1 the Structural Characteristics of Farmer Cooperatives and Their Behavioral Consequences

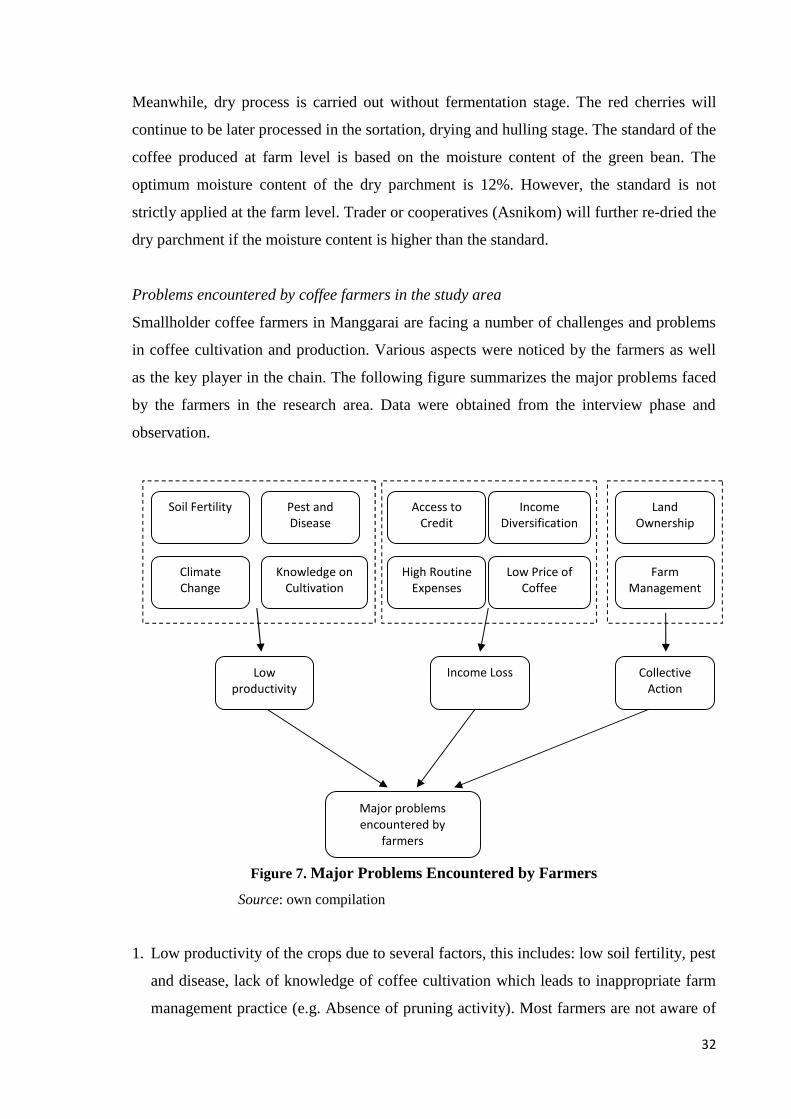

Academic year 2014-2015

The Role of Farmer Cooperatives in the Development ofCoffee Value Chain in East Nusa Tenggara Indonesia

Yuniarti Pratiwi, Sisilia Ita

Promotor : Prof. Dr. Wolfgang Bokelmann

Thesis submitted in partial fulfilment of the requirementsfor the joint academic degree of International Master of Science in Rural Development from Ghent

University (Belgium), Agrocampus Ouest (France), Humboldt University of Berlin (Germany),Slovak University of Agriculture in Nitra (Slovakia) and University of Pisa (Italy) in collaboration with

Wageningen University (The Netherlands),

i

ACKNOWLEDGEMENT

First of all, I would like to express my sincere gratitude to my supervisor, Prof.

Wolfgang Bokelmann, for his kind support and guidance throughout the process. Further, I

am also grateful to IMRD secretariat, all the professors and coordinators in Ghent

University, University of Pisa, and Humboldt University of Berlin for their continuous

support during the study period.

I also extend my thanks to Lembaga Penyaluran Dana Pendidikan (LPDP) Indonesia

for providing me an opportunity to study in the IMRD program with financial support. My

sincere thanks also go to my group of fellow students of IMRD, I have been blessed with

such friendly and cheerful fellow students.

In Manggarai, Indonesia, I would like to offer my gratitude to all respondents, the

officials of Department of Estate Crops and Horticulture Manggarai Regency, Asnikom,

and UD. Indokom Flores for providing me a valuable information during my data

collection. A special thanks to my new family and friends in Manggarai for sharing a

sincere help, encouragement and guidance during my field work.

And most of all, many thanks to my beloved parents for their loving support,

encouragement and attention for me to achieve my dreams. I attribute all my success in life

to the moral, intellectual and physical education I received from them. I would also like to

thank my beloved brother, my partner, and all of my friends. Thank you for always being

there cheering me up and stood by me during good and bad times.

Yuniarti Pratiwi, Sisilia Ita

Berlin, July 2015

ii

ABSTRACT

Coffee sector has been contributing a substantial value to the livelihood of the rural

people. However, smallholder farmer in the coffee sector often finds barriers and

challenges to elevate their situation in the worldwide marketplace. This thesis is a study of

the role of farmer cooperatives in the development of value chain in Manggarai, East Nusa

Tenggara, Indonesia. It specifically uses the value chain analysis as the comprehensive

method to see the existing coffee value chain in the study area.

Several actors accounted to be the key player of the coffee value chain in the study

area, such as trader and exporter. Referable to the market liberalization, the

trader/middleman has an enormous advantages, to reap the benefits of smallholder farmers.

This unfavorable situation for smallholder farmers, therefore, became the driving force on

the involvement of farmer cooperatives in the coffee value chain.

Following this, the theoretical, conceptual and analytical background used in the

study try to illustrate and portray the role of farmer cooperatives in the coffee value chain.

Farmer cooperatives are found out to be the actor which enables the farmer to develop their

production and processing system via certain functions offered by the cooperative in the

context of value chain development, such as: access to financial resources; provision of

farm input, knowledge, and market information; and networking access. Farmer

cooperatives are also able to improve the value chain through process and product

upgrading. Along with the involvement of farmers in the cooperatives, they also engaged

in the value chain development. Nevertheless, an extensive coordination between players

in the value chain is important to reinforce the learning procedure. Therefore, farmer

cooperatives can be a central player in order to maintain the coordination system in the

coffee value chain.

iii

TABLE OF CONTENTS

ACKNOWLEDGEMENT.......................................................................................................... i

ABSTRACT............................................................................................................................... ii

LIST OF FIGURES ....................................................................................................................v

LIST OF TABLES.....................................................................................................................vi

ABBREVIATIONS ..................................................................................................................vii

1. INTRODUCTION ................................................................................................................1

1.1. Overview of Coffee Sector in Indonesia ......................................................................2

1.2. The Development of Coffee Sector in Indonesia, Government Policy and State

Institutions ................................................................................................................... 4

1.3. Problem Statement........................................................................................................5

Objectives and Research Questions..............................................................................6

1.4.Outline of the Study Report ............................................................................................7

2. REVIEW OF LITERATURE ...............................................................................................8

2.1. Theoretical Framework.................................................................................................8

2.1.1. The Concept of Value chain ...............................................................................8

2.1.2. Governance of Value Chain..............................................................................10

Governance and Coordination of Value Chain.................................................12

2.1.3. Upgrading the Value Chain ..............................................................................13

2.1.4. Smallholders and Farmers Cooperatives ..........................................................14

2.2. Empirical Evidences ...................................................................................................18

2.3. Remarks from Literature Review ...............................................................................20

3. METHODOLOGY .............................................................................................................21

3.1. Conceptual Framework...............................................................................................21

3.2. Research Methods.......................................................................................................22

3.2.1. Sampling Procedure..........................................................................................24

3.2.2. Description of Data Analysis ............................................................................25

3.3. Limitations of the Study ............................................................................................26

4. RESULTS ...........................................................................................................................27

4.1. Size and Structure of Smallholder Coffee Farms .......................................................27

4.2. Mapping of the Coffee Value Chain...........................................................................29

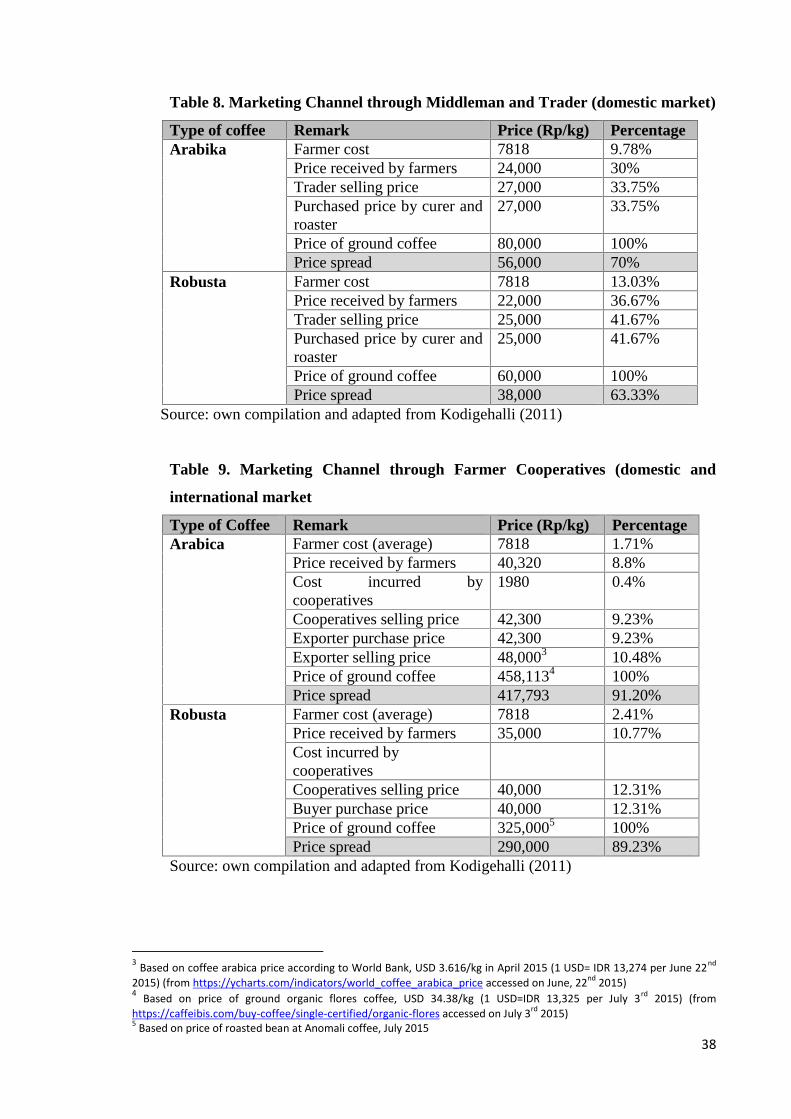

4.3. Price Spread and Value Addition of Coffee ...............................................................36

iv

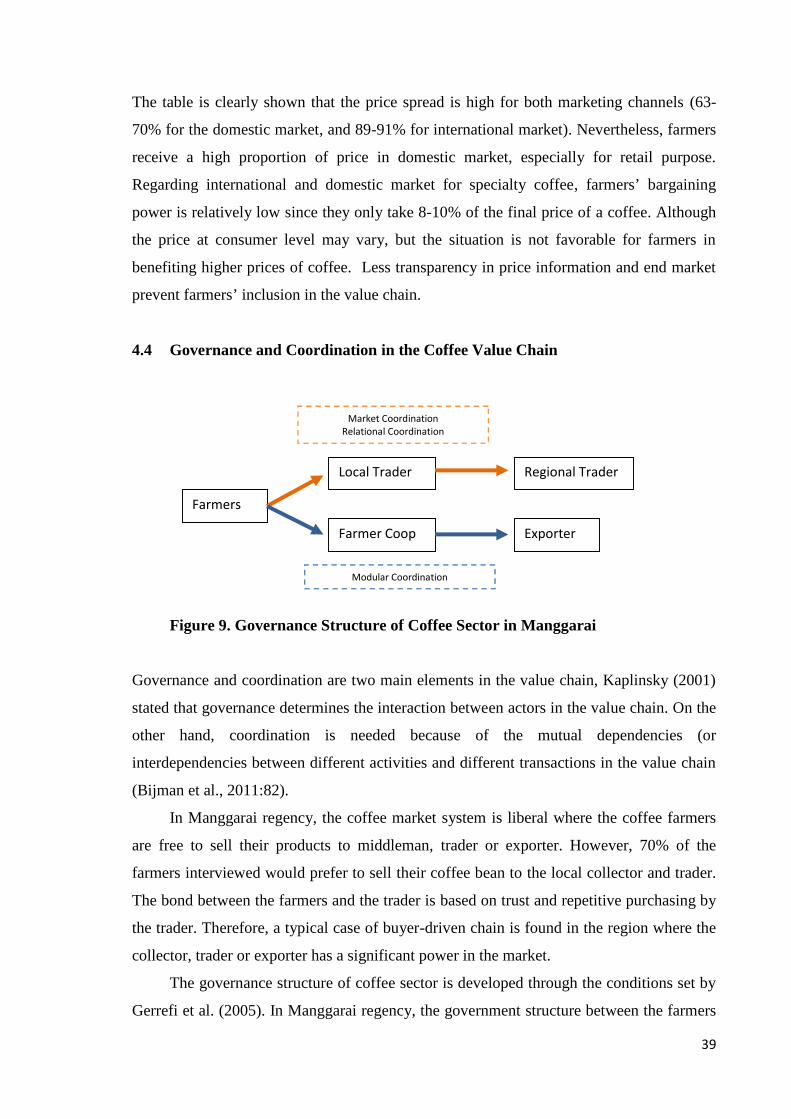

4.4. Governance and Coordination in the Coffee Value Chain .........................................39

4.5. SWOT Analysis of the Coffee Value Chain...............................................................40

5. DISCUSSION.....................................................................................................................43

5.1. The Role of Farmer Cooperatives in the Development of Coffee Value Chain.........43

5.2. Determinants of the Farmer’s Inclusion and Participation in Cooperative ................47

5.3. Opportunities for Upgrading the Coffee Value Chain................................................50

6. SUMMARY AND CONCLUSIONS .................................................................................53

6.1. Summary.....................................................................................................................54

6.2. Conclusions.................................................................................................................55

6.3. Recommendations for Future Research ......................................................................55

REFERENCES .........................................................................................................................57

ANNEXES................................................................................................................................61

v

List of Figures

Figure 1. Total Coffee Production by Top 10 Producing Countries...........................................1

Figure 2. Coffee Production in Different Region in 2013 ..........................................................3

Figure 3. Conceptual Framework in the Coffee Value Chain ..................................................22

Figure 4. Map of the Study Region in Manggarai, East Nusa Tenggara, Indonesia ................23

Figure 5. Mapping of Coffee Value Chain in Manggarai ........................................................29

Figure 6. Schematic View of Arabica Coffee Processing ........................................................31

Figure 7. Major Problems Encountered by Farmers.................................................................32

Figure 8. The Number of Coffee Traded to Another Island (outside Flores) ...........................35

Figure 9. Governance Structure of Coffee Sector in Manggarai ..............................................39

vi

List of Tables

Table 1. Farm Size and Coffee Production in Indonesia (2008-2013) .......................................4

Table 2. Key Determinants of Global Value Chain Governance .............................................11

Table 3. Service Provided by Farmer Organizations................................................................16

Table 4. General Characteristics of the Study Area..................................................................24

Table 5. Data Sources for the Study .........................................................................................25

Table 6. Farm Size and Coffee Production in East Nusa Tenggara .........................................28

Table 7. The Size of Coffee Cultivation in Manggarai Regency..............................................28

Table 8. Marketing Channel through Middleman and Trader ..................................................38

Table 9. Marketing Channel through Farmer Cooperatives .....................................................38

vii

ABBREVIATIONS

AEKI: Asosiasi Eksportir Kopi Indonesia (Association of Indonesian Coffee Exporters)

ASNIKOM: Asosiasi Petani Kopi Manggarai (Associations of Coffee Farmers in

Manggarai)

GDP: Gross Domestic Product

Ha: Hectare

ICO: International Coffee Organization

IDR: Indonesian Rupiah

INDOKOM: UD. Indokom Flores/PT. Indokom Citra Persada

USD: United States Dollar

SWOT: Strengths, Weaknesses, Opportunities and Threats analysis

1

CHAPTER 1. INTRODUCTION

According to World Bank (2004), coffee is one amongst the world’s most important

commodities traded in nearly 60 countries. Coffee is considered as “the top cash crop in

developing countries”. Therefore, it emphasizes the value of coffee in economic sector in

the developing countries (Wahyudi and Jati, 2012: 6). Coffee also plays an important role

in the livelihood of smallholder farmers. International Coffee Organization noted that

coffee supports millions of smallholder farmers and generate immense employment

opportunities in rural areas (Kodigehalli, 2011:1). As depicted by (Rice, 2003),

smallholder still predominate the global coffee world, frequently supplying the volume of a

producing country’s coffee harvest, along with the massive percentage of any rural farm

labor. Smallholder coffee growers spread across the rural landscapes in Asia, Latin

America and Africa with less than 10 hectares of land (Rice, 2003:230).

The fact that the major quantity of world coffee production is directed towards the

export market indicates the importance of coffee as an export commodity (Kodigehalli,

2011:1). In international market, the global top 10 producing countries are Brazil, Vietnam,

Indonesia, Colombia, Ethiopia, India, Honduras, Mexico, Uganda, and Guatemala. In that

sense, developing countries carry out over than 90% of the world’s coffee production.

Meanwhile, the majority of the coffee consumers are in the developed and industrialized

countries.

Figure 1. Total Coffee Production by Top 10 Producing Countries (in thousand 60 kg bags)

Source: International Coffee Organization (2014)

45,342

9,00012,500

6,6253,500 5,400 5,517 3,900 3,800

27,500

05,000

10,00015,00020,00025,00030,00035,00040,00045,00050,000

2

In 2005, the demand of coffee was increased, although the coffee production in some

countries was rather stagnant or slightly declined. During the 2005/2006, the ICO forecast

the demand excess supply situation. ICO estimated the world production at around 105

million bags, compared to world demand of 114 million bags (Slob, 2006:8). In the context

of economic contribution, Rice (2003) described the fact that coffee continues to generate

significant private and public revenues. However the situation failed to address the social

and environmental sides of the commodity. For example, the production surplus from the

previous year has had devastating social consequences for millions of coffee growers, the

downstream business dependent upon these producers, and countries whose foreign

exchange depends upon the crop (Rice, 2003:223).

1.1 Overview of Coffee Sector in Indonesia

Historically, coffee is not a domestic plant in Indonesia. Yet, over time coffee has spread in

most regions in Indonesia. According to Iqbal (2011), Indonesia has been produced

Arabica and Robusta coffee since the Dutch colonization during the 1696-1699. Coffee

was introduced by the Dutch Royal East Indies Company (Verenigde Oostindische

Compagnie or VOC) for research purposes. Subsequently, through the program cultur

stelsel (forced planting policy), coffee crops began to disseminate across the country

(Iqbal, 2011:1).

As one amongst the top producing countries in the world, Indonesia is currently

being the world’s second largest Robusta exporter after Vietnam. While for Arabica,

Indonesia is ranked fourth after Brazil, Vietnam and Colombia. The overall production in

2010 was estimated to about 685 thousand tons (Arifin, 2013:87). Regarding this number

of coffee production, Indonesia could play a role to cover the rising demand of coffee.

Coffee sector also occupies an important contribution towards economic situation.

Coffee is one of Indonesia’s main export-driven commodities. The volume of export in

2013 amounted to be 532,139 tonnes. The value of exports reached USD 1,166,179

(National Statistics Agency, 2013). Robusta contributes 85% of the coffee production in

Indonesia, and mostly comes from the production center in Lampung province. And the

remaining 15% is Arabica production in highland areas in Aceh, North Sumatera, South

Sulawesi, Kintamani highland in Bali and Bajawa highland in Flores East Nusa Tenggara

(Arifin, 2003:87).

With the perfect climate to cultivate coffee, coffee can be planted anywhere in

Indonesia despite the location of producing regions which are relatively dispersed. The

3

primary coffee producing provinces in Indonesia are South Sumatra, Lampung, Bengkulu

and Aceh. East Nusa Tenggara ranked seventh after East Java and South Sulawesi (Iqbal,

2011:2). Sumatra dominates the coffee production with 74.2%, then followed by Sulawesi

9.0%, Java 8.3%, Nusa Tenggara 5.8%, Kalimantan 2.0%, and Maluku and Papua 0.6%. In

general, the taste of coffee depends on various factors, this includes: climate condition; soil

condition; cultivation techniques; and post harvest handling. Therefore, each region may

produce a variety of specialty coffees such as Java, Mandheling, Gayo, Flores, Lintong,

Kintamani, Toraja, etc. (Wahyudi and Jati, 2012:3). Flores coffee is renowned as best-taste

coffee among other Indonesian coffee. The characteristics of Flores coffee are chocolaty,

sweet, fruity, and has slightly citrus aftertaste. Flores coffee grows at altitudes between

1200-1800 meters above sea level (Wahyudi and Jati, 2012:6).

Figure 2. Coffee Production in Different Region in 2013 (000 tonnes)

Source: National Statistics Agency (BPS) Indonesia (2013)

The coffee plantation in Indonesia is still dominated by smallholder plantation.

Smallholders accounted 90.1% of coffee production in Indonesia while the rest

respectively developed by government (6%) and private sectors (3.9%) (Iqbal, 2011:2).

Coffee production by smallholder farmers is mostly located in rural areas, especially in the

dry and mountainous area. The number of coffee farmers in Indonesia is 1.97 million with

an average of 0.6 Ha of land ownership. Furthermore, assuming family member of coffee

Aceh9%

Sumatera Utara10%

Sumatera Barat5%

SumateraSelatan

24%Bengkulu

10%

Lampung23%

Jawa Timur9%

Nusa TenggaraTimur

4%

Sulawesi Selatan6%

4

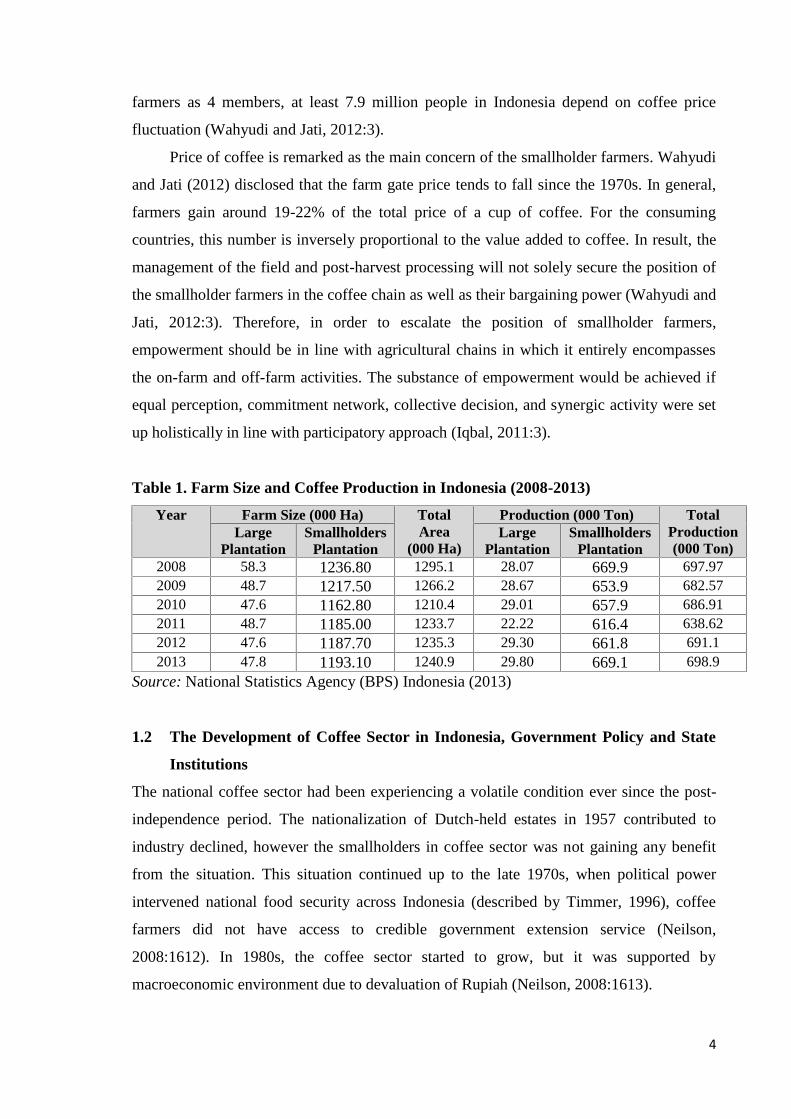

farmers as 4 members, at least 7.9 million people in Indonesia depend on coffee price

fluctuation (Wahyudi and Jati, 2012:3).

Price of coffee is remarked as the main concern of the smallholder farmers. Wahyudi

and Jati (2012) disclosed that the farm gate price tends to fall since the 1970s. In general,

farmers gain around 19-22% of the total price of a cup of coffee. For the consuming

countries, this number is inversely proportional to the value added to coffee. In result, the

management of the field and post-harvest processing will not solely secure the position of

the smallholder farmers in the coffee chain as well as their bargaining power (Wahyudi and

Jati, 2012:3). Therefore, in order to escalate the position of smallholder farmers,

empowerment should be in line with agricultural chains in which it entirely encompasses

the on-farm and off-farm activities. The substance of empowerment would be achieved if

equal perception, commitment network, collective decision, and synergic activity were set

up holistically in line with participatory approach (Iqbal, 2011:3).

Table 1. Farm Size and Coffee Production in Indonesia (2008-2013)

Year Farm Size (000 Ha) TotalArea

(000 Ha)

Production (000 Ton) TotalProduction(000 Ton)

LargePlantation

SmallholdersPlantation

LargePlantation

SmallholdersPlantation

2008 58.3 1236.80 1295.1 28.07 669.9 697.972009 48.7 1217.50 1266.2 28.67 653.9 682.572010 47.6 1162.80 1210.4 29.01 657.9 686.912011 48.7 1185.00 1233.7 22.22 616.4 638.622012 47.6 1187.70 1235.3 29.30 661.8 691.12013 47.8 1193.10 1240.9 29.80 669.1 698.9

Source: National Statistics Agency (BPS) Indonesia (2013)

1.2 The Development of Coffee Sector in Indonesia, Government Policy and State

Institutions

The national coffee sector had been experiencing a volatile condition ever since the post-

independence period. The nationalization of Dutch-held estates in 1957 contributed to

industry declined, however the smallholders in coffee sector was not gaining any benefit

from the situation. This situation continued up to the late 1970s, when political power

intervened national food security across Indonesia (described by Timmer, 1996), coffee

farmers did not have access to credible government extension service (Neilson,

2008:1612). In 1980s, the coffee sector started to grow, but it was supported by

macroeconomic environment due to devaluation of Rupiah (Neilson, 2008:1613).

5

As described by Neilson (2008), the development of such form like cooperative in

Indonesia started from the “New Order” regime in 1966-1997. The government was

committed to economic development, thus village cooperatives (KUD-Koperasi Unit

Desa) were established across the nation. Nevertheless, the associations were highly

politicized by the authorities and further corruption practice and political misuse were

found after “New Order” regime. Although the coffee sector was never exposed to such

situation and intervention by the government, but the majority of Indonesian farmers was

becoming wary of any attempt at supply chain controlled by the government (Neilson,

2008:1613). In the 1989, International Coffee Organization (ICO) was the only channel for

the government to involve in the coffee sector. Export allocation was managed by the

Association of Indonesian Coffee Exporters (Asosiasi Eksportir Kopi Indonesia-AEKI),

however the favorable situation belonged to exporters with strong political connections.

Hence, when AEKI was no longer managing the export quota, the government-mandated

export levy provided additional benefit for those associations which was subject to very

little public financial accountability (Neilson, 2008:1613).

1.3 Problem Statement

In Indonesia agricultural sector, value-added has grown much slower than in the non-farm

economy. From 1990-2005, agricultural GDP grew at only 2.3% per year (WDR, 2008),

less than half 4.8% growth in aggregate GDP over this period (Barichello et al., 2009:37).

In the context of value-added activities, various issues have been confronted by the farmers

such as the insufficient technical knowledge to escalate the value of the product in a

sustainable way and to connect the wide-range market. On the other hand, the complexity

of marketing coffee has risen since the enforcement of product certification which leads to

constraints increment faced by smallholder farmers. Various research studies have been

carried out to see the functions of farmer’s group in term of providing support and services

to the farmers. However, this study mainly focused on the role of farmer cooperatives in

the context of value chain development and assistance to connect to market linkages.

Initially, the main objectives of the establishment of the farmers' group in Indonesia

was to support the livelihood of the rural farmers. Over the decade, the number of farmer

group has been increased. Even so, farmer groups are mainly established in Java and

Sumatera, and only cover the main agricultural product such as rice and horticultural

products. The case of low existence of farmer group in the cash crop sector is in line with

the low participation of the farmers in such group or association. The example can be

6

drawn from the study done by Hartatri and de Rosari (2011) who tried to see the Arabica

coffee industry in Manggarai and East Manggarai. Based on the research, less than 50% of

the coffee farmers join the farmers’ group (Hartatri and de Rosari, 2011:56). Therefore, it

is important to investigate the hindering force for farmers to involve in the collective action

organizations.

It is also important to point out the governance system of farmer cooperatives in

order to improve the value chain coordination. In many instances, the existing farmer

cooperatives are being challenged by the involvement of many actors along the value

chain. On one hand, many farmer cooperatives have been successfully delivered the role of

intermediaries. And on the other hand, some perform a minor role in the value chain

coordination. Further attention needs to be drawn on what are the determinants for the

farmer to involve in farmer cooperatives.

The study was carried out in Manggarai regency, part of the East Nusa Tenggara

province in Indonesia. The previous background will be used to carry out a research study

entitled “The role of farmer cooperatives in the development of coffee value chain in East

Nusa Tenggara Indonesia”. And the following key research question will be carried out

during the research study using in depth analysis of coffee value chain:

Research Questions:

How does the establishment of farmer cooperatives improve the coordination and

performance in the development of coffee value chain?

Therefore, with this background the research study aims to achieve the following

objectives:

To describe the coffee value chain in Manggarai East Nusa Tenggara and actors

involved in the chain (mapping)

To analyze the governance and coordination mechanism in the coffee value chain

To analyze the coffee value chain through SWOT analysis

To discuss the role of farmer cooperatives towards inclusion of smallholder coffee

farmers in the development of coffee value chain

7

1.4 Outline of the Study Report

The following study report is organized into seven main chapters. The first chapter consists

of a brief introduction of the coffee sector in the world and in Indonesia. It also provides

the description of the existing problem and the objectives of the study. The second chapter

provides the review of literature associated with the study objectives. Third chapter gives

an overview of the conceptual framework, feature of the study area, sampling and analysis

procedure of the data. The fourth chapter presents the empirical results, and based on the

literature review as well as data gained from study, discussion part is shown in chapter

five. Chapter six summarizes the entire research study and then followed by the

conclusions drawn in response to research findings. And the final chapter lists the sources

of research material, including papers, journals and books used in the research study.

8

CHAPTER 2. REVIEW OF LITERATURE

The following chapter has made an attempt to elaborate several theories and concepts used

in the study. A critical review of the previous research work is carried out in order to gain

better understanding of the subject. The theoretical evidences are drawn from the value

chain theory in conjunction with the theory of cooperative.

2.1 Theoretical Framework

2.1.1 The Concept of Value Chain

As described by Kaplinsky and Morris (2001), a value chain can be defined as “the full

range of activities which are required to bring a product or service from conception,

through the different phases of production, delivery to the final consumer and final

disposal after use”. The study in the value chain sector will improve the attempt to

understand the distribution of power and value in the chain and to be able to address the

agency of workers and small producers (Mitchell and Coles, 2011:11).

According to Kaplinsky (2004), the following key elements are important in value

chain which need to be recognized and which transform a heuristic into an analytical tool:

“Value chains are repositories for rent, and these rents are dynamic

Governance plays an important role to utilize the value chain

Effective value chains arise from systemic as opposed to point-efficiency” (Kaplinsky,

2004:9)

Given that coffee is one amongst the most important export commodity in most

developing countries, the concept of global value chain (GVC) is applicable to this

situation. Albeit the concept is relatively similar, global value chain distinct because its

activities that spread over international borders and not constrained within one country

(Mitchell and Coles, 2011:11). However, producers in developing country often face

important barriers in order to fulfil quality, standards and regulations in international

market. Several authors, notably, De Janvry and Sadoulet (2005), Daviron and Gibbon

(2002) and Reardon and Barret (2000) have described that lack of institutional and

infrastructural support, availability of resources and efficient and effective coordination in

value chain often hinders producers and smallholder farmers to increase their bargaining

position in the value chain (Trienekens, 2011:52).

9

Trienekens (2011:53) accounted several constraints for developing country producers

to upgrade the value chain. The constraints are associated with market access (local,

regional and international) and market orientation (described by Grunert et al., 2005),

available resources and physical infrastructures (described by Porter 1990) and institutions

(regulative, cognitive and normative; described by Scott 1995).

Market access and market orientation

According to Trienekens (2011), several factors such as technological capabilities of

producers, available infrastructures, bargaining power and market knowledge and

orientation determine the market access. Meanwhile, Grunert et al. (2005) characterized

the market orientation of the actors in the chain includes these key points: intelligence

generation referring to current and future end-user needs; dissemination of this

intelligence among the actors; and the responsiveness of the actors towards the needs of

the end-user (Grunert et al., 2005:430). The characteristics of the end-market will

likewise bear upon the activities carry out by the actors along the value chain.

Knowledge and willingness to comply with the demands in the value chain’s end-

market, thus will be conditional to participation in high value adding value chains

(referred to Grunert et al., 2006). For this cause, the key condition for the inclusion of

producers in the value chain is access to market information and the power to translate it

to market intelligence (Trienekens, 2011:55).

Resources and physical infrastructures

Access to market is not the one and only factor for producers in order to sell their

products in the broader market. According to Trienekens (2011), supporting

infrastructures, resources, including knowledge and capabilities are substantial to

generate a successful value chain. Furthermore, this determined by three different

aspects such as low level of available physical resources (e.g. Input materials and

supplies), the geographical location of the producers, availability of educated labor and

the availability of knowledge, and the level and availability of technology that can be

used for production and distribution activities in the value chain (Trienekens, 2011:55).

Institutional voids

Mair and Marti (2008) defined the institutional voids as the failure of the institutional

arrangements to support the market mechanism (Trienekens, 2011:56). Moreover,

Trienekens (2011) made a distinction between regulative, normative and cognitive

institutions, according to the terminology used by Scott (1995). These sets of

institutions (e.g. Government legislations, rules and policies, business practices as well

10

as the cognitive institutions) can prevent the value chain upgrading by setting trade

barriers, limiting the information flow, imposing taxes as well as limiting value adding

practices (Trienekens, 2011:56).

Correspondingly, Mitchell and Coles (2011) also defined the changes in the value

chain which is the inclusion of new participants in the chain, continued participation under

new terms, expulsion of members and non-participation. And this is adhered to the

upgrading strategies for small producers that grouped into three types: improve process,

product or volume; change and/or add functions; improve value chain coordination

(Mitchell and Coles, 2011:29 ff). However, doing a significant change and upgrading

strategies is particularly challenging for smallholder farmer who wants to step into the

global value chain. Therefore, the following literature will develop the theory of collective

action and farmer cooperatives to correlate the farmer’s inclusion in the coffee value chain.

2.1.2 Governance of Value Chain

According to Humphrey and Schmitz (2004), governance in term of value chain can be

determined as the process of specifying, communicating and enforcing compliance with

key product and process parameters along the value chain (Neilson, 2008:1609). The

governance analysis provides a better understanding of how a chain is controlled and

coordinated when asymmetry of power emerges (Gereffi and Fernandez-Stark, 2011:8).

Moreover, Fromm (2007) explained the role of ‘governance’ can be undertaken by buyers

(buyer-driver chains) or producers (producer-driven chains). In a producer-driven chain,

the main transnational manufacturers play the central role in coordinating production

networks. While in buyer-driven chain, production networks is decentralized in a number

of exporting countries, typically in developing nations (Fromm, 2007:7).

Furthermore, according to Gereffi et al. (2005) there are five governance types which

have several key determinants. Several variables as follows affect the shape of global value

chain structure:

The complexity of information and knowledge transfer required to sustain a particular

transaction in respect to product and process specifications

Codification of the information and knowledge, whether it is easy to codified,

efficiently transmitted and without transaction-specific investment between the parties

The capabilities of the actual and potential suppliers in relation to the requirements of

the transaction (Gereffi et al., 2005:85)

11

Table 2. Key Determinants of Global Value Chain Governance

GovernanceType

InformationComplexity

Ability toCodify

Information

SupplierCapabilities

Degree of ExplicitCoordination andPower Asymmetry

Market Low High High Low

High

Modular High High HighRelational High Low HighCaptive High High Low

Hierarchy High Low LowSource: Gereffi et al. (2005:87)

The five different types of governance structures have different characteristics, which are

explained in the following sections.

Market

The specific characteristic of the market governance relies on the simplicity of the

information. Information on product specifications amongst the actors is easily

transmitted, and exchanges within the chain require little or no formal cooperation. The

cost of switching to new partners is low for both producers and buyers. Instead of

powerful lead firm, the price determines the central governance mechanism (Gereffi and

Fernandez-Stark, 2011:9).

Modular

In this chain, complex transactions are relatively easy to codify. Suppliers aim to

conclude consumers’ satisfaction which result in extensive consumer base investment.

Relationship between actors later becomes significant because of the high information

flow across the inter-link firm. In order to maintain the function of modular governance,

information technology and standards for exchanging information are required (Gereffi

and Fernandez-Stark, 2011:9).

Relational

The frequent interactions and knowledge sharing between players in the chain has a

high influence in the relational value chain. The linkage between actors requires trust

and generates mutual reliance, which is regulated through reputation, social and spatial

proximity, family and ethnic affiliations. Under those conditions, it takes time to make

the linkage which lead to high cost and difficulties to switch to a new collaborator in the

chain (Gereffi and Fernandez-Stark, 2011:9).

12

Captive

In these chains, respective supplier posses low competence to produce complex

products and specifications. For this reason, it requires intervention and restraint from

the lead firm. The lead firm encourages the build-up of transactional dependence in

order to prevent others in benefiting the efforts of the lead firm. So the suppliers face

significant switching costs and are ‘captive’. The opportunism arises through the control

of lead firms, while at the same time the linkages could provide resources and market

access to the subordinate firms to progress to exit an unattractive option (Gereffi et al.,

2005:87).

Hierarchy

Hierarchy governance occurs when product specifications cannot be codified, products

are complex, or highly competent suppliers are rare to be found. Consequently, vertical

integration and managerial control within lead firms that produce and manufacture

products in-house are required. (Gereffi and Fernandez-Stark, 2011:10).

2.1.2.1 Governance and Coordination of Value Chain

In the context of governance mechanism, coordination between actors in the chain is

substantial. Different activities and different transactions in the value chain imply the

mutual dependencies or (independencies). Malone and Crowston (1994) defined co-

ordination as managing dependencies between activities. Meanwhile, Thompson (1967)

noted three different types of interdependencies-pooled, sequential, and reciprocal

interdependency (Bijman et al., 2011:84).

In a system of pooled interdependency, each part of an organization renders a discrete

contribution to the whole and each is supported by the whole. The whole system is

threatened if the actors perform inadequately. The main coordination mechanisms in

collaborations of a pooled interdependency type are the development and implementation

of standards for production, distribution and product quality (Bijman et al., 2011:84).

Sequential interdependency is relatively relevant in the context of value chains. In this

arrangement, the output of one function is the input to another part. The typical main

coordination mechanism is managerial discretion, i.e. coordination by plan or command.

Thus, it requires lead firm or coordinating agent who plans the flow of the products and

information and directs adaptation to changing internal and external conditions (Bijman et

al., 2011:84 ff).

13

The third form is reciprocal interdependency where the output of each part is an input

for every other part, so each part posses contingency for the other parts. The coordination

mechanism is the mutual adjustment amongst part of the chain, thus implies joint decision

making and problem solving to coordinate individual activities. In this mechanism,

information exchange and feedback from past transactions and partners’ past conduct is

crucial in order to foster learning and reinforce social norms and informal sanctioning

mechanisms (Bijman et al., 2011:85).

Muradian and Pelupessy (2005) described a term “inter-segment coordination” in the

context of coordination between suppliers in developing countries and buyers in

industrialized countries into several types as follows:

Market transactions: typical characteristics are low or missing coordination between

actors, low information exchange, prices and standard attributes are the main control

mechanism

Weak coordination: it represents complex but not-so-specific (easy to codify)

information exchange. The monitoring cost is relatively low (for buyers) as well as the

cost of switching partners (both for suppliers and buyers)

Strong coordination: typically complex and specific information exchange between

parties. The cost for monitoring and switching partners is considerably high. Mutual

dependence between parties is likely to happen.

Vertical integration: it requires complex and very specific information. Standards,

processes, and logistics are controlled through ownership (Muradian and Pelupessy,

2005:2031).

2.1.3 Upgrading the Value Chain

According to Gereffi et al. (2011), the ‘governance’ of the value chains is the key concept

for the top down view. Governance focuses mainly on lead firms and the organization of

the international industries. Meanwhile, ‘upgrading’ is the main concept for the bottom up

perspective which focuses on the strategies used by countries, regions and other economic

stakeholders to maintain or improve their positions in the global economy (Gereffi et al.,

2011:12).

Stamm (2004) has defined upgrading as “the process that enables firms to hold on

more value-intensive functions in the chain, make it harder to replace, and thus

appropriate a larger part of the generated profits” (Stamm, 2004:27). Furthermore, there

are various elements associated with the possibilities for upgrading. The main components

14

are the basic character of the marketplace, the substitutability of the partners, the level of

competency of corporate management, the desegregation of the firm in clusters that

promote collective learning process, and the efficiency of the institutional corporate

management, which enables the firm to tap assets that it cannot itself produces (Stamm,

2004:27).

Additionally, Kaplinsky (2000) characterized four forms of upgrading as process

improvement, product improvement, changing functional positions (adjusting activities or

shifting to new activities) and moving out of the value chain into a new value chain

(Kaplinsky et al., 2000:76).

2.1.4 Smallholders and Farmer Cooperatives

Coffee farming is crucial as the source of income for smallholders farmer in most of

developing countries. Although, the number of private plantation is quite small, they might

have the possibility to break the barrier and an access broader market channel. However,

small-scale farmers might have several constraints that prevent them from reaching the

market. The demand for high quality products and consistent volumes is one of the

possible constraints that they might face. According to Trienekens (2011), several studies

have been drawn the important barrier encountered by developing country producers

regarding institutional and infrastructural support. As described De Janvry and Sadoulet

(2005), Daviron and Gibbon (2002), Reardon and Barret (2000), smallholders also faced a

various disadvantage such as little capital to invest, use traditional techniques, depend on

family labor and limitations to access international key market players (Trienekens,

2011:52).

There are some common constraints that prevent the smallholder farmer to reach the

market and to participate in the broader value chain. Gaiha and Thapa (2007) specified that

collection costs are high if the small producers are scattered and infrastructure is weak.

This case is particularly emerging in developing countries. In addition, the weakness of

small-holders is the illiteracy and limited business skills in negotiating with suppliers. In

particular contexts, weak public extension services and input markets, along with limited

access to credit, force small-holders to use outdated techniques (Gaiha and Thapa,

2007:13).

In addition, the small-holder farmers also have two major disadvantages in terms of

their interactions with upstream and downstream agents. First, regarding to economies of

scale which cannot be reached by small farm sizes leads to higher transaction costs.

15

Therefore, they have higher unit costs of procuring inputs, obtaining credit and other

financial services, getting agronomic and market information, implementing standards and

certification and marketing (Wiggins et al., 2010:1343). Second, higher degrees of

concentration in upstream and downstream markets can lead to asymmetries in market

power. The result is small family farms more vulnerable to opportunistic behavior (Fischer

and Qaim, 2012:1256).

It is disclosed by Rao and Qaim (2011) that for farmers in general the participation in

the bigger level of market channels might be associated with market assurance as well as

stability in supply volume and prices of the products. This has potentially entailed rising

incomes. But, the constraints and market imperfection might generate small-holder

exclusion and this will lead to increasing disparities and marginalization (Rao and Qaim,

2011:784). As described by Vorley et al. (2007) lower transaction cost is one of the

examples generated by the establishment of farmer organization. By taking role as

intermediaries, farmers organizations are able to connect the farmers and supermarkets by

providing economies of scale and specialized skills in assembling, grading, and

transferring information between buyers and sellers (Moustier et al., 2010:69).

Nevertheless, it does not inevitably signify that the farmers can get across the high-value

market. For example, Fischer and Qaim (2012) indicated that in the settlement of banana

producers association in Kenya gives benefit more into the product and very context

specific, so it does not solely improve market access for smallholder farmers (Fischer and

Qaim, 2012:1267). Furthermore, Gulati et al. (2007) also conveyed that small-holder

farmers often lack in market information, struggle to meet buyers’ food safety and quality

control requirement, and are seldom able to provide standardized products on a continuous

basis. Thus, in order to help the small-holder farmers to benefit from the new market a

relevant strategy is necessary (Hellin et al., 2007:3).

Although several difficulties may hinder smallholder from accessing the market,

Lipton (2006), Boselie, Henson and Weatherspoon (2003) and Swinnen (2006) have

argued that smallholders enjoy several advantages compared to large commercial farmers

in term of intermediation and internalization. Intermediation takes place if the public and

private agencies cooperate (e.g. National governments define the food safety standards,

and the private agencies might help the smallholders to implement the standards, public

sector through private financing might strengthen the rural infrastructure, and suppliers

might help finance the provision of input and provide extension service). On the other

hand, internalization involves producers organization, especially smallholders that

16

negotiate production and marketing arrangements with the suppliers (Gaiha and Thapa,

2007:13).

Several researches show the example of how small - holder farmers can access the

retail market and one of those is through collective action. Hellin et al. (2007) used the

term of collective action as voluntary action taken by a group to achieve common interests.

Collective action can exist even in the absence of farmer organization, which is commonly

seen as the formal expression of collective action (Hellin et al., 2007:5).

Stockbridge et al. (2003) defined different levels that farmer organizations may

operate. The opportunities and challenges faced at different levels or organization vary. In

general, larger organization of small-holder farmers offer the potential for economies of

scale. However, the benefits need to be balanced against the cost and difficulties that

occurred with organizing large numbers of people (Stockbridge et al., 2003:2).

Table 3. Service Provided by Farmer Organizations

Marketing services (input supply, output marketing and processing, market information)

Facilitation of collective production activities

Financial services (savings, loans and other forms of credit)

Technology services (education, extension, research)

Education services (business skills, health, general)

Welfare services (health, safety nets)

Policy advocacy

Managing common property resources (water, pasture, fisheries, forests

(Stockbridge et al., 2003:2).

In most growing nations in Asia who have exceptional characteristics in collectivization,

the majority of the farmers’ organization indicates their significant role in several sectors.

Thapa and Gaiha (2011) also argued that farmer/producer organizations have the

possibility to overcome challenges related to high transaction costs. These organizations

could be cooperatives, associations, and societies. The organization supports small-holder

farmers in gaining access to markets and public services, and for advocacy (Thapa and

Gaiha, 2011:20). In addition, Howells (2006) also mentioned the term of innovation

intermediary. It is defined as “an organization or body that acts as an agent or broker in

any aspects of the innovation process between two or more parties. The activities cover:

helping to provide information about potential collaborator; brokering a transaction

17

between actors; acting as a mediator, or go-between, for bodies or organizations that are

already collaborating; and helping find advice, funding and support for the innovation

outcomes of such collaborations” (Yang et al., 2014:115).

Roy and Thorat (2008) disclosed that producer cooperatives can exploit economies

of scale by the collectivization of output of the farmers. Still, economies of scale in

production are different from economies of scale in marketing that are rife in high value

export market. The conflict lies in the requirements for marketing in terms of information

procurement and dissemination, the role of reputation and branding and the importance of

negotiations (Roy and Thorat, 2008:1876). Although Fischer and Qaim (2012) argued that

cooperative organizations do not necessarily mean that the farmers can get better access to

market, but the farmers’ organization can be the important catalyst for innovation adoption

and upgrading of production systems through promoting efficient information flows

(Fischer and Qaim, 2012:1267).

Generally speaking, the value chain development can be the opportunity for farmers

to get into new markets and improve their quality as well as quantity of their products. The

study carried out by Zheng et al. (2011) found that cooperative could help the farmers in

terms of sales of agricultural products, provide market information, offer technical services

during production, financial assistance, government subsidies and provision of affordable

production material (Zheng et al., 2011:452). To put it another way, collective action, such

as a farmers organization or contract farming can be the key channel to accomplish certain

goal especially to tackle challenges and difficulties faced by farmers. Shifting from

traditional cooperatives to new generation cooperatives may also extend their functions

and provide more services to the farmers. Nevertheless, it needs support from other actors

to better link farmers to market in a sustainable way in order to increase the benefits of the

farmer.

On the contrary, a farmers’ organization is facing several problems as well. Sartorius

and Kirsten (2007) specified that farmer distrust is a common example of the problems in

farmer organization. Combination of farmer distrust and perceived loss of autonomy and

feelings of exploitation would be the hindering factor of the institutional arrangement in

most developing countries (Sartorius and Kirsten, 2007:651). Fahlbeck (2007) also

summarized the potential problem in farmer cooperatives: (1) the per-member capital

invested in the cooperation is large; (2) the cooperative has a close membership; (3) few of

the member firms are legally incorporated; (4) the intergenerational transfer of

membership within families is prohibited; and (5) the cooperative is large and has a diverse

18

membership (Fahlbeck, 2007:257). In addition, Mujawamariya (2013) has been listed

internal and external problems from several studies. Free riding, noncompliance,

underinvestment, poor management, membership desertion and heterogeneity among

members will affect cooperatives’ efficiency and effectiveness (Mujamariya et al.,

2013:73).

For this reason, several assistances are needed to strengthen the role or the power of

farmer organization in the higher market either for upstream or downstream level. Thus, it

is sometimes important to include the outsiders to the farmer cooperatives. The facilitator

plays a crucial role by catalyzing the collective action, provide information and technical

assistance, and builds the capacity of a group to be effectively engaged in marketing

activities (Markelova et al., 2009:5). The government role is also important to flourish the

cooperatives, as stated by Birchall (2003, 2004), government support in form of small

grants, policy frameworks and regulation have the ability to empower cooperatives

member and support cooperatives enterprises (Borda-Rodriguez and Vicari, 2014:45).

Additionally, Borda-Rodriguez and Vicari (2014) studied the factors of the resiliency

of the cooperatives; (1) membership that further explained by the characteristics of the

membership in the cooperatives (homogenous/heterogeneous, benefits and members’

loyalty, women’s inclusion; (2) collective skills: cooperatives as a collective space of

learning; (3) networks as access to knowledge and resources; (4) innovation that will

reduce donor dependency, increase members’ loyalty, improve the expertise, upgrade the

production process, as well as enable them to participate in national and international

markets; (5) role of government (Borda-Rodriguez and Vicari, 2014:47 ff).

2.2 Empirical Evidences

A global coffee crisis situation since the early 1990s has been noted by Linton (2005). The

coffee crisis resulting a rising number in poverty case, especially for farmers. The majority

of the coffee farmers is suffering while Northern consumers continue to pay premium

prices for the coffee they consume. In response to ensure that coffee production is

sustainable in term of farmers’ socio-economic condition as well as the environment, new

standards do emerge via self-regulation (Linton, 2005:600 ff).

In terms of regulation systems, Muradian and Pelupessy (2005) showed the effect of

voluntary regulation systems towards the position of the farmers in the coffee chain. The

application of the voluntary regulation systems in the chain generates two potential

benefits: (i) it increases the ability to reap economic rent (upgrading) and (ii) it improves

19

the chances of gaining access to, or remaining in, a particular market (Muradian and

Pelupessy, 2005:2036).

Saarelainen and Sievers (2011) expanded the purpose of collective action

organization depending on the activities it carries on. The potential action is through

vertical coordination (buyer-seller relationship) and horizontal coordination (inter-firm

coordination, linkages to service providers and to policy makers). However, it frequently

occurs that there is a combination of horizontal and vertical coordination in the chain. The

organizations are taking on more proactive roles, higher-up or further-down the chain and

engaging in value chain integration (Saarelainen and Sievers, 2011:4).

Furthermore, Saarelainen and Sievers (2011) have drawn the example of engagement

between farmer cooperatives, international organization, and local government in soybean

production and value chain addition in Kenya. The cooperative is able to improve the value

chain by providing training, high-quality input (seeds, fertilizer) as well as soft loans for

participating farmers. In addition, the cooperative encourages the farmer to adopt the value

added processing in three different levels; household level, cottage level, and industry

level. The cooperative also facilitated the market linkages and identified a potential market

both for domestic and export market (Saarelainen and Sievers, 2011:5).

Fromm (2007) disclosed the case of upgrading the value chain done by smallholder

producers in Honduras. In the context of the product upgrading, the driving factors for the

small producers to change and improve the product are competitiveness among producers,

consumer demand, new market opportunities, and “tools” to survive in the business. While

in the process upgrading, small producers implemented changes through field practices and

post-harvest management. Functional upgrading defined as the value addition practice by

changing the mix of activities carried out within the firm or moving the locus of activities

to different links in the value chain. And the research indicated that competitiveness is the

primary concern for most firms to implement improvements toward functional upgrading

(Fromm, 2007:18 ff).

Wollni and Zeller (2007) showed empirical evidence in coffee marketing in Costa

Rica. Membership in cooperatives has an adequate effect to the inclusion of the coffee

farmer in specialized markets. In addition, smallholder farmers are more likely to market

their coffee through cooperative channels as opposed to private channels (Wollni and

Zeller, 2007:10 ff).

In the context of membership in cooperative, Borda-Rodriguez and Vicari (2014)

further elaborated the membership as the factor of cooperative’s resilience based on the

20

type of diversity (heterogeneous or homogeneous), benefits and members’ loyalty, and

women’s inclusion. Although the problem generated by the diversity of the member is rare,

‘diverse’ membership can be a cause of concern because it has the potency to weaken

cooperative governance. Members may have different interests and expectations and

therefore governance can be a subject of conflict process. In the context of members’

loyalty, it depends on the level of members’ satisfaction towards services and benefits

gained by the members. In addition, low levels of literacy and lack of understanding of the

mechanism of cooperative work also affect the members’ loyalty (Borda-Rodriguez and

Vicari, 2014:47 ff).

Training and extension programs also mentioned as the factor that affect the

participation of smallholder farmers in the specialty market. According to Wollni and

Zeller (2007), the probability of farmer’s participation will increase if farmers received

training and extension program in quality enhancing practiced. Nevertheless, education and

experience have a significant and positive effect on farmer’s participation (Wollni and

Zeller, 2007:10).

Meanwhile, Barham and Chitemi (2009) have investigated the collective action

initiatives to improve marketing performance. In the context of infrastructure, the

commodities and the source of input are the driving forces to improve the marketing

performance. And variables in the social structure (group maturity, number of group

activities, a higher proportion of male leaders, and better educated groups) can play an

enabling role in a group’s ability to take advantage of market opportunities (Barham and

Chitemi, 2009:59).

2.3 Remarks from Literature Review

Based on the research studies, the value chain approach creates a comprehensive figure of

the various activities involved in the coffee sector, the role of each actor along the chain

and the coordination mechanism between actors. Saarelainen and Sievers (2011) have

made a clear picture of the role of cooperative to improve the value chain by providing

various input factors as well as market linkages for domestic and international market

(Saarelainen and Sievers, 2011:5). Therefore, the study makes an attempt to use the value

chain analysis, the concept of governance as well as the theory of cooperative to see the

engagement of cooperative in the coffee value chain in the study area.

21

CHAPTER 3. METHODOLOGY

This chapter covers the outline of the research methodology used in the study. The first

part aims at elaborating the conceptual framework used to see the coffee value chain in

Manggarai and the coordination amongst actors. And the following part accounts the

general characteristics of the study area, sampling procedures and description of the

analysis.

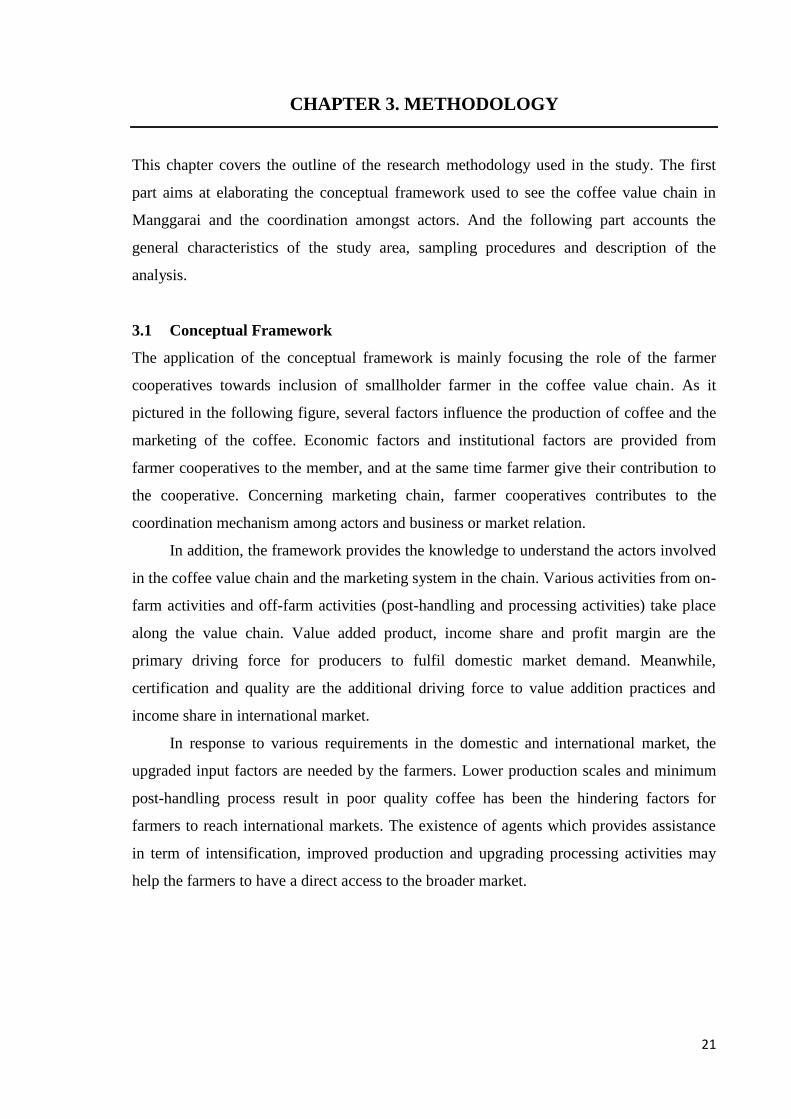

3.1 Conceptual Framework

The application of the conceptual framework is mainly focusing the role of the farmer

cooperatives towards inclusion of smallholder farmer in the coffee value chain. As it

pictured in the following figure, several factors influence the production of coffee and the

marketing of the coffee. Economic factors and institutional factors are provided from

farmer cooperatives to the member, and at the same time farmer give their contribution to

the cooperative. Concerning marketing chain, farmer cooperatives contributes to the

coordination mechanism among actors and business or market relation.

In addition, the framework provides the knowledge to understand the actors involved

in the coffee value chain and the marketing system in the chain. Various activities from on-

farm activities and off-farm activities (post-handling and processing activities) take place

along the value chain. Value added product, income share and profit margin are the

primary driving force for producers to fulfil domestic market demand. Meanwhile,

certification and quality are the additional driving force to value addition practices and

income share in international market.

In response to various requirements in the domestic and international market, the

upgraded input factors are needed by the farmers. Lower production scales and minimum

post-handling process result in poor quality coffee has been the hindering factors for

farmers to reach international markets. The existence of agents which provides assistance

in term of intensification, improved production and upgrading processing activities may

help the farmers to have a direct access to the broader market.

22

Figure 3. Conceptual Framework in the Coffee Value Chain

3.2 Research Methods

The study is carried out in Manggarai, part of East Nusa Tenggara Province in Indonesia.

Manggarai is one of the major producers of coffee in the province. The location is suitable

for coffee cultivation where the topography of the area is approximately 1000 meters

above sea level. Manggarai regency is located in between West Manggarai and East

Manggarai regency which are also the coffee producing regions in East Nusa Tenggara.

According to National Statistics Agency (2013), in September 2013 the percentage

of poor people in East Nusa Tenggara accounted for 20.24% and it slightly decreased

0.17% from September 2012. Though the overall rate seems declining, but in absolute

terms increased by 8.86 thousand people within the same period.

In the whole region of Manggarai, the number of the farmers' group in 2014 is 1272

groups and the member reach the number of 34,015 people. Government especially from

the Department of Estate Crops and Horticulture divides the class of the farmers group

according to their level of knowledge and establishment year of the farmers' group. From

1272 groups, the beginner level consists of 470 groups, advanced consist of 722 groups,

while there are also additional groups called madya and utama that each consist of 76

groups and 5 groups. However, from the total number of 1272 farmer groups in the region,

a group which focuses and working in coffee cultivation are only 81 groups.

Institutional Factors• Training• Technical

assistance

• Value additionproduct

• Income share• Profit margin

COFFEEFARMERS

FarmerCooperatives

DOMESTICMARKET

INTERNATIONALMARKET

• Value additionproduct

• Certificationproduct

Economic Factors• Subsidies• Credit• Investments

Member Value Proposition

Member Contribution

Governance ofthe value chain

23

Map showing the Two Major Coffee-growing Regions in Flores

Source: Marsh et al. (2007:9)

Figure 4. Map of the Study Region in Manggarai, East Nusa Tenggara, Indonesia

Source: National Statistics Agency (BPS) Manggarai Regency, 2014

24

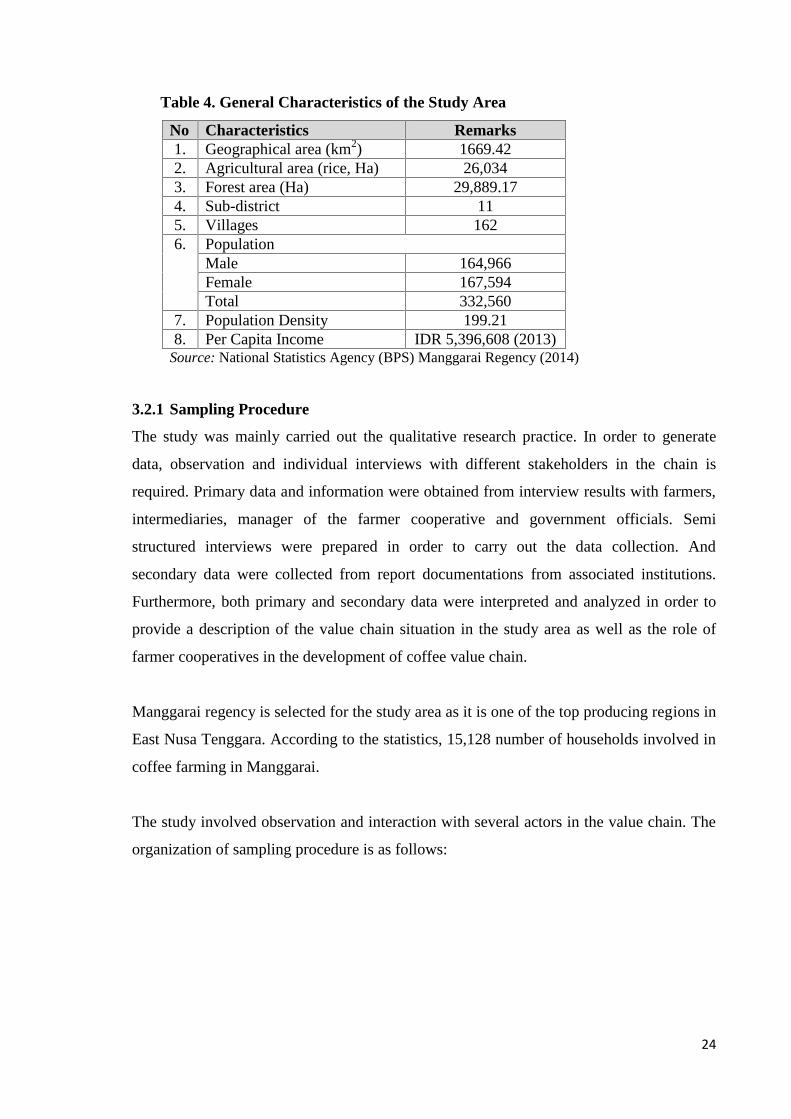

Table 4. General Characteristics of the Study Area

No Characteristics Remarks1. Geographical area (km2) 1669.422. Agricultural area (rice, Ha) 26,0343. Forest area (Ha) 29,889.174. Sub-district 115. Villages 1626. Population

Male 164,966Female 167,594Total 332,560

7. Population Density 199.218. Per Capita Income IDR 5,396,608 (2013)

Source: National Statistics Agency (BPS) Manggarai Regency (2014)

3.2.1 Sampling Procedure

The study was mainly carried out the qualitative research practice. In order to generate

data, observation and individual interviews with different stakeholders in the chain is

required. Primary data and information were obtained from interview results with farmers,

intermediaries, manager of the farmer cooperative and government officials. Semi

structured interviews were prepared in order to carry out the data collection. And

secondary data were collected from report documentations from associated institutions.

Furthermore, both primary and secondary data were interpreted and analyzed in order to

provide a description of the value chain situation in the study area as well as the role of

farmer cooperatives in the development of coffee value chain.

Manggarai regency is selected for the study area as it is one of the top producing regions in

East Nusa Tenggara. According to the statistics, 15,128 number of households involved in

coffee farming in Manggarai.

The study involved observation and interaction with several actors in the value chain. The

organization of sampling procedure is as follows:

25

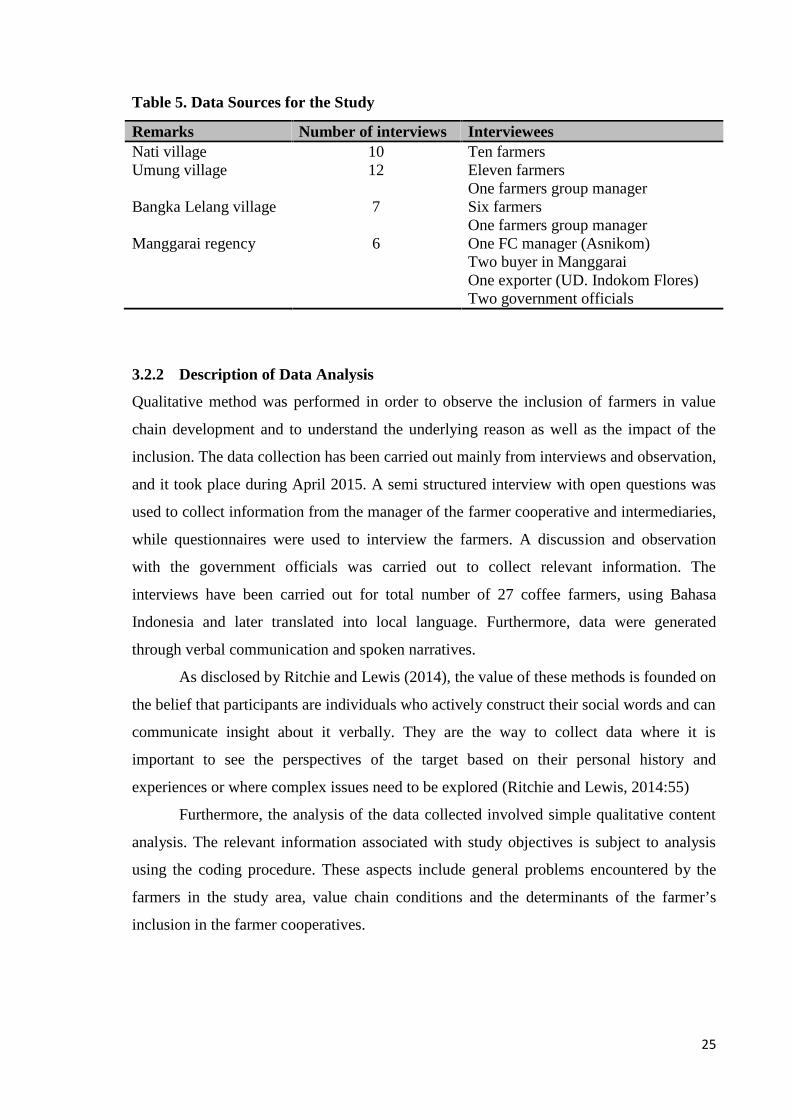

Table 5. Data Sources for the Study

Remarks Number of interviews IntervieweesNati village 10 Ten farmersUmung village 12 Eleven farmers

One farmers group managerBangka Lelang village 7 Six farmers

One farmers group managerManggarai regency 6 One FC manager (Asnikom)

Two buyer in ManggaraiOne exporter (UD. Indokom Flores)Two government officials

3.2.2 Description of Data Analysis

Qualitative method was performed in order to observe the inclusion of farmers in value

chain development and to understand the underlying reason as well as the impact of the

inclusion. The data collection has been carried out mainly from interviews and observation,

and it took place during April 2015. A semi structured interview with open questions was

used to collect information from the manager of the farmer cooperative and intermediaries,

while questionnaires were used to interview the farmers. A discussion and observation

with the government officials was carried out to collect relevant information. The

interviews have been carried out for total number of 27 coffee farmers, using Bahasa

Indonesia and later translated into local language. Furthermore, data were generated

through verbal communication and spoken narratives.

As disclosed by Ritchie and Lewis (2014), the value of these methods is founded on

the belief that participants are individuals who actively construct their social words and can

communicate insight about it verbally. They are the way to collect data where it is

important to see the perspectives of the target based on their personal history and

experiences or where complex issues need to be explored (Ritchie and Lewis, 2014:55)

Furthermore, the analysis of the data collected involved simple qualitative content

analysis. The relevant information associated with study objectives is subject to analysis

using the coding procedure. These aspects include general problems encountered by the

farmers in the study area, value chain conditions and the determinants of the farmer’s

inclusion in the farmer cooperatives.

26

3.3 Limitations of The Study

The research undertaken to perform the study encompasses some limitations. Time was the

primary constraint in order to collect a large sample of data. As this is also individual

project, therefore the sample size was limited to 27 farmers and few key informants. The

research method mainly used qualitative tools. Another factor hindering the in-depth

analysis of the study was the location of the farmers which were isolated and scattered. The

information taken from the farmers and also from the key informants consist of some

approximations, especially for the size, production and income issues, which lead to bias.

Given that the study was only carried out in 3 farmers group in the whole regency, it may

not represent the factual case of the regency.

Seasonal bias: conducting field work during off season takes away the advantages to

observe the harvesting activity, collecting and selling process of coffee as well as to

observe the market and the price mechanism in the coffee sector in the study area.

Hierarchical bias: as most of the interviews was arranged by the government officials

(Department of Estate Crops and Horticulture), thus the selected location for the study

were predominantly chosen by the officials. Although the selection was based on the

appropriateness to the objectives, nevertheless it might lead to bias.

Interpretative bias: due to the fact that most farmers only speak the local language,

therefore translations were done by the government official. However, although there

was an attempt to confirm the answer by asking in different ways, there can be bias

related to translations and interpretations from local language to Bahasa Indonesia.

27

CHAPTER 4. RESULTS

This chapter will cover the analysis of the coffee value chain in the Manggarai Regency in

East Nusa Tenggara on the basis of: (1) Size and structure of smallholders coffee farms;

(2) Mapping the stages and actors in the coffee value chain; (3) Price spread and value

addition of coffee; (4) Governance and coordination in coffee value chain; (5) SWOT

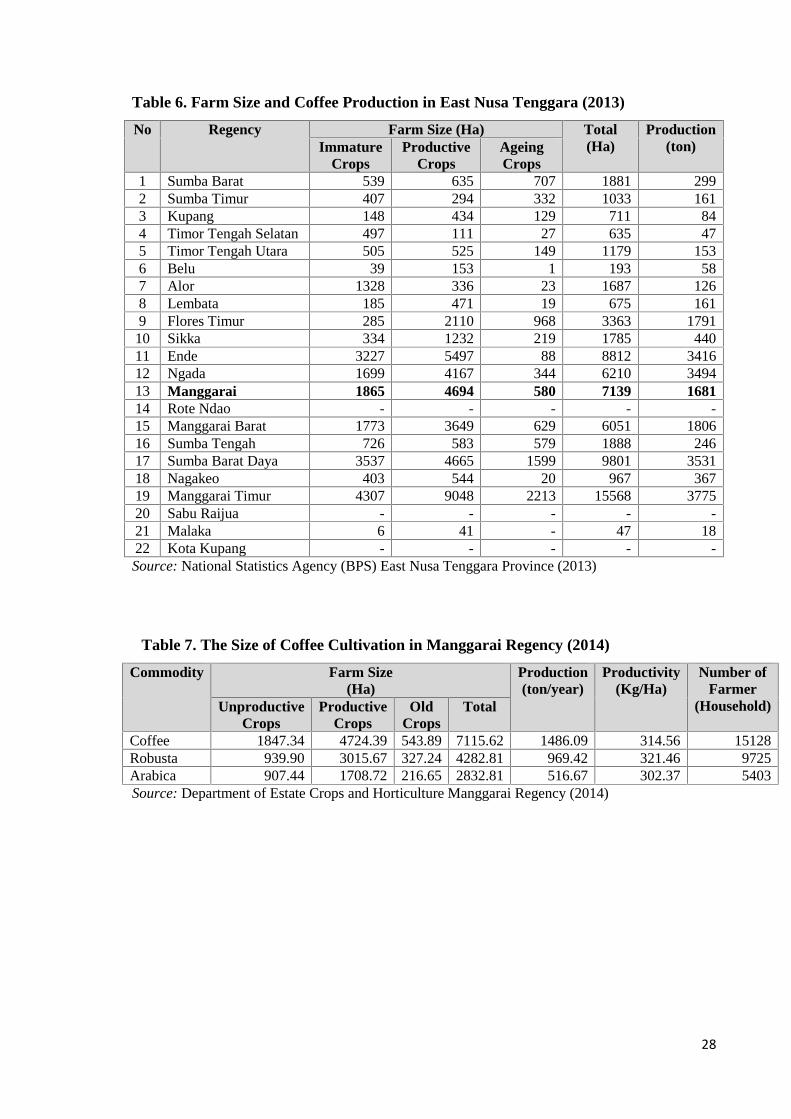

analysis of the coffee value chain.

4.1 Size and Structure of Smallholders Coffee Farms

East Nusa Tenggara is one of the top coffee producing regions in Indonesia with high

involvement of smallholder farmers. However, the amount can be determined as the lowest

among other coffee producing provinces. In East Nusa Tenggara, the top 3 coffee

producing regencies are notably Ngada, Manggarai and East Manggarai. In most of the

area in East Nusa Tenggara especially in Manggarai regency, coffee is grown at both low

altitudes and high altitude. Robusta is mainly grown at low altitudes and Arabica are

grown at high altitude and mountainous area.

According to the farmer, coffee crops have been grown in the region since 2

generations. Before the 1980s, the farmers were mainly planting Robusta. Afterward,

during the development project, including an agriculture extension on the 1990s, Arabica

was started to be cultivated in the area. And now the majority of smallholder farmers

grows 2 varieties, Arabica and Robusta. In 2013, Manggarai regency produced 1681

tonnes of coffee in total.

The characteristic of the coffee farms is polyculture. Coffee crops are usually planted

along with other crops such as cloves, yam and cassava. Coffee crops also needed cover

trees for its growth, thus there are also cover trees such as dadap (erythrina spp1) and

sengon (paraserianthes sp2) on the coffee farms. In the area, smallholders usually planted

the crops with the average space 2.5 x 2.5 meters.

As coffee is a perennial crop, harvesting period is usually in April until October. The

peak harvesting period for Arabica is during April-June, while for Robusta is June-

October. Harvesting method starts with picking the red cherry fruits, then followed by

sortation and pelling (husked skin) using traditional wooden pulping tool or mechanical

equipment.

1 Scientific name referred to Iqbal (2011)2 Scientific name referred to Iqbal (2011)

28

Table 6. Farm Size and Coffee Production in East Nusa Tenggara (2013)

No Regency Farm Size (Ha) Total(Ha)

Production(ton)Immature

CropsProductive

CropsAgeingCrops

1 Sumba Barat 539 635 707 1881 2992 Sumba Timur 407 294 332 1033 1613 Kupang 148 434 129 711 844 Timor Tengah Selatan 497 111 27 635 475 Timor Tengah Utara 505 525 149 1179 1536 Belu 39 153 1 193 587 Alor 1328 336 23 1687 1268 Lembata 185 471 19 675 1619 Flores Timur 285 2110 968 3363 179110 Sikka 334 1232 219 1785 44011 Ende 3227 5497 88 8812 341612 Ngada 1699 4167 344 6210 349413 Manggarai 1865 4694 580 7139 168114 Rote Ndao - - - - -15 Manggarai Barat 1773 3649 629 6051 180616 Sumba Tengah 726 583 579 1888 24617 Sumba Barat Daya 3537 4665 1599 9801 353118 Nagakeo 403 544 20 967 36719 Manggarai Timur 4307 9048 2213 15568 377520 Sabu Raijua - - - - -21 Malaka 6 41 - 47 1822 Kota Kupang - - - - -Source: National Statistics Agency (BPS) East Nusa Tenggara Province (2013)

Table 7. The Size of Coffee Cultivation in Manggarai Regency (2014)

Commodity Farm Size(Ha)

Production(ton/year)

Productivity(Kg/Ha)

Number ofFarmer

(Household)UnproductiveCrops

ProductiveCrops

OldCrops

Total

Coffee 1847.34 4724.39 543.89 7115.62 1486.09 314.56 15128Robusta 939.90 3015.67 327.24 4282.81 969.42 321.46 9725Arabica 907.44 1708.72 216.65 2832.81 516.67 302.37 5403Source: Department of Estate Crops and Horticulture Manggarai Regency (2014)

29

4.2 Mapping of the Coffee Value Chain

Neilson (2008) described that it is common for coffee to change hands three or four times

along traditional trade networks before reaching exporter agents or processing mills. Since

the nationalization of Dutch-held estates in 1957 (described by Neilson, 2008), coffee

sector in Indonesia is liberalized and market situation thus becomes independent despite

the limited intervention from the government regarding export quota (Neilson, 2008:1613).

The following map of the coffee value chain reflects the sequence of stages involved in

distribution of coffee from smallholders to consumers in domestic and international

markets.

Figure 5. Mapping of Coffee Value Chain in Manggarai

Source: own compilation and adapted from Neilson (2014)

Dry Parchment

Farmer

AsnikomCollector

Farmer Farmer

Dry Parchment

Sorted Parchment

ExporterPT. Indokom Citra

Persada UD. Nugi Indah UD. AnekaUD. Monas

USA, Germany, Australia,Middle East

Inter Island Trade

Sorted & Roasted CoffeeGraded Coffee

Domestic Consumers

Local Trader & Distributor

c.a 20% of production is consumed bydomestic consumers (mostly Robusta)

c.a 75% of production is exported as greenbeans, and 5% is exported as processedcoffee

Processed Coffee

30

4.2.1. Coffee Farmers

Like most of the cases in the coffee sector in Indonesia, the majority of the farmers in

Manggarai regency is smallholder farmers. In the whole region, there are 15,128

households depend their livelihood on coffee sector. Although topography of the region is

more suitable for Arabica, most of the farmers have grown Arabica and Robusta. The

average cropping area is ranging from a quarter hectares to 4 hectares. All farmers in the

study area do not rent any area for cultivation purpose nor lease their land to the outsider.

The farmers completely rely on their land for agricultural production and for their main

household income.

The social and economic characteristics of the farmers

About 52% of the farmers interviewed are in the 45-60 age cohort. The second largest

group includes farmers aged 30-45 (37%). Thus, it can be considered that farmers in the

study area are relatively still in the productive age range. This is important since they also

play a role as the main labor force in the coffee sector. Most farmers have been engaged in