The SKF Group

32

29 January 2009 1

-

Upload

ria-english -

Category

Documents

-

view

17 -

download

0

description

The SKF Group. Year-end results 2008 Tom Johnstone, President and CEO. Summary. Record sales and profit full-year 2008. Weakening markets by the end of the year. Acquired: Cirval S.A., GLO s.r.I., PEER Bearing company, QPM Aerospace’s metallic rod business. - PowerPoint PPT Presentation

Transcript of The SKF Group

29 January 2009

1

The SKF Group

Year-end results 2008

Tom Johnstone, President and CEO

29 January 2009

3Summary

• Record sales and profit full-year 2008.

• Weakening markets by the end of the year.

• Acquired: Cirval S.A., GLO s.r.I., PEER Bearing company, QPM Aerospace’s metallic rod business.

• Announced two new energy efficient roller bearing types.

• Signed a new contract in China with the world’s largest trailer axle manufacturer, Guangdong Fuwa Engineering Manufacturing Co. Ltd

• Announced investments for the first SKF factory in Russia and for expanding the capacity for manufacturing of large size bearings in China, Sweden and Germany.

• Distributed SEK 4,554 m to shareholders.

• Six Sigma, annualized savings SEK 462 m (up >50% from 2007)

• Included in Dow Jones Sustainability Indexes for the ninth year in succession.

29 January 2009

4

SEKm 2008 2007

Net sales 16,307 15,070

Operating profit 1,450 1,831

Operating margin 8.9% 12.1%

Profit before taxes 1,107 1,710

Net profit 819 1,105

Basic earnings per share, SEK 1.75 2.33

Cash flow after operating investments before financial items -150 617

Cash flow after operating investments before financial items, excluding acquisitions

18 1,123

Fourth quarter 2008

29 January 2009

5

SEKm 2008 2007

Net sales 63,361 58,559

Operating profit 7,710 7,539

Operating margin 12.2% 12.9%

Profit before taxes 6,868 7,138

Net profit 4,741 4,767

Basic earnings per share, SEK 10.14 10.09

Cash flow after operating investments before financial items 65 2,126

Cash flow after operating investments before financial items, excluding acquisitions

1,349 3,335

Full year 2008

29 January 2009

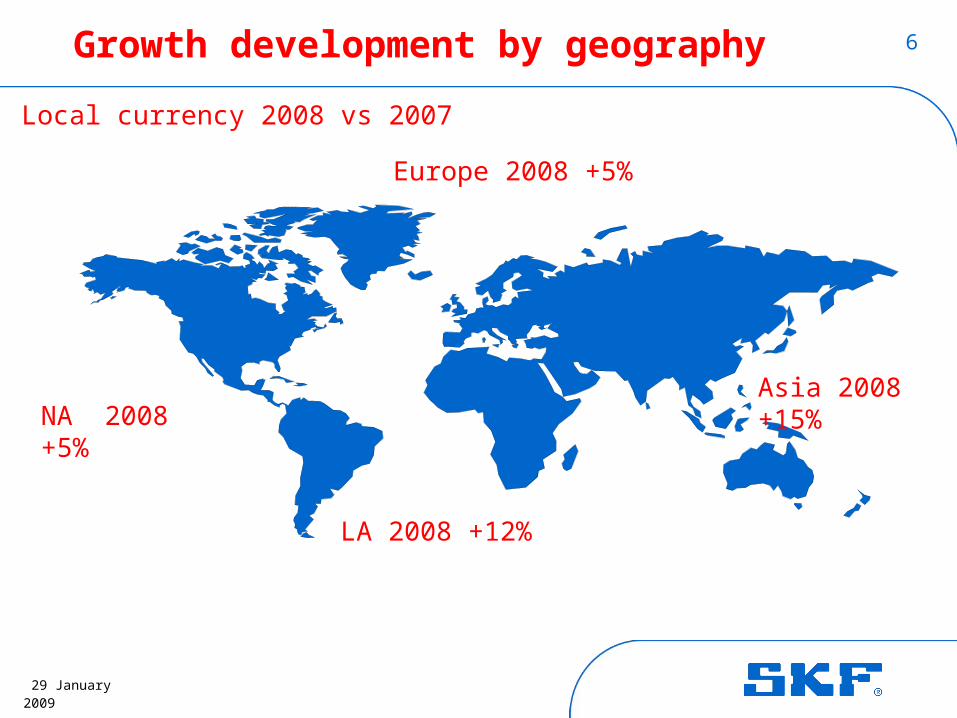

6Growth development by geography

Europe 2008 +5%

NA 2008 +5%

Asia 2008 +15%

LA 2008 +12%

Local currency 2008 vs 2007

29 January 2009

7

02468

101214

2006 2007 2008

Growth in local currency

% Y-o-Y

Acquisitions/DivestmentsOrganic growth

7.5*

13.2

* Excluding effect from Ovako:2006 10.1%

Long-term target level: 6-8% per annum

7.1

29 January 2009

8Sales in local currencies (excl. structural changes)

-6

-4

-2

0

2

4

6

8

10

12% change y-o-y

2006 2007 2008

29 January 2009

9Components in net sales

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

6.0 2.5 3.3 8.8 7.9 6.9 9.0 6.3 4.9 6.2 2.7 -13.0

-4.9 -0.5 1.1 4.6 4.0 4.6 3.7 1.0 1.0 1.3 0.5 2.4

2.9 2.0 2.0 2.3 1.8 2.7 2.0 3.2 3.8 4.0 6.4 8.5

4.0 4.0 6.4 15.7 13.7 14.2 14.7 10.5 9.7 11.5 9.6 -2.1

8.0 1.0 -2.1 -5.8 -5.6 -2.3 -1.9 -2.0 -1.2 -4.1 -0.9 10.3

12.0 5.0 4.3 9.9 8.1 11.9 12.8 8.5 8.5 7.4 8.7 8.2

Percent y-o-y

Volume

Structure

Price / Mix

Sales in local currency Currency

Net sales

2006 2007 2008

29 January 2009

10Operating margin

0

2

4

6

8

10

12

14

2006 2007 2008

%

* excluding income from the jointly controlled company Oy Ovako Ab

12.6 12.9

11.3*

12.2

Long-term target level: 12%

29 January 2009

11Operating margin

%

0123456789

1011121314

2006 2007

Long-term target level: 12%

2008

29 January 2009

12

-12

-7

-2

3

8

13

18

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Operating margin per division

Industrial

Service

Automotive

%

2006 2007 2008

Excluding one-off items (eg. restructuring, impairments, capital gains)

29 January 2009

13Industrial Division

Acquisitions

• QPM Aerospace’s metallic rod business

SEKm 2008 2007

Net sales 22,748

19,693

Sales incl. intra-Group sales

33,260

29,157

Operating profit 3,929 3,434

Operating margin 11.8% 11.8%

Q4 2008Net sales growth 23.1%15.5%

organic growth 6.8% 10.2% structure 2.3% 3.0%currency effects 14.0% 2.3%

Major investments

• New factory in Ahmedabad, India• New factory in Tver, Russia• Increase the manufacturing capacity in Dalian, China • Investments in large size bearings in Sweden and Germany

• In Q4 2007, SEK 30 m in restructuring activities and other one-time items.

• In Q4 2008, SEK 80 m in restructuring activities and other one-time items.

29 January 2009

14Service Division

Acquisitions

• Cirval S.A.

SEKm 2008 2007

Net sales 21,529

19,339

Sales incl. intra-Group sales

23,670

21,136

Operating profit 3,444 2,860

Operating margin 14.6% 13.5%

Q4 2008Net sales growth 11.3%11.3%

organic growth 2.0% 10.9% structure 0% 0.3%currency effects 9.3% 0.1%

New activities

• Established the first SKF Solution Factory in Shanghai.• Launched the SKF Certified Rebuilder programme for electric motors in Europe and South Africa.• Launched the Distributor Value Program to support SKF authorized distributors in documenting the value they bring to customers.

29 January 2009

15Automotive Division

Acquisitions

• GLO s.r.l• SKF Automotive Bearings

Company Ltd.

SEKm 2008 2007

Net sales 18,727 19,449

Sales incl. intra-Group sales

23,215 23,703

Operating profit 627 1,135

Operating margin 2.7% 4.8%

Major investments

• Opened a new factory in China• Established new technology centre in China and expanded centre in India.

• In Q4 2007, SEK 270 m in restructuring activities and other one-time items.

• In Q4 2008, SEK 250 m in restructuring activities and other one-time items.

Q4 2008Net sales growth -16.3%-3.7%

organic growth -22.9% -3.8% structure 0.2% -0.5%currency effects 6.4% 0.6%

29 January 2009

16Activities to adapt to lower demand

Announced in Q4 2008: • Short-time working: 2,400 employees

Reduction: 2,500 employees (whereof: 1,300 temporary and 1,200 registered)

• Restructuring and impairment costs of SEK 470 m, whereof SEK 340 m in Q4 2008. Full-year benefit SEK 250 m in 2010

Implemented in 2008:• Reduction of temporary workers: 200 during Q3

550 during Q4• Reduction of registered employees: 500 during Q4

.

29 January 2009

17Currency effects on the balance sheet EUR/SEK, Close

05 06 07 08 098.5

9.0

9.5

10.0

10.5

11.0

11.5

USD/SEK, Close

05 06 07 08 095.5

6.0

6.5

7.0

7.5

8.0

8.5

The currency effects on working capital and fixed assets were around 10% for the fourth quarter and 12% for the year.

This has had an impact on ratios.

29 January 2009

18

18

19

20

21

22

23

24

25

Inventories as % of annual sales

%

2006 2007

Long-term target level: 18%

2008

x excl. currency effects

29 January 2009

19Return on capital employed

23

24

25

26

2006 2007 2008

ROCE: Operating profit plus interest income, as a percentage of twelve months average of total assets less the average of non-interest bearing liabilities.

%

Long-term target level: 24%

29 January 2009

20Net debt (Short-term financial assets minus loans and post-employment benefits)

-16,000

-14,000

-12,000

-10,000

-8,000

-6,000

-4,000

-2,000

0

SEKm

AB SKF, dividend paid (SEKm):2006 Q2 1,8212007 Q2 2,0492008 Q2 2,277

Redemption (SEKm):

2007 Q2 4,5542008 Q2 2,277

2006 2007 2008

29 January 2009

21Cash flow, after operating investments before financial items

-700

-500-300

-100

100300500

700900

1,100

1,3001,500

1,700

2006 2007

SEKm

Cash out fromacquisitions (SEKm): 2006 2,1292007 1,2092008 1,284

Cash in from Ovako (SEKm):2006 Q4 1,2172007 Q2 46

2008

29 January 2009

22SKF capital structure

• a dividend of SEK 3.50 per share

• a mandate to the Board to repurchase a maximum of 5% of the company's own shares

The AB SKF Board proposes the AGM to decide on:

29 January 2009

232009 – external environment

• Global, deep and very fast downturn in demand

• Financial markets are not stable yet

• Government incentives still to take effect

• Consumer and business confidence low

• Good demand continues in some areas

Uncertain business environment - difficult to forecast

29 January 2009

24Vehicle production outlook

Light vehiclesQ408

EstimatedQ109

Forecast

Western Europe -28% -27%

North America -24% -42%

Heavy vehiclesQ408

EstimatedQ109

Forecast

Western Europe: -14% -33%

North Americaof which Class 8

8%-2%

-28%-33%

Source: JD Power, December 2008

Source: Global Insight 28 January 2009

29 January 2009

25January 2009: Outlook for the first quarter 2009

The demand for SKF products and services is expected to be significantly lower for the Group in total and for all regions. It is also expected to be significantly lower for the Automotive and Service Divisions and lower for the Industrial Division.

The manufacturing level will be significantly lower to reflect both the new demand situation and to reduce inventory.

29 January 2009

26Volume trends(based on current assumptions)

Daily volume trends for: Q4 2008 Q1 2009

Net sales2008

Europe

56%

North America

17%

Asia Pacific

19%

Latin America

5%

Total

Outlook Q12009 vs

2008

---

---

--

---

---

29 January 2009

27

13% Cars

5% Trucks

20% Industrial OEM,

General+Special

3% Electrical and two-wheeler

9% VSM

23% Industrial distribution

12% Industrial OEM, Heavy+Off-

highway

5% Aerospace

3% Railway

6% Energy

Expected demand by main segment – Q1 2009(based on current assumptions) Net sales 2008

29 January 2009

28Guidance for the first quarter 2009

• Tax level: 31-32%

• Financial net for first quarter:SEK -200 million

• Exchange rates on operating profit versus 2008Q1: SEK 200 million

Full year: SEK 1 billion

• Additions to PPE: Around SEK 2 billion for 2009

Guidance is approximate and based on current assumptions and exchange rates

29 January 2009

29Key focus areas ahead - 2009

• Profit and cash flow- maintain positive price/mix- drive operational efficiency and cost reduction- reduce working capital and investments

• Adjustment of manufacturing output to new demand levels- restructuring- short-time working

• Growing segments and geographies

• Strengthening the platform/segment approach

• Competence development

SKF Care and Six Sigma as guiding lights

29 January 2009

30SKF Care

Employee Care

Community CareEnvironmental Care

Business Care

BeyondZeroT

M

0

2

4

6

8

10

12

14

2003 2004 2005 2006 2007 2008

SKF Care

Operating margin

29 January 2009

31SKF Group Vision

To equip the worldwith SKF

knowledge

29 January 2009

32