The Economic Outlook for the U.S. and Indiana - IN.gov Economic Outlook for the U.S. and Indiana Jim...

32

The Economic Outlook for the U.S. and Indiana Jim Diffley Senior Director Chief Regional Economist IHS Global Insight April 15, 2011

Transcript of The Economic Outlook for the U.S. and Indiana - IN.gov Economic Outlook for the U.S. and Indiana Jim...

The Economic Outlook for

the U.S. and Indiana

Jim Diffley

Senior Director

Chief Regional Economist

IHS Global Insight

April 15, 2011

Copyright © 2010 IHS Global Insight. All Rights Reserved.

2

Global Outlook Summary

• The global economic expansion is continuing at a healthy

pace, but risks are mounting.

• Japan’s economy will recover from the devastating March 11

earthquake; global supply chains face near-term disruptions.

• Turbulence in MENA presents risks to oil supplies and prices.

• Europe faces an extended period of weak growth as sovereign

debt problems are resolved.

• Emerging markets continue to offer the best growth prospects.

Copyright © 2010 IHS Global Insight. All Rights Reserved.

3

-8

-6

-4

-2

0

2

4

6

8

2001 2003 2005 2007 2009 2011 2013

3

4

5

6

7

8

9

10

11

Real GDP Growth (Left scale) Unemployment Rate (Right scale)

(Annual percent change) (Percent)

A Growing U.S. Economy Will Cut Unemployment

Copyright © 2010 IHS Global Insight. All Rights Reserved.

4

2009 2010 2011 2012

Real GDP -2.6 2.9 2.8 2.9

Consumption -1.2 1.7 2.6 2.6

Residential Investment -22.9 -3.0 -1.0 25.9

Business Fixed Investment -17.1 5.7 9.0 7.7

Federal Government 5.7 4.8 -0.1 -3.3

State & Local Govt. -0.9 -1.4 -1.8 -1.0

Exports -9.5 11.7 9.9 9.6

Imports -13.8 12.6 5.8 6.7

(Percent change)

U.S. Economic Growth by Sector

Copyright © 2010 IHS Global Insight. All Rights Reserved.

5

Is Inflation Heating Up?

• Inflationary pressures

• Rapid growth in emerging markets

• Expansionary monetary policies

• Oil supply disruptions in Libya

• Rising commodity prices

• Countervailing restraints

• Excess productive capacity

• Slack labor markets

• Global competition

Copyright © 2010 IHS Global Insight. All Rights Reserved.

6

0

1

2

3

4

5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

In U.S. Dollars In GDP-Weighted Currency Basket

(IHS Global Insight Indexes, 2002:1=1.0)

Industrial Materials Prices Have Surged

Copyright © 2010 IHS Global Insight. All Rights Reserved.

7

(Year-over-year percent change)

-2

-1

0

1

2

3

4

5

6

1998 2000 2002 2004 2006 2008 2010 2012 2014

All-Urban CPI Core CPI Employment Cost Index

U.S. Core Inflation Will Drift Upward

Copyright © 2010 IHS Global Insight. All Rights Reserved.

8

(Percent)

0

2

4

6

8

10

12

1990 1993 1996 1999 2002 2005 2008 2011 2014

Federal Funds 10-Year Treasury 30-Year Mortgage Rate

U.S. Interest Rates Will Rise in 2012

Copyright © 2010 IHS Global Insight. All Rights Reserved.

9

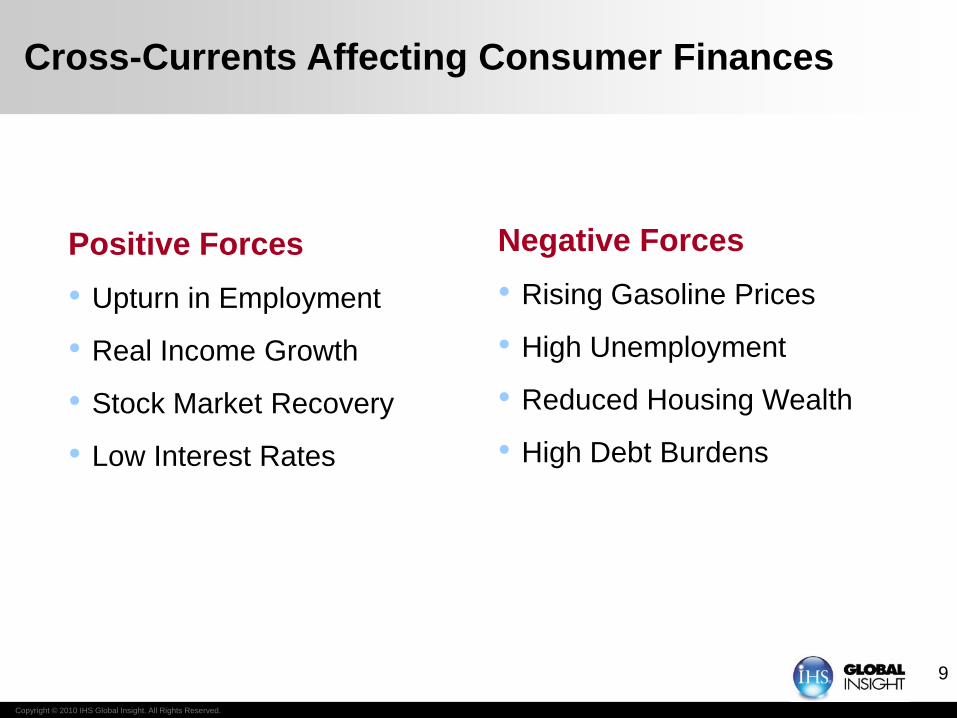

Cross-Currents Affecting Consumer Finances

Positive Forces

• Upturn in Employment

• Real Income Growth

• Stock Market Recovery

• Low Interest Rates

Negative Forces

• Rising Gasoline Prices

• High Unemployment

• Reduced Housing Wealth

• High Debt Burdens

Copyright © 2010 IHS Global Insight. All Rights Reserved.

10

-4

-2

0

2

4

6

8

2001 2003 2005 2007 2009 2011 2013

50

60

70

80

90

100

110

Real Consumption Growth Consumer Sentiment

(Annual percent change) (Reuters/Michigan Index, 1966=100)

Consumers Are Cautious: Real Spending Growth

Copyright © 2010 IHS Global Insight. All Rights Reserved.

11

-6

-3

0

3

6

9

12

2000 2002 2004 2006 2008 2010 2012 2014

Durable Goods Nondurable Goods Services

(Percent change, chained 2005 dollars)

Durable Goods Lead the Ups and Downs in Real

U.S. Consumer Spending

Copyright © 2010 IHS Global Insight. All Rights Reserved.

12

A Delayed Recovery in Housing Markets

• The recession led to a drop-off in household formation.

• Home affordability has greatly improved, boosting demand.

• High mortgage foreclosure rates are adding to excess supply,

depressing prices and holding back new construction.

• Sustained job growth will spark a housing market recovery.

• Multifamily units’ share of housing starts will rise.

Copyright © 2010 IHS Global Insight. All Rights Reserved.

1313

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

165

175

185

195

205

215

225

Housing Starts (Left scale) FHFA House Price Index (Right scale)

(Million units)

U.S. Housing Starts Have Hit Bottom:

Prices Not Quite There Yet

(Purchase-only index, 1991Q1 = 100)

Copyright © 2010 IHS Global Insight. All Rights Reserved.

14

Risks to the US Forecast

Downside Risks

– Oil supply disruptions spread, causing prices to soar.

– Financial instability returns; housing recession drags on.

– Consumers retrench after setbacks to asset values and purchasing power.

– Businesses are reluctant to hire or invest.

Upside Risks

– Credit channels function smoothly, supporting investment.

– Rapid technological progress boosts real income growth.

– Robust growth in many emerging markets fuels exports.

Copyright © 2010 IHS Global Insight. All Rights Reserved.

15

-8

-6

-4

-2

0

2

4

6

2007 2008 2009 2010 2011 2012 2013

Baseline (60%) Pessimistic (20%) Optimistic (20%)

(Percent change, annual rate)

Real GDP Growth in Alternative Scenarios

Copyright © 2010 IHS Global Insight. All Rights Reserved.

16

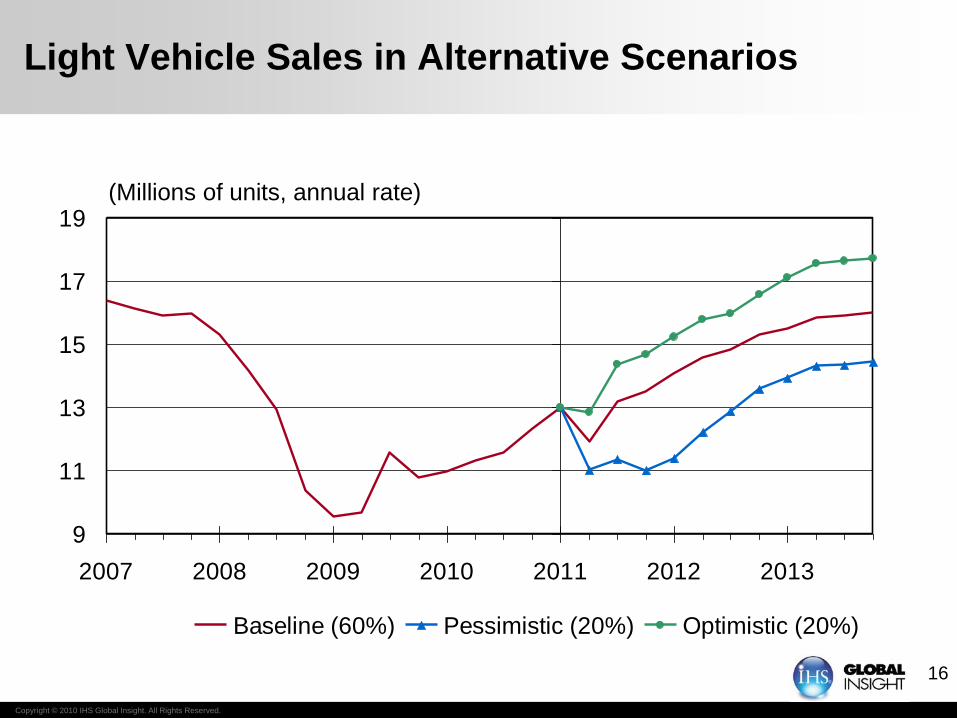

9

11

13

15

17

19

2007 2008 2009 2010 2011 2012 2013

Baseline (60%) Pessimistic (20%) Optimistic (20%)

(Millions of units, annual rate)

Light Vehicle Sales in Alternative Scenarios

Copyright © 2010 IHS Global Insight. All Rights Reserved.

17

Bottom Line

• The economic recovery is on a self-sustaining course, barring a

major oil market disruption.

• Job growth will enable consumers to spend more confidently.

• Business equipment investment, exports, consumer durables,

and housing construction will drive the expansion.

• Although food and energy prices are accelerating, high

unemployment will restrain wage gains and core inflation

• The federal government needs an “exit strategy” from deficit

spending or financial markets will eventually impose one.

Regional Outlook

Copyright © 2010 IHS Global Insight. All Rights Reserved.

Percent

-0.7 to 0.0

0.1 to 0.8

0.8 to 2.3

2.3 to 3.5

3.6 to 4.6

Labor markets reverse coursed in 2010

Year-over-year Employment Change, December 2010, %; Indiana 0.8%

Copyright © 2010 IHS Global Insight. All Rights Reserved.

West South

Central

-2

-1

0

1

2

3

4

5

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0 2.5 3.0

Year/year (%)

3-m

th a

vg

an

nu

ali

ze

d (

%)

New England Mid Atlantic South Atlantic

East North Central West North Central East South Central

West South Central Mountain Pacific

Expanding

Contracting Slipping

Improving

Momentum is building in most regions

Employment Momentum

February 2011

TX: -2.6%

Copyright © 2010 IHS Global Insight. All Rights Reserved.

Peak

-14.2 to -9.0

-8.9 to -6.2

-6.2 to -3.7

-3.6 to 0.6

0.6 to 4.3

But many states are still deep in the hole

Peak to February 2011 Employment Change, %US: -5.6%

IN : -6.8%

Copyright © 2010 IHS Global Insight. All Rights Reserved.

Percent

0.8 to 1.3

1.4 to 1.6

1.6 to 1.8

1.9 to 2.4

Recovery gathers momentum in 2011

Employment Growth 2011Q4, year-over-year %

US: 1.5%

IN: 1.8%

Copyright © 2010 IHS Global Insight. All Rights Reserved.

Percent

1.9 to 2.4

2.4 to 2.7

2.8 to 3.1

3.1 to 3.8

Medium-term performance: GSP

Real Gross State Product Growth 2011-2016, % annual rate

TX: 3.8%

US: 3.0%

IN : 2.8%

Copyright © 2010 IHS Global Insight. All Rights Reserved.

Percent

1.1 to 1.3

1.4 to 1.7

1.7 to 2.0

2.1 to 2.6

Medium-term performance: Jobs

Employment Growth 2011-2016, % annual rate

US: 1.8%

IN: 1.8%

Copyright © 2010 IHS Global Insight. All Rights Reserved.

Return To Peak

2010 to 2011

2012

2013

2014 to 2015

Past 2015

Indiana will recover lost jobs early in 2014

Year of Return to Peak Employment

Indiana Outlook

Copyright © 2010 IHS Global Insight. All Rights Reserved.

27

Bottom Line

• Deeper, earlier recession than most

• Among 2010 growth leaders early in the year

– Transportation equipment rebound

– Low paying temp and business services jobs

• Slow recovery, but a recovery is indeed in place

• Medium term performance near average among states

– Outpacing other midwest manufacturing giants

Copyright © 2010 IHS Global Insight. All Rights Reserved.

28

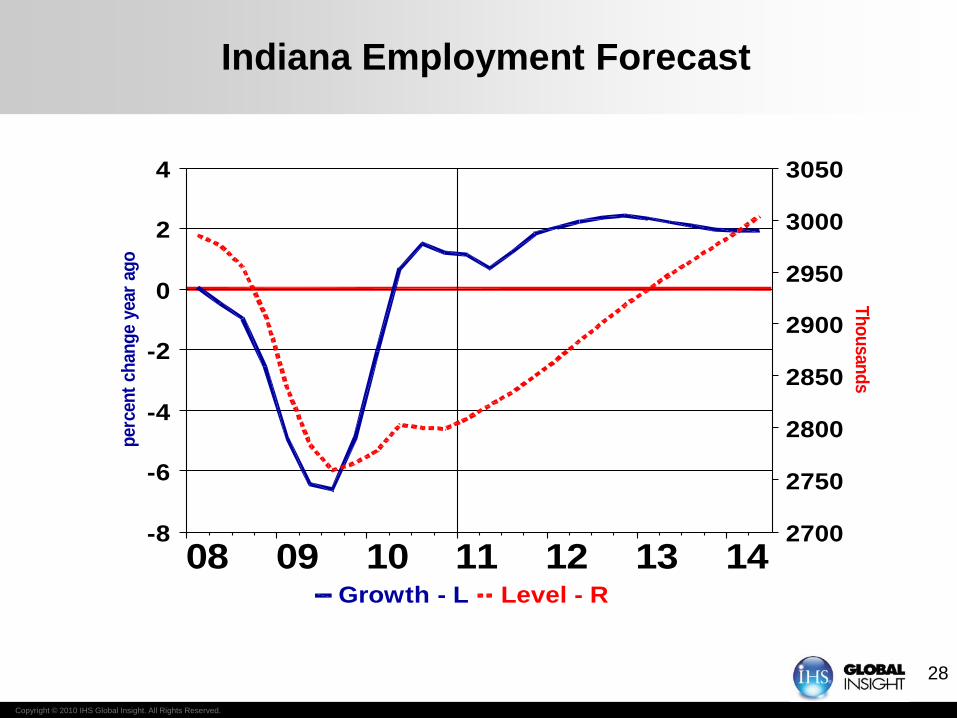

Indiana Employment Forecast

14131211100908

4

2

0

-2

-4

-6

-8

3050

3000

2950

2900

2850

2800

2750

2700

perc

en

t ch

an

ge y

ear

ag

o

Th

ou

san

ds

Growth - L Level - R

Copyright © 2010 IHS Global Insight. All Rights Reserved.

29

Wage Gains Return

(nominal total wages and salaries)

131211100908

10

5

0

-5

-10

-15

10

5

0

-5

-10

-15

per

cen

t ch

ang

e ye

ar a

go

percen

t chan

ge year ag

o

Indiana US

Copyright © 2010 IHS Global Insight. All Rights Reserved.

30

Cars and Houses

131211100908

400

350

300

250

200

150

100

50

30

25

20

15

10

tho

usa

nd

s tho

usan

ds

Indiana New Car Registrations - LIndiana Housing Starts - R

Copyright © 2010 IHS Global Insight. All Rights Reserved.

31

(Percent unless otherwise noted)

Forecast Summary

2009 2010 2011 2012

Employment -5.7 0.3 1.2 2.3

Unemployment Rate 10.4 10.2 8.8 8.5

Personal Income -2.4 3.2 5.0 3.1

Housing Starts (000) 13.1 13.2 13.7 21.7

Retail Sales -7.2 6.6 7.6 5.3

Real Gross State Product -5.0 2.0 2.4 3.1

Thank you!

Jim Diffley

Senior Director

Chief Regional Economist

IHS Global Insight