 Us individuals ages 18 to 88. For results based on a randomly chosen sample of this size, there is 95% confidence that the results have a statistical precision of plus or minus 1.5% of what they would be if the entire population of Us online adults had been surveyed. Forrester weighted the data by age, gender, broadband adoption, income, and region to demographically represent the adult Us online population.

Forrester conducted its north american Consumer technographics Financial services Online Benchmark recontact survey, 2015, an online survey fielded in June 2015 of 9,717 Us individuals ages 18 to 88. For results based on a randomly chosen sample of this size, there is 95% confidence that the results have a statistical precision of plus or minus 0.99% of what they would be if the entire population of Us online adults (defined as those online weekly or more often) had been surveyed. Forrester weighted the data by age, gender, income, broadband adoption, and region to represent the adult Us online population.

companies Interviewed for This report

We would like to thank the individuals from the following companies and others who generously gave their time during the research for this report.

ageas

allstate insurance

aviva

Backbase

the Co-operators

Cuvva

Discovery insurance

guidewire software

the hartford Financial services

hCl technologies

hearsay social

infosys

legal & general

MaiF

nationwide Mutual insurance

next generation insurance

Policygenius

Prudential Corporation asia

saP

shelter Mutual insurance

slice insurance technologies

tata Consultancy services

trōv

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

16

Landscape: The Digital Insurance Strategy Playbook

Endnotes1 From the mischief caused by napster to the arrival of the iPhone and the (once improbable) reality of wearables and

self-driving cars, our world has changed — and so have your customers. Business leaders can no longer assume that consumers make rational decisions about which products to buy and use. today’s empowered customers no longer purchase products; they buy experiences. see the “the rise Of the Empowered Customer” Forrester report.

2 source: Forrester’s Consumer technographics north american Financial services Customer life Cycle survey, Q2 2016 (Us) and Forrester’s European Consumer technographics Financial services survey 2, 2015.

3 We asked Us online adults who had purchased insurance in the past 36 months how they originally found out about that product. Offline touchpoints include friends or family, a branch or office of a financial services provider, offline interaction with an insurance agent or financial advisor (over the phone or in person), direct mail, offline media advertisements or shows (e.g., tV, radio, newspaper, magazines), a real estate agent, or other offline way. source: Forrester’s Consumer technographics north american Financial services Customer life Cycle survey, Q2 2016 (Us).

4 Online touchpoints include the financial provider’s website, mobile website, or app; emails from a financial provider; a comparison shopping website (e.g., Bankrate.com, Creditcards.com, google Compare, insweb, lending tree); online interaction with an insurance agent or financial advisor (e.g., email or video chat); social media or blogs (e.g., Facebook, twitter, Pinterest, linkedin); online ads; online videos; online search results; and others. source: Forrester’s Consumer technographics north american Financial services Customer life Cycle survey, Q2 2016 (Us).

5 We asked 8,896 European online adults ages 18 and older (online weekly or more) who have purchased insurance in the past three years how they found information about or researched their most recent insurance purchase. source: Forrester’s European Consumer technographics Financial services survey 2, 2015.

6 We found that 62% of home insurance buyers in the Us state that they bought their most recent policy from an agent or financial advisor; the same proportion did the same for their most recent car insurance purchase, while 51% of life insurance buyers did so. source: Forrester’s Consumer technographics north american Financial services Customer life Cycle survey, Q2 2016 (Us). see the “loyal insurance agents Drive sales” Forrester report.

7 We asked 525 Us online adults who had purchased life insurance and 600 Us online adults who had purchased home insurance in the past 36 months which of the following, if any, described how they interact with the financial provider of their most recently purchased insurance. We found that 31% of home insurance customers and 30% of life insurance customers interact with their insurance company through email. source: Forrester’s Consumer technographics north american Financial services Customer life Cycle survey, Q2 2016 (Us).

8 source: Forrester’s Consumer technographics north american Financial services Online Benchmark recontact survey, Q3 2016 (Us).

9 the British insurance Brokers association (BiBa) surveyed the 30 leading telematics brands in the UK to determine the number of live policies currently in use in the market. the results showed a significant increase of 132,000 compared with the same time last year. there are now almost 455,000 live policies, compared with 323,000 in December 2014. source: “40% increase in telematics motor policies in a year,” BiBa press release, March 14, 2016 (https://www.biba.org.uk/latest-news/40-increase-in-telematics-motor-policies-in-a-year/).

smart wireless devices, smartphones, and smart cars have converged to create an alternative pricing model for the car insurance industry: usage-based insurance (UBi). UBi offers customers personalized insurance rates that are based on their driving behavior, using rating factors such as the time of day, the distance traveled, and their driving style. see the “telematics Will Disrupt the Car insurance industry” Forrester report.

10 source: Forrester’s European Consumer technographics Financial services survey 2, 2015.

11 Coverage can be purchased on the sure app for any flight up until the point of departure and is available up to one year in advance of travel. source: sure (https://www.sureapp.com/).

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

17

Landscape: The Digital Insurance Strategy Playbook

12 Most of these startups package, price, and sell insurance from established insurers and re-insurers. trōv works with suncorp group in australia, axa in the UK, and Munich re in the Us — which provide both financial backing and an insurance license. in germany, appsichern’s policies are underwritten by tokio Marine or Bayrische. Cuvva works with a panel of underwriters to offer the best possible hour rate. swiss re is the risk carrier and financer behind Community life in germany.

13 this data comes from a tracking device that could be a black box installed in the car, a self-installed onboard diagnostics device, or an app installed on a gPs-enabled smartphone. Each device delivers different value, with advantages and disadvantages in terms of price, installation, data collection capabilities, accuracy, and sharing feedback with customers. see the “telematics Will Disrupt the Car insurance industry” Forrester report.

14 Friendsurance, for example, boasts that its model incurs between 20% and 40% fewer claims than regular insurance. it passes the saving on to customers, claiming to cut the average individual insurance bill by half. in this way, it encourages customers to stay claim-free. source: “Friendsurance,” P2P Foundation, January 2, 2014 (https://wiki.p2pfoundation.net/Friendsurance).

social insurance enables people in need of insurance to connect and pool their money and risks. startups like Friendsurance, guevara, and tongJuBao facilitate this and aim to offer coverage that is cheaper, more transparent, and more relevant to the customer. eBusiness and channel strategy professionals should read this report to learn who the main players in this area are, assess their disruptive potential, and understand how to outsmart them. see the “Disrupting Finance: social insurance” Forrester report.

15 launched in late 2010, BiMa currently operates across 15 countries in africa, asia, and latin america, including ghana, senegal, tanzania, Uganda, Bangladesh, Cambodia, indonesia, Pakistan, Papua new guinea, the Philippines, sri lanka, Brazil, haiti, honduras, and Paraguay. source: BiMa (http://www.bimamobile.com/). see the “Disrupting Finance: Digital insurers” Forrester report.

16 source: Cuvva interview with Forrester, July 14, 2016.

17 When a user wants to protect an individual item in their trōv, they simply swipe right to initiate protection, swipe right again to claim, and swipe left to turn protection off. the chat has the advantage of being fully auditable. source: trōv (http://www.trov.com/).

18 hyperadoption is defined as the rapid and simultaneous uptake of unprecedented behaviors. new technologies like drones or wearables and the services that they afford us will be in common use — in many cases, by the hundreds of millions, and in a few cases, by the billions — by 2025. Keeping up with these changes will be challenging enough in its own right. you must also try to understand the unintended consequences of hyperadoption for your business. see the “Will People really Do that?” Forrester report.

19 time spent with media has continued to grow as young people began consuming content heavily across multiple devices simultaneously. now, with streams of information at her fingertips, the average adult consumes five times more content than she did 30 years ago. source: richard alleyne, “Welcome to the information age — 174 newspapers a day,” the telegraph, February 11, 2011 (http://www.telegraph.co.uk/news/science/science-news/8316534/Welcome-to-the-information-age-174-newspapers-a-day.html). see the “the rise Of the Empowered Customer” Forrester report.

20 today, consumers orchestrate their own mobile experiences by choosing apps, finding websites, or opting in for messaging. tomorrow, mobile will migrate from being a collection of standalone experiences that a single enterprise owns and controls to being a choreographer of blended experiences from an ecosystem of developers and vendors building on shared data to address mobile moments. see the “the Future Of Mobile: From app silos to Open Ecosystems” Forrester report.

21 WeChat is more than a social messaging app. Companies can use the platform to reinvent customer relationships, as it is a channel for advertising, payment, eCommerce, linking online to offline, and smart services. see the “reinvent Customer relationships With WeChat Mobile” Forrester report.

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

18

Landscape: The Digital Insurance Strategy Playbook

22 WeChat enables Metlife to facilitate direct-to-consumer product sales, advertise its brand, and integrate its service and social channels. see the “how Ecosystems Underpin Digital Business in insurance” Forrester report.

23 source: Forrester research Consumer Wearables Forecast, 2016 to 2021 (Us).

Wearables purchased by consumers matter to digital business professionals for two important reasons: 1) they will offer unprecedented longitudinal data of all kinds, and 2) they are a new medium to win, serve, and retain customers in their micro moments. this report includes a forecast of wearables sales volume for the next five years, including a discussion of the drivers and inhibitors of that growth. it concludes with a discussion of what it means for digital business professionals and recommendations for the near and long term. see the “Create a Micro Moments (not a Wearables) strategy” Forrester report.

24 seven percent of Us online adults report remotely accessing at least one of the following: all of the lights in their home (turn any/all lights on or off from anywhere); home security; climate control; remote home monitoring; remote appliance control; or energy management. source: Forrester’s north american Consumer technographics Devices and telecom Online Benchmark recontact survey, 2015.

the Us digital home continues to evolve, and Forrester has been tracking this evolution for more than a decade. year after year, we’ve witnessed the home becoming more digital and more connected. today, the vast majority of households have a home network with, on average, more than five devices connected to it, including PCs, tablets, and smartphones. the natural progression of the hyperconnected consumer is to create an even more connected home by trying out smart home devices. however, only a few households have adopted these. this report examines the digital home of today, profiles the early adopters of smart home devices across six use cases, and describes how device makers can drive greater adoption of smart home products. see the “the networked Digital home is Well Established, But the smart home is still nascent” Forrester report.

25 in the words of simon Morgan, head of property at UK insurer hiscox, “there has been an emergence of catastrophe rating tools from [risk modelling providers] rMs and air . . . these models have levelled the playing field. it is harder for an underwriter to differentiate himself from people with no experience.” source: Oliver ralph, “insurers plug in to domestic technology,” Financial times, May 16, 2016.

26 Opening up the Cuvva app lets users see which of their Facebook friends has a car available to borrow and how much that rental would be. Car owners can also share their car with friends and ask for a contribution toward running costs. source: Cuvva interview with Forrester, July 14, 2016.

27 this trend is picking up pace: some 12% of metropolitan Chinese online adults have used lodging marketplaces like airbnb, and 15% have used car sharing services like Car next Door. source: Forrester’s asia Pacific Consumer technographics Consumer technology, travel, and auto survey, 2015.

in the UK or in london, consumers are increasingly becoming contractors as they offer their services through platforms like taskrabbit.

28 Forrester predicts that these technologies will replace 16% of Us jobs but create the equivalent of 9%, which means we’ll lose a net 7% of Us jobs by 2025. see the “the Future Of White-Collar Work: sharing your Cubicle With robots” Forrester report.

29 source: “a guide to Cyber risk,” allianz (http://www.agcs.allianz.com/assets/PDFs/risk%20bulletins/Cyberriskguide.pdf).

30 We asked 571 global business and technology decision-makers, “Which of the following initiatives are likely to be your organization’s top business priorities over the next 12 months?” their responses range from 1 (not on our agenda) to 5 (critical priority). source: Forrester’s global Business technographics Priorities and Journey survey, 2016.

31 Forrester’s digital business maturity model groups companies into one of four levels, from the lowest maturity of digital skeptics (level 1) to the highest maturity of differentiators (level 4). ten percent of insurance companies are skeptics (level 1), and 61% are adopters (level 2), as compared with 8% and 42%, respectively, in all other industries. source: Forrester’s global Business technographics Marketing survey, 2015.

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

19

Landscape: The Digital Insurance Strategy Playbook

32 you need to transform your business by applying digital thinking across everything you do — how you win, serve, and retain customers; how you operate your internal processes; and how you source business services. in short, you must become a digital business. see the “the Digital Business imperative” Forrester report.

33 Vitality is a wellness platform for health and life insurers. Customers can link their fitness devices and loyalty programs to get rewarded for healthy living with points and discounts. Discovery has rolled out Vitality globally with its partners in the UK (initially through Prudential, but now Vitality is owned wholly by Discovery); in China with Ping an insurance; in eight asian countries with aia; in the Us with humana and John hancock; and in germany and France with generali. source: “Vitality history,” Vitality (http://www.thevitalitygroup.com/company/).

34 Because life products are generally more complex, they are seen as much more difficult for consumers to research and buy online. and digital efforts need to be tied to results. as one Us-based insurance executive told us, “it was my decision [to start with P&C]; that’s where the money comes from. if you’re going to invest, you find the place that will give you the highest returns.” One north american insurer sees the biggest growth and revenue potential in small business and commercial insurance, so that’s “where they try to lead in digital.”

35 in early 2015, MassMutual unveiled a new digital insurance agency, haven life. Operating as an independent business unit in new york City, haven life is chartered to sell a MassMutual-issued term life policy to Massachusetts residents. the policy was created and optimized to render an immediate decision on applications. the Massachusetts results were strong enough for haven life to expand into eight additional states in October 2015. see the “haven life rethinks life insurance Distribution For a Millennial World” Forrester report.

36 Forrester defines digital experience platforms as software to manage, deliver, and optimize digital experiences consistently across every phase of the customer life cycle. Professionals responsible for delivering great digital experiences need an array of software to create and manage them. they must evaluate, implement, integrate, and build front-end experiences from a fragmented product landscape. tech vendors try to help by bringing more complete digital experience portfolios to the market. see the “Vendor landscape: Digital Experience Platforms” Forrester report.

37 in Forrester’s 40-criteria evaluation of digital experience platform vendors, we identified the 10 most significant software providers — acquia, adobe, Demandware, EPiserver, iBM, Oracle, saP hybris, salesforce, sDl, and sitecore — in the category and researched, analyzed, and scored them. see the “the Forrester Wave™: Digital Experience Platforms, Q4 2015” Forrester report.

38 Delivering digital customer experiences across branded digital touchpoints, primarily web and mobile, requires a unique set of skills: customer experience strategy, user experience (UX), implementation of key digital experience and marketing technologies, front-end development, and customer analytics and optimization. see the “Market Overview: Digital Experience Delivery service Providers, 2015” Forrester report.

in Forrester’s 31 criteria evaluation of digital experience service providers, we identified the 11 most significant services providers in the category — accenture interactive, Deloitte Digital, DigitaslBi, iBM interactive Experience, infosys, isobar, MrM//McCann, razorfish global, sapientnitro, VMl, and Wipro — and analyzed their offerings. see the “the Forrester Wave™: Digital Experience service Providers, Q4 2015” Forrester report.

39 When technology is at the heart of the transformation, evaluate the industry knowledge of the consultancy specific to the systems you will use. For example, if you’re a $3 billion regional P&C insurer, knowledge of guidewire’s claims system for your region, products, and company size is far more valuable than simply having knowledge of guidewire and the P&C industry; it’s the combination that reduces the unknowns. see the “selecting your Business transformation Consultancy” Forrester report.

40 at recent customer and analyst events, traditional consulting and systems integration providers — including accenture, Capgemini, Cognizant, Deloitte Digital, Fujitsu, infosys, niit technologies, PwC, saP services, and Wipro — made major announcements about their digital services and digital transformation capabilities. these firms are scrambling to achieve growth and to win the mindshare (and wallet share) of business buyers. see the “Brief: Making sense Of the Digital services tsunami” Forrester report.

For EBusinEss & ChannEl stratEgy ProFEssionals

The State Of Digital Insurance, 2016october 17, 2016 | updated: December 7, 2016

© 2016 Forrester research, inc. unauthorized copying or distributing is a violation of copyright law. [email protected] or +1 866-367-7378

20

Landscape: The Digital Insurance Strategy Playbook

41 Digital business is much more than bolting on a new mobile app or predictive analytics. it requires deep, thorough preparation for rapid business reconfiguration in the face of an unknown, disruptive future. integration strategy is key to designing and delivering the business building blocks that drive business agility. see the “Vendor landscape: integration strategy and Delivery service Providers” Forrester report.

42 Forrester’s digital business maturity model 4.0 allows you to plot your organizational maturity, offers comparative benchmarks, and helps guide your actions to elevate your digital capabilities. see the “the Digital Maturity Model 4.0” Forrester report.

We work with business and technology leaders to develop customer-obsessed strategies that drive growth.

Products and services

› core research and tools › data and analytics › Peer collaboration › analyst engagement › consulting › events

Forrester research (nasdaq: Forr) is one of the most influential research and advisory firms in the world. We work with business and technology leaders to develop customer-obsessed strategies that drive growth. through proprietary research, data, custom consulting, exclusive executive peer groups, and events, the Forrester experience is about a singular and powerful purpose: to challenge the thinking of our clients to help them lead change in their organizations. For more information, visit forrester.com.

client suPPort

For information on hard-copy or electronic reprints, please contact client support at +1 866-367-7378, +1 617-613-5730, or [email protected]. We offer quantity discounts and special pricing for academic and nonprofit institutions.

Forrester’s research and insights are tailored to your role and critical business initiatives.

roles We serve

Marketing & Strategy ProfessionalscMoB2B MarketingB2c Marketingcustomer experiencecustomer insights

› eBusiness & channel strategy

Technology Management Professionalscioapplication development & deliveryenterprise architectureinfrastructure & operationssecurity & risksourcing & vendor Management

Technology Industry Professionalsanalyst relations

131963