The Current State of Financial and Accounting Education in Latin America Taiki Hirashima Independent...

21

The Current State of Financial and Accounting Education in Latin America Taiki Hirashima Independent Consultant CReCER Regional Conference Mexico D.F., June 2007 THE WORLD BANK

-

Upload

marylou-arline-lawrence -

Category

Documents

-

view

215 -

download

0

Transcript of The Current State of Financial and Accounting Education in Latin America Taiki Hirashima Independent...

The Current State of Financial and Accounting Education in Latin America

Taiki HirashimaIndependent Consultant

CReCER Regional ConferenceMexico D.F., June 2007

THE WORLD BANK

Disclaimer

The findings, interpretations, and conclusions expressed in this

presentation are entirely those of the presenter. They do not

necessarily represent the view of the World Bank, its Executive

Directors, or the countries they represent.

Background

Lack of other filters for entering the profession: undergraduate degree is often the only prerequisite for entering the profession

Most countries do not require professional experience or passing of professional qualification examination prior to registration as a public accountant (except Mexico and Brazil).

DemographicsTrends in education: lack of convergence (different policies, models, institutions, quality approaches across countries and even within the same country).

Challenges in accounting education in Latin America

Background

Research paper under construction.

This presentation summarizes our preliminary findings.

About this study

Methodology

Sources of information

Primary data: survey sent to 43 universities throughout Central/South America and MexicoSecondary sources

World Bank ROSC programIFAC compliance assessmentBrazil case study through papers, thesis and other accounting educations diagnosis

This is a first attempt aiming to analyze such a complex matter across Latin America, which inherently contains

overwhelming challenges and difficulties.

Presentation of preliminary results

Outline

Today’s presentation will cover the following topics, always trying to analyze strengths and opportunities of Latin America countries towards global accounting convergence:

Accounting curriculaAccounting facultyAccounting studentsSummary and tentative conclusionsNext steps

Preliminary results

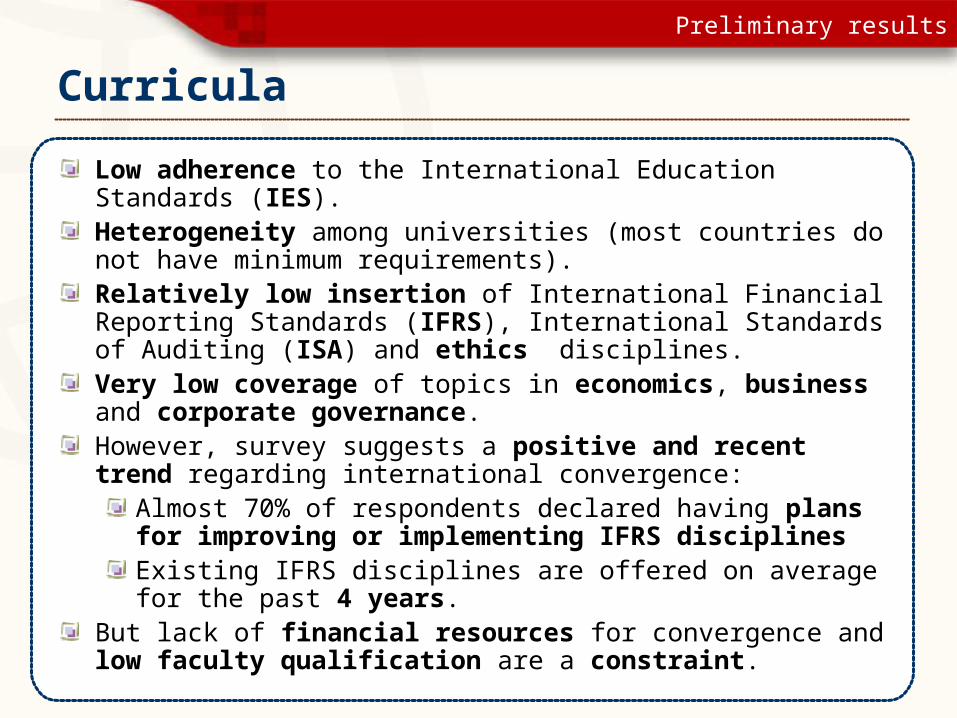

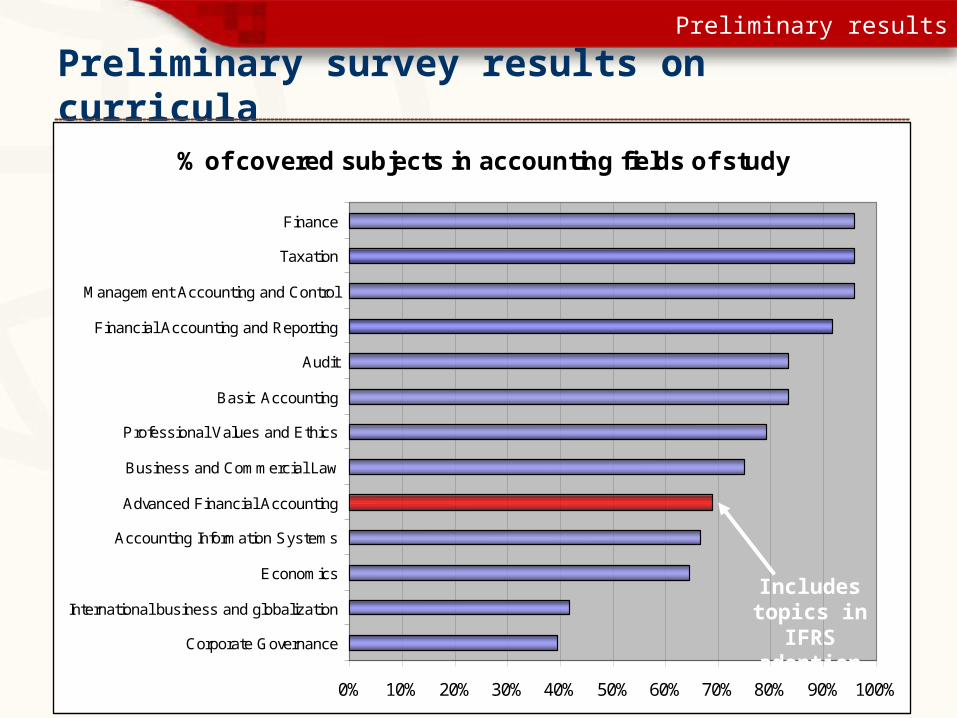

Low adherence to the International Education Standards (IES). Heterogeneity among universities (most countries do not have minimum requirements).Relatively low insertion of International Financial Reporting Standards (IFRS), International Standards of Auditing (ISA) and ethics disciplines. Very low coverage of topics in economics, business and corporate governance.However, survey suggests a positive and recent trend regarding international convergence:

Almost 70% of respondents declared having plans for improving or implementing IFRS disciplinesExisting IFRS disciplines are offered on average for the past 4 years.

But lack of financial resources for convergence and low faculty qualification are a constraint.

Curricula

% of covered subjects in accounting fields of study

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Corporate Governance

International business and globalization

Economics

Accounting Information Systems

Advanced Financial Accounting

Business and Commercial Law

Professional Values and Ethics

Basic Accounting

Audit

Financial Accounting and Reporting

Management Accounting and Control

Taxation

Finance

Preliminary results

Includes topics in IFRS

adoption

Preliminary survey results on curricula

% of insertion of "International Accounting" discipline in accounting undergraduate curricula

0%

5%

10%

15%

20%

25%

30%

Mid-west Northeast North Southeast South

0%

5%

10%

15%

20%

25%

Case study - BRAZIL

Curricula – Case Study Brazil

Source: Weffort (2003)

National Average

Preliminary results

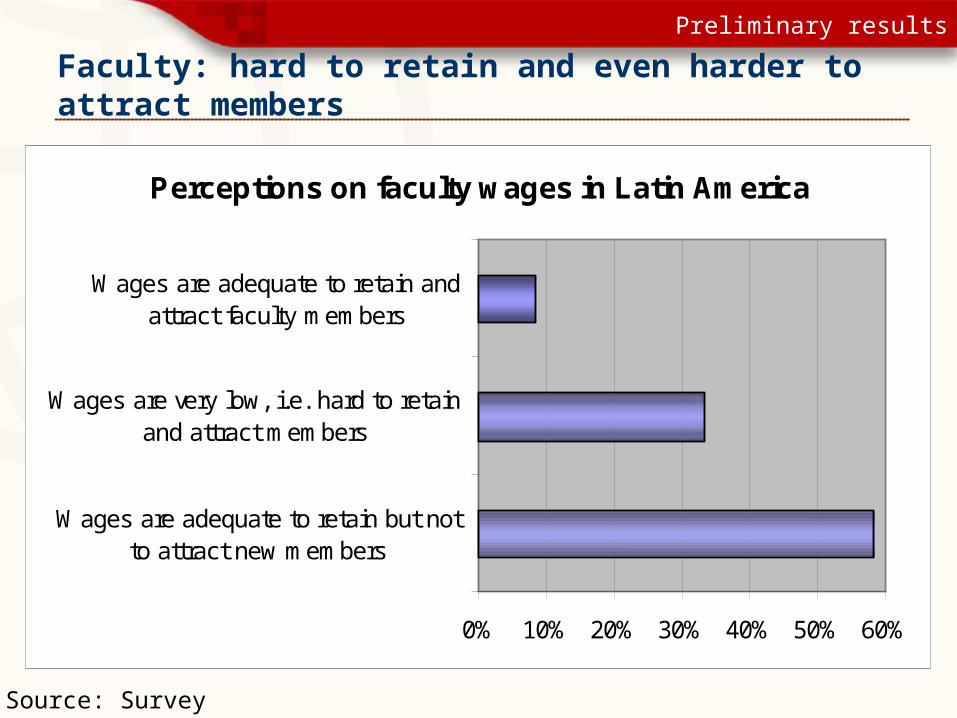

Age of faculty members – seems that we have the “perfect” balance between experience and sustainable efforts to face convergence challenges.Low wages: less than US$1,200 per month for full-time positions in average. Most of faculty members are part-time (65% on survey).Low level of international certification and exchange.Research, despite positive trend, still needs significant improvements, to prepare talented and updated faculty.English language skills are a constraint.

Faculty

Preliminary results

Includes topics in IFRS

adoption

Faculty age: promising human capital for future challenges

Average age of faculty members

0% 10% 20% 30% 40% 50%

<30 years old

31-40 years old

41-50 years old

51-60 years old

61-70 years old

>70 years oldBalance between experience and remaining working time

Source: Survey

Preliminary results

Includes topics in IFRS

adoption

Faculty: hard to retain and even harder to attract members

Source: Survey

Perceptions on faculty wages in Latin America

0% 10% 20% 30% 40% 50% 60%

Wages are adequate to retain but notto attract new members

Wages are very low, i.e. hard to retainand attract members

Wages are adequate to retain andattract faculty members

Preliminary results

Includes topics in IFRS

adoption

Research as knowledge bank for quality education – perspectives must be improved

Survey so far has shown that accounting research is incipient:Low engagement in research, since 65% of faculty, in average, are part-time.Less than 50% of faculty is engaged in publishing accounting papers or books.Only 10% of faculty engages in international academic exchange.

Brazilian case also shows need for improvements in preparing qualified faculty:

Graduate Programs in Brazil (2006)

13

5062

17

16

2

0102030405060708090

Accounting Economics BusinessAdministration

PhD

Master

Source: CAPES

Preliminary results

Low ratio of applications / admissions (ranging from 1.2 to 2.5 so far in survey).Steady growth in actual admissions (Brazil case). Survey indicates stable demand (last 10 years) for more than 50% of respondents.Survey indicates that pass rate is lower compared to “hard sciences” (e.g. engineering) and around the same compared to other social sciences. However, rates are decreasing in time (slightly).

Attracting high-caliber students

Preliminary results

Survey suggests an overall adequacy of infrastructure:67% declared to have enough relevant textbooks available.69% declared that university library is updated.71% declared that their students have access to materials from other libraries.63% declared to have enough PC’s and internet access for accounting students in the university.

However, availability of translated IFRS, ISA and Code of Ethics seems to be a constraint.

Attracting high-caliber students

Environment for attracting high-caliber students needs improvements

% of respondents that indicated avalilability of the following materials:

0% 10% 20% 30% 40% 50% 60%

Translation of ISA

Translation of IFRS

Translation of Code of Ethics (IFAC)

English version of IFRS

English version of ISA

English version of Code of Ethics (IFAC)

Source: Survey

Preliminary results

Applications / Admissions ratio

-

0.50

1.00

1.50

2.00

2.50

2001 2002 2003 2004 2005

Accounting

Economics

B. Administration

Brazil case

Source: MEC/INEP

Oversupply

Case study - BRAZIL

Brazil case: failure in certification exam

Source: Conselho Federal de Contabilidade (Federal Accounting Council)

186

592333

10

332368

97 72

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006

Absent

Failed

Approved

HeterogeneousCurricula

Low QualityEducation

Failure inCertification

Exam+ =

Case study - BRAZIL

Summary

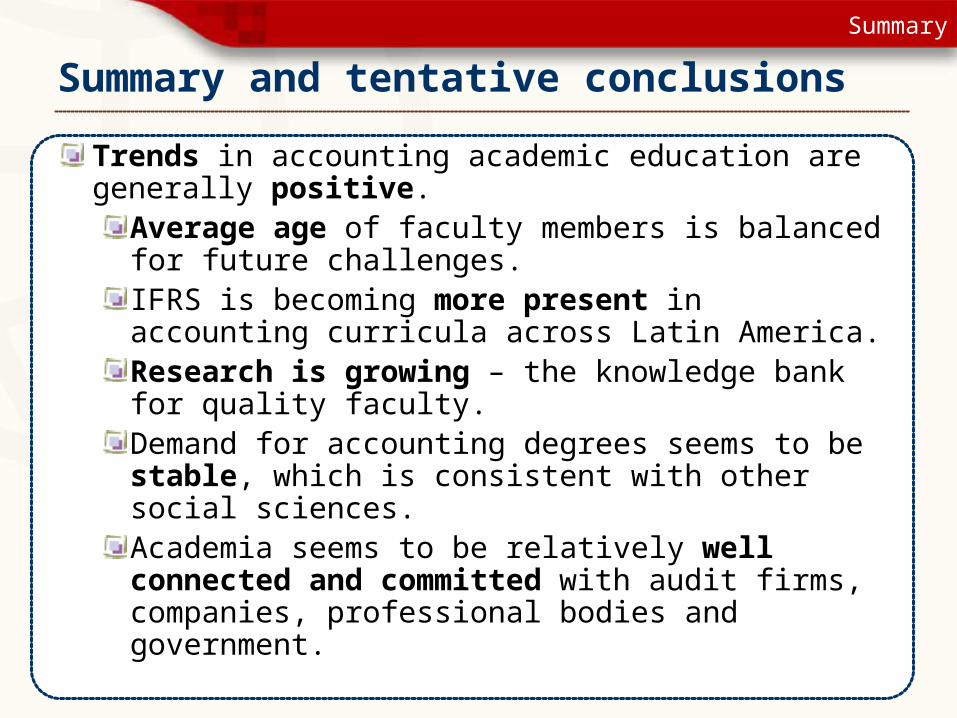

Trends in accounting academic education are generally positive.

Average age of faculty members is balanced for future challenges.IFRS is becoming more present in accounting curricula across Latin America.Research is growing – the knowledge bank for quality faculty.Demand for accounting degrees seems to be stable, which is consistent with other social sciences.Academia seems to be relatively well connected and committed with audit firms, companies, professional bodies and government.

Summary and tentative conclusions

Summary

However, qualification (including English language) of both students and faculty are a currently constraint for global convergence.In general terms, accounting in companies is not a profession to be “proud of” (low wages, low competition in application processes, low level of full-time faculty, high concentration of hires by audit firms).Part-time faculty

Faculty position as a complementary job. Research still incipient.Accounting Curricula

Heterogeneity in an increasing sophistication environment.Low adherence to IES.Low presence of IFRS and ISA.

Governments should stand more actively regarding surveillance of accounting education (e.g. prevent oversupply, monitor quality, examine before practice), probably with assistance of qualified bodies.

Summary and tentative conclusions

Summary

Survey enrichment through a more representative sample is a major goal:

Questionnaires sent to 43 universities. Replies so far - 12 universities.

Conclusion of the study expected to happen in the upcoming months.

Research paper will be included in the World Bank publication based on CReCER Conference (to be issued late 2007/early 2008).

Next steps