The CreditMetrics Package - Welcome to Rmetrics · PDF fileThe CreditMetrics package Provides...

35

Introduction Fundamentals Examples Summary and Outlook The CreditMetrics Package Andreas Wittmann Munich, Germany andreas_wittmann@gmx.de 1st R/Rmetrics User and Developer Workshop, July 10th, 2007 Thune, Switzerland 1 / 35

Transcript of The CreditMetrics Package - Welcome to Rmetrics · PDF fileThe CreditMetrics package Provides...

IntroductionFundamentals

ExamplesSummary and Outlook

The CreditMetrics Package

Andreas Wittmann

Munich, Germany

1st R/Rmetrics User and Developer Workshop,

July 10th, 2007

Thune, Switzerland

1 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Outline

1 IntroductionMotivationCredit Risk

2 FundamentalsCreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

3 ExamplesComputation of thresholdsCalculation of Credit SpreadComputation of CVaRHistogram

2 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

About Credit Risk and why is it important? (1)

Credit RiskRisk of loss that arises when a party defaults, i. e. does not payyou what he/she owes you (full amount and on time).

Reasons: bankruptcy / financial troubles / technicalproblem / legal reasons / refusalParties: corporate / bank / sovereign / public authority /single personDebts: interest and principal payments on bonds, loans,credit derivatives / cash-flows of derivatives / contract fees

DefaultA company defaults if the value of its Assets falls below acertain level, i. e. lower than its Liabilities.

3 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

About Credit Risk and why is it important? (2)

In general the main risk faced by a bank⇒ Typically 50% of the (economic) capital of a bankKey parameter of the margin taken by a bank when it lends.Hence, it is a key parameter of the market value of afinancial instrument.Thus, a change of the level of Credit (Default) Risk is alsoa Credit Risk.

4 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

Credit Value at Risk (CVaR) (1)

A measure of the losses caused on a portfolio byDefaults:

L̃ = Exposure At Default · Loss Given Default

Deterioration of credit quality⇒ This adds complexity

5 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

Credit Value at Risk (CVaR) (2)

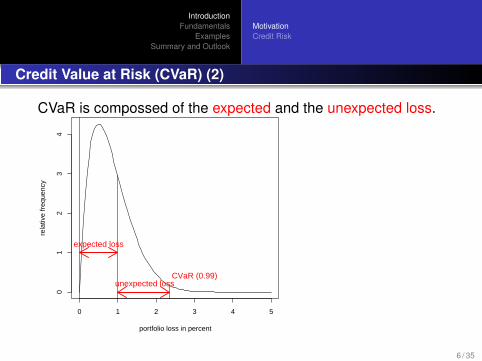

CVaR is compossed of the expected and the unexpected loss.

portfolio loss in percent

rela

tive

freq

uenc

y

0 1 2 3 4 5

01

23

4

expected loss

unexpected lossCVaR (0.99)

6 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

Credit Risk models

model background computation of loss distr.CreditMetrics option price theory monte carlo simulation

CreditPortfolioView macroeconomics monte carlo simulationCreditRisk+ actuary sciences analytical approximation

model input data model byCreditMetrics price of shares J.P. Morgan

CreditPortfolioView macroeconomical data McKinseyCreditRisk+ default rates Credit Suisse Group

7 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

The CreditMetrics package

Provides a collection of functions for calculating key datafrom the CreditMetrics Risk model.This model uses an one-year Migration Matrix.The Migration Matrix uses historical transition probabilitiesbetween rating classes.(A credit rating assesses the credit worthiness of anindividual, corporation, or even a country.)Feasible migrations at time t determine the value of acredit position.This can be calculated analytically, but this is extensivewith a high number of obligors.An approach which uses simulation is applied.

8 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

Main parameters for Credit Risk (1)

To compute the loss distribution the following informations arenecessary.

Probability of Default (PD): Is the probability that a loanwill not be repayed and fall into default.⇒What is my risk of loosing money?Exposure At Default (EAD): Can be seen as anestimation of the extent to which a bank may be exposedto a counterparty in the event of, and at the time of, thatcounterpartys default.⇒What is my amount at risk?

9 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

Main parameters for Credit Risk (2)

Loss Given Default (LGD): Is the fraction of EAD that willnot be recovered following default.⇒ If my counterparty defaults, how much am I going toloose?Credit Spread: Is the difference in yield between differentsecurities due to different credit quality.⇒What is the Market Value of my Credit Risk?

10 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

MotivationCredit Risk

Main parameters for Credit Risk (3)

Expected Loss (EL) can be calculated from the product ofthese quantities

EL = PD · EAD · LGD

Besides the expected loss also the loss distribution can becomputed.

11 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

CreditMetrics

Historical transition probabilities between rating classesprovide a basis.⇒ MigrationsThese are illustrated in a one-year Migration Matrix.Possible migrations up to time t determine the value of acredit position.This value can be calculated analytically.But with a high number of debitors this is very extensive.⇒ CorrelationsTherefore a simulation-based approach is used.

12 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Migration Matrix

Gives transition probabilities from initial rating (rows) intotarget rating (columns).Sum of rows has to be 1.Constructed with the basis of historical data.

Example of Migration Matrix (probabilities in percent)AAA AA A BBB BB B CCC D

AAA 90.81 8.33 0.68 0.06 0.12 0 0 0AA 0.70 90.65 7.79 0.64 0.06 0.14 0.02 0A 0.09 2.27 91.05 5.52 0.74 0.26 0.01 0.06BBB 0.02 0.33 5.95 85.93 5.30 1.17 1.12 0.18BB 0.03 0.14 0.67 7.73 80.53 8.84 1.00 1.06B 0.01 0.11 0.24 0.43 6.48 83.46 4.07 5.20CCC 0.21 0 0.22 1.30 2.38 11.24 64.86 19.79

13 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Simulation Approach

Idea: Company returns Vt are assumed to be standardnormal distributed Vt ∼ N(0,1) and simulated.Company value Vt at time t determines the rating at time t .Levels this off, the company remains in the same ratingclass.Migration thresholds (quantils) can be computed withtransition probabilities.

14 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

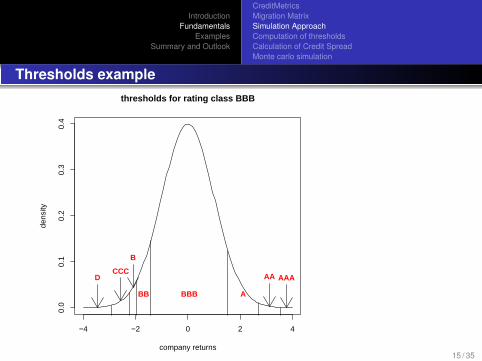

Thresholds example

−4 −2 0 2 4

0.0

0.1

0.2

0.3

0.4

thresholds for rating class BBB

company returns

dens

ity

DCCC

B

BB BBB A

AA AAA

15 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

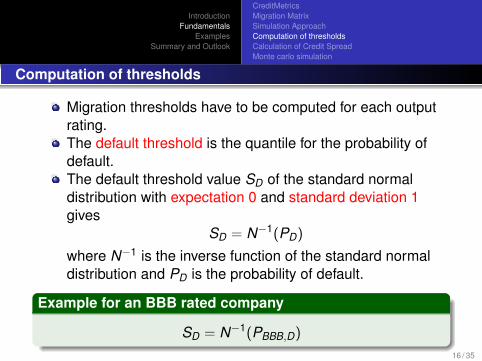

Computation of thresholds

Migration thresholds have to be computed for each outputrating.The default threshold is the quantile for the probability ofdefault.The default threshold value SD of the standard normaldistribution with expectation 0 and standard deviation 1gives

SD = N−1(PD)

where N−1 is the inverse function of the standard normaldistribution and PD is the probability of default.

Example for an BBB rated company

SD = N−1(PBBB,D)

16 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Threshold for migration to CCCis computed with

SD = N−1(PBBB,D + PBBB,CCC)

⇒ For each rating class thresholds can be computed

17 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Calculation of Credit Spread (1)

The Credit Spread is the risk premium demanded by themarket.According migration the nominal is differently calculated

V0 = Vte−(rt+CSt )t

where t is the time.Under a riskless probability measure the value of a creditposition at time t is computed as

V0 = E [Vt ]e−rt t .

The default event is bernoulli distributed, so the expectedvalue is

E [Vt ] = Vt(1− PDt) + Vt(1− LGD)PDt .

18 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

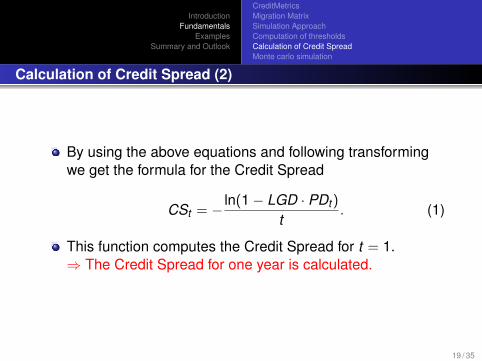

Calculation of Credit Spread (2)

By using the above equations and following transformingwe get the formula for the Credit Spread

CSt = − ln(1− LGD · PDt)

t. (1)

This function computes the Credit Spread for t = 1.⇒ The Credit Spread for one year is calculated.

19 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Monte carlo simulation

The company yield is assumed to be standard normaldistributed.Depending on Vt the company is located in a differentrating classThis location is performed with the Migration Matrix bydetermining the thresholds.In order to implement a valuation at time t , the CreditSpreads must be computed.With these the nominal is risk adjusted calculated.For a portfolio with many credits correlations are includedby simulating correlated company yield returns.⇒ Choleskey methodSo the simulated ratings for each firm at time t = 1 can becomputed.

20 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Antithetic Sampling

An amount of random numbers can be duplicated with thereflection method, here the calculating effort is low.

Relection method with normal distributionGiven a sequence of normal distributed random numbers(Z1, . . . ,Zn) with Zi ∼ N(0,1) for i = 1 : n.The reflected random numbers Z̃i can be computed with

Z̃i = (−1) · Zi .

The sequence

Z̃1 = −Z1, . . . , Z̃n = −Zn.

is therefore normal distributed also.21 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Correlations (1)

Returns are often more or less heavy correlated.How is it possible for Monte Carlo simulation to createcorrelated random numbers?.

IdeaGiven: Random vector Z ∼ N(0, I)Simple linear transformation X = µ+ AZ yields

X ∼ N(µ,AAT ).

If X should have the covarianz matrix Σ, then Σ = AAT

must be true.With Cholesky decomposition the matrix A can becomputed from Σ.

22 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Correlations (2)

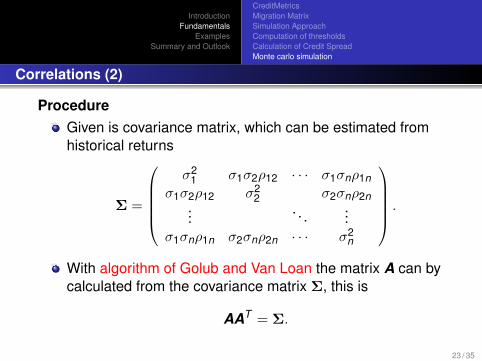

ProcedureGiven is covariance matrix, which can be estimated fromhistorical returns

Σ =

σ2

1 σ1σ2ρ12 · · · σ1σnρ1nσ1σ2ρ12 σ2

2 σ2σnρ2n...

. . ....

σ1σnρ1n σ2σnρ2n · · · σ2n

.

With algorithm of Golub and Van Loan the matrix A can bycalculated from the covariance matrix Σ, this is

AAT = Σ.

23 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Correlations (3)

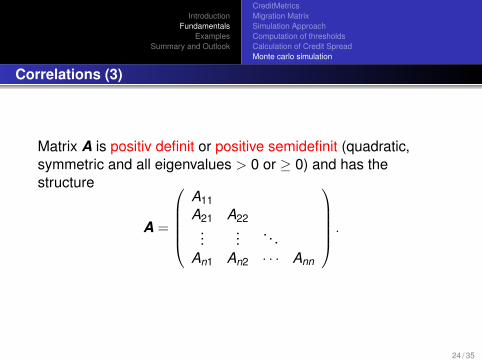

Matrix A is positiv definit or positive semidefinit (quadratic,symmetric and all eigenvalues > 0 or ≥ 0) and has thestructure

A =

A11A21 A22

......

. . .An1 An2 · · · Ann

.

24 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

CreditMetricsMigration MatrixSimulation ApproachComputation of thresholdsCalculation of Credit SpreadMonte carlo simulation

Correlations (4)

With matrix A correlated random numbers X = µ+ AZ can becomputed.

X1 = µ1 + A11Z1

X2 = µ2 + A21Z1 + A22Z2...

Xn = µn + An1Z1 + An2Z2 + · · ·+ AnnZn

where Z ∼ N(0, I) and X has the given covariance structure.

25 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Computation of thresholdsCalculation of Credit SpreadComputation of CVaRHistogram

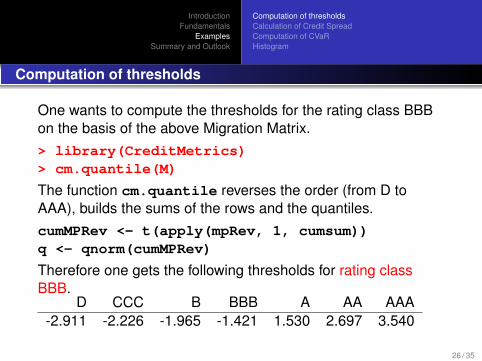

Computation of thresholds

One wants to compute the thresholds for the rating class BBBon the basis of the above Migration Matrix.> library(CreditMetrics)> cm.quantile(M)

The function cm.quantile reverses the order (from D toAAA), builds the sums of the rows and the quantiles.cumMPRev <- t(apply(mpRev, 1, cumsum))q <- qnorm(cumMPRev)

Therefore one gets the following thresholds for rating classBBB.

D CCC B BBB A AA AAA-2.911 -2.226 -1.965 -1.421 1.530 2.697 3.540

26 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Computation of thresholdsCalculation of Credit SpreadComputation of CVaRHistogram

Calculation of Credit Spread

One wants to compute the credits spreads for all rating classes,the LGD is assumed to be 45%.> library(CreditMetrics)> cm.cs(M, 0.45)

The function cm.cs uses equation (1).cs <- -(log(1 - lgd * pd))

Therefore one gets the following Credit Spreads for all ratingclasses.

AAA AA A BBB BB B CCC0.00005 0.00005 0.00027 0.00081 0.00478 0.02368 0.09327

27 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Computation of thresholdsCalculation of Credit SpreadComputation of CVaRHistogram

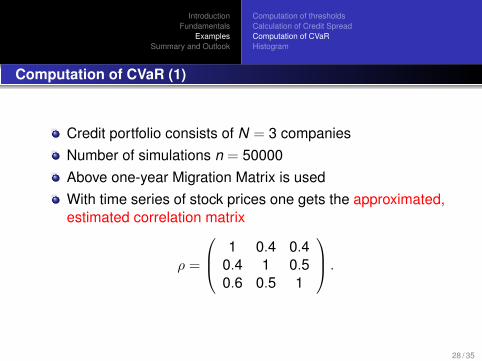

Computation of CVaR (1)

Credit portfolio consists of N = 3 companiesNumber of simulations n = 50000Above one-year Migration Matrix is usedWith time series of stock prices one gets the approximated,estimated correlation matrix

ρ =

1 0.4 0.40.4 1 0.50.6 0.5 1

.

28 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Computation of thresholdsCalculation of Credit SpreadComputation of CVaRHistogram

Computation of CVaR (2)

Riskless interest rate: r = 0.03Exposure At Default:ead = (4000000,1000000,10000000)

Loss Given Default: lgd = 0.45Companies have the rating = (BBB,AA,B)

Confidence level: α = 0.99

29 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Computation of thresholdsCalculation of Credit SpreadComputation of CVaRHistogram

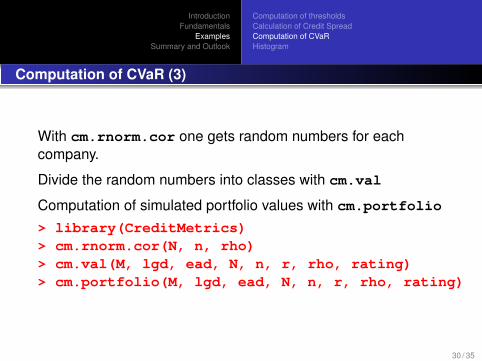

Computation of CVaR (3)

With cm.rnorm.cor one gets random numbers for eachcompany.

Divide the random numbers into classes with cm.val

Computation of simulated portfolio values with cm.portfolio

> library(CreditMetrics)> cm.rnorm.cor(N, n, rho)> cm.val(M, lgd, ead, N, n, r, rho, rating)> cm.portfolio(M, lgd, ead, N, n, r, rho, rating)

30 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Computation of thresholdsCalculation of Credit SpreadComputation of CVaRHistogram

Computation of CVaR (4)

Computation of simulated profits and losses with cm.gain

Computation of Credit Value at Risk with cm.CVaR

> cm.gain(M, lgd, ead, N, n, r, rho, rating)> cm.CVaR(M, lgd, ead, N, n, r, rho, alpha, rating)

1%4015408

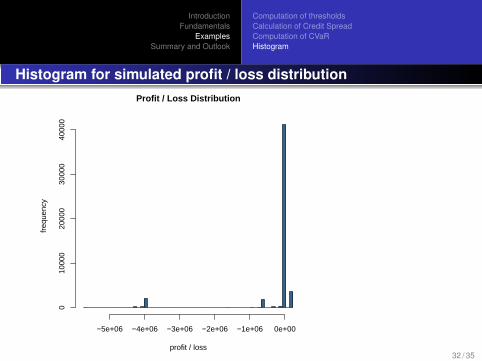

⇒ potential negative value change of credit portfolio, which willwith probability 0.99 not excess 4015408 in one year

31 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Computation of thresholdsCalculation of Credit SpreadComputation of CVaRHistogram

Histogram for simulated profit / loss distributionProfit / Loss Distribution

profit / loss

freq

uenc

y

−5e+06 −4e+06 −3e+06 −2e+06 −1e+06 0e+00

010

000

2000

030

000

4000

0

32 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Summary

Credit Risk is in general the main risk faced by a bank.CVaR is a measure of the losses caused on a portfolio.CreditMetrics is a Credit Risk model by J.P. Morgan anduses price of shares as input data.CreditMetrics package provides a collection of functions forcalculating key data from the CreditMetrics Risk model.One-year Migration Matrix uses historical transitionprobabilities.Feasible migrations at time t determine the value of acredit position.Analytical calculation is extensive with a high number ofobligors.A simlulation-based approach is applied.

33 / 35

IntroductionFundamentals

ExamplesSummary and Outlook

Outlook

A few bug fixes for the yet existing package have to bedone.At the present stage a company / debt can only belong toone country and one industry, e. g. german bankingsector.A two-factor FAMILLY model which incorporates manycountries and industries will be developed for the future.Different LGD’s for different companies in the portfolio isalso an extension for the next version.

34 / 35

Appendix

For Further Reading

Paul GlassermanMonte Carlo Methods in Financial Engineering.Springer, 2004.

Greg M. Gupton, Christopher C. Finger and Mickey BhatiaCreditMetricsTM– Technical DocumentJ.P. Morgan, 1997, www.riskmetrics.com

Nils Friewald and Manuel LingoCredit Risk – Numerical MethodsVienna University of Economics and BusinessAdministration, 2006

35 / 35