Recent Economic Developments in Latvia and Medium-term Outlook

Macquarie ResearchCommodities

The medium-term nickel market outlook

May 2015

Macquarie Commodities Research

Macquarie Capital (Europe) Limited

Ropemaker Place28 Ropemaker St

London, UK EC2Y 9HD

Jim Lennon – Consultant to Macquarie+44 7768 766 729

In preparing this research, we did not take into account the investment objectives, financial situation and particular needs of the reader. Before making an

investment decision on the basis of this research, the reader needs to consider, with or without the assistance of an adviser, whether the advice is appropriate

in light of their particular investment needs, objectives and financial circumstances. Please see disclaimer.

Page 2

The nickel outlook: take-off delayedFrom being the best-performing base metal in the previous decade,

nickel has been one of the worst performing this decade

Nickel went from best to worst almost entirely due to massive growth in

Chinese nickel pig iron production, fuelled by imports of nickel ore from

Indonesia and (to a lesser extent) the Philippines

Prices rallied prematurely in 2014 following the announcement of a ban

on Indonesian ore exports from January 2014 and have subsequently

retreated to pre-ban lows

The recovery in prices has been delayed by an overhang of Indonesian

ore stocks and higher ore exports from the Philippines

By end-2015, however, we think nickel will move into a structural deficit

pushing prices higher out to 2020 – there are not enough large-scale

projects to meet expected demand growth

Page 3

Growth in nickel pig iron production (fuelled

mainly by Indonesian ore) “killed” nickel market

000t nickel 2006-14

2006 2014 Change

Supply

Production - ex NPI 1324 1518 194

NPI 0 483 483

Total 1324 2001 677

Demand

Ex-China consumption 1149 937 -212

China consumption 287 952 665

Total 1437 1890 453

Source: INSG, Macquarie Research, May 2015

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2006 2007 2008 2009 2010 2011 2012 2013 2014

'000

t N

i

World nickel supply and demand since 2006

World production ex-NPI NPI production

World consumption

Page 4

Large over-supply in recent years...

Source: INSG, Macquarie Research, May 2015

48

10

-26

4

32

-111

-40

121

90

-36

35

121

173

102

4

6

8

10

12

14

16

18

20

22

-150

-100

-50

0

50

100

150

200

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

LM

E/p

rdu

ce

rs s

toc

ks

in

we

ek

's u

se

'000t supply/demand balance

Nickel supply/demand balance and stocks to 2014

Balance (LHS) Stocks in weeks of use (RHS)

Page 5

The bigger, longer term picture: stock

overhang is very high

Source: LME, Macquarie Research, May 2015

0

2

4

6

8

10

12

0

10000

20000

30000

40000

50000

60000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

LME

sto

cks:

we

eks

' co

nsu

mp

tio

n

$/to

nn

e c

on

stan

t 20

15$

LME stocks and prices since 1980Prices in constant $2015 and stocks as weeks's use

LME price LME stocks in week's demand

Page 6

Total nickel stocks: highest of any of the main

base metals...but falling overall

19.5

22.1

9.8

7.08.3

5.6

0

5

10

15

20

25

30

0

5

10

15

20

25

30

Al Ni Zn Cu Sn Pb

Estimated total stocks for base metals End-April 2014(weeks of annual consumption)

Exchange Other Raw Materials

26.1 26.4

10.9

6.3 7.15.6

0

5

10

15

20

25

30

0

5

10

15

20

25

30

Al Ni Zn Cu Sn Pb

Estimated total stocks for base metals End-Dec 2013(weeks of annual consumption)

Exchange Other Raw Materials

Source: INSG, ICSG, ILZSG, IAI, LME, SHFE, CRU, Comex, Macquarie Research, May 2015

Page 7

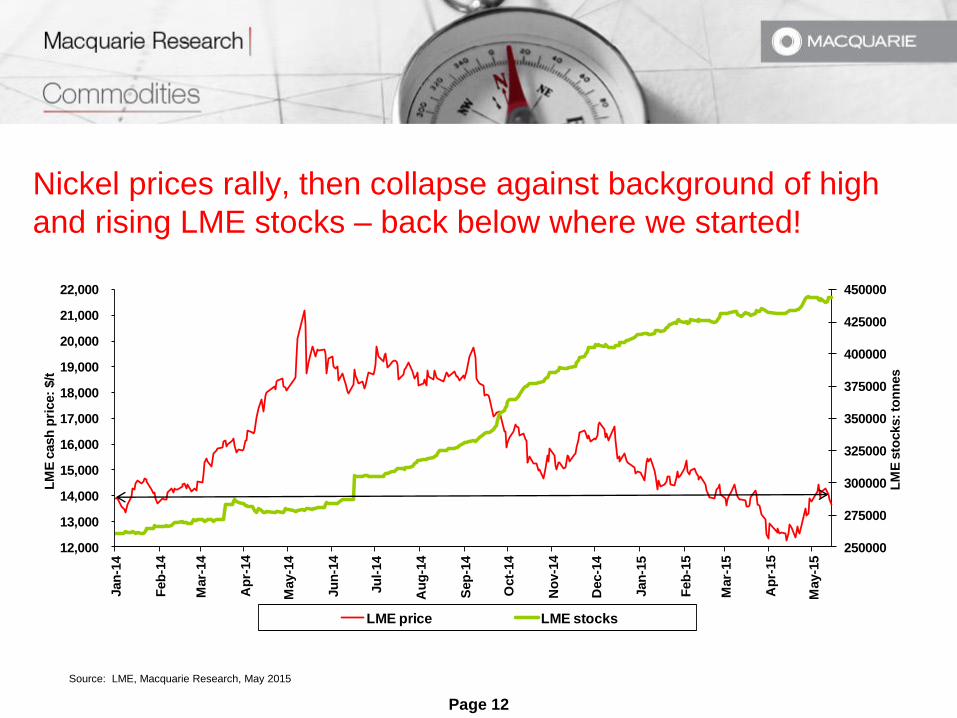

The year in retrospect...Following Indonesian ore ban from January 14, 2014, fund buying sent

LME nickel prices and nickel ore prices sharply higher, driven mainly by

fund speculative buying

Rise was premature due to large stockpiles of Indonesian nickel ore built

in China in 2013 and large non-LME stocks (mainly in China)

Higher nickel prices led to a strong restocking cycle in stainless steel

(global production up 16% YoY in Q2 2014)

Philippines ore exports surge from April 2014 and LME stock rises

accelerate from May (Qingdao financing scandal)

Funds took profits and nickel prices started to fall sharply

Stainless steel demand fell sharply in Q4 2014/Q1 2015, leading to mini-

collapse in demand.

Page 8

What we got wrong in 2014

Main deviation from our forecast a year ago was that Chinese nickel pig

iron production was 100kt higher than we were projecting for 2014 at

480kt vs. our expectation of 380kt

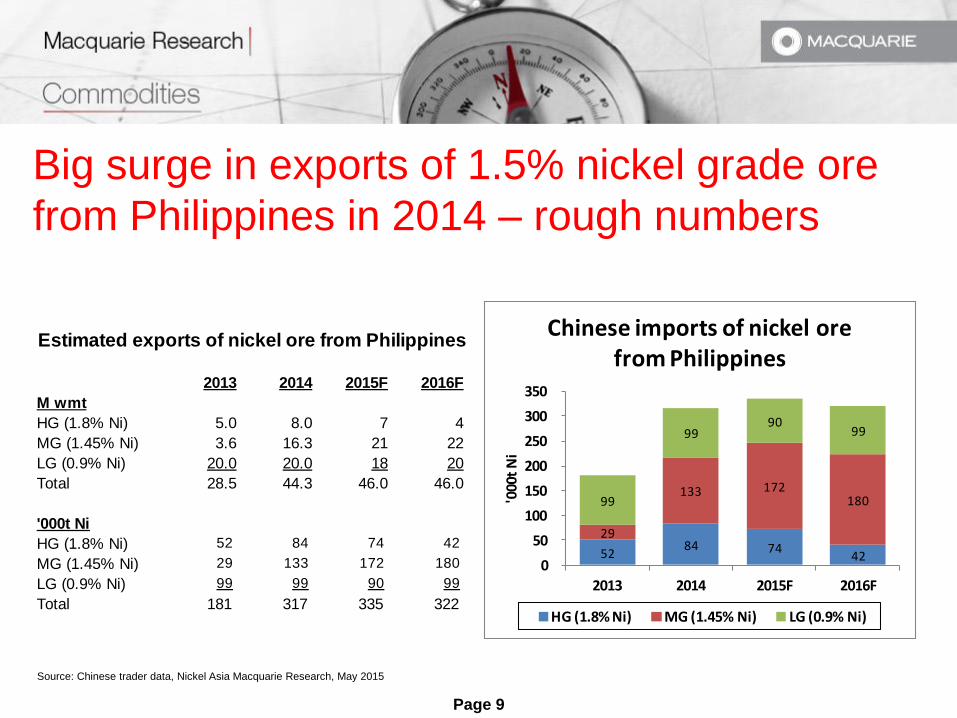

This difference was due to ore use from the Philippines growing much

more rapidly than we expected.

Demand was almost exactly what we expected but H1 2014 was higher

and H2 2014 was lower than projected.

Page 9

Big surge in exports of 1.5% nickel grade ore

from Philippines in 2014 – rough numbers

Source: Chinese trader data, Nickel Asia Macquarie Research, May 2015

Estimated exports of nickel ore from Philippines

2013 2014 2015F 2016F

M wmt

HG (1.8% Ni) 5.0 8.0 7 4

MG (1.45% Ni) 3.6 16.3 21 22

LG (0.9% Ni) 20.0 20.0 18 20

Total 28.5 44.3 46.0 46.0

'000t Ni

HG (1.8% Ni) 52 84 74 42

MG (1.45% Ni) 29 133 172 180

LG (0.9% Ni) 99 99 90 99

Total 181 317 335 322

52 84 74

42

29

133 172 180 99

99 90

99

0

50

100

150

200

250

300

350

2013 2014 2015F 2016F

'000

t N

i

Chinese imports of nickel ore from Philippines

HG (1.8% Ni) MG (1.45% Ni) LG (0.9% Ni)

Page 10

Chinese NPI production held up in 2014 based on

Indonesian ore destocking and more Pilipino ore

Source: INGS, Umetal, Chinese Customs, Macquarie Research, May 2015

40 70 80

20

120

154

59

80

95

16

-

-365

210 50

500 480

385

--

6

-

50

100

150

200

250

300

350

400

450

500

2013 2014 2015f

'000t N

i

Estimated Chinese nickel pig iron production by ore source

Philippines HG Philippines MG Philippines LG

Indonesian LG Indonesian HG Sulphide concs

0

100

200

300

400

500

600

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

'000t

ni an

nu

ali

sed

Estimated monthly Chinese nickel pig iron production

Page 11

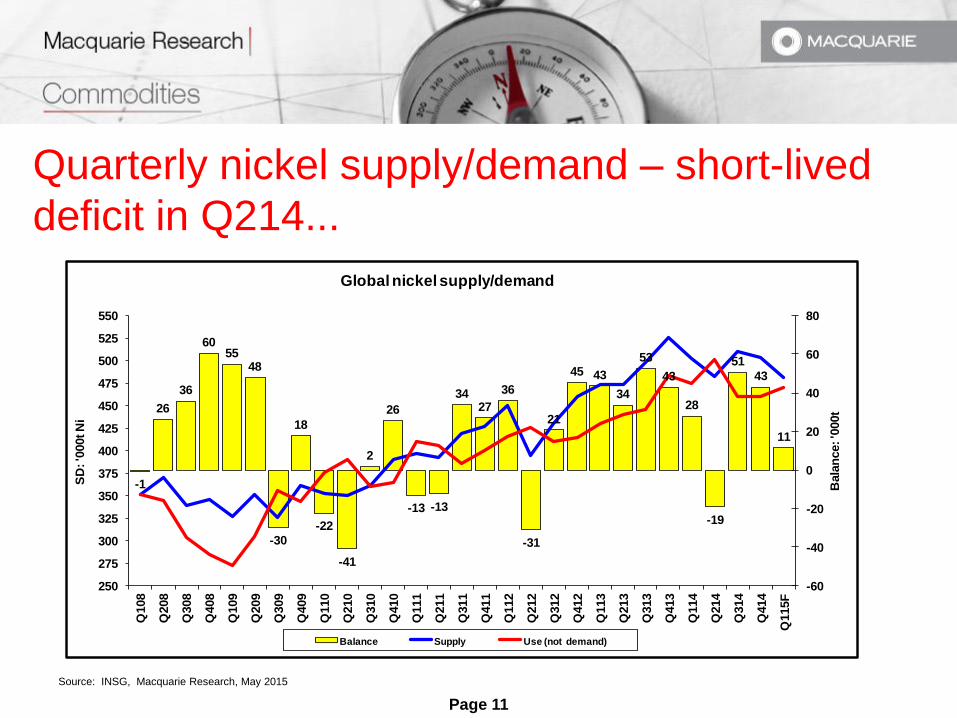

Quarterly nickel supply/demand – short-lived

deficit in Q214...

Source: INSG, Macquarie Research, May 2015

-1

26

36

6055

48

-30

18

-22

-41

2

26

-13 -13

3427

36

-31

21

45 43

34

53

43

28

-19

51

43

11

-60

-40

-20

0

20

40

60

80

250

275

300

325

350

375

400

425

450

475

500

525

550

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Q115F

Bala

nce: '0

00t

SD

: '0

00t N

i

Global nickel supply/demand

Balance Supply Use (not demand)

Page 12

Nickel prices rally, then collapse against background of high

and rising LME stocks – back below where we started!

Source: LME, Macquarie Research, May 2015

250000

275000

300000

325000

350000

375000

400000

425000

450000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

22,000

Jan

-14

Feb

-14

Mar-

14

Ap

r-14

May-1

4

Ju

n-1

4

Ju

l-14

Au

g-1

4

Sep

-14

Oct-

14

No

v-1

4

Dec-1

4

Jan

-15

Feb

-15

Mar-

15

Ap

r-15

May-1

5

LM

E s

tocks: to

nn

es

LM

E c

ash

pri

ce:

$/t

LME price LME stocks

Page 13

Currency has been another factor suppressing

prices in US dollar terms

80

100

120

140

160

180

200

Jan 2014

Feb 2014

Mar 2014

Apr 2014

May 2014

Jun 2014

Jul 2014

Aug 2014

Sep 2014

Oct 2014

Nov 2014

Dec 2014

Jan 2015

Feb 2015

Mar 2015

Apr 2015

May 2015

Ind

ec

Jan

20

14

=1

00

Index of LME nickel prices in different currencies(monthly averages)

Russia

Brazil

Euro

Japan

Aust.

Canada

China

USA

Source: LME, Bloomberg, Macquarie Research, May 2015

Page 14

Weaker energy prices have lowered operating

costs for miners and smelters

Brent crude price$/barrel

Source: Bloomberg, Mysteel, Macquarie Research, May 2015

Chinese coke and coking coal prices$/tonne

0

20

40

60

80

100

120

140

160

2006 2008 2010 2012 2014

Between 10-30% of mining

costs are oil-linked

100

120

140

160

180

200

220

240

260

280

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

$/t

on

ne

ex-

VA

T

Coke Coking coal

Page 15

Role of funds- fund long liquidation since

November 2014 and recently short covering

Source: LME, Macquarie Research, May 2015

12000

13000

14000

15000

16000

17000

18000

19000

20000

21000

22000

800000

900000

1000000

1100000

1200000

1300000

1400000

1500000

1600000

1700000

1800000

1900000

2000000

2100000

Ja

n-1

4

Fe

b-1

4

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Ju

n-1

4

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oc

t-1

4

No

v-1

4

De

c-1

4

Ja

n-1

5

Fe

b-1

5

Ma

r-1

5

Ap

r-1

5

Ma

y-1

5

Pri

ce:

$/t

on

ne

LM

E fu

ture

op

en

in

tere

st:

to

nn

es

LME futures open interest and price

Open interest LME price

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

LME

3M

pri

ce:

$/t

on

ne

Lots

: ne

t lo

ngs

Money manager net longs and nickel price

Money manager net longs LME 3-month price

Page 16

Why the Indonesian ban has yet to have a

significant impact on nickel prices

The Chinese built enormous stockpiles of Indonesian ore ahead of the

ban

The Philippines (and Guatemala to a lesser extent) has partly stepped in

as a replacement to Indonesian ore

China had enormous unreported stocks of primary nickel which it

destocked during 2014 and early 2015

The stainless steel market crashed at the end of 2014/early 2015

Page 17

In China destocking of primary nickel and nickel ore was

steady in 2014 – now nearing an end?

Source: INGS, Umetal, Chinese Customs, Macquarie Research, May 2015

12

38

1

8

1

-2

1

-3

4

-6

5

1511

73

-3

-11

-3-9

6 3

-6

1419

5

-6

2

-18

-27

-8

-23

-15-13-14-20

-2 -4 -5

-40

-20

0

20

40

60

80

100

Jan

-12

Feb

-12

Mar-

12

Ap

r-12

May-1

2Ju

n-1

2Ju

l-12

Au

g-1

2S

ep

-12

Oct-

12

No

v-1

2D

ec-1

2Jan

-13

Feb

-13

Mar-

13

Ap

r-13

May-1

3Ju

n-1

3Ju

l-13

Au

g-1

3S

ep

-13

Oct-

13

No

v-1

3D

ec-1

3Jan

-14

Feb

-14

Mar-

14

Ap

r-14

May-1

4Ju

n-1

4Ju

l-14

Au

g-1

4S

ep

-14

Oct-

14

No

v-1

4D

ec-1

4Jan

-15

Feb

-15

Mar-

15

'00

0t n

i

Chinese nickel market moved into big destocking since May 2014

Apparent stock change Apparent demand

Estimated usage (based on INSG)

0

5

10

15

20

25

30

Jan 14 Feb 14 Apr 14 Jun 14 Aug 14 Oct 14 Dec 14 Jan 15 Mar 15

Mt

Chinese nickel ore port stocks by origin

Indonesian ore Filipino ore

Page 18

Chinese price discount to LME narrowing

suggesting less exports and more imports

Source: Chinese Customs, LME, SMM, Macquarie Research, May 2015

5 5

13

-4

4

21

12 11

3027

19

10 10

6

2

11

1 2

68

6

17 17 17

9 8 85 4

2 2

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Jan

-14

Feb

-14

Mar

-14

Ap

r-14

May

-14

Jun

-14

Jul-

14

Au

g-14

Sep

-14

Oct

-14

No

v-14

De

c-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-15

'000

t N

i

LME stock changes and Chinese metal exports

LME stock change China nickel exports

-533 -833

-2,035

-1,140

-486 -777 -993

-538

-504

-470 -707

-401

93

127

509

517

-463

-336

-1,606

-1,590

130 77

-1,122

-630

-497

-442

-1,815

-416

6

85

366

563

-2500

-2000

-1500

-1000

-500

0

500

1000

Jan-14

Feb

-14

Mar-14

Ap

r-14

May-14

Jun

-14

Jul-14

Au

g-14

Sep

-14

Oct-14

No

v-14

De

c-14

Jan-15

Feb

-15

Mar-15

Ap

r-15

$/to

nn

e N

i

Chinese nickel prices minus LME price

Jinchuan metal minus LME price 10% NPI minus LME price

Page 19

Stainless dominates nickel use and growth

40%

45%

50%

55%

60%

65%

70%

75%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014F

% o

f to

tal p

rim

ary

Stainless share in primary nickel use

Stainless70%

Non-ferrous10%

Plating7%

Alloy steel5%

Castings3%

Others5%

2013 world nickel use by application

Source: INSG, Macquarie Research, May 2015

Page 20

Q414/Q115 falls in stainless production in

Europe, Korea, Taiwan and Japan

Source: INSG, ISSF, Tex, AISI, CRU Macquarie Research, May 2015

2014 2014 2014 2014 2015

'000t Q1 Q2 Q3 Q4 Q1E

USA 557 607 604 621 659

Japan 838 842 861 790 812

Europe 2059 2024 1610 1537 1915

Korea 529 510 507 492 505

Taiwan 257 310 277 259 258

India 725 739 750 760 792

China 5031 5601 5515 5575 5095

Other 1032 1019 1009 1027 1074

Total 10302 10914 10383 10302 10318

Total Ex-China 5271 5313 4868 4726 5222

Chinese net exports 702 1,059 962 841 734

% change yoy

USA 13.5% 24.9% 14.3% 18.3% 18.3%

Japan 9.5% 6.4% 7.1% -3.0% -3.1%

Europe 0.3% 9.2% 7.3% -13.1% -7.0%

Korea 3.5% -1.3% -6.7% -13.9% -4.5%

Taiwan -7.8% 24.9% 8.4% -13.3% 0.5%

India 12.5% 12.5% 9.1% 9.8% 9.2%

China 12.1% 23.3% 8.4% 4.3% 1.3%

Other 9.5% 5.8% 6.0% 6.4% 4.1%

Total 8.1% 16.1% 7.3% 0.1% 0.2%

Total Ex-China 4.6% 9.3% 6.2% -4.4% -0.9%

Chinese net exports 40.9% 70.8% 76.5% 43.2% 4.6%

7.2% 7.7%

11.4%

13.9%

8.1%

16.1%

7.3%

0.1% 0.2%

-2.5% -3.0%

-0.7%

6.8%

4.6%

9.3%

6.2%

-4.4%

-0.9%

13000

14000

15000

16000

17000

18000

19000

-10%

-5%

0%

5%

10%

15%

20%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1E

2013 2013 2013 2013 2014 2014 2014 2014 2015

Ni:

$/

ton

ne

% c

ha

ng

e Y

oY

World World Ex-China LME Ni price

Page 21

China has dominated world stainless steel

production growth over the past 10 years

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

1950

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2010

2014

'000

t st

ain

less

World stainless steel; melt production

Ex-China China

'000t SS 2006-14

2006 2014 Change

SS production

China 4881 21722 16841

Ex-China 23177 20178 -2998

Total 28057 41901 13843

Share of total

China 17% 52%

Ex-China 83% 48%

Source: INSG, ISSF, Tex, AISI, CRU Macquarie Research, May 2015

Page 22

Why did stainless output fall so much ex-China?

Since 2006 China has gone from a

net importer of 2.5mt to a net exporter

of 3mt – a 5.5mt swing

Massive rise in Chinese exports in

2013 and 2014 (net exports rose 46%

and 58% YoY respectively). China’s

net exports rose from 7% of non-

Chinese demand in 2012 to 10% in

2013 and 15% in 2014.

Note that Europe (ex-Turkey)

accounted for 15% of 2014 exports –

in March EU applied large anti-

dumping duties against China and

Taiwan

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

-4000

-3500

-3000

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

2000

2500

3000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

% o

f n

on

-Ch

inese d

em

an

d

'000t S

S p

rod

ucts

Chinese net exports of stainless steel products

Chinese net imports China % of non-Chinese use

Source: Chinese Customs, WBMS, Macquarie Research, May 2015

Page 23

Chinese net exports of stainless to Europe

plunge in Q1 2015

399,413

495,777437,221

472,350

573,498

861,194

775,854

669,366

590,890

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115

ton

ne

s SS

pro

du

cts

Chinese net exports of stainless steel - total

28,947

56,79150,694

71,987

107,447

151,762153,090

102,038

59,826

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115

ton

ne

s SS

pro

du

cts

Chinese net exports of stainless steel - Europe

25,062 25,134 25,091 24,59629,951

42,829

62,936

69,22565,775

0

10000

20000

30000

40000

50000

60000

70000

80000

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115

ton

ne

s SS

pro

du

cts

Chinese net exports of stainless steel - North America

318,662

381,645

323,460337,273

397,097

615,849

509,989

447,116419,332

0

100000

200000

300000

400000

500000

600000

700000

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115

ton

ne

s SS

pro

du

cts

Chinese net exports of stainless steel - Asia

6,353

7,908

10,43911,48811,177

12,509

14,923

12,340

14,956

0

2000

4000

6000

8000

10000

12000

14000

16000

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115

ton

ne

s SS

pro

du

cts

Chinese net exports of stainless steel - Africa

9,28010,428

13,51112,914

15,456

20,633

16,67518,303

14,703

0

5000

10000

15000

20000

25000

Q113 Q213 Q313 Q413 Q114 Q214 Q314 Q414 Q115to

nn

es

SS p

rod

uct

s

Chinese net exports of stainless steel - Middle East

Source: Chinese Customs, WBMS, Macquarie Research, May 2015

Page 24

Pointers to a mid-15 recovery in nickel prices

Post Chinese New Year bounce in Chinese demand.

Chinese primary destocking near an end – LME stocks should start

falling by mid-2015?

Ex-Chinese stainless destocking to end by Q2 2015?

Chinese government stimulus now underway should steady Chinese

growth decline and lead to modest H2 recovery

Chinese port stocks of high-grade ore to be depleted during April-June

period – could trigger rally in ore prices

Fund short-covering

Page 25

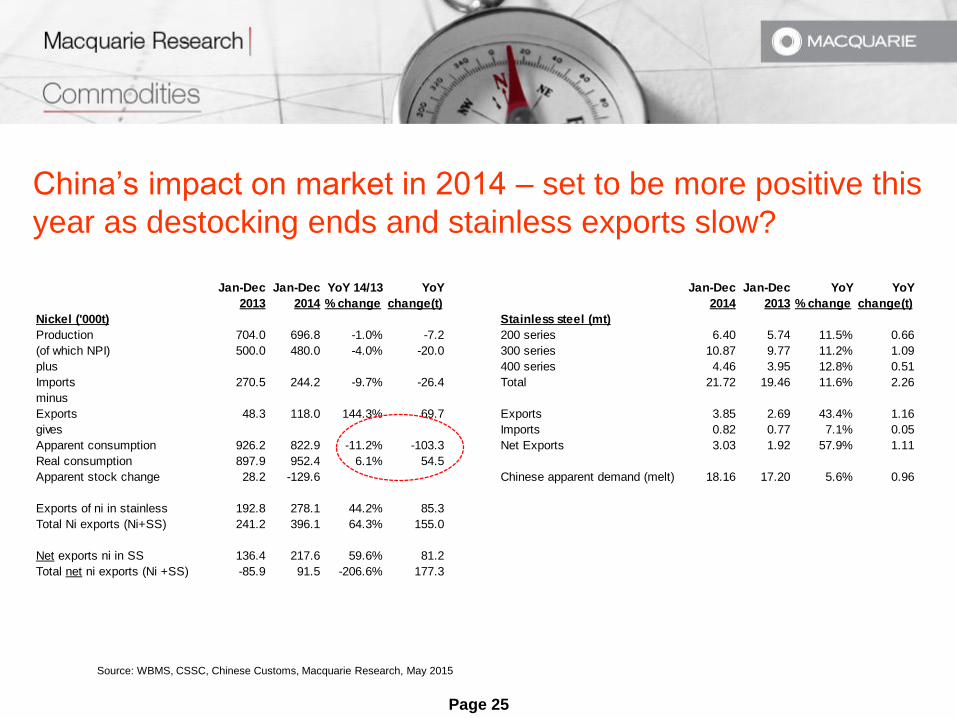

China’s impact on market in 2014 – set to be more positive this

year as destocking ends and stainless exports slow?

Source: WBMS, CSSC, Chinese Customs, Macquarie Research, May 2015

Jan-Dec Jan-Dec YoY 14/13 YoY Jan-Dec Jan-Dec YoY YoY

2013 2014 % change change(t) 2014 2013 % change change(t)

Nickel ('000t) Stainless steel (mt)

Production 704.0 696.8 -1.0% -7.2 200 series 6.40 5.74 11.5% 0.66

(of which NPI) 500.0 480.0 -4.0% -20.0 300 series 10.87 9.77 11.2% 1.09

plus 400 series 4.46 3.95 12.8% 0.51

Imports 270.5 244.2 -9.7% -26.4 Total 21.72 19.46 11.6% 2.26

minus

Exports 48.3 118.0 144.3% 69.7 Exports 3.85 2.69 43.4% 1.16

gives Imports 0.82 0.77 7.1% 0.05

Apparent consumption 926.2 822.9 -11.2% -103.3 Net Exports 3.03 1.92 57.9% 1.11

Real consumption 897.9 952.4 6.1% 54.5

Apparent stock change 28.2 -129.6 Chinese apparent demand (melt) 18.16 17.20 5.6% 0.96

Exports of ni in stainless 192.8 278.1 44.2% 85.3

Total Ni exports (Ni+SS) 241.2 396.1 64.3% 155.0

Net exports ni in SS 136.4 217.6 59.6% 81.2

Total net ni exports (Ni +SS) -85.9 91.5 -206.6% 177.3

Page 26

China a net nickel exporter in 2014!(Ex raw

materials). Big swing in 2015?

Source: WBMS, CSSC, Chinese Customs, Macquarie Research, May 2015

Jan-Dec Jan-Dec YoY 15/14 YoY

2014 2015F % change change(t)

Nickel ('000t)

Production 696.8 616.8 -11.5% -7.2

(of which NPI) 480.0 385.0 -19.8% -20.0

plus

Imports 244.2 403.2 65.1% -26.4

minus

Exports 118.0 30.0 -74.6% 69.7

gives

Apparent consumption 822.9 990.0 20.3% -103.3

Real consumption 952.4 1004.5 5.5% 54.5

Apparent stock change -129.6 -14.5

Exports of ni in stainless 278.1 278.1 0.0% 85.3

Total Ni exports (Ni+SS) 396.1 308.1 -22.2% 155.0

Net exports ni in SS 217.6 217.6 0.0% 81.2

Total net ni exports (Ni +SS) 91.5 -155.6 -270.1% 177.3

267 305 277 264 237

418

-36-106 -105

-153-242 -230

-47

-33 -31

-41

-111

-30

-400

-300

-200

-100

0

100

200

300

400

500

2010 2011 2012 2013 2014 2015f

'00

0t

Ni

Primary Ni imports Ni in Stainless Primary Ni exports Total

Page 27

Stainless steel in 2015

World stainless production growth

projected to slow from 9.4% and

7.8% in 2013 and 2014 to 4.2%

this year (previous forecast:5.2%)

US and Chinese growth slowing

while Europe to benefit from less

imports from China and Taiwan

Chinese growth to decelerate

due to much lower growth in

exports and weaker domestic

demand growth

Source: INSG, Vale, ISSF, Macquarie Research, May 2015

Year Year Year

'000t 2013 2014E 2015F

USA 2030 2389 2439

Japan 3175 3331 3364

Europe 7175 7230 7380

Korea 2143 2038 2140

Taiwan 1081 1103 1114

India 2680 2973 3211

China 19461 21722 22846

Other 1143 1115 1152

Total 38887 41901 43646

Total Ex-China 19426 20178 20800

Chinese net exports 2250 3563 3382

% change yoy

USA 2.6% 17.7% 2.1%

Japan 1.4% 4.9% 1.0%

Europe -3.7% 0.8% 2.1%

Korea -1.1% -4.9% 5.0%

Taiwan -2.2% 2.0% 1.0%

India 8.5% 10.9% 8.0%

China 20.8% 11.6% 5.2%

Other 2.0% -2.5% 3.4%

Total 9.4% 7.8% 4.2%

Total Ex-China 0.0% 3.9% 3.1%

Chinese net exports 46.2% 58.4% -5.1%

Page 28

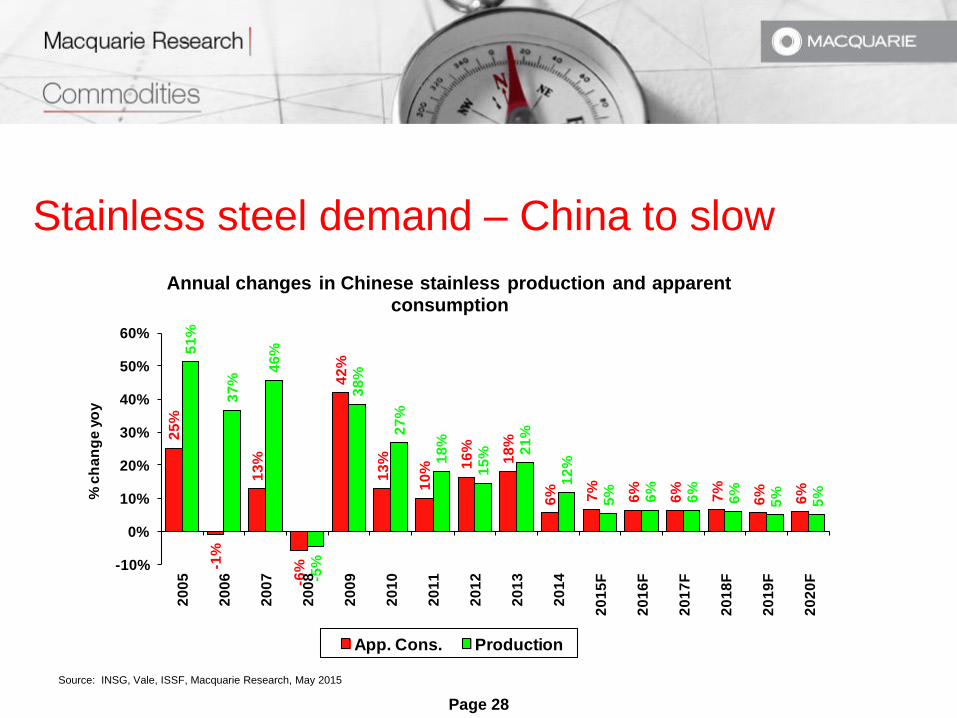

Stainless steel demand – China to slow

Source: INSG, Vale, ISSF, Macquarie Research, May 2015

25

%

-1%

13

%

-6%

42

%

13

%

10

% 16

%

18

%

6% 7%

6%

6%

7%

6%

6%

51

%

37

%

46

%

-5%

38

%

27

%

18

%

15

% 21

%

12

%

5% 6%

6%

6%

5%

5%

-10%

0%

10%

20%

30%

40%

50%

60%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

F

20

16

F

20

17

F

20

18

F

20

19

F

20

20

F

% c

ha

ng

e y

oy

Annual changes in Chinese stainless production and apparent consumption

App. Cons. Production

Page 29

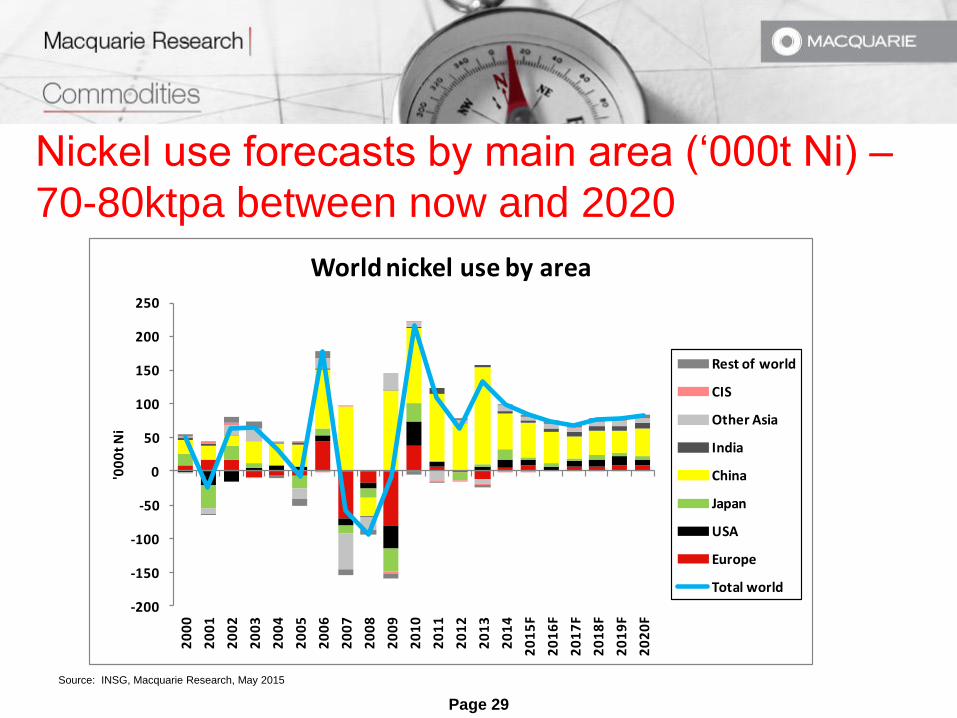

Nickel use forecasts by main area (‘000t Ni) –

70-80ktpa between now and 2020

Source: INSG, Macquarie Research, May 2015

-200

-150

-100

-50

0

50

100

150

200

250

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

F

20

16

F

20

17

F

20

18

F

20

19

F

20

20

F

'00

0t

Ni

World nickel use by area

Rest of world

CIS

Other Asia

India

China

Japan

USA

Europe

Total world

Page 30

Main nickel supply changes…870kt this

decade

Source: Company Reports, INSG, Macquarie Research, May 2015

0

100

200

300

400

500

600

20

10

20

14

20

15

F

20

16

F

20

17

F

20

18

F

20

19

F

20

20

F

'00

0t

Ni

Main capacity increases to 2020Taguang

FeNix

Ramu

Taganito

Ambatovy

Barro Alto

Talvivarra

Rustenburg

Nova-Bollinger

Pomalaa

Kwangyang

Koniambo

Poiseiden

Ban Phuc

Eagle

Enterprise

Kevista

Ravensthorpe

Onca Puma

VNC (Goro)

159

282

361

500 480

385350 350 350

3253000

0

1

23

2555

90125 160 200

0

100

200

300

400

500

600

2010 2011 2012 2013 2014 2015f 2016f 2017f 2018f 2019f 2020f

'000 t

pa N

i in

NP

I

Nickel pig iron production

Indonesia China

Page 31

Will Indonesian ban stay? Will Philippines

impose a ban?

Speculated by some that lack of progress in building NPI plants will lead

to a full or partial rescinding of ore export ban.

Partially relented for those building plants?

We still think that this is unlikely – no indication from top government

officials that this will be the case

Even a partial ban would be disastrous for the market since “everyone”

would say that they are building plants, making enforcement impossible!

Any ban from Philippines would be announced with a multiple-year

delay (up to five years) – no short-term market impact

Page 32

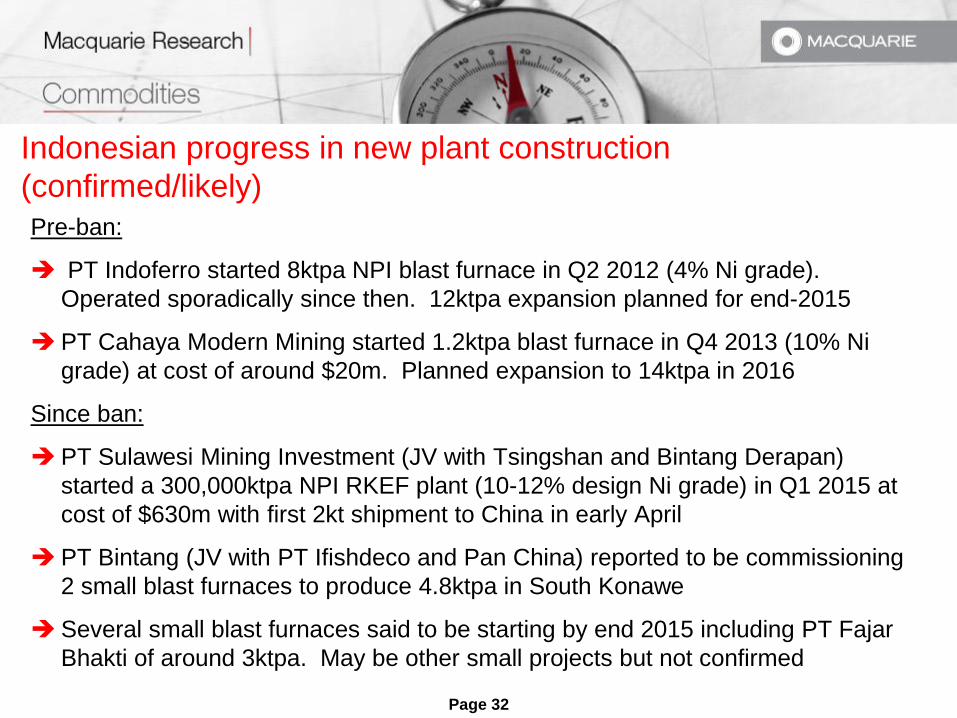

Indonesian progress in new plant construction

(confirmed/likely)

Pre-ban:

PT Indoferro started 8ktpa NPI blast furnace in Q2 2012 (4% Ni grade).

Operated sporadically since then. 12ktpa expansion planned for end-2015

PT Cahaya Modern Mining started 1.2ktpa blast furnace in Q4 2013 (10% Ni

grade) at cost of around $20m. Planned expansion to 14ktpa in 2016

Since ban:

PT Sulawesi Mining Investment (JV with Tsingshan and Bintang Derapan)

started a 300,000ktpa NPI RKEF plant (10-12% design Ni grade) in Q1 2015 at

cost of $630m with first 2kt shipment to China in early April

PT Bintang (JV with PT Ifishdeco and Pan China) reported to be commissioning

2 small blast furnaces to produce 4.8ktpa in South Konawe

Several small blast furnaces said to be starting by end 2015 including PT Fajar

Bhakti of around 3ktpa. May be other small projects but not confirmed

Page 33

Beyond the confirmed there are a multitude of projects...over

250ktpa identified from press/interviews

Source: Jakarta Post, CM Group, Chinese press, interviews with industry, Macquarie Research, May 2015

0

50

100

150

200

250

300

2014F 2015F 2016F 2017F 2018F 2019F

'00

0t

Ni

Projects Indonesian NPI production to 2020

Shenwu-Titan Phase III

Shenwu-Titan Phase II

Delong Ni Industry Zone

Ningxia Hengshun

Brillimetal Phase I1

Indoferro Phase II

Wenzhou Huadi Industry Phase I

PT Multi Baja Industri (Group: RKA)

Hanking Phase I

Hanking Phase I

PT Cahaya Modern Metal Mining Phase 2

PT Central Omega Resources YUSCO

Weiye Toprich Hong Kong

PT. Sambas Mineral Mining

China’s Meng La Chen Feng Mining Development Company Ltd

Zhejiang Baoli mining

Shenwu-Titan Phase I

Shaanxi Energy Metals&minerals Resources

Brillimetal Phase I

Wenzhou Huadi Industry Phase I

Ifshideco

Lianyungang Blackstone International

Zhenshi Holding group

Integra Mining Nusantara

Kembar Emas Sultra

Tsingshan/Sulawesi Mining Phase II

Tsingshan/Sulawesi Mining Phase I

PT Indoferro phase 1

PT Cahaya Modern Metal Mining

0

50

100

150

200

250

300

2014F 2015F 2016F 2017F 2018F 2019F 2020F

'00

0t

Ni i

n N

PI

Indonesian NPI potential projects to 2020

Existing Under construction/likely Possible

Page 34

What is likely?

PT Sulawesi Mining Investment (Tsingshan/Bintang Derapan)

construction of a further 600,000 tpa RKEF NPI plant to be completed by

end 2016 (around 60ktpa Ni) at a capex of $1.02bn

Tsingshan has confirmed plans to build integrated 2mtpa stainless steel

slab plant to come on stream in two phases by mid-2016 and mid-2017

which presumably will absorb all its NPI production by hot metal transfer

We can identify around 150ktpa of committed and likely capacity

(commercial confidentiality precludes more detail!)

Beyond that there are another 130-150ktpa of potential projects but

many announced last year are already “dead”.

Page 35

Issues surrounding projects

Many of the announced projects were based on an assumption that the

Indonesian government would relax the ban for companies with projects

under construction

Major issues regarding building of infrastructure, in particular power

plants – many projects are reliant on third party funding of industrial

estates that would provide shared power and other infrastructure - so far

only PTSMI (Tsingshan) and Well Harvest (for alumina) are under

construction out of 13 possible projects

Many of the projects have yet to secure land/ore access or operating

permits

Many companies are facing losses on iron ore or NPI operations in

China and are financially constrained in a low iron ore/nickel price

environment

Page 36

The economics of NPI are phenomenal compared to

conventional processes at current ore prices

100000

60000

80000

5000

15000 15000

25000

40000

12000 12000 11000

1850015000

21000

1100013500

29500

2250025000

19375 17625

23625

1537520500

0

20000

40000

60000

80000

100000

120000

HPAL (integrated) HPAL (intermediate) FeNi (recent) Old NPI China RKEF (1.8% Ni ore)

China RKEF (1.5% Ni ore)

Indonesian NPI (RKEF)?

Chinese HPAL?

$/t

on

ne

The "economics" of new capacity - based on today's parameters

Capex Opex Incentive price

Source: Company data, Wood Mackenzie, Macquarie Research, April 2015

Page 37

Sourcing of ore for Chinese nickel pig iron –

Indonesian destocking to end in 2015

Source: Industry estimates, Macquarie Research, May 2015

40 75 80

50 40 40 40 40

20

120

174 190 195 195

167 139

59

75

75 100 105 105 108

111

365

210 50

- - --

-

500 480

385

350 350 350 325 300

-

50

100

150

200

250

300

350

400

450

500

2013 2014 2015f 2016f 2017f 2018f 2019f 2020f

'000t Ni Sourcing or ore for Chinese Nickel pig iron production

Philippines HG Philippines MG Philippines LG

Indonesian LG Indonesian HG Other feed (laterites/sulphides?)

Page 38

We think that Chinese nickel pig iron will be

more expensive in future

As ore supply gets reduced, price

of ore relative to LME price will

rise further

Once blending opportunities with

higher grade ore are reduced

(Indonesian stocks exhausted and

high-grade reserves in Philippines

depleted) conversion costs for ore

into NPI will also rise

Higher NPI costs will push up

NPI prices relative to LME price

0%

5%

10%

15%

20%

25%

30%

35%

40%

2009 2010 2011 2012 2013 2014 2015

% o

f L

ME

Nickel in ore as a % of LME price for Chinese NPI producers

1.8% Ni ore 1.5% Ni ore

Source: SMM, LME, Macquarie Research, May 2015

Page 39

Will Chinese stainless steel producers lose

competiveness due to changing NPI landscape?

Source: LME, CRU, SMM, Mysteel, Macquarie Research, May 2015

-5000

0

5000

10000

15000

20000

25000

30000

2010 2011 2012 2013 2014 2015

$/t

on

ne

of

ni

What you pay for nickel differs!Monthly averages, Jan 2010-April 2014

LME Ni

25% Ni FeNi (credit for free Fe)

10% NPI (credit for free Fe)

EU ni in scrap (no free Fe)

1.7% NPI (with scrap credit)

Page 40

China appears to be losing competiveness in

304 grade stainless steel

-600

-500

-400

-300

-200

-100

0

100

2010 2011 2012 2013 2014 2015

$/t

on

ne

of

cru

de

SS

Chinese costs of Ni minus EU costsMonthly average Jan 2010-April 2015

500

700

900

1100

1300

1500

1700

1900

2100

2300

2010 2011 2012 2013 2014 2015

$/t

on

ne

of

cru

de

SS

Estimated cost of nickel to EU and Chinese stainless producers

Monthly averages, Jan 2010-April 2015

Europe China

Source: LME, CRU, SMM, Mysteel, Macquarie Research, May 2015

Page 41

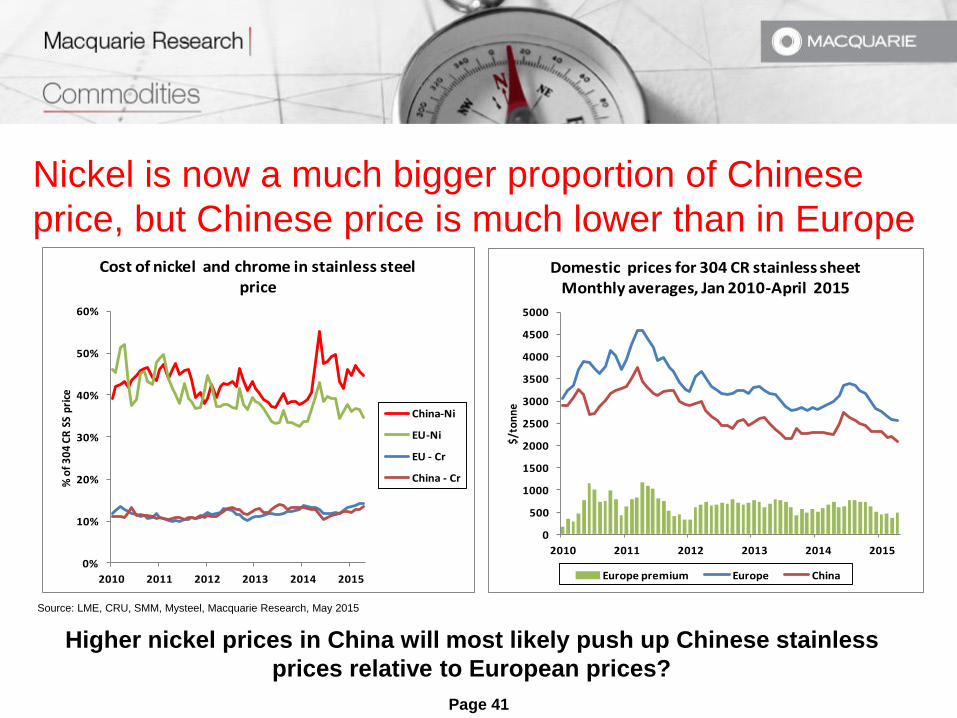

Nickel is now a much bigger proportion of Chinese

price, but Chinese price is much lower than in Europe

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012 2013 2014 2015

% o

f 3

04

CR

SS

pri

ce

Cost of nickel and chrome in stainless steel price

China-Ni

EU-Ni

EU - Cr

China - Cr

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2010 2011 2012 2013 2014 2015

$/t

on

ne

Domestic prices for 304 CR stainless sheetMonthly averages, Jan 2010-April 2015

Europe premium Europe China

Source: LME, CRU, SMM, Mysteel, Macquarie Research, May 2015

Higher nickel prices in China will most likely push up Chinese stainless

prices relative to European prices?

Page 42

Chinese nickel price advantage disappears

Chinese nickel advantage eroded

as cost of making nickel pig iron

goes up relative to nickel price

Hot metal transfer (integrated

NPI-stainless) still offers greater

competiveness

Will Chinese stainless price rise in

future relative to European

prices? – Most likely-100

0

100

200

300

400

500

600

700

800

2010 2011 2012 2013 2014 2015 YTD

$/to

nn

e

European price outweighs China nickel advantageAnnual averages

EU premium over China - stainless price

Chinese nickel advantage over Europe

Source: LME, CRU, SMM, Mysteel, Macquarie Research, May 2015

Page 43

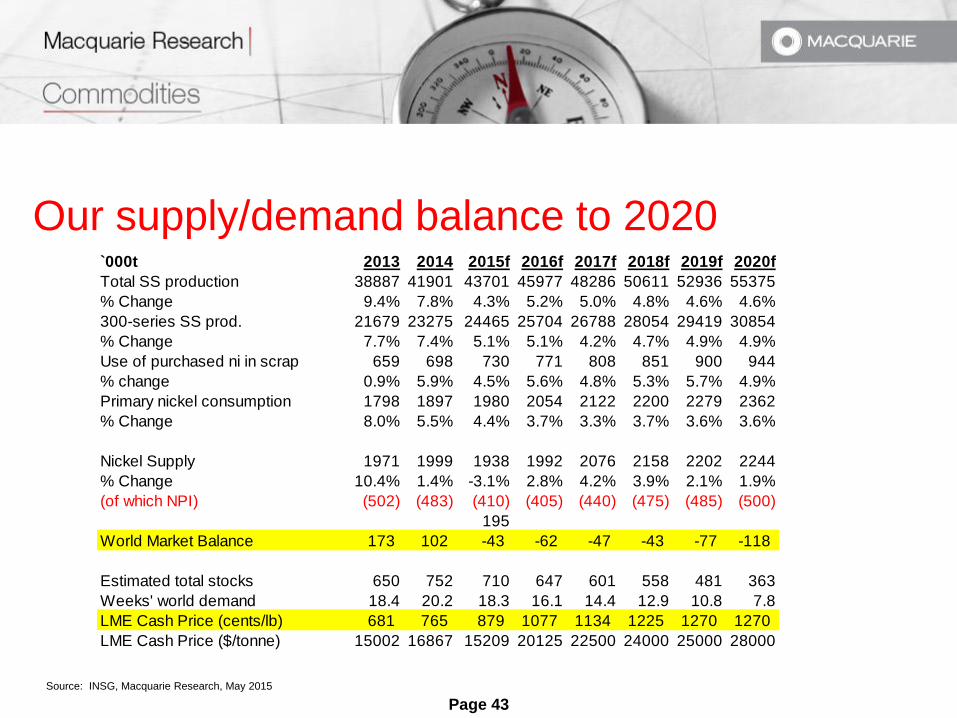

Our supply/demand balance to 2020

Source: INSG, Macquarie Research, May 2015

`000t 2013 2014 2015f 2016f 2017f 2018f 2019f 2020f

Total SS production 38887 41901 43701 45977 48286 50611 52936 55375

% Change 9.4% 7.8% 4.3% 5.2% 5.0% 4.8% 4.6% 4.6%

300-series SS prod. 21679 23275 24465 25704 26788 28054 29419 30854

% Change 7.7% 7.4% 5.1% 5.1% 4.2% 4.7% 4.9% 4.9%

Use of purchased ni in scrap 659 698 730 771 808 851 900 944

% change 0.9% 5.9% 4.5% 5.6% 4.8% 5.3% 5.7% 4.9%

Primary nickel consumption 1798 1897 1980 2054 2122 2200 2279 2362

% Change 8.0% 5.5% 4.4% 3.7% 3.3% 3.7% 3.6% 3.6%

Nickel Supply 1971 1999 1938 1992 2076 2158 2202 2244

% Change 10.4% 1.4% -3.1% 2.8% 4.2% 3.9% 2.1% 1.9%

(of which NPI) (502) (483) (410) (405) (440) (475) (485) (500)

195

World Market Balance 173 102 -43 -62 -47 -43 -77 -118

Estimated total stocks 650 752 710 647 601 558 481 363

Weeks' world demand 18.4 20.2 18.3 16.1 14.4 12.9 10.8 7.8

LME Cash Price (cents/lb) 681 765 879 1077 1134 1225 1270 1270

LME Cash Price ($/tonne) 15002 16867 15209 20125 22500 24000 25000 28000

Page 44

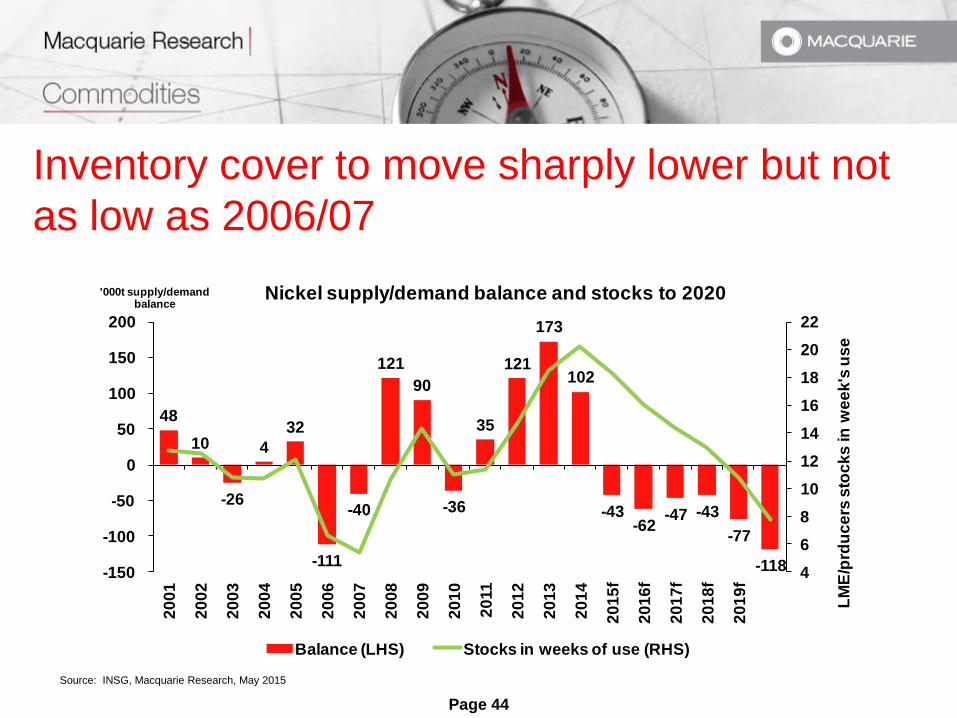

Inventory cover to move sharply lower but not

as low as 2006/07

Source: INSG, Macquarie Research, May 2015

48

10

-26

4

32

-111

-40

121

90

-36

35

121

173

102

-43 -62

-47 -43

-77

-118 4

6

8

10

12

14

16

18

20

22

-150

-100

-50

0

50

100

150

200

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

f

20

16

f

20

17

f

20

18

f

20

19

f

LM

E/p

rdu

ce

rs s

toc

ks

in

we

ek

's u

se

'000t supply/demand balance

Nickel supply/demand balance and stocks to 2020

Balance (LHS) Stocks in weeks of use (RHS)

Page 45

In conclusion – the medium-term outlook

Deficits should finally arrive from 2015 onwards due to Indonesian ban and prices should move sustainably higher

Out to 2020, a major deficit has been avoided by the Chinese using lower-quality ore from Philippines (at higher cost)

New NPI capacity from Indonesia will not grow fast enough to offset losses from China

China nickel cost advantage in making stainless has been eliminated – this will lead to higher Chinese stainless steel domestic prices

Key to longer run prices is cost of building capacity outside Indonesia – recent experience suggests that if non-Chinese players build it, prices need to be $23-25,000/t to generate a return

Page 46

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand

Outperform – return > 3% in excess of benchmark return

Neutral – return within 3% of benchmark return

Underperform – return > 3% below benchmark return

Benchmark return is determined by long term nominal GDP

growth plus 12 month forward market dividend yield.

Macquarie – Asia/Europe

Outperform – expected return >+10%

Neutral – expected return from -10% to +10%

Underperform – expected <-10%

Macquarie First South - South Africa

Outperform – return > 10% in excess of benchmark return

Neutral – return within 10% of benchmark return

Underperform – return > 10% below benchmark return

Macquarie - Canada

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Macquarie - USA

Outperform – return > 5% in excess of benchmark return

Neutral – return within 5% of benchmark return

Underperform – return > 5% below benchmark return

Volatility index definition*This is calculated from the volatility of historic price

movements.

Very high–highest risk – Stock should be expected to

move up or down 60-100% in a year – investors should

be aware this stock is highly speculative.

High – stock should be expected to move up or down

at least 40-60% in a year – investors should be aware

this stock could be speculative.

Medium – stock should be expected to move up or

down at least 30-40% in a year.

Low–medium – stock should be expected to move up

or down at least 25-30% in a year.

Low – stock should be expected to move up or down

at least 15-25% in a year.

* Applicable to Australian/NZ stocks only

Recommendation – 12 months

Note: Quant recommendations may differ from

Fundamental Analyst recommendations

Financial definitions

All "Adjusted" data items have had the following

adjustments made:

Added back: goodwill amortisation, provision for

catastrophe reserves, IFRS derivatives & hedging,

IFRS impairments & IFRS interest expense

Excluded: non recurring items, asset revals, property

revals, appraisal value uplift, preference dividends &

minority interests

EPS = adjusted net profit /efpowa*

ROA = adjusted ebit / average total assets

ROA Banks/Insurance = adjusted net profit /average

total assets

ROE = adjusted net profit / average shareholders funds

Gross cashflow = adjusted net profit + depreciation

*equivalent fully paid ordinary weighted average

number of shares

All Reported numbers for Australian/NZ listed

stocks are modelled under IFRS (International

Financial Reporting Standards).

Recommendation proportions – For quarter ending 31 March 2015

AU/NZ Asia RSA USA CA EUR

Outperform 48.99% 59.51% 49.30% 43.79% 59.59% 52.20% (for US coverage by MCUSA, 7.42% of stocks followed are investment banking clients)

Neutral 34.12% 26.62% 35.21% 50.29% 34.93% 31.32% (for US coverage by MCUSA, 5.68% of stocks followed are investment banking clients)

Underperform 16.89% 13.87% 15.49% 5.93% 5.48% 16.48% (for US coverage by MCUSA, 0.87% of stocks followed are investment banking clients)

Company-Specific Disclosures:

Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures.

Analyst Certification:

The views expressed in this research accurately reflect the personal views of the analyst(s) about the subject securities or issuers and no part of the compensation of the analyst(s) was,

is, or will be directly or indirectly related to the inclusion of specific recommendations or views in this research. The analyst principally responsible for the preparation of this research

receives compensation based on overall revenues of Macquarie Group Ltd ABN 94 122 169 279 (AFSL No. 318062) (MGL) and its related entities (the Macquarie Group) and has taken

reasonable care to achieve and maintain independence and objectivity in making any recommendations.

General Disclaimers:

Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America Ltd; Macquarie Capital (USA) Inc;

Macquarie Capital Securities Ltd and its Taiwan branch; Macquarie Capital Securities (Singapore) Pte Ltd; Macquarie Securities (NZ) Ltd; and Macquarie First South Securities (Pty)

Limited; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities (Thailand) Ltd are

not authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia), and their obligations do not represent deposits or other liabilities of

Macquarie Bank Limited ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of any of the above mentioned

entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect of the obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35

million. This research has been prepared for the general use of the wholesale clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other

person. If you are not the intended recipient you must not use or disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail

and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has

established and implemented a conflicts policy at group level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant to regulatory requirements (including

the FCA Rules) which sets out how we must seek to identify and manage all material conflicts of interest. Nothing in this research shall be construed as a solicitation to buy or sell any

security or product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account your investment objectives, financial situation or

particular needs. Before making an investment decision on the basis of this research, you need to consider, with or without the assistance of an adviser, whether the advice is appropriate

in light of your particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an

individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and

international stock market or economic conditions, which may adversely affect the value of the investment. This research is based on information obtained from sources believed to be

reliable but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it.

Opinions expressed are subject to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising

from any use of this research and/or further communication in relation to this research. Clients should contact analysts at, and execute transactions through, a Macquarie Group entity in

their home jurisdiction unless governing law permits otherwise.

Disclaimer: The information contained in this e-mail is confidential and has been furnished to you solely for your use. You may not disclose, reproduce or distribute the information in any

way. Macquarie does not guarantee the integrity of this e-mail or attached files.

Macquarie Capital (USA) Inc. affiliate research reports and affiliate employees are not subject to the disclosure requirements of FINRA rules. Any persons receiving this report directly from

Macquarie Capital (USA) Inc. and wishing to effect a transaction in any security described herein should do so with Macquarie Capital (USA) Inc. In Germany, this research is issued

and/or distributed by Macquarie Capital (Europe) Limited, Niederlassung Deutschland, which is authorised and regulated by the UK Financial Conduct Authority and in Germany by BaFin.

Macquarie salespeople, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions which are contrary to the

opinions expressed in this research. Macquarie Research produces a variety of research products including, but not limited to, fundamental analysis, macro-economic analysis,

quantitative analysis, and trade ideas. Recommendations contained in one type of research product may differ from recommendations contained in other types of research, whether as a

result of differing time horizons, methodologies, or otherwise.

Page 47

Country-Specific Disclaimers:

Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the Australian Securities Exchange.

New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. Canada: In Canada, research is prepared, approved and distributed by

Macquarie Capital Markets Canada Ltd, a participating organisation of the Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Macquarie Capital Markets North

America Ltd., which is a registered broker-dealer and member of FINRA, accepts responsibility for the contents of reports issued by Macquarie Capital Markets Canada Ltd in the United

States and sent to US persons. Any US person wishing to effect transactions in the securities described in the reports issued by Macquarie Capital Markets Canada Ltd should do so with

Macquarie Capital Markets North America Ltd. The Research Distribution Policy of Macquarie.Capital Markets Canada Ltd is to allow all clients that are entitled to have equal access to our

research. United Kingdom: In the United Kingdom, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated by the Financial Conduct

Authority (No. 193905). Germany: In Germany, research is issued and distributed by Macquarie Capital (Europe) Ltd, Niederlassung Deutschland, which is authorised and regulated in

the United Kingdom by the Financial Conduct Authority (No. 193905). France: In France, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and

regulated in the United Kingdom by the Financial Conduct Authority (No. 193905). Hong Kong & Mainland China: In Hong Kong, research is issued and distributed by Macquarie Capital

Securities Ltd, which is licensed and regulated by the Securities and Futures Commission. In Mainland China, Macquarie Securities (Australia) Limited Shanghai Representative Office

only engages in non-business operational activities excluding issuing and distributing research. Only non-A share research is distributed into Mainland China by Macquarie Capital

Securities Ltd. Japan: In Japan, research is Issued and distributed by Macquarie Capital Securities (Japan) Limited, a member of the Tokyo Stock Exchange, Inc., Osaka Securities

Exchange Co. Ltd. (Financial Instruments Firm, Kanto Financial Bureau (kin-sho) No. 231, a member of Japan Securities Dealers Association and The Financial Futures Association of

Japan and Japan Investment Advisers Association). India: In India, research is issued and distributed by Macquarie Capital Securities (India) Pvt. Ltd. (CIN: U65920MH1995PTC090696),

formerly known as Macquarie Capital (India) Pvt. Ltd., 92, Level 9, 2 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra (East), Mumbai – 400 051, India, which is a SEBI

registered stockbroker having membership with National Stock Exchange of India Limited (INB231246738), BSE Limited (INB011246734) and has applied to SEBI for a certificate under

the SEBI (Research Analysts) Regulations, 2014. Malaysia: In Malaysia, research is issued and distributed by Macquarie Capital Securities (Malaysia) Sdn. Bhd. (Company registration

number: 463469-W) which is a Participating Organisation of Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission. Taiwan: In

Taiwan, research is issued and distributed by Macquarie Capital Securities Ltd, Taiwan Branch, which is licensed and regulated by the Financial Supervisory Commission. No portion of

the report may be reproduced or quoted by the press or any other person without authorisation from Macquarie. Nothing in this research shall be construed as a solicitation to buy or sell

any security or product. Research Associate(s) in this report who are registered as Clerks only assist in the preparation of research and are not engaged in writing the research. Thailand:

In Thailand, research is produced, issued and distributed by Macquarie Securities (Thailand) Ltd. Macquarie Securities (Thailand) Ltd. is a licensed securities company that is authorized

by the Ministry of Finance, regulated by the Securities and Exchange Commission of Thailand and is an exchange member of the Stock Exchange of Thailand. The Thai Institute of

Directors Association has disclosed the Corporate Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange Commission of Thailand.

Macquarie Securities (Thailand) Ltd does not endorse the result of the Corporate Governance Report of Thai Listed Companies but this Report can be accessed at: http://www.thai-

iod.com/en/publications.asp?type=4. South Korea: In South Korea, unless otherwise stated, research is prepared, issued and distributed by Macquarie Securities Korea Limited , which is

regulated by the Financial Supervisory Services. Information on analysts in MSKL is disclosed at

http://dis.kofia.or.kr/websquare/index.jsp?w2xPath=/wq/fundMgr/DISFundMgrAnalystStut.xml&divisionId=MDIS03002001000000&serviceId=SDIS03002001000. South Africa: In South

Africa, research is issued and distributed by Macquarie First South Securities (Pty) Limited, a member of the JSE Limited. Singapore: In Singapore, research is issued and distributed by

Macquarie Capital Securities (Singapore) Pte Ltd (Company Registration Number: 198702912C), a Capital Markets Services license holder under the Securities and Futures Act to deal in

securities and provide custodial services in Singapore. Pursuant to the Financial Advisers (Amendment) Regulations 2005, Macquarie Capital Securities (Singapore) Pte Ltd is exempt

from complying with sections 25, 27 and 36 of the Financial Advisers Act. All Singapore-based recipients of research produced by Macquarie Capital (Europe) Limited, Macquarie Capital

Markets Canada Ltd, Macquarie First South Securities (Pty) Limited and Macquarie Capital (USA) Inc. represent and warrant that they are institutional investors as defined in the

Securities and Futures Act. United States: In the United States, research is issued and distributed by Macquarie Capital (USA) Inc., which is a registered broker-dealer and member of

FINRA. Macquarie Capital (USA) Inc, accepts responsibility for the content of each research report prepared by one of its non-US affiliates when the research report is distributed in the

United States by Macquarie Capital (USA) Inc. Macquarie Capital (USA) Inc.’s affiliate’s analysts are not registered as research analysts with FINRA, may not be associated persons of

Macquarie Capital (USA) Inc., and therefore may not be subject to FINRA rule restrictions on communications with a subject company, public appearances, and trading securities held by a

research analyst account. Information regarding futures is provided for reference purposes only and is not a solicitation for purchases or sales of futures. Any persons receiving this report

directly from Macquarie Capital (USA) Inc. and wishing to effect a transaction in any security described herein should do so with Macquarie Capital (USA) Inc. Important disclosure

information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures, or contact your registered representative at 1-888-MAC-STOCK, or

write to the Supervisory Analysts, Research Department, Macquarie Securities, 125 W.55th Street, New York, NY 10019.

© Macquarie Group

Page 48