The High Yield Handbook - QUANTLABS.NETquantlabs.net/academy/download/free_quant... · The High...

211

European High Yield Credit Research January 2006 Our ‘Bottom-Up’ View of European High Yield The High Yield Handbook www.GlobalMarkets.bnpparibas.com Please refer to important information found at the end of the report ■ 2006 European High Yield Market Outlook ■ 81 Credit Snapshots: Recommendations, Financials, Structures, Covenants Part 1

Transcript of The High Yield Handbook - QUANTLABS.NETquantlabs.net/academy/download/free_quant... · The High...

European High Yield Credit Research January 2006

Our ‘Bottom-Up’ View of European High Yield

The High Yield Handbook

www.GlobalMarkets.bnpparibas.com Please refer to important information found at the end of the report

n 2006 European High Yield Market Outlook

n 81 Credit Snapshots:Recommendations, Financials, Structures, Covenants

Th

eH

igh

Yield

Han

db

oo

kJan

uary

2006

AMSTERDAMBNP ParibasHerengracht 4771017 BS AmsterdamNetherlandsTel + 31 20 550 1212Fax + 31 20 625 3921

DUBLINBNP Paribas5 George’s DockIFSCDublin 1IrelandTel + 353 1 612 50 00Fax + 353 1 612 51 00

LONDONBNP Paribas10 Harewood AvenueLondon NW1 6AAUnited KingdomTel + 44 20 7595 2000Fax + 44 20 7595 2555

MUMBAIBNP ParibasFrench Bank Building62 Homji StreetFortMumbai 400 001IndiaTel + 91 22 22642 006Fax + 91 22 22679 710

SHANGHAIBNP Paribas (China) Limited13/F Shanghai Stock Exchange Building528 Pu Dong Road (S)Shanghai 200120People’s Republic of ChinaTel + 86 21 5840 5500Fax + 86 21 5879 1702

BRUSSELSBNP ParibasAvenue Louise, 489B-1000 - BrusselsBelgiumTel + 32 2 518 08 11Fax + 32 2 518 09 34/511 4626

HONG KONGBNP Paribas63/F Two International Finance Centre8 Finance StreetHong KongTel + 852 2909 8888Fax + 852 2865 2523

MANILABNP Paribas30/F Philamlife Tower8767 Paseo de RoxasMakati City 1226PhilippinesTel + 632 885 0252Fax + 632 885 7028

SAN FRANCISCOBNP ParibasOne Front Street23rd FloorSan FranciscoCA 94111U.S.A.Tel + 1 415 772 1370Fax + 1 415 391 3390

TAIPEIBNP Paribas3 - 6/F, 52 Min Sheng East RoadSec. 4, Taipei 105P.O.Box 118-980 TaipeiTaiwanTel + 88 62 27 16 1167Fax + 88 62 27 15 2027

BANGKOKBNP Paribas29th FloorAbdulrahim Place990 Rama IV RoadBangkok 10500Tel + 66 2 636 19 00Fax + 66 2 636 19 33/34/35

GENEVABNP Paribas2 Place de Hollande1211 Geneva 11SwitzerlandTel + 41 22 787 7111Fax + 41 22 787 8000

MADRIDBNP ParibasHermanos Becquer 3PO Box 5078428006 MadridSpainTel + 34 91 745 9000Fax + 34 91 745 8888

PARISBNP Paribas3 rue d’Antin75078 Paris Cedex 2FranceTel + 33 1 42 98 12 34Fax + 33 1 42 98 11 42

SYDNEYBNP Paribas60 Castlereagh StreetSydney NSW 2000AustraliaTel + 61 2 9232 8733Fax + 61 2 9221 3026

ATHENSBNP Paribas94 Vassilissis Sofias Avenue and1 Kerasountos Street115 28 Athensor: P.O.Box 171 58 - 100 24 AthensGreeceTel + 30 210 74 68 000Fax + 30 210 74 86 726

FRANKFURTMainzer Landstrasse 16D-60325Frankfurt am MainGermanyTel + 49 69 71 930Fax + 49 69 71 93219

LUXEMBOURGBNP Paribas10A Boulevard Royal2093 LuxembourgTel + 35 24 64 61Fax + 35 24 64 64 141

NEW YORKBNP ParibasThe Equitable Tower787 Seventh AvenueNew YorkNY 10019U.S.A.Tel + 1 212 841 3000Fax + 1 212 841 3555

SINGAPOREBNP Paribas20 Collyer Quay#05-01 Tung CentreSingapore 049319Tel + 65 6439 5000Fax + 65 6538 4300

CHICAGOBNP Paribas209 South La Salle StreetChicagoIllinois 60604U.S.A.Tel + 1 312 977 2200Fax + 1 312 977 1380

LISBONBNP ParibasAv. 5 de Outubro, 2061050-065 LisbonPortugalTel + 351 21 791 0000Fax + 351 21 795 5616

MILANBNP ParibasPiazza San Fedele 220121 MilanItalyTel + 39 02 72 471Fax + 39 02 86 6388

SEOULBNP Paribas23rd & 24th Floor, Taepyeongno Building310 Taepyeongno 2-ga, Jung-guSeoul 100-767KoreaTel + 82 2 317 1700Fax + 82 2 757 2530

TOKYOBNP ParibasTokyo Sankei Building20th Floor1-7-2- Otemachi, Chiyoda-kuTokyo 100-0004JapanTel + 81 3 5290 1000Fax + 81 3 3529 1120

Part 1

Thursday 19th January 2006Renaissance Chancery Court Hotel252 High Holborn London WC1V 7EN

Annual

High YieldConference

The High Yield Handbook ⎪ January 2006

3 European High Yield Research

Introduction Our 2006 High Yield Handbook is similar to the 2005 version but with an increased number of credits covered and the addition of our 2006 Market Outlook. In 2005, we expanded our single-name research coverage to comprise roughly 90% of the European market in the BB-CCC spectrum while at the same time focussing increasingly on structural and technical factors affecting price action. Notwithstanding the current market trend, our analyses and publications remain fundamentally-driven, involving detailed company and sector assessment and frequent dialogue with issuers and investors.

A glance through the pages that follow suggests that the European High Yield market is alive and well. Investors in European high yield have enjoyed 3 consecutive years of positive returns; despite the increasingly LBO-dominated new issuance, the European market has never seen the diversity (in ratings and sectors) it currently enjoys and the number of market participants (mutual funds, hedge funds, underwriters) continues to reach new highs. Moreover, despite all the talk of the shortening economic cycles this credit cycle appears to be moving forward arduously (or mercifully) slowly. Our bottom up assessment of the credits in the market gives us little cause for panic; conversely, we find it hard to find a significant number of bad apples.

All this good news would suggest that the market is primed to disappoint soon, and looking at the balance of risk and valuations, risk aversion would not be an unreasonable reaction. Credit spreads are not far from their all time lows of early 2005 and by any measure absolute yields are dismally low. The current market population is dominated by the 2003-2005 vintages whose successful performance leaves the majority of bonds dangerously high in price terms, when considering the likelihood of increasing European government bond yields and the picture-perfect execution implied by credit spreads. Given the slim pickings, investors will be increasingly dependent on new issue performance to earn returns respectable enough to warrant exposure to junk-rated credit.

The environment therefore seems opportune for a slow but steady separation of high and low quality credit, and investors will be rewarded by monitoring companies and managements closely. To that end, we hope this publication is a useful resource.

Aizaz Shaikh Head of European High Yield Research

The High Yield Handbook ⎪ January 2006

4 European High Yield Research

European High Yield � 2006 Outlook Executive Summary In 2006, we expect European high yield to post a total return in the 4-5% range, based on the development of a number of scenarios.

A downside case sees a significantly higher number of stressed credits, as well as materially reduced liquidity in the credit markets, in which scenario we would expect total returns to be closer to 0-2%.

In our base case, we see little shift in European default rates, though an increase in corporate financial risk should result in a higher number of �stressed� credits, causing greater credit differentiation than we saw in the 2003-2005 period.

Our view is underpinned by a continuing environment of stable credit quality in the broad-based population of European HY bonds, non-threatening macro-economic factors and balanced supply/demand characteristics in the high yield bond market.

Key Risk Factors ! European 5-year government yields increasing beyond the current 50bp

expectation, causing a reversal in liquidity. Though typically less sensitive to government rates, extension risk (duration) is significant in the current High Yield market.

! Default or stress in benchmark situations. A GM bankruptcy or cracking of a significant or recent LBO would fundamentally alter the current risk appetite for credit.

Q1 2005 Spreads: The Bottom of the Cycle

0 %

1 %

2 %

3 %

4 %

5 %

6 %

2002-Q1 2002-Q3 2003-Q1 2003-Q3 2004-Q1 2004-Q3 2005-Q1 2005-Q3bp

200 bp

400 bp

600 bp

800 bp

1,000 bp

1,200 bp

1,400 bp

Quarterly High YieldDefault Rate (global)(LHS)

10 y Euro GovernmentBenchmark Yield (LHS)

Eurozone GDP growth yoy (LHS)

� High Yield OAS Spreads (RHS)

Source - BNP Paribas, Ecowin

Aizaz Shaikh [email protected] +44 20 7595 8607 Tran Dang, CFA [email protected] +44 20 7595 8291

The High Yield Handbook ⎪ January 2006

5 European High Yield Research

2006 Outlook After the third consecutive year of positive returns for European High Yield investors, we are �going out on a limb� to forecast a low single-digit (4�5%) return year for 2006. Our base case scenario envisions 50bp in average High Yield credit spread widening and 5-year government rates increasing by 30bp by year end, but still positive total return from both High Yield credit and government bonds (comparatively our investment grade strategists anticipate negative returns from investment grade credit).

It is important to note that based on the average running yield in European High Yield of 6.5% (6.7% unconstrained), at year-end 2005 the scenario highlighted above would result in an total return in the low 3% range if investors were to hold a current market neutral position through to year-end 2006 (we have estimated an additional 1�1.5% total return from new issues in 2006 to reach the 4-5% target). The low absolute return likely from the existing population of bonds should not only force greater demand for new issues but also intensify speculation at the higher yielding portions of the market. Given a likely environment of slow but steady credit deterioration, we anticipate these factors will create higher volatility, more trading opportunities and significant credit separation on performance and relative value.

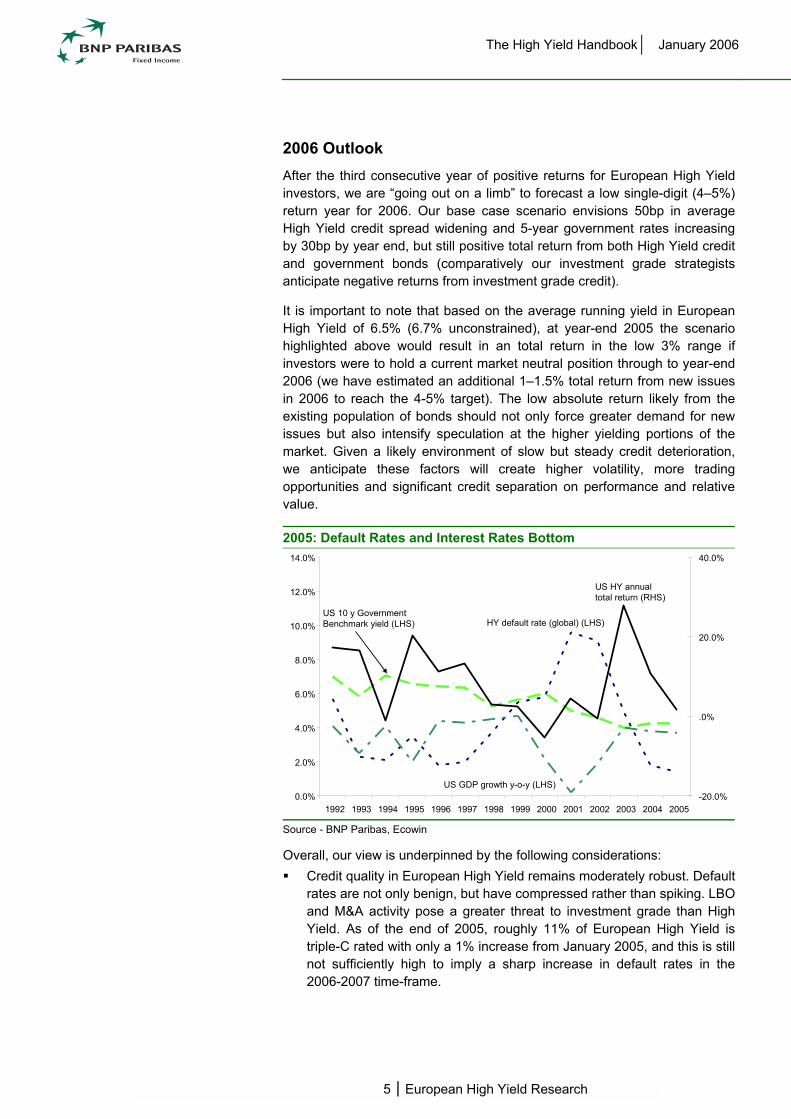

2005: Default Rates and Interest Rates Bottom

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005-20.0%

.0%

20.0%

40.0%

HY default rate (global) (LHS)US 10 y GovernmentBenchmark yield (LHS)

US GDP growth y-o-y (LHS)

US HY annualtotal return (RHS)

Source - BNP Paribas, Ecowin Overall, our view is underpinned by the following considerations: ! Credit quality in European High Yield remains moderately robust. Default

rates are not only benign, but have compressed rather than spiking. LBO and M&A activity pose a greater threat to investment grade than High Yield. As of the end of 2005, roughly 11% of European High Yield is triple-C rated with only a 1% increase from January 2005, and this is still not sufficiently high to imply a sharp increase in default rates in the 2006-2007 time-frame.

The High Yield Handbook ⎪ January 2006

6 European High Yield Research

! Eurozone macroeconomic factors are not threatening. In an environment of mild economic (GDP) growth, central bank action and inflation worries have been underwhelming and in Europe these factors do not pose a major hazard.

! Supply and Demand factors are generally in-line, with the imbalance primarily reflecting a lack of supply. While LBO volume is high, corporate refinancing has been muted, largely because much of this activity has been completed over the last 3 years of healthy credit market conditions. While the market expects a fat first quarter of new issuance volume (roughly �11bn), the significant bond maturities in 2006 (roughly �10bn) should provide a counterbalance. This stated, as deal size is rapidly increasing and buyouts increasingly unpredictable, forecasting new issue volume beyond 1-2 quarters is difficult.

While this represents our base case, we note that a combination of the following downside scenarios could contribute to a negative return year:

! Minor increase in the default rate but significant change in risk aversion: A GM/GMAC default coupled with a �cracking� of any of the major leveraged structures (Wind, Basell, Rexel, WDAC, KDG, NTL) could push average total return into negative territory for market-weighted investors.

! Credit market liquidity dries up and risk aversion increases: Less likely, but harder to predict and potentially more dangerous, a macro shock, either oil, inflation- or rates-related could remove the ubiquitous liquidity that has driven credit spreads to tight levels.

The High Yield Handbook ⎪ January 2006

7 European High Yield Research

Valuations and Returns Away from a broad-based deterioration in credit quality, the twin dilemmas facing High Yield investors today are the limited risk premium (spreads) for non-investment grade credit and the low absolute return. While we are somewhat concerned by the tightness of spreads, and do anticipate some spread widening, we are more troubled by the low absolute yield levels. Not only are the low yields problematic ahead of what could be more than just a brief rate increase cycle, but it could also pose a problem as capital moves to better rewarding assets such as equities, in a stronger economic environment, or higher in the capital structure (loans and crossover credit) in a deteriorating environment.

In 2005 through 1 December, European High Yield returned 5.9% in a year of modest spread tightening and stable credit quality. While 2005 was a subdued year for High Yield investors in Europe, from the record 30% in 2003 and 14% in 2004, the asset class performed well in comparison to US High Yield which has posted a 2% total return so far in 2005, lagging Europe for a third consecutive year, and in comparison to a 4% total return for European investment grade bonds. In contrast, European equities were up 15% for the year. We note the correlations (see table) indicate total returns on High Yield as more closely related to equities than investment grade bonds.

Total Returns for EUR HY and Other Asset Classes

4%

12%

49%

21%

-4%

-15%

-5%

-2%

-9%

6%

-14%

5%

-19%

-12%

7%

-7%

-1%

-36%

-22%

8%

26%28%

18%

29%

7%

15%

11%9%

11%8%

6%

2%

20%

5%3%3%

1%

29%

-4%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

1998 1999 2000 2001 2002 2003 2004 2005

� High Yield $ High Yield DJ Stoxx 50 S&P500 I Boxx � C t

Source: BNP Paribas, Ecowin, Bloomberg � Data for 2005 in this report refer to the period 1 January to 1 December 2005 - EUR HY and USD HY indices are constrained indices

The High Yield Handbook ⎪ January 2006

8 European High Yield Research

Going forward, as of 1 December 2005, the current (constrained) market average yield is 6.5%, comprising an average coupon value of roughly 8%, with 4.3 average years to worst call. The average yield for single B credit in Europe is 7.4% versus 7.9% in US High Yield. (On an unconstrained basis the average yield is 6.7%). These data are hardly compelling; given the risk profile of much of the single-B spectrum of the market investors maybe better rewarded in the equity or subordinated capital portions of the capital markets.

On the positive side, given the link between the drivers of High Yield and equity returns, High Yield investors should have a positive year in 2006 in the event of strong earnings momentum as long as the ECB remains somewhat restrained.

In terms of High Yield credit, we saw a widening of the average of European non-investment spreads by 48bp between 1 January and 1 December 2005 to 348bp, with the widepoint of 480bp in June. We define the market as EUR HY fixed coupon bonds, with remaining time to maturity over 1 year. The market appears to have reached its bottom in HY spreads in this cycle in February 2005 when the average of non-investment grade spreads reached 242bp, the tightest since market inception in 1997.

Spreads for EUR HY Bonds by Rating

bp

200 bp

400 bp

600 bp

800 bp

1,000 bp

1,200 bp

1,400 bp

1,600 bp

Dec-01

Mar-02

Jun-02

Sep-02

Dec-02

Mar-03

Jun-03

Sep-03

Dec-03

Mar-04

Jun-04

Sep-04

Dec-04

Mar-05

Jun-05

Sep-05

Dec-05

BB �HY

B �HY

CCC and below �HY

� HY (constrained)

Source � BNP Paribas, Ecowin � OAS spreads to government curves � Ratings based on average of S&P, Moody�s and Fitch notes � includes GM /GMAC and Ford Extension Risk and Current Pricing Ordinarily High Yield will be less sensitive to interest rate movements than investment grade bonds, given the relative returns coming from the government and credits portion of the respective bonds. However, the high cash price of bonds in the European High Yield market is worrying as it creates a particularly unique vulnerability for certain bonds in the market.

The High Yield Handbook ⎪ January 2006

9 European High Yield Research

Price Distribution of EUR High Yield Fixed Coupon Bonds, Excluding GM in EUR bn of amounts outstanding January 2005 December 2005

% of total EUR bn % of total EUR bn Price <100 14% 7 19% 9 100 < Price < 110 53% 27 59% 30 Price >110 33% 16 22% 11 Total 100% 50 100% 50

Source � BNP Paribas, Bloomberg Not only do a large majority of bonds trade above par (81%), but 22% trade above 110. We believe a significant portion of this debt is from the 2003-2005 vintage of High Yield issuance, where mild credit enhancement has occurred in the context of a flattening yield curve. Not only are these bonds vulnerable from a credit weakening standpoint (given that the price action would imply near-perfect execution), but an increase in government rates beyond expectations could have a pronounced impact on bond prices due to their call structures. More specifically, an upward shifting and steepening yield curve, could mechanically shift the worst-call dates for these bonds (particularly those trading between 105-112) to their second, third or last call. While this is purely a mechanical shift in worst call dates, it can be understood conceptually that in an environment of rising interest rates, companies are more likely to keep the current bonds outstanding rather than refinancing them in the short/medium term. This extension of expected maturity, and the resulting change in duration, could accelerate bond price movements on the downside, without necessarily a shift in spreads (although spread widening would ensue along with the extension of the worst-call date in line with an upward sloping credit curve). Currently 30% of the callable EUR High Yield bonds are priced based on a worst call date being the next call.

The High Yield Handbook ⎪ January 2006

10 European High Yield Research

2006 Scenarios for High Yield Below, we outline some basic scenarios for 2006 and their expected impact on European High Yield. In 2005, the total return of 5.9% in European High Yield was comprised of a 3% from the government curve and a 2.9% credit return.

For 2006, we expect 2006 total return to vary between 0% and 5%, with 4-5% being our base case scenario. Our economists forecast 5-year interest rates in the Eurozone to increase by 30bp to 3.35% by December 2006, which would give a return of 1.8% on government bonds for the year. Our assessment is based on the EUR currency fixed rate bonds.

1. Base Scenario: Credit Spreads to Widen by 50bp We forecast a market average widening of 50bp in 2006 for EUR High Yield (vs. a 48bp widening to 338bp between January 2005 and December 2005) based on:

! A tightening by the ECB towards 2.75% and by the Fed to 4.75% by end 2006, with core inflation maintained;

! Oil price between $55-60/bbl over 2006; ! Eurozone GDP growth of 2% and US GDP growth of 3.5%; ! No surprise from Ford or GM;

If we take 3.3 as the duration of the EUR High Yield market (which has an average time to worst of 4.3 years), we forecast that the credit return would be 338bp-3.3*50bp = 173bp. Hence, we expect a 2006 total return of 1.8% + 1.7% = 3.5%. If we adjust for bond maturities and redemptions and additional total return from new issuance volume, we arrive to a total return of between 4% and 5%.

2. Downside Scenarios: Either GM or Worse GM/GMAC Default 2.1 GM Corp Default by End 2006 EUR bonds issued by GM Corp represent approximately 0.6% of EUR High Yield indices (constrained at 3%). If we assume that GM Corps bonds fall to 35 cents to the dollar, the yield on the bonds would widen by 1,100bp, which would lead to a 0.6%*1100 = 7bp additional widening of the index (more precisely 14bp widening of the EUR HY index if we take into account the longer duration of the GM Corp bonds compared to the EUR High Yield universe).

If we assume another 20bp widening from an increase in risk aversion from the market, the credit return for 2006 would be 0.6 % and total return 2.4%. If we adjust for bond maturities and redemptions and additional total return from new issuance volume, we arrive to a total return of 3.2%.

The High Yield Handbook ⎪ January 2006

11 European High Yield Research

2.2 Both GM Corp and GMAC default GM and GMAC bonds currently represent about �11bn of the �62bn market of EUR High Yield bonds with over 1 year to maturity. If we consider once again a 3% constrained index and we assume that spreads widen by 500bp on the GMAC bonds (we take a duration of 2 years and weighting of 2.4%) and 1,100bp on the GM Corp bonds before leaving the EUR index, we would have a negative impact on the index spread of 2.4%*500*2/3.3+0.6%*1100*7/3.3= 21bp.

If we assume another 25bp widening from an increase in risk aversion from the market, the credit return for 2006 would be 0.2% and total return 2 %. If we adjust for bond maturities and redemptions and additional total return from new issuance volume, we arrive to a total return of 2.8%.

3. Scenario 3: Scenario 2 combined with a more difficult Macro/economic environment We would forecast a widening of 150bp in 2006 for EUR High Yield based on:

! A tightening by the ECB towards 3% and by the Fed to 5% by end 2006; ! An average oil price of above $70/bbl over 2006; ! A sharp fall in US consumer spending; ! The fact that EUR High Yield credit spreads reached a record-high

150bp above the current level in Spring 05; Under this scenario, the credit return would be 338bp-3.3*150bp = -157bp.

We would expect a 2006 total return for EUR High Yield of between 0% and 1%.

The High Yield Handbook ⎪ January 2006

12 European High Yield Research

State of the European High Yield Market at Year End 2005 2005: Slight Deterioration in Credit Quality in European High Yield � More so in EUR Bonds Credit quality in European High Yield deteriorated slightly in 2005, with bonds rated B- and below representing 33% of the market (excluding GM) in December 2005 vs 30% in January 2005 (CCC ratings were 12% versus 10% in January).

Rating Distribution of European High Yield Market, Excluding GM, F January 2005 December 2005

% of market EUR bn % of market EUR bn

BB family 44% 40 43% 44 B+/B 23% 20 21% 21 B- 19% 17 21% 21 CCC family 11% 10 12% 12 NR 4% 3 3% 3 Total 100% 91 100% 101

Source � BNP Paribas, Ecowin, Bloomberg Ratings are based on average of Moody�s, S&P and Fitch notes Our definition of the European High Yield bond market include bonds denominated in EUR, GBP, CHF and USD and issued by European incorporated entities, including fixed rate, floating rate and PIK notes of amount outstanding over �100mn. We exclude bonds maturing within 1 year. We estimate that the European High Yield bond market is comprised of �115bn face value debt outstanding as of 1 December 2005 (+ �10bn maturing in 2006); or roughly 15% of the size US High Yield market. By currency, EUR bonds represent �71bn, USD bonds �32bn, GBP bonds �11bn and CHF bonds �1bn. These data include GM Corp and GMAC bonds totalling �13bn and Ford bonds totalling �1bn. If we consider EUR fixed cash pay coupon bonds only, deterioration in rating is greater.

Rating Distribution of EUR High Yield Fixed Coupon Bond, Excluding GM, F January 2005 December 2005

% of total EUR bn % of of total EUR bn

BB family 49 % 25 40% 20 B+/B 18% 9 18% 9 B- 20% 10 28% 14 CCC family 13% 6 15% 8 Total 100% 50 100% 50

Source - BNP Paribas, Ecowin, Bloomberg The slight deterioration is due to the lower quality of new issuance (see below), which was partially compensated by a higher number of upgrades vs downgrades by the rating agencies on the outstanding High Yield credits. Between 1 January 2005 and 1 December 2005, the composite rating of 34 issuers (representing �15bn of bonds) within European High Yield was upgraded while 23 issuers (�6bn of bonds) were lowered. Overall, agency

The High Yield Handbook ⎪ January 2006

13 European High Yield Research

rating changes in 2005 for European High Yield issuers was not significantly different from recent history and we have seen a slight decrease in downgrades � we expect a similar trend in 2006.

S&P�s Issuer Ratings Transition in Europe (% of Issuers)

From To Trailing 12m Sept �05 2004 Average

�81 � �04

BBB BB and below 2.6 1.6 5.6 BB B and below 8.4 9.9 9.6 B CCC and below 3.9 3.3 10.0 CCC/C D 20.0 40.0 28.7

From To Trailing 12m Sept �05 2004 Average

�81 � �04

BB BBB and above 5.6 2.0 5.7 B BB and above 7.8 8.3 5.8 CCC/C B and above 40.0 40.0 11.6

Source � BNP Paribas, S&P The amount of fallen angel debt in the European High Yield market remained fairly constant over 2005, primarily as GM paper replaced the maturing debt of credits that fell into High Yield in the 2001-2003 period. Excluding GM, fallen angels represented 27% (�27bn) of the market in December 2005 vs. 37% (�34bn) in January (the drop is largely driven by the exclusion of bonds maturing in 2006). Including GM, fallen angels represented 35% (�41bn) of the market in December.

Rating Distribution of European HY Bonds Outstanding (EUR bn) Industry Distribution of European HY Bonds

Outstanding (EUR bn)

� bn

� 5 bn

� 10 bn

� 15 bn

� 20 bn

� 25 bn

BB+ BB BB- B+ B B- CCC+ CCC CCC- CC C NR

as of 1 December 2005as of 1 January 2005

BB ratings: 48% of European High Yield

of which GM/GMAC:13% B ratings: 39% of European High Yield

CCC ratings: 10 % of European High Yield

GMAC �10bnGM �1bn

GM �2bn

�0 bn

�5 bn

�10 bn

�15 bn

�20 bn

�25 bn

�30 bn

Auto M

anufa

cturer

s

Buildin

g Mate

rials

Chemica

ls

Energy

Financ

ial / O

ther

Food C

onsu

mer Reta

il

Indus

trial

Packa

ging

Service

s Tran

sport

Steel

TMT

as of 1 December 2005as of 1 January 2005

GM/GMAC �13bn

Source � BNP Paribas � Ratings are average of S&P, Moody�s and Fitch � Excludes bonds with less than one year to maturity

Source � BNP Paribas � Ratings are average of S&P, Moody�s and Fitch � Excludes bonds with less than one year to maturity

The European High Yield market remains well diversified in terms of industry exposures. Telecoms Media and Technologies, with �25bn outstanding, still represents a significant portion of the market (23% excluding GM), but nowhere near its 75% dominance in 2000.

The High Yield Handbook ⎪ January 2006

14 European High Yield Research

Quality of Recent Issuance Given that new issuance and maturities result in a turnover of roughly 20% of the European High Yield market annually, it is important to examine quality of recently issued paper as a gauge of market health.

In 2005, the share of overall new issuance used to refinance debt and general corporate purposes fell significantly to 40% from over 60% in 2004. Comparatively the volume of LBO-financing deals has been the most notable change, increasing to �5bn (or 26% of total new issue voume) in 2005 vs. �2bn (or 16%) in 2003. Additionally, acquisition and dividend deals and a material amount (roughly �3bn) of deeply subordinated Payment-in-Kind (*) notes has resulted in a marked change in deal quality towards increasingly shareholder-friendly transactions.

*(Almatis, Ardagh, Avio, Cognis, Ecobat, Jefferson Smurfit, Kabel Deutschland World Directories).

European High Yield Issuance in 2005: Use of Proceeds (EUR bn) European High Yield Issuance in 2005: Bond

Ratings at issuance (EUR bn)

�0 bn

�5 bn

�10 bn

�15 bn

�20 bn

�25 bn

2002 2003 2004 2005

Issued by Financial institutionsShare repurchasing programmeRestructuringAcquisitionDividend to shareholdersLBO acquisitionDebt refinancingGeneral Corporate Purposes

�0 bn

�5 bn

�10 bn

�15 bn

�20 bn

�25 bn

2000 2001 2002 2003 2004 2005

NRCCCB-B/B+BB

Source � BNP Paribas Source � BNP Paribas

As a consequence the credit quality of new issuance deteriorated in 2005, with the proportion of B-/CCC growing from 23% of rated issuance in 2003 to 46% in 2005. Additionally, we estimate that leverage in LBO transactions has increased by between 0.5x and 1.0x EBITDA over past the past two years.

The High Yield Handbook ⎪ January 2006

15 European High Yield Research

European High Yield Issuance: Industry of Issuer (EUR bn)

�0 bn

�5 bn

�10 bn

�15 bn

�20 bn

�25 bn

2000 2001 2002 2003 2004 2005

TMTSteelServices TransportPackagingIndustrialFood Consumer RetailFinancial / OtherEnergyChemicalsBuilding MaterialsAuto Manufacturers

Source � BNP Paribas From a sectoral standpoint, TMT once again led the way, and was also the largest share of LBO-related High Yield issuance with the �1.3bn deal for the acquisition of Tim Hellas by a TPG/Apax, which was the largest all-bond financed leveraged buyout in Europe and Wind, the largest European LBO to-date.

The High Yield Handbook ⎪ January 2006

16 European High Yield Research

Quality of Recent Issuance Given that new issuance and maturities result in a turnover of roughly 20% of the European High Yield market annually, it is important to examine quality of recently issued paper as a gauge of market health.

In 2005, the share of overall new issuance used to refinance debt and general corporate purposes fell significantly to 40% from over 60% in 2004. Comparatively the volume of LBO-financing deals has been the most notable change, increasing to �5bn (or 26% of total new issue voume) in 2005 vs. �2bn (or 16%) in 2003. Additionally, acquisition and dividend deals and a material amount (roughly �3bn) of deeply subordinated Payment-in-Kind (*) notes has resulted in a marked change in deal quality towards increasingly shareholder-friendly transactions.

*(Almatis, Ardagh, Avio, Cognis, Ecobat, Jefferson Smurfit, Kabel Deutschland World Directories).

European High Yield Issuance in 2005: Use of Proceeds (EUR bn) European High Yield Issuance in 2005: Bond

Ratings at issuance (EUR bn)

�0 bn

�5 bn

�10 bn

�15 bn

�20 bn

�25 bn

2002 2003 2004 2005

Issued by Financial institutionsShare repurchasing programmeRestructuringAcquisitionDividend to shareholdersLBO acquisitionDebt refinancingGeneral Corporate Purposes

�0 bn

�5 bn

�10 bn

�15 bn

�20 bn

�25 bn

2000 2001 2002 2003 2004 2005

NRCCCB-B/B+BB

Source � BNP Paribas Source � BNP Paribas

As a consequence the credit quality of new issuance deteriorated in 2005, with the proportion of B-/CCC growing from 23% of rated issuance in 2003 to 46% in 2005. Additionally, we estimate that leverage in LBO transactions has increased by between 0.5x and 1.0x EBITDA over past the past two years.

The High Yield Handbook ⎪ January 2006

17 European High Yield Research

European High Yield Issuance: Industry of Issuer (EUR bn)

�0bn

�5bn

�10bn

�15bn

�20bn

�25bn

2000 2001 2002 2003 2004 2005

TMTSteelServices TransportPackagingIndustrialFood Consumer RetailFinancial / OtherEnergyChemicalsBuilding MaterialsAuto Manufacturers

Source � BNP Paribas From a sectoral standpoint, TMT once again led the way, and was also the largest share of LBO-related High Yield issuance with the �1.3bn deal for the acquisition of Tim Hellas by a TPG/Apax, which was the largest all-bond financed leveraged buyout in Europe and Wind, the largest European LBO to-date.

The High Yield Handbook ⎪ January 2006

18 European High Yield Research

Default Rates: No Signs Yet of the Expected Increase Default Rates and GDP Growth Rates

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

HY default rate (global) (LHS)

US GDP growth y-o-y (LHS)

Source - BNP Paribas, Ecowin We expect the non-investment grade default rate to remain well below its long term average rate (4.9% for global issuers) in 2006, causing some restraint to the widely expected spread-widening. In 2005, after 3 years of steady decline, the European High Yield default rate reached 0% in the first quarter of 2005 and is currently at 0.4%. This is likely to increase in 2006 as the larger proportion of CCC issuance since 2003 is likely to put pressure on market credit spreads over the next 2 years (cumulative average default rate for CCC is 36% after 2 years ). S&P forecasts US speculative default rate to grow from 2% today to 2.6% at end of 2006.

Correlation between Spreads and Default Rates

bp

200 bp

400 bp

600 bp

800 bp

1,000 bp

1,200 bp

1,400 bp

May-02 Sep-02 Jan-03 May-03 Sep-03 Jan-04 May-04 Sep-04 Jan-05 May-05 Sep-05%

2%

4%

6%

8%

10%

12%

14%

16%

OAS Spreads (LHS)

European Default rate � High YieldCompanies (LHS)

Source - BNP Paribas, Ecowin, S&P

The High Yield Handbook ⎪ January 2006

19 European High Yield Research

Earnings and Sectoral Outlook In 2006, corporate earnings growth is likely to continue but at a slower pace, due to high energy prices and the high cost of raw materials. Our equity analysts (BNP Paribas Exane) expect 9% earnings growth in Europe in 2006 vs 14% in 2005 (and +10% for S&P500 in 2005). The Eurozone economies seem to have improved over the past few months; our economists forecast a 2% GDP growth in 2006 vs. 1.4% in 2005. However, the health of the economy is still fragile as the recovery is currently driven by external demand and not domestic consumption.

The impact of a stronger US dollar vs. the Euro should benefit European companies, however the main earnings risk remains the threat of a renewed increase in oil and raw material prices. In our view, there is a potential downside risk from current expectations if oil prices continue to trend higher after their decline from August records, as central banks appear to be more concerned over inflation to the potential detriment of economic growth.

Consensus expectations for higher interest rates in 2006 (50bp in Fed target rate by end of H1 2006, 50bp in ECB main refinancing rate to 2.75% by end 06) mean a more difficult environment for credit markets in general, and a surprise move by the ECB would be a negative catalyst for European High Yield.

From an event risk standpoint, GM filing for Chapter 11 is a risk - especially if a Delphi strike affects GM production, leading to large cash burns or if the sale of GMAC is delayed � this could have direct knock-on effect on suppliers and indirect effect on high beta names in the European High Yield universe. What is a mild positive for European investors is that 80% of the GM EUR outstanding bonds are issued by GMAC, which means that if GMAC is sold, the final impact on European credit spreads could be mild.

Key High Yield Sectors 1. TMT Contributed by Aizaz Shaikh, Senior High Yield Analyst

TMT continues to be an area of intense activity for European High Yield with a significant volume of new issuance and re-issuance. In 2005, M&A was the driver of much of the price action as consolidation in cable, mobile, and wireline telecom created opportunities to make and lose money. In terms of credit quality, 2005 was a year of mild improvement in certain sectors (directories, mobile) but higher financial risk in others (cable, telecom). In 2006 we would expect the current trends to continue, but also accelerate, as the frenzy for higher shareholder returns drives increasingly challenging deal structures. All this stated, TMT still is favourably positioned as a sector of decent immunity against cyclical weakness in the economy. Balance sheets in TMT are still healthy from the 2002-2004 reparation period, though some slight damage has been done in 2005. We do not expect to see a default in the roughly 30 credits TMT in European High Yield in 2006, however underperformance from the cable sector (as growth targets fail) or from

The High Yield Handbook ⎪ January 2006

20 European High Yield Research

certain telecom services companies (C&W, COLT, Wind) as competition becomes severe, would not be a surprise.

2. Industrials & Chemicals Contributed by Adam Harnetty, Senior High Yield Analyst

From a sector standpoint, mild earnings growth should remain in industrial sectors; the majority of the European High Yield capital goods companies have a stable outlook at S&P.

Given the increased risks in respect of worldwide growth and the secular changes occurring within Europe, it is difficult to have a particularly bullish view on the sector. Within general industrials, there are credits with secular stories we like, such as Alstom and Corus, whereas companies like Invensys and Grohe will be particularly sensitive to any weakening in the general economic outlook.

Within the chemicals sector, we would look to avoid exposure to very commoditised businesses and have a higher weighting towards speciality type companies where raw materials are typically a lower portion of the company's cost base. Of course, to the extent that growth surprises on the upside, this recommendation would be reversed.

While most European High Yield issuers have little exposure to the Far East, China and India continue to influence the fortunes of European industrial companies. Growth in China and India, due to increased domestic demand and off-shoring, has resulted in huge demand for commodities while serving as a disinflationary force for manufactured goods. This trend is set to continue with the following impacts:

! Commodity prices are likely to stay high; ! Basic manufacturing will continue to migrate away from Europe; ! A continuation of pressure on manufactured goods prices. Finally, energy costs (and especially oil) are a significant factor in many industrial companies and especially the chemicals industry. It would appear that prices are likely to remain high in the current environment. It is not at all clear that the supply of crude oil can be materially increased. Indeed given the lack of spare refining capacity, even if more crude oil were to become available it is not at all obvious that the price of refined products would fall significantly.

3. Consumers, Retail and Services Contributed by Oleksiy Soroka, Senior High Yield Analyst

We do not believe that consumer sector bonds will outperform the market in 2006. We think for this to happen, the retail environment and consumer confidence in Europe would need to improve materially relative to the current levels. At this stage, we are not convinced that this will be the case and, therefore, maintain our cautious stance with regards to the consumer sector notes. A strong macroeconomic recovery in Europe presents a positive risk relative to our base-case scenario.

The High Yield Handbook ⎪ January 2006

21 European High Yield Research

However, we expect more pressure in consumer and retail where we see weak consumer sentiment. S&P has 1/3 of European consumer goods companies under negative outlook or credit watch negative, the highest proportion among industries in Europe covered by S&P.

In terms of individual sub-sectors, we believe that retailers and food manufacturers will have another lacklustre year in 2006. We think that airlines will have a positive year, in spite of the continued high fuel prices. We do not expect any actual defaults in consumer sectors in 2006. However, a number of the consumer bonds are already in the "stressed" territory and things might get worse for some of them.

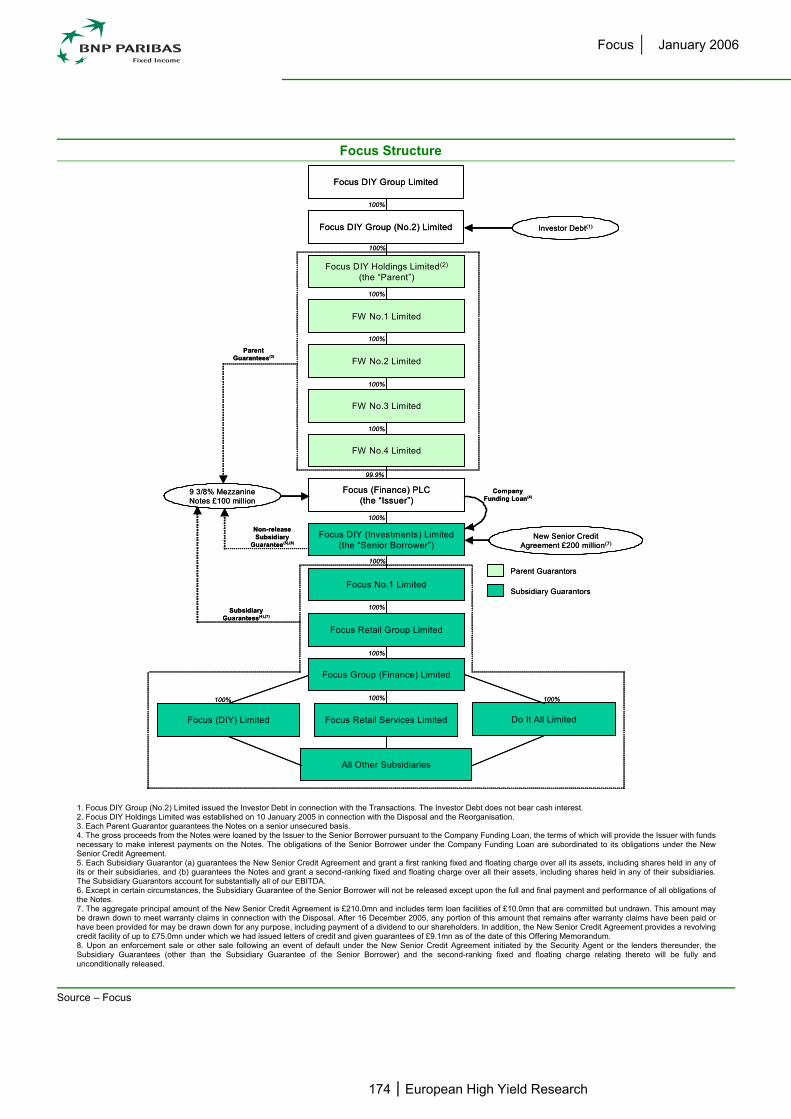

For instance, we are still cautious with regards to Focus as we do not see a recovery in the UK DIY market until the latter part of 2006. In addition, we note that IT Holding remains reliant on the support of its Italian bank group. Should that support falter, the company may face a liquidity crisis (we think that the banks will remain supportive throughout 2006). Waterford Wedgwood would be the most straightforward default candidate, were it not for a continued support of its shareholders.

Finally, we expect that operating results should improve at Fage Dairy. We expect that large and highly levered consumer sector LBO's, such as Rexel and Vendex, will continue to delever gradually during 2006. We now do not anticipate that any of the crossover names will actually make it to high grade next year, as we now expect that Ahold will only cross over the line in 2007.

The High Yield Handbook ⎪ January 2006

22 European High Yield Research

2006 Market Supply and Demand 2005 European High Yield Issuance: Healthy, but Short of 2004 and Below Expectations The low interest environment and attractive performance of the asset class in 2004 resulted in another healthy volume of new paper � roughly �21bn � in 2005. While this number was not far from the record levels of 2004, the anticipated volume was about �5-7bn higher. The cancellation or delay of a number of transactions into 2006 destabilized the market slightly in favour of the issuers with demand outstripping supply.

Overall, the European High Yield share of global High Yield issuance continued to increase, representing 30% of US issuance in 2005 vs 8% in 2002, however in the second half of 2005, the US market was significantly more active than Europe.

In 2006, we expect new issuance volume to reach �25bn, about the same as in 2004. This compares with bond maturities of roughly �10bn in 2006 and roughly �30bn in total by 2008.

European and US HY Issuance 2000-2005 (USD bn) Maturity Date of European HY market (Amount

Outstanding - EUR bn)

128

5

16

3025

43

79

59

131136

85

$0 bn

$20 bn

$40 bn

$60 bn

$80 bn

$100 bn

$120 bn

$140 bn

2000 2001 2002 2003 2004 2005

European High Yield issuanceUS High Yield issuance

�bn

�2bn

�4bn

�6bn

�8bn

�10bn

�12bn

�14bn

�16bn

Q106 Q206 Q306 Q406 2007 2008 2009 2010 2011 2012 2013 2014 2015 After2015

Total 2006 �10bn

Source � BNP Paribas Source � BNP Paribas

Difficult Supply/Demand Equation, Despite Significant Market Liquidity

Overall, we believe the current European High Yield market demonstrates balanced supply/demand features as seen with the more �reasonable� pricing of transactions in the second half of 2005 versus the first half. Still, in 2006 the supply and demand equation will be more difficult as a significant amount of new issuance is likely and mutual outflows, which have been steady, are likely to exacerbate in a number or scenarios. While investors and hedge funds continue to demonstrate significant cash and liquidity, we believe a minor disruption due to heightened risk aversion or unexpected interest rate movements could dramatically withdraw interest in non-investment grade credit until valuations are materially more attractive. This scenario, which occurred in the second quarter of each of the last 2 years, could be more pronounced in 2006 as other asset classes (i.e. equities, loans) present more appealing risk/reward characteristics.

The High Yield Handbook ⎪ January 2006

23 European High Yield Research

European High Yield Issuance Calendar for Q1 2006 (Estimated) Issuer Amount (mn) Use of Proceeds Almatis �200 Fund the acquisition by Investcorp Amadeus �900 Fund the acquisition by Cinven and BC Partners Colt Telecom �500 Refinancing of bonds and converts European Beverages �300 Fund the acquisition by Blackstone/Lion Capital Fresenius �700 Fund the acquisition of Helios Ineos �2,500 Fund the acquisition of Innovene

ISS �975 Fund the acquisition by EQT and Goldman Sachs Capital Partners

NTL �2,600 Fund the acquisition by Telewest ONO �270 Fund the acquisition of Auna�s cable division

TDC �2,275 Fund the acquisition by Apax, Blackstone, KKR, Permira and Providence.

Total �11,220 Source - BNP Paribas In terms of supply, the European High Yield Issuance calendar for Q1 2006 is heavy, partly because the second half of 2005 saw muted activity with certain large deals postponed to the New Year. In Q1 2006, �11bn equivalent in High Yield deals are expected to price, the majority of which will most probably be rated B or below. This compares with �8bn issued in Q1 2005, the period of tightest non-investment grade spreads in Europe to date, and which was followed by a significant pull back in spreads and investor interest in new issue.

Additionally, the growth of leveraged transactions is set to continue in 2006, with the emerging trend of private equity club deals increasing the size (and therefore number) of potential LBO targets. It is likely that the TMT sector will continue to be fertile ground for the large buyouts, in this context. Over the first 9 months of 2005, leveraged loan issuance was roughly �100bn vs. �44bn in 2004.

On the demand side, market conditions are less favourable than 1 year ago. US High Yield mutual funds, even though only represent 15% of investors, show negative signs � $12bn left the US High Yield mutual funds in 2005, compared to a $20bn inflow in 2003 and $3bn outflow in 2004 � underpinning the wariness of US investors toward High Yield over the past year.

AMG data � US Mutual Funds Inflow/Outflow 2002-2005 (USD bn)

-$3 bn

-$2 bn

-$1 bn

$ bn

$1 bn

$2 bn

$3 bn

$4 bn

Jan-02 Apr-02 Jun-02 Sep-02 Dec-02 M ar-03 M ay-03 Aug-03 Nov-03 Feb-04 Apr-04 Jul-04 O ct-04 Jan-05 M ar-05 Jun-05 Sep-05

W eely AM G Flow4 week m oving average

2002: +$8.0 bn (Inflow)

2003: +$20.0 bn (Inflow)

2004: -$3.0 bn (Outflow)

2005: -$12.0 bn (O utflow)

Source � BNP Paribas, AMG

The High Yield Handbook ⎪ January 2006

24 European High Yield Research

Companies Included in this Analysis Ticker Group Name Ticker Group Name Ticker Group Name ABB ABB FIAT Fiat NOMOS Commerzbank AES AES FKI FKI NSKIES New Skies AG Agco FOCFIN Focus NTLI NTL AGROK Agrokor FREGR Fresenius NYCO Nycomed AGZFIN Antargaz FSTINV First Investment Bank OCRNO Ocean Rig AHBR Allg Hypobank Rheinb GALFIN Global Automotive Logistics OI Owens Illinois AHOLD Ahold GAZPRU Gazprom ONOFIN Ono AHTLN Ashtead GBLXQ Global Crossing ORICB Industry & Construction Bank St Petersburg ALAFP Alcatel GERRES Gerresheimer PAREX Parex Banka ALFARU Alfa Bank GGY Compagnie Gle de Geophysique PENTAP Kloeckner Pentaplast ALLIBK Alliance Bank GILGR Gildemeister PERI Peri ALMAT Almatis GM GMAC PGSNO Petroleum Geo Services ALOFP Alstom GMKNRU Norilsk Nickel PIAGIM Piaggio ALROSA Alrosa GROHE Grohe PIPEHO Polypipe ANTTEN Antenna TV HCA HCA PPOUS Polypore ARGID Ardagh HCFB HCFB PREEM Preem ASPRO Avio HEADHO Head PREGIS Pregis ATUGRP ATU HECKKO Heckler & Koch PROMBK JSC Promsvyazbank AVECIA Avecia HEI HeidelbergCement PROSIE Prosieben BAB British Airways HELLAS Tim Hellas RAYAC Rexel BARY Barry Callebaut HHLCN Petrokazakhstan REMFIN Remy Cointreau BASLNV Basell HORN Hornbach RHA Rhodia BAXI Baxi HUNTSM Huntsman RHIAG Rhiag BCPLU Celanese IESYRP Iesy RIFP Allied Domecq BGY British Energy IFCOF Ifco RIVDEE Riverdeep BKBLN Brake Bros IMPEX Impex ROCKWO Rockwood BOMB Bombardier IMPMET Impress ROSBNK Rosbank BTAS Bank Turanalem INEACR Lucite RUSB Russian Standard Bank CABCOM Cablecom INMARS Inmarsat SAFILO Safilo CARMLI Carmeuse INTERG Intergas SAMC Samsonite CBBUS Concordia Bus INVTEL Invitel SAS SAS CCK Crown IRM Iron Mountain SAUR Saur CEDCUS Central European Distribution ISATIJ Indosat SCHEFE Schefenacker CELLSA Cell C ISSDC ISS SEAT Seat Pagine Gialle CETV Central European Media ISYSLN Invensys SGL SGL Carbon CFRMA CFR Marfa ITHOLD IT Holding SICPA Sicpa CHMFRU Severstal JENGR Jenoptik SINEK Sinek Capital CIRSA Cirsa JONDIV JohnsonDiversey SISFIN Sistema Capital CLONDA Clondalkin KABEL Kabel Deutschland SLTBSS Esselte CMACG CMA CGM KABLBW Kabel BW SOFTBK Softbank CODERE Codere KAMPS Kamps STENA Stena COGNIS Cognis KAPPA Kappa STZ Constellation Brands COLTEL Colt Telecom KKB Kazkommerts SUNSAG Sun Sage CORUS Corus KLOCK Kloeckner TEKS Teksid CPNL Calpine KOFFP Kaufman & Broad TELEC Tele Columbus CSK Chesapeake KRONOS Kronos TGHGR Thiel Logistik CULLI Culligan KVINO Aker Kvaerner TLNET Telenet CWLN Cable & Wireless LBCLUX LBC TMENRU Tyumen Oil DAMOVO Damovo LEA Lear TRW TRW Automotive DANKA Danka LEVI Levi Strauss TUIGR TUI DRRA Dura LR Legrand TVNSPZ TVN DUERR Duerr LUXHOL Luxfer UBF United Biscuits ECOBAT Ecobat LVLT Level 3 Communications UNM Provident EDITIS Editis MAUSER Mauser UPC UPC EIRCOM Eircom MBRDRU Moskow Bank VED Vedanta ELECAR Electricidad de Caracas MDPAC Jefferson Smurfit VENDEX Vendex ELETUR Elektrownia Turow MEGAFO Megafon VIP Vimpelcom ELN Elan MEPC MEPC VOD Mobifon EMI EMI MESSA M-Real WASTER Waste Recycling EP El Paso METSO Metso WBDFRU Wimm-bill-dann ESCADA Escada MICC Millicom WDAC World Dierctories ETL Eurotunnel MMKFIN MMK WINDIM Wind EVCINA Ineos Vinyls MOBTEL Mobile Telesystems WMG Warner Music EVRAZ Evraz MTUAER MTU Aero WTRFRD Waterford Wedgwood EXCLIJ Excelcomindo MTW Manitowoc XRX Xerox F Ford NELL Basell YELFIN Yell FAGEGA Fage Dairy NIKOIL Nikoil YIOULA Yioula Glassworks FDCSJ FoodCorp NLC Nalco

Source � BNP Paribas

The High Yield Handbook ⎪ January 2006

25 European High Yield Research

List of Issuers � Part 1 ABB 26 Invitel 220 Ahold 30 IT Holding 224 Alstom 32 Jenoptik 230 Antenna 36 Kabel BW 236 Ardagh 42 Kabel Deutschland 240 Avio Holding Spa (Aspropulsion) 46 Kamps 246 Barry Callebaut 50 Klockner Pentaplast 250 Basell 54 Kronos 254 Brake Brothers 58 Legrand 258 British Airways 64 Lucite 262 Cable & Wireless 66 MTU 266 CableCom 70 Nalco 270 UPC 71 NTL Cable plc 276 Carmeuse 80 ONO 280 Cell C 84 Polypore 284 Central European Media 90 Preem 288 CIRSA 94 Rallye 292 Clondalkin 100 Remy Cointreau 298 CMA CGM 104 Rexel 304 Codere 110 Rhodia 310 Cognis 116 Rockwood 314 Colt Telecom 122 Safilo 320 Corus 126 SAS 324 Culligan 130 Saur 328 Ecobat 136 Seat Pagine Gialle 334 Editis 140 Sicpa 340 Eircom 146 Smurfit Kappa Group 344 EMI 152 Sol Melia 350 Escada 158 Tele Columbus 352 Fage Dairy 162 Telenet 356 FKI 168 Tim Hellas 362 Focus 172 TUI 368 Gildemeister 178 TVN 372 GM 182 United Biscuits 376 Grohe 186 Unity Media (Iesy) 380 Head NV 190 Vendex KBB 386 Heckler & Koch 194 Warner 392 Hornbach 198 Wind 400 Impress Group 202 World Directories 406 Ineos Vinyls (EVC) 206 Yell 412 Inmarsat 210 Invensys 216

ABB Ltd ⎪ January 2006

26 European High Yield Research

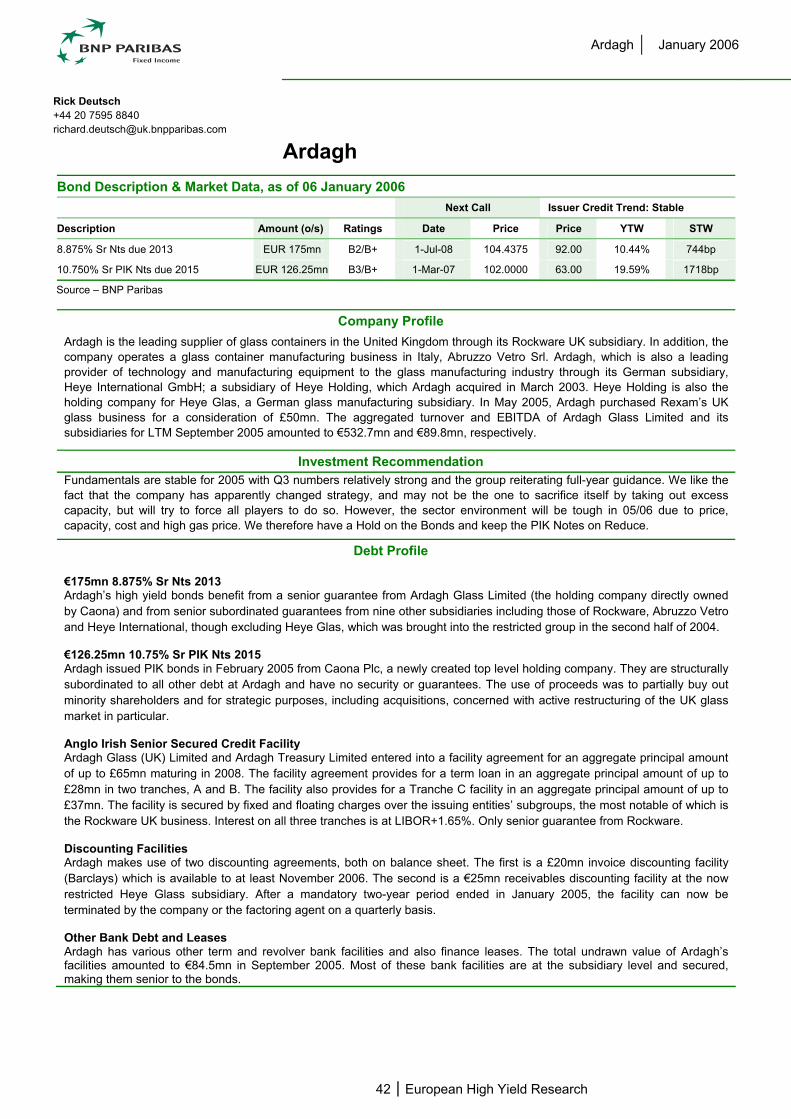

ABB Ltd Bond Description & Market Data, as of 5 January 2006

Next Call Issuer Credit Trend: Positive

Description Amount (o/s) Ratings Date Price Price YTW STW

9.5% Sr Nts due 2008 EUR 500mn Ba2/BB- NC NC 114 3.65% 69bp 10% Sr Nts due 2009 GBP 200mn Ba2/BB- NC NC 116.29 6.10% 156bp 6.5% Sr Nts due 2011 EUR 650mn Ba2/BB- NC NC 112.8 4.03% 86bp

Source � BNP Paribas

Company Profile The ABB Group is a global provider of power and automation technologies that enable utility and industry customers to improve performance while lowering environmental impact. ABB works with their customers to engineer and install networks, facilities and plants with particular emphasis on enhancing efficiency and productivity for customers that source, refine and distribute energy. The group was formed in 1988 through a merger between Asea AB and BBC Brown Boveri AG. In June 1999, ABB Ltd became the holding company for the entire ABB Group. For the 12 months ended 30 September 2005, the group�s sales totalled $22.4bn with an EBITDA of $2.1bn, implying an EBITDA margin of 9.5%. Net debt stood at $866mn at the end of 30 September 2005.

Investment Recommendation ABB continues to make good progress on its restructuring and on growing revenues and the order book. As a result, cash flow has been materially strengthened. Importantly, ABB has come to an agreement with plaintiffs on its major asbestos suit, and is awaiting the final outcome of the Appeals Court process. Resolution of this issue is key to any move back to investment grade, which we expect in H1 06. Bond prices strike us as fair with the exception of the GBP bond which we think is expensive given our view of a move back to investment grade in H106 and the consequent step down of its coupon.

Debt Profile ABB�s gross debt at 30 September 2005 stood at $4,494mn. This was comprised of approximately $1.7bn of convertible bonds ($968mn 4.625% 2007 and CHF1bn 3.5% 2010), $2.1bn of bonds (�500mn 9.5% 2008, £200mn 10% 2009, CHF500mn 3.75% 2009 and �650mn 6.5% 2011) and $0.7bn of unanalysed debt. In terms of bank facilities, ABB recently signed a $2bn 5 year revolving credit facility due July 2010. In October 2005 ABB repurchased CHF392mn of the 2009 bond leaving CHF108mn outstanding.

Adam Harnetty, ACA +44 20 7595 8831 [email protected]

ABB Ltd ⎪ January 2006

27 European High Yield Research

ABB Ltd Structure

ABB Ltd

ABBHolding AG

ABB CapitalB.V.

ABB InternationalFinance Limited

ABB FinanceInc.

ABB Asea BrownBoveri Ltd

ABB FinancialServices B.V.

99.9996%

0.0004%

Keep-Well Agreement

ABB Ltd

ABBHolding AG

ABB CapitalB.V.

ABB InternationalFinance Limited

ABB FinanceInc.

ABB Asea BrownBoveri Ltd

ABB FinancialServices B.V.

99.9996%

0.0004%

Keep-Well Agreement

Keep-Well Agreement If the Issuer at any time will run short of cash and other liquid assets to meet any payment obligation on its debt, then the Issuer will promptly notify ABB Ltd of the shortfall and ABB Ltd will make available to the Issuer, before the due date of such payment obligation, funds sufficient to enable the Issuer to fulfil such payment obligation as it falls due. However, the agreement is not a guarantee by ABB Ltd of the payment of any indebtedness, liability or obligation of the Issuer.

Source � ABB

ABB Ltd ⎪ January 2006

28 European High Yield Research

Bond Covenants

EUR 500mn 9.5% (currently at 11%) Senior Notes 2008

GBP 200mn 10% (Currently at 11.5%) Senior Notes 2009

EUR 650mn 6.5% Senior Notes 2011

Bond description EUR Notes 9.5% + GBP Notes 10% EUR Notes 6.5%

Issuing entity ABB International Finance Ltd ABB International Finance Ltd

Ranking Senior notes Senior notes Position vs. bank debt No information provided No information provided

Position vs. other bonds Pari passu Pari passu

Security/guarantees None None

Optional redemption Optional early redemption (Call) � none Optional early redemption (Call) � none

Optional early redemption (Put) � none Optional early redemption (Put) � change of control

Change of control No 101 put if accompanied by ratings decline

Tax redemption Yes � at their principal amount Yes � at their principal amount

Negative pledge Yes Yes

Cross default Yes Yes

Fall away covenants No No

Anti-layering No No

Asset sales No No

Debt limit No No

Restricted payments No No

Transactions with affiliates No No

Rate of interest increase

The rate of interest may be increased/decreased depending upon the ratings assigned to the notes. Interest paid is 9.5% if Moody�s and S&P assign Baa3 and BBB- rating, respectively. In case of a downgrade by the aforementioned agencies or a termination of coverage by the aforementioned agencies (Rating decrease event), then the interest rate will be 9.5% plus 1.5% p.a. A return to the aforementioned ratings will reinstate the 9.5% coupon.

No

Source � BNP Paribas, ABB

ABB Ltd ⎪ January 2006

29 European High Yield Research

ABB Ltd, Financial Model FYE 31 December Actual Actual Restated Restated Restated Actual Actual Actual Actual Actual Forecast ForecastUSD mn 2002 2003 Q1 04 Q2 04 Q3 04 Q4 04 2004 Q1 05 Q2 05 Q3 05 2005 2006

PROFIT & LOSS Revenue 17,466 18,795 4,528 5,209 5,013 5,971 20,721 5,088 5,724 5,648 22,800 24,168 Cost of sales -13,067 -14,080 -3,350 -3,930 -3,834 -4,643 -15,757 -3,783 -4,327 -4,258 Gross Profit 4,399 4,715 1,178 1,279 1,179 1,328 4,964 1,305 1,397 1,390 SG&A -3,954 -3,830 -918 -948 -909 -1,011 -3,786 -955 -1,008 -929 Amortisation -41 -40 -11 -11 -12 -11 -45 -11 -11 -11 Other expense -58 -189 -2 1 -6 -42 -49 52 -7 -8 EBIT 346 656 247 321 252 264 1,084 391 371 458 1,695 1,933 D&A 611 585 148 148 142 195 633 142 145 156 600 600 EBITDA 957 1,241 395 469 394 459 1,717 533 516 614 2,295 2,533

Net Interest -126 -410 -79 -50 -28 -66 -223 -41 -95 -55

Revenue growth y/y 7.6% 5.1% 7.6% 10.1% 17.6% 10.2% 12.4% 9.9% 12.7% 10.0% 6.0% Gross margin 25.2% 25.1% 26.0% 24.6% 23.5% 22.2% 24.0% 25.6% 24.4% 24.6% EBITDA margin 5.5% 6.6% 8.7% 9.0% 7.9% 7.7% 8.3% 10.5% 9.0% 10.9% 10.1% 10.5%

CASHFLOW

Change in working capital 418 253 -285 -467 89 645 20 -555 -259 -167 Cash from operating activities 19 -161 -141 -136 322 880 962 -235 168 387

Capex -602 -547 -98 -137 -109 -199 -543 -79 -101 -133 Acquisitions/disposals 2,365 488 16 283 806 53 1,158 -5 -13 -23 Other 888 813 -806 852 -164 -143 -261 -442 692 -213 Cash from investing activities 2,651 754 -888 998 533 -289 354 -526 578 -369

Net debt repayment -2,815 -1,028 -1,070 -647 -1,027 29 -2,752 -185 -25 -218 Other 3 2,619 -40 -22 3 6 -53 6 -43 -11 Cash from financing activities -2,812 1,591 -1,110 -669 -1,024 35 -2,805 -179 -68 -229

FX & Other 167 149 53 138 106 87 382 -122 -104 12

Net change in cash 25 2,333 -2,086 331 -63 713 -1,107 -1,062 574 -199

BALANCE SHEET

Cash & Equivalents 2,925 5,142 3,820 3,405 3,596 4,200 4,200 3,651 3,575 3,628

Total Debt 7,928 7,887 6,748 6,115 5,178 5,534 5,534 5,161 4,912 4,494

Net Debt 5,003 2,745 2,928 2,710 1,582 1,334 1,334 1,510 1,337 866

Pension Liability 2,077 1,820

LTM RATIOS Coverage 7.6 3.0 3.8 4.8 6.8 7.7 7.7 10.0 8.3 8.3 EBITDA-Capex/Interest 2.8 1.7 2.3 3.1 4.7 5.3 5.3 7.2 6.1 6.3

Gross leverage 8.3 6.4 4.9 3.9 3.3 3.2 3.2 2.8 2.6 2.1 Net leverage 5.2 2.2 2.1 1.7 1.0 0.8 0.8 0.8 0.7 0.4

Source � BNP Paribas, ABB

Ahold ⎪ January 2006

30 European High Yield Research

Ahold Bond Description & Market Data, as of 5 January 2006

Next Call Issuer Credit Trend: Positive

Description Amount (o/s) Ratings Date Price Price YTW STW

6.375% Senior Notes due 2007 EUR 200mn Ba2/BB NC NC 104.79 3.70% 75bp 5.875% Senior Notes due 2008 EUR 1,500mn Ba2/BB NC NC 105.28 3.57% 58bp 5.875% Senior Notes due 2012 EUR 600mn Ba2/BB NC NC 107.70 4.42% 119bp

Source � BNP Paribas

Company Profile Ahold operates a number of large supermarket chains in the United States and in Europe, and runs foodservice business in North America. Ahold�s largest US retail franchises include Stop & Shop (Massachusetts, Connecticut, Rhode Island, New Jersey and New York), Giant-Carlisle (Maryland, Virginia and West Virginia) and Giant Food/Giant Landover (Maryland, Virginia, Delaware, New Jersey, District of Columbia). In Europe, Ahold�s Albert Heijn is the leading food retailer in The Netherlands. Ahold also owns 60% of ICA AB, a food retailer and wholesaler in Scandinavia and the Baltic countries (the retailer is not consolidated in the group�s financials). Ahold also operates supermarkets in Portugal (Jeronimo Martins) and in Central Europe. In the US, Ahold is the second-largest foodservice operator, in terms of turnover, after Sysco Corporation. In February 2003, significant accounting irregularities were uncovered in Ahold�s financials. The company has since changed the top managers and restated its accounts for the period of 2001-2003. We calculate that for the twelve months ended 9 October 2005, in its continuing operations, Ahold had turnover of �45,491mn and EBITDA of �2,319mn. At the end of third quarter 2005, the company had lease-adjusted leverage of 3.6x and lease-adjusted coverage of 2.4x.

Investment Recommendation We maintain our HOLD/Positive Credit Trend recommendation for Ahold�s notes. We continue to think that the company is on track to regain an investment-grade status, but we now feel that it may take longer than we have originally envisaged to achieve this. We note that the agreed sizeable cash payout slated for 2006 and related to the settlement of the class actions will probably delay the upgrade until 2007 (rather than the second half of 2006 we expected earlier). S&P�s comment published on 26 November 2006 states that the magnitude of the cash payout related to the settlement �will delay the potential restoration of an investment-grade rating� and that the company is now expected to reach the minimum parameters commensurate with the current rating level by the end of 2006. S&P�s issuer credit rating for Ahold is BB+ (Positive Outlook), while the bond rating is one notch lower, at BB. Moody�s has Ahold�s senior implied rating at Ba2 (Outlook Positive) and the bond rating is the same. We think that the rating agencies will need to see a consistent and satisfactory operating performance by the company, including an improvement in profitability of the US Foodservice business, before effecting any further upgrades. In our view, a marked deterioration in the company�s profitability will delay the ratings upgrade further.

Debt Profile As of 9 October 2005, Ahold had total debt of �8,856mn, including long-term portion of �7,944mn and short-term portion of �912mn. The company�s total debt comprised bonds and loans of �5,661mn, finance leases of �1,830mn, cumulative preferred financing shares of �666mn and short-term borrowings of �699mn. On 18 May 2005, Ahold signed a new credit facility with a syndicate of 15 banks. This is a five-year �2.0bn multi-currency facility which matures in five years. The facility is unsecured and is, therefore, pari passu with the company�s unsubordinated bonds. This is subject to a leverage covenant, which falls away when the corporate rating is BBB/Baa2 or better. As of the end of third quarter 2005, the credit facility was undrawn, except for the use of letters of credit in the amount of $665mn (�549mn). As of 9 October 2005, Ahold also had pension and other retirement benefit liabilities of �563mn.

Oleksiy Soroka, CFA +44 20 7595 4878 [email protected]

Ahold ⎪ January 2006

31 European High Yield Research

Ahold, Financial Model BNPP BNPP BNPP BNPP BNPPFYE 31 December Actual Actual Actual Actual Actual Actual F�cast F�cast F�cast F�cast F�castEUR mn 2002 2003 2004 Q1 05 Q2 05 Q3 05 Q4 05 2005 2006 2007 2008 P&L SUMMARY Sales breakdown Net sales 62,683 56,068 52,000 12,966 10,447 10,249 12,291 45,953 47,106 47,601 48,757 % change -10.6% -7.3% -1.0% -0.9% 0.7% 3.9% 0.7% 2.5% 1.0% 2.4% Operating profit breakdown Stop & Shop/Giant-Landover Arena 1,186 1,012 681 235 150 166 245 796 812 791 790 % change 7.5% 7.4% 5.3% 6.1% 4.9% 5.5% 7.0% 5.9% 5.9% 5.9% 5.8% Giant-Carlisle/Tops Arena 219 105 113 39 44 -17 -17 49 64 74 73 % change 3.5% 1.9% 2.2% 2.6% 3.7% -1.5% -1.3% 1.0% 1.3% 1.5% 1.5% Albert Heijn Arena 348 289 297 90 67 62 76 295 308 316 324 % change 5.5% 4.6% 4.6% 4.5% 4.4% 4.3% 4.5% 4.4% 4.5% 4.5% 4.5% Central Europe Arena -40 -59 -54 -12 -2 -12 -14 -40 -18 5 19 % change -2.6% -3.7% -3.2% -3.0% -0.5% -2.8% -2.8% -2.3% -1.0% 0.3% 1.0% Schuitema 27 13 27 31 98 98 99 100 % change 2.9% 1.8% 3.8% 3.8% 3.1% 3.1% 3.1% 3.1% Other retail 2 0 0 0 2 0 0 0 Total retail sales 381 272 226 320 1,199 1,264 1,284 1,306 % change 4.4% 3.9% 3.4% 4.1% 4.0% 4.1% 4.2% 4.2% US Foodservice 160 -200 -74 17 35 43 55 150 277 341 402 % change 0.9% -1.3% -0.5% 0.4% 1.0% 1.2% 1.3% 1.0% 1.7% 2.0% 2.3% Group Support Office -52 -59 -907 -55 -1,073 -210 -210 -210 Operating profit 239 718 208 346 248 -638 320 276 1,331 1,415 1,498 operating margin 0.4% 1.3% 0.4% 2.7% 2.4% -6.2% 2.6% 0.6% 2.8% 3.0% 3.1% EBITA before impairments & gains on disposal & one-offs 2,399 1,328 1,341 391 268 337 405 1,401 1,519 1,603 1,686 % of net sales 3.8% 2.4% 2.6% 3.0% 2.6% 3.3% 3.3% 3.0% 3.2% 3.4% 3.5% Estimated Depreciation 1,285 1,126 1,047 246 178 183 190 797 857 917 977 EBITDA before impairments & gains on disposal & one-offs 3,684 2,454 2,388 637 446 520 595 2,198 2,376 2,520 2,663 % of net sales 5.9% 4.4% 4.6% 4.9% 4.3% 5.1% 4.8% 4.8% 5.0% 5.3% 5.5% Net cost of rentals and operating leases 866 822 682 136 136 136 136 544 510 464 418 EBITDAR before impairments & gains on disposal & one-offs 4,550 3,276 3,070 773 582 656 731 2,742 2,886 2,984 3,081 Net interest income -944 -952 -717 -193 -137 -128 -125 -583 -453 -337 -313 Gain (loss) on foreign exchange -50 14 5 3 20 16 15 54 0 0 0 Other financial income and expense -14 0 1 -22 0 0 0 -22 0 0 0 Net financial expense -1,008 -938 -711 -212 -117 -112 -110 -551 -453 -337 -313 Income before income taxes -769 -220 -503 134 131 -750 210 -275 879 1,078 1,186 Income taxes -390 72 -66 -35 -18 282 -80 149 -307 -377 -415 effective tax rate -50.7% 32.7% -13.1% 26.1% 13.7% 37.6% 38.0% 54.3% 35.0% 35.0% 35.0% Income after income taxes -1,159 -148 -569 99 113 -468 130 -126 571 701 771 Share in income/loss of joint ventures and equity investees -38 161 146 30 26 40 35 131 140 150 160 Minority interest -11 -14 -13 -5 -11 -5 -5 -26 -28 -30 -32 Net income -1,208 -1 -436 124 128 -433 160 -21 683 821 899 Dividends on cumulative pref fin. shares/inc from discont�d ops -38 -38 -44 10 2 194 0 206 0 0 0 Net income available to common shareholders -1,246 -39 -480 134 130 -239 160 185 683 821 899 CASH FLOW ITEMS EBITDA 3,684 2,454 2,388 637 446 520 595 2,198 2,376 2,520 2,663 Net cash interest expense -944 -952 -717 -193 -137 -128 -125 -583 -453 -337 -313 Other operating cash items -64 14 6 6 7 3 5 21 20 20 20 Cash flow before changes in working capital & cash taxes 2,676 1,516 1,677 450 316 395 475 1,636 1,944 2,203 2,371 Cash effect from changes in working capital 76 468 -94 -182 51 8 -50 -173 -50 -50 50 Change in other non-current assets -7 18 30 34 -2 0 0 32 0 0 0 Change in other provisions 33 53 42 12 21 0 0 33 0 0 0 Corporate income taxes paid -423 -13 -113 -47 -40 53 -21 -55 -6 -377 -415 Change in other non-current liabilities 100 -111 29 -3 -10 -263 0 -276 0 0 0 Other operating cash items 0 0 0 0 0 0 0 0 0 0 0 Net cash from operating activities 2,455 1,931 1,571 264 336 193 404 1,197 1,887 1,776 2,006 Purchase of tangible and intangible fixed assets (capex) -2,160 -1,357 -1,402 -225 -342 -366 -517 -1,450 -1,500 -1,500 -1,500 Free cash flow 295 574 169 39 -6 -173 -113 -253 387 276 506 BALANCE SHEET ITEMS Cash and cash equivalents at end of period (cont�d ops) 1,002 3,340 3,270 3,947 3,107 3,019 2,042 2,042 2,077 1,648 1,682 Including cash on hand 261 271 274 275 275 285 295 305 Cash and cash equivalents without cash on hand 3,686 2,836 2,745 1,767 1,767 1,792 1,353 1,377 Loans 5,416 5,592 5,550 4,371 4,371 3,888 3,680 3,303 Finance lease liabilities 1,592 1,708 1,728 1,719 1,719 1,617 1,515 1,413 Cumulative preferred financing shares 666 666 666 666 666 666 666 666 Long-term portion of long-term debt 8,768 7,231 7,674 7,966 7,944 6,756 6,756 6,171 5,861 5,382 Short-term borrowings 660 703 699 699 699 699 699 699 Current portion of loans 1,748 205 111 280 280 483 208 377 Current portion of finance lease liabilities 97 94 102 102 102 102 102 102 Short-term debt and current portion of long-term debt 1,991 2,039 2,505 1,002 912 1,081 1,081 1,284 1,009 1,178 Total debt 12,907 10,759 9,270 10,179 8,968 8,856 7,837 7,837 7,455 6,870 6,560 Net debt 11,905 7,419 6,000 6,232 5,861 5,837 5,795 5,795 5,378 5,222 4,878 CREDIT RATIOS Total debt/EBITDA 3.5x 4.4x 3.9x 4.4x 3.9x 3.8x 3.6x 3.6x 3.1x 2.7x 2.5x Net debt/EBITDA 3.2x 3.0x 2.5x 2.7x 2.6x 2.5x 2.6x 2.6x 2.3x 2.1x 1.8x EBITDA/Net interest expense 3.9x 2.6x 3.3x 3.4x 3.5x 3.7x 3.8x 3.8x 5.2x 7.5x 8.5x Net lease-adjusted debt/EBITDAR* 4.1x 4.3x 3.7x 3.8x 3.7x 3.6x 3.7x 3.7x 3.3x 3.0x 2.7x EBITDAR/(Net interest and lease expenses)** 2.5x 1.8x 2.2x 2.2x 2.3x 2.4x 2.4x 2.4x 3.0x 3.7x 4.2x

Source � BNP Paribas Estimates, Ahold Leverage and Coverage are based on the last 12 months� results. Some of the ratios are adjusted for the effects of acquisitions and disposals. In addition, these 2 measures are usually calculated based on EBITDA adjusted for exceptional or non-recurring items. *Leverage is defined as net lease-adjusted debt (x8 operating leases)-to-EBITDAR. ** Coverage is defined as EBITDAR-to-(net interest+rental expenses).

Alstom ⎪ January 2006

32 European High Yield Research

Alstom Bond Description & Market Data, as of 5 January 2006

Next Call Issuer Credit Trend: Positive

Description Amount (o/s) Ratings Date Price Price YTW STW

5% Senior Notes due 2006 EUR 227.6mn NR NC NC 100.5 4.00% 134bp EB + 220 Notes due 2009 EUR 600mn NR NC NC 103 3.60% 62bp 6.25% Senior Notes due 2010 EUR 1,000mn NR NC NC 106 4.62% 151bp

Source � BNP Paribas

Company Profile

Alstom is a global producer of products and services that supply the electrical power generation and transport markets. The company has production facilities in Europe (principally France, UK and Germany), North and South America, Asia and Africa. For the 12 months ended 30 September 2005, the Company had sales of �14.1bn and employed approximately 70,000 people in around 70 countries. The company is organised into 4 main divisions, power turbo systems, power service, transport and marine.

Investment Recommendation

The company�s operational and financial issues now appear well and truly behind them. Having hit a low point in H1FY05 revenues have grown strongly off the back of an improving order book. Operating margins have rebounded from a mixture of cost cutting, better contract execution and increased scale. The operational issues relating to the GT24/GT26 turbines also appear resolved with Alstom having gained new orders and the existing installed fleet is operating without incident. Alstom�s bonds have performed strongly since issued but we believe that the operational improvement will continue and drive spreads tighter. Accordingly, we have a BUY recommendation on Alstom�s bonds.

Debt Profile

The group�s main borrowings are as follows:

! Bonds Outstanding As at 30 September 2005, the group had 3 material bond issues outstanding. A 5% 2006 bond for �228mn which had been reduced from �650mn following a tender offer. In February 2005, the group issued a new �1bn 6.25% 5-year bond to finance a tender of its existing issues and raise additional finance. In September 2005 the Group issued �600mn of floating rate notes due March 2009 at Euribor plus 220bp to be used for general corporate purposes.

! Bank Debt

The group has 2 main facilities: � �704mn multi-currency revolver due 3 August 2006, undrawn at 30 September 2005. This facility is pari passu with the public bond issues. � �1,563mn PSSD subordinated bank facility due 30 September 2008, following various repayments and related cancellations, �418mn was drawn and �121mn was available at 30 September 2005.

! Other Debt

Other debt at 30 September 2005 amounts to �750mn and is structurally senior to the bonds. Included within this amount are �205mn preference shares due in 2006, �128mn of bilateral loans, �4mn of securitised receivables and �413mn of other borrowings.

! Capital Leases

Under IFRS, the company now capitalises finance leases. As at 30 September 2005 finance leases totalled �250mn.

Adam Harnetty, ACA +44 20 7595 8831 [email protected]

An officer, director, or employee of BNP Paribas currently sits on the board of Alstom.

Alstom ⎪ January 2006

33 European High Yield Research

Alstom Structure

ALSTOM(France)

ALSTOM Holdings(France)

8

7

6

5

4

3

2

1

ALSTOM UK Holdings Ltd(Holding - UK)

ALSTOM Espana IB(Holding � Spain)

ALSTOM NV(Holding � Netherlands)

ALSTOM Power Holdings Ltd(Holding � Brazil)

ALSTOM (China) Investment Co. Ltd(Holding � China)

ALSTOM Mexico SA de CV(Holding � Mexico)

ALSTOM Inc.(Holding � USA)

ALSTOM GmbH(Holding � Germany)

ALSTOM Power Holdings(France)

ALSTOM Power Boilers SA(France)

ALSTOM Power Service SA(France)

ALSTOM Power Hydro(France)

4

4

4

4

4

4

4

4

4

4

44

4

4

2

ALSTOM Power Turbomachines

(France)

ALSTOM Power Services GmbH

(Germany)

ALSTOM Power Italia SpA

(Italy)

ALSTOM Power SP Zoo(Poland)

ALSTOM Power Sweden AB

(Sweden)

ALSTOM Power Switzerland Ltd

(Switzerland)

ALSTOM Power Centrales(France)

ALSTOM Power Hydraulique

(France)

ALSTOM Power sro

(Czech Republic)

ALSTOM Power Inc

(USA)

ALSTOM Power UK Holdings Ltd

(UK)

ALSTOM Power Asia Pacific SdnBhd (Malaysia)

ALSTOM Power Generation AG

(Germany)

ALSTOM KK(Japan)

ALSTOM Power Boiler GmbH

(Germany)

ALSTOM Transport SA (France)

ALSTOM Ferroviaria SpA(Italy)

ALSTOM Transporte(Spain)

ALSTOM LHB GmbH (Germany)

ALSTOM Transporte SA DE CV (Mexico)

ALSTOM Brasil Ltda(Brazil)

ALSTOM Transport (UK)

ALSTOM Transportation Inc (USA)

ALSTOM Signaling Inc. (USA)

4

3

1

5

5

2

6

8

Chantiers de L�Atlantique(France)

ALSTOM Leroux Naval (France)

A.M.R. (France)

ALSTOM Power Conversion SA

(France)

ALSTOM Power Conversion

GmbH (Germany)

ALSTOM Power Conversion Ltd

(UK)

1

2

ALSTOM(France)

ALSTOM Holdings(France)

8

7

6

5

4

3

2

1

ALSTOM UK Holdings Ltd(Holding - UK)

ALSTOM Espana IB(Holding � Spain)

ALSTOM NV(Holding � Netherlands)

ALSTOM Power Holdings Ltd(Holding � Brazil)

ALSTOM (China) Investment Co. Ltd(Holding � China)

ALSTOM Mexico SA de CV(Holding � Mexico)

ALSTOM Inc.(Holding � USA)

ALSTOM GmbH(Holding � Germany)

ALSTOM Power Holdings(France)

ALSTOM Power Boilers SA(France)

ALSTOM Power Service SA(France)

ALSTOM Power Hydro(France)

4

4

4

4

4

4

4

4

4

4

44

4

4

2

ALSTOM Power Turbomachines

(France)

ALSTOM Power Services GmbH

(Germany)

ALSTOM Power Italia SpA

(Italy)

ALSTOM Power SP Zoo(Poland)

ALSTOM Power Sweden AB

(Sweden)

ALSTOM Power Switzerland Ltd

(Switzerland)

ALSTOM Power Centrales(France)

ALSTOM Power Hydraulique

(France)

ALSTOM Power sro

(Czech Republic)

ALSTOM Power Inc

(USA)

ALSTOM Power UK Holdings Ltd

(UK)

ALSTOM Power Asia Pacific SdnBhd (Malaysia)

ALSTOM Power Generation AG

(Germany)

ALSTOM KK(Japan)

ALSTOM Power Boiler GmbH

(Germany)

ALSTOM Transport SA (France)

ALSTOM Ferroviaria SpA(Italy)

ALSTOM Transporte(Spain)

ALSTOM LHB GmbH (Germany)

ALSTOM Transporte SA DE CV (Mexico)

ALSTOM Brasil Ltda(Brazil)

ALSTOM Transport (UK)

ALSTOM Transportation Inc (USA)

ALSTOM Signaling Inc. (USA)

4

3

1

5

5

2

6

8

Chantiers de L�Atlantique(France)

ALSTOM Leroux Naval (France)

A.M.R. (France)

ALSTOM Power Conversion SA

(France)

ALSTOM Power Conversion

GmbH (Germany)

ALSTOM Power Conversion Ltd

(UK)

1

2

Source � Alstom

Alstom ⎪ January 2006

34 European High Yield Research

Bond Covenant Bond description EB + 220 Notes due 2009 6.25% Senior Notes due 2010

Issuing entity Alstom Alstom

Ranking Senior Notes Senior Notes

Position vs. bank debt Pari passu/Senior Pari passu/Senior

Position vs. other bonds Pari passu Pari passu

Security/guarantees None None

Optional redemption No No

Tax redemption Yes � at par Yes � at par

Negative pledge Yes but listed/traded bonds only Yes but listed/traded bonds only

Cross default Yes Yes

Fall away covenants No No

Anti-layering No No

Change of control Put at 101, based on >50% voting power Put at 101, based on >50% voting power

Asset sales No No

Debt limit None None

Restricted payments None None

Transactions with affiliates None None

Source � BNP Paribas, Alstom

Alstom ⎪ January 2006

35 European High Yield Research

Alstom, Financial Model

IFRS IFRS IFRS IFRS

FYE 31 March Actual Actual Actual Actual Actual Actual Actual EUR mn 2002 2003 2004 H1 05 H2 05 2005 H1 06

PROFIT & LOSS Orders 22,686 19,123 16,500 8,363 7,478 15,841 7,454

Revenues 23,453 21,351 16,688 6,316 7,211 13,527 6,938 Cost of sales -19,623 -19,187 -14,304 -5,376 -6,190 -11,566 -5,810 Gross Margin 3,830 2,164 2,384 940 1,021 1,961 1,128 SG&A -2,889 -2,671 -2,084 -803 -791 -1,594 -781 Operating Income 941 -507 300 137 230 367 347 Restructure Charges -227 -268 -655 -69 -289 -358 -38 Pension & other -227 -354 -516 -41 -34 -75 -6 EBIT 487 -1,129 -871 27 -93 -66 303 Financial Expense -294 -270 -460 -242 -156 -398 -88 Tax -10 263 -251 -23 -140 -163 -75 Minority Interests -36 -12 2 -4 3 -1 -3 Goodwill -286 -284 -256 0 0 0 0 Net Profit/(Loss) -139 -1,432 -1,836 -242 -386 -628 137