THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY

69

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Transcript of THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY2014-2019

The Gambia sesame sector development and export strategy was developed on the basis of the process, methodology and technical assistance of the International Trade Centre ( ITC ). The views expressed herein do not reflect the official opinion of ITC. This document has not been formally edited by ITC.

The International Trade Centre ( ITC ) is the joint agency of the World Trade Organization and the United Nations

Street address: ITC 54-56, rue de Montbrillant 1202 Geneva, Switzerland

Postal address: ITC Palais des Nations 1211 Geneva 10, Switzerland

Telephone: +41-22 730 0111

Fax: +41-22 733 4439

E-mail: [email protected]

Internet: http://www.intracen.org

photo next page : Sarah R.Layout : Jesús Alés ( sputnix.es )

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

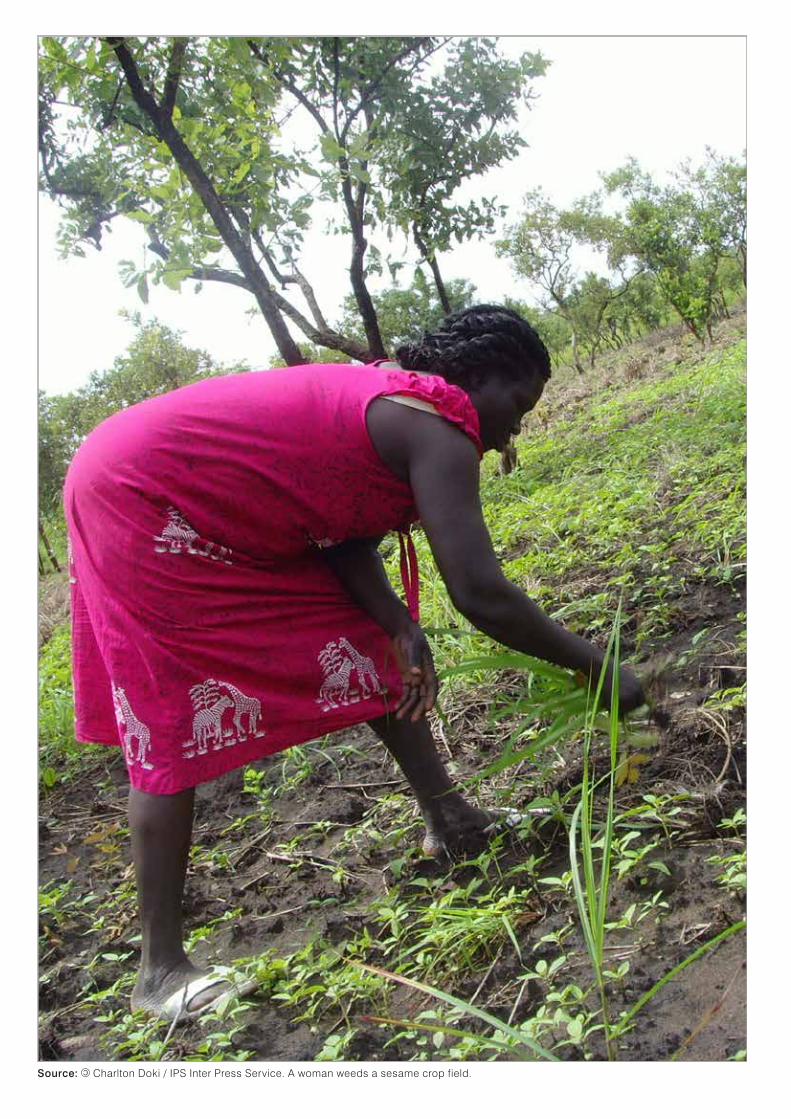

Source: Charlton Doki / IPS Inter Press Service. A woman weeds a sesame crop field.

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019 III

ACKNOWLEDGEMENTS

The Gambia sesame sector development and export strategy was made possible with the support of the Enhanced Integrated Framework (EIF), the commit-ment of the Ministry of Trade, Regional Integration and Employment (MOTIE) and the Ministry of Agriculture (MOA), and the active participation of various interme-diary organizations including the National Agricultural Research Institute (NARI), Gambia Investment and Export Promotion Agency (GIEPA), Agribusiness Services Plan Association and the National Women Farmers Association (NAWFA).

This document represents the ambitions of the private and public sector stakeholders who devoted themselves extensively in defining the enhancements and future orientations for the sector to raise its growth and trade performance.

Technical support and guidance from the International Trade Centre (ITC) was rendered through Mr Charles Roberge and Mr Isaac Ndungú. Mr. Mohammed E. Jammeh was the national consultant and coordinated stakeholder consultations. Mr. Njaga Jawo, Executive Director of NAWFA, provided guidance throughout the design process.

The efforts and contributions of all sesame sector stake-holders, particularly the members of the National Sesame Sector Taskforce, towards the development of the sector strategy are highly appreciated.

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019IV

FOREWORD BY ARANCHA GONZÁLEZ, EXECUTIVE DIRECTOR, ITC

Sesame is a relatively new crop in The Gambia that emerged as an alternative staple and export commodity to groundnut. The sector’s rapid growth in the 1990s and early 2000s was achieved as a result of efforts by national and international partners to organize sesame growers associations ( SGAs ), which are mainly composed of women. Waning support from international partners and the partial weakening of the SGAs in recent years has seen Gambian sesame production contract.

This sesame sector development and export strategy comes at an opportune time to revitalise the sector. The strategy is aligned with and builds on national develop-ment plans including the National Development Vision 2020, the Agriculture and Natural Resources ( ANR ) Policy 2009-2015, the Gambian National Agricultural Investment Plan ( GNAIP ) 2011-2015, Program for Accelerated Growth and Employment ( PAGE ) 2012-2015 and the National Trade Policy.

With the commitment of the Ministry of Trade, Industry, Regional Integration and Employment ( MOTIE ), the Ministry of Agriculture ( MOA ), and the private sector, this sesame strategy aims for The Gambia to become an im-portant producer, processor and exporter of quality sesa-me seeds and value-added products in West Africa. This augurs well in terms of creating new synergies through intercropping with other emerging sectors such as cash-ew, employment generation for rural youth and women as well as contributing to food security in The Gambia.

The participative design process of this ITC-facilitated sector strategy involved close cooperation with the public and the private sectors and has secured stakeholders’ ownership of the strategy. Concerted efforts of public, private and international partners to identify the sec-tor’s constraints and opportunities will enable a renewed expansion of the sector. With production rehabilitated, stronger value chain processes, improved governance and by leveraging port facilities, the sector’s ability to capitalize on new emerging market access opportuni-ties will increase.

The success of the strategy will now depend on its imple-mentation. Without effective implementation of the strat-egy’s plan of action, the sesame sector’s potential will remain unexploited. The public and private coordination efforts deployed during the design of the strategy now need to shift focus to mobilizing resources and managing and monitoring the implementation of the strategy. ITC is delighted to have partnered in this initiative and stands ready to continue with its engagement and extending as-sistance in the transition to implementation of the cashew sector strategy.

Arancha GonzálezITC Executive Director

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019 V

OFFICIAL STATEMENT FROM THE MINISTER OF TRADE, INDUSTRY, REGIONAL INTEGRATION AND EMPLOYMENT

The development of the sesame sector strategy, under the Sector Competitiveness and Export Diversification Project, is part of the national efforts to promote the pro-duction of sesame which has emerged over the years as an alternative cash crop to groundnut that could also contribute to food security in the Gambia. This strategy provides a focus direction in the crusade to address a variety of supply-side issues that hindered the develop-ment of the sesame sector in the Gambia. The Ministry of Trade, Industry, Regional Integration and Employment thus lend its support to the preparation of this strategy which is in line with national food security and export diversification policies of the government.

The formulation of the strategy has been participatory, involving public and private sectors as well as the Non-governmental organizations, and Government will collab-orate with all partners for its effective implementation. The strategy aims to increase the volume of sesame produced in the Gambia and this will be supported with improved ca-pacities for processing for access to high value markets.

The Government of the Gambia looks forward to the thor-ough execution of the strategy and will continue its efforts in maintaining macroeconomic stability, improving the competitiveness of the economy and encouraging pri-vate investment in production and processing of sesame to achieve the vision of strategy i.e. “To be among the leading producers, processors and exporters of qual-ity value-added sesame products within the sub-region and Africa”.

The National Coordination Committee for the sesame sec-tor will also be closely linked to the NES Implementation Committee to ensure effective coordination and moni-toring of the implementation of the strategy as well as to ensure synergy in the national efforts to promote develop-ment of the sesame sector in the Gambia.

The Government of the Gambia looks forward to effec-tive partnership with all relevant private stakeholders, key financial and technical partners, donors and investors in the implementation of the strategy.

Finally, I also wish to extend my thanks and gratitude to ITC, and all other institutions and individuals who sup-ported the preparation of this strategy.

Hon. Abdou KolleyMinister of Trade, Industry, Regional

Integration and Employment

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019VI

OFFICIAL STATEMENT FROM THE MINISTER OF AGRICULTURE

The agricultural sector is guided by the Agriculture and Natural Resources ( ANR ) Policy and Gambia National Agriculture Investment Programme ( GNAIP ) to achieve the development goals of the agricultural sector in The Gambia. Considering that there is a great need for in-creased and focused investment in the agriculture sector, the GNAIP is an important strategy to mobilise the much needed investment to help increase agricultural produc-tion, productivity and most importantly, ensure food and income security, and reduce poverty. The Development of agricultural chains and market promotion is an im-portant sub-component of the GNAIP comprising the development of food processing chains, strengthening of national operator support services and promotion of intra-regional and extra-regional trade.

The Gambia Sector Development and Export Strategy-Sesame developed under the Sector Competitiveness and Export Diversification Project therefore, compliments and contributes to the realization of the goals of both the GNAIP and ANR Policy by intervening in the development of the sesame sector.

The development of this strategy document particularly took an approach which included a value chain analy-sis and diagnostic of the sector, defined strategic ori-entations and developed detailed plan of action with clear objectives, activities, target measures, and roles for implementing institutions. It is also important to note that all these involved the active participation of sector stakeholders.

Therefore, it is strongly believed that the contents of this sector strategy carries the collective thoughts on the chal-lenges of the sector and what actions need to be taken to reach our common objective.

Hence, the Ministry of Agriculture gives its full support and also call on all its partners to provide support in what-ever form to the full implementation of the strategy to contribute to the development of the agriculture sector in general and the sesame sector in particular.

Hon. Solomon OwensMinister of Agriculture

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019 VII

STATEMENT FROM NAWFA

Sesame as a relatively new crop in the Gambia has gained prominence in the recent past and is becoming a competitor of other cash crops. Sesame as a close subtitle to groundnut is becoming a major export crop next to groundnut and cashew and is playing a vital role to the socio economic development of the Gambia. The growing sesame industry has great potential in both the domestic and international markets mainly driven by the commercially viable and conducive national policy instru-ments and business environment.

The dynamic private sector of the Gambia has paved the way for a vibrant sesame sector growth and development.

NaWFA is an apex of membership based National Women Farmers’ Association dedicated to promoting and improvement of the sesame industry in the Gambia. It has been in the fore front of sesame promotion since its introduction in the early eighties by Catholic Relief Society ( CRS ). NaWFA Focuses more on increased production and productivity, improved access to markets, promotion of value-added processing, increased access to produc-tive resources by farmers, improved organizational man-agement and advocacy skills of farmers, literacy levels and enhancing members capacity to influence relevant policies and decision making at all levels.

The Sesame Sector Development Committee estab-lished under the Sector Competitiveness and Export Diversification Project ( SCEDP ) was tasked with the re-sponsibility of overseeing and coordinating the develop-ment and implementation of a sector strategy. NaWFA was given the honor of chairing the committee and was well represented in all the committee’s deliberations.

During the period under review Sesame stakehold-ers who constituted the committee met several times which resulted to the formulation of the Sesame Sector Strategy. Multi-stakeholder workshops were conducted to diagnose the value chain and the sector constraints, defined the overall development visions of the sector and proposed strategic objectives. The Sesame Sector Development Committee together with stakeholders

constructed the problem tree from which an action plan was formulated based on prioritization of activities to complete the development of the sector strategies. The Sector strategy was finally validated by the stakeholders including Government.

The project has immensely contributed to the building of capacities of stakeholders including NAWFA in enabling the establishment of a strategy implementation commit-tee that is responsible for coordinating the Sesame Sector strategy implementation 2013 to 2019. This will form the basis for the development of more proposals to raise funds for the sesame sector. NaWFA is currently acting as the national secretariat (temporal) and tasked with re-sponsibility of chairing the committee meetings.

NaWFA as an association on behave of its entire mem-bership would like to express its appreciation to the Government of The Gambia and its bi-lateral partner-ship with the ITC and its line ministry of Trade and the Enhanced Integrated Framework project for giving so much support for the sesame sector. We pray that the vision, mission and the goals we set for ourselves are successfully achieved.

Njagga .B. Jawo Executive Director

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019VIII

ACKNOWLEDGEMENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . III

FOREWORD BY ARANCHA GONZÁLEZ, EXECUTIVE DIRECTOR, ITC . . . . . . . . . . . IV

OFFICIAL STATEMENT FROM THE MINISTER OF TRADE, INDUSTRY, REGIONAL INTEGRATION AND EMPLOYMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . V

OFFICIAL STATEMENT FROM THE MINISTER OF AGRICULTURE . . . . . . . . . . . . . . . VI

STATEMENT FROM NAWFA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . VII

ACRONYMS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . XI

EXECUTIVE SUMMARY 1

INTRODUCTION 5

WHERE WE ARE NOW 6

HISTORICAL PERSPECTIVE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

CURRENT CONTEXT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

VALUE CHAIN OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

CURRENT VALUE CHAIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

SECTOR IMPORTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

GLOBAL PERSPECTIVE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

THE GAMBIA’S SESAME TRADE PERFORMANCE . . . . . . . . . . . . . . . . . . . . . . 16

THE INSTITUTIONAL PERSPECTIVE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

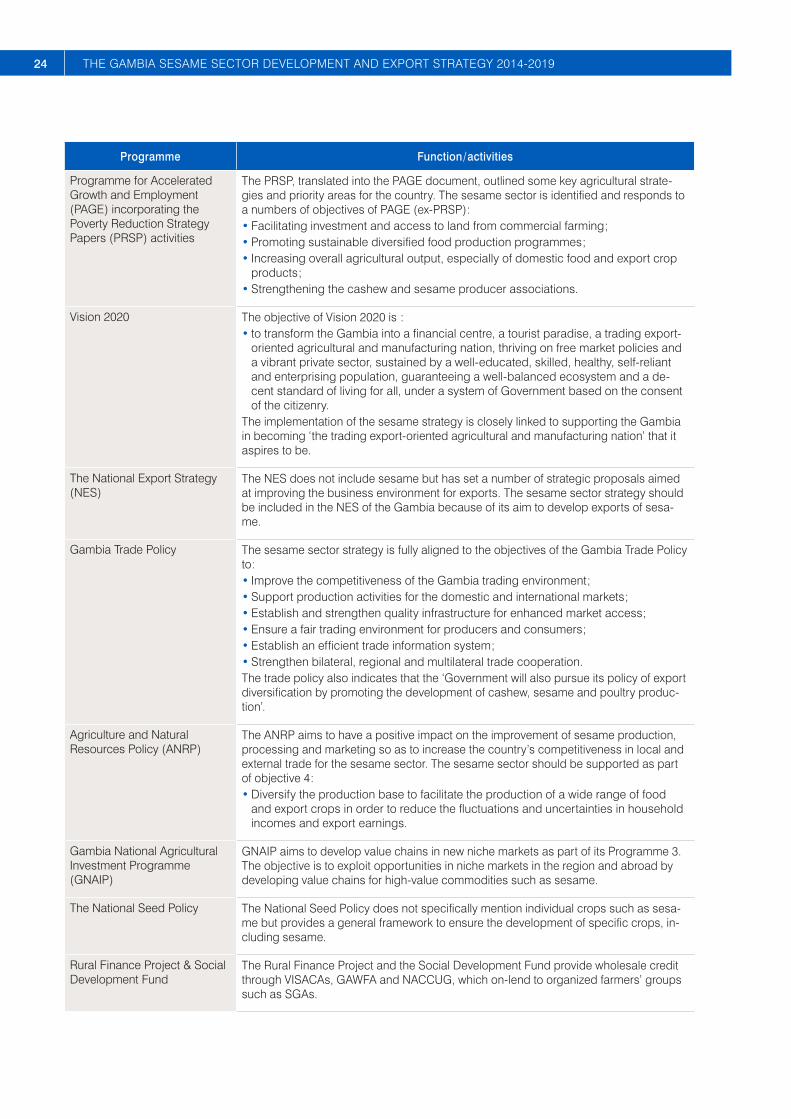

RELEVANT DEVELOPMENT STRATEGIES AND PROGRAMMES . . . . . . . . . . 23

TRADE COMPETITIVENESS ISSUES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

WHERE WE WANT TO GO 31

VISION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

FUTURE VALUE CHAIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

MARKET IDENTIFICATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

STRATEGIC OPPORTUNITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

CONTENTS

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019 IX

HOW TO GET THERE 37

STRATEGIC OBJECTIVES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

IMPORTANCE OF COORDINATED IMPLEMENTATION . . . . . . . . . . . . . . . . . . 37

PLAN OF ACTION FOR THE GAMBIA’S SESAME SECTOR 39

BIBLIOGRAPHY 49

APPENDIX 1 : SECTOR STRATEGY DESIGN STAKEHOLDERS 51

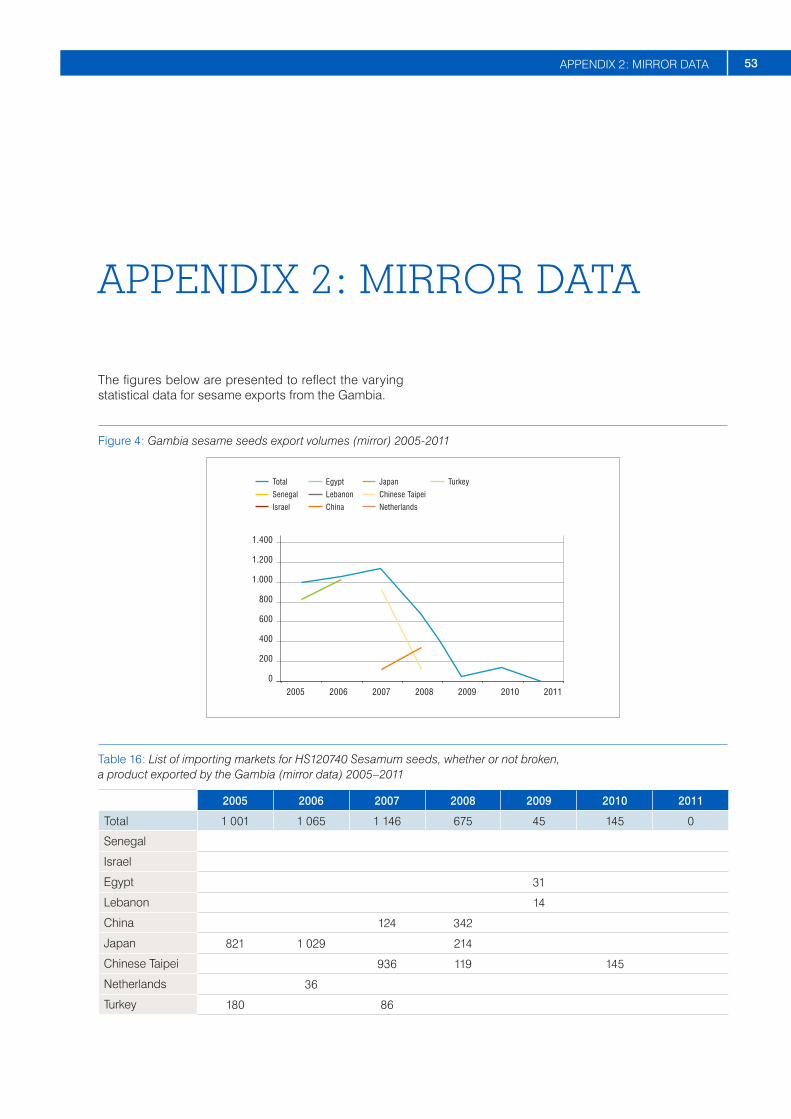

APPENDIX 2 : MIRROR DATA 53

LIST OF FIGURES

Figure 1 : Unit value differential per main buyers ( 2011 ) ( percent ) . . . . . . . . . . . . . . . . 15

Figure 2 : Total value of imports and exports for the Gambia ( 2007–2011 ) . . . . . . . . . . 15

Figure 3 : The Gambia’s sesame exports ( mirror data ) 2001–2011 . . . . . . . . . . . . . . . . . 16

Figure 4 : Gambia sesame seeds export volumes ( mirror ) 2005-2011 . . . . . . . . . . . . . . 53

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019X

TABLES

Table 1 : Sesame production, harvested areas, yields and exports 2005–2011 . . . . . . 7

Table 2 : Global producers of sesame seeds 2006-2011 . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Table 3 : Varieties of sesame seeds studied by NARI ( 2004 ) . . . . . . . . . . . . . . . . . . . . . . . 8

Table 4 : Production cycle of sesame in the Gambia . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Table 5 : Major importers of sesame seeds and oil . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

Table 6 : Major exporters of sesame seeds and sesame oil . . . . . . . . . . . . . . . . . . . . . . . 14

Table 7 : Gambian sesame exports ( direct data ), 2008-2011* . . . . . . . . . . . . . . . . . . . . . 16

Table 8 : Gambian sesame exports ( mirror data ), 2007–2010 . . . . . . . . . . . . . . . . . . . . . 17

Table 9 : Gambian sesame sector policy support network . . . . . . . . . . . . . . . . . . . . . . . . 18

Table 10 : Gambian sesame sector trade services network . . . . . . . . . . . . . . . . . . . . . . . 19

Table 11 : Gambian sesame sector business services network . . . . . . . . . . . . . . . . . . . . 21

Table 12 : Gambian sesame sector civil society network . . . . . . . . . . . . . . . . . . . . . . . . . 22

Table 13 : Perception of Gambian sesame sector TSIs – influence vs. capability . . . . 22

Table 14 : Short-term phase ( 0-3 years ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Table 15 : Medium-long term phase ( 3+ years ) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Table 16 : List of importing markets for HS120740 Sesamum seeds, whether or not broken, a product exported by the Gambia ( mirror data ) 2005–2011 . . . . . . 53

THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019 XI

ACRONYMS

ANRP Agricultural and Natural Resources Policy

ASYCUDA Automated System for Customs Data

CRR Central River Region

CRS Catholic Relief Services

DCD Department of Community Development

DOA Department of Agriculture

DOP Department of Planning

EIF Enhanced Integrated Framework

EU European Union

FAO Food and Agriculture Organization of the United Nations

FBS Farmer Business School

FFS Farmer Field Schools

GAP Good Agricultural Practices

GAWFA Gambia Women’s Finance Association

GCCI Gambia Chamber of Commerce and Industry

GIEPA Gambia Investment and Export Promotion Agency

GNAIP Gambia National Agricultural Investment Programme

GRA Gambia Revenue Authority

GSB Gambia Standards Bureau

GTTI Gambia Technical Training Institute

ITC International Trade Centre

MFI Microfinance Institution

MOA Ministry of Agriculture

MOBSE Ministry of Basic and Secondary Education

MOFEA Ministry of Finance and Economic Affairs

MOTIE Ministry of Trade, Regional Integration & Employment

MoU Memorandum of Understanding

NACCUG National Association of Cooperative Credit Unions

NACOFAG National Coordinating Organization for Farmers’ Associations, the Gambia

NARI National Agriculture Research Institute

NAWFA National Women Farmers Association

NBR North Bank Region

NCC–sesame National Coordination Committee for the sesame sector

NES National Export Strategy

NGO Non-Governmental Organization

PAGE Plan for Accelerated Growth and Employment

PoA Plan of Action

PRSP Poverty Reduction Strategy Papers

SCEDP Sector Competitiveness and Export Diversification Project

SGA Sesame Growers Association

SWOT Strength, Weakness, Opportunities and Threats

TSI Trade Support Institution

URR Upper River Region

UTG University of the Gambia

VISACA Village Savings and Credit Association

Source: liloh. Sesame harvest.

Source: Malino. Sesame-fruit

1EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

The Gambia sesame sector development and export strategy has been designed following a participatory process involving the public and private sectors. Using the technical guidance and support of the International Trade Centre, the strategy analyses key constraints fac-ing the sector in order to identify strategic opportunities to improve and sustain the competitiveness of the sector.

The sesame sector has emerged as an alternative cash crop to groundnut that could also contribute to food se-curity in the Gambia. The sector’s importance is linked to its growing production and export volumes between 2000 and 2010. However, this high performance has declined in the last few years for a variety of reasons, ranging from internal coordination to limited access to critical inputs. The sector’s future development will depend on the ability of sector stakeholders from both the public and private sectors to address and resolve key constraints.

CURRENT PERFORMANCE

At the moment production is much reduced from its 1986 peak of 4,000 tons cultivated over an area of 12,000 hectares ( ha ). According to Food and Agriculture Organization of the United Nations ( FAO ) statistics, ses-ame production, harvested areas and yields have re-mained relatively constant since 2005 with an average production volume of 2,697 tons per year cultivated over an average area of 7,225 ha.

The current low volumes of sesame seed production limit the development of a processing industry. There is some limited processing of sesame in the Gambia,1 with most of the transformation being done through traditional pro-cesses to produce sesame oil, biscuits, sesame cake ( animal feed ) and paste at village level.

The Gambia’s sesame exports show major fluctuations over the years, with a clear growth recorded up to 2009.

1. In order to promote the processing of sesame into oil, a Catholic Relief Services ( CRS ) project in the 1980s strategically installed 16 oil expellers ( processing equipment ) around the country.

Thereafter there was a sharp decline in production and exports. According to Comtrade data ( mirror data ),2 the highest total export value of sesame was recorded in 2008 at over US $ 1 million. The analysis shows the bulk of the Gambia’s total sesame exports between 2008 and 2010 going to Senegal with no exports reported in 2011. While direct data indicates exports in recent years being mini-mal and going only to Senegal, mirror data reflects higher values of exports and to a variety of destinations. This im-age of Gambian sesame exports demonstrates a much greater capacity of the country to export to varied desti-nations and reach some of the world’s largest importers.

The development of the sesame sector has been hin-dered by a variety of supply-side issues such as limited cultivated areas dedicated to sesame production ; inad-equate quality and quantity of seeds available for plant-ing ; low application of Good Agricultural Practices ( GAP ) ; imperfect access to key inputs for efficient production ; important post-harvest losses ; and insufficient business management skills. Numerous challenges, such as the fragile organization and limited coordination of the sec-tor and the absence of structured government support for development of the sector, also impede its growth.

STRATEGIC ORIENTATIONS

The strategy design process has defined a number of market and strategic opportunities available to sec-tor stakeholders to stimulate the sector’s growth. In the short term, the objective of the strategy is to increase the volume of sesame produced in the Gambia in order to position the sesame sector as a reliable provider of high quality seeds. This is a key requirement to initiate further development of processing and exports. Once sesame production volumes increase, key target markets have been identified such as Chinese Taipei, China, Senegal, Japan, Israel, Lebanon and Turkey.

2. Direct data refers to the statistics reported by the Government of the Gambia to the United Nations statistics division and its trade department ( Comtrade ). Mirror data refers to data reported by importing countries to Comtrade.

2 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

In the longer term attention will turn to Gambian hotels and restaurants and diaspora retail shops. Provision of sesame products to the tourism industry in the Gambia will require the development of processing capacities to provide varied and high quality products. An increase in processing capacity and adherence to quality require-ments will permit the development of an export market for processed products. A key target group for initiating exports of Gambian processed sesame products is the Gambian diaspora in the European Union ( EU ) and the United States of America.

In terms of structural enhancements to the sector, the strategy proposes to intercrop with other produce to in-crease acreage ; reduce wastage in post-harvest han-dling ; expand processing capacity ; link with the tourism sector ; provide specialized business and farming skills training ; develop a youth integration programme ; and initiate organic production programmes.

ROADMAP TO SECTOR DEVELOPMENT

In order to realize the development and export potential of the Gambian sesame sector, the following vision has been adopted :

“To be among the leading producers, processors and exporters of quality value-added sesame products

within the subregion and Africa. ”

Source: Saksan.

3EXECUTIVE SUMMARY

To achieve this vision, the strategy will reduce binding constraints on trade competitiveness and capitalize on strategic options identified for the Gambian sesame sec-tor. The sector strategy vision will be achieved through the implementation of the Plan of Action ( PoA ). This PoA revolves around the following strategic objectives, each spelling out specific sets of activities intended to address both challenges and opportunities facing the sesame sector in the Gambia :

� Increase in a sustainable manner the volume of sesa-me production in the Gambia ;

� Strengthen the coordination, organization and institu-tional arrangements of sesame sector support institu-tions for better service delivery ;

� Improve market development methods to increase do-mestic production / consumption and expand exports in value and volumes ;

� Increase socioeconomic benefits by promoting value addition across the entire sector value chain.

To build the desired competitiveness the sector requires credible institutional support systems in both government and private sectors. An umbrella body needs to be es-tablished to coordinate the activities of and support to the sector. Until this occurs, NAWFA should coordinate the sector’s activities in collaboration with the proposed National Coordinating Committee for sesame ( NCC–ses-ame ). The existing initiatives in the country such as the Agricultural and Natural Resources Policy ( ANRP ), the Plan for Accelerated Growth and Employment ( PAGE ), the Seed Policy, the National Export Strategy ( NES ), and GIEPA’s investment promotion efforts will need to

be stepped up to facilitate the expansion of production and processing and the development of key target mar-kets, including the tourism industry.

IMPLEMENTATION MANAGEMENT

The achievement of these ambitious objectives will re-quire continuous and coordinated efforts from all relevant private and public stakeholders as well as support from key financial and technical partners, donors and inves-tors. Several institutions are designated to play a leading role in the implementation of the sector PoA and bear the overall responsibility for successful execution of the strategy. Each institution mandated to support the export development of the sesame sector is clearly identified in the strategy’s PoA.

The proposed NCC – sesame will facilitate the public –private partnership in coordinating and implementing the sesame strategy. In particular, the committee will be tasked with coordinating the implementation of activi-ties in order to optimize the allocation of both resources and efforts across the wide spectrum of stakeholders. Responsibilities of the committee will also include moni-toring the results of activities and outputs, while at the same time recommending to the Gambian government actions or policies that could serve to achieve the stra-tegic objectives. Moreover, the committee will play a key role in recommending revisions and updates to the strat-egy so that it continues to evolve in alignment with the Gambia’s changing needs.

Source: Dick Culbert. Sesamum indicum, source of sesame oil and seeds.

4 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Box 1 : Methodological note

The approach used by ITC in the strategy design process relies on a number of analytical elements such as value chain analysis, trade support network ( TSN ) analysis, problem tree, and strategic options selection, all of which form major building blocks of this sector export strategy document.

Value chain analysis : A comprehensive analysis of the sector’s value chain is an integral part of the strategy develop-ment process. This analysis results in the identification of all players, processes and linkages within the sector. The process served as the basis for analysing the current performance of the value chain and for deliberating on options for the future development of the sector.

TSN analysis : The trade support network comprises the support services available to the primary value chain play-ers discussed above. It is constituted of policy institutions, trade support organisations, business services providers and civil society. An analysis of the quality of service delivery and constraints affecting the constituent trade support institutions ( TSIs ) is an important input to highlight gaps in service delivery relative to specific sector needs. A sec-ond analysis of TSIs assessed their level of influence ( i.e. their ability to influence public policy and other develop-ment drivers in the country and therefore make things happen or change ) and their level of capacity to respond to the sector’s needs.

Problem tree analysis : The problem tree analysis used is based on the principles of root causes analysis. The prob-lem tree provides a deeper understanding of what is causing the sector’s constraints and where solution-seeking activities should be directed. As a critical step in the analytical phase of the sector’s performance, the problem tree guides the design of realistic activities in the strategy’s plan of action.

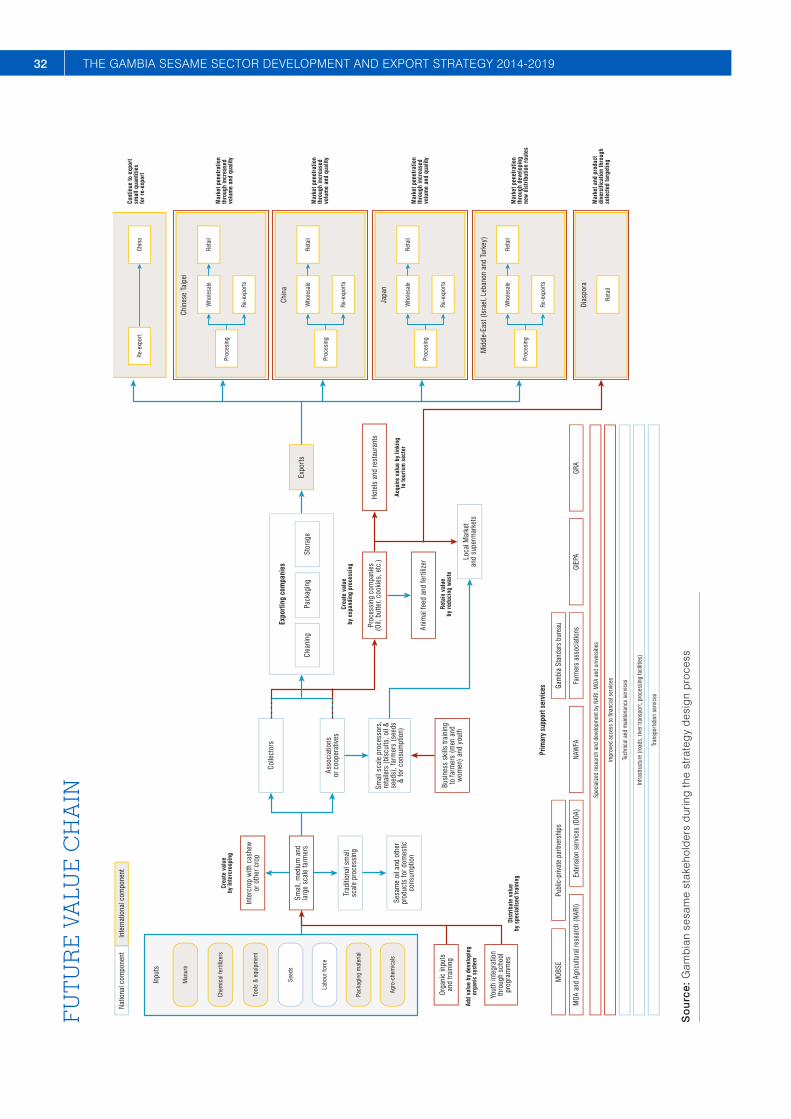

Strategic orientations : The strategic options for the development of the sector are reflected in the future value chain, which is the result of consultations, surveys and analysis conducted as part of the sector strategy design process. The future perspective has two components:

� A market-related component involving identification of key markets in the short and medium- to-long term for Gambian exporters, and ;

� Structural changes to the value chain that result in either strengthening of linkages, or introduction of new linkages. Realistic and measurable plans of actions : The definition of recommendations and strategic directions for the de-velopment of the sector is essential to guide its development, but is not enough. It is important to clearly define the actions to be implemented to stimulate growth. The development of a detailed action plan, defining which activities need to be undertaken by sector stakeholders is necessary to the effective implementation of the strategy. An action plan, developed with the support of ITC, includes performance indicators to ensure effective monitoring and evalu-ation of the strategy’s implementation.

5INTRODUCTION

INTRODUCTION

The sesame sector analysis and strategy presented in this document have been elaborated as part of the Sector Competitiveness and Export Diversification Project ( SCEDP ) of the Enhanced Integrated Framework ( EIF ). The project is being elaborated and implemented in full cooperation with the Government of the Gambia. The ini-tiative has also been fully supported by the private sector operators of the sector.

Sesame has emerged in the last 20 years as an alterna-tive cash crop to groundnut that could also contribute to food security in the Gambia. The sesame sector’s per-formance has declined in the last few years for a variety of reasons, ranging from poor internal coordination to

limited access to critical inputs. The sector’s future de-velopment is limited by the ability of sector stakeholders from the public and private sector to address and correct key constraints.

This document presents the expectations of the private and public sectors for improvement of the sesame sec-tor in the Gambia. Without concerted efforts to address critical issues and identified market development oppor-tunities, the sector’s full potential will remain untapped. The five year PoA of the strategy proposes realistic and achievable activities that will contribute to rejuvenating the sesame sector.

Source: Tracy Benjamin. Sesame seed oil.

6 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

WHERE WE ARE NOW

HISTORICAL PERSPECTIVESesame production was started with the support of Catholic Relief Services ( CRS ) in the 1980s. By 1986 sesame production had reached 12,000 ha and 4,000 metric tons total output was achieved. The objectives of improved health through nutrition, empowering women and the use of sesame seed oil resulted in the emergence of integrated complementary agricultural production ac-tivities and the creation the Oil Seed Promotion Project, which later evolved into the current Sesame Growers Associations ( SGAs ).

Through the SGA project sesame was promoted as a cash crop for women farmers, providing an alternative food and income source. To ensure good yields and an appropriate variety of produce, high quality sesame seeds were imported and 30 Farmer Field Schools ( FFSs ) for sesame were established to produce certified seeds. To strengthen the institutional capacity of the SGAs the National Women Farmers Association ( NAWFA ) was formed in 1999 and its Secretariat put in place the fol-lowing year.

The availability of markets for sesame seeds led to a shift in favour of producing seeds for sale to local markets and positive response from the demand side encour-aged their production and export trade. CRS and NAWFA were able to initiate important linkages in the areas of sesame production and marketing. Consequently, with CRS support NAWFA was able to export approximately 200 tons of white sesame to the Netherlands. This was a good marketing experience for SGAs and NAWFA. Early successes permitted the raising of rural women’s export earnings through sesame cultivation.

The development of the sesame industry in the Gambia was therefore very closely linked to the activities of CRS. Sesame was initially grown mainly for its oil, whose pri-mary use was ( and largely remains among some peo-ple ) for cooking. It is an important element in the diets of Gambians. To promote the processing of sesame into oil CRS strategically installed 16 oil expellers ( process-ing equipment ) around the country for use by project participants.

The end of CRS support in 2007 gradually saw most of the 30 FFSs close shop, with a drastic reduction in produc-tion of certified sesame seeds. By 2012, only three seed multiplication centres in the country ( Giroba Kunda in

the Upper River Region ( URR ), Sapu in the Central River Region ( CRR ) and Chamen in the North Bank Region ( NBR ) ), each with 25 ha with some limited focus on ses-ame, were still operational and working in collaboration with the National Agriculture Research Institute ( NARI ).

The end of CRS support also led to a gradual decline of governance structures in the sesame industry. SGAs slowly started failing to hold regular meetings ; NAWFA itself became erratic in holding Annual General Meetings and in its support to SGAs. The industry took a difficult downward turn. Sesame production declined sharply with exports reduced almost to zero, and major export con-tacts were lost.

CURRENT CONTEXTSesame farming in the Gambia is dominated by small landholders, most of whom farm on less than one hectare,3 which leads to a fragmented production struc-ture and heavy reliance on collectors to amalgamate production. An increase in sesame production has been identified as a key requirement to rejuvenate the sector and its export capacity.

PRODUCTION

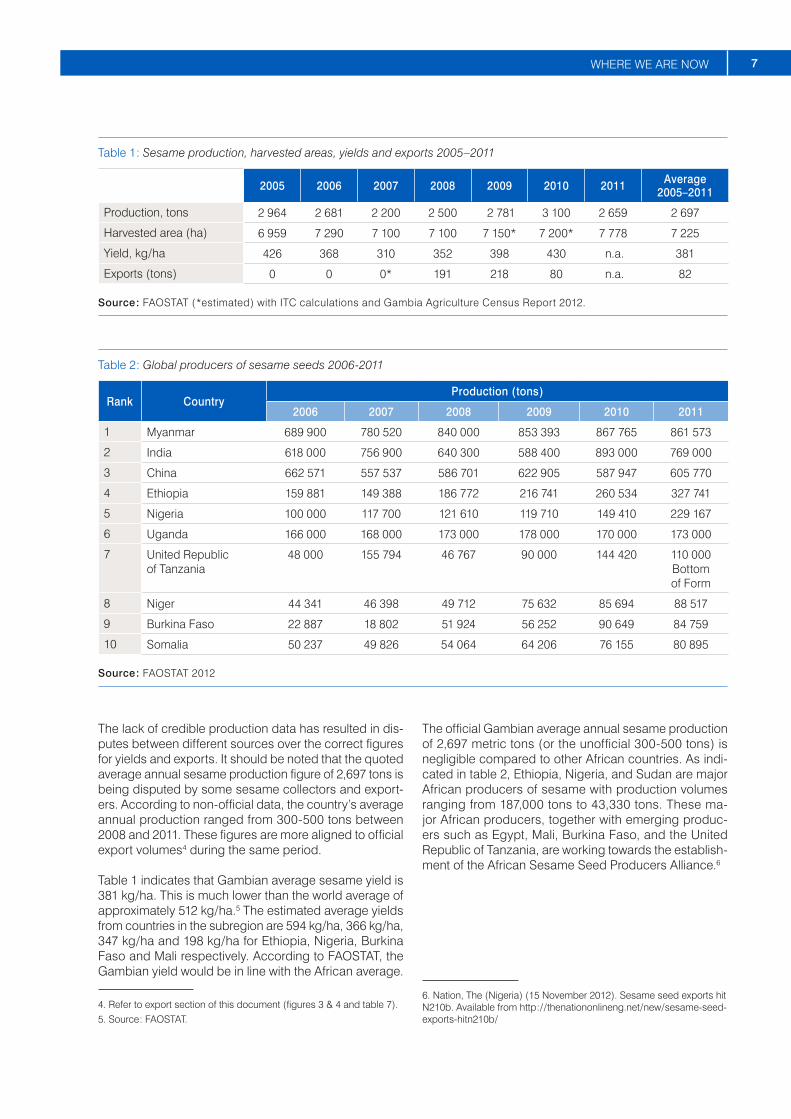

At the moment production is much reduced from its 1986 peak of 4,000 tons cultivated over an area of 12,000 ha. In the past, sesame production was mostly concentrated in CRR North and South, followed by NBR. According to FAO statistics, sesame production, harvested areas and yields have remained relatively constant since 2005 with an average production volume of 2,697 tons per year cultivated over an average area of 7,225 ha.

The most recent Agriculture Census ( 2012 ) showed a revised trend, with NBR taking the lead in both area cul-tivated and production. The official production levels for 2011 are 2,659 tons cultivated over an area of 7,778 ha ( see table 1 ).

3. According to the Agricultural Census of 2011 / 2012, 65.5 % of farms are smaller than one hectare.

7WHERE WE ARE NOW

Table 1 : Sesame production, harvested areas, yields and exports 2005–2011

2005 2006 2007 2008 2009 2010 2011 Average 2005–2011

Production, tons 2 964 2 681 2 200 2 500 2 781 3 100 2 659 2 697

Harvested area ( ha ) 6 959 7 290 7 100 7 100 7 150* 7 200* 7 778 7 225

Yield, kg / ha 426 368 310 352 398 430 n.a. 381

Exports ( tons ) 0 0 0* 191 218 80 n.a. 82

Source : FAOSTAT ( *estimated ) with ITC calculations and Gambia Agriculture Census Report 2012.

Table 2 : Global producers of sesame seeds 2006-2011

Rank CountryProduction ( tons )

2006 2007 2008 2009 2010 2011

1 Myanmar 689 900 780 520 840 000 853 393 867 765 861 573

2 India 618 000 756 900 640 300 588 400 893 000 769 000

3 China 662 571 557 537 586 701 622 905 587 947 605 770

4 Ethiopia 159 881 149 388 186 772 216 741 260 534 327 741

5 Nigeria 100 000 117 700 121 610 119 710 149 410 229 167

6 Uganda 166 000 168 000 173 000 178 000 170 000 173 000

7 United Republic of Tanzania

48 000 155 794 46 767 90 000 144 420 110 000 Bottom of Form

8 Niger 44 341 46 398 49 712 75 632 85 694 88 517

9 Burkina Faso 22 887 18 802 51 924 56 252 90 649 84 759

10 Somalia 50 237 49 826 54 064 64 206 76 155 80 895

Source : FAOSTAT 2012

The lack of credible production data has resulted in dis-putes between different sources over the correct figures for yields and exports. It should be noted that the quoted average annual sesame production figure of 2,697 tons is being disputed by some sesame collectors and export-ers. According to non-official data, the country’s average annual production ranged from 300-500 tons between 2008 and 2011. These figures are more aligned to official export volumes4 during the same period.

Table 1 indicates that Gambian average sesame yield is 381 kg / ha. This is much lower than the world average of approximately 512 kg / ha.5 The estimated average yields from countries in the subregion are 594 kg / ha, 366 kg / ha, 347 kg / ha and 198 kg / ha for Ethiopia, Nigeria, Burkina Faso and Mali respectively. According to FAOSTAT, the Gambian yield would be in line with the African average.

4. Refer to export section of this document ( figures 3 & 4 and table 7 ).5. Source : FAOSTAT.

The official Gambian average annual sesame production of 2,697 metric tons ( or the unofficial 300-500 tons ) is negligible compared to other African countries. As indi-cated in table 2, Ethiopia, Nigeria, and Sudan are major African producers of sesame with production volumes ranging from 187,000 tons to 43,330 tons. These ma-jor African producers, together with emerging produc-ers such as Egypt, Mali, Burkina Faso, and the United Republic of Tanzania, are working towards the establish-ment of the African Sesame Seed Producers Alliance.6

6. Nation, The ( Nigeria ) ( 15 November 2012 ). Sesame seed exports hit N210b. Available from http : / / thenationonlineng.net / new / sesame-seed-exports-hitn210b /

8 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

One of the key reasons explaining the low production vol-ume in Gambia is that sesame is not regarded by farmers as a main cash crop. Only when there is a failure in other crops ( such as groundnut and cashew ) do farmers turn to sesame as an alternative cash crop.

Sesame is planted well after most crops are grown, at a time when late season vegetables such as tomatoes, bitter tomatoes and melons are to be cultivated, there-by creating competition for the limited land available for production. Sesame also competes for labour with other crops. At the start of the sesame planting season the grasses are tall and plentiful labour is required to prepare the land. The crop that sesame competes with most for labour and similar inputs is groundnuts, the most impor-tant cash crop of the Gambia. Competition is even keener

because farmers have not yet experienced much return on investment in the sesame sector. A key reason for this is the limited use of good agricultural practices ( GAP ) in harvest and post-harvest, leading to important losses.

Furthermore, there is the belief that sesame cultivation could have negative effects on soil fertility because the crop is a deep-root feeder. In fact it is the opposite, as the deep-root feeding nature of sesame recycles important plant nutrients ( which may otherwise be lost from the subsoil ) to plant life. The dropping of foliage of sesame plants at maturity can thus be added back to the soil to improve the fertility of the topsoil. This situation confirms a need to disseminate information and training to farmers.

SESAME VARIETIES

The absence of sesame seeds of pure variety has been cited 7 as a key limitation to increasing sesame production in general. In the Gambia there is a high occurrence of admixture of different seed varieties. Over the past few years, and due to the decline of seed multiplication cen-tres, many traditional varieties from the subregion have entered the Gambian farming system through informal distribution channels. Furthermore, there are limited num-bers of sesame seed providers. This informal trade of seeds encourages mixing of seeds, thereby rendering farmers unable to identify the varieties planted. This situ-ation leads to post-harvest losses because the different varieties mature at different rates.

At the moment most producers are reliant on NAWFA for sourcing seeds, whereas the responsibility for supervis-ing seed multiplication should rest with NARI, with much less involvement of the private sector. The current situa-tion does not enable the development of a professional seed multiplication value chain with the capacity to re-spond effectively to demand.

7. Owens, Solomon J.E and Jack, Isatou ( 2003 ). Sesame Best Practices Study. Catholic Relief Services.

Table 3 : Varieties of sesame seeds studied by NARI ( 2004 )

Variety Number of branches & seed colour Days to maturity Average yield

( kg per hectare )

Primoca 6 ( brown mixed ) 108 300 – 400

Cross No. 3 5 ( brown mixed ) 103 n.a. ( trial variety )

38-1-7 4 ( brown mixed ) 92 n.a. ( trial variety )

Jaalgon 128 3 ( brown mixed ) 93 300 – 400

32-15 4 ( white seeded ) 97 400 – 500

S-42 4 ( white seeded ) 99 500 – 600

Source : NARI Research Trial Reports 2004.

Source: Stephan Hochhaus. Roasting Sesame

9WHERE WE ARE NOW

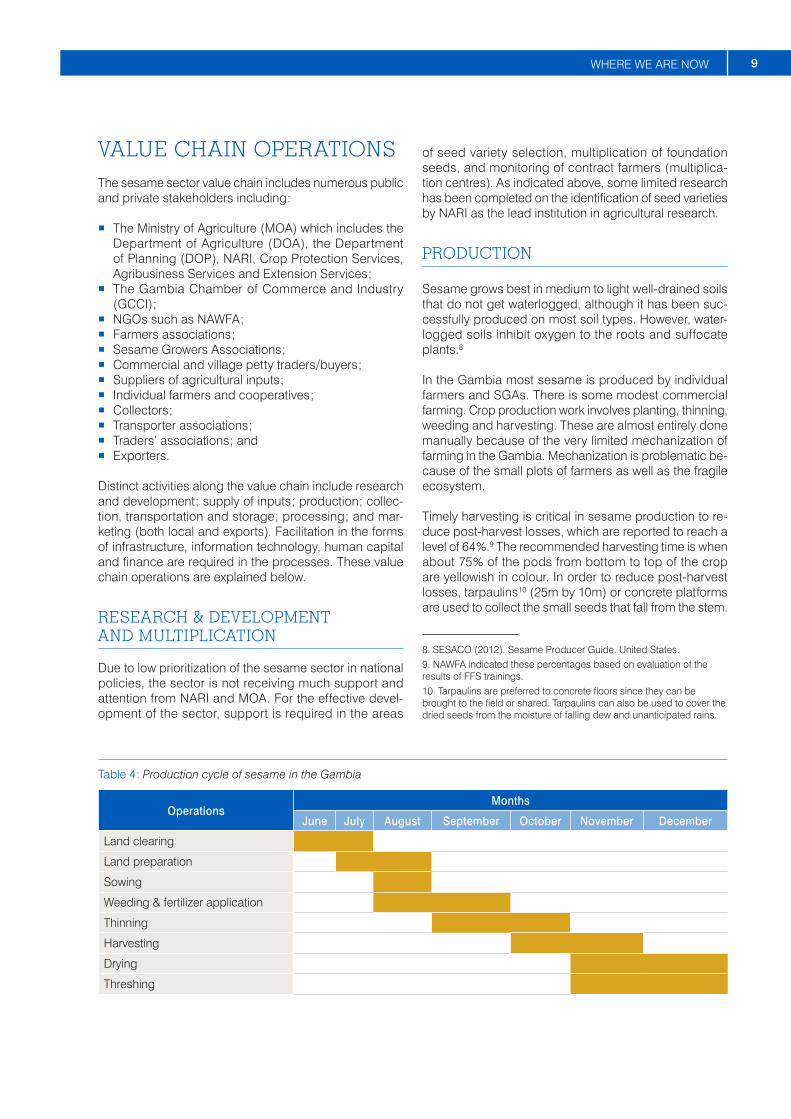

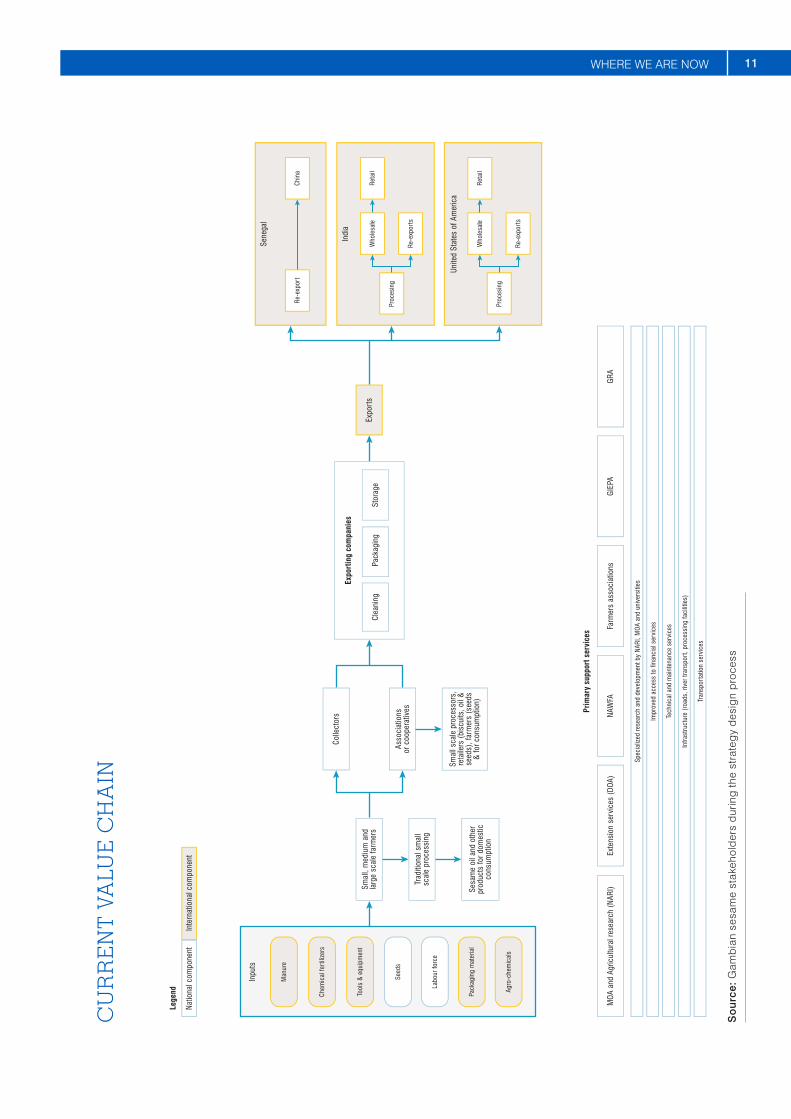

VALUE CHAIN OPERATIONSThe sesame sector value chain includes numerous public and private stakeholders including :

� The Ministry of Agriculture ( MOA ) which includes the Department of Agriculture ( DOA ), the Department of Planning ( DOP ), NARI, Crop Protection Services, Agribusiness Services and Extension Services ;

� The Gambia Chamber of Commerce and Industry ( GCCI ) ;

� NGOs such as NAWFA ; � Farmers associations ; � Sesame Growers Associations ; � Commercial and village petty traders / buyers ; � Suppliers of agricultural inputs ; � Individual farmers and cooperatives ; � Collectors ; � Transporter associations ; � Traders’ associations ; and � Exporters.

Distinct activities along the value chain include research and development ; supply of inputs ; production ; collec-tion, transportation and storage ; processing ; and mar-keting ( both local and exports ). Facilitation in the forms of infrastructure, information technology, human capital and finance are required in the processes. These value chain operations are explained below.

RESEARCH & DEVELOPMENT AND MULTIPLICATION

Due to low prioritization of the sesame sector in national policies, the sector is not receiving much support and attention from NARI and MOA. For the effective devel-opment of the sector, support is required in the areas

of seed variety selection, multiplication of foundation seeds, and monitoring of contract farmers ( multiplica-tion centres ). As indicated above, some limited research has been completed on the identification of seed varieties by NARI as the lead institution in agricultural research.

PRODUCTION

Sesame grows best in medium to light well-drained soils that do not get waterlogged, although it has been suc-cessfully produced on most soil types. However, water-logged soils inhibit oxygen to the roots and suffocate plants.8

In the Gambia most sesame is produced by individual farmers and SGAs. There is some modest commercial farming. Crop production work involves planting, thinning, weeding and harvesting. These are almost entirely done manually because of the very limited mechanization of farming in the Gambia. Mechanization is problematic be-cause of the small plots of farmers as well as the fragile ecosystem.

Timely harvesting is critical in sesame production to re-duce post-harvest losses, which are reported to reach a level of 64 %.9 The recommended harvesting time is when about 75 % of the pods from bottom to top of the crop are yellowish in colour. In order to reduce post-harvest losses, tarpaulins 10 ( 25m by 10m ) or concrete platforms are used to collect the small seeds that fall from the stem.

8. SESACO ( 2012 ). Sesame Producer Guide. United States.9. NAWFA indicated these percentages based on evaluation of the results of FFS trainings.10. Tarpaulins are preferred to concrete floors since they can be brought to the field or shared. Tarpaulins can also be used to cover the dried seeds from the moisture of falling dew and unanticipated rains.

Table 4 : Production cycle of sesame in the Gambia

OperationsMonths

June July August September October November December

Land clearing

Land preparation

Sowing

Weeding & fertilizer application

Thinning

Harvesting

Drying

Threshing

10 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

COLLECTION, TRANSPORTATION AND STORAGE

Traders normally buy sesame from three sources : directly from farmers, through collecting agents or from NAWFA. The product is then transported to towns and eventually to Banjul or border posts for export.

SGAs, individual farmers and traders singled out trans-port as the most expensive part of the marketing process. This is aggravated by insufficient availability of transport means during the marketing period. Transport fees are considered high, averaging US $ 1.67 to US $ 2.67 11 per 50 kg bag in 2012. Transportation is by trucks and animal-drawn carts.

Adequate storage facilities and conditions from farm level to urban warehouses are essential to ensure the sesame seeds are not contaminated or infested by pests.12 At the moment there is insufficient storage at both farm and community levels.

PACKAGING, CLEANING AND EXPORTING

Sesame seeds are usually packed in multi-walled paper bags of 22 kg or 25 kg, jute and nylon bags of 25 kg or 50 kg, or jute bags of 50 kg. At the moment the packing

11. Using an exchange rate of GMD30 to US $ 1.12. ITC ( 2013 ). Quality Assurance Framework ( QAF ) for Cashew Nuts and Sesame Products in the Gambia.

of sesame seeds is not considered a key issue since the small volumes are packed in reused nylon or jute bags. However, to ensure adequate quality is maintained it has been indicated that nylon bags are best.13 The limited volume of processed sesame oil is packed in recycled capped plastic bottles.

Once collected, sesame is transported to the buyer’s main depot for cleaning ( to ensure quality control ) and re-bagging. Exporters require that the sesame they buy be 98 %-99 % free from foreign matter. In addition to traders and exporters cleaning the sesame, NAWFA also does some limited cleaning. Once cleaned the sesame is packed and transported to Senegal or the port of Banjul, where it is exported.

PROCESSING

There are some individuals and groups who process small volumes of sesame in the Gambia. The products are sold in the local market or exported in small quanti-ties to other West African countries.14 Small scale sesame processing permits the production of sesame oil, biscuits, sesame cake and paste at village level.

13. Bilateral discussions with NAWFA.14. In order to promote the processing of sesame into oil, a CRS project in the 1980s strategically installed 16 oil expellers ( processing equipment ) around the country.

Box 2 : Overview of key input requirements for production of sesame

Inputs such as chemical fertilizers and farm implements are expensive and this limits their use in sesame production. They are mostly obtained from foreign sources and distributed through periodic markets ( Lumoos ) and local private outlets.

The main chemical fertilizers used in sesame production are compound fertilizer ( nitrogen, phosphorus & potassium ) and urea ( 46 % nitrogen ). The best alternatives to chemical fertilizers are organic composts and kraal manure. These organic manures help to improve soil fertility, soil structure and soil water-holding capacity, as well as helping protect topsoil from erosion.

The farm implements needed for sesame cultivation range from heavy machinery in the form of tractors to light equipment / implements such as power tillers, rotovators, animal-drawn ploughs, seeders and sine hoes / tine weeders.

Nat

iona

l com

pone

nt

Inpu

ts

Smal

l, m

ediu

m a

ndla

rge

scal

e fa

rmer

sEx

port

s

Trad

ition

al s

mal

lsc

ale

proc

essi

ng

Asso

ciat

ions

or c

oope

rativ

es

Colle

ctor

s

Sesa

me

oil a

nd o

ther

prod

ucts

for d

omes

ticco

nsum

ptio

n

Smal

l sca

le p

roce

ssor

s,re

taile

rs (

bisc

uits

, oil

&se

eds)

, far

mer

s (s

eeds

& fo

r con

sum

ptio

n)

Exte

nsio

n se

rvic

es (

DO

A)M

OA

and

Agric

ultu

ral r

esea

rch

(NAR

I)N

AWFA

Farm

ers

asso

ciat

ions

GIE

PAG

RA

Prim

ary

supp

ort s

ervi

ces

Stor

age

Pack

agin

gCl

eani

ng

Expo

rtin

g co

mpa

nies

Spec

ializ

ed re

sear

ch a

nd d

evel

opm

ent b

y N

ARI,

MO

A an

d un

iver

sitie

s

Impr

oved

acc

ess

to fi

nanc

ial s

ervi

ces

Tech

nica

l and

mai

nten

ance

ser

vice

s

Infra

stru

ctur

e (r

oads

, riv

er tr

ansp

ort,

proc

essi

ng fa

cilit

ies)

Tran

spor

tatio

n se

rvic

es

Sene

gal

Indi

a

Unite

d St

ates

of A

mer

ica

Tool

s &

equ

ipm

ent

Chem

ical

fert

ilize

rs

Man

ure

Seed

s

Labo

ur fo

rce

Pack

agin

g m

ater

ial

Agro

-che

mic

als

Lege

nd

Inte

rnat

iona

l com

pone

nt

Who

lesa

leRe

tail

Proc

esin

g

Re-e

xpor

ts

Who

lesa

leRe

tail

Proc

esin

g

Re-e

xpor

ts

Re-e

xpor

tCh

ina

So

urc

e: G

amb

ian

sesa

me

stak

ehol

der

s d

urin

g th

e st

rate

gy

des

ign

pro

cess

11WHERE WE ARE NOW

CU

RR

EN

T V

ALU

E C

HA

IN

12 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

SECTOR IMPORTSThe sesame sector in the Gambia imports farm imple-ments, fertilizers, packaging and, at times, high quality seeds. Many agricultural inputs are applicable across a variety of crops and this is expected to apply even in the Gambia. Sesame seeds for sowing are mainly imported from Senegal and Burkina Faso.

In 2012 Gambia imported vegetable and cooking oil / fats ( HS 15 ) to the value of US $ 47,865,000. The majority of the imports were palm oil and margarine. The importa-tion of vegetable and cooking oils is of particular interest because the original impulse of CRS for the development of sesame in the Gambia was to contribute to food se-curity by popularizing sesame oil to supplement house-hold diets. Protective clothing is also imported. Increasing production of sesame seeds, and eventually the further processing into oil and other products, could contrib-ute to reducing expenditure on imports of vegetable and cooking oil.

GLOBAL PERSPECTIVEThe global market for sesame seeds and sesame oil products is about US $ 2.1 billion ( 2012 ), as shown in ta-bles 5 and 6 below.

MAJOR IMPORTERS

Global trade flows ( imports ) of both sesame seeds and oil have experienced a significant period of growth since 2008, with estimated annual growth rates of 5 % and 7 % respectively.

China is the leading importer of sesame seeds, with im-ports that are more than double that of the second largest importer – Japan. The top three importers in 2012 – China, Japan and Turkey – comprise more than 48 % of all global imports. Asia leads imports with three Asian countries in the top five ranks of importers.

Most import markets for sesame seeds are growing at or below the average global rate of growth, with China, Viet Nam and the United Arab Emirates as the exceptions. Chinese imports of sesame have consistently outstripped the global growth rate, indicating an expanding import market and increasing global share in imports. In Africa and the Middle East, Israel, Egypt and Lebanon are major buyers of sesame seeds.

Sesame oil import markets are growing at a faster pace than the sesame seed market. The growth is impressive at 7 %. The United States is the biggest importer but ex-hibits below average growth rates, indicating that other emerging importers are becoming increasingly important players in the sesame oil market.

The United States and EU markets clearly exhibit a prefer-ence for sesame oil products. For instance, the EU and the United States comprise almost 56 % of the global share of sesame oil imports. This is unlike the sesame seed market, where Asia dominates the market in terms of demand ( although the EU also has a fair share of im-ports ). The only Asian importer in the top five rankings for sesame oil – Hong Kong – is losing market share. Japanese imports of sesame seeds are regressing at a rate of 5 % while at the same time outpacing the global import rate for sesame oil. Table 5 shows the major import markets for sesame seeds and oils.

Source: NAWFA.

13WHERE WE ARE NOW

Table 5 : Major importers of sesame seeds and oil

Sesame seeds ( HS 120740 ) Sesame oil ( HS 151550 )

Importers Value import-ed in 2012 ( US $ thou-sands )

Annual growth in value 2008-2012 ( % )

Share in world imports ( % )

Importers Value imported in 2012 ( US $ thou-sands )

Annual growth in value 2008-2012 ( % )

Share in world imports ( % )

World 1 906 824 5 100 World 186 399 7 100

1 China 521 147 19 27.3 1 United States 63 611 6 34.1

2 Japan 240 569 –5 12.6 2 United Kingdom 10 011 3 5.4

3 Turkey 159 933 6 8.4 3 Canada 9 092 5 4.9

4 Republic of Korea

125 753 3 6.6 4 Hong Kong, China

8 860 2 4.8

5 Viet Nam 85 600 107 4.5 5 Germany 8 302 13 4.5

6 United States 71 681 –4 3.8 6 Japan 7 926 10 4.3

7 Israel 71 552 3 3.8 7 France 7 529 7 4

8 Germany 51 785 0 2.7 8 Australia 7 383 10 4

9 Greece 45 602 –7 2.4 9 Singapore 5 816 10 3.1

10 Egypt 42 843 0 2.2 10 Brazil 5 438 13 2.9

11 Chinese Taipei 40 026 5 2.1 11 China 5 362 5 2.9

12 Lebanon 34 903 3 1.8 12 Netherlands 4 686 –1 2.5

13 United Arab Emirates

28 004 9 1.5 13 Switzerland 2 679 16 1.4

14 Netherlands 26 635 –8 1.4 14 Malaysia 2 667 –4 1.4

15 Mexico 22 002 –11 1.2 15 Mexico 2 566 4 1.4

Sources : ITC calculations based on UN Comtrade statistics. The world aggregation represents the sum of reporting and non-reporting countries. The data in this colour represents mirror figures based on partner data.

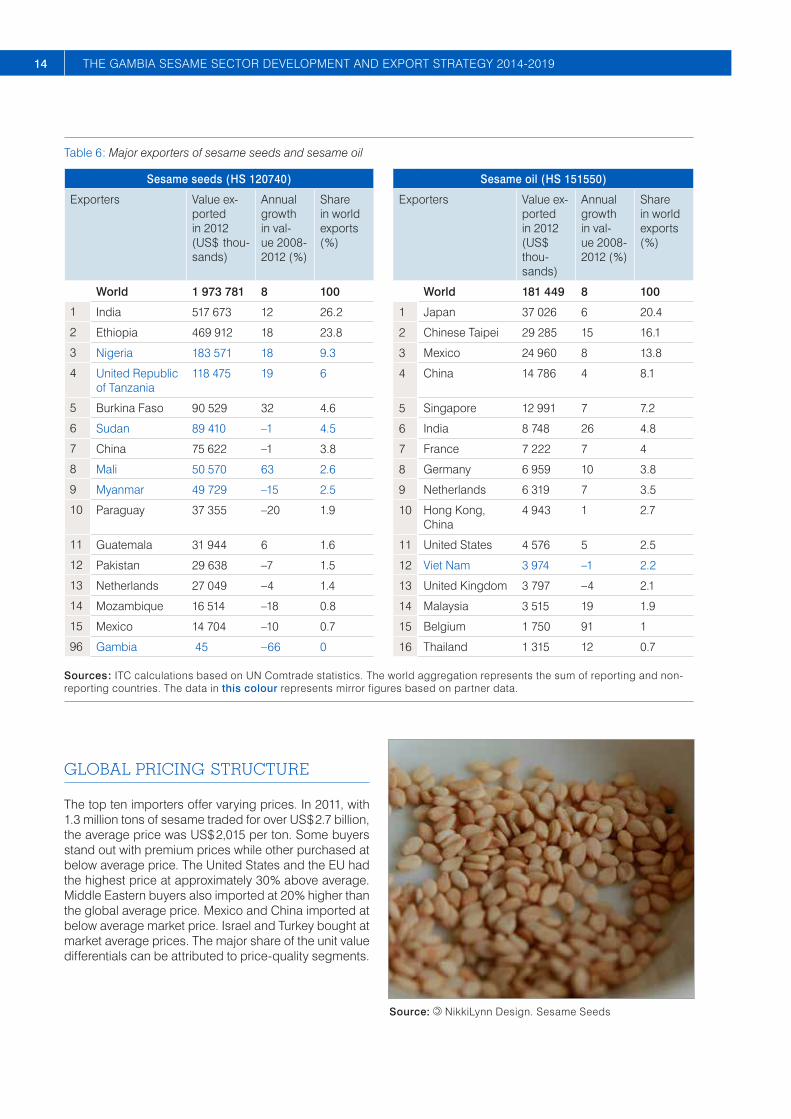

MAJOR EXPORTERS

The export market for sesame seeds is currently domi-nated by India, which has experienced significant growth in the last five years. Indian sesame exports have grown from US $ 434 million in 2008 to US $ 517 million in 2012. India has gained back its position of leading exporter of sesame seeds after it was successively overtaken by Ethiopia in 2009 and Nigeria in 2010 as the leading exporters. Five countries ( India, Ethiopia, Nigeria, the United Republic of Tanzania and Burkina Faso ) are grow-ing sesame seed exports at a rate above the global aver-age, thereby gaining significant market shares.

African producers ( Nigeria, Ethiopia, Sudan, the United Republic of Tanzania and Burkina Faso ) play an impor-tant role in the export of sesame seeds, with these five players accounting for more than 48 % of global exports. The sesame oil export market is less polarized than the market for sesame seeds. Japan is the leading exporter and there is close competition between the other lead-ing exporters such as Chinese Taipei, Mexico, China and Singapore.

Many exporters have surpassed the average global growth rate for sesame oil. These fast emerging export-ers include Chinese Taipei, India, Germany, Malaysia and Belgium.

14 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Table 6 : Major exporters of sesame seeds and sesame oil

Sesame seeds ( HS 120740 ) Sesame oil ( HS 151550 )

Exporters Value ex-ported in 2012 ( US $ thou-sands )

Annual growth in val-ue 2008-2012 ( % )

Share in world exports ( % )

Exporters Value ex-ported in 2012 ( US $ thou-sands )

Annual growth in val-ue 2008-2012 ( % )

Share in world exports ( % )

World 1 973 781 8 100 World 181 449 8 100

1 India 517 673 12 26.2 1 Japan 37 026 6 20.4

2 Ethiopia 469 912 18 23.8 2 Chinese Taipei 29 285 15 16.1

3 Nigeria 183 571 18 9.3 3 Mexico 24 960 8 13.8

4 United Republic of Tanzania

118 475 19 6 4 China 14 786 4 8.1

5 Burkina Faso 90 529 32 4.6 5 Singapore 12 991 7 7.2

6 Sudan 89 410 –1 4.5 6 India 8 748 26 4.8

7 China 75 622 –1 3.8 7 France 7 222 7 4

8 Mali 50 570 63 2.6 8 Germany 6 959 10 3.8

9 Myanmar 49 729 –15 2.5 9 Netherlands 6 319 7 3.5

10 Paraguay 37 355 –20 1.9 10 Hong Kong, China

4 943 1 2.7

11 Guatemala 31 944 6 1.6 11 United States 4 576 5 2.5

12 Pakistan 29 638 –7 1.5 12 Viet Nam 3 974 –1 2.2

13 Netherlands 27 049 –4 1.4 13 United Kingdom 3 797 –4 2.1

14 Mozambique 16 514 –18 0.8 14 Malaysia 3 515 19 1.9

15 Mexico 14 704 –10 0.7 15 Belgium 1 750 91 1

96 Gambia 45 –66 0 16 Thailand 1 315 12 0.7

Sources : ITC calculations based on UN Comtrade statistics. The world aggregation represents the sum of reporting and non-reporting countries. The data in this colour represents mirror figures based on partner data.

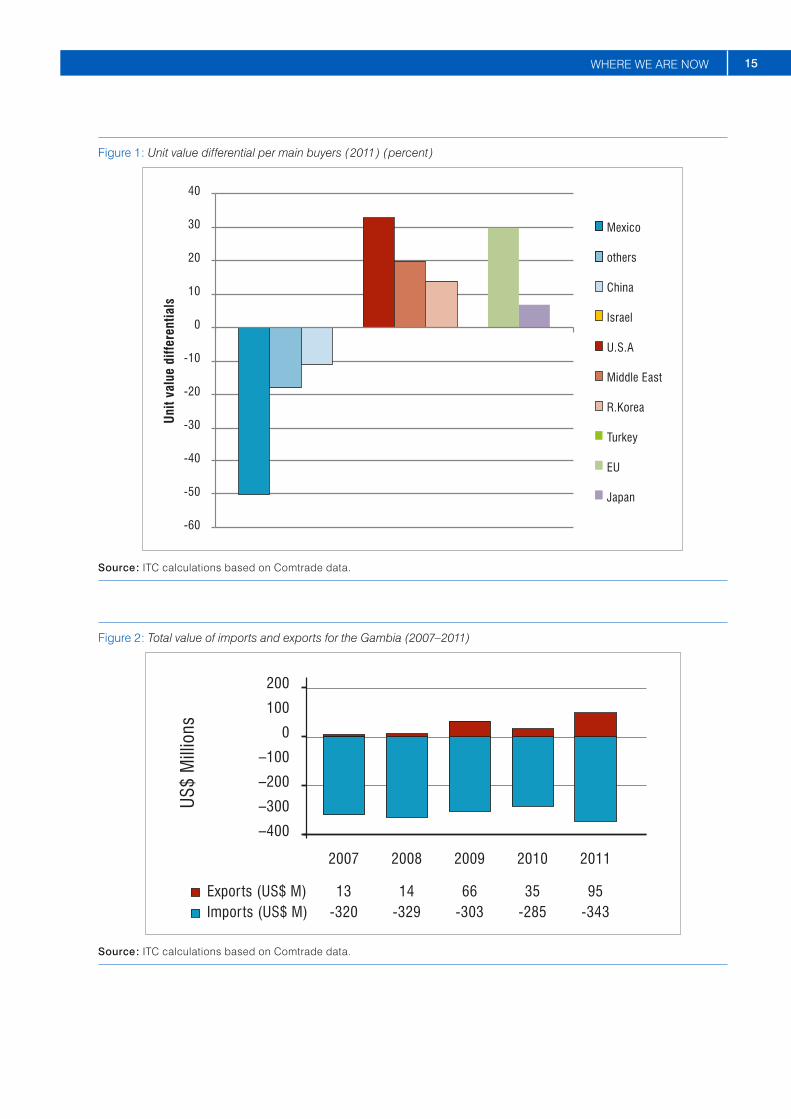

GLOBAL PRICING STRUCTURE

The top ten importers offer varying prices. In 2011, with 1.3 million tons of sesame traded for over US $ 2.7 billion, the average price was US $ 2,015 per ton. Some buyers stand out with premium prices while other purchased at below average price. The United States and the EU had the highest price at approximately 30 % above average. Middle Eastern buyers also imported at 20 % higher than the global average price. Mexico and China imported at below average market price. Israel and Turkey bought at market average prices. The major share of the unit value differentials can be attributed to price-quality segments.

Source: NikkiLynn Design. Sesame Seeds

15WHERE WE ARE NOW

Figure 1 : Unit value differential per main buyers ( 2011 ) ( percent )

-60

-50

-40

-30

-20

-10

0

10

20

30

40

Mexico

others

China

Israel

U.S.A

Uni

t val

ue d

iffer

entia

ls

Middle East

R.Korea

Turkey

EU

Japan

Source : ITC calculations based on Comtrade data.

Figure 2 : Total value of imports and exports for the Gambia ( 2007–2011 )

–400

–300

–200

–100

0

100

200

Exports (US$ M) 13 14 66 35 95-320 -329 -303 -285 -343

2007 2008 2009 2010 2011

Imports (US$ M)

US$

Mill

ions

Source : ITC calculations based on Comtrade data.

16 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Figure 3 : The Gambia’s sesame exports ( mirror data ) 2001–2011Va

lue

in U

S$ th

ousa

nds

200620052004200320022001

0

200

400

600

800

1.000

1.200

2007 2008 2009 2010 2011

Source : ITC calculations based on Comtrade data.

Table 7 : Gambian sesame exports ( direct data ), 2008-2011*

Imports Exported value in

2008

Exported quantities

Unit Exported value in

2009

Exported quantities

Unit Exported value in

2010

Exported quantities

Unit Exported value in

2011

Exported quantities

Unit

World 75 191 393 16 218 73 3 80 38 0 0 0

Senegal 65 14 4 643 2 12 167 3 80 38 0 0 0

India 0 2 32 63 0 0 0 0

Singapore 0 2 79 25 0 0 0 0

United States

10 177 56 9 95 95 0 0 0 0

Sources : ITC calculations based on UN Comtrade statistics. ( Note : no data were reported for 2007 or 2011. ) * No direct exports were recorded for 2007 and 2011. 2012 Comtrade data ( mirror ) already shows exports of sesame to Senegal ( US $ 23,000 ) and Israel ( US $ 22,000 ) even if all the full year data is not entirely processed.

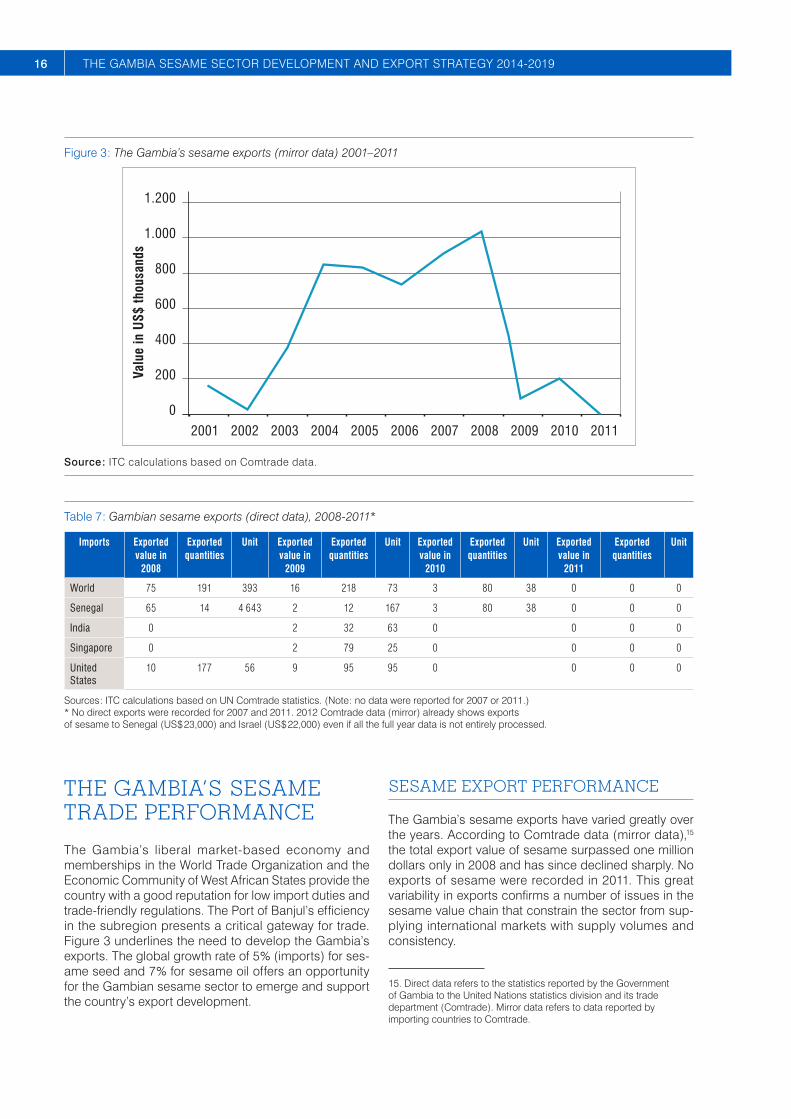

THE GAMBIA’S SESAME TRADE PERFORMANCE

The Gambia’s liberal market-based economy and memberships in the World Trade Organization and the Economic Community of West African States provide the country with a good reputation for low import duties and trade-friendly regulations. The Port of Banjul’s efficiency in the subregion presents a critical gateway for trade. Figure 3 underlines the need to develop the Gambia’s exports. The global growth rate of 5 % ( imports ) for ses-ame seed and 7 % for sesame oil offers an opportunity for the Gambian sesame sector to emerge and support the country’s export development.

SESAME EXPORT PERFORMANCE

The Gambia’s sesame exports have varied greatly over the years. According to Comtrade data ( mirror data ),15 the total export value of sesame surpassed one million dollars only in 2008 and has since declined sharply. No exports of sesame were recorded in 2011. This great variability in exports confirms a number of issues in the sesame value chain that constrain the sector from sup-plying international markets with supply volumes and consistency.

15. Direct data refers to the statistics reported by the Government of Gambia to the United Nations statistics division and its trade department ( Comtrade ). Mirror data refers to data reported by importing countries to Comtrade.

17WHERE WE ARE NOW

According to direct data ( table 7 ) the bulk of the Gambia’s total sesame exports between 2008 and 2010 went to Senegal. Two key reasons have been advanced for ex-plaining the export of sesame to Senegal. The first rea-son provided is the stability and higher value of the CFA ( Central African ) franc versus the Gambian dalasi, which encourages collectors and traders to travel to Senegal to sell their sesame. A second reason that could explain the flow of sesame to Senegal is the presence of a preferen-tial trade agreement between China – the largest importer in the world – and Senegal.

However, when looking at mirror data ( table 8 ) the picture of Gambian sesame exports is very different. According to this data, the values of sesame exports are much greater than reported and the destinations of sesame exports much more varied. Chinese Taipei is a major im-porter of Gambian sesame with an imported value of over US $ 1 million dollars for the time period. China is the second largest importer with cumulated imports of above US $ 660,000. This image of Gambian sesame exports demonstrates a much greater capacity of the country to export to varied destinations and reach some of the world’s largest importers.

In either case – using direct or mirror data – the conflict in statistics demonstrates a need to improve data record-ing of exports in the Gambia. Data collection is already improving with the rolling out of the Automated System for Customs Data ( ASYCUDA ) in the Gambia.16 This should provide a better picture of sesame exports in the next few years.

16. United Nations Conference on Trade and Development ( n.d. ). ASYCUDA Database. Available from http : / / www.asycuda.org / dispcountry.asp?name=Gambia. Accessed 9 August 2013.

The performance of Gambian sesame exports demon-strates a clear growth in exports until 2009, followed by a sharp decline in production and exports. The export con-straints section of this strategy explains in further detail the various causes of this situation ; namely the low avail-ability of seeds, the difficult access to inputs, the chal-lenges of governance and the low support to the sector.

THE INSTITUTIONAL PERSPECTIVEThe Gambia is yet to build an elaborate network of trade support institutions ( TSIs ) which can reliably support trade development operations. In the case of sesame the situation is even direr as it was not a priority focus crop until two years ago.

The TSIs providing important services to the Gambian sesame sector can be categorized according to the fol-lowing support areas :

� Policy support network � Trade services network � Business services network � Civil society network.

Tables 9 to 12 identify the main TSIs whose service deliv-ery affects the sesame sector in the Gambia. An assess-ment of the TSIs along three key dimensions – importance of TSI to the sector development, current responsiveness to the sector’s needs and resource availability – was com-pleted. The ranking ( high / medium / low ) for each TSI was completed by sector stakeholders on the basis of their perception.

Table 8 : Gambian sesame exports ( mirror data ), 2007–2010

2007 2008 2009 2010

US $ Tons US $ / ton

US $ Tons US $ / ton

US $ Tons US $ / ton

US $ Tons US $ / ton

World 901 000 1 038 000 83 000 200 000

Egypt 0 0 0 0 0 0 67 000 31 2 161 0 0 0

Lebanon 0 0 0 0 0 0 16 000 14 1 143 0 0 0

China 113 000 124 911 551 000 342 1 611 0 0 0 0 0 0

Japan 0 0 0 312 000 214 1 458 0 0 0 0 0 0

Chinese Taipei 713 000 936 762 175 000 119 1 471 0 0 0 200 000 145 1 379

Turkey 75 000 86 872 0 0 0 0 0 0 0 0 0

Source : ITC calculations based on UN Comtrade statistics.

18 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

POLICY SUPPORT NETWORK

The institutions in the policy support network represent ministries and competent authorities responsible for in-fluencing or implementing policies at the national level.

Table 9 : Gambian sesame sector policy support network

InstitutionFunction for the sesame

sectorDescription of role

Importance of TSI to

the sector

Level of responsiveness to sector needs

Resources available

to support the sector

• Ministry of Trade, Industry, Region-al Integration and Employment (MO-TIE)

• Regulatory and gener-al support

• Policies

• Regulation of trade, industry and employment issues.

• Overseeing trade, industry and employment policies.

H M M

• Ministry of Agri-culture (Depart-ments of Planning and Agriculture, Agribusiness & NARI)

• Regulatory • Extension

services• Policies

• Registration of cooperative bod-ies and growers associations.

• Provide extension link between farmers and NARI; conduct on-farm trials; seed selection, mul-tiplication and certification; and collection and processing of data on sesame.

• ANRP, seed and cooperatives policies oversight.

H M L

• Ministry of Fi-nance & Eco-nomic Affairs (MOFEA)

• (Central Bank of the Gambia, Gambia Revenue Authority)

• Regulatory• Policies

• Prudential regulation of banks and non-bank financial institu-tions.

• Overseeing the Financial Institu-tions Act and financial policies, including the microfinance pol-icy.

H M H

• Ministry of Basic and Secondary Education (MOB-SE)

• Policies • Nutrition of children in school feeding programmes and assist-ing in the adoption of agriculture by children and youth, as well as supporting short-term hunger is-sues and environmental man-agement.

M M H

19WHERE WE ARE NOW

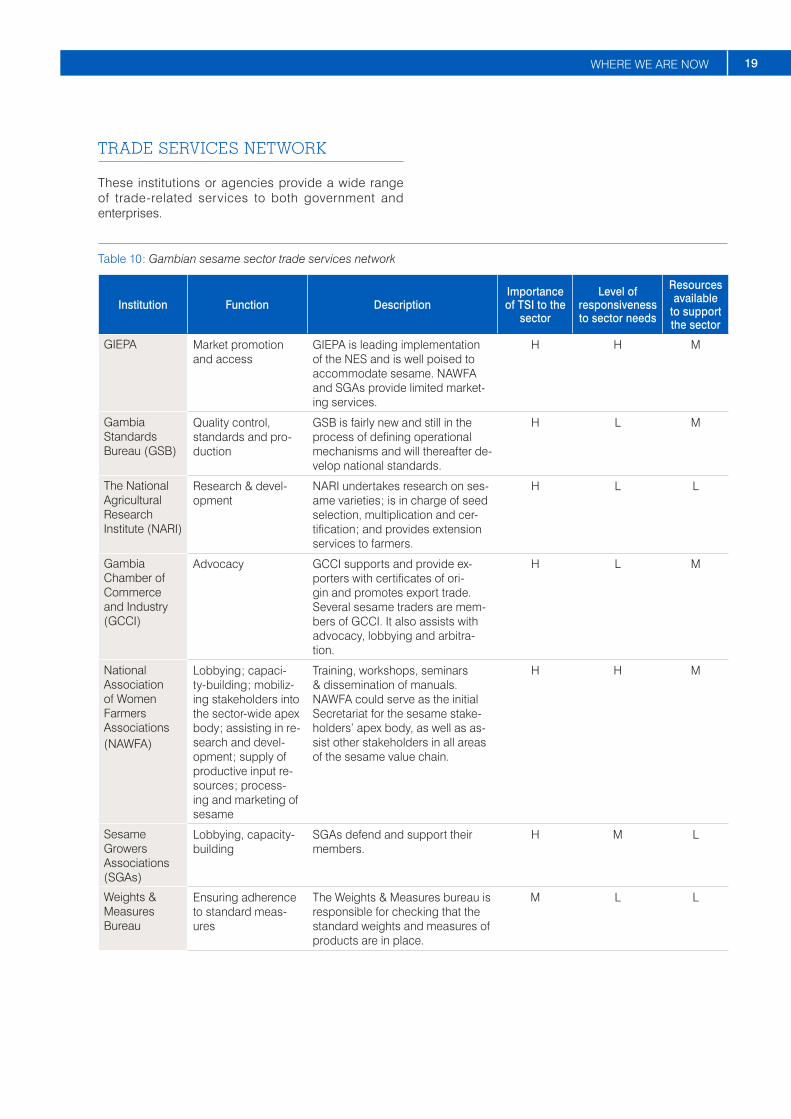

TRADE SERVICES NETWORK

These institutions or agencies provide a wide range of trade-related services to both government and enterprises.

Table 10 : Gambian sesame sector trade services network

Institution Function DescriptionImportance of TSI to the

sector

Level of responsiveness to sector needs

Resources available

to support the sector

GIEPA Market promotion and access

GIEPA is leading implementation of the NES and is well poised to accommodate sesame. NAWFA and SGAs provide limited market-ing services.

H H M

Gambia Standards Bureau ( GSB )

Quality control, standards and pro-duction

GSB is fairly new and still in the process of defining operational mechanisms and will thereafter de-velop national standards.

H L M

The National Agricultural Research Institute ( NARI )

Research & devel-opment

NARI undertakes research on ses-ame varieties ; is in charge of seed selection, multiplication and cer-tification ; and provides extension services to farmers.

H L L

Gambia Chamber of Commerce and Industry ( GCCI )

Advocacy GCCI supports and provide ex-porters with certificates of ori-gin and promotes export trade. Several sesame traders are mem-bers of GCCI. It also assists with advocacy, lobbying and arbitra-tion.

H L M

National Association of Women Farmers Associations( NAWFA )

Lobbying ; capaci-ty-building ; mobiliz-ing stakeholders into the sector-wide apex body ; assisting in re-search and devel-opment ; supply of productive input re-sources ; process-ing and marketing of sesame

Training, workshops, seminars & dissemination of manuals. NAWFA could serve as the initial Secretariat for the sesame stake-holders’ apex body, as well as as-sist other stakeholders in all areas of the sesame value chain.

H H M

Sesame Growers Associations ( SGAs )

Lobbying, capacity-building

SGAs defend and support their members.

H M L

Weights & Measures Bureau

Ensuring adherence to standard meas-ures

The Weights & Measures bureau is responsible for checking that the standard weights and measures of products are in place.

M L L

20 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

Institution Function DescriptionImportance of TSI to the

sector

Level of responsiveness to sector needs

Resources available

to support the sector

Department of Agriculture Food Technology Services

Ensuring use of proper post-har-vest technology and food safety

Food Technology Services assists farmers with appropriate post-har-vest methodologies for agricultural food products as well as ensuring food safety.

H M L

Department of Agribusiness Services

Registration of co-operatives & sup-port to cooperative bodies in the form of accounting & book-keeping training, as well as auditing of books of accounts

The Registrar of Cooperatives, who is based in the Agribusiness Department, is responsible for the implementation of the Cooperatives Act.

H L L

National Nutrition Agency

Policy guidance in relation to food and nutrition security

The National Nutrition Agency as-sists with policy issues relating to food, nutrition and health securi-ty in the Gambia so as to meet the dietary needs and food preferenc-es of Gambians.

M L M

Ministry of Agriculture Department of Planning ( DOP )

Conduct of research and depository for agricultural data and information

DOP collects production data on sesame, groundnuts and cereals ( rice and coarse grains ).

H L L

Food Safety and Quality Authority

Regulatory The Food Safety & Quality Authority works in close collabo-ration with GSB ( which develops standards for all products ). It is to serve as the regulatory body for adherence to food standards, in-cluding products of sesame.

H L L

Source: Willie_Langdji. Sesame press for processing sesame and groundnuts (peanuts) into oil and cake.

21WHERE WE ARE NOW

BUSINESS SERVICES NETWORK

These are associations, or major representatives, of com-mercial service providers used by exporters to carry out international trade transactions.

Table 11 : Gambian sesame sector business services network

Institution Function DescriptionImportance

of TSI to the sector

Level of responsiveness to sector needs

Resources available to support the

sector

Sandika Petty Traders Association

Collection and storage of sesame products

Sandika stakeholders play a vi-tal role in the aggregation and marketing of sesame from farmers to large buyers, es-pecially those at the Brikama Market. They would, howev-er, require some support in the functions they perform, espe-cially in providing storage fa-cilities.

H M L

Transporters Union Transportation of sesame products

Oversee the aggregation and transportation of products.

H M L

Microfinance institutions ( e.g. Village Savings and Credit Associations ( VISACAs ), National Association of Cooperative Credit Unions ( NACCUG ), Reliance Finance and Gambia Women’s Finance Association ( GAWFA ) ), commercial banks and others

Funding Most funding is at village lev-el from VISACAs and micro-lenders at high interest rates. The majority of farmers are ei-ther ‘unbanked’ or are unable to raise the high collateral de-manded by banks.

H L M

Source: Jacqueline.

22 THE GAMBIA SESAME SECTOR DEVELOPMENT AND EXPORT STRATEGY 2014-2019

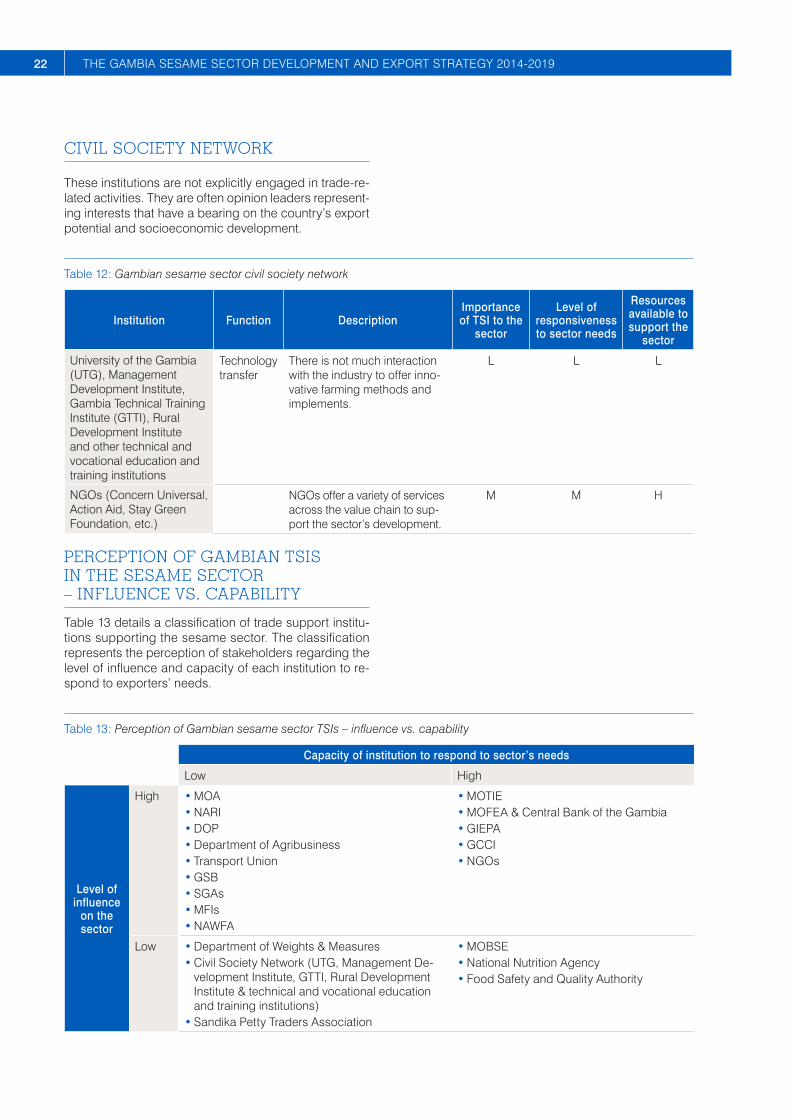

CIVIL SOCIETY NETWORK

These institutions are not explicitly engaged in trade-re-lated activities. They are often opinion leaders represent-ing interests that have a bearing on the country’s export potential and socioeconomic development.

Table 12 : Gambian sesame sector civil society network

Institution Function DescriptionImportance of TSI to the

sector

Level of responsiveness to sector needs

Resources available to support the

sector

University of the Gambia ( UTG ), Management Development Institute, Gambia Technical Training Institute ( GTTI ), Rural Development Institute and other technical and vocational education and training institutions

Technology transfer

There is not much interaction with the industry to offer inno-vative farming methods and implements.

L L L

NGOs ( Concern Universal, Action Aid, Stay Green Foundation, etc. )

NGOs offer a variety of services across the value chain to sup-port the sector’s development.

M M H

PERCEPTION OF GAMBIAN TSIS IN THE SESAME SECTOR – INFLUENCE VS. CAPABILITY

Table 13 details a classification of trade support institu-tions supporting the sesame sector. The classification represents the perception of stakeholders regarding the level of influence and capacity of each institution to re-spond to exporters’ needs.

Table 13 : Perception of Gambian sesame sector TSIs – influence vs. capability

Capacity of institution to respond to sector’s needs

Low High

Level of influence

on the sector