The MetroIBA Education Committee welcomes you to the webinar: Understanding How Banks Lenders Look...

18

The MetroIBA Education Committee welcomes you to the webinar: Understanding How Banks Lenders Look at Your Small Business Presented by Roger Hamilton, BankCherokee August 18, 2015 9 – 10am CST

-

Upload

berniece-mccarthy -

Category

Documents

-

view

214 -

download

0

Transcript of The MetroIBA Education Committee welcomes you to the webinar: Understanding How Banks Lenders Look...

The MetroIBA Education Committee welcomes you to the webinar:

Understanding How Banks Lenders Look at Your Small Business

Presented by Roger Hamilton, BankCherokee

August 18, 2015 9 – 10am CST

Understanding How Bank Lenders Look at Your Small Business

Presented by Roger Hamilton,Commercial Lender/Sr. Vice President

Understanding How Bank Lenders Look at Your Small Business

Types of Business Loans Loan Application & Financial Reporting The Five C’s of Credit Assessment of Capital Assessment of Capacity Role of Financial Covenants Examples Summary & Questions

Types of Business Loans:

Line of Credit Importance of Principal Payments/Clean-up

Equipment Loans Down payment is typically modest

Real Estate Loans Down payment ranges from 5-25%

SBA Loan Programs 7a Guaranty, Capline & 504 program

Importance of Personal Recourse

Owner-occupied Commercial Real Estate Loan Options

20% Down 10% Down 3.3% DownConventional SBA 504 SBA 504 with

Uses of cash: Loan Loan Non-profitPurchase property 480,000 480,000 480,000Improvements to property 120,000 120,000 120,000Closing costs 12,000 12,000 12,000 Total Uses 612,000 612,000 612,000Sources of cash: BankCherokee 1st mortgage 480,000 300,000 300,000SBA 504 2nd mortgage 240,000 240,000MCCD 3rd mortgage 40,000Owner's equity contribution 132,000 72,000 32,000 Total Sources 612,000 612,000 612,000

The "as-completed" appraisal came back at $600,000 or $50 per SFon a 12,000 SF building, as compared to project costs of $600,000.

Loan Application & Financial Reporting

FYE Statements for past 3 years (Tax Returns) Interim Financial with prior year comparison Account Receivable & Account Payable

. Aging Reports Debt Schedule Projections (fast growing or turnaround company) Personal Financial Statement Personal Tax Returns for past 2 years

The 5 C’s of Credit

Capacity: Ability to Repay Loan from Cash

Flow

Capital: Assessment of Tangible Net Worth

Collateral: Assets to Secure the Loan

Character: Integrity / Personal Credit Score

Conditions: Industry Specific and Economy

Assessment of Capital

Tangible Net Worth Calculation Total Shareholders Equity Less: Notes due from Officers, Shareholders or Affiliates

Goodwill or other Similar Intangible AssetsPlus:Subordinated debt

= Tangible Net Worth

Leverage Ratio Total Liabilities less Subordinated Debt

Tangible Net Worth

Cash Flow Calculation Net Income

Less: DistributionsPlus: Depreciation & Amortization Expenses

Interest Expenses= Traditional Cash Flow

Debt Service Coverage Ratio (DSCR) Traditional Cash Flow Interest Expenses Plus CMLTD (prior period)

or Scheduled Principal & Interest Payments

Assessment of Capacity

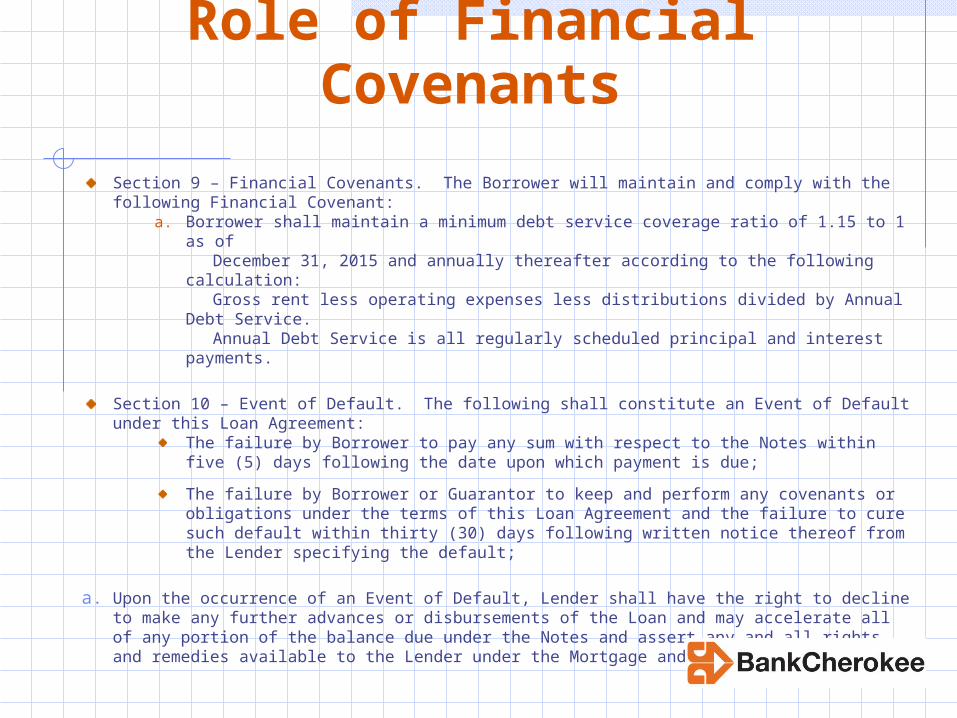

Role of Financial Covenants

Section 9 – Financial Covenants. The Borrower will maintain and comply with the following Financial Covenant:

a. Borrower shall maintain a minimum debt service coverage ratio of 1.15 to 1 as of

December 31, 2015 and annually thereafter according to the following calculation:

Gross rent less operating expenses less distributions divided by Annual Debt Service.

Annual Debt Service is all regularly scheduled principal and interest payments.

Section 10 – Event of Default. The following shall constitute an Event of Default under this Loan Agreement:

The failure by Borrower to pay any sum with respect to the Notes within five (5) days following the date upon which payment is due;

The failure by Borrower or Guarantor to keep and perform any covenants or obligations under the terms of this Loan Agreement and the failure to cure such default within thirty (30) days following written notice thereof from the Lender specifying the default;

a. Upon the occurrence of an Event of Default, Lender shall have the right to decline to make any further advances or disbursements of the Loan and may accelerate all of any portion of the balance due under the Notes and assert any and all rights and remedies available to the Lender under the Mortgage and Security Agreement.

Maximum Capital Expenditures

Minimum Clean-up Days on Credit

Line

Minimum Capital Levels

Other Financial Covenants:

May not provide match of FY taxable income

to the FY tax distribution

Ignores source & uses of cash flow from the balance sheet (operating company)

Ignores reclassified distributions

Bank’s loans will get repaid from future cash flow NOT past cash flow

Limitations of Traditional Cash flow

Manufacturing Company DSCR based on definition 12/31/10 12/31/11 12/31/12 12/31/13 12/31/14 12/31/15Net Income 259 205 125 143 442 400Distributions 0 -202 -141 -91 -131 -354Depreciation 45 62 47 222 28 28Interest 91 88 89 84 81 80 Cash Flow 395 153 120 358 420 154Debt Service 1st mortgage 59 59 59 59 59 59Debt Service 2nd mortgage 47 47 47 47 47 47Interest-Bank credit line 21 23 28 24 18 18Debt Service equipment loan 30 33 Total Debt Service 127 129 134 130 154 157 DSCR 3.11 1.19 0.90 2.75 2.73 0.98

Manufacturing Company DSCR based on matching taxable income to the related tax distribution

12/31/10 12/31/11 12/31/12 12/31/13 12/31/14 12/31/15Net Income 259 205 125 143 442 400Distributions -202 -141 -91 -131 -354 -320Depreciation 45 62 47 222 28 28Interest 91 88 89 84 81 80 Cash Flow 193 214 170 318 197 188Debt Service 1st mortgage 59 59 59 59 59 59Debt Service 2nd mortgage 47 47 47 47 47 47Interest-Bank credit line 21 23 28 24 18 18Debt Service equipment loan 30 33 Total Debt Service 127 129 134 130 154 157 DSCR 1.52 1.66 1.27 2.45 1.28 1.20

Retail Company Capital Analysis

2010 2011 2012 2013 2014

Total Stockholder's Equity 324 339 445 412 521

Less:

Due from Shareholder -105 -78 -74 -132 -215

Due from Affiliate 0 0 0 0 59

Plus:

Subordinated Debt 0 0 0 0 0

Tangible Net Worth 219 261 371 280 247

Total Liabilities 758 907 1,265 1,968 2,024

Leverage Ratio 3.5x 3.5x 3.4x 7.0x 8.2x

Retail Company Capacity Analysis (using traditional cash flow) 2011 2012 2013 2014Net Income 120 185 17 114 Less: Distributions (33) (100) (73) (4)Plus: Depreciation Expense 151 57 78 118 Interest Expense 19 24 90 78 Traditional Cash Flow 257 166 112 306 Credit Line Interest 6 8 16 16 Installment Loans 13 36 78 117 Total Debt Service 19 44 94 133

Debt Service Coverage Ratio (DSCR) 13.5x 3.8x 1.2x 2.3x

Retail Company Capacity Analysis (using modified traditional cash flow) 2011 2012 2013 2014Net Income 120 185 17 114 Less: Distributions (33) (100) (73) (4)Reclassified Distributions 0 0 (58) (83)Due from Affiliate 0 0 0 (59)Plus: Depreciation Expense 151 57 78 118 Interest Expense 19 24 90 78 Modified Traditional Cash Flow Credit Line Interest 6 8 16 16 Installment Loans 13 36 78 117 Total Debt Service 19 44 94 133 DSCR 13.5x 3.8x 0.6x 1.23x

Summary & QuestionsContact Information:

Roger Hamilton Commercial Lender/Sr. Vice President

email: [email protected]

Phone: 651.291.6263

BankLocal. BankCherokee.

Recommended reading: Forbes ArticleHow's Your Flow? Cash Flow Not Profit As Predictor Of Entrepreneurial Success

http://onforb.es/1LeJvt2

Thank you for attending today’s webinar!

We hope to see you at these upcoming events:

• Member’s-Only - Business Owner’s Roundtable Thurs Aug 27, 7:30-9:00am

• 1st Tuesday Networking Events 4:30 – 6:30pm, Sept 1st @ The Wedge Table

• Public Policy Caucus – Member Only – Sept 29th, 6 – 8:15pm• Free Webinar Oct 20th, Start Thinking About What’s Next For You –

NOW!• Visit www.buylocaltwincities.com/events for more information

Not a MetroIBA member? Visit www.buylocaltwincities.com/join to learn more about the benefits of being a member and to join online today!