![Importance of anisotropy in the spin-liquid … · PHYSICAL REVIEW B 88, 155139 (2013) Importance of anisotropy in the spin-liquid candidate Me 3EtSb[Pd(dmit) 2] 2 A. C. Jacko, Luca](https://static.fdocuments.in/doc/165x107/5b8452a77f8b9aef498c13a1/importance-of-anisotropy-in-the-spin-liquid-physical-review-b-88-155139-2013.jpg)

The importance of liquid alternatives in a portfolio context · The importance of liquid...

38

For professional investors and advisers only. The importance of liquid alternatives in a portfolio context Andrew Dreaneen | Head of Schroder GAIA Product & Business Development This presentation is only for qualified investors attending the Liquid Alternative event. Industry Overview – Schroder GAIA & GAIA II Update

Transcript of The importance of liquid alternatives in a portfolio context · The importance of liquid...

For professional investors and advisers only.

The importance of liquid

alternatives in a portfolio

context

Andrew Dreaneen | Head of Schroder GAIA Product &

Business Development

This presentation is only for qualified investors attending the Liquid Alternative event.

Industry Overview – Schroder GAIA & GAIA II

Update

Agenda

Global hedge fund landscape

Drivers for hedge fund allocations and common misconceptions

Available strategies & setting a framework

Thoughts and considerations for choosing UCITS hedge funds

Schroders capabilities in liquid alternatives

Conclusions

1

Global hedge fund

landscape

Global hedge fund assets

3

Source: HFI Global Autumn Review 2016

Global hedge fund assets

4

Source: HFI Global Autumn Review 2016

Drivers for hedge fund

allocations and common

misconceptions

Global alternative assets

(US$ in trillions) by asset class type

Demand for Alternatives Substantial growth forecasted over the next five years

3,2

4,8

0.9

2.1

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

2012 2015F 2018F 2020F

6

Source: Strategy and PWC 2015

Global alternative assets

(US$ in trillions) by sector

Global alternative assets

(US$ in trillions) by region

8.1

10.8

14.6

18.1

2,8

5,6

1,5

2,5

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

2012 2015F 2018F 2020F0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

16,0

18,0

20,0

2012 2015F 2018F 2020F

8.1

10.8

14.6

18.1

8.1

10.8

14.6

18.1

Commodities

Liquid

alternatives

Institutional

loans

Real estate

Hedge funds

Private equity

Sovereign

wealth funds

Insurers

High-net-worth

Mass affluent

Pension funds

Middle East

and Africa

Latin America

Asia-Pacific

Europe

North America

0.5

1.0

$Bn Club of UCITS Absolute Return Investors Reasons for Allocating

7

Source: Morgan Stanley Absolute Return UCITS Survey Results November 2015. 155 Respondents with Absolute Return UCITS AUM: $91bn

Source: Schroders as at 30 September 2016 (strategy inception for each manager). *Please not Two Sigma is based on simulated returns, please refer to the full simulated

performance disclaimers at the back of the presentation

Providing uncorrelated

returns to overall

portfolio; 55%

Reduce equity beta; 6%

Substitute for fix income

exposure; 8%

Managing cash to offset illiquid

instruments; 7%

Simply look for outperformance

; 22%

Reduced duration risk;

2%

Investment considerations for Allocating

S&P 500 MSCI

World

MSCI AC

Asia

Pacific

ML High

Yield

index

HFRI

Egerton 0.47 0.50 - - 0.68

Sirios 0.42 0.47 - - 0.60

Indus - 0.66 0.79 - 0.74

Paulson 0.24 0.28 - - 0.39

BSP - - - 0.03 0.08

NGA 0.54 - - 0.71 0.65

BlueTrend 0.00 0.03 - 0.03 0.14

Two

Sigma* -0.23 -0.23 - -0.18 -0.16

Cat Bond -0.08 -0.02 - 0.09 -0.02

Ex

am

ple

s

93.2 60.1 50.6

58 207 185

45.7% 29.5% 24.8%

Who are the main providers of liquid alternatives today?

Hedge Fund Managers Long Only Asset Managers Convergence Asset Managers

# P

rod

uc

ts

Source: HFR, HFI, Strategic Consulting analysis, as at 30 September 2015.

AU

M (

US

Db

n)

8

Using distribution capabilities to build alternatives businesses Marketing HF expertise to UCITS investor base

AUM dominated by Asset Managers 75%: but Hedge Fund Managers now 25%

% A

UM

US Based Managers Abrams Capital Management GMT Capital

Adage Capital Management GoldenTree Asset Management

Anchorage Capital Group Greenlight Capital

Angelo, Gordon & Co. HBK Capital Management

Apollo Management Highfields Capital Management

Appaloosa Management JANA Partners

Avenue Capital Group Kayne Anderson Capital Advisors

Bain Capital/Brookside Capital Partners King Street Capital Management

Balyasny Asset Management Lone Pine Capital

Baupost Group Luxor Capital Group

Blue Ridge Capital Magnetar Capital

BlueMountain Capital Management Marathon Asset Management

Bracebridge Capital Mariner Investment Group

Bridgewater Associates Mason Capital Management

Carlson Capital Millennium Management

Caxton Associates Monarch Alternative Capital

Centerbridge Partners Moore Capital Management

Cerberus Capital Management MSD Capital

Citadel Pennant Capital Management

Coatue Capital Perry Capital

Convexity Capital Management Pershing Square Capital Management

Corvex Management Pine River Capital Management

D.E. Shaw Group PointState Capital

Davidson Kempner Capital Management Renaissance Technologies

Discovery Capital Management Samlyn Capital

DW Partners Scopia Capital

EJF Capital Senator Investment Group

Element Capital Silver Point Capital

Ellington Management Group Soroban Capital Partners

Elliott Management Corporation Steadfast Capital Management

Emerging Sovereign Group Taconic Capital Advisors

Eton Park Capital Management Third Point

Farallon Capital Management Tiger Global Management

Fir Tree Partners Trian Fund Management

First Quadrant ValueAct Capital Management

Glenview Capital Management Viking Global Investors

AQR Capital Management Maverick Capital

Beach Point Capital Management MKP Capital Management

Blackstone Group/GSO Capital Partners Och-Ziff Capital Management Group

Canyon Capital Advisors Omega Advisors

Fortress Investment Group Paulson & Co.

Graham Capital Management Tudor Investment Corp

Grantham, Mayo, Van Otterloo Two Sigma Investments

Halcyon Asset Management Visium Asset Management

Indus Capital Partners York Capital Management

US Based Managers Abrams Capital Management GMT Capital

Adage Capital Management GoldenTree Asset Management

Anchorage Capital Group Greenlight Capital

Angelo, Gordon & Co. HBK Capital Management

Apollo Management Highfields Capital Management

Appaloosa Management JANA Partners

Avenue Capital Group Kayne Anderson Capital Advisors

Bain Capital/Brookside Capital Partners King Street Capital Management

Balyasny Asset Management Lone Pine Capital

Baupost Group Luxor Capital Group

Blue Ridge Capital Magnetar Capital

BlueMountain Capital Management Marathon Asset Management

Bracebridge Capital Mariner Investment Group

Bridgewater Associates Mason Capital Management

Carlson Capital Millennium Management

Caxton Associates Monarch Alternative Capital

Centerbridge Partners Moore Capital Management

Cerberus Capital Management MSD Capital

Citadel Pennant Capital Management

Coatue Capital Perry Capital

Convexity Capital Management Pershing Square Capital Management

Corvex Management Pine River Capital Management

D.E. Shaw Group PointState Capital

Davidson Kempner Capital Management Renaissance Technologies

Discovery Capital Management Samlyn Capital

DW Partners Scopia Capital

EJF Capital Senator Investment Group

Element Capital Silver Point Capital

Ellington Management Group Soroban Capital Partners

Elliott Management Corporation Steadfast Capital Management

Emerging Sovereign Group Taconic Capital Advisors

Eton Park Capital Management Third Point

Farallon Capital Management Tiger Global Management

Fir Tree Partners Trian Fund Management

First Quadrant ValueAct Capital Management

Glenview Capital Management Viking Global Investors

AQR Capital Management Maverick Capital

Beach Point Capital Management MKP Capital Management

Blackstone Group/GSO Capital Partners Och-Ziff Capital Management Group

Canyon Capital Advisors Omega Advisors

Fortress Investment Group Paulson & Co.

Graham Capital Management Tudor Investment Corp

Grantham, Mayo, Van Otterloo Two Sigma Investments

Halcyon Asset Management Visium Asset Management

Indus Capital Partners York Capital Management

UK Based Managers Capula Investment Management LLP

Lansdowne Partners

The Children's Investment Fund

AKO

Brevan Howard Asset Management LLP

Cheyne Capital Management

CQS (UK) LLP

Egerton Capital

Marshall Wace LLP

Odey Asset Management

Winton Capital Management Limited

Man GLG

The $5 billion dollar hedge fund club Many of the largest hedge fund managers now available in UCITS

Source: Schroders analysis and HFI data based on US and UK headquartered hedge fund centric managers with $5bn+ AUM data as at 01 January 2015. Those launched UCITS

funds in blue as at 31 May 2016.

75%

20%

9

Performance comparison UCITS vs. offshore hedge funds

Despite limitations, liquid alts can provide similar benefits

to hedge funds

10

Source: HFR as of 30 September 2016

Industry performance

HFRI HFRU

Number of

funds 2,200 500

Regulatory

regime Flexible UCITS

Opportunity set

Index YTD 2016 F/Y2015 F/Y 2014 Annualised

Return

Annualised

Volatility Drawdown Months to Recover

Correlation

to S&P 500 (5

years)

Traditional Hedge Fund HFRI Offshore Hedge Fund

Weighted Composite Index 4.2% -1.1% 3.0% 2.6% 6.4% -20.1% 14 0.85

Liquid Alternatives HFRU UCITS Hedge Fund

Composite Index 0.5% 1.5% 4.7% 1.9% 3.3% -6.3% 10 0.68

-30%

-20%

-10%

0%

10%

20%

30%

2008 2009 2010 2011 2012 2013 2014 2015 2016

HFRI Fund Weighted Composite Index HFRU Hedge Fund Composite Index

Available strategies &

setting a framework

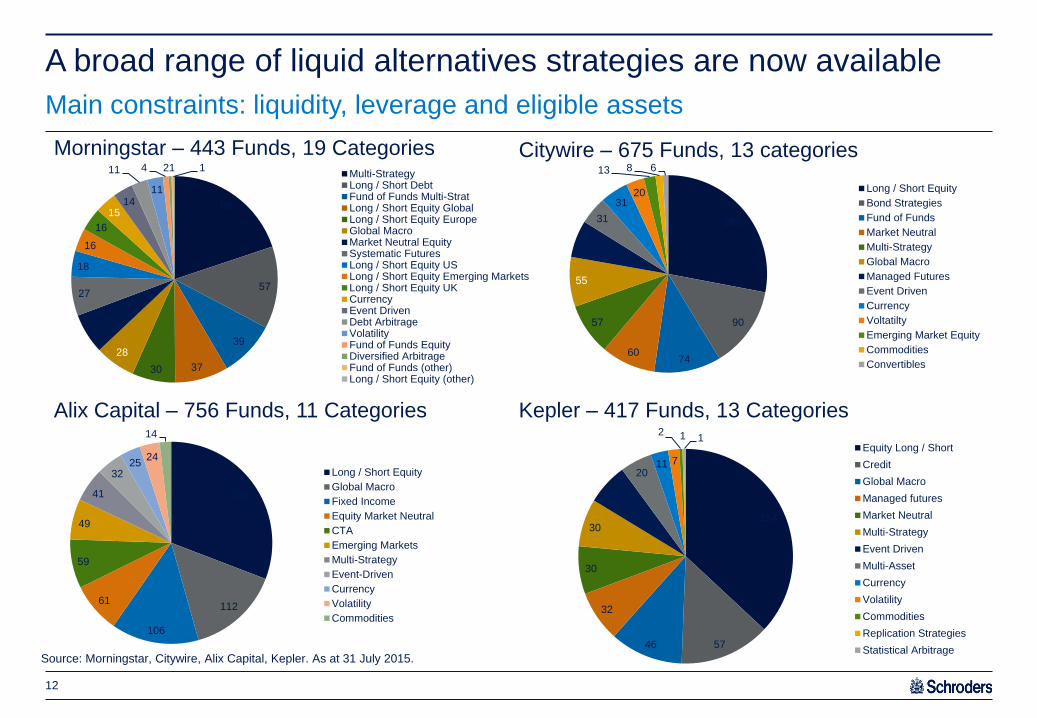

233

112

106

61

59

49

41

32 25

24

14

Long / Short Equity

Global Macro

Fixed Income

Equity Market Neutral

CTA

Emerging Markets

Multi-Strategy

Event-Driven

Currency

Volatility

Commodities

A broad range of liquid alternatives strategies are now available

Source: Morningstar, Citywire, Alix Capital, Kepler. As at 31 July 2015.

12

88

57

39

37 30

28

28

27

18

16

16

15 14

11

11

4 2 1 1 Multi-StrategyLong / Short DebtFund of Funds Multi-StratLong / Short Equity GlobalLong / Short Equity EuropeGlobal MacroMarket Neutral EquitySystematic FuturesLong / Short Equity USLong / Short Equity Emerging MarketsLong / Short Equity UKCurrencyEvent DrivenDebt ArbitrageVolatilityFund of Funds EquityDiversified ArbitrageFund of Funds (other)Long / Short Equity (other)

Morningstar – 443 Funds, 19 Categories

189

90

74 60

57

55

41

31

31 20

13 8 6

Long / Short Equity

Bond Strategies

Fund of Funds

Market Neutral

Multi-Strategy

Global Macro

Managed Futures

Event Driven

Currency

Voltatilty

Emerging Market Equity

Commodities

Convertibles

154

57 46

32

30

30

26

20 11 7

2 1 1 Equity Long / Short

Credit

Global Macro

Managed futures

Market Neutral

Multi-Strategy

Event Driven

Multi-Asset

Currency

Volatility

Commodities

Replication Strategies

Statistical Arbitrage

Alix Capital – 756 Funds, 11 Categories Kepler – 417 Funds, 13 Categories

Citywire – 675 Funds, 13 categories

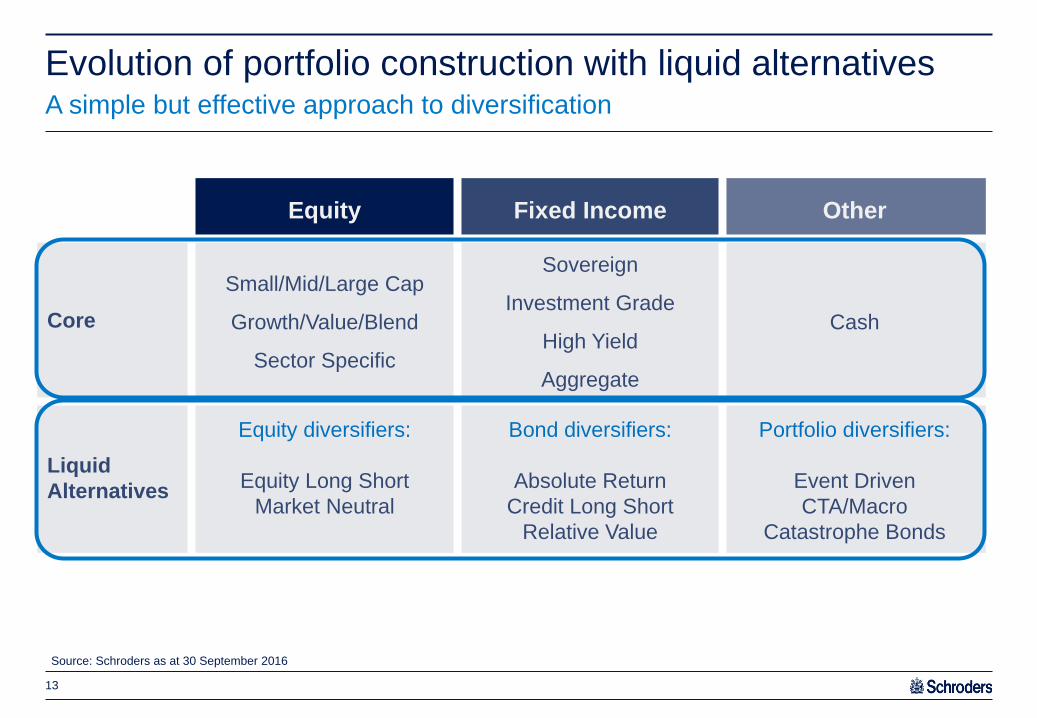

Main constraints: liquidity, leverage and eligible assets

Equity Fixed Income Other

Core

Small/Mid/Large Cap

Growth/Value/Blend

Sector Specific

Sovereign

Investment Grade

High Yield

Aggregate

Cash

Liquid

Alternatives

Equity diversifiers:

Equity Long Short

Market Neutral

Bond diversifiers:

Absolute Return

Credit Long Short

Relative Value

Portfolio diversifiers:

Event Driven

CTA/Macro

Catastrophe Bonds

Evolution of portfolio construction with liquid alternatives A simple but effective approach to diversification

13

Source: Schroders as at 30 September 2016

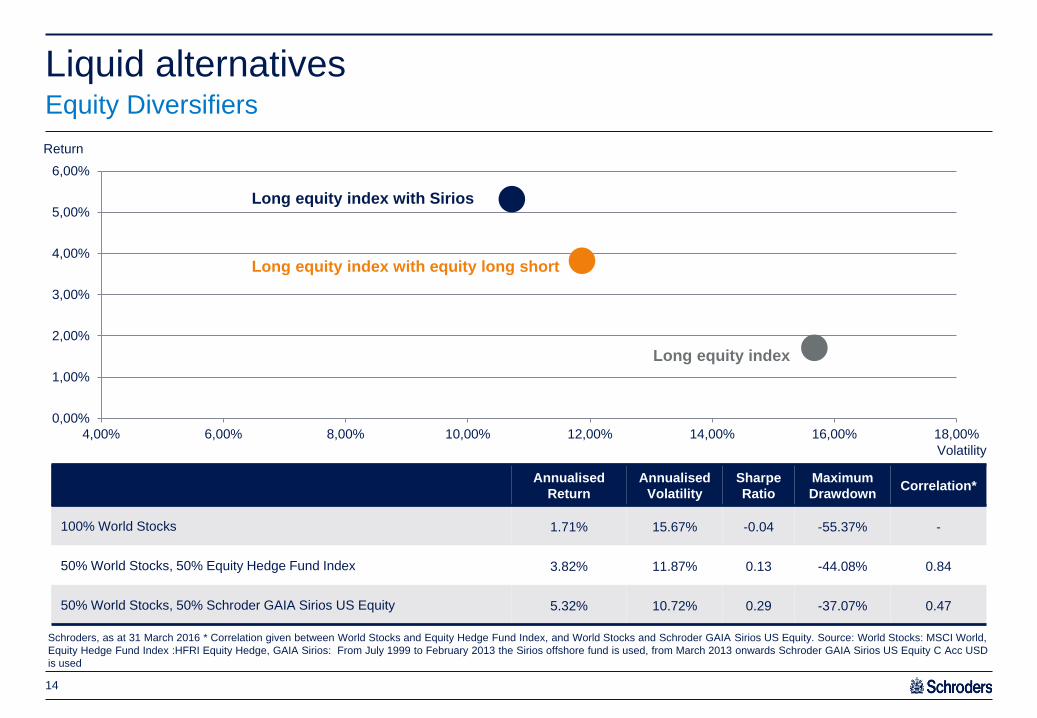

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

4,00% 6,00% 8,00% 10,00% 12,00% 14,00% 16,00% 18,00%

Liquid alternatives Equity Diversifiers

14

Schroders, as at 31 March 2016 * Correlation given between World Stocks and Equity Hedge Fund Index, and World Stocks and Schroder GAIA Sirios US Equity. Source: World Stocks: MSCI World,

Equity Hedge Fund Index :HFRI Equity Hedge, GAIA Sirios: From July 1999 to February 2013 the Sirios offshore fund is used, from March 2013 onwards Schroder GAIA Sirios US Equity C Acc USD

is used

Annualised

Return

Annualised

Volatility

Sharpe

Ratio

Maximum

Drawdown Correlation*

100% World Stocks 1.71% 15.67% -0.04 -55.37% -

50% World Stocks, 50% Equity Hedge Fund Index 3.82% 11.87% 0.13 -44.08% 0.84

50% World Stocks, 50% Schroder GAIA Sirios US Equity 5.32% 10.72% 0.29 -37.07% 0.47

Volatility

Return

Long equity index with equity long short

Long equity index

Long equity index with Sirios

0%

1%

2%

3%

4%

5%

6%

4,00% 4,50% 5,00% 5,50% 6,00% 6,50% 7,00% 7,50% 8,00%

Liquid alternatives Portfolio Diversifiers - CTA

15

Schroders, as at 31 March 2016 *Correlation given between a portfolio of 20% Cash, 40% World Stocks, 40% World Bonds and CTA index, followed by Bluetrend. Source: Cash :USD 1M LIBOR,

World Stocks: MSCI World, World Bonds: Barclays Global Aggregate, CTA Index: Newedge CTA Index, Bluetrend: BlueTrend Fund Limited (Class A USD) inception date was 1 April 2004. The

management fee for Class A Shares was 1.5% from inception to 30 June 2011 and 2% from 1 July 2011 to 31 July 2014.

Volatility

Annualised

Return

Annualised

Volatility

Sharpe

Ratio

Maximum

Drawdown Correlation*

20% Cash, 40% World Stocks, 40% World Bonds 3.59% 7.37% 0.25 -25.97% -

32% World Stocks, 32% World Bonds, 16% Cash, 20% CTA Index 3.62% 6.16% 0.30 -19.24% 0.05

32% World Stocks, 32% World Bonds, 16% Cash, 20% Bluetrend 5.13% 6.81% 0.49 -16.43% 0.12

Return

Traditional portfolio with CTA index

Traditional portfolio

Traditional portfolio with BlueTrend

Thoughts and

considerations for

choosing UCITS

hedge funds

UCITS Hedge Fund vs. Offshore Hedge Fund High level considerations

17

UCITS hedge fund Offshore hedge fund

Prime broker Requirement to have an independent custodian

so

typical prime broker arrangement is not possible

Prime broker

Eligible Assets Prescribed includes by of way of example cash,

transferable securities, derivatives, funds

Flexible

Commodities, Property Excludes commodity futures, limited to equities,

ETFs,

and financial indices

Can also invest in derivatives on individual

commodities, properties, and physical

property/commodities

Borrowing Limited to 10% on a temporary basis Can borrow e.g. up to 200% on a permanent

basis

Leverage 200% global exposure or prescribed VaR limit Flexible

Short sales Short sales not permitted, can only seek short

exposure via derivatives

Short sales permitted

Diversification 5/10/40 Flexible

Minimum dealing/

valuation frequency

Twice monthly (typically weekly) Annually although most monthly or quarterly

Rigorous manager selection process and monitoring Overview

18

Source: Schroders, 30 September 2016

Strategy selection

Investment due diligence

Operational due diligence

Ongoing risk management

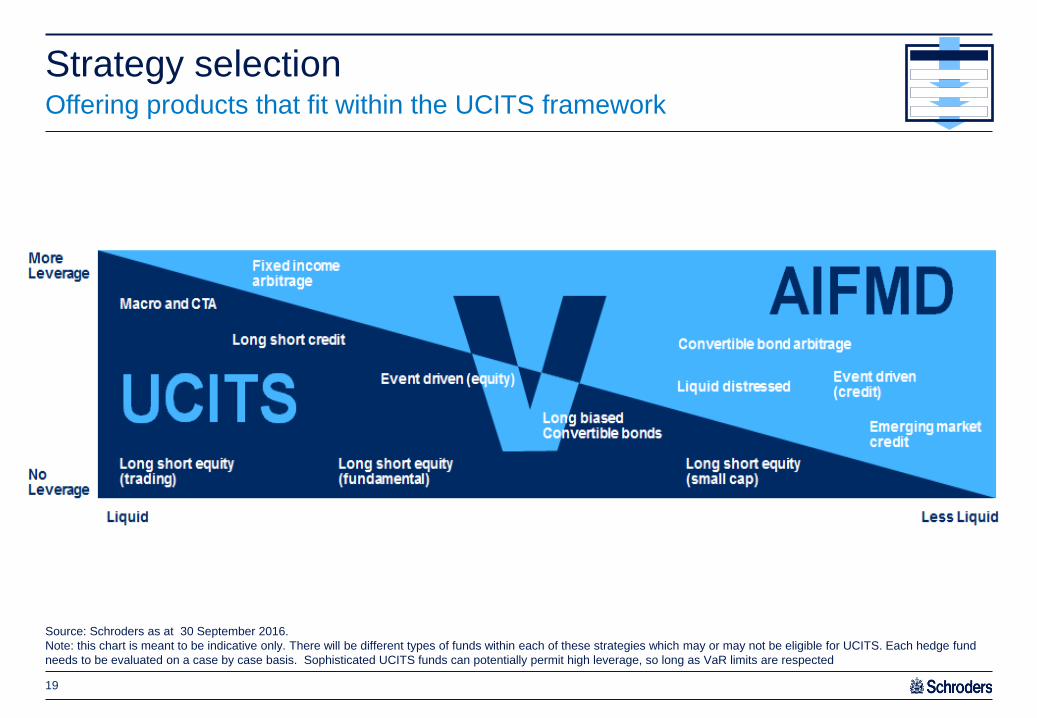

Strategy selection Offering products that fit within the UCITS framework

19

Source: Schroders as at 30 September 2016.

Note: this chart is meant to be indicative only. There will be different types of funds within each of these strategies which may or may not be eligible for UCITS. Each hedge fund

needs to be evaluated on a case by case basis. Sophisticated UCITS funds can potentially permit high leverage, so long as VaR limits are respected

GAIA Investment Committee

Investment manager selection Full due diligence performed based on key requirements for a given strategy

20

Source: Schroders, as at 30 September 2016

Experience

Track record and skill

Investment process

Integrity

Size

Reputation

Investment due diligence

Risk management capabilities

Fit with regulatory requirements

– Investment diversification rules

– Asset eligibility

– Market & liquidity risks

Preliminary regulatory

compatibility assessment

Initial review of available regulatory, marketing, and personnel materials

Full documentation review covering all key business areas

Onsite visit including thorough validation of all points and processes raised in the documentation review

Operational due diligence

Group due diligence Independent group due diligence process

21

Source: Schroders, as at 30 September 2016

Full background check review on entire firm and employees

Initial high level RFI

Key financial and insurance policy verification undertaken

Internal stakeholder review and sign off

Detailed review of:

Organisational structure

Investment risk/Operational risk framework including capabilities of managing a regulated fund

Compliance: Key policies and procedures to be provided

Operation: How a fund is managed in a regulated environment

Full IT/Security/BCP to ensure minimum Schroders/industry best practices

A full review and discussion with the investment manager

On-desk review of end-to-end processes. Testing of processes and output validation

Challenging the RFI responses where appropriate (based on internal review)

Explanation of how GAIA operates and how the Manager will need to adapt to its framework

DD

conclusion

and ongoing

monitoring

Post DD visit, conclusion report issued to senior management

Integration planning and launch of product commences with Lux and Manager

Group policy dictates annual RFI review with an on-site visit every two years

Pre-full

DD review

Full DD and

RFI review Onsite

review

Monthly GAIA risk meetings

Monthly monitoring by Schroder GAIA Investment Committee

Quarterly monitoring by Schroder GAIA II Board

Robust risk management with independent oversight and governance

Source: Schroders, 30 September 2016

Schroder GAIA risk management framework Several layers of risk management oversight for each hedge fund

22

Investment manager risk controls

Pre-trade compliance

Daily reviews

Portfolio limits/risk controls (leverage, liquidity, sector, single position, VaR)

Independent regulatory risk and compliance monitoring

Post-trade compliance monitoring

Investment risk monitoring: counterparty risk, liquidity, global exposure, VaR

Independent daily risk oversight

Performed by specialist hedge fund analysts in conjunction with multi asset risk team

Investment guidelines/stress tests/style drift/exposures/performance

Operational due diligence

Initial detailed operational due diligence

On-going monitoring of original due diligence findings

Annual update of initial report, biennial formal update including on site visit

Governance meetings

NGA

Extensive global and local distribution support Over 250 distribution professionals servicing clients in >30 countries

23

Source: Schroders, as at 31 August 2016

US offshore Netherlands

Denmark

Germany

Switzerland

Austria

UK

Luxembourg

Spain

Italy

Portugal

France

Sweden

Finland

Norway

Greece

Belgium

Ireland China

Hong Kong

Korea

Japan

Singapore

Taiwan Brazil

Colombia

Chile

Peru

Panama

Uruguay

Argentina

Mexico

Israel

Dubai

Targeted fund information for investors

globally

Active support for global intermediary partners

Comprehensive marketing information

Fund launch video

Dedicated website

Monthly factsheets

Quarterly letters

Quarterly webcasts

Peer analysis

Specialised client reports

Explanatory sales documents

Sales support

Transparent client-friendly marketing materials Ensures investors are well informed

24

Source: Schroders, as at 30 September 2016

Introducing

Schroder GAIA

Launch date Manager Fund Strategy Geographic focus AUM (USD)

2 Mar 2016 Schroder GAIA II NGA Turnaround Distressed Predominantly US 12m

Schroder GAIA

Schroder GAIA and Schroder GAIA II Overview of sub-funds

26

Total AUM 5,159m Source: Schroders as at 30 September 2016 *Hard closed, but subject to Capacity Restricted Dealing.

Schroder GAIA II

Launch date Manager Fund Strategy Geographic focus AUM (USD)

25 Nov 2009 Schroder GAIA Egerton Equity* Equity long short Global 1,377m

27 Feb 2013 Schroder GAIA Sirios US Equity Equity long short Predominantly US 1,366m

21 Oct 2013 Schroder GAIA Cat Bond Catastrophe Bonds Global 1,099m

25 Jun 2014 Schroder GAIA Paulson Merger Arbitrage Merger Arbitrage US, Canada and Western Europe

503m

17 Jun 2015 Schroder GAIA BSP Credit Credit long short Predominantly US 35m

9 Dec 2015 Schroder GAIA BlueTrend Trend Following Global 350m

6 Jul 2016 Schroder GAIA Indus PacifiChoice Equity long short Pan Asian including

Japan 92m

24 Aug 2016 Schroder GAIA Two Sigma Diversified Equity Market Neutral /

Systematic Macro Predominantly US 325m

Independent money management firm based in London, founded in 1994

by John Armitage

Experienced investment team of 16 professionals

Employee investments account for c. 7% of total firm assets

Key to success is research-intensive stock picking. ‘Bottom-up’ approach

to stock selection creates a portfolio that is dynamic, eclectic, and

uncorrelated

The strategy aims to deliver equity type returns with less volatility than the

market over the medium to long term

Egerton Capital Limited: AUM $14.6bn Performance objective

Schroder GAIA Egerton Equity Equity long short fund with significant outperformance over time

27

Source: Schroders and Egerton as at 31 August 2016. *Performance shown for chain-linked track record of Egerton long short Equity B1 USD since its inception in September 1994. Egerton’s

offshore fund has been used from December 1994 to November 2009. From December 2009 onwards Schroder GAIA Egerton Equity C Acc USD Hedged has been used. MSCI World Index is used.

Performance is shown net of fees, NAV to NAV.

Performance analysis (Egerton’s equity long short strategy*)

Fundamental long short equity fund, typically long-biased

Straightforward, liquid strategy investing predominantly in large cap equities

Opportunistically invest in corporate bonds

Uses little or no leverage

Reduces volatility through the use of alpha shorts, hedges (e.g. index put

options) and cash

Avoids large drawdowns

Fund key features

Strategy* Index

Annualised return 13.3% 6.7%

Annualised volatility 9.6% 14.0%

Sharpe ratio 1.1 0.3

Maximum drawdown -28.3% -50.8%

Portfolio Manager John Armitage, Egerton

Inception date 25 November 2009

Base currency EUR

Institutional share class fee 1.25%/20%

Liquidity Weekly (on Wed) and month end

0%

500%

1000%

1500%

2000%

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

14

20

15

Schroder GAIA Egerton Equity Strategy MSCI World

Egerton Long/Short vs. Schroder GAIA Egerton Equity Similarities and differences between GAIA Egerton UCITS and Cayman fund

28

The Egerton Long/Short strategy can operate comfortably within the UCITS framework. However, there will be performance divergence through time as a result of the differences

outlined above

Source: Sirios as at 30 September 2015

Egerton Long/Short Schroder GAIA Egerton

Equity

Investment manager John Armitage, Egerton Capital

Investment strategy Market directional equity long short

Portfolio liquidity Liquid portfolio focussed on mid/ large cap securities

Leverage/ gross

exposure Max 150%

Typical number of

positions

Longs 40 – 60 positions

Shorts 60 – 100 positions

Long exposure

(single securities) Mainly physical securities/ occasionally synthetic

Short exposure

(single securities)

Mainly physical

securities/occasionally

synthetic

Always synthetic (UCITS

requirement)

Options Occasionally used for hedging (single name and indices)

Institutional fees 1.00%/15% performance fee 1.25%/15% performance fee

Dealing frequency Monthly (30 days notice) Weekly (3 days notice)

Minimum investment $1m $500,000

90

100

110

120

130

140

150

160

170

180

190

nov/09 nov/10 nov/11 nov/12 nov/13 nov/14 nov/15

Schroder GAIA Egerton Equity C Acc EUR

Egerton European Equity Fund Ltd - Class B

Globally renowned hedge fund founded by John Paulson in 1994

Strategies include merger arbitrage, event-driven, credit and special situations’.

The merger funds have one of the longest and most successful track records, compounding at 11.2% over the last 22 years**

Proven team of 54 experienced investment professionals consisting of both sector and M&A transaction specialists

The fund targets an absolute return of 8 – 10% net of fees

Paulson & Co. AUM $11.1bn* Performance objective

Schroder GAIA Paulson Merger Arbitrage Superior risk-adjusted returns that are uncorrelated to the broader markets

29

Source: Schroders as at 31 August 2016. * Paulson as at 1 September 2016. **Inception July 1994 . Performance shown for Paulson Partners LP from July 1994 until June 2014 and Schroder GAIA

Paulson Merger Arbitrage C Acc USD has been used from July 2014 onward. Performance is shown net of fees, NAV to NAV.

Performance analysis (Paulson Partners LP**)

An absolute return focused merger arbitrage UCITS fund looking at

opportunities in US, Canada and Europe

Predominantly listed equities with opportunistic exposure to credit

Aims to deliver returns in all market cycles by using different strategies. ie;

cash/stock deals, topping bids, bankruptcies, restructurings

High potential for alpha generation given sophisticated investment approach

seeking unique and complex merger situations

Capital preservation, low correlation to markets and low volatility – just 2

down years since inception in 1994 and returned +7.9% in 2008

Portfolio Managers John Paulson, Andrew Hoine, Jim Hoffman

Inception Date 25 June 2014

Base Currency USD

Institutional share class fee 1.25%/20%

Liquidity Weekly (on Wed) and month end

Ann. Ret. Ann. Vol. Correlation to Paulson

Paulson Merger Arbitrage** 11.2% 9.5% 1.00

S&P500 9.5% 14.9% 0.24

HFRI Merger Arbitrage

Index 7.1% 3.5% 0.43

Fund key features

0%

200%

400%

600%

800%

1000%

1200%

1400%

1994 1996 1998 1999 2001 2003 2005 2006 2008 2010 2012 2013 2015Schroder GAIA Paulson Merger ArbitrageStrategy

Paulson Partners LP vs. Schroder GAIA Paulson Merger Arbitrage

Main similarities and differences between GAIA Paulson UCITS and US Onshore fund

30

Paulson Partners LP Schroder GAIA Paulson Merger

Arbitrage

Investment manager John Paulson, Paulson & Co.

Investment strategy Merger Arbitrage

Portfolio liquidity Liquid portfolio focussed on mid/ large cap securities

Leverage/gross

exposure

Leverage of up to 1.5x of the long

market value in the portfolio and 2.0x

of the long plus short market value in

the portfolio

200%

Typical number of

positions 30 – 60, diversified across geography, sector and instrument type

Long exposure

(single securities)

Mainly physical

securities/occasionally synthetic

Mainly synthetic

securities/occasionally physical

Short exposure

(single securities)

Mainly physical

securities/occasionally synthetic

Always synthetic (UCITS

requirement)

Asset classes

Predominantly listed equity with

opportunistic

exposure to credit

Bank debt, commodities and

private/restricted equity are not

permitted within UCITS

Concentration Issuer Size (at cost) <12%

Issuer Size (at market) <18% Restricted by UCITS 5/10/40 rule

Fees 1.0%/20% performance fee 1.25%/20% performance fee

Dealing frequency Quarterly (60 days notice) Weekly and month end (3 days

notice)

Minimum

investment $5m $500,000

Source: Schroders and Paulson & Co. as at 31 July 2015

65

70

75

80

85

90

95

100

105

110

jun/14 dez/14 jun/15 dez/15 jun/16

Schroder GAIA Paulson Merger Arbitrage C Acc USD

Pauslon Partners LP

-50%

0%

50%

100%

150%

200%

250%

300%

Jan-0

4

Aug

-04

Ma

r-0

5

Oct-

05

Ma

y-06

Dec-0

6

Jul-0

7

Fe

b-0

8

Sep

-08

Apr-

09

Nov-0

9

Jun-1

0

Jan-1

1

Aug

-11

Ma

r-1

2

Oct-

12

Ma

y-13

Dec-1

3

Jul-1

4

Fe

b-1

5

Sep

-15

Apr-

16

BlueTrend Barclays Global Aggregate Bond Index

HFRI Fund Weighted Composite Index MSCI WorldInvestment team Head Leda Braga

Inception date 9 December 2015

Base currency USD

Institutional share class fee 1.50%/20%

Liquidity Weekly (on Wed) and month end

Systematica founded in January 2015 after a decade of experience within

BlueCrest Capital Management

Systematica manage total assets of $9.5bn, with $7.4bn in their trend-

following strategy*

Investment team headed by Leda Braga, former President and Head of

Systematic Trading at BlueCrest Capital Management

The fund aims to provide capital growth by adopting a pure systematic trend

following strategy, across global markets, based on quantitative signals with

multiple time horizons. It targets returns of 10-15%.

Investment Manager: AUM $9.5 bn* Performance objective

Schroder GAIA BlueTrend Diversified Systematic Macro Trend Following Strategy

31

Source: Systematica Investments and Schroders, as at 31 August 2016. * Systematica Investments, as at 1 August 2016. AUM data based on estimates, and is subject to change. Managed by BlueCrest Capital Management Group from inception

to 1 January 2015 when Systematica Investments Limited (acting in its capacity as general partner of Systematica Investments LP) became the investment manager. **BlueTrend strategy refers to an SMA from January 2004 to March 2004 and

BlueTrend Fund Limited (Class A USD) from 1 April 2004 to 31 December 2015. From 1 January 2016 onwards performance is provided for Schroder GAIA BlueTrend C Acc USD. Performance is shown net of fees, NAV to NAV.

Performance analysis (BlueTrend strategy**)

Diversified systematic trend following fund, launched in April 2004

Extremely competitive track record with average annualised return of 10%,

with 14% annualised volatility

Positive in 9 out of the past 10 years

Uncorrelated returns over time/delivered positive returns in both up and

down markets

Performed well in periods of prolonged market downturns like 2008

Trades the most liquid assets among equity, currency, commodity and

fixed income

Strategy

Annualised return 9.8%

Annualised volatility 14.1%

Maximum drawdown -22.1%

Fund key features

BlueTrend vs. Schroder GAIA BlueTrend

Main similarities and differences between GAIA BlueTrend UCITS and offshore fund

32

BlueTrend Master Fund Limited Schroder GAIA BlueTrend

Investment

manager

Systematica Investments Limited (acting as a general partner of

Systematica Investments LP)

Investment

strategy Trend Following

Domicile Cayman Islands Luxembourg

Portfolio liquidity Liquid and diversified portfolio across 200 markets

Leverage/gross

exposure 600% – 2,300%

Long/short

exposures Futures

Asset classes Commodities, FX, Bonds, Equity Indices

Government

concentration No restrictions

Government exposure

replicated through IRS (no

govt. exposure over 100%

per UCITS regulations)

Fees 1.50% / 20% performance fee* 1.50% / 20%** performance

fee

Dealing frequency Monthly (30 days’ notice) Weekly and month-end (3

days’ notice)

Minimum

investment US$1m US$500,000*

*For investments up to $75 million. **C share class. Please note these are the stated management and performance fees and do not include other administrative fees.

Source: Schroders and Systematica Investments, as at 30 September 2016.

85

90

95

100

105

110

115

jan/16 mar/16 mai/16 jul/16 set/16

Schroder GAIA BlueTrend C Acc BlueTrend Offshore

Conclusion

Source: Schroders, September 2016

33

Liquid Alternatives represent a new and rapidly growing asset class for investors

Whilst UCITS has a number of constraints, many hedge fund strategies can be run

comfortably within the framework

Long short strategies make sense now to help diversify client portfolios

Investors should consider blending long only strategies together with long short

strategies, and include alternative funds within the core portfolio as opposed to an

alternatives bucket

Fund selectors should focus on established managers that have a proven track record

of producing consistent risk adjusted returns

Emphasis should be on strategies with uncorrelated returns streams, reduced volatility

and proven downside protection

Schroders offers a broad range of liquid alternative funds including a leading platform

of external managers

Two Sigma Diversified simulated returns Methodology

34

The return stream presented in the next slide seeks to reflect the simulated performance of a hypothetical portfolio focused on liquid strategies in US equity,

futures and FX markets for the period referenced. Specifically, the hypothetical portfolio is constructed by allocating (a) 15% of the portfolio’s capital in support of

a managed futures portfolio (the “Macro" portfolio) and (b) 85% of the portfolio’s capital in support of an equity market neutral portfolio (the "Equity" portfolio, and

together with Macro portfolio, the “Adjusted Results”). The simulated performance of the hypothetical portfolio were then each further modified on a pro-forma

basis to adjust performance and volatility based on certain historically-perceived variables: (i) volatility was adjusted by scaling the simulated performance of the

hypothetical portfolio in a given year such that volatility is presented half-way between the hypothetical volatility result and targeted volatility (8.0%) and (ii)

performance was discounted by subtracting 75% of the average monthly simulated performance of the Adjusted Results. In each case, “Gross Returns” of Class

C Shares are gross of fees and estimated operating expenses and net of estimated trading expenses. "Net Returns” of Class C Shares are net of a hypothetical

1.4% annualized management fee accrued and paid monthly in advance and a hypothetical 20% performance fee (or allocation) accrued monthly and paid

annually (subject to standard high water mark, where applicable), but are gross of estimated operating expenses and net of estimated trading expenses. Please

note that fees vary by share class and additional fees and fund expenses apply.

The simulated strategy's settings or investment methodology may not be representative of any future portfolio due to, among other things, the addition or deletion

of trading models, changes in optimization settings, changes in model weightings and other variables. The simulated and/or pro-forma performance results shown

are for illustration purposes only as part of an ongoing business discussion with a sophisticated party and should not be relied upon when making an investment

decision. Certain factors will likely cause the simulations to generate better performance than live trading of the associated strategy. These factors (which are

further discussed on the last page of this report) include, but are not limited to, the following: (i) the simulations benefit from the use of the most recent models,

research and optimizer settings used by Two Sigma (as defined below), all of which have been tested historically and in most cases have been fit to a period

similar to the one shown and, therefore, benefit from portfolio settings that have been found to be optimal for such time period (e.g., more risk is taken in the

simulations than would otherwise likely have been taken during periods of high volatility or deemed systemic risk); and (ii) the lack of operating expenses which, if

included, would degrade performance in a compounded fashion over time. The last page of this document provides important details regarding these simulated

performance statistics, which are subject to the explanations and disclaimers discussed therein. Past performance, especially simulated performance, is not an

indicator or guarantee of future results

The simulated performance results shown above are for illustrative purposes only and were prepared for the recipient as part of ongoing discussions. Two Sigma Advisers, LP (the “Investment Manager”) has worked with its affiliated investment adviser, Two Sigma Investments, LP (together with the Investment Manager, "Two Sigma") to engineer certain software that attempts to simulate the trading patterns that would have resulted had the Investment Manager utilized certain quantitative trading models over the period of January 1, 2005 through the date of this report. These simulated results should not be relied upon.

These simulated results are based largely on historical information available from certain proprietary databases of Two Sigma compiled, in part, from multiple commercially available data sources, as well as certain assumptions made by Two Sigma about, among other things, trade execution, financing and market impact costs. While Two Sigma has expended considerable efforts attempting to clean and cross-check these inputs, Two Sigma cannot and has not independently verified the accuracy or completeness of such information, nor have the results of the simulation been independently verified or audited. Should any information used in the above simulation prove to be inaccurate, the simulated results themselves may be inaccurate.

In addition, all simulated results have many inherent limitations. In particular, simulated results are often prepared with the benefit of hindsight, meaning models utilized in these simulations may have been developed explicitly with the benefit of data from the time period covered by these simulations. Additionally, simulated results do not involve financial risk or reflect actual trading under actual market conditions and do not reflect the ability to withstand losses or to adhere to an investment program despite trading losses. The simulation was also performed using only a finite number of variables. The actual performance of any trading program the Investment Manager ultimately elects to employ in the future will from time to time be dependent on, and influenced by, any number of factors, many of which (i) have not been taken into account in performing the simulation; (ii) are inherently difficult to quantify; and (iii) are outside the Investment Manager's control. Due to the nature of simulations, it is likely that actual trading performance will be materially lower than the simulated performance set forth herein.

Simulations were run using Two Sigma's tradable universe of global futures, currencies, and equities that met proprietary inclusion criteria intended to foster, among other goals, adequate liquidity and issuer uniqueness, as well as a number of other factors.

The tradable universe of global futures, currencies and equities, as well as trading models used by Two Sigma have evolved and are likely to continue to evolve over time. There can be no assurance that the trading program pursued by the Investment Manager on behalf of any of its investment products in actual trading will be the same or substantially the same as the ones that were subjected to the above simulation.

Future performance may be affected by existing and/or new events or factors, which may or may not have played any material role in the past. Therefore no assurance or guarantee can be given that the actual trading results achieved using those strategies and/or models employed during this simulation, and/or others that are being used and/or may be used in the future, are or will be as successful and/or achieve the same results as those presented above. Past performance, especially simulated performance, is not an indicator or guarantee of future results.

The results of the simulation are being provided to you by the Investment Manager solely to assist you in considering your potential interest in making an investment in a potential future investment product to be managed by the Investment Manager.

In the event of any conflict between this document and the prospectus, the prospectus shall prevail. The securities discussed herein shall not be offered or sold, nor shall there be any solicitation of any offer to buy such securities, in any jurisdiction in which such offer, sale or solicitation would be unlawful until the requirements of the laws of such jurisdictions have been satisfied.

An investment in any investment product is speculative and involves significant risk, including the risk of a total loss of capital. Opportunities for withdrawal or transfer of interests in a strategy may be limited and therefore an investor may not have access to its capital when it desires.

This information is being furnished to the recipient on a confidential basis, is not intended for public use or distribution, and by accepting this file, you agree to keep confidential the existence of this document and the information contained herein. The recipient should not disclose, reproduce, distribute or otherwise make available the existence of and/or all or any portion of the information contained herein to any other person (other than its employees, officers and advisors on a need-to-know basis, whom the recipient will cause to keep the information confidential) without Schroders and the Investment Manager's prior written consent.

Important Information regarding simulated returns

35

Risk Considerations

For professional investors and advisers only. This material is not suitable for retail clients.

This document is intended to be for information purposes only and it is not intended as promotional material in any respect. The material is not intended as an

offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or

tax advice, or investment recommendations.

Important Information

The views and opinions contained herein are those of Schroder Investment Management (Switzerland) AG, and may not necessarily represent views expressed

or reflected in other Schroders communications, strategies or funds. This document is intended to be for information purposes only and it is not intended as

promotional material in any respect. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment

recommendations. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. The data has been sourced by

Schroders and should be independently verified prior to further publication or use. No responsibility can be accepted for errors of fact or opinion.

This document does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of Schroder GAIA and Schroder GAIA II (the

“Companies”). Nothing in this document should be construed as advice and is therefore not a recommendation to buy or sell shares. The offering of shares in

certain jurisdictions may be restricted and accordingly persons are required, by the Companies, to inform themselves of and observe any such restrictions.

Subscriptions for shares of the Companies can only be made on the basis of its latest prospectus together with the latest audited annual report (and subsequent

unaudited semi-annual report, if published). The prospectus, the key investor information document(s) for Switzerland (if available), the articles of association, the

annual and semi-annual reports can be obtained, free of charge, at the offices of the Swiss representative, Schroder Investment Management (Switzerland) AG,

Central 2, P.O. Box, CH-8021 Zurich (authorised and regulated by FINMA) and the Swiss paying agent, Schroder & Co. Bank AG, Central 2, P.O. Box, CH-8021

Zurich.

Investments in the Companies entails risks, which are fully described in the prospectus.

The Company has its registered office in Luxembourg and is regulated by the Commission de Surveillance du Secteur Financier.

Past performance is no indication of future fund performance. This depends on the trends in markets, investment returns and exchange rates (if

relevant), and how successful the asset manager is in implementing the investment policy. The performance shown does not take account of any

commissions and costs charged when subscribing and redeeming units. Prices of shares and the income from them may fall as well as rise and

investors may not get back the amount originally invested.

This document is issued by Schroder Investment Management (Switzerland) AG, Central 2, 8001 Zurich For your security, communications may be taped or

monitored.

Third party data is owned or licensed by the data provider and may not be reproduced or extracted and used for any other purpose without the data provider's

consent. Third party data is provided without any warranties of any kind. The data provider and issuer of the document shall have no liability in connection with the

third party data. The Prospectus and/or www.schroders.ch contains additional disclaimers which apply to the third party data.

Important Information

36

This material was prepared by Schroder Investment Management, in response to a request from the client sent to Schroder and should not be understood as an

analysis of any securities, advertising material, offer to purchase or sell, offer or recommendation of any financial assets or investment. The purpose of this

material is exclusively informative and does not include investment objectives, financial conditions or the particular and specific needs of any shareholders or other

investors. The opinions stated in this material pertain to Schroder and may change at any time. The opinions are based on the date of their submission and do not

encompass any fact that may have arisen after this date, hence, Schroder is not compelled to update this material to reflect such provisions after the submission

of the same. This material is for exclusive Financial Intermediary, Institutional and Consultant and should not be used as support material by other individuals.

THIS MATERIAL IS HIGHLY CONFIDENTIAL AND SHOULD NOT BE REPRODUCED OR DISTRIBUTED, ENTIRELY OR PARTIALLY, TO PERSONS

OTHER THAN THE ORIGINAL RECIPIENTS. The Fund and the distribution of the shares of the same are not registered at the Brazilian Securities Commission

"CVM", and therefore do not meet certain requirements and procedures usually observed in public offerings of securities registered with the CVM, with which

investors in Brazilian capital markets may be familiar. For this reason, the access of the investors to certain information regarding the Fund may be restricted.

SCHRODER DOES NOT GUARANTEE PERFORMANCE.

Important information

37