STUDY REPORT - daln.gov.vn · PDF file3.3.1 The role of agricultural cooperatives and farmer...

70

Mekong Delta Agricultural Cooperatives’ and Farmer Groups’ Capacity Assessment – The Cases Of Ca Mau, Bac Lieu, Soc Trang and An Giang Province STUDY REPORT Implemented by

Transcript of STUDY REPORT - daln.gov.vn · PDF file3.3.1 The role of agricultural cooperatives and farmer...

Mekong Delta Agricultural Cooperatives’ and Farmer Groups’ Capacity Assessment – The Cases Of Ca Mau, Bac Lieu,Soc Trang and An Giang Province

STUDY REPORT

Implemented by

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

32

Table Of Contents1. Introduction1.1 Study context

1.2 Study objectives

1.3 Study method

1.3.1 Method of information collection

1.3.2 Survey sample

2. Policy Overview2.1 Overview of policies encouraging production-trade linkage associated with the

LSRF concept

2.1.1 The approach of preferential and supportive policies

2.1.2 Preference and support for enterprises in cooperation and production-trade-linkage associated with LSRF establishment

2.1.3 Preferential policies for organisations representing farmers in the linkage

2.1.4 Preferential support for farmers participating in linkage and LSRF production

2.2 Overview of policies encouraging agricultural cooperative development

2.2.1 Policies for preferential access to credit

2.2.2 Policies for preferential land allocation and leases

2.2.3 Policies for preferential tax treatment

2.2.4 Policies encouraging new establishment and agricultural cooperative re-registration

2.2.5 Policies supporting retraining and training

2.2.6 Policies supporting trade promotion and market expansion

2.2.7 Policies supporting the application of science and technology, new technology

2.2.8 Policies supporting infrastructure investment and participating in target programme and socio–economic development programme

2.2.9 Several additional support policies for agricultural cooperatives

2.3 Policies encouraging the development of farmer groups

2.3.1 Tax preference

2.3.2 Credit preference

2.3.3 Additional types of support

2.4 Provincial policies in support of the development of ACs/FGs and production-trade linkage associated with the LSRF approach

2.4.1 Ca Mau province

2.4.2 Bac Lieu province

2.4.3 Soc Trang province

2.4.4 An Giang province

3. The Current Situation of Production–Trade Linkages Associated with Large Scale Rice Fields

3.1 Implementation in recent years in the 4 provinces surveyed

3.2 AC and FG implementation of the LSRF approach

3.3 Linkage between agricultural cooperatives / farmer groups and enterprises / traders

3.3.1 The role of agricultural cooperatives and farmer groups in trade linkage

3.3.2 Investment support by partners for agricultural cooperatives and farmer groups in trade linkage

3.3.4 Benefits gained from the rice trading linkage

3.3.5 Difficulties encountered by ACs/FGs in trade linkage

3.3.6 Support needs when implementing linkage and LSRF

3.4 ACs and FGs which do not implement the LSRF approach

3.4.1 Reasons why ACs and FGs do not implement the LSRF approach

3.4.2 AC/FG needs for implementing the LSRF approach

3.5 ACs and FGs which do not engage in trade linkage

3.5.1 Reasons why ACs and FGs do not engage in rice trading linkage

3.5.2 AC/FG needs for trade linkage

4. Current Capacity and Operation of Agricultural Cooperatives in The Four Provinces Surveyed

4.1 Current development of ACs in the provinces surveyed

4.2 Current capacity of AC managers

4.2.1 Education level

4.2.2 Capacity and work experience of key managers in agricultural cooperatives

4.2.3 Capacity-building for cooperative personnel

4.3 The participation of members in agricultural cooperatives

4.3.1 The number and scale of production of members

4.3.2 Capital contribution from members of agricultural cooperatives

4.3.3 Use by members of AC services

4.3.4 Involvement in AC management

1414

15

15

15

15

1616

16

17

17

18

18

19

20

21

23

23

24

24

25

25

25

26

26

26

26

26

27

28

28

29

29

30

32

32

33

37

40

41

43

43

44

46

46

47

48

48

49

49

50

52

55

55

55

56

56

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

54

4.4 Current situation of governance capacity of ACs

4.5 Current capital and assets situation of agricultural cooperatives

4.5.1 Land

4.5.2 Assets

4.5.3 Capital

4.6 Production and business operation of agricultural cooperatives

4.6.1 Goals and strategies

4.6.2 Business operations that ACs are implementing and will implement

4.6.3 Linkage and association with other stakeholders

4.6.4 Application of good agricultural practices and building the brand name

4.7 Performance of agricultural cooperatives

4.7.1 Turnover and profit

4.7.2 Price of services that ACs provide to members

4.8 Government support for ACs

4.9 Strengths and difficulties of agricultural cooperatives

4.9.1 Strengths

4.9.2 Difficulties of ACs

4.10 Agricultural cooperatives’ support requirements

4.10.1 Issues on which ACs need support

4.10.2 Contents and methods of building capacity for cooperative managers

5. Current Capacity and Operation of Farmer Groups in The Four Provinces Surveyed

5.1 Numbers of farmer groups in the four provinces surveyed

5.2 Capacity of FG managers

5.2.1 Education level

5.2.2 Capacity and work experience of key personnel

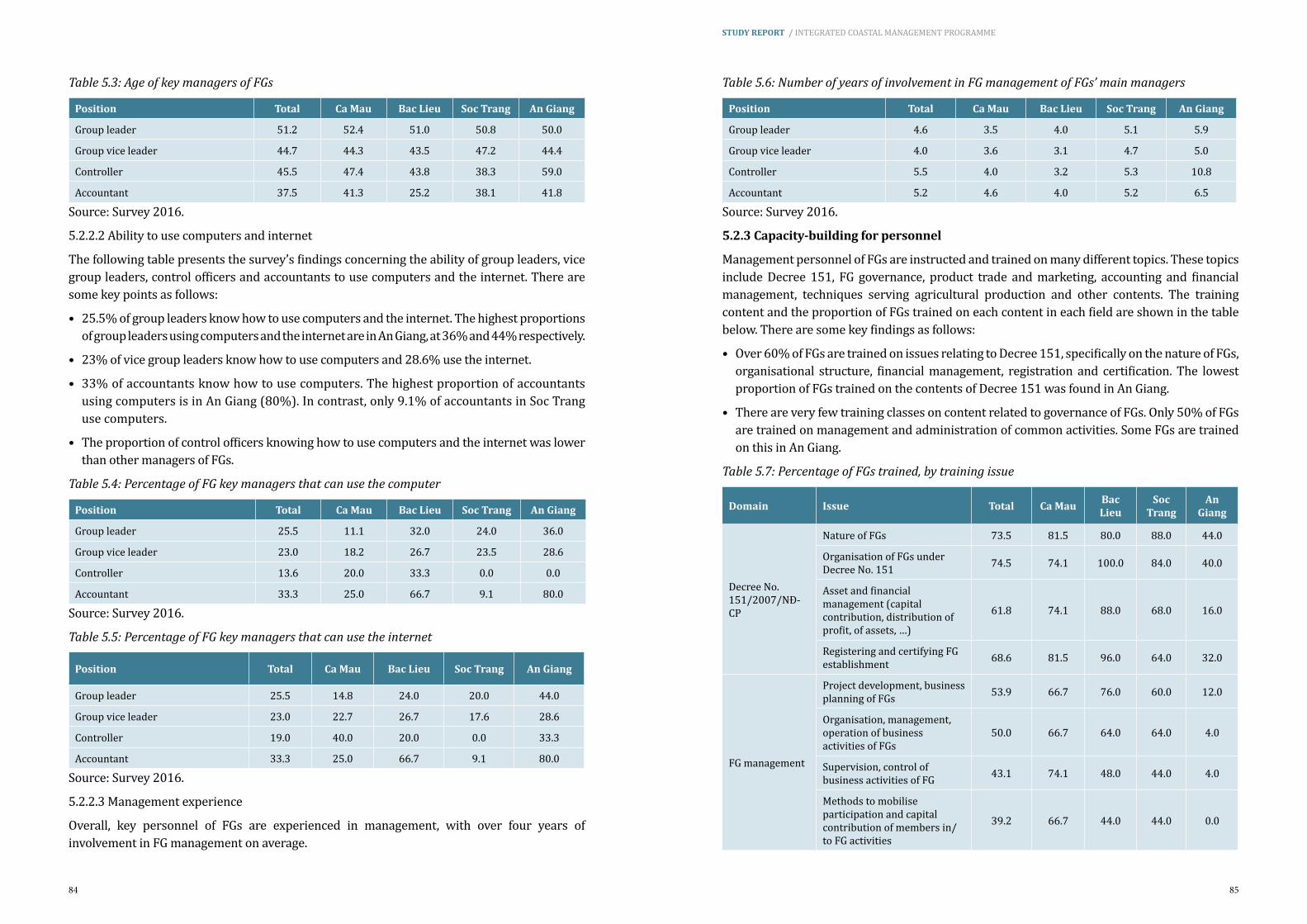

5.2.3 Capacity-building for personnel

5.3 Membership of farmer groups

5.3.1 The number and scale of production of members

5.3.2 Capital contribution

5.3.3 The use of services

5.3.4 Involvement in FG management

5.4 Farmer group governance

5.4.1 Executive administration

5.4.2 Partnership agreement/collaborative regulations

5.4.3 Task assignments among members of management personnel

5.4.4 Operational management

5.5 Capital and assets

5.5.1 Land

5.5.2 Assets

5.5.3 Capital

5.6 Operation of farmer groups

5.6.1 Goals and strategies

5.6.2 Ongoing production and business operations

5.6.3 Services rendered for non-members of farmer groups

5.6.4 Services provided in 2014-2015 that will no longer be provided in the coming period

5.6.5 New services in the coming period

5.7 Performance of farmer groups

5.7.1 Turnover and profit

5.7.2 Performance

5.7.3 Price of services that FGs provide to members

5.8 Government support for FGs

5.9 Strengths and difficulties of farmer groups

5.9.1 Strengths

5.9.2 Difficulties of FGs

5.10 Farmer groups’ support requirements

5.10.1 Issues on which FGs need support

5.10.2 Contents and methods of building capacity for management personnel

6. Current Shortcomings and Challenges for The Development of Acs, Fgs, Linkage and Lsrf

6.1 Current shortcomings and challenges in production-trade linkage and LSRF

6.1.1 Policies not strong enough to encourage enterprises to engage in linkage between the production and trade of rice

57

59

59

60

61

64

64

66

72

73

73

73

74

75

78

78

78

80

80

80

82

82

82

82

83

85

87

87

88

88

89

89

89

90

91

92

92

92

93

94

94

94

96

97

98

98

100

100

101

102

103

105

105

106

107

107

108

109

109

110

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

76

6.1.2 Low number of enterprises having sufficient potential for linkage

6.1.3 Weakness in capacity of agricultural cooperatives/farmer groups

6.1.4 Other shortcomings

6.2 Shortcomings and challenges for cooperative development

6.2.1 The relatively high proportion of nominal and weak cooperatives

6.2.2 Operations of agricultural cooperatives failing to satisfy the needs of their members

6.2.3 Weak capacity of agricultural cooperatives

6.2.4 Inadequate awareness of the nature and role of agricultural cooperatives

6.2.5 Drawbacks of preferential policies on agricultural cooperatives

6.2.6 Public services failing to support agricultural cooperatives

6.2.7 Unsuitable cooperative model

7. Some Typical Linkage Models7.1 Model of linkage between enterprises/agencies supplying materials and ACs/FGs

7.2 Model of commercial enterprise in production-trade linkage and support for agricultural cooperatives

7.3 Model of AC organising LSRF for members, buying paddy of members and reselling to trading partner

7.4 Factors ensuring the success of agricultural cooperatives

7.4.1 Participation of members

7.4.2 Capacity of AC managers

7.4.3 Public and transparent governance

7.4.4 Operations matching the needs of members

7.4.5 Suitable scale of agricultural cooperatives

8. Solutions for Development of Acs And Fgs And Promotion Of Linkage Between Rice Production And Trade

8.1 Approach to the development of ACs/FGs and linkage between production and trade

8.1.1 Finding a scale of linkage that matches the local conditions

8.1.2 Deciding on whether development as AC or FG better fits capacity and operational management

8.1.3 Linkage between production and trade as a basis to promote the development of ACs/FGs

8.1.4 Support to build capacity for the strategic success of ACs/FGs

8.2 Proposed AC model

8.3 Solutions for promoting rice production under the large scale rice field and production-trade linkage models

8.4 Solutions to build AC capacity and operations

8.4.1 Raising awareness among local government, AC managers and membership

8.4.2 Training the state management staff on ACs

8.4.3 Training and using network of consultants

8.4.4 Training on governance and operation for managers

8.4.5 Assistance to implement production and business plans and establish necessary regulations

8.4.6 Assistance to implement common technical processes and have quality certification

8.4.7 Strengthening the role of public authorities

8.5 Solutions to support FGs

9. Conclusions9.1 Current situation of linkage between rice production and trade

9.2 Current situation of the development of agricultural cooperatives and farmer groups

9.3 Policies and solutions for local implementation

10. References11. Appendix

111

111

111

111

111

111

111

112

113

113

114

114114

115

117

118

118

119

119

119

119

120

120

120

120

121

121

121

122

122

122

123

123

124

127

127

127

127

128128

129

130

131132

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

98

Tables CategoryTable 3.1: Rice sowing area in LSRF in 4 provinces surveyed (ha)

Table 3.2: Percentage of ACs and FGs implementing the LSRF approach

Table 3.3: Percentage of ACs and FGs applying collective rice production process

Table 3.4: Percentage of ACs and FGs experiencing difficulties in LSRF implementation

Table 3.5: Percentage of ACs and FGs surveyed with an agreement with trading partners

Table 3.6: Types of partners with which ACs and FGs have trading agreements

Table 3.7: Roles of ACs and FGs in linkage for trading paddy produce

Table 3.8: Percentage of ACs and FGs with agreements and investment by trading partners

Table 3.9: Forms of partner investment in ACs in rice trading linkage

Table 3.10: Additional costs for enterprises in linkage with ACs and FGs

Table 3.11: Requirements of trading partners upon ACs and FGs and role in linkage

Table 3.12: Percentage of ACs and FGs receiving support when engaging in linkage

Table 3.13: Benefits gained through linkage in paddy trading

Table 3.14: Profit increase (in %) though linkage compared to situation without linkage

Table 3.15: Forms of determining paddy price

Table 3.16: Percentage of ACs and FGs which sold their paddy at a price higher than the market price

Table 3.17: Benefits gained by ACs and FGs from linkage with trading partners

Table 3.18: Difficulties encountered by ACs and FGs in linkage

Table 3.19: Percentage of members of ACs and FGs fulfilling commitments to trading partners

Table 3.20: Types of support needed by ACs in rice trading linkage and in LSRF

Table 3.21: Types of support needed by FGs in rice trading linkage and in LSRF

Table 3.22: Reasons why ACs and FGs did not apply LSRF (% of ACs and FGs)

Table 3.23: Percentage of ACs and FGs expecting to implement the LSRF approach

Table 3.24: Types of support needed by ACs to engage in the LSRF approach

Table 3.25: Types of support needed by FGs to engage in the LSRF approach

Table 3.26: Reasons for ACs and FGs not linking to trading partners

Table 3.27: Percentage of ACs and FGs wanting to engage in linkage for paddy sale

Table 3.28: Types of support needed by ACs and FGs to have linkage with paddy trading partners

Table 4.1: Current situation in the 4 provinces surveyed

Table 4.2: Percentage of ACs at various performance levels

Table 4.3: Education level of AC managers

Table 4.4: Age of key managers of ACs

Table 4.5: Percentage of AC key managers that can use the computer

Table 4.6: Percentage of AC key managers that can use the internet

Table 4.7: Number of years of involvement in AC management of ACs’ main managers

Table 4.8: Percentage of ACs trained, by training issue

Table 4.9: Percentage of AC staff trained, by training issue

Table 4.10: Members and sizes of ACs

Table 4.11: Contribution of chartered capital by AC members

Table 4.12: Percentage of members using AC services

Table 4.13: Percentage of AC members that has letter of participation and participated in AC’s congress

Table 4.14: Percentage of ACs having management regulations

Table 4.15: Percentage of ACs assigning specific tasks to individual managers and recording the minutes of meetings (% of ACs)

Table 4.16: Operating activities of ACs (% of ACs)

Table 4.17: Percentage of ACs that expels members if they do not use the AC’s services

Table 4.18: Percentage of ACs producing financial reports and audits

Table 4.19: Percentage of ACs having collective land

Table 4.20: Percentage of ACs having machines and equipment for business activities

Table 4.21: Value of assets and machinery of ACs for business activities (million VND)

Table 4.22: Register and implementation of chartered capital contribution of ACs

Table 4.23: Real chartered capital contribution of AC members, by AC size

Table 4.24: Current debt of ACs

Table 4.25: Partners in debt to ACs

Table 4.26: Reasons why ACs experience difficulty in gaining loans from commercial banks

Table 4.27: Operational objectives of ACs at present and in the near future

Table 4.28: Strategies of ACs

Table 4.29: Percentage of ACs engaging in group business activity

Table 4.30: Services rendered by ACs to members

Table 4.31: Services rendered by ACs to non-members

Table 4.32: Percentage of ACs that provided the services in 2014-2015 but no longer provides them in 2016

29

30

30

31

32

32

33

34

34

35

36

37

38

38

39

39

40

40

41

41

42

43

44

44

45

46

47

47

48

49

49

50

50

50

50

53

54

55

55

56

56

57

57

58

58

59

59

60

60

61

62

62

63

63

64

65

66

66

67

68

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

1110

Table 4.33: Percentage of ACs having new service to provide in near future

Table 4.34: Reasons why ACs provide new services (% of ACs)

Table 4.35: Difficulties of ACs when providing new services (% of ACs)

Table 4.36: Activities that ACs want to do, but are unable to

Table 4.37: Percentage of ACs that want to, but can not do a given new activity

Table 4.38: Reasons why ACs do not implement desirable activities

Table 4.39: Percentage of ACs with linkage to other stakeholders to serve their members

Table 4.40: Types of stakeholders with which ACs have linkage contract to serve their members

Table 4.41: Percentage of ACs applying good production practice process

Table 4.42: Turnover and profit of ACs

Table 4.43: Operational performance of ACs in 4 provinces surveyed

Table 4.44: Operational performance of ACs by AC size

Table 4.45: Evaluation of prices of inputs and production services provided by ACs

Table 4.46: Support by state to ACs in 4 provinces surveyed

Table 4.47: Percentage of ACs receiving state support, by type of support

Table 4.48: Percentage of ACs seeking guidance from stakeholders when necessary

Table 4.49: Strong points of ACs in 4 provinces surveyed (Unit: % of ACs)

Table 4.50: Difficulties of ACs in 4 provinces surveyed

Table 4.51: The greatest difficulties of ACs at present (% of ACs)

Table 4.52: Percentage of ACs requiring support, by issue

Table 4.53: Training needs of ACs (% of ACs)

Table 4.54: Training methods that ACs want (% of ACs)

Table 5.1: Number of FG in provinces surveyed

Table 5.2: Education level of FG managers

Table 5.3: Age of key managers of FGs

Table 5.4: Percentage of FG key managers that can use the computer

Table 5.5: Percentage of FG key managers that can use the internet

Table 5.6: Number of years of involvement in FG management of FGs’ main managers

Table 5.7: Percentage of FGs trained, by training issue

Table 5.8 Percentage of FG staff trained, by training issue

Table 5.9: Members and sizes of FGs

Table 5.10: Contribution of chartered capital by FG members

Table 5.11: Percentage of members using FG services

Table 5.12: Managerial organisation of FGs

Table 5.13: % of FGs having assigned tasks for managers

Table 5.14: Percentage of FGs having regulations stipulated in cooperation contract

Table 5.15: Percentage of FGs having managerial regulations

Table 5.16: Percentage of FGs whose cooperation contracts are certified by PPC

Table 5.17: Percentage of FGs that has assigned tasks to members of their managerial committee

Table 5.18: Operational management of FGs (unit: % of FGs)

Table 5.19: Percentage of FGs having common land

Table 5.20: Percentage of FGs having machines and equipment for business activities

Table 5.21: Value of assets and machinery of FGs for business activities (million VND)

Table 5.22: Chartered capital, debt and working capital of FGs (million VND)

Table 5.23: Operational objectives of FGs at present and in the near future

Table 5.24: Business strategy of FGs

Table 5.25: Percentage of FGs wanting to develop into AC

Table 5.26: Services rendered by FGs to members

Table 5.27: Services rendered by FGs to non-members

Table 5.28: Percentage of FGs that provided services in 2014-2015 but no longer provides them in 2016

Table 5.29: Percentage of FGs expecting to provide new service in near future

Table 5.30: Reasons why FGs provide new services (% of FGs)

Table 5.31: Difficulties of FGs when providing new services (% of FGs)

Table 5.32: Turnover and profit of FGs (Unit: million VND)

Table 5.33: Operational performance of FGs in 4 provinces surveyed

Table 5.34: Operational performance of FGs by FG size

Table 5.35: Evaluation of prices of inputs and production services provided by FGs

Table 5.36: Support by state to FGs in 4 provinces surveyed

Table 5.37: Percentage of FGs receiving state support, by type of support

Table 5.38: Percentage of FGs seeking guidance from stakeholders when necessary

Table 5.39: Strong points of FGs in 4 provinces surveyed (Unit: % of FGs)

Table 5.40: Difficulties of FGs in 4 provinces surveyed

Table 5.41: The greatest difficulties of FGs at present (% of FGs)

69

69

70

71

71

72

72

72

73

73

74

74

75

75

76

77

78

78

79

80

81

82

82

83

84

84

84

85

85

86

87

88

88

89

90

90

91

91

92

92

92

93

93

94

95

95

96

97

98

98

98

99

100

100

101

102

102

103

103

105

105

106

107

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

1312

Table 5.42: Issues on which FGs need support (% of FGs)

Table 5.43: Training needs of FGs (% of FGs)

Table 5.44: Training methods that FGs want (% of FGs)

Table 11.1: Types of AC staff trained in Ca Mau, by training issue (% of ACs)

Table 11.2: Types of AC staff trained in Bac Lieu, by training issue (% of ACs)

Table 11.3: Types of AC staff trained in Soc Trang, by training issue (% of ACs)

Table 11.4: Types of AC staff trained in An Giang, by training issue (% of ACs)

Figure CategoryFigure 4.1: Structure of ACs in the provinces surveyed

Figure 4.2: Client strategy of ACs

Figure 4.3: Ways that ACs provide new services

Figure 5.1: Proportion of members that participated in last meeting of FG

Figure 5.2: Client categories served by FGs

List Of Abbreviations

Abbreviation Meaning

1M5R 1 must 5 reduction

3R3G 3 reduction 3 gain

AC Agricultural cooperative

DARD Department of Agriculture and Rural Development

FG Farmer group

ICMP Integrated Coastal Management Programme

LSRF Large scale rice field

MB Member

PPC Provincial People’s Committee

VND Viet Nam Dong

107

108

109

132

133

134

135

48

65

70

89

96

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

1514

1. Introduction1.1 Study context

Since 2013, Viet Nam has embarked upon agricultural restructuring geared towards improving value added and promoting sustainable development. The aim of this restructuring is to increase the value added and the competitiveness of agricultural products in Viet Nam, and to deliver benefits for farmers. The context is that Viet Nam’s economy has integrated deeply into the world economy. One of the important measures to achieve restructuring is to reorganise commodity production in a manner that addresses the key role of enterprises and cooperative economic organisations of farmers such as agricultural cooperatives and farmer groups. There are many policies encouraging enterprises, agricultural cooperatives, farmer groups and households. In the crop sector, the Prime Minister issued Decision No. 62/2013/QD-TTg, which aims to encourage development and cooperation and promote production-trade linkage and the large scale rice field (LSRF) concept. The main object of this policy is rice production.

Many preferential policies and instruments supporting the development of agricultural cooperatives and farmer groups have been established by the state. The 2012 law on cooperatives, with special guidelines, and the new policies issued to develop agricultural cooperatives by giving them a new orientation all seek to enhance economic cooperation. Government Decree No.151 is concerned with the development of farmer groups. In addition to the policy of the Central Government, the provinces also have specific policies for the development of agricultural cooperatives, farmer groups and linkage.

Although there are many preferential policies and incentives, and local people are interested in developing links between production and product consumption and agricultural cooperatives, production-trade linkage associated with the LSRF concept is very limited. The rice cropping area involved in production-trade linkage has remained small, however, in the LSRF associated with the linkage in production-trade is less than rice area of linkage in production-trade. There are many reasons for this. They concern policy issues, implementation aspects as well as the capacity of stakeholders in the linkage chain and in LSRF management, especially agricultural cooperatives and farmer groups. A number of agricultural cooperatives and farmer groups have sought to improve efficiency, which is also subject to constraints, and to better serve the needs of their members.

Phase 2 of Integrated Coastal Management Programme (ICMP) implementation in 5 provinces in the Mekong Delta aims to support sustainable development in coastal areas in the Delta, responding to the challenges of climate change and other environmental changes. One of the programme’s approaches is to help farmers adapt to climate change. In particular, the project aims to assist small-scale farmers in engaging in rice production-trade linkage with sustainable farming processes that reduce the use of pesticides and maintain environmental quality.

One of the programme’s approaches is to help local people develop the LSRF model associated with production-trade linkage. As a basis to help local policy development as well as activities, ICMP has designed a plan of action in support of the development of production-trade linkage and LSRF. Research has been performed to survey and evaluate organisational and implementation aspects in linkage, and the operational capacity of ACs and FGs. On this basis, solutions are to be

proposed to the provincial authorities, by which the programme supports the development of ACs and FGs involved in production-trade linkage and rice production under the LSRF approach.

1.2 Study objectives

The research had several specific objectives:

• To provide an overview of preferential policies and support instruments for ACs and FGs, and of policies that encourage production-trade linkages associated with the LSRF concept.

• To assess the capacity and operation of ACs and FGs in terms of human resources, administration, property, capital and efficiency.

• To review the implementation of production-trade linkage approaches associated with the LSRF concept.

• To identify the difficulties in terms of management capability and operational mechanisms as well as the support needs of ACs and FGs and the various difficulties in production-trade linkage associated with the LSRF concept.

• To propose solutions for improving the capacity and operation of ACs and FGs as well as promoting rice production under the LSRF and production-trade linkage concepts.

1.3 Study method

1.3.1 Method of information collection

The research was conducted by the following methods:

• Methodology expert: this method was used in the research to provide an overview, analyse policy documents and gather other secondary materials.

• Round table discussion: this was used to communicate with the state management agencies, support agencies for linkage, agricultural cooperatives, and local farmer groups.

• Direct interview: this used questionnaire sheets to conduct interviews with members of management boards, directors and chief accountants of agricultural cooperatives and heads of companies.

1.3.2 Survey sample

The research was conducted in four provinces: Ca Mau, Bac Lieu, Soc Trang and An Giang. The purpose of the research was to serve the local authorities and ICMP in devising policies and solutions in support of AC and FG development, production-trade linkage and the LSRF concept in rice production. The research therefore only covered ACs engaged in crop production, especially ACs producing rice.

Due to the differences in the number of crop cooperatives in the four provinces, the number of surveyed ACs in the sample in each province differed accordingly.There are very few crop cooperatives in Ca Mau and Bac Lieu, so in each of those provinces only 10 agricultural cooperatives were surveyed (this is almost all the crop cooperatives in those two provinces). In Soc Trang and An Giang there are more crop cooperatives, so in each of those provinces 30 ACs were surveyed. A total of 80 agricultural cooperatives were surveyed. In Soc Trang and An Giang provinces, the research prioritised ACs which have organised production operations on the basis of the LSRF approach or production-trade linkage.

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

1716

2. Policy OverviewThis part focused on reviewing the policies issued by the Government, including: i) policies for encouraging production-trade linkage and LSRF; ii) policies for agricultural cooperative development; iii) policies for farmer group development. Finally, support policies in the four provinces surveyed were also reviewed.

2.1 Overview of policies encouraging production-trade linkage associated with the LSRF concept

There are many preferential policies and support instruments for stakeholders involved in rice production-trade linkage and LSRF establishment. These policies and instruments encourage enterprises in the value chain and the organisations (ACs, FCs), representing farmers. However, to receive these state preferences and support, enterprises, farmer organisations and farmers must meet a number of specific conditions.

2.1.1 The approach of preferential and supportive policies

The general approach in the development of policies to encourage cooperation, production-trade linkage and LSRF production is as follows:

1. This policy of encouragement means that participation is not mandatory for enterprises in the value chain, farmer organisations and farmers. Participation in cooperation, production-trade linkage and LSRF production is voluntary on the part of the stakeholders in the value chain.

2. The approach proceeds on a project basis. To receive preference and support, stakeholders involved in production-trade cooperation and linkage must have a project or plan to establish an LSRF which is approved by the competent authority at the PPC (Article 5, Circular 15/2014). Thus, enterprises representing farmer organisations must develop the project or plan of establishing an LSRF and submit it to the competent authority for evaluation and approval. Only when approval is given, will the implementation of the project linkage associated with the LSRF receive support.

3. The LSRF project or plan must be located in the LSRF planning area of the province. Thus, if enterprises and representing farmer organisations would like to engage in an LSRF project, the first step is that the provincial authority determines the LSRF planning area.

4. There is a contract which is signed by stakeholders involved in cooperation and linkage.

5. The minimum duration of the project or planning is five years for annual crops and seven years for perennial crops.

6. The project must include both production under LSRF and consumption of products. If only buying output products or buying products without production under LSRF, the project is not eligible for receiving preferences or support from the state under Decision 62.

7. Enterprises must have strong potential in terms of both financial and human resources. Enterprises must ensure that they have the material area, drying capabilities, warehouses, processing facilities and investment capacities for farmers to produce.

8. The Government only regulated the principles and conditions for preferences and support and not the specific content of preferences and support. The specific level of support is stipulated by the individual province based on its resources. The provincial budget needs to make provision for such support.

2.1.2 Preference and support for enterprises in cooperation and production-trade linkage associated with LSRF establishment

Enterprises involved in cooperation, production-trade linkage and LSRF establishment receive preferences and support relating to land, export, temporary storage, infrastructure planning for production, and access to preferential credit from the Government. The specific preferences and support for enterprises are as follows:

Preference and support under Decision 62/2012:

• Exemption from land use and land lease when the state allocates or leases land for the project to build processing plants, warehouses, worker housing, and public buildings serving the LSRF project;

• Priority to participate in the Government’s export contract or temporary storage programme for agricultural products;

• Partial contribution of funds for implementing planning, improving fields, completing transport systems and field irrigation, upgrading electrical systems;

• Support up to 50% of funding for the organisation of training and technical guidance to farmers.

Preferential access to credit

Implementing Resolution 14/NQ - CP, the state bank issued Decision 1050/ QD-NHNN dated 28 May 2014 guiding the implementation of a pilot loan programme under Resolution 14 with a number of specific credit mechanisms. For instance, the preferential lending interest rate is lower than the conventional interest rate by 1 to 1.5% per year. The level of loan can be up to 70% of the project value. In the event that customers do not have enough collateral, the bank can lend without the collateral on the basis of cash flow control. If a chain link loans over 12 months, but not more than 18 months, every stage of production, processing and consumption is less than 12 months, and customers commit to pay a part of the debt after each stage, the commercial banks may consider applying short-term interest rates for customers.

Decree No. 55/2015/ND-CP on credit policies in service of agricultural development allowed commercial banks to provide ACs and FCs with credit without collateral, to a maximum of 70% of the project value, and loans for planning under the model of production-trade linkage and LSRF establishment (Article 14, Decree 55/2015).

2.1.3 Preferential policies for organisations representing farmers in the linkage

According to Decision 62/2013, organisations representing farmers consist of ACs, FCs without FGs. The ACs and FCs participating in cooperation, rice production-trade linkage and LSRF projects receive preference and support as follows:

• Exemption from land use and land lease when the state allocates or leases land for a project to build processing plants, warehouses, worker housing, and public buildings serving the LSRF project;

• Priority to participate in the Government’s export contract or temporary storage programme for agricultural products;

• Support up to 30% in the first year and 20% in the second year of the actual cost of pesticides, labour force, machine hire to perform general services for members;

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

1918

• Support up to 50% of funding for staff training of ACs, FCs towards management, economic contracts and production techniques;

• Support up to 100% of funding for training courses and technical guidance to farmers to produce agricultural products under contract.

Preferential access to credit

• In implementation of Resolution 14/NQ - CP, the state bank issued Decision 1050/ QD-NHNN dated 28 May 2014 guiding the implementation of a pilot loan programme under Resolution 14. This involves a number of specific credit mechanisms, such as a preferential lending interest rate lower than the conventional lending interest rate by 1 to 1.5% per year. The level of loan can be up to 70% of the project value. In the event that customers do not have enough collateral, the bank can lend without collateral on the basis of cash flow control. If a link chain loans over 12 months, but not more than 18 months, every stage of production, processing, consumption is less than 12 months, and customers commit to pay a part of the debt after each stage, the commercial banks may consider applying short-term interest rates for customers.

• Decree No.55/2015/ND-CP on credit policies in service of agricultural development allowed commercial banks to provide ACs and FCs loans without collateral, to a maximum of 70% of the project value, and loans for planning under the model of production-trade linkage and LSRF establishment (Article 14, Decree 55/2015).

2.1.4 Preferential support for farmers participating in linkage and LSRF production

Under Decision 62/2013, farmers who participate in cooperation, production-trade linkage and LSRF establishment receive the following support:

• One-of support for up to 30% of the cost of purchasing seeds getting the quality inspector certification and the same quality certified, or reaching higher to do crop in the first season in the LSRF project.

• Support for 100% funding of training and technical guidance for farmers.

• Support for 100% funding of warehousing in enterprises, whereby the maximum duration is 3 months for government-implemented temporary storage of agricultural products.

2.2 Overview of policies encouraging agricultural cooperative development

Since it was founded in 1954, and up to the present, the institution of the agricultural cooperative (AC) has always been a component of the collective economy. However, there have been some changes in the nature of ACs that reflect the historical situation of the country. The first law on cooperatives was enacted in 1996, and revised in 2003 and 2012. From 2013 to now, ACs in Viet Nam have operated under the law on cooperatives enacted in 2012. There are many ACs, especially in the north, where they were established before the first AC law was promulgated. Since then, they have experienced many changes in AC law, notably the amendments of 2003 and 2012. Therefore, the operation of ACs in Viet Nam has been strongly influenced by historical factors.

According to the AC law which was passed in 2012, an AC is a collective economic organisation with co-owners and legal entity status, which can be established voluntarily by at least 7 members (individuals, households, organisations) who cooperate with and assist one another mutually in production, business and job creation. Moreover, it aims to meet the common needs

of members, in a manner based on autonomy, self-responsibility, equality and democracy in AC management. Some principles of AC organisation and operation are as follows:

• Legal entity status: an AC is a collective economic organisation with legal entity status.

• Number of members: there are at least seven members, who are individuals, households or organisations.

• Organisational structure: there must be a Board, Supervisory Board (or control officers), director and accountant.

• Operation: an AC is implemented by members for the main purpose of service operation or job creation for members.

• Capital contribution: all members must contribute to the authorised capital of ACs or FCs, no later than 6 months from the date of registering the AC. A member is entitled to contribute the highest authorised capital, which must not exceed 20% of the authorised capital of the AC.

• Responsibility for membership: to ensure the proper role of the ACs, which is to support their members, the Government has set the rule that AC service provision for members must make up at least 68% of the total value of AC service operation.

• Profit distribution mechanism: the 2012 law on cooperatives required ACs to spend most of the profit after tax for distribution to members, apportioned according to the value of the services rendered by them, with the remainder of the profit being distributed according to the capital contributed. This principle is completely contrary to the provisions of the 2003 law on cooperatives, under which most of the profits are divided according to capital contributions. However, a problem with the 2012 law was that the documents providing guidance on how to implement the law did not clearly explain how income was to be determined.

• Undivided assets: an AC’s assets are not divided when it is disbanded, bankrupted or membership ends.

The 2012 law on cooperatives provided that ACs had to apply to re-register by 31 June 2016 at the latest. Only those ACs meeting the new requirements could re-register under the provisions of the 2012 law.

ACs are viewed as performing an important role in the collective economy, and therefore receive preferential policies and support from the state.

2.2.1 Policies for preferential access to credit

Under the 2012 law on cooperatives, ACs receive: (i) Support for accessing capital and funding for cooperative development (Section D, Clause 1, Article 6); and (ii) support for preferential credit for ACs operating in agriculture, forestry, fisheries and salt production (Section C, Clause 3, Article 6). ACs can receive preferences and support as follows:

Decree 193/2013 regulates policy on access to capital and cooperative development funding (paragraph 4, Article 24) and on preferential credit for ACs operating in agriculture, forestry, fisheries and salt production (Clause 3, Article 25) as follows:

(1) Support for preferential interest rates and loan guarantees for funding to support the development of ACs (Decree 193/2013). ACs receive preferential loans for up to 5 years from

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

2120

investment funds, and are supported with a maximum refund of 80% of nominal capital expenditure that may not exceed 3 years.

(2) When ACs have a project to invest in production, business and export, this has access to preferential investment in accordance with the law on investment.

(3) Preferential loans are supported by the Government under Decree No. 41/2010, whereby ACs operating in agriculture and rural areas can borrow capital without collateral if they have assets of up to 500 million. Decree 55/2015 replaced ND41 with many amendments and supplements to create more favourable conditions for providing credit to ACs. ACs can be mortgaged for loans up to the amount of 3 billion.

(4) Support for preferential credits is targetted to operations reducing post-harvest losses1: (a) ACs are supported with 100% of the commodity value and 100% of the interest in the first two years and 50% of the interest in the third year; (b) ACs are also supported in the interest rate and receive subsidies covering the interest rate gap of the loan, to a maximum of 70% of the loan for the project and a maximum duration of 12 years for ACs investing in production lines, machines and equipment to reduce losses in agriculture, or in projects for manufacturing machines and equipment for agricultural production.

(5) In addition, ACs receive support for loan interest when loans are granted to enter into contracts for production-consumption linkage with value-chain enterprises as mentioned above.

2.2.2 Policies for preferential land allocation and leases

Decree 193 (Paragraph 2, Article 25) regulates land allocation policy and land leases serving AC or FC operation in agriculture, forestry, aquaculture and salt production. Land support for ACs and FCs is implemented under the provisions of the land law. Currently, there are no specific guidelines for land policy implementation under Decree 193 by the ministries or departments. Land policies applicable to the 2003 law on agricultural cooperatives, set forth in Decree No. 88/2005 / ND-CP (Article 5) and some other documents, are as follows:

Content of land support policies: ACs are allocated land with/without payment (for ACs); moreover, they are assigned land lease to develop production and business establishments and render services directly for their members.

Duration of the assigned land allocation or land lease: (i) duration is not more than 50 years under the review, the decision on the basis of investment projects; or the application for land allocation, land lease; (Ii) duration is not more than 70 years for projects involving large-scale investment but slow capital recovery; investment projects in geographical areas with difficult socio-economic conditions or extremely difficult ones. ACs are allocated land by the state and are granted land-use right certificates under the provisions of Article 53 of Decree No. 181/2004 / ND-CP guiding implementation of the 2003 law on land.

Exemption from and reduction of leases of land and water surfaces2: ACs lease land and water surfaces to engage in agriculture, forestry, aquaculture, salt production and some other forms of production. In particular: (1) Decision No 68/2013/QD-TTg replaced Decision No 63/2010/QD-TTg and Decision No 65/2010/QD-TTg on the policies for support to reduce post-harvest losses in agricultural products and fisheries.(2) Decree No. 142/2005/ND-CP dated 14 November 2005 on cost collection of land lease and water surface lease; Circular No. 120/2005/TT-BTC of the Minister of Finance dated 30 December 2005 guiding the implementation of Decree No. 142/2005/ND-CP; Circular No. 141/2007/TT-BTC dated 30 November 2007 of the Minister of Finance on guidelines and amendment to Circular No. 120/2005/TT-BTC.

+ Duration of and preferential exemption from lease of land and water surfaces for ACs: (1) Exemption from land lease for three years applies if the project is on the list of areas to encourage investment, or if the project at the new business establishment of an economic organisation is implemented as planned relocation because of environmental pollution; (2) Exemption from land lease for five years applies if the project invests in areas with difficult socio-economic conditions, which are on the list of particular areas in order to encourage investment; (3) Exemption from land lease for seven years applies if the project has invested in areas with extremely difficult socio-economic conditions, which are on the list of particular areas to encourage investment; (4) Exemption from land lease for fifteen years applies if the project has invested in areas with extremely difficult socio-economic conditions, which are on the list of particular areas to encourage investment; (5) Exemption from land lease for the entire duration of the project applies if the project has invested in areas with extremely difficult socio-economic conditions, which are on the list of particular areas to encourage investment.

* The preferential exemption from AC land lease:

(1) Members of ACs lease land to use for agricultural production purposes (for perennial crops) under a project approved by competent authorities. The period of setting up an orchard is exempted from land lease, depending upon the type of tree and in accordance with planting techniques and perennial management, by the Ministry of Agriculture and under rural development provisions.

(2) Currently, under Decision No. 62/2013/QD-TTg ACs are exempted from land-use fees or land lease when the state allocates or leases land for the construction of drying yards, processing facilities or warehouses designed to serve an LSRF project.

+ Duration of and preferential exemption from lease of land and water surfaces for ACs: (1) ACs are exempted from 50% of the cost of land lease if they must pay for the entire duration of land lease as a basis for their business; (2) ACs lease land to use for agriculture, forestry, aquaculture or salt production and are affected by damage caused by natural disasters or fires: (a) If the damage is below 40% of output, the price of land lease is cut by a proportion corresponding to the percentage of damage; (b) if the damage is more than 40% of output, the AC is exempted for the year of loss.

2.2.3 Policies for preferential tax treatment

The 2012 law on cooperatives regulated that the state offer preferential income tax treatment for enterprises and preferential terms for some other taxes.

Policies for preferential corporate income tax

The income of ACs is exempted including (Clause 1, Article 4, Decree No. 218/2013/ND-CP): (i) income from cultivation, livestock, aquaculture and salt production; (ii) income from the agricultural cooperative in agriculture, forestry, fisheries and salt production carried out in areas with difficult socio-economic conditions or with extremely difficult ones; (iii) income from the provision of direct technical services to serve agriculture, such as irrigation, drainage, ploughing and harrowing the soil, dredging canals, controlling pests, treating diseases of crops and livestock, rendering services for harvesting agricultural products; (iv) income from the implementation of contracts for scientific research and technological development, or from the sale of products produced from tests or from new technology applied for the first time in Viet Nam; (v) income from undivided assets of ACs

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

2322

established and operated under the provisions of the law on cooperatives (Section 10, Article 4, Decree 218); (vi) income from the transfer of technology under the priority areas transferred to organisations and individuals in areas with extremely difficult socio-economic conditions (Clause 11, Article 4, Decree 218).

There are several conditions for the operation of ACs in agriculture, forestry, aquaculture and salt production which are exempted from corporate income tax if the proportion of supplies and services provided for members of an AC is over 68% of the total value of products and services of that cooperative (Decree 218 and Decree 193).

Tax rate of corporate income tax: (1) To be eligible for the 20%3 tax rate the AC’s total sales and service provision of the preceding year must not exceed 20 billion; (2) To be eligible for the 10%4 tax rate, income from the AC’s operations in agriculture, forestry, aquaculture and salt production which is not in areas of difficult socio-economic conditions or extremely difficult ones (except the income of ACs regulated in Clause 1, Article 4, Decree 218 as mentioned above).

Duration of tax exemption and tax cut: The duration of tax exemption and tax cut is calculated continuously from the first year in which the AC gained income, and its taxable income from the investment project receiving tax preference. In particular: (i) Tax exemption for four years and 50% tax cut for the next nine years: For newly established ACs investing in areas with extremely difficult socio-economic conditions. Such newly established ACs in the socialisation carried out on the list of areas with difficult socio-economic conditions or extremely difficult ones. (ii) Tax exemption for four years and 50% tax cut for the next five years: For newly established ACs in the socialisation carried out that there are not on the list of areas with difficult socio-economic conditions or extremely difficult ones. (iii) Tax exemption for two years and 50% tax cut for the next four years: For newly established ACs investing in areas with difficult socio-economic conditions.

Policies for other types of preferential tax treatment

License tax5: (i) License tax exemption for: service teams and stores, stores operating under ACs to provide directly the technical services needed for agricultural production; (ii) 50% license tax cut for central people’s credit fund of commune, ACs specialised in business services serving agricultural production, stores, stalls, shops etc. in mountain areas. Four levels of license tax apply to ACs (Circular No. 28/2011/TT-BTC): 3 million/year if the registered capital is more than 10 billion, 2 million/year if the registered capital is 5-10 billion, 1.5 million/year if the registered capital is between 2 and 5 billion and 1 million/year if the registered capital is less than 2 billion.

Value-added tax: (i) The 2008 law on value-added tax6: ACs are not subject to VAT on products and services such as cultivation, livestock, aquaculture and fishing; plant varieties and domestic animals; agricultural services (irrigation, drainage, ploughing, dredging canals,...); credit services, stock trading; medical services, veterinaries, health care for people and pets;

(3) Clause 2, Article 10, Decree 218/2013/ND-CP dated 26 December 2013 of the Government guiding the implemention of the 2013 law on corporate income tax.(4) Section e, Clause 2, Article 15, Decree 218/2013ND-CP guiding the implemention of the 2013 law on corporate income tax.(5) Circular No. 42/2003/TT-BTC dated 7 May 2003 of the Ministry of Finance guiding the implementation of Decree No. 75/2002/ND-CP dated 30 August 2002 of the Government on revising license tax.(6) Article 5, Law on value-added tax No. 13/2008/QH dated 3 June 2008 of the National Assembly.

public services for sanitation; teaching and vocational training; (ii) ACs and their members are not subject to value-added tax for aquaculture products which are exploited and sold7.

Personal income tax: tax exemption for households and individuals directly employed in aquaculture and fisheries8.

Import tax: import tax exemption for machinery, equipment, raw materials and components imported to the country that are not produced in the country, upgrading ships with a total main engine capacity of 400 CV or more9.

2.2.4 Policies encouraging new establishment and agricultural cooperative re-registration

Under Decree 193 ACs are supported in new establishment and re-registration by the state.

Specifically the following apply to new ACs: (i) Cooperative founders are assisted with free information, consulting, training on cooperative laws before establishing. (ii) ACs are supported with regulation consultancy, guidance and implementation of procedures for the establishment, registration and operation of cooperative organisations (Paragraph 6, Article 24). ACs preparing to establish anew receive financial support for founders (car payment, documents, food...)10.

ACs are re-registered and operate under the 2012 law on cooperatives, thereby receiving support for the establishment of new cooperatives.

2.2.5 Policies supporting retraining and training

Decree 193 (Clause 1, Article 24) stipulates that training for cooperative managers and members of cooperatives is funded by the state as follows:

• The objects of support for retraining and training consist of (a) the Management Board, Supervisory Board and the Chief Accountant, and (b) members doing work involving technical and professional expertise at the AC.

• The form and level of support is regulated by the provincial people’s committee and the city people’s committee. The funds are from local budgets or project development programmes.

+ These items in ACs are supported: (a) fares for using public transport (except airplane) from head offices of AC to on-site training; (b) costs of buying curriculum materials; (c) costs of organisation, classroom management, hall hire, faculty remuneration, visiting, surveying. Moreover, ACs engaged in agriculture, forestry, aquaculture and salt production are also supported with 50% of the cost of food and accommodation in accordance with the provisions of the training facilities.

+ The people in ACs and members of ACs sent for training (formal or in-service) at universities, colleges, secondary vocational schools and vocational schools are supported with at least 50% of tuition fees. They must meet the following conditions: (a) no more than 40 years old; (b) eligible for enrolment in training facilities; (c) sent to study by decision of the Management Board; (d) written commitment to work for the agricultural cooperative for at least 5 years after graduation.

(7) Decree No. 67/2014/ND-CP dated 7 July 2014 on some aquaculture development (valid until 31 December 2016).(8) Decree No. 67/2014/ND-CP dated 7 July 2014 on some aquaculture development (valid until 31 December 2016).(9) Decree No. 67/2014/ND-CP dated 7 July 2014 on some aquaculture development (valid until 31 December 2016).(10) Circular No. 173/2012/TT-BTC guiding the financial mechanism supporting cooperative founders, training objects and retraining of agricultural cooperatives.

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

2524

• Content of retraining and training: (i) To provide knowledge about policies and laws related to establishment and development of ACs; (ii) To provide knowledge about consultancy, support, updated economic information and planning; methods of organising production, management, product marketing of ACs; (iii) To train some majors of intermediate level, colleges and inter-university programme; (iv) To upgrade vocational training and capacity-building skills. Further support for ACs for retraining and training takes the following form:

+ ACs are supported with 100% of material costs and 50% of travel expenses for participating in training courses on agricultural expansion for ACs11.

+ Cooperative founders are reimbursed the costs of formal training and retraining in professional and technical expertise12.

+ ACs are supported in developing linkage and LSRF projects in accordance with Decision No. 62/2013 / QD-TTg as mentioned above.

2.2.6 Policies supporting trade promotion and market expansion

Under Decree 193/2013 (Paragraph 2, Article 24), ACs are supported by the state: (i) participation in exhibitions in Viet Nam and abroad; (iii) development of brand name, trademark, origin of goods; (iv) development and implementation of electronic portals, e-commerce exchanges for ACs and FCs.

In addition, ACs are “prioritised in the contracts for agricultural export or temporary storage of agricultural programmes of the Government”, according to Decision No. 62/2013 / QD-TTg on participating in linkage to build the LSRF approach.

2.2.7 Policies supporting the application of science and technology, new technology

Policies to support the application of science and technology and new technology for ACs are regulated in Decree 19313: (i) The annually endowed Fund for the national and provincial level of Science and Technology Development has a budget item supporting ACs and FCs in innovation and technology applications. This involves grants, partly for scientific research. Assistance is provided with funding of 60-100% for capital projects of production testing. Interest-free loans are available for projects applying the results of research and development in the country; loans are available at preferential interest rates for technology innovation projects. (ii) The state supports scientific and technological research in parallel with business funding of scientific and technological research for ACs and FCs. Research projects and the application of advanced science and technology and new technology are approved by competent authorities.

Policies are in place to support the application of innovation and improved technology in agricultural and fishery expansion. (i) If an AC has a project applying innovation and improving technology, this is eligible for medium and long term loans from the Fund for development of science and technology14. (ii) If an AC has organised training courses for members to acquire new technologies under the programme for applying and transferring models of science

(11) Decree 02/2010/ND-TTg dated 8 January 2010 of the Government on agricultural expansion.(12) Circular No. 173/2012/TT-BTC guiding the financial support mechanism for cooperative founders, objects of training and retraining of ACs.(13) Clause 3, Article 24, Decree 193/2013/ND-CP dated 21 November 2013 of the Government on regulation detailed a number of articles of the 2012 law on cooperatives.(14) The fund was establised under Decree No. 122/2003/ND-CP aiming to support lending to perform the tasks of science and technology by organisations and individuals (including agricultural cooperatives).

and technology for the socio-economic development of rural and mountain areas, those are supported with 100% funding: (iii) The ACs are the beneficiaries of agricultural expansion policies and fisheries policies in accordance with regulation on policies for agricultural extension and encouraging rural industrial development15.

In addition, to develop linkage and pursue the LSRF approach16, ACs are supported with up to 30% in the first year and 20% in the second year of the actual cost of pesticides, labour and machinery hire to perform collective crop protection services for members.

2.2.8 Policies supporting infrastructure investment and participating in target programme and socio–economic development programme

Policies to support investment and development of infrastructure for ACs in agriculture, forestry, fisheries and salt production include (Item a, Clause 1, Article 25, Decree 193) headquarters, drying yards, warehouses, primary processing factories, processing factories, electricity, water, markets, irrigation works, infrastructure, aquaculture areas, agricultural supplies stores, inland transportation for production, business for community members of ACs and FCs. The basis for such projects is approval by the competent authorities.

2.2.9 Several additional support policies for agricultural cooperatives

ACs facing difficulties caused by natural disasters and pest infestation are supported with capital and seeds (Paragraph 4, Article 25, Decree 193). This depends on the extent of damage, the danger of pests and the specific need presented by the actual situation that the ACs, FCs have operated in agriculture, forestry, fisheries and salt production, they would be received support policies, preferential for capital, seeds as provision mentioned17.

ACs are exempted from land-use fees or land lease when they construct drying factories, processing factories and warehouses to serve an LSRF project18.

In addition to preferential policies and types of support for each specific AC, there are a number of regulations as well as guidelines for provinces concerning investment in and development of ACs; these are issued by the government. The latest news is that the Government has issued Decision 445/2016, which requires the provinces of the Mekong Delta to establish a new type of AC model. Decision 593/2016 on the pilot regional linkage for a number of major agricultural products in the Mekong Delta makes mention of AC development.

2.3 Policies encouraging the development of farmer groups

Until now, Decree 151/2007/ ND-CP is the highest legislative framework addressing FGs. Decree 151 regulates issues including FG establishment, cooperation contracts and the content of the cooperation contracts, organisational structures, executive management, and the roles

(15) Decree No. 02/2010/ND-CP dated 8 January 2010 on agricultural extension; Decree No. 56/2005/ND-CP dated 26 April 2005 of the Government on agricultural extension, fishery extension; Decree No. 134/2004/ND-CP dated 9 June 2004 on encouraging the development of rural industries.(16) Clause c, Section 1, Article 5 of Decision No. 62/2013/QD-TTg dated 25 October 2013 of the Prime Minister on policy to encourage development cooperation, production-trade linkage and LSRF development.(17) Decision 142/2009/QD-TTg of the Prime Minister dated 31 December 2009 on mechanisms and policies to support planting seeds, livestock, aquaculture to restore production in areas damaged by natural disasters and pests; and Decision No. 49/2012/QD-TTg of the Prime Minister dated 8 November 2012 amending and supplementing Article 3 of Decision 142/2009/QD-TTg of the Prime Minister dated 31 December 2009 on mechanisms and policies to support planting seeds, livestock, aquaculture to restore production in areas damaged by natural disasters and pests;(18) Clause a, Section 1, Article 5 of Decision No. 62/2013/QD-TTg dated 25 October 2013 of the Prime Minister on policy to encourage development cooperation, production-trade linkage and LSRF development.

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

2726

and responsibilities of the head and members of FGs. Decree 151 only sets out the principles governing state support for FGs, without stipulating specific support policies. Support and preferences for FGs are set out in a number of other documents. In particular, state support policies for FGs are as follows:

2.3.1 Tax preference

Income tax: FGs are exempted from income tax on the performance of direct technical services to serve agriculture such as irrigation, drainage, ploughing and harrowing the soil, dredging canals, services for pest control, managing diseases of crops and livestock, rendering services for harvesting agricultural products (Paragraph 2, Article 4 Decree 218/2013).

Value-added tax: FGs are not subject to VAT for i) products of cultivation, livestock, aquaculture and fisheries fishing unprocessed or preliminary processing by FGs itself produced, catching sold out; ii) operation of irrigation and drainage, ploughing, infield canal dredging serving agricultural production, services for harvesting agricultural products; iii) credit services, medical services, veterinarians, health care for people and domestic animals (Article 5, 2008 law on value-added tax).

2.3.2 Credit preference

Under Decree 55/2015, credit institutions provide loans to FGs in the form of unsecured loans to 300 million. However, neither Decree 55/2015 nor Decision 62/2013 contain any regulations on preferential credit for FGs participating in linkage in LSRF establishment.

2.3.3 Additional types of support

Decree 151/2007 states that FGs receive support for participating in the design and implementation of plans, projects and programmes promoting the development of the collective economy, plans, projects and programmes of socio-economic development, job creation and the alleviation of poverty in the locality. Thus, FGs may receive other assistance depending on the specific projects and programmes as well as local capacity. This provision offers local flexibility in supporting farmer groups. Therefore, many localities have specific provisions on FG support. These involve training to improve capability, agricultural extension, brand name development, participation in trade fairs to introduce products, etc.

2.4 Provincial policies in support of the development of ACs/FGs and production-trade linkage associated with the LSRF approach

This section presents a number of specific policies of four provinces in support of ACs and FGs as well as supporting production-trade linkage and LSRF production.

2.4.1 Ca Mau province

Ca Mau province has planned 40,000 ha for LSRF rice production. Of this area, 60% is in Tran Van Thoi district and 40% in the Thoi Binh and U Minh districts and Ca Mau city. Among them, 29,510 ha of LSRF area produces high-quality rice with 2 crops/year; 10,040 ha produce both rice and shrimps, and 450 ha winter rice.

Implementing Decision 62/2013/QD-TTG, Ca Mau provincial people’s committee issued Decision No.30/2015/QD-UBND regulating the level of support for collaboration development and production-trade linkage associated with LSRF establishment in Ca Mau province. In particular:

• Support for farmers to take part in training and retraining courses, covering 50% of costs for enterprises and 100% for ACs;

• 50% support for the costs of organising training classes for AC officials;

• 30% support for the costs in the first year and 20% in the second year for the actual cost of pesticides, labour force and machine hire to perform general services for members involved in LSRF linkage;

• 30% support for seed costs for farmers in the first cropping year associated with LSRF establishment.

The total cost of supporting farmers is equivalent to about 1 million/ha. However, Ca Mau province does not regulate the support level for farmers for paddy storage during 3 months.

In addition, Ca Mau province has issued various documents to direct the development of collective economy (ACs, FGs) in the province. Currently, Ca Mau province only implements the LSRF policies (not its own policies) regulated by the central government. According to the provincial report about the results of policy implementation to support the development of economic cooperation in 3 years (2013, 2014, 2015):

• Loan capital comes mainly from the Cooperative Development Support Fund managed by the Cooperative Alliance. 32 ACs borrowed 4,860 million in 2013, 6 ACs borrowed 1,350 million in 2014 and 13 ACs borrowed 1,905 million in 2015.

• Training classes are organised to train the key staff of ACs and FGs. Funding for assisting with training content, retraining for business setup and production planning, services and negotiation skills to sign agreements amounted to 474.58 million for 1,605 people (in 2013, 2014 and 2015).

2.4.2 Bac Lieu province

Bac Lieu province, instead of promulgating a policy to implement Decision 62/2013/QD-TTg on production-trade linkage associated with LSRF establishment, promulgated Plan No. 38/KH-UBND dated 22 August 2013 on LSRF establishment model and guidance to apply a production handbook in accordance with VietGap direction of 2013-2014. This means that the provincial support policies only implement LSRF establishment and apply the VietGAP model, but do not require production-trade linkage.

Farmers participating in building the LSRF model and applying a production handbook in accordance with VietGAP direction receive:

• Investment in irrigation, irrigation infield (preferably from irrigation capital and programme 132);

• 100% of loan interest for borrowing to buy the machines for production;

• 50% of the cost of buying original seeds;

• 100% of the cost of buying row seeding tools, motorised sprayers, foliar fertilisers, microorganic fertilisers for seed treatment, microorganic pesticides for pest treatment, costs of technical training.

As part of provincial support for AC and FG development, the province has issued documents and plans to direct the development of collective economy in the period from 2016 to 2020. The

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

2928

province issued Decision No. 37/QD-UBND dated 5 August 2014 to regulate assistance with establishing new ACs and training as well as retraining to improve capacity for ACs.

2.4.3 Soc Trang province

In early 2012, Soc Trang Provincial People’s Council adopted Resolution No. 12 on a Development Scheme for specialty rice production until 2015. The province focuses on investment, on supporting the development of regional production of high-quality aromatic rice and making a brand name for rice of Soc Trang province. The province’s approach is to pursue LSRF establishment, with concentrated production areas linked to enterprises on the product demand side. ACs and FGs play an important role in organising production in LSRFs with high-quality products. To implement this strategy, the province supports the planning and production of quality seed, capacity-building training for staff of ACs, FGs and farmers, establishing agricultural extension, investing in improved irrigation and providing market information.

After Decision 62/2013/QD-TTg was issued, Soc Trang provincial people’s committee issued Plan No. 23/KH-UBND dated 17 March 2015 on the Development of LSRF in the period from 2014 to 2025. The Plan’s target is that LSRF area will reach 29,010 ha in 2025 and that 90% of the LSRF area and output will be subject to contracts for material supplies and product trade with enterprises. The minimum LSRF area for ACs and FGs is 300 ha. Measures promote production-trade linkage and the application of uniform technical process, and encourage the application of sustainable farming techniques (GAP, 1 must 5 reduction, …).

In addition to policies in support of implementation of LSRF and linkage, Soc Trang province has issued plans to support the development of ACs and FGs. Beyond the establishment of the cooperative development support fund with capital of 5 billion, the province does not have its own policies supporting ACs and FGs.

One of the specific features in Soc Trang’s policy is to support the LSRF concept and encourage linkage in production-trade. 90% of LSRF area is involved in production-trade linkage till 2025. The projects producing under LSRF without linkage in production-trade are also supported by the province. The approach is positive because the organisation of production under LSRF can help to cut production costs and ensure more even product quality. It positively facilitates AC and FG development and delivers benefits for production-trade linkage.

2.4.4 An Giang province

An Giang province has implemented the LSRF model in such a manner that the minimum area is 50 ha between 2015 and 2017 and 300 ha until 202019. In addition, An Giang province issued Decision No. 12/2016/QD-UBND dated 2 March 2016 on assistance in development cooperation and production-trade linkage associated with LSRF to support ACs and FGs, enterprises and farmers involved in the linkage.

Support for ACs and FGs: One of the specific features of An Giang is that the province supports both FGs involved in production-trade linkage and those involved in LSRF establishment. ACs and FGs receive the following forms of support: i) Funding to organise training and technical guidance for crop farmers producing under contracts, including all costs of materials, food and accommodation, travel, trainer hire, etc. ii) Pesticides, labour, machine hire to apply common pesticides for members. The maximum support does not exceed 3,250,000 VND/ha in the first

(19) Decision No. 1966/QD-UBND dated 21 September 2015 An Giang provincial people’s committee.

year and 2,160,000 VND/ha in the second year. iii) One-off funding to organise training courses for cooperative staff on management, economic contracts and production techniques, including all costs of materials, food, accommodation and tuition.

Support for farmers: i) One-off support up to 30% of the cost to buy certified seeds for the first crop implementing the LSRF concept; ii) support for 100% of funding to build warehouses at enterprises in cases in which the Government implements the policy for temporary storage of agricultural products.

Support for enterprises: Support for funding to organise training and technical guidance for crop farmers producing under contracts, including all costs of food, accommodation, travel, materials, trainer hire and stationery.

In addition, An Giang province has set up a Cooperative Development Assistance Fund. The Fund supports 70% of credit with an interest rate of 0% for the cooperative project. The province also issued action plans implementing the scheme on “Pilot completion and replication of the model of new style agricultural cooperatives in Mekong Delta An Giang in the period 2016-2020”.

3. The Current Situation of Production–Trade Linkages Associated with Large Scale Rice Fields

3.1 Implementation in recent years in the 4 provinces surveyed

Following Decision 62/2013, the Mekong Delta in general and the four provinces surveyed in particular are implementing the LSRF approach. However, there are differences in the degree of implementation in each province. Among the four provinces surveyed, An Giang and Soc Trang provinces host the largest LSRF area.

Table 3.1: Rice sowing area in LSRF in 4 provinces surveyed (ha)

Year Ca Mau Bac Lieu Soc Trang An Giang

2011 1525 13150

2012 834 4862 22950

2013 726 11591 34000

2014 12168 17996 32781

2015 8567 6164 23723 40615

LSRF area / total rice sowing area ratio in 2015 (%) 6.6 3.4 16.0 6.5

Source: Synthesis from DARD reports, 2016

There is a few area both rice area of the LSRF and rice area of the LSRF associating with linkage in production-trade, even rice area of the LSRF associating with linkage in production-trade is fewer. The survey findings in four provinces show that very few enterprises are involved in linkage with traders.

From September 2012 to March 2015, Ca Mau province has implemented the LSRF model on 8,567 ha (compared to the overall rice planting area in the province, which is 129,766 ha, the LSRF area is very small). 7,390 households are involved in the model in 39 villages in 18 communes in U Minh, Tran Van Thoi, Cai Nuoc districts and Ca Mau city. Each LSRF project received 1-2 varieties of rice seed from provincial assistance. Rice varieties include OM 6976,

STUDY REPORT / INTEGRATED COASTAL MANAGEMENT PROGRAMME

3130

OM 6162, OM 4218, OM 5451, OM 8017 and ST 20. Rice seed certification is assisted, with over 80% being certifiied. Local people bought in 70% of rice seeds, the other 30% coming from their own planting or from exchange with other households. In recent years, only two enterprises participated in buying LSRF-produced rice. These are Ca Mau agricultural products & Foodstuff Import – Export JSC which has purchased about 10,000 tons, and Can Tho GFC Co. Ltd, which has purchased about 300 tons of ST20 rice.

3.2 AC and FG implementation of the LSRF approach

Among the total surveyed, 43% of ACs implement the LSRF approach with an average area of 165 ha. The An Giang ACs implementing LSRF manage smaller areas (112 ha) than the Ca Mau ACs (330 ha). Many Ca Mau ACs implementing LSRF manage not only the area of the ACs’ members, but also that of households not involved in ACs.

Table 3.2: Percentage of ACs and FGs implementing the LSRF approach

Province% of ACs

implementing LSRF

Average area of LSRF per AC

(ha)

% of FGs implementing

LSRF

Average area of LSRF per FG

(ha)