The ICMR (Re)Insurance Specialty Index (RISX)

13

The ICMR (Re)Insurance Specialty Index (RISX) White Paper Insurance Capital Markets Research 04 December 2021 The ICMR (Re)Insurance Specialty Index is an equity benchmark based on publicly listed companies with underwriting subsidiaries in the Lloyd’s of London insurance market (Lloyd’s). It measures their aggregate eq- uity performance, weighted by their premiums written both at Lloyd’s and globally. The index is administered and calculated by Moorgate Bench- marks Ltd, a Morningstar company. Contents About the ‘RISX’ Index 2 About Specialty (Re)insurance 5 About Lloyd’s of London 7 About ESG 9 Methodology 10 Conclusion 11 Licensing 12 About ICMR 12 About Moorgate Benchmarks 12 Disclaimer 13 1

Transcript of The ICMR (Re)Insurance Specialty Index (RISX)

The ICMR (Re)Insurance Specialty Index(RISX)

White Paper

Insurance Capital Markets Research

04 December 2021

The ICMR (Re)Insurance Specialty Index is an equity benchmark basedon publicly listed companies with underwriting subsidiaries in the Lloyd’sof London insurance market (Lloyd’s). It measures their aggregate eq-uity performance, weighted by their premiums written both at Lloyd’s andglobally. The index is administered and calculated by Moorgate Bench-marks Ltd, a Morningstar company.

Contents

About the ‘RISX’ Index 2

About Specialty (Re)insurance 5

About Lloyd’s of London 7

About ESG 9

Methodology 10

Conclusion 11

Licensing 12

About ICMR 12

About Moorgate Benchmarks 12

Disclaimer 13

1

RISX

About the ‘RISX’ Index

The ICMR (Re)Insurance Specialty Index (RISX) index is an equity index benchmarkfor investments within the Lloyd’s of London insurance market (Lloyd’s).

The RISX index measures the equity performance of publicly listed global insuranceand reinsurance companies that control syndicates at Lloyd’s. RISX constituent com-panies are weighted based on their premiums written at Lloyd’s and globally, not ontheir market capitalisation.

The RISX index is the first of its kind to measure the performance of companies muchmore closely associated with specialty and major catastrophe risk than other equityindices, which tend to include life companies and brokers. This means the RISX indexis far closer to describing the performance of diversified alternative insurance assetsthan any other published equity index.

The index was created by Insurance Capital Markets Research (ICMR), the analyticand consulting firm created by the former heads of research and analysis at Lloyd’s.

Two versions of the RISX index are calculated daily by Moorgate Benchmarks Ltd, aMorningstar company, a price return index (ticker: ‘RISX’) and a net total return index(ticker: ‘RISXNTR’). The index is available via the usual platforms, such as Bloomberg,Refinitiv, and www.risxindex.com.

© Insurance Capital Markets Research 2

RISX

Performance Characteristics

Index return and risk statistics at close 2021-12-03

Return (%) Max Drawdown (%)Annualised

return (%)Annualised risk (%)

Index Level 1m 3m 1yr Ytd 3m 1yr 3yr 3yr 5yr 10yr 3yr 5yr 10yr

RISX 2,889.4 -2.9 -2.8 11.5 11.8 6.5 7.5 42.2 0.8 3.9 9.0 21.0 17.3 14.6RISXNTR 4,383.8 -2.9 -2.5 13.7 13.9 6.4 7.3 41.9 2.8 5.9 11.3 21.0 17.3 14.6

The RISX index back test is as far as mid-2006 following Lloyd’s publication of fullGAAP annual accounting financial statements from year-end 2005. The verticalstripes on the chart above represent major insurance and reinsurance claims eventsin excess of US$10bn insured global loss. The reaction of the RISX index to real-time catastrophe events can be seen, with the impact of COVID-19 having the mostsignificant recent negative impact.

Index Characteristics

The following chart compares underwriting performance of the RISX index againstthe reported Pro-Forma aggregate of the Lloyd’s of London market. The metric usedis the insurance industry standard metric of combined ratio, which comprises the to-tal calendar year claims plus the total calendar year costs (both business acquisitioncosts and operating expenses) divided by the calendar year premium receipts.

© Insurance Capital Markets Research 3

RISX

The above chart shows the similarity in combined ratio performance of the reportedPro-Forma aggregate Lloyd’s of London market over the last 15 years when com-pared to the backtest of the RISX index. This is not surprising, given the existence ofthe subscription market, mentioned below in “About Specialty (Re)insurance”, wheremultiple specialty (re)insurance companies share different percentages of the samerisks, whether through their Lloyd’s of London subsidiaries or otherwise, year afteryear.

The peaks in the chart correspond with years in which there were significant catastro-phe claims - 2005 hurricanes Katrina, Rita and Wilma; 2011 Chile earthquake; Thai-land floods and Fukushima earthquake/tsunami; 2017 hurricanes Harvey, Irma andMaria; 2020 hurricane Laura and COVID.

Given the similarity in combined ratios, the RISX index also shows similar return oncapital characteristics to the reported Pro-Forma aggregate Lloyd’s of London mar-ket over a similar time period.

The above chart shows the comparable returns on capital for the RISX index and theaggregate Lloyd’s of London market. The peaks from the previous chart are matched

© Insurance Capital Markets Research 4

RISX

by troughs in this chart for the same reasons.

A further reason for the similarity in returns is the capital efficiency of both Lloyd’sof London and specialty (re)insurance companies. Neither Lloyd’s of London busi-nesses nor specialty (re)insurance companies tend to retain capital on the balancesheet that won’t be used to support future underwriting in the short term. Over time,significant use is made of dividends, special dividends and/or share buy-backs.

Churn within the RISX index over time has typically occurred where a constituentcompany has either sold their Lloyd’s business, either to another constituent com-pany or via a take-private transaction (eg an MBO or private equity acquisition) orwhere a previously private Lloyd’s business has been acquired by a listed specialty(re)insurance company. The following chart shows how the total number of con-stituents in the RISX index has evolved over the course of the backtest.

Currently, over 80% of Lloyd’s of London’s capital is provided by companies repre-sented in the RISX index. These companies’ Lloyd’s subsidiaries also account forover 80% of Lloyd’s total underwriting premium.

About Specialty (Re)insurance

Specialty (re)insurance focuses on large and complex risks, principally commercialproperty, infrastructure, transport and liability risks . It also encompasses reinsur-ance, which is the protection insurance companies themselves purchase to reducetheir aggregation risk from catastrophe, e.g. from hurricane damage claims.

Specialty (re)insurance business tends not to behave like a retail insurance businesswith its large, homogeneous groupings of broadly similar risks, e.g. home or motorpolicies. The underwriting result of specialty (re)insurance business is more volatilegiven the fortuitous nature of larger claims and natural catastrophes

© Insurance Capital Markets Research 5

RISX

The global premium income for commercial insurance and reinsurance is c.USD 1.0 trillion, of which the RISXindex components write c.USD 500 billion annually

The profitability of specialty (re)insurance underwriting is driven by both premiumpricing levels and the frequency/severity of catastrophe claims activity. When pre-mium pricing levels are generally high (a hard market), even the occurrence of somesevere catastrophe claims will not prevent overall profitability. When premium pric-ing levels are generally low (a soft market), the absence of catastrophe claims canstill lead to profitable outcomes. However, the occurrence of catastrophe claims ina soft market can compound capital destruction and balance sheet weakening.

Underwriting return of the aggregated RISX index companies. Years with major catastrophes: 2005 (HurricanesKatrina, Rita, Wilma), 2011 (Canterbury EQ, NZ; Tohoku EQ & tsunami, Japan), 2017 (Hurricanes Harvey, Irma, Maria),2019 (California wildfires), 2020 (COVID, Hurricane Laura)

Successful specialty (re)insurance companies tend towards a diversified portfolio ofrisks, backed up by continual modelling of potential impacts from theoretical catas-

© Insurance Capital Markets Research 6

RISX

trophe claims events. This enables them to understand their balance sheet expo-sures in real time. Because many of the risks underwritten are so large and complex,the vast majority are underwritten by more than one specialty (re)insurance com-pany - the so-called subscription market model. One company will price the wholerisk and will then underwrite a percentage of it, the remainder being submitted toother specialty (re)insurance companies to follow with smaller percentages on thesame terms. In this way, large risks can be underwritten in their entirety by a group ofspecialty (re)insurance companies, not leaving the insurance buyer overly exposedto just one such company. It also means that, over time, differences in underwritingperformance between specialty (re)insurance companies exhibit more gradual shiftsthan sharp swings. This is because these companies often share the same risks yearafter year.

In recent years, these companies’ appetite for certain exposures has been out-stripped by the appetite of certain capital markets investors keen to access cashflows from specific risks. These relate principally to catastrophe bonds.

Many specialty (re)insurance companies hedge their own risk through issuing catas-trophe bonds in the growing Bermuda catastrophe bond market, a market of overUS$100bn of exposure limits. This makes many specialty (re)insurance companiesboth aggregators of risk and traders of risk. Capital markets investors’ interest inthese types of specialty (re)insurance risk is driven by it generally being seen as adiversified asset class with lower correlation to investment market risk.

More comprehensive contextual analyses of specialty reinsurance performance canbe found in the S&P 2020 Global Reinsurance Highlights Report. Those for specialtyinsurance can be found in the Deloitte Insurance Industry Outlook.

About Lloyd’s of London

The Lloyd’s of London market is the leading global speciality insurance and reinsur-ance marketplace, underwriting complex and large risks. Its annual premiums arein excess of £35bn (US$50bn) and it sets global pricing on specialty risk many timesthis amount.

The market comprises over 50 individually capitalised and regulated businesses. Inaddition, there is a policyholder protection fund to which all businesses subscribefunds annually. This is to pay valid claims if any one of the market’s regulated busi-nesses becomes unable to.

Consequently, policies issued are Lloyd’s of London policies, not policies of the indi-vidual businesses. Lloyd’s maintains a single market-wide financial strength ratingfrom each of the largest global rating agencies as well as a network of international li-cences to trade around the world. In over 300 years of continuous operation, Lloyd’s

© Insurance Capital Markets Research 7

RISX

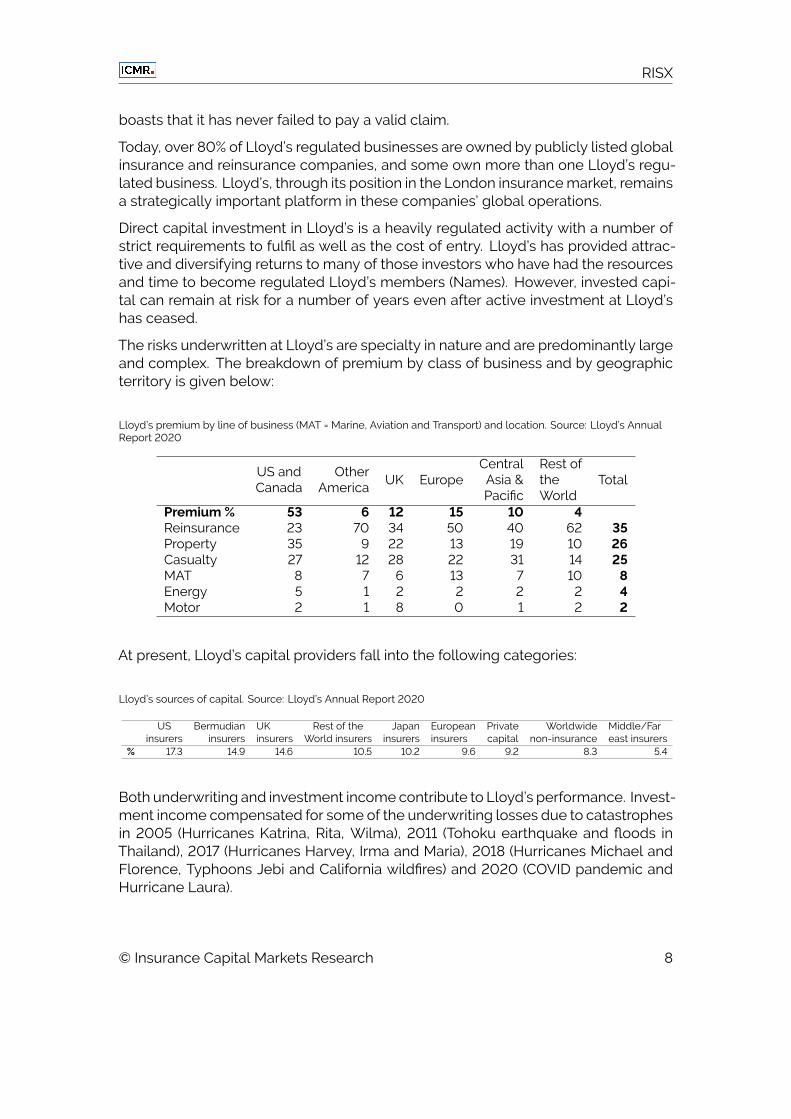

boasts that it has never failed to pay a valid claim.

Today, over 80% of Lloyd’s regulated businesses are owned by publicly listed globalinsurance and reinsurance companies, and some own more than one Lloyd’s regu-lated business. Lloyd’s, through its position in the London insurance market, remainsa strategically important platform in these companies’ global operations.

Direct capital investment in Lloyd’s is a heavily regulated activity with a number ofstrict requirements to fulfil as well as the cost of entry. Lloyd’s has provided attrac-tive and diversifying returns to many of those investors who have had the resourcesand time to become regulated Lloyd’s members (Names). However, invested capi-tal can remain at risk for a number of years even after active investment at Lloyd’shas ceased.

The risks underwritten at Lloyd’s are specialty in nature and are predominantly largeand complex. The breakdown of premium by class of business and by geographicterritory is given below:

Lloyd’s premium by line of business (MAT = Marine, Aviation and Transport) and location. Source: Lloyd’s AnnualReport 2020

US andCanada

OtherAmerica

UK EuropeCentral

Asia &Pacific

Rest oftheWorld

Total

Premium % 53 6 12 15 10 4Reinsurance 23 70 34 50 40 62 35Property 35 9 22 13 19 10 26Casualty 27 12 28 22 31 14 25MAT 8 7 6 13 7 10 8Energy 5 1 2 2 2 2 4Motor 2 1 8 0 1 2 2

At present, Lloyd’s capital providers fall into the following categories:

Lloyd’s sources of capital. Source: Lloyd’s Annual Report 2020

USinsurers

Bermudianinsurers

UKinsurers

Rest of theWorld insurers

Japaninsurers

Europeaninsurers

Privatecapital

Worldwidenon-insurance

Middle/Fareast insurers

% 17.3 14.9 14.6 10.5 10.2 9.6 9.2 8.3 5.4

Both underwriting and investment income contribute to Lloyd’s performance. Invest-ment income compensated for some of the underwriting losses due to catastrophesin 2005 (Hurricanes Katrina, Rita, Wilma), 2011 (Tohoku earthquake and floods inThailand), 2017 (Hurricanes Harvey, Irma and Maria), 2018 (Hurricanes Michael andFlorence, Typhoons Jebi and California wildfires) and 2020 (COVID pandemic andHurricane Laura).

© Insurance Capital Markets Research 8

RISX

The heavily regulated nature of specialty (re)insurance in general, and the Lloyd’s ofLondon market in particular, requires changes of ownership of businesses at Lloyd’sto be vetted and approved. Planned growth within Lloyd’s must also be approved,as Lloyd’s seeks to protect its brand, financial strength rating and global network oflicences.

Since 2003, Lloyd’s internal performance management directorate has monitoredthe performance of the marketplace closely and controls who can own a Lloyd’sbusiness, who can start a business and who can grow its business. This approachhas attracted and encouraged more professional global insurance businesses to par-ticipate and invest in the Lloyd’s market.

Further information on Lloyd’s of London, its history, performance and regulation canbe found at www.lloyds.com.

About ESG

The global specialty (re)insurance industry and Lloyd’s have a long track record incontributing to helping communities and businesses to recover from disaster.

Climate change is and has been a major topic in the global specialty (re)insuranceindustry, through the increasing impact of natural catastrophes on policyholders. Allthe major global (re)insurance companies have initiatives to monitor climate changeand carry out research in modelling its impact. It is core to their business model, butis also a potential growth opportunity, e.g. 40–60% of losses from natural catastro-phes in 2017 were not insured.

In its 2020 ESG report, Lloyd’s reported that over the last decade it provided £145bnin claims payments to customers in their time of need, as well as the insurance andreinsurance critical to propelling the advancement of clean energy and resilient in-frastructure around the world.

© Insurance Capital Markets Research 9

RISX

Furthermore, the report states: *“Importantly, for the first time Lloyd’s are setting tar-gets for responsible underwriting and investment to help accelerate society’s tran-sition from fossil fuel dependency, towards renewable energy sources. Followingfeedback from and in consultation with our market, Lloyd’s will start to phase out in-surance cover for, and investments in, thermal coal-fired power plants, thermal coalmines, oil sands, or new Arctic energy exploration activities.*

From 1 January 2022, Lloyd’s managing agents will be asked to no longer provide newinsurance coverages or investments in these activities. To enable the market to supporttheir customers who aremaking the transition away from these energy sources towardssustainable energy and business models, managing agents will be asked to phase outexisting coverages by 1 January 2030.

*In addition, we have also committed to the phasing out of the market’s and theCorporation’s existing investments in thermal coal-fired power plants, thermal coalmines, oil sands, or new Arctic energy exploration activities by the end of 2025.“*

All companies in the index have recognised the importance of sustainable under-writing and investment, with clear accountability at board level.

The insurance industry is committed to build a more inclusive environment to at-tract and retain the best talents. In recent years, Lloyd’s has also made significantprogress in driving culture change across the market and the industry, including set-ting publicly accountable gender and ethnicity targets.

The governance of insurance companies is overseen by regulators and scrutinisedby rating agencies, while Lloyd’s itself oversees the governance of all business atLloyd’s, setting out clear standards and principles.

Methodology

The RISX index has been created as a tradable equity index. Constituents areweighted by trailing net premium, adjusted where necessary to ensure the trad-ability of each underlying constituent when traded as part of an index portfoliotrade.

The methodology uses triple relative weighting; constituent companies relative toeach other, constituent companies relative to their owned syndicates and, finally,syndicates relative to the Lloyd’s market aggregate. The result is that those con-stituent companies which trade predominantly through their Lloyd’s subsidiaries willhave higher weightings compared to those for whom their Lloyd’s subsidiaries areincidental to their global premium volume. Thus, the RISX index is not based onmarket capitalisation.

The index is reviewed quarterly—in March, June, September and December—with

© Insurance Capital Markets Research 10

RISX

the objective of reflecting change in the underlying ownership and control of busi-nesses in the Lloyd’s of London market in a timely manner, while limiting undue indexturnover. The RISX index is owned and provided by IC Capital Markets Ltd and is ad-ministered, calculated and distributed by Moorgate Benchmarks Ltd, a Morningstarcompany. The index is designed to be compliant with both the IOSCO Principles forFinancial Benchmarks and the UK and EU Benchmarks Regulations.

Moorgate is regulated by the Financial Conduct Authority as a registered benchmarkadministrator under the UK Benchmarks Regulation and by BaFin as a registeredbenchmark administrator under the EU Benchmarks Regulation.

Governance of the index is provided through the Moorgate Benchmarks Index Man-agement Committee, which is responsible for the management and implementa-tion of the methodology rules, their continuing fitness for purpose and any periodicamendments thereto. It is also responsible, in the event of the rules not providing aclear process for the management of any situation, for determining the process tobe followed.

Conclusion

• The RISX index creates the world’s first specialty (re)insurance equity index andis a real time equity benchmark for investments in the Lloyd’s of London insur-ance market

• The index is based exclusively on listed companies’ participation in the Lloyd’sof London insurance market, the oldest continuous specialty (re)insurance mar-ket in the world

• The index is a key/lead indicator of how earnings from this sector accrue frompremium and claims over time, and implies real-time price-to-book value mul-tiples across the Lloyd’s of London insurance market

• The index represents a diversified universe of listed companies (currently 29)that participate at Lloyd’s of London

• The index offers an alternative benchmark for specialty (re)insurance-drivenresults that is more targeted than existing generalist insurance equity indices

• Two versions of the index are calculated daily, a price return index (ticker: ‘RISX’)and a net total return index (ticker: ‘RISXNTR’)

• Lloyd’s and specialty (re)insurers’ earnings depend by and large on the fortu-itous nature of claims (e.g. hurricanes or earthquakes), making it a diversifyingasset within a portfolio

• Climate change is a key focus of specialty (re)insurance• Almost all specialty (re)insurers and Lloyd’s have set targets for responsible

underwriting and investment to help accelerate society’s transition from fos-sil fuel dependency towards renewable energy sources, as part of their ESGcommitments

© Insurance Capital Markets Research 11

RISX

• The global specialty (re)insurance industry is a highly regulated industry andis reliant on maintaining superior financial strength ratings across all the keyrating agencies

Licensing

For information about licensing the RISX index, please contact:

About ICMR

Insurance Capital Markets Research (ICMR, the trading name of IC Markets ResearchLtd), is a specialist analytic and consulting firm.

We provide quantitative research on the global specialty (re)insurance industry. Ourclients are insurance carriers, intermediaries and investors.

One of our core capabilities is the independent assessment of performance and re-turn profiles of insurance entities and portfolios, both within Lloyd’s and globally. Ourresearch focuses on investment strategies and the development of products to ac-cess the global specialty (re)insurance industry and Lloyd’s of London in particular.

Our founders were Lloyd’s former heads of analysis and research who also workedtogether in the capital markets and ILS. ICMR was established in early 2020 andlaunched the RISX Index in 2021: www.risxindex.com.

About Moorgate Benchmarks

Moorgate Benchmarks are experts in designing, managing and calculating indicesfor clients; streamlining operations using leading-edge technology; and implement-ing best practice governance systems to meet EU Benchmarks Regulation.

Moorgate Benchmarks was founded in 2018 and is independent and employee-owned. It has one minority shareholder, ETFS Capital. It offers real-time index calcu-lation and iNav / IOPV calculation services tailored to companies’ needs, regardlessof methodology or timezone used, and regardless of index, related data or under-lying data source used. Using highly flexible and limitlessly scalable infrastructure,Moorgate Benchmarks is authorised under both the UK and EU Benchmarks Regula-tions, and compliant with the IOSCO Principles for Financial Benchmarks. In Septem-ber 2021, Morningstar, Inc. acquired Moorgate Benchmarks Ltd.

© Insurance Capital Markets Research 12

RISX

Disclaimer

This document was prepared by Insurance Capital Markets Research (ICMR, the trading name of IC Markets Re-search Ltd), including all statistical tables, charts, graphs or other illustrations contained herein, unless otherwisenoted. ICMR is not a legal, tax or accounting adviser and makes no representation as to the accuracy or complete-ness of any data or information gathered or prepared by ICMR and contained in this document.

ICMR is not an investment advisor. ICMR is not regulated by the Financial Services Authority.

ICMR does not accept any liability for any loss or damage which is incurred from you acting or not acting as a resultof reading any ICMR publications. You acknowledge that you use the information ICMR provides at your own risk.ICMR publications do not offer investment advice and nothing in them should be construed as investment advice.You should always carry out your own independent verification of facts and data before making any investmentdecisions.

This document is not intended to provide the sole basis for any evaluation by you of any transaction, security orinstrument. The data and analysis provided by ICMR herein or in connection herewith are provided “as is”, withoutwarranty of any kind whether expressed or implied. In no event will ICMR be liable for loss of profits or any otherindirect, special, incidental and/or consequential damage of any kind, howsoever incurred or designated, arisingfrom any use of the analysis provided herein or in connection herewith. The results presented herein are subject tosignificant variability. Any opinions that ICMR publishes may be wrong and may change at any time.

The information contained in ICMR publications is not, and should not be read as, an offer or recommendation tobuy or sell or a solicitation of an offer or recommendation to buy or sell any securities. ICMR publications are not,and should not be seen as, a recommendation to use any particular investment strategy.

Neither ICMR, nor Moorgate Benchmarks nor RISX are associated or affiliated in any way with Lloyd’s of London or

the Society of Lloyd’s or the Corporation of Lloyd’s.

© Insurance Capital Markets Research 13