The current economic situation Jönköping March 2009 Deputy Governor Svante Öberg

37

The current economic situation Jönköping March 2009 Deputy Governor Svante Öberg

-

Upload

eleanor-knight -

Category

Documents

-

view

25 -

download

0

description

The current economic situation Jönköping March 2009 Deputy Governor Svante Öberg. Summary. The financial turmoil worsened last autumn and has developed into a global financial crisis. - PowerPoint PPT Presentation

Transcript of The current economic situation Jönköping March 2009 Deputy Governor Svante Öberg

The current economic situation

Jönköping March 2009

Deputy GovernorSvante Öberg

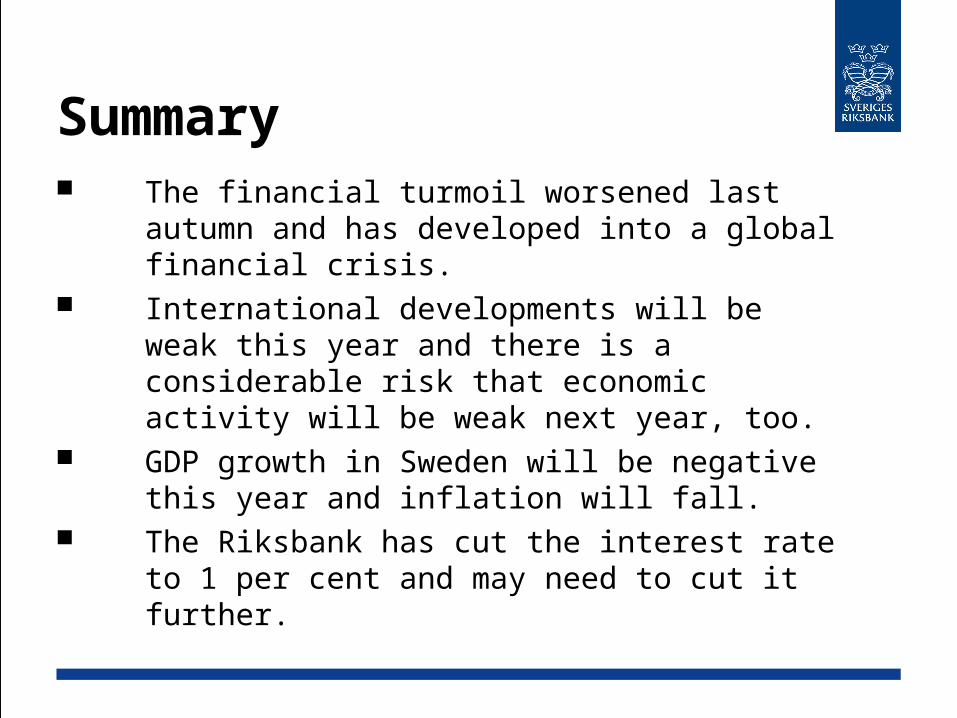

Summary The financial turmoil worsened last autumn

and has developed into a global financial crisis.

International developments will be weak this year and there is a considerable risk that economic activity will be weak next year, too.

GDP growth in Sweden will be negative this year and inflation will fall.

The Riksbank has cut the interest rate to 1 per cent and may need to cut it further.

Contents Financial market International outlook Sweden Monetary policy

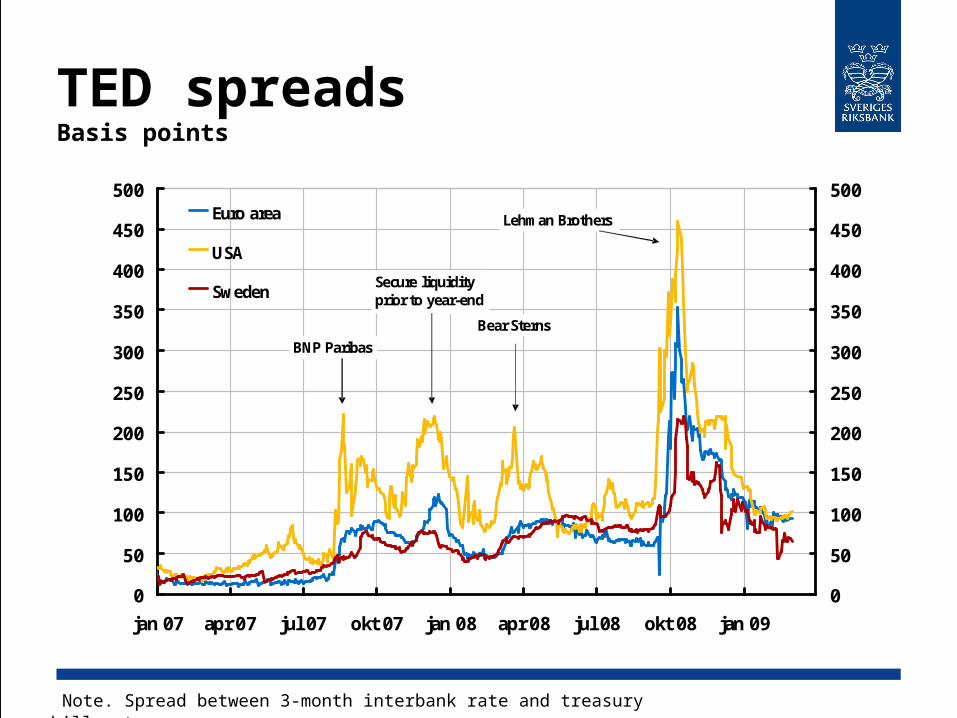

TED spreads Basis points

Note. Spread between 3-month interbank rate and treasury bill rate.

0

50

100

150

200

250

300

350

400

450

500

jan 07 apr 07 jul 07 okt 07 jan 08 apr 08 jul 08 okt 08 jan 09

0

50

100

150

200

250

300

350

400

450

500Euro area

USA

Sweden

BNP Paribas

Secure liquidity prior to year-end

Bear Sterns

Lehman Brothers

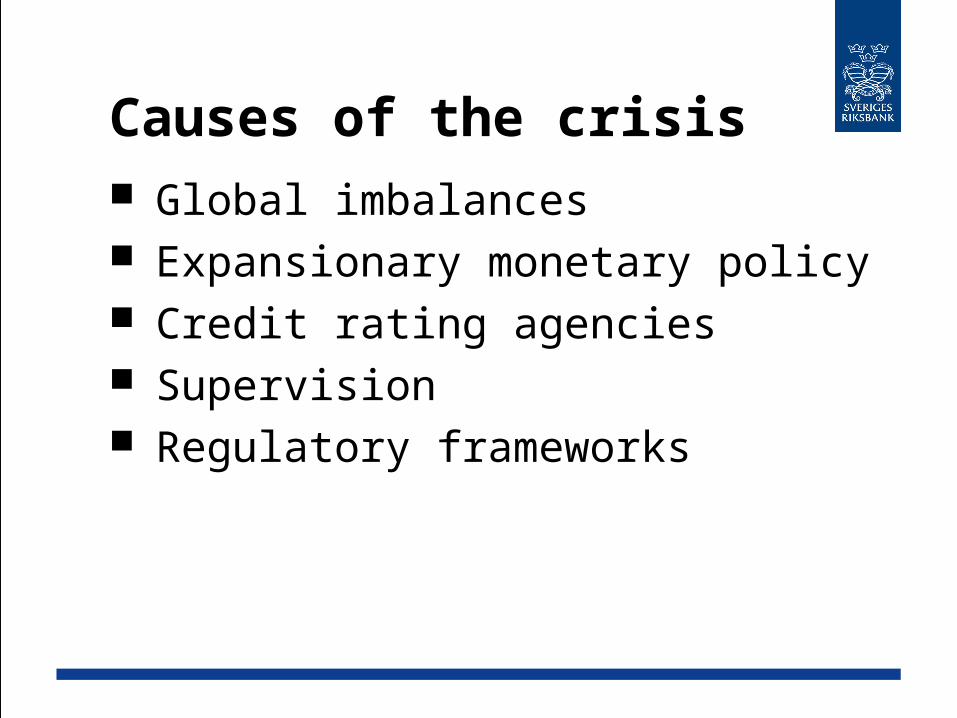

Causes of the crisis Global imbalances Expansionary monetary policy Credit rating agencies Supervision Regulatory frameworks

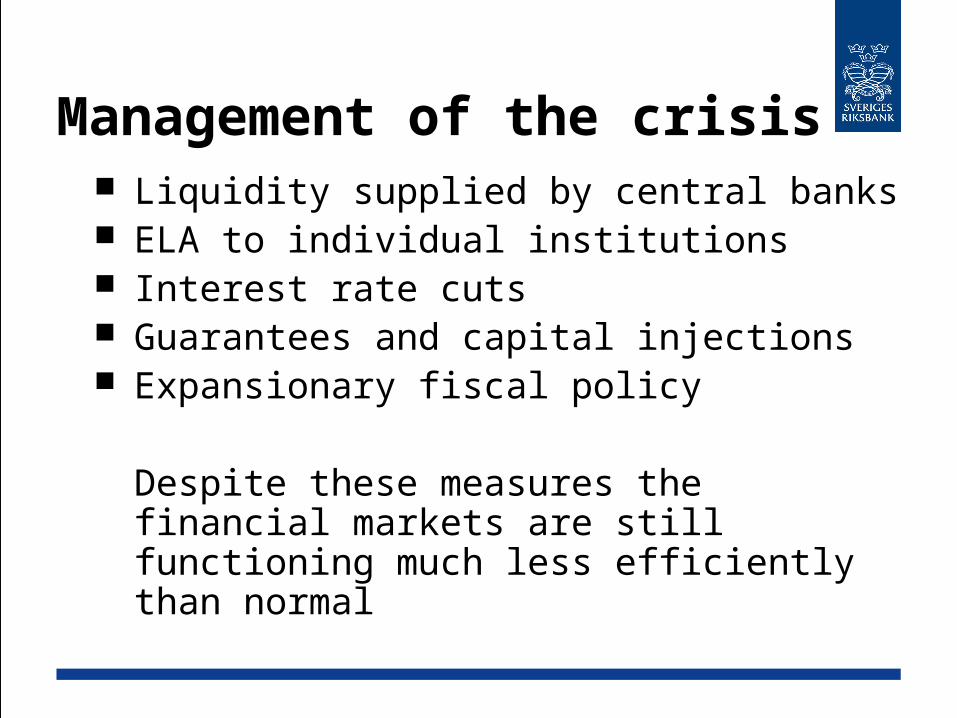

Management of the crisis Liquidity supplied by central banks ELA to individual institutions Interest rate cuts Guarantees and capital injections Expansionary fiscal policy

Despite these measures the financial markets are still functioning much less efficiently than normal

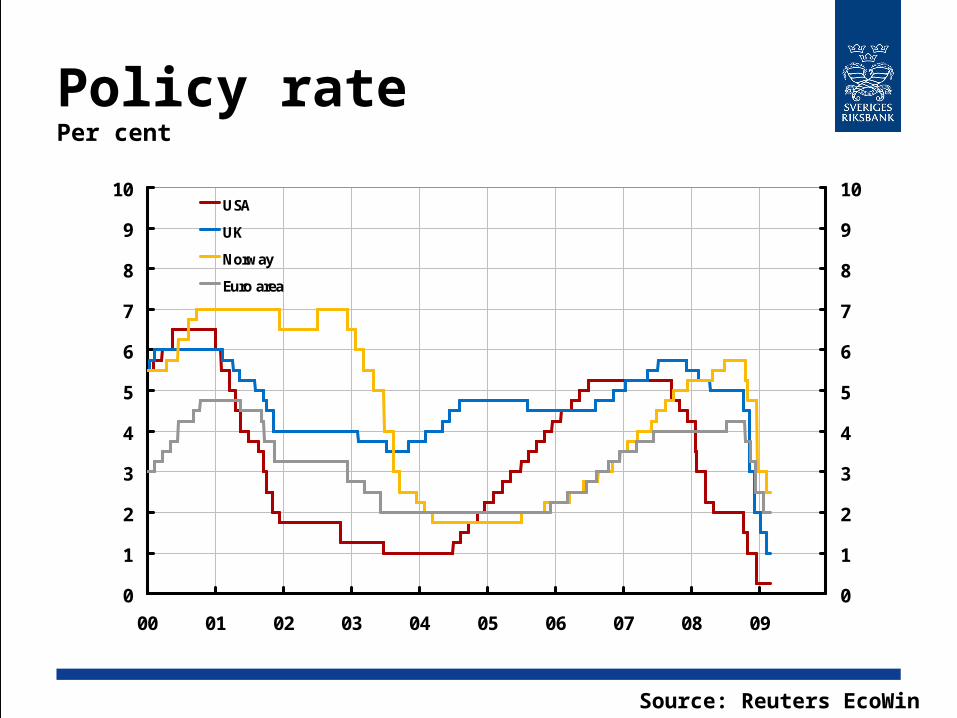

Policy ratePer cent

Source: Reuters EcoWin

0

1

2

3

4

5

6

7

8

9

10

00 01 02 03 04 05 06 07 08 09

0

1

2

3

4

5

6

7

8

9

10USA

UK

Norway

Euro area

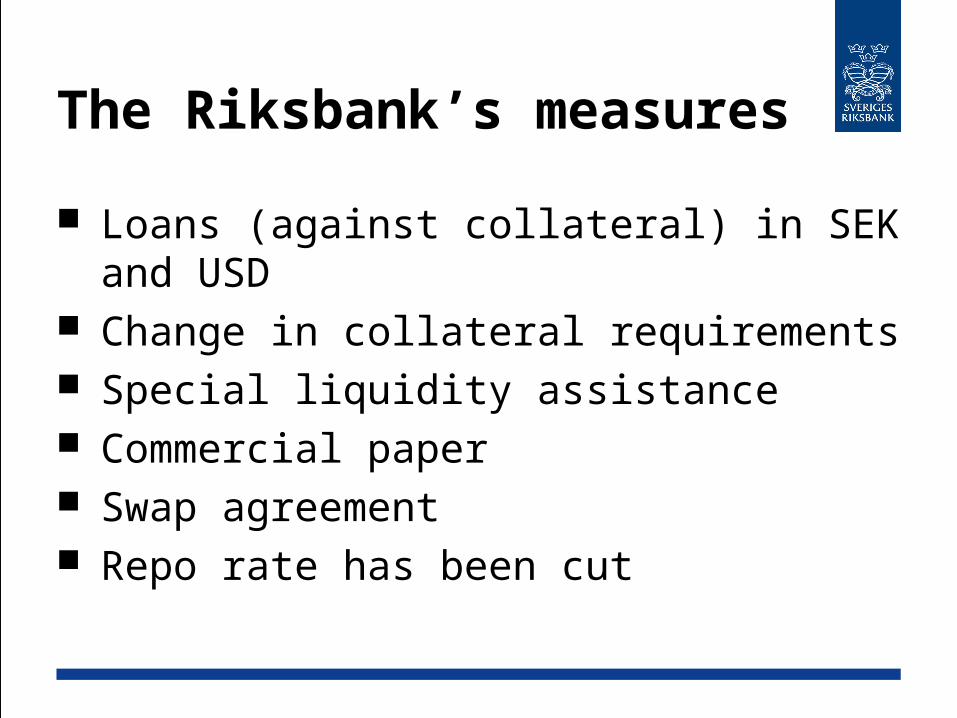

The Riksbank’s measures

Loans (against collateral) in SEK and USD

Change in collateral requirements Special liquidity assistance Commercial paper Swap agreement Repo rate has been cut

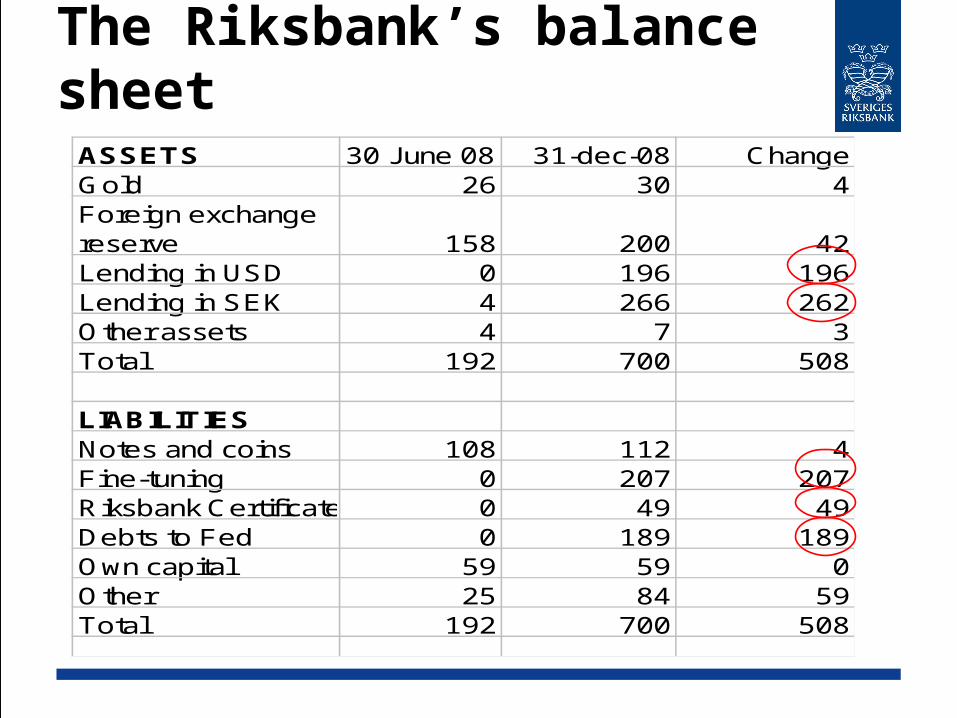

The Riksbank’s balance sheetASSETS 30 June 08 31-dec-08 ChangeGold 26 30 4Foreign exchange reserve 158 200 42Lending in USD 0 196 196Lending in SEK 4 266 262Other assets 4 7 3Total 192 700 508

LIABILITIESNotes and coins 108 112 4Fine-tuning 0 207 207Riksbank Certificates 0 49 49Debts to Fed 0 189 189Own capital 59 59 0Other 25 84 59Total 192 700 508

Contents Financial market

International outlook Sweden Monetary policy

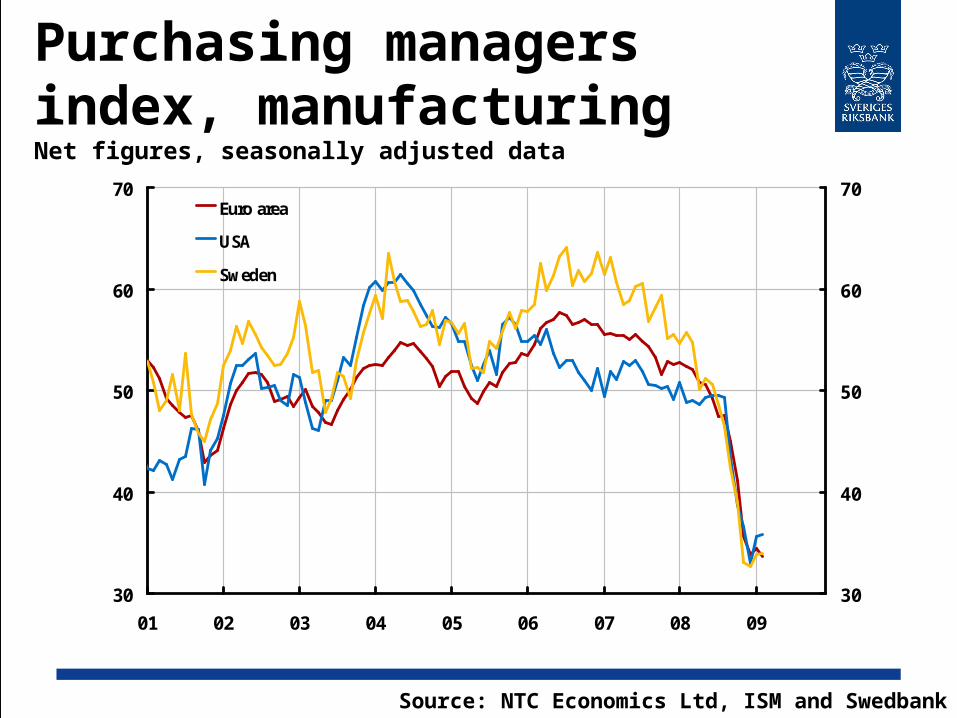

Purchasing managers index, manufacturingNet figures, seasonally adjusted data

Source: NTC Economics Ltd, ISM and Swedbank

30

40

50

60

70

01 02 03 04 05 06 07 08 09

30

40

50

60

70Euro area

USA

Sweden

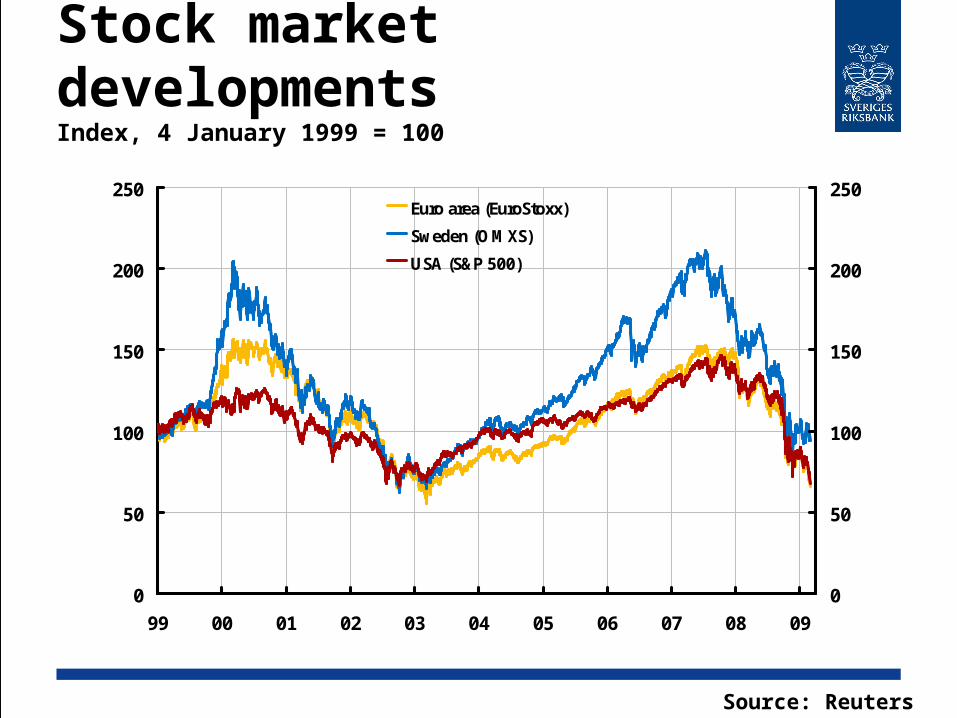

Stock market developmentsIndex, 4 January 1999 = 100

Source: Reuters Ecowin

0

50

100

150

200

250

99 00 01 02 03 04 05 06 07 08 09

0

50

100

150

200

250Euro area (EuroStoxx)

Sweden (OMXS)

USA (S&P 500)

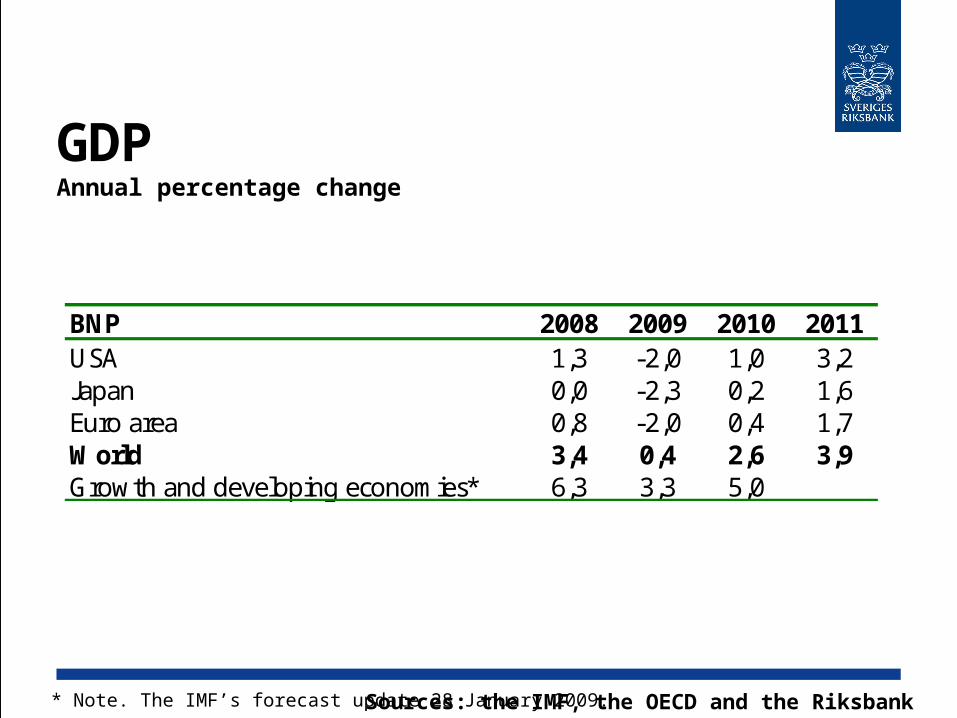

GDPAnnual percentage change

Sources: the IMF, the OECD and the Riksbank* Note. The IMF’s forecast update 28 January 2009.

BNP 2008 2009 2010 2011USA 1,3 -2,0 1,0 3,2Japan 0,0 -2,3 0,2 1,6Euro area 0,8 -2,0 0,4 1,7World 3,4 0,4 2,6 3,9Growth and developing economies* 6,3 3,3 5,0

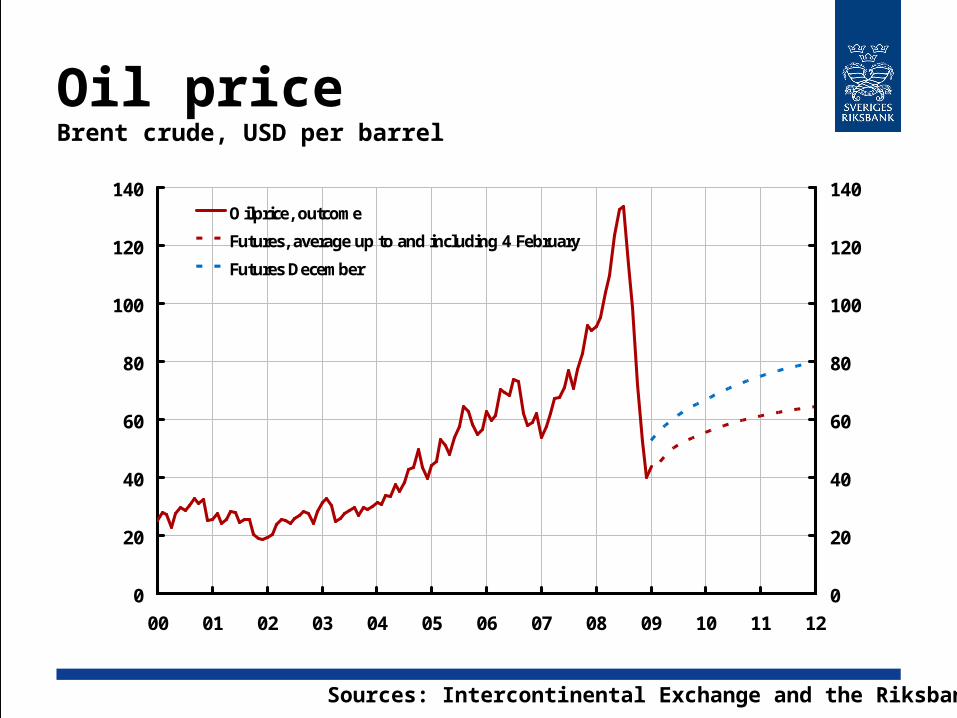

Oil priceBrent crude, USD per barrel

Sources: Intercontinental Exchange and the Riksbank

0

20

40

60

80

100

120

140

00 01 02 03 04 05 06 07 08 09 10 11 12

0

20

40

60

80

100

120

140Oilprice, outcome

Futures, average up to and including 4 February

Futures December

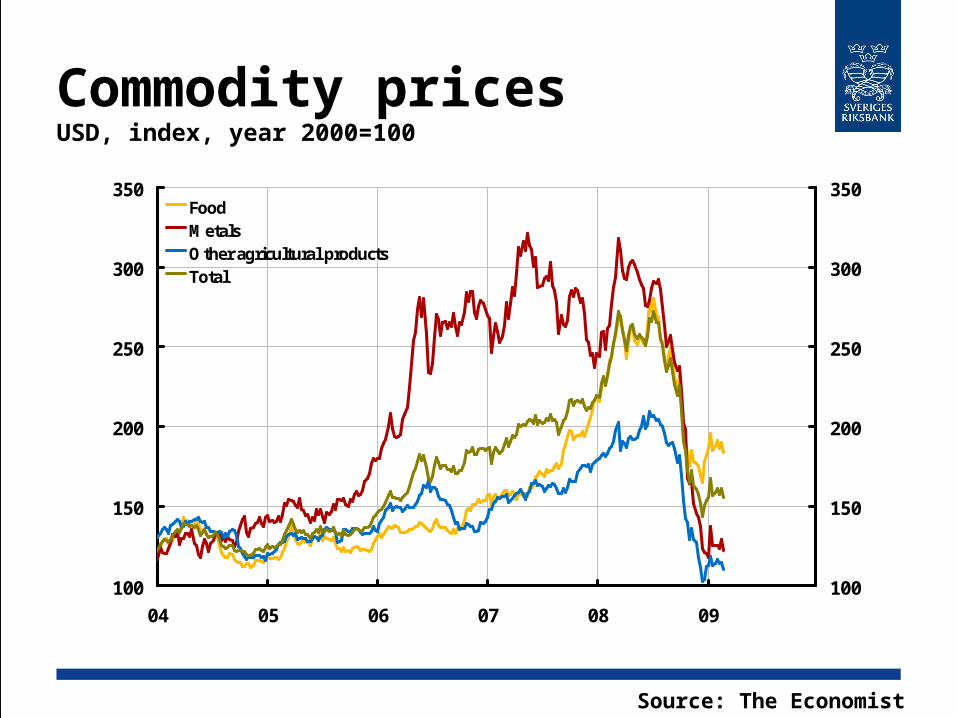

Commodity pricesUSD, index, year 2000=100

Source: The Economist

100

150

200

250

300

350

04 05 06 07 08 09

100

150

200

250

300

350FoodMetalsOther agricultural productsTotal

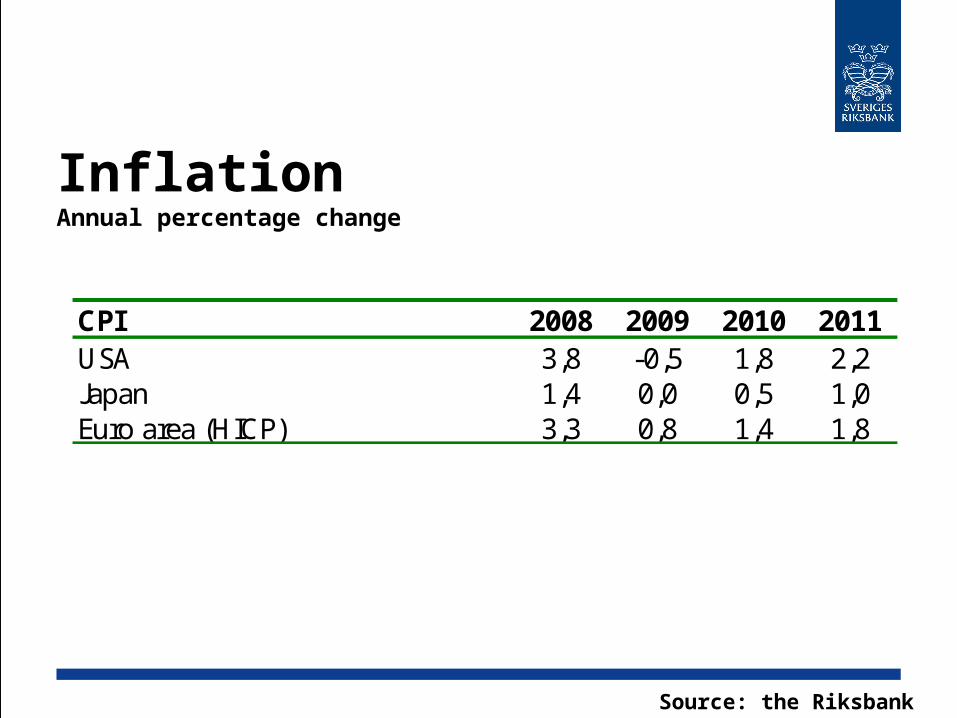

InflationAnnual percentage change

Source: the Riksbank

CPI 2008 2009 2010 2011USA 3,8 -0,5 1,8 2,2Japan 1,4 0,0 0,5 1,0Euro area (HICP) 3,3 0,8 1,4 1,8

Growth picks up again in 2010

Forceful measures to stabilise the financial markets

Expansionary fiscal and monetary policy

Low inflation

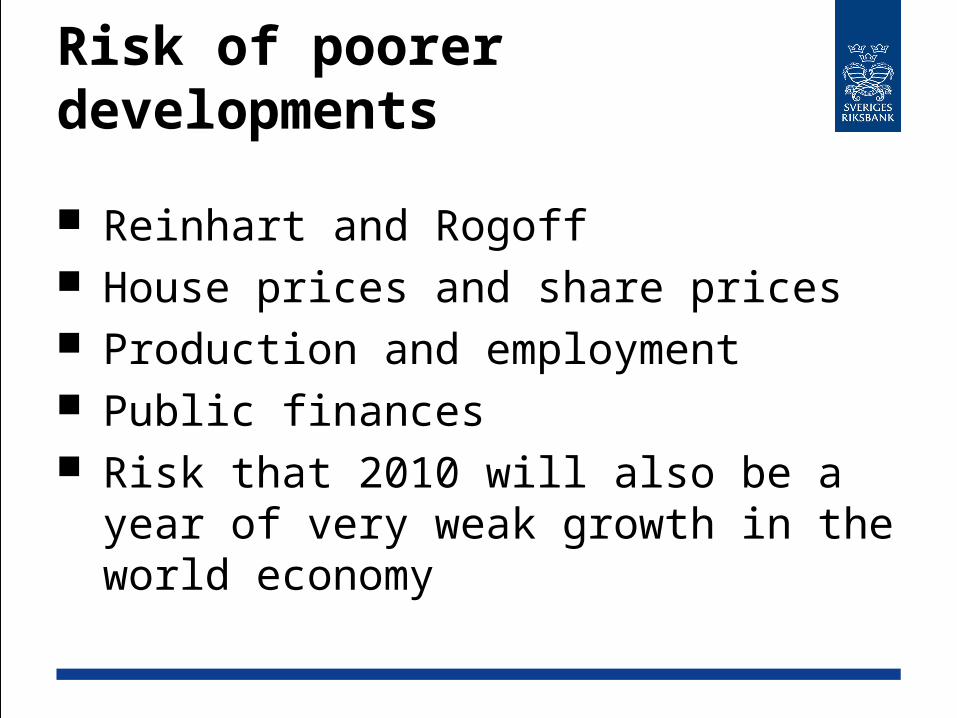

Risk of poorer developments

Reinhart and Rogoff House prices and share prices Production and employment Public finances Risk that 2010 will also be a year of

very weak growth in the world economy

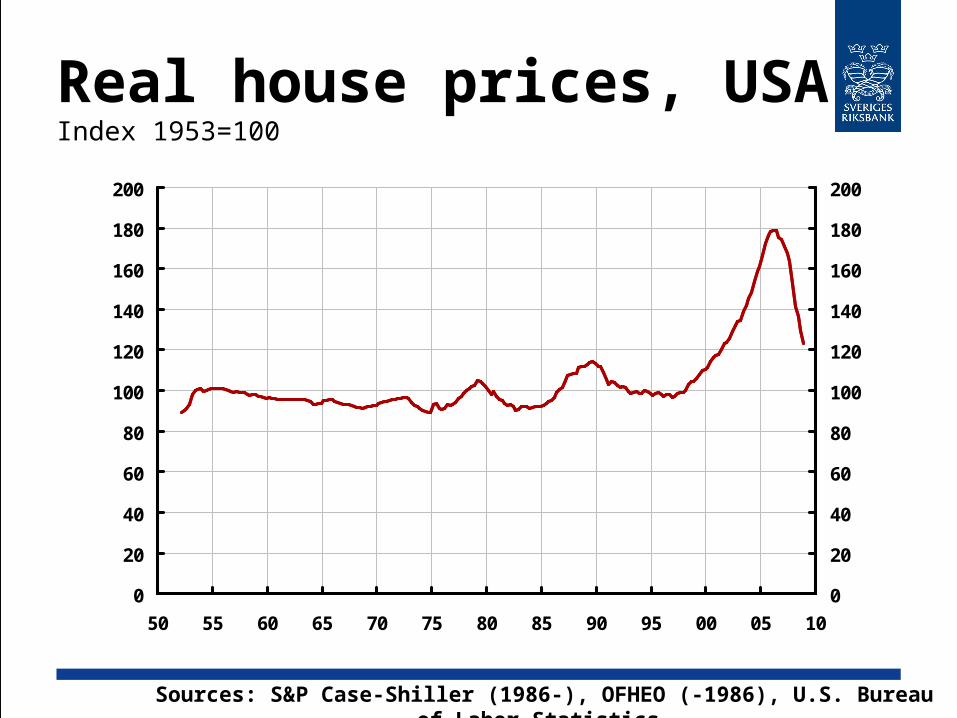

Real house prices, USAIndex 1953=100

Sources: S&P Case-Shiller (1986-), OFHEO (-1986), U.S. Bureau of Labor Statistics

0

20

40

60

80

100

120

140

160

180

200

50 55 60 65 70 75 80 85 90 95 00 05 10

0

20

40

60

80

100

120

140

160

180

200

Contents Financial market International outlook

Sweden Monetary policy

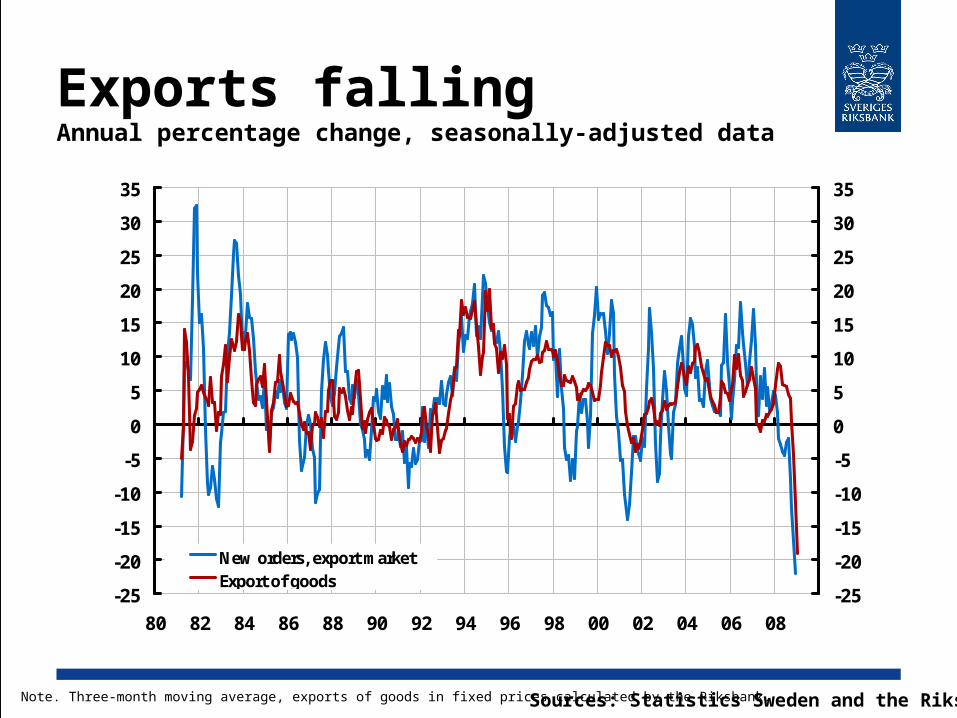

Exports fallingAnnual percentage change, seasonally-adjusted data

Note. Three-month moving average, exports of goods in fixed prices calculated by the Riksbank.Sources: Statistics Sweden and the Riksbank

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

35

New orders, export marketExport of goods

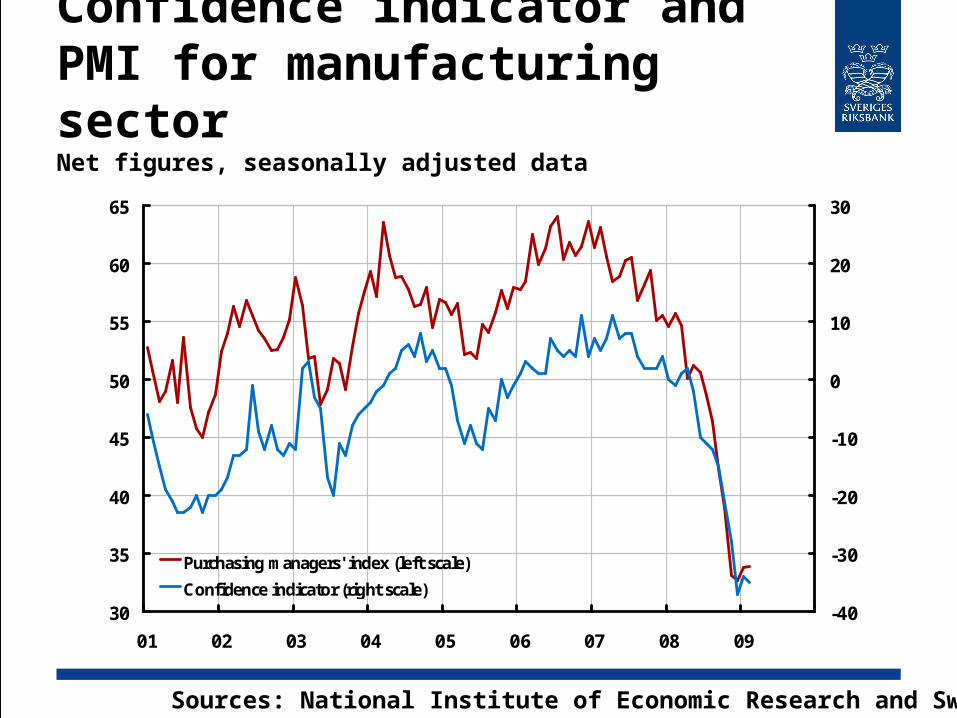

Confidence indicator andPMI for manufacturing sectorNet figures, seasonally adjusted data

Sources: National Institute of Economic Research and Swedbank

30

35

40

45

50

55

60

65

01 02 03 04 05 06 07 08 09

-40

-30

-20

-10

0

10

20

30

Purchasing managers' index (left scale)

Confidence indicator (right scale)

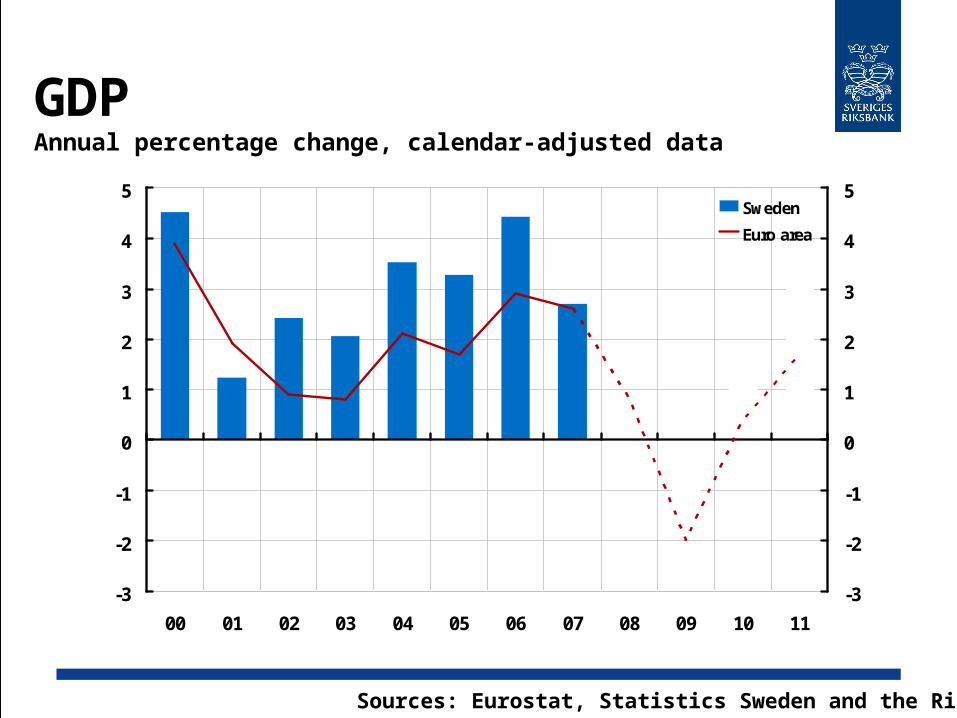

GDPAnnual percentage change, calendar-adjusted data

Sources: Eurostat, Statistics Sweden and the Riksbank

-3

-2

-1

0

1

2

3

4

5

00 01 02 03 04 05 06 07 08 09 10 11

-3

-2

-1

0

1

2

3

4

5Sweden

Euro area

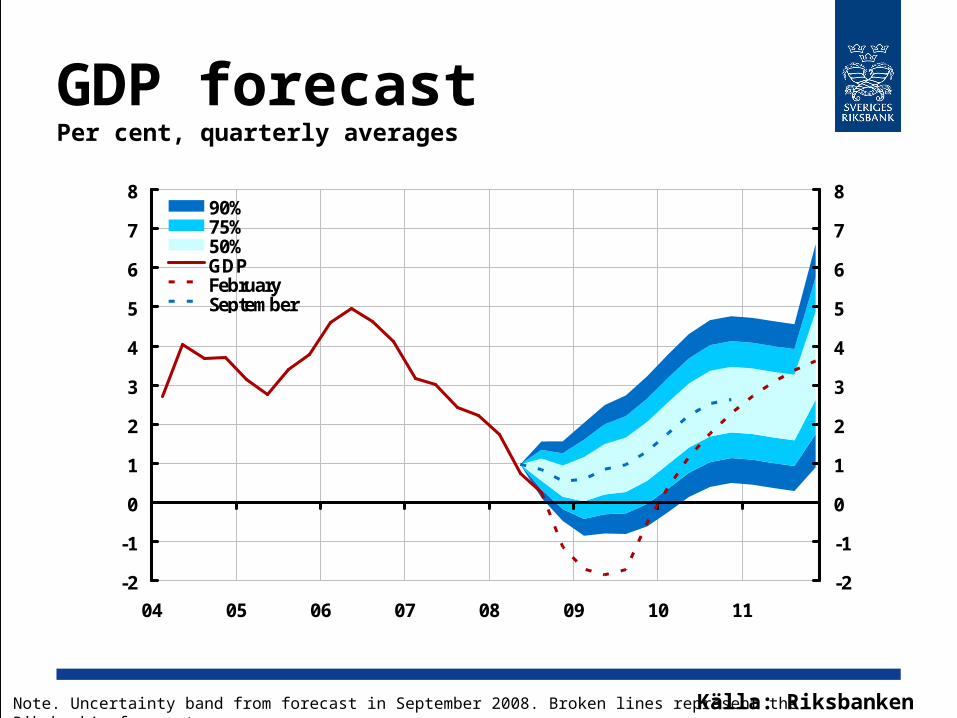

GDP forecastPer cent, quarterly averages

Källa: RiksbankenNote. Uncertainty band from forecast in September 2008. Broken lines represent the Riksbank’s forecasts.

-2

-1

0

1

2

3

4

5

6

7

8

04 05 06 07 08 09 10 11

-2

-1

0

1

2

3

4

5

6

7

890%75%50%GDPFebruarySeptember

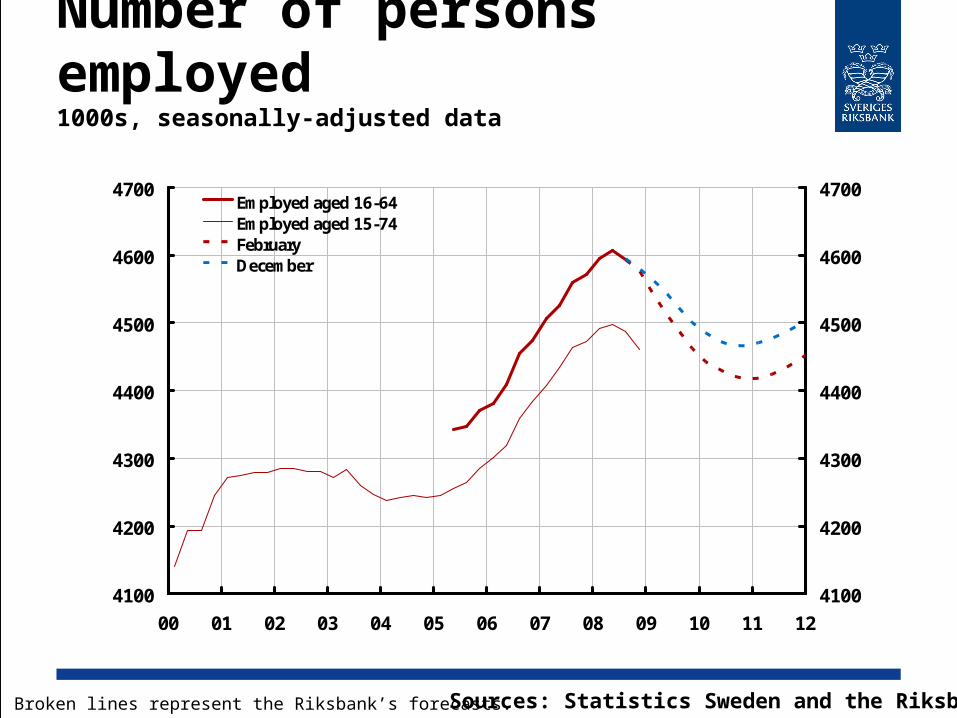

Number of persons employed1000s, seasonally-adjusted data

Sources: Statistics Sweden and the Riksbank

4100

4200

4300

4400

4500

4600

4700

00 01 02 03 04 05 06 07 08 09 10 11 12

4100

4200

4300

4400

4500

4600

4700Employed aged 16-64 Employed aged 15-74 FebruaryDecember

Note. Broken lines represent the Riksbank’s forecasts.

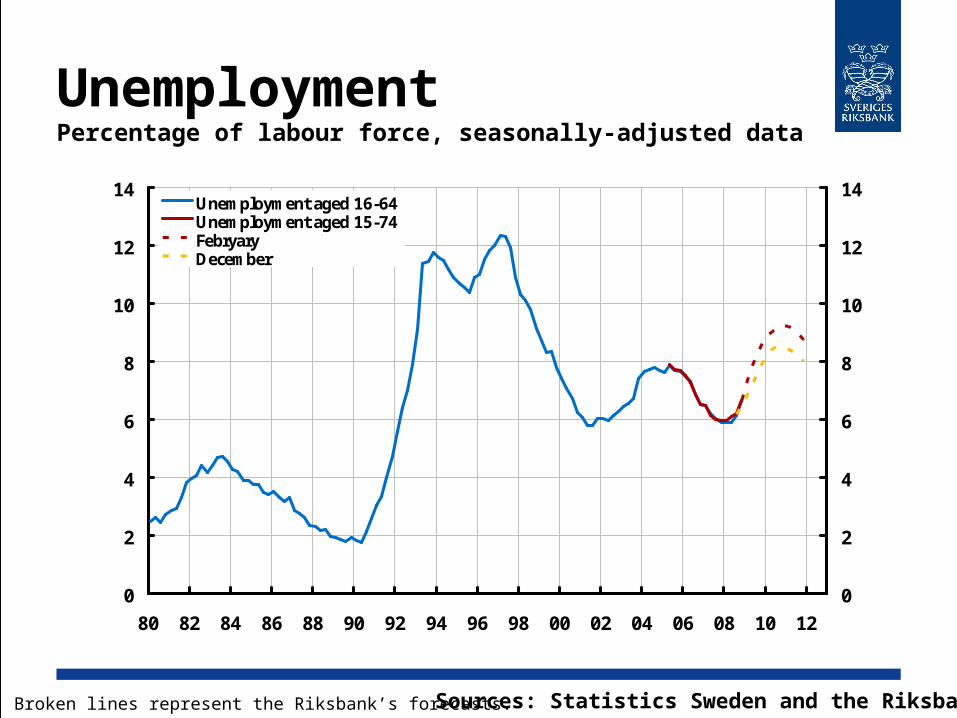

UnemploymentPercentage of labour force, seasonally-adjusted data

Sources: Statistics Sweden and the Riksbank

0

2

4

6

8

10

12

14

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

0

2

4

6

8

10

12

14Unemployment aged 16-64 Unemployment aged 15-74 FebryaryDecember

Note. Broken lines represent the Riksbank’s forecasts.

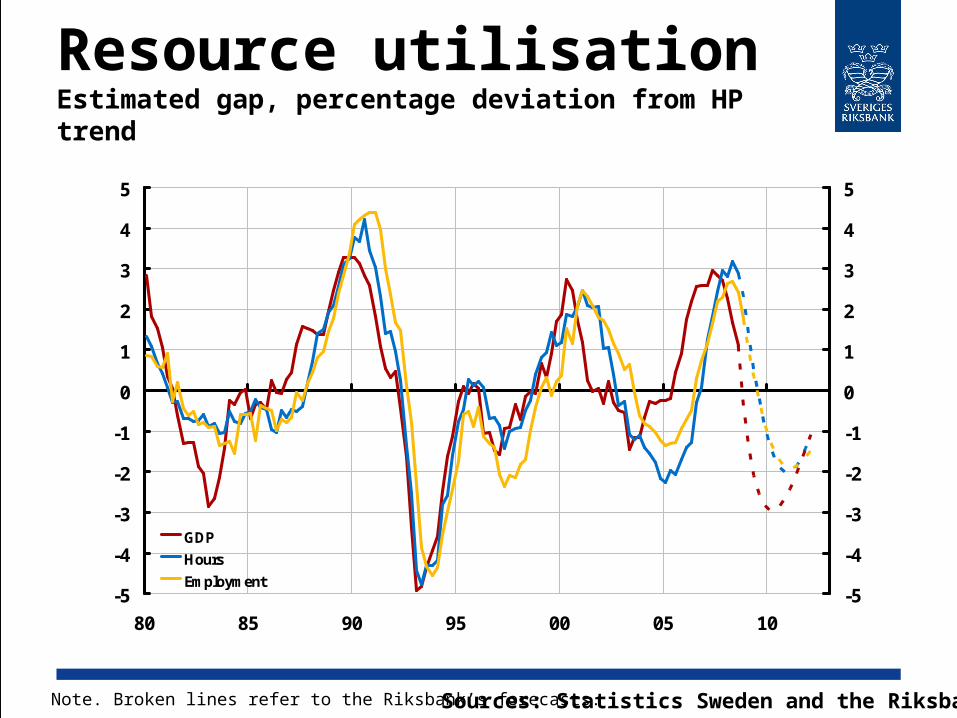

Resource utilisationEstimated gap, percentage deviation from HP trend

Sources: Statistics Sweden and the RiksbankNote. Broken lines refer to the Riksbank’s forecasts.

-5

-4

-3

-2

-1

0

1

2

3

4

5

80 85 90 95 00 05 10

-5

-4

-3

-2

-1

0

1

2

3

4

5

GDP

Hours

Employment

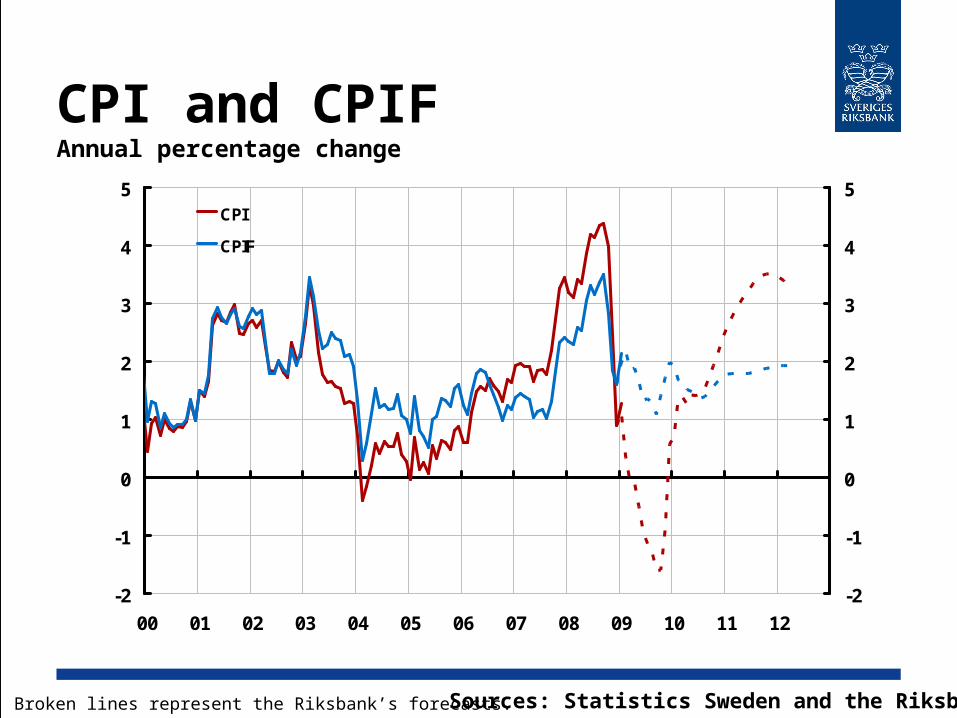

CPI and CPIFAnnual percentage change

Sources: Statistics Sweden and the Riksbank

-2

-1

0

1

2

3

4

5

00 01 02 03 04 05 06 07 08 09 10 11 12

-2

-1

0

1

2

3

4

5CPI

CPIF

Note. Broken lines represent the Riksbank’s forecasts.

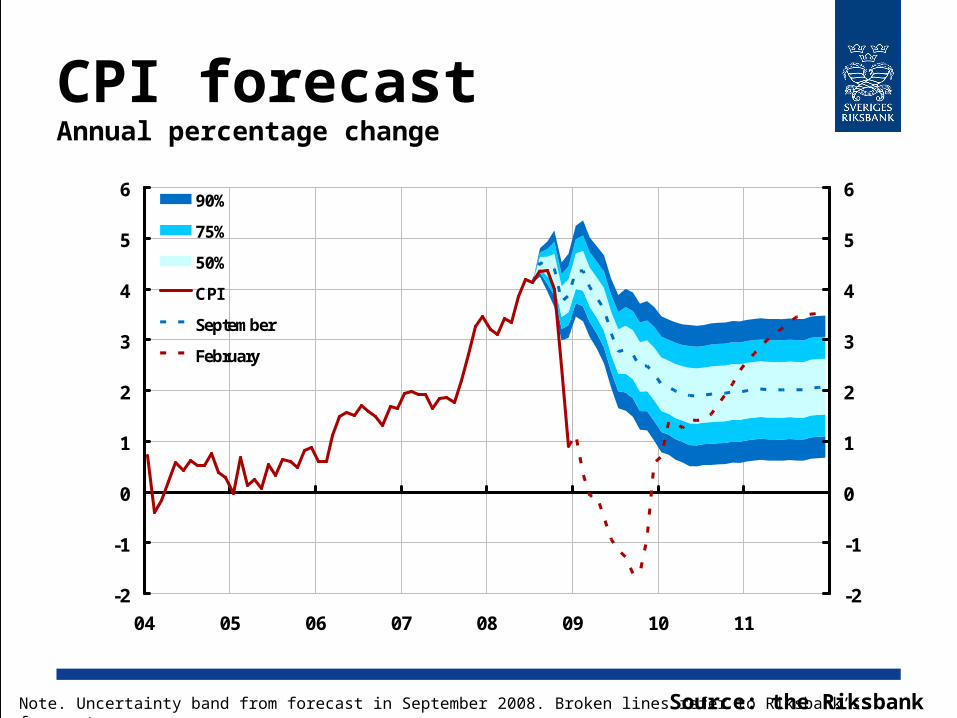

CPI forecastAnnual percentage change

Source: the RiksbankNote. Uncertainty band from forecast in September 2008. Broken lines refer to Riksbank’s forecasts.

-2

-1

0

1

2

3

4

5

6

04 05 06 07 08 09 10 11

-2

-1

0

1

2

3

4

5

690%

75%

50%

CPI

September

February

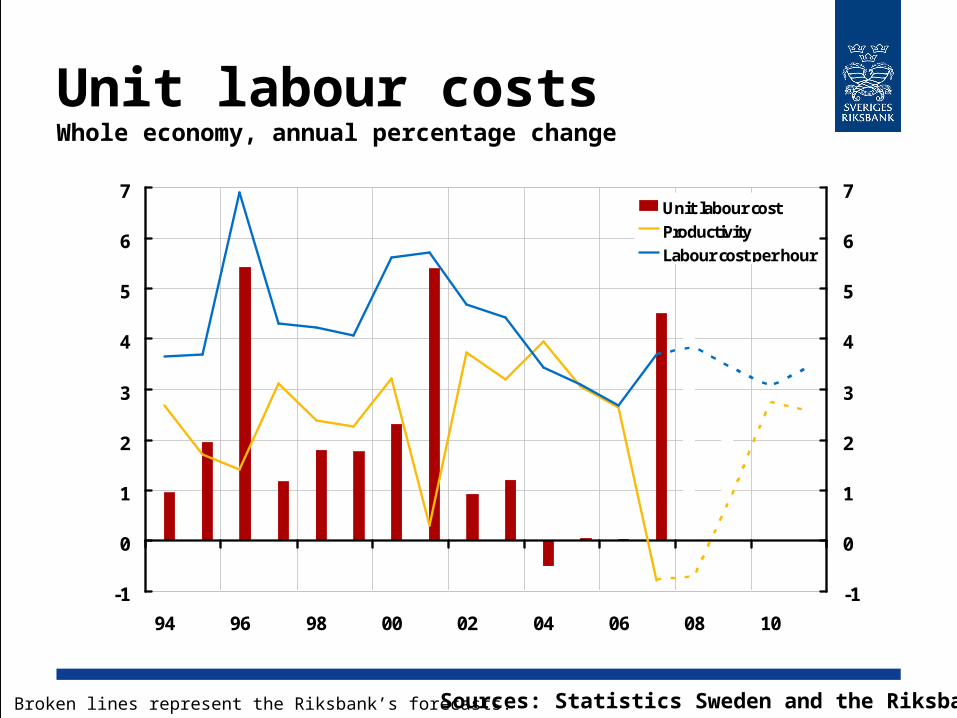

Unit labour costs Whole economy, annual percentage change

Sources: Statistics Sweden and the Riksbank

-1

0

1

2

3

4

5

6

7

94 96 98 00 02 04 06 08 10

-1

0

1

2

3

4

5

6

7Unit labour costProductivityLabour cost per hour

Note. Broken lines represent the Riksbank’s forecasts.

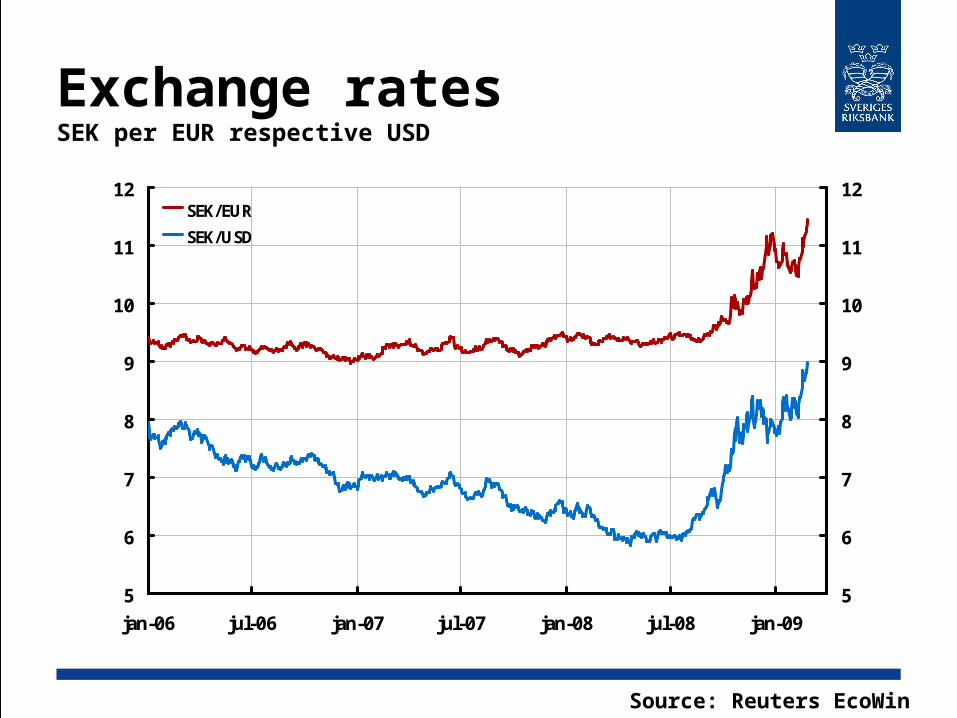

Exchange ratesSEK per EUR respective USD

Source: Reuters EcoWin

5

6

7

8

9

10

11

12

jan-06 jul-06 jan-07 jul-07 jan-08 jul-08 jan-09

5

6

7

8

9

10

11

12SEK/EUR

SEK/USD

Contents Financial market International outlook Sweden

Monetary policy

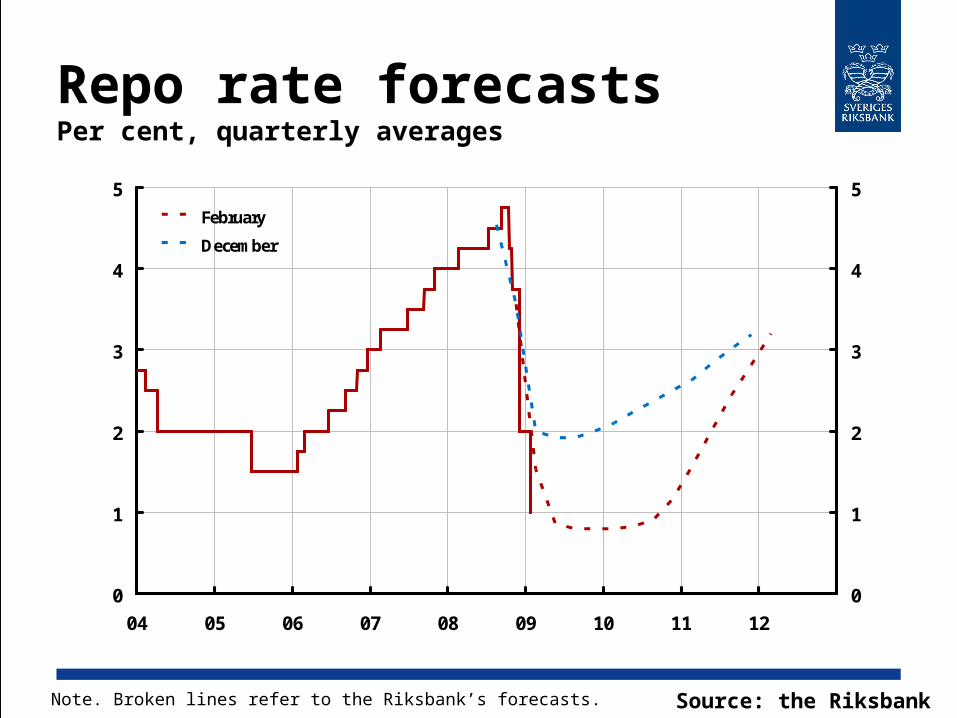

Repo rate forecastsPer cent, quarterly averages

Source: the RiksbankNote. Broken lines refer to the Riksbank’s forecasts.

0

1

2

3

4

5

04 05 06 07 08 09 10 11 12

0

1

2

3

4

5February

December

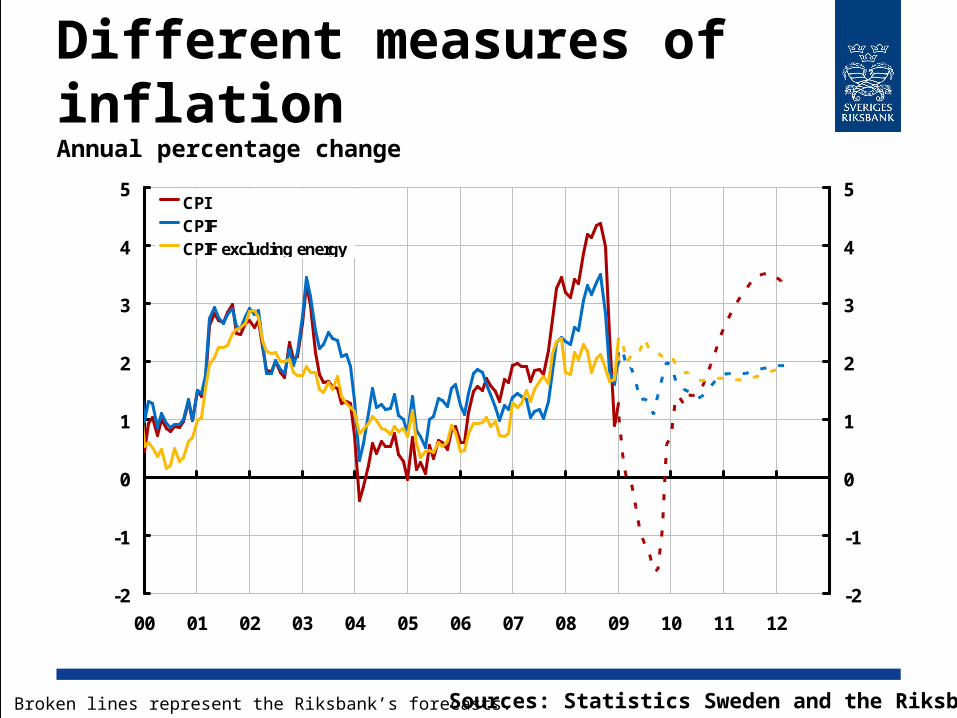

Different measures of inflationAnnual percentage change

Sources: Statistics Sweden and the Riksbank

-2

-1

0

1

2

3

4

5

00 01 02 03 04 05 06 07 08 09 10 11 12

-2

-1

0

1

2

3

4

5CPICPIFCPIF excluding energy

Note. Broken lines represent the Riksbank’s forecasts.

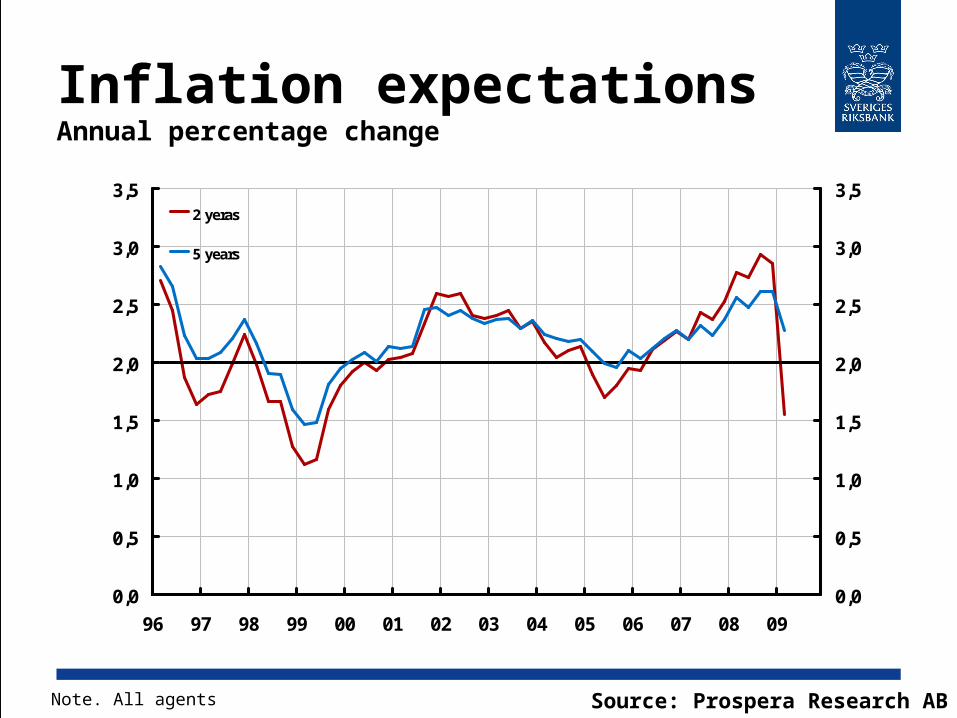

Inflation expectationsAnnual percentage change

Source: Prospera Research ABNote. All agents

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

96 97 98 99 00 01 02 03 04 05 06 07 08 09

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,52 yeras

5 years

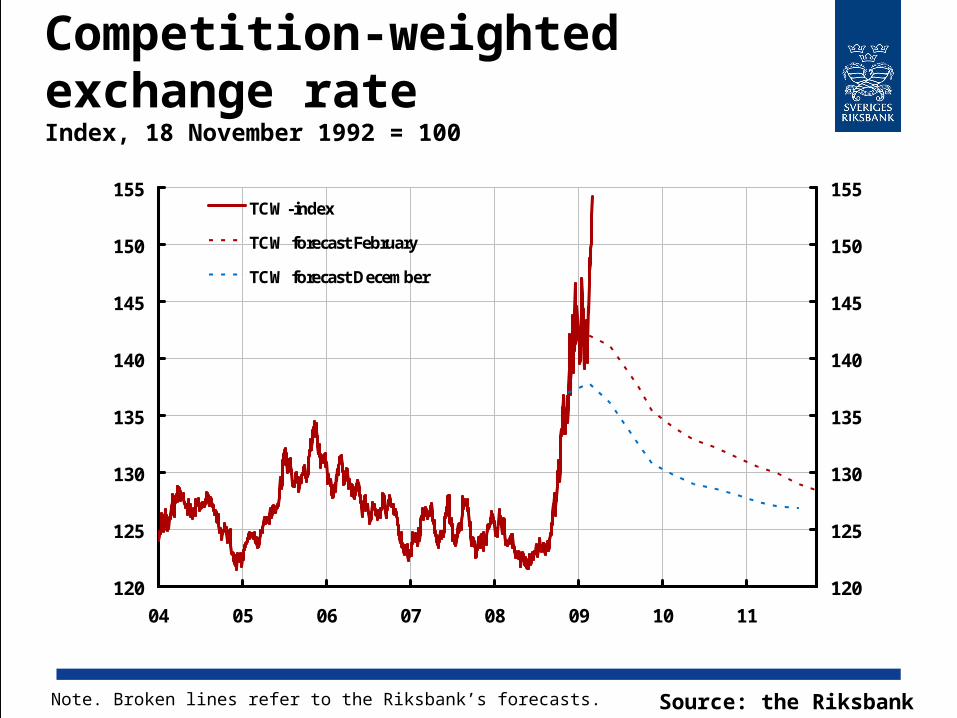

Competition-weighted exchange rateIndex, 18 November 1992 = 100

Source: the RiksbankNote. Broken lines refer to the Riksbank’s forecasts.

120

125

130

135

140

145

150

155

04 05 06 07 08 09 10 11

120

125

130

135

140

145

150

155TCW-index

TCW forecast February

TCW forecast December

Summary The financial turmoil worsened last autumn

and has developed into a global financial crisis.

International developments will be weak this year and there is a considerable risk that economic activity will be weak next year, too.

GDP growth in Sweden will be negative this year and inflation will fall.

The Riksbank has cut the interest rate to 1 per cent and may need to cut it further.