The Great Escape?€¦ · The Great Escape? A Quantitative Evaluation of the Fed’s Non-Standard...

33

The Great Escape? A Quantitative Evaluation of the Fed’s Non-Standard Policies Marco Del Negro, Andrea Ferrero Gauti Eggertsson, Nobuhiro Kiyotaki Federal Reserve Bank of New York and Princeton University ESSIM, Tarragona (Bank of Spain); May 25, 2010 Disclaimer: The views expressed are mine and do not necessarily reflect those of the Federal Reserve Bank of New York or the Federal Reserve System

Transcript of The Great Escape?€¦ · The Great Escape? A Quantitative Evaluation of the Fed’s Non-Standard...

The Great Escape?

A Quantitative Evaluation of the Fed’s Non-Standard Policies

Marco Del Negro, Andrea FerreroGauti Eggertsson, Nobuhiro Kiyotaki

Federal Reserve Bank of New York and Princeton University

ESSIM, Tarragona (Bank of Spain); May 25, 2010

Disclaimer: The views expressed are mine and do not necessarily reflect those of the FederalReserve Bank of New York or the Federal Reserve System

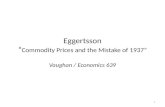

The Fed’s Response to a Black Swan

Oct07 Jan08 Apr08 Jul08 Oct08 Jan09 Apr090

0.5

1

1.5

2

2.5

Months

Trill

ions

of $

Source: Board of Governors of the Federal Reserve System, Release H.4.1

OtherTreasury SecuritiesCurrency SwapsPrimary CreditTAFReposPDCF and Other Broker−Dealer CreditOther Credit (includes AIG)Maiden Lane I,II & IIIAMLFCPFFTALFAgency DebtAgency MBS

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Questions

• We incorporate the financial friction proposed by Kiyotaki andMoore (2008) – differences in liquidity across assets – into a DSGEmodel with standard real and nominal rigidities and ask:

1 Can a KM-type liquidity shock quantitatively generate thecrisis?

• Large response of both macro and financial variables.

2 What is the quantitative effect of unconventional monetarypolicy in such a setting?

• In an environment where standard monetary policy nolonger works (the “great escape” from the liquidity trap)

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Questions

• We incorporate the financial friction proposed by Kiyotaki andMoore (2008) – differences in liquidity across assets – into a DSGEmodel with standard real and nominal rigidities and ask:

1 Can a KM-type liquidity shock quantitatively generate thecrisis?

• Large response of both macro and financial variables.

2 What is the quantitative effect of unconventional monetarypolicy in such a setting?

• In an environment where standard monetary policy nolonger works (the “great escape” from the liquidity trap)

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

KM Model – The Actors

1 Entrepreneurs =

{SavingInvesting

kt+1 =

{λkt + it with probability κλkt with probability 1− κ

2 Intermediate firms

3 Final good producing firms

4 Capital producing firms

5 Workers

6 Government

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Entrepreneurs & Frictions

• Balance sheet:

Assets Liabilities

real bonds lt+1own equity

issuedqtn

It+1

nominal bonds bt+1/Pt

equity ofother entrepreneurs qtn

Ot+1

capital stock qtkt+1 net worthqtnt+1

+lt+1 + bt+1/Pt

where nt ≡ nOt + (kt − nIt).

• Income: rkt nt

• Constraint:

nt+1 ≥ (1− φt)λnt +

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Entrepreneurs & Frictions

• Balance sheet:

Assets Liabilities

real bonds lt+1own equity

issuedqtn

It+1

nominal bonds bt+1/Pt

equity ofother entrepreneurs qtn

Ot+1

capital stock qtkt+1 net worthqtnt+1

+lt+1 + bt+1/Pt

where nt ≡ nOt + (kt − nIt).

• Income: rkt nt

• Constraint:

nt+1 ≥ (1− φt)λnt + (1− θ)it

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Entrepreneurs & Frictions

• Balance sheet:

Assets Liabilities

real bonds lt+1own equity

issuedqtn

It+1

nominal bonds bt+1/Pt

equity ofother entrepreneurs qtn

Ot+1

capital stock qtkt+1 net worthqtnt+1

+lt+1 + bt+1/Pt

where nt ≡ nOt + (kt − nIt).• Income: rkt nt

• Constraint:

nt+1 ≥ (1− φt)λnt + (1− θ)it︸ ︷︷ ︸BorrowingConstraint

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Entrepreneurs & Frictions

• Balance sheet:

Assets Liabilities

real bonds lt+1own equity

issuedqtn

It+1

nominal bonds bt+1/Pt

equity ofother entrepreneurs qtn

Ot+1

capital stock qtkt+1 net worthqtnt+1

+lt+1 + bt+1/Pt

where nt ≡ nOt + (kt − nIt).• Income: rkt nt

• Constraint:

nt+1 ≥ (1− φt)λnt︸ ︷︷ ︸ResaleabilityConstraint

+ (1− θ)it

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Entrepreneur’s problem

Max{cs ,is ,ns+1,ls+1}∞t IE t

∞∑s=t

βs−t log(cs)

subject to

nt+1 − (1− φt)λnt ≥ (1− θ)it

ct + pIt it + qt(nt+1 − it) + lt+1 +bt+1

Pt= (rkt + λ)nt + rt−1lt +

Rt−1btPt

lt+1 ≥ 0, bt+1 ≥ 0

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Entrepreneur’s problem – Saver

Max{cs ,is ,ns+1,ls+1}∞t IE t

∞∑s=t

βs−t log(cs)

subject to

nt+1 − (1− φt)λnt ≥ (1− θ)it ← not binding

⇓

ct + qtnt+1 + lt+1 +bt+1

Pt= (rkt + qtλ)nt + rt−1lt +

Rt−1btPt

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Entrepreneur’s problem – Investor

Max{cs ,is ,ns+1,ls+1}∞t IE t

∞∑s=t

βs−t log(cs)

subject to

nt+1 − (1− φt)λnt ≥ (1− θ)it ← binding

⇓

ct+qRt nt+1+lt+1+bt+1

Pt≤ [rkt +( φtqt + (1− φt)qRt )λ]nt+rt−1lt+

Rt−1btPt

where

qt > 1 > qRt =pIt − θqt

1− θ

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Key equilibrium conditions

(1− κ)IE t [1

cst+1

rkt+1 + qt+1λqt ] + κIE t [

1c it+1

rkt+1 + ((1− φt+1)qRt+1 + φt+1qt+1)λqt ]

=

(1− κ)IE t [1

cst+1rt ] + κIE t [

1c it+1

rt ]

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Key equilibrium conditions

(1− κ)IE t [1

cst+1

rkt+1 + qt+1λqt ] + κIE t [

1c it+1

rkt+1 + ((1− φt+1)qRt+1 + φt+1qt+1)λqt ]

=

(1− κ)IE t [1

cst+1rt ] + κIE t [

1c it+1

rt ]

(pIt −qtθt)It = β( κrt−1Lt + (rkt +qtφtλ)κKt )− (1−β)(1−φt)qRt λκKt

rkt Kt = It [1 + S( ItI∗

)] + τt

+ (1− β){rt−1Lt + [rkt + (1− κ + κφt)qtλ+ κ(1− φt)qRt λ]Kt

}︸ ︷︷ ︸consumption

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Key equilibrium conditions

(1− κ)IE t [1

cst+1

rkt+1 + qt+1λqt ] + κIE t [

1c it+1

rkt+1 + ((1− φt+1)qRt+1 + φt+1qt+1)λqt ]

=

(1− κ)IE t [1

cst+1rt ] + κIE t [

1c it+1

rt ]

(pIt − qtθt)It = β( κrt−1Lt+ (rkt + qtφtλ)κ(Kt − Ng

t ) )− (1− β)(1− φt)qRt λκ(Kt − Ngt )

rkt Kt = It [1 + S( ItI∗

)] + τt

+ (1− β){rt−1Lt + [rkt + (1− κ + κφt)qtλ+ κ(1− φt)qRt λ](Kt − Ng

t )}︸ ︷︷ ︸

consumption

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Government

• Taylor rule:Rt = R∗ (πt/π∗)

ψ1

• The government budget constraint is:

Lt+1 − rt−1Lt +Bt+1 − Rt−1Bt

Pt= τt ,

• In absence of intervention: Lt+1 = L∗, Bt+1 = 0.

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Unconventional monetary policy

• Intervention rules:

Ngt = K∗ξ(

φtφ∗− 1).

qt (Ngt − Ng

t ) = Lt − Lt .

• The government budget constraint:

τt = (rt + qtλ)Ngt − rt−1Lt + rkt N

gt − qtN

gt+1 + Lt+1,

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Liquidity Share: LL+qK

1990 1992 1994 1996 1998 2000 2002 2004 2006 20086

8

10

12

14

16

18

Quarters

Perc

ent

Liquidity Share

ls2008Q4

− ls2008Q3

= 23.5%

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Steady State as a Function of φ∗

(for L∗/Y∗ = .40)

0.1 0.12 0.14 0.16 0.18 0.212.5

13

13.5

14

14.5

15

φ

%

Liquidity share

0.1 0.12 0.14 0.16 0.18 0.20.8

1

1.2

1.4

1.6

φ

q

0.1 0.12 0.14 0.16 0.18 0.2−10

−5

0

5

10

φ

% an

nuali

zed

Real return on liquid asset

0.1 0.12 0.14 0.16 0.18 0.2−4

−2

0

2

4

6

8

φ

% an

nuali

zed

Equity premium

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Calibration

• Impose θ = φ = 15% to obtain:

1 steady state liquidity share of 14%2 real return on liquid assets of 2% (1952Q1:2008Q4)

• Probability of receiving investment opportunity: κ = 6%

Doms and Dunne (1998) and Cooper, Haltiwanger and Power (1999)

• Standard stuff:• Discount factor: β = 0.991• Depreciation rate: λ = 0.975 (Annual depreciation = 10%)• Capital share: γ = 0.33• Taylor rule response to inflation: ψ1 = 1.5• Inverse Frisch elasticity: ν = 1• Nominal rigidities : ζp = ζw = .66• Investment adjustment costs: S ′′(1) = 3

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Calibration of the φt Shock and the Fed’s Response

• Expected duration of the liquidity shock (Markov process):• 8 quarters (Baseline) , 8 years (Extreme) (Japan, Great Depression)

−2 0 2 4 6 8 10 12 14 16 18 200

5

10

15

20

25

% Δ

from

stead

y stat

e

Liquidity Share

−2 0 2 4 6 8 10 12 14 16 18 200

0.2

0.4

0.6

0.8

1

Time (Quarters after initial shock)

Trilli

ons o

f $

Government Purchase of Private Equity

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Paths for the Nominal Interest Rate

−2 0 2 4 6 8 10 12 14 16 18 20−1

−0.5

0

0.5

1

1.5

2

2.5

3

3.5

4

Quarters

Annu

alize

d %

poi

nts

Nominal Interest Rate

IRFContingency

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Response of Macro Variables to a liquidity shock(with intervention)

0 10 20−6

−4

−2

0

% Δ

from

ste

ady

stat

e

Output

0 10 20−5

−4

−3

−2

−1

0

Annu

alize

d %

poi

nts

Inflation

0 10 200

0.5

1

1.5

2

2.5Nominal Interest Rate

2006 2008 2010−6

−4

−2

0

Quarters

Log−

leve

l (20

08Q

2 =

0)

GDP

2006 2008 2010−10

−5

0

5

Quarters

Annu

alize

d %

poi

nts

CPI

2006 2008 20100

2

4

6

Quarters

FFR

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Response of Financial Variables to a liquidity shock(with intervention)

0 5 10 15 200

100

200

300

400

Annu

alize

d bp

s.

Spread Illiquid−Liquid Assets

0 5 10 15 20−8

−6

−4

−2

0

% Δ

from

ste

ady

stat

e

Tobin Q

2006 2007 2008 20090

100

200

300

400

500

Quarters

Annu

alize

d bp

s.

Empirical Spreads (1st P.C.)

2006 2007 2008 2009−60

−40

−20

0

20

Quarters

Log−

leve

l (20

08Q

2 =

0)

Wilshire 5000

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

The Effect of Policy Intervention

0 5 10 15 20−10

−8

−6

−4

−2

0

% Δ

from

ste

ady

stat

e

Output

0 5 10 15 20−8

−6

−4

−2

0

Annu

alize

d %

poi

nts

Inflation

0 5 10 15 200

100

200

300

400

Quarters

Annu

alize

d bp

s.

Spread Illiquid−Liquid Assets

0 5 10 15 20−15

−10

−5

0

Quarters

% Δ

from

ste

ady

stat

e

Tobin Q

Policy Response No InterventionDel Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

The Great Escape?

−2 0 2 4 6 8 10 12 14 16 18 20−20

−15

−10

−5

0

% Δ

from

ste

ady

stat

e

Output

−2 0 2 4 6 8 10 12 14 16 18 20−20

−15

−10

−5

0

Quarters

Annu

alize

d %

poi

nts

Inflation

Policy ResponseNo Intervention

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Multipliers

E0

∑∞t=0(Y I

t − Y Nt )

E0

∑∞t=0 N

gt+1

Baseline Great Escape

Full model 0.643 2.240No zero bound constraint 0.247 0.309No nominal rigidities 0.064 0.052

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

The Role of the Nominal Rigidities

0 5 10 15 20−15

−10

−5

0

% Δ

from

ste

ady

stat

e

Output

0 5 10 15 20−6

−4

−2

0

2

4

Annu

alize

d %

poi

nts

Real Interest Rate

0 5 10 15 20−10

−8

−6

−4

−2

0

Quarters

% Δ

from

ste

ady

stat

e

Investment

0 5 10 15 20−15

−10

−5

0

5

Quarters

% Δ

from

ste

ady

stat

e

Consumption

Baseline & Intervention Baseline & No Intervention Flex Price & Intervention Flex Price & No InterventionDel Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

The Role of the Zero Bound

0 5 10 15 20−15

−10

−5

0

% Δ

from

ste

ady

stat

e

Output

0 5 10 15 20−8

−6

−4

−2

0

Quarters

Annu

alize

d %

poi

nts

Inflation

0 5 10 15 20−4

−2

0

2

Quarters

Annu

alize

d %

poi

nts

Nominal Interest Rate

ZB & InterventionZB & No InterventionNO ZB & InterventionNO ZB & No Intervention

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Conclusions

1 Liquidity shocks as in Kiyotaki-Moore model can generatequantitatively large movements in real and financial variables → canexplain some features of the crisis

2 Swap of liquid for illiquid assets (unconventional policy) is effectivein reducing impact on spreads and real variables

• Caveat: This is not a model for normative analysis!!!

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Investment Adjustment Costs

• Capital producers:

maxItC (It) = pIt It − It [1 + S(ItI∗

)]

with S(1) = S′(1) = 0, S′′(1) > 0

⇒ pIt = 1 + S( ItI∗

) + S ′( ItI∗

) ItI∗

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Sticky Prices

• Monopolistic competitors produce intermediate goods withtechnology:

yt (i) = Atkt (i)γ lt (i)1−γ ,

subject to Calvo price rigidity (ζp).

• Final goods producers aggregate: yt =[∫ 1

0yt (i)

11+λf ,t di

]1+λf ,t

• Inflation determined by New-Keynesian Phillips curve

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape

Workers

Max{c′s ,h′s ,n′s+1,b′s+1,l

′s+1} ∞t Et

∞∑s=t

βs−tU[c ′s −∫

ω0

1 + νhs(ω)

′ 1+νdω]

subject to

c ′t + qt(n′t+1 − λn′t) + l ′t+1 − rt−1l

′t +

b′t+1−Rt−1b′t

Pt≤

rkt n′t +

∫ Wt(ω)Pt

h′t(ω)dω + C (It) +∫P(i)di + τt

l ′t+1 ≥ 0, b′t+1 ≥ 0, n′t+1 ≥ 0

and to Calvo nominal rigidities (ζw ). Differentiated labor h′t (w), packedinto a composite:

h′t =

[∫ 1

0

h′t (w)1

1+λw di

]1+λw

.

Del Negro, Ferrero, Eggertsson, Kiyotaki The Great Escape