The Contributions of Savings and Loans on GDP … Contribution of Savings and... · depends on its...

140

The Contributions of Savings and Loans on GDP Growth: The Case of Indonesia Muhammad Fadli Hanafi 1 Berly Martawardaya, S.E., M.Sc. 2 Andi M. Alfian Parewangi, S.E., M.E. 3 Abstract The capital consists of savings, loans, FDI, and DDI and is important production factors. The contribution of savings and loans are estimated using panel regression and Generalized Method of Moment (GMM). The results show that savings and loans (investment, working capital, and consumption) have significant effect on economic growth with the respective negative and positive effects. Moreover, FDI, DDI, School Enrollment Rate, and Population Growth also play a significant role on growth with distinctive coefficient describing respective effects for each variable on growth. Furthermore, sector-specific analysis gives very dynamic effects on growth in the case of Indonesia. In order to identify long-run bidirectional relationship between variables, we employ Granger Causality Test using Vector Error Correction Model (VECM). As presents in the result and analysis, only loan for consumption performs causal relationship with GDP growth during the period. JEL Classifications : E21, O47, P42 Keywords: Savings, Loans, and Gross Domestic Product 1 Undergraduate student majoring finance at Department of Management, University of Indonesia; [email protected]. 2 Lecturer and Researcher at Faculty of Economics and Business, University of Indonesia 3 Lecturer and Researcher at Faculty of Economics and Business, University of Indonesia. Head of Research Department at Fundamental Asia (www.fundamental-asia.org)

-

Upload

nguyenduong -

Category

Documents

-

view

215 -

download

0

Transcript of The Contributions of Savings and Loans on GDP … Contribution of Savings and... · depends on its...

The Contributions of Savings and Loans on GDP

Growth: The Case of Indonesia

Muhammad Fadli Hanafi1

Berly Martawardaya, S.E., M.Sc.2

Andi M. Alfian Parewangi, S.E., M.E.3

Abstract

The capital consists of savings, loans, FDI, and DDI and is important production factors. The

contribution of savings and loans are estimated using panel regression and Generalized

Method of Moment (GMM). The results show that savings and loans (investment, working

capital, and consumption) have significant effect on economic growth with the respective

negative and positive effects. Moreover, FDI, DDI, School Enrollment Rate, and Population

Growth also play a significant role on growth with distinctive coefficient describing

respective effects for each variable on growth. Furthermore, sector-specific analysis gives

very dynamic effects on growth in the case of Indonesia. In order to identify long-run

bidirectional relationship between variables, we employ Granger Causality Test using Vector

Error Correction Model (VECM). As presents in the result and analysis, only loan for

consumption performs causal relationship with GDP growth during the period.

JEL Classifications : E21, O47, P42

Keywords: Savings, Loans, and Gross Domestic Product

1 Undergraduate student majoring finance at Department of Management, University of Indonesia;

[email protected]. 2 Lecturer and Researcher at Faculty of Economics and Business, University of Indonesia

3 Lecturer and Researcher at Faculty of Economics and Business, University of Indonesia. Head of Research

Department at Fundamental Asia (www.fundamental-asia.org)

2

3

CONTENT

1 INTRODUCTION ............................................................................................... 5

2 THEORY AND LITERATURES ....................................................................... 7

2.1. Saving and Loans ............................................................................................................. 7

2.2. The Role of Saving on Growth ...................................................................................... 12

2.3. Existing Literatures ........................................................................................................ 16

3 METHODOLOGY ............................................................................................ 22

3.1. Empirical Model ............................................................................................................. 22

3.2. Data ................................................................................................................................ 23

3.3. Panel Data Estimation .................................................................................................... 24

3.3.1. Alternative Specification ........................................................................................ 25

3.3.2. Determining the Best Model ................................................................................... 32

3.4. Parameter Estimation ..................................................................................................... 36

3.4.1. Ordinary Least Square ............................................................................................ 36

3.4.2. Maximum Likelihood ............................................................................................. 41

3.4.3. Generalized Method of Moment ............................................................................. 42

3.5. Model Validation............................................................................................................ 44

3.5.1. Adjusted R-Square .................................................................................................. 44

3.5.2. Marginal Cost of Information ................................................................................. 45

3.5.3. Correlogram ............................................................................................................ 47

3.5.4. Q-Statistics .............................................................................................................. 47

3.6. Diagnostic Analysis........................................................................................................ 48

3.6.1. Heteroscedasticity ................................................................................................... 48

3.6.2. Normality ................................................................................................................ 50

4

3.6.3. Serial Autocorrelation ............................................................................................. 51

3.6.4. Goodness of Fit ....................................................................................................... 52

3.6.5. Model Specification Error ....................................................................................... 53

3.6.6. Parameter Stability .................................................................................................. 54

4. EMPIRICAL FINDINGS .................................................................................. 54

4.1. Variance of Model Specification ..................................... Error! Bookmark not defined.

4.2. Discussions ...................................................................... Error! Bookmark not defined.

5. CONCLUSION ................................................................................................. 77

5

1 INTRODUCTION

Economic growth is the function of capital, human capital, and innovation of technology

(Solow and Swan, 2002). Capital itself is divided into foreign capital represented by Foreign

Direct Investment (FDI) and domestic capital represented by Domestic Direct Investment

(DDI), domestic savings, and domestic loans including loan for investment, loan for working

capital, and loan for consumption. Moreover, human capital and the innovation of technology

remain an important determinant of growth as well.

Banking sector, through its savings loan distribution, has played a very strategic role

in promoting better economic performance as indicated by higher Gross Domestic Product.

Jung (1986); and Levine, Loayza, and Beck (1999) revealed that in less developed countries,

financial development causes economic growth while, in developed countries, economic

growth causes financial development. Adequate national savings to support sufficient long

term funding in real economic activities is highly important to avoid insufficient investment

for, especially, social and physical infrastructure.

There have been numerous studies focusing on analyzing the role of savings and

loans on economic growth. The relationship between national savings and economic growth

is quantitatively strong and robust to different types of data and methodologies (Mankiw et

al. 1992, Attanasio et al. 2000, and Banerjee and Duflo. 2005) and is often taken as an

axiomatic in the development literature (Deaton, 1994). Many developing countries,

especially those characterized as the Third World including Indonesia, have claimed their

potential savings would be able to push the growth rate on real gross domestic production

(Liu and Guo, 2002). Lin (1992) expressed that economic development of a country highly

depends on its capability to mobilize their savings to raise the nation‟s productivity. Lean and

Song (2008) found that household savings and enterprise saving growth have played a

strategic role in promoting the growth. The high growth was led by the explosion of

household saving ratio that has reached a high level in the recent years (Modigliani and Cao,

2004).

6

It tends to occur in an open economy such as New Zealand promote higher growth

through its ability to access foreign saving to meet investment demands as well as

maintaining the level of domestic savings (Claus, Haugh, Scobie, and Tornquist, 2000).

However, strong financial system and public institution are required to optimize accumulated

capital, through savings, as it may idle or ineffectively used as reflected in Egypt (Hall and

Jones, 1999; Easterly and Levine, 2001). Dichotomy between domestic and foreign savings

is no longer necessary as many investment funded by foreign savings (Aghion, Comin,

Howitt, and Tecu, 2009). Al-Foul (2010) suggested that long-run relationship between

savings and national growth exist in Morocco while it surprisingly does not occur in Tunisia

employing real gross domestic product and real gross domestic savings 1965-2007 for

Morocco and 1961-2007 for Tunisia using a newly developed approach of cointegration of

Pesaran et al. (2001). Carroll and Weil (1994) found that high income growth appear to be

followed by periods of high savings

In another side, the focus on bank intermediary activities on loan distribution has

shown that it is related to the boom and bust of economic cycles. Schumpeter (1911) believed

that efficient allocation of savings through identification and funding of entrepreneurs (loans)

would stimulate more productivity and is subsequently supported by McKinnon (1973),

Shaw (1973), Fry (1988), and King and Levine (1993) by suggesting the above postulation

about the significance of banks to the performance of the economy. In the other cases,

Cappiello, Kadareja, Sorensen, and Protopapa (2010) found that the changes of credit supply

in euro area, both in terms of values and credit standards, have a positive and statistically

significant effect on GDP. Surprisingly, neither Driscoll (2004) nor Ashcraft (2006) found

compelling facts for causal relationship between credit supply and real output for the US

case. Other findings by Takats and Upper (2013) expressed that bank lending, to the private

sector, is essentially uncorrelated to economic performance after crises that were preceded by

credit booms.

There are couple hypothesis on how savings promote higher economic performance.

Growth of savings can stimulate economic growth through investment (Harrod, 1939;

Domer, 1946; and Solow, 2009). In some empirical studies, Alguacil et al (2004) and Singh

7

(2009), strongly supported the hypothesis among others. Long term funding such as loan

through high saving could supply high investment as a major contributor to GDP (Carroll et

al., 2000; Makin, 2006). Otherwise, the second hypothesis stated that economic growth

promote higher savings rate as supported by, among others, Sinha and Sinha (1998), Saltz

(1999), Agrawal (2001), Anoruo and Ahmad (2001), and Narayan and Narayan (2006).

Previously, Baumol, Blackman, and Wolfe (1991), Deaton and Paxson (1992), and Bosworth

(1993) suggested that higher growth rate would stimulate higher savings in the long-term.

Meanwhile, Demetriades and Adrianova (2004) expressed that when real economy grows;

there will be more savings that allow extending new loans. It has been emphasized by Shan

and Jianhong (2006) focusing on China economy where they found two-way causality

between finance and growth that confirmed previous findings by Demetriades and Hussein

(1996) who observed 13 different countries. Thus, this paper employs bidirectional

relationship between savings, loans, and GDP using Granger Causality Test.

Up to 2012, only few researches examining the relationship between savings and

loans by sector. Thus, the paper will completely examine the inter-sector linkages based on

the nine sector of economic activities. According to the above findings, this paper tries to

examine the role of savings and loans of Gross Domestic Products of Indonesia employing

quarterly observation on separated real economic activities base from 1988 to 2012.

2 THEORY AND LITERATURES

2.1. Saving and Loans

Intermediation activities through savings and loans have been strategic activities of banks to

promote better economic performance of a state. The focus of the impact of savings on

economy has been a primary concern throughout many economic literatures. Sturm (1981)

explained there are some motives of, especially, household savings such as saving for

retirement, precautionary saving, and saving for bequest. Saving is a key macroeconomic

variable, as it potential source of investment and thus economic growth. It also plays a role in

the monetary transmission mechanism (Beckmann, Hake, and Urvova, 2012). Savings can be

mathematically expressed by the following equation:

8

Eq. 1

where S is savings, Y is total income, and C is total household consumption expenditure.

From the above equation, primary determinants of saving are income and consumption.

Furthermore, the change of savings due to the change of income is explained in marginal

propensity to save. It can be mathematically explained as follow

Eq. 2

where MPS is the marginal propensity to save, is the change of saving, and is the

change of income. Marginal propensity to save is the opposite of marginal propensity to

consume as mathematically defined as .

An important implication of marginal propensity to save is measurement of the

multiplier. A multiplier measures the magnified change in aggregate product i.e. the gross

domestic product, resulting from a change in an autonomous variable (for example,

government expenditure, investment expenditures, etc.). The effect of a change in production

creates a multiplied impact because it creates income which further creates consumption.

However, the resulting consumption is also an expenditure which thus, generates more

income, which creates more consumption. This next round of consumption leads to a further

change in production, which generates even more income, and which induces even more

consumption. And thus, as it goes on and on, it results in a magnified, multiplied change in

aggregate production initially triggered by a change in autonomous variable, but amplified by

the creation of more income and increase in consumption.

By accounting identity, the national saving ratio equals the weighted average of the

saving ratio in the three principle subsectors of the economy; private households, business,

and general government (spending and fiscal policy). A comprehensive study of the national

saving ratios as well as sectoral income shares. The economic model of national saving is

started by assuming simple economic model with closed economy there are three uses for

9

GDP, (the goods and services it produces in a year). If Y is national income (GDP), then the

three uses of C consumption, I investment, and G government purchases can be expressed as:

Eq. 3

National savings can be thought of as the amount of remaining money that is not

consumed, or spent by government. In a simple model of a closed economy, anything that is

not spent is assumed to be invested:

Eq. 4

is disposable income. less consumption is the private savings.

National savings should be split into private savings and public savings. A new term, T is

taxes paid by consumers that goes directly to the government as shown here:

( ) ( )

Eq. 5

( ) is disposable income. ( ) less consumption ( ) is private savings. The term

( ) is government revenue though taxes minus government expenditures which is

public savings, also known as the Budget surplus.

( )

Eq. 6

The interest rate plays the important role of creating equilibrium between saving and

investment. In an open economy, the model can be described as follow:

Eq. 7

10

( )

Eq. 8

( ) - Domestic demand

Eq. 9

= National accounts identity

Eq. 10

Let , where is disposable income, Y is income, Tr is transfer, and

T is Tax. As is the accumulation of consumption and saving, thus,

Eq. 11

Eq. 12

( )

Eq. 13

( )

Eq. 14

, is the portion of national savings not used to financed domestic investment as it

has to anticipated for the Twin Deficit matters. By assuming no increase in savings,

investment needs to be decreased as deficit increases, and it really threatens economic

performance in the long-run. Thus, the role of saving is highly crucial and very strategic.

Besides, the contribution of bank lending or frequently called as bank credit has been

one of the major concern on macroeconomic literatures as well. Hahn (1920) on his

Economic Theory of Bank Credit concerned with the effects of credit criterion and credit

11

extension on production. From the beginning, he believed that bank credit has the importance

of a stimulus of the conjuncture. In an advance economy with highly developed credit

institutions, which can grant loans in excess of the amount of savings deposited, the money

supply is completely elastic being “more and more inclined to accommodate itself to the

level of demand. In such an organized credit economy stability of the price level requires

equality between the natural (equilibrium) rate and the money rate of interest, i.e. the rate of

interest charged on loans. Discrepancies between the two rates lead to cumulative process.

The financing of production is essentially performed by the creation and destruction

of credit. Schumpeter shares Wicksell‟s view that the disturbance of economic equilibrium

primarily emerges from an enlargement of profitable investment options due to technical

progress rather than by an artificial lowering of the money rate of interest by the banks which

thereby causes a period of expansion which is unsustainable. Hahn (1920) concluded that

every expansion of credit results in an expansion of goods because of a change in its

distribution. Credit takes the goods out of nothing where they would have remained without

credit expansion. He suggested that expansion of credit means nothing else than an increase

of demand for goods leading to an expansion of production since, as Hahn implicitly assumes

to be the case, unemployed resources are available. Hahn (1920) emphasizes, as later

Keynes, the deflationary consequences of voluntary savings and the positive effects of an

expansionary credit policy for innovations and employment. Afterwards, Hahn (1920) began

his research of the influence of credit on capital, the core and most revolutionary part of

Economic Theory of Bank Credit with the dictum “Capital formation is not the result of

saving but of the granting of credit.” He suggested that credit constitutes the conditio sine

qua non4 of the production of commodities and all capital formation in a modern economy.

His insights are subsequently summarized in the following ideas. The first is the

limits to inflationary credit expansion in the long run. The second is that a consequence of

4 Condition sine qua non literally means an indispensable or essential ingredient or condition, without which

something could not have happened or existed. There are a number of situations when the phrase "conditio sine

qua non" applies. Anytime something would not have happened unless something else happened first, the

predicating event is said to be conditio sine qua non. (http://www.wisegeek.com/what-does-conditio-sine-qua-

non-mean.htm). Ladislaus von Bortkiewicz has aptly summarized Hahn‟s (1920) main thesis in the statement,

“Am Anfang war die Schuld” or “In the beginning was the debt”

12

the autonomous credit creation power of banks which makes possible the conjunctures, an

“economic theory of bank credit” must be formulated as a business-cycle theory. The third is

that Credit expansions may help to overcome depressions, but they should never be used in

boom periods to perpetuate them or to make bearable structural maladjustments, particularly

excessive wages. “A timely stabilization of the conjuncture, not their stimulation on and on

by inflation is desirable.” And the last is a failure in the limit of credit expansion results in

progressive inflation and a possible ruin of state finances.

According to Hahn the activity of banks consists in functioning as guarantors, i.e. to

procure trust for debtors. Money and credit markets therefore are nothing else than markets

on which credit in the literal sense of trust is traded. Credit expansion does not only affect

distribution but also production. Inflationary credit expansion leads to an increase in overall

demand which on its part stimulates the production of goods. Hahn considers the economic

“organism” as “elastic” so that hitherto underutilized resources could be activated.

Nevertheless, Schumpeter (1931), in a remarkable contrast to Hahn the credit system does

not play the role of an active producer of business cycles but rather a passive role.

2.2. The Role of Saving on Growth

Determinant of economic growth have been a great ever-lasting debate among economists

from the modern down of the profession (Noy and Nualsri, 2007). Robert Solow‟s (1956)

model has been widely used as a theoretical framework for understanding cross-country

growth patterns (McQuinn and Whelan, 2006). The model has two key points, where the first

assuming that the economy can be classified with a neoclassical aggregate production with

exogenous technological dynamics. Thus, we adopt the model with a Cobb-Douglas

aggregate production function as follow:

( )

Eq. 15

13

Where is aggregate output, is capital, is the number of labors, and is exogenous

labor-augmenting technological changes. The second key point assumes the capital stock

accumulates according to the following equation:

Eq. 16

Where s is investment share of output also assumed to be exogenous. The properties of this

model can perhaps be better understood by using a reformulated version of the production

function derived as follows:

Eq. 17

Where output per worker can be expressed as

( )

Eq. 18

This is the decomposition of output per worker into technology and capital-output

components referred to the introduction. If we denote the growth rates of technology and the

number of workers as g and n respectively, then one can easily combine the separate

dynamics for output and capital to obtain the dynamics of the capital-output ratio as:

( )

Eq. 19

where

14

( )( )

Eq. 20

and

( )

Eq. 21

These results provide a simple analytical formulation of the Solow model‟s long-run

predictions as well as its shorter-run dynamics. The capital-output ration tends to coverage

over time at rate to an equilibrium level that is a function of the investment s, the growth

rate of technology g, the growth in the number of workers n and the depreciation rate . Once

the economy has reached this value for the capital-output ratio, output per worker then grows

at the rate g given by the rate of labor augmenting technological progress.

That the equilibrium level of the capital-output ratio is independent of the level of

is a key advantage of equation (4) as a decomposition of the determinants of growth. In

contrast, the more familiar decomposition of output per worker into technology and capital-

per-worker terms suffers from disadvantage that capital-per-worker depends positively on

in the long-run, making it more difficult to disentangle the long-run effects of technology and

non-technology factors.

To understand the link between capital-output dynamics and output per worker

dynamics, it is useful to note that the log of capital-output ratio can also be approximated as

displaying a simple convergence property. In other words, letting be the log of this ratio,

then

(

) ( )

Eq. 22

15

This result allows for a simple characterization of the dynamics of output per worker.

Again letting lower case letters represent logged variables, we can take logs of equation (4)

to get

( )

Eq. 23

The steady-state path for output per worker is defined as the level of output per

worker consistent with the capital-output ratio being at its equilibrium level:

( )

Eq. 24

Using equation (8), output per worker dynamics can be expressed as

( )

Eq. 25

Thus, the convergence speed, , of the capital-output ratio is also the so-called

conditional convergence speed of output-per-worker. In other words, this is the speed at

which output-per-worker closes has two components to it: Growth is determined by

technological progress as well as the gap between and . In contrast, movements in the

capital-output ratio are determined only by the gap between output and its steady state level.

16

Figure 1 Solow Growth Model and Population Growth Rate Change

Source: Wikipedia Exogenous Growth Model5

2.3. Existing Literatures

Determinant of GDP has been widely discussed through many existing literatures, including

the contribution of savings and loan on GDP. Aghion, Comin, and Howitt (2009) believe that

savings, especially domestic, really a matter for innovation and therefore growth as it enables

the local entrepreneur who is familiar with local conditions. A cross-country regressions

show that lagged is positively related to productivity growth in poor countries but not in rich

countries. They develop a theory that of endogenous local saving and growth in an open

economy with domestic and foreign investor. They explained that growth in relatively poor

countries results mainly from innovations that allow local sectors to catch up with the current

frontier technology. However, catching up with the frontier in any sector requires the

cooperation of foreign investors who is familiar with the frontier technology and a domestic

entrepreneur who is familiar with the local conditions to which technology must be adapted.

In such country, domestic saving matters for technology adoption, and therefore growth as it

allows the local entrepreneur to take an equity stake in this cooperative venture, which

mitigates an agency that would otherwise discourage the foreign investors from participating.

The dependent variable is a measure of growth of productivity (TFP) while independent

5 http://chula.livocity.com/econ/Macro%20Charit%20-

%20Paitoon/Charit%20too/Exogenous_growth_model.htm accessed Wednesday, 11 December 2013, 14.31

17

variable of interest is the average saving rate in ten-year period using OLS estimation

technique.

Al Foul (2010) conducted an analysis on causal long-run relationship between

savings and economic growth from MENA countries. The research observed two countries,

Morocco (1965-2007) and Tunisa (1961-2007) using a newly developed approach to

cointegration namely Autoregressive Distributed Lag (ARDL) considering each variable as a

dependent variable by Pesaran et al. (2001) that performs well with small samples and

regardless of the orders of the respective time series (i.e., whether time series are I(0), I(1), or

I(0)/I(1). The results showed that the long-run relationship exist between variables in the case

of Morocco, while it was not proven in Tunisia. By employing Granger causality test, Al

Foul (2010) found bidirectional relationship in Morocco while in the case of Tunisia, the

results suggest that there is unidirectional ganger causality between real GDP and real Gross

Domestic Savings and runs from saving growth to economic growth.

Caroll and Weil (1994) examine the relationship between income growth and saving

using both cross-country and household data. They examined the panel of non-overlapping

five year averages of saving and growth. They used model of consumption with habit

formation as standard permanent income models cannot explain these findings. They, firstly,

found that growth causes savings while savings do not lead growth. Secondly, those

household who expect faster income growth appear to save more than households who

should expect slower income growth.

Saltz (1999) investigates the long-run relationship between saving and economic

growth in 17 developing countries. He identified the existing bidirectional relationship

between variables among the countries. He found 4 countries have causal relationship from

saving to the real GDP while 10 countries have the reverse causal relationship from

economic growth to saving.

Claus, Haugh, Scobie, and Tornquist (2002) investigate the link between savings,

investment, and growth in New Zealand. In an open economy, total saving comprises saving

by domestic agents (government, firms, and households) plus foreign saving. Diversified

18

portfolios, large inflows of foreign investment into New Zealand and investment rates

comparable to those in OECD countries suggest that New Zealand has been able to access

foreign saving to meet investment demands. For this case, they employed net national

savings, total gross capital formation (investment), the current account, and real GDP growth

for 12 selected OECD countries from 1972-2001. For the New Zealand experience, they

applied the variables used to compare with OECD countries except investment employing

OLS estimation technique. They found that savings a positive and significant long-run

relationship to GDP growth while applying Granger causality test, they found that savings

and growth have a bidirectional relationship. Nevertheless, higher income led to the decrease

of savings as household preferred to increase their consumption (thus lowering savings (in

anticipation of higher output growth in the future.

The research work by Swiston (2008) on the USA used a VAR containing two lags to

construct a model with variables such as nominal interest rate, yield on investment grade

corporate bonds with remaining maturity of 5-10 years to capture long term interest rate, real

GDP, oil prices, equity returns and real effective exchange rate made positive contribution in

that direction. He posited that credit availability proxied by survey results on lending

standards is an important driver of the business cycle, accounting for over 20% of the typical

contribution of financial factors to growth. A net tightening in lending standards of 20%

basis points reduces economic activity by ¾% after one year and 1¼% after two years.

Hevia and Loayza (2011) investigated long-run relationship between savings and loan

in Egypt. They focused on illustrating the mechanism linking national saving and economic

growth, with the purpose of understanding the possibilities and limits of saving-based growth

agenda in the context of the Egyptian economy. They conducted complementary simulations,

firstly, the one designed to measure the savings rates required to finance a given rate of

economic growth set to 4% of GDP growth per worker. In that case, investment need to

increase by 37% of GDP as the marginal return to capital decreases, thus national savings

need to increase by, first 35% of GDP, then 50% in 10 years, and almost 80% by the end of

25-year period to promote economic growth. Secondly, what economic growth rates can be

financed if the saving rate is fixed at a given rate, set to 20% of national saving to GDP. They

19

found that the growth rate of GDP per worker will start at 0.8%, and then decrease gradually

to 0.7% in 25 years as explained by diminishing returns to capital which is constant rate in

this simulation. The simulation has proven that higher national savings would lead

remarkable growth performance, as occurred in China.

In the case of the long-run relationship between savings and growth in China, Lean

and Song (2008) conducted the investigation in four representative provinces, i.e. Beijing,

Shanghai, Guizhou, and Xinjiang covering the period from 1955 to 2004. By applying

Johansen-Juselius (1990) cointegration test, they found that China;s economy seems to be

contegrated with household savings and enterprise savings. By applying granger causality

test based on Vector Error Correction Model (VECM), household savings and economic

growth performed bidirectional relationship in the short-run while in the long run,

unidirectional causality exist from economic growth to the enterprise saving growth all

samples.

Loans or credit distributions also become the main concern in the paper. Cappiello,

Kadareja, Saensen, and Patropapa (2010) examined whether bank loans and credit standard

have an effect on output focusing on the Euro area such as Austria, Belgium, Greece, Ireland,

Italy, Netherland, Portugal, and Spain. They employ quarterly data from 1999 to 2008 for

nominal GDP, real GDP, GDP deflator, money (M3 less currency and M2 minus currency

and time deposit). In contrast to the US findings, changes in the supply of credit, both in

terms of volumes and credit standards applied on loans to enterprises, have significant effects

on real economic activities by applying OLS panel regressions.

Interestingly, other findings have been observed in Nigerian case by Oluitan (2010).

He used bivariate model as proposed by Ghirmay (2004) on his research in 16 Sub-Saharan

Africa countries and multivariate model proposed by Tang (2003) on his research about bank

lending and economic growth in Malaysia. He examined the relationship by applying

cointegration test and direction of causality using Error Correction Method (ECM) and OLS

estimation technique. The following variables are real GDP, real private sector credit, real

total export, GDP Per Capita, Ratio of Bank Deposit to GDP, and Private Sector Deposit to

GDP. He found that the autoregressive coefficient for the real private sector credit growth

20

was negative, large, and significant in all the results, but the first model that tested the

bivariate relationship between credit and real output showed a positive coefficient. It implies

that the relationship among all these variables is weak.

Nevertheless, a discussion on gross domestic cannot be separated from other

determinants. Economists have found that Foreign Direct Investment (FDI), Domestic Direct

Investment (DDI), Human Capital, Inflation, Trade Openness, and Population are the

frequent determinants in many economic literatures. Alfaro (2003) examined the link

between FDI and Economic Growth. He found that FDI contributes various relationships on

growth in primary, manufacturing, and service sectors. He uses an empirical analysis using

cross-country data from different regions (e.g. Asia and the Pacific, Africa, Latin America,

and the Caribbean) for the period 1981-1999 and found a positive relationship between FDI

and growth mainly in manufacturing sector while it tends to be ambiguous as primary sectors

perform negative relationship. As confirmed by Anwar and Nguyen (2010) focusing on

Vietnam case, the relationship FDI on growth tends to be positive and significant. Moreover,

the effect would be higher if the investment is addressed, mainly, to education and training to

improve the local qualification and generate more output in the long-run. The role of

education (or in general, of the formation of human capital) in the growth process has been

extensively analyzed in the theory literature (Nelson and Phelps, 1996; Welch, 1970; Lucas,

1988; Azariadis and Drazen, 1990; and Romer, 1990; among others).

Seren (2001) examined how human capital affects growth estimating pooled data for

different samples of countries during the period 1960-1990 divided into five-year intervals.

She observed using the following data, income, population, labor force, and investment rates.

She found various significance and positive relationship between human capital and growth.

Meanwhile, inflation rate and trade openness is also a primary concern in economic growth.

Betyak (2012) examined some determinants of economic growth in, especially, crisis

countries in European Union. Using least square panel regression analysis, he found that

inflation rate has a positive relationship in the case of Portugal, Italy, Ireland, and Spain.

Interestingly, the relationship is negative in the case of Greece. Meanwhile, trade openness

21

has been positively related to GDP growth in Portugal, Italy, and Spain while Greece seems

to be negative.

Besides, the analysis of determinant of GDP based on economic activities-based

sector also becomes the primary concern to generate accurate selected contributions on GDP.

Burgess (2011) measured financial sector output and its contribution to UK GDP. By

observing some financial service industries such as monetary intermediation, insurance

companies, pension funds, and activities auxiliary to financial intermediation, he found

insignificant relationship between financial output sectors on GDP.

Furthermore, Diao, Hazell, Resnick, and Thurlow (2007) investigated the role of

agriculture in development focusing on the implications for Sub-Saharan Africa. By

examining different typology of agricultural conditions, natural resources, and geographic

location, they found that growth potential and poverty reduction potential of agriculture

varies substantially across continents. They found that agriculture growth is till important for

most-low African countries. As stated in the previous research, Vodel (1994) observed

different 27 countries in terms of agriculture contribution in growth. Using social accounting

matrixes, he found that significant relationship appeared in the early stages, while the

forward linkages are much weaker.

Moreover, Arcand (2000) shows that the link between nutrition (agriculture product)

and economic growth is robust to the use of different data sets and different econometric

techniques, ranging from OLS to GMM. Using three different cross-county data sets, he

found that nutrition affects growth directly, through labor productivity, and indirectly,

through improvements of life expectancy.

Anyanwu, Offor, Adesope, and Ibekwe (2013) observed the relationship between

GDP and agriculture, industry, building and construction, wholesale and retail, and trade and

services share of GDP. By employing multiple regression, they found that agriculture had

been dominant since 1960 to 1989 while industry contributed more on GDP started from

1990 to 2008. Building and construction remained to contribute least to GDP throughout the

22

period of observation. However, some significant determinants on GDP were agriculture,

industry, wholesale and retail trade, and service sectors.

Strategic Finance Group (2007) on economic frontier analyzed the association

between unexpected changes in electricity volume and GDP growth for residential

customers. They employ several data such as real GDP, electricity price, and gas prices. They

apply Vector Error-Correction Model (VECM) to describe the long-run and the short-rum

relationship between the two time-series employed. Using simple linear regression

estimation, GDO growth and growth in electricity volumes suggest that the elasticity of

volume growth to GDP may be significantly less than one (few changes on volume leads

huge changes in GDP growth).

Based on theoretical grounds and literatures study we build empirical model to

estimate on this paper. The specification of proposed model and its variants will be discussed

on the next session of this paper.

3 METHODOLOGY

3.1. Empirical Model

The paper investigates the long-run relationship among savings and loans on gross domestic

product of Indonesia from 1988 to 2012. It is considered important to observe bidirectional

relationship between savings, loans, and gross domestic product of Indonesia. Granger

causality test is also employed to identify long-run bidirectional relationship between

savings, loans, and gross domestic product of Indonesia.

The paper employs three independent variables while six others are determined as the

controlling variables. Interestingly, the paper uses both panel and time series to analyze the

long-run relationship between desired independent variables and Indonesia‟s output. As loans

for investment and working capital are detailed by its cross-sections, thus it will be analyzed

using panel approach in order to provide more accurate output (Greene, 2010) with the

following model:

23

Eq. 26

Where is Gross Domestic Product, is a set of dependent variables (loan for

investment and working capital), is a set of control variables such as FDI, DDI, and labor

by sector, and is the error term.

As savings and loan for consumption are not detailed by sector of real economic

activities, they will be analyzed using the following time series model.

Eq. 27

Where is Gross Domestic Product, is a set of dependent variables (loan for investment,

working capital, consumption, and savings), is a set of control variables such as FDI,

DDI, years of schooling and labor by sector, and is the error term.

3.2. Data

Referring to Solow Model, the following variables have been determined accordingly, and

based on the frequent previous literatures. The theory included capital proxied by FDI, DDI,

Savings and Loans while human capital aspects are proxied by labor-based nine economic

activities, school participation rate, and years of schooling. Meanwhile, as stated in the

frequently previous literatures, trade openness, inflation, and population are added to the

model.

24

Table 1. Variable and Data

Variables Names Units Sources

Dependent GPD/Labor Nominal Bank Indonesia

Independents Savings Billion Rp Bank Indonesia

Loan for Investment Billion Rp Bank Indonesia

Loan for Working Capital Billion Rp Bank Indonesia

Loan for Consumption Billion Rp Bank Indonesia

Controls FDI Billion Rp Investment Coordination Board

DDI Billion Rp Investment Coordination Board

School Participation Rate Percentage (%) National Bureau of Statistics

Population Growth Percentage (%) Index Mundi

The following variables are estimated using panel approach. As saving and loan for

consumption is not detailed by sector-based real economic activities, thus we also employ

time series approach. Time series as being utilized in the model, is a set of data that is

collected sequentially in time (Reinert, 2010).

3.3. Panel Data Estimation

Panel data is a data sets consisting of multiple observations on each sampling unit (Baltagi,

2006). Panel data are a type of longitudinal data (Hsiao 2003). In other words, we can further

explain that data panel contains two or more observations on many units. Data panel has been

very popular in many research on social and behavior field. It is repeated measures of one or

more variables on one more persons-repeated cross-sectional time series (Bruderl, 2005).

Compared to the other two types of data (time series and cross section), data panel has

several benefits like being able to control the heterogeneity of individual, providing complete

25

data with low level of colinearity and higher degree of freedom, appropriate to examine

dynamics of adjustments, more reliable to identify and measure both individual and time

effect that cannot be solved by time series and cross section data, and appropriate to build

and test a model with complex behavior. A panel data set also allows us to control for

unobserved cross section heterogeneity (Wooldridge, 2001)

Hurlin (2010) described the terminology and notations are explained by through

individual or cross section unit that could be country, region, state, form, consumer,

individual, couple of individuals or countries (gravity model6) and also double index where

is cross-section unit and is the series of time.

where and are and vectors of exogenous variables. is constant, and

are and vectors of parameters. is over and , with ( ) . It is

noted that variables unobservable and correlated with (Baltagi and Kao, 2000)

3.3.1. Alternative Specification

As mentioned above, data panel is a combination between time series and cross section so

that data panel modeling involves the two characteristics of those two types of data. Data

panel basically involves more than one objects and observations (Winarno, 2009). According

to Nachrowi (2006) data panel regression model uses some of the following approaches.

3.3.1.1. Generalized Least Square

Generalized Least Square is introduced to improve upon estimation efficiency when var(y) is

not a scalar variance-covariance matrix (Fox, 2002). GLS is then becoming an alternative as

OLS is inefficient since disturbances are nonspherical7. A drawback of the GLS method is

that it is difficult to implement. In practice, certain structures (assumptions) must be imposed

6 In economics, gravity model is the standard of non-zero trade flows in macroeconomics

(http://arxiv.org/abs/1304.3252) 7 Spherical disturbance means the variance of error is equal to population variance

26

on ( ) so that a feasible GLS estimator can be computed8. This approach results in two

further difficulties, however. First, the postulated structures on var(y) need not be correctly

specified. Consequently, the resulting feasible GLS estimator may not be as efficient as one

would like. Second, the finite-sample properties of feasible GLS estimators are not easy to

establish. Consequently, exact tests based on the feasible GLS estimation results are not

readily available.

Often we have analysis situations where it is unreasonable to assume that our errors

are independent and identically distributed. Heteroskedasticity, that is unequal variances of

the error term, may be a problem. It is also common to have data where errors are correlated

(Winship, 2007)

In a typical linear regression model we observe data { }

on n statistical units. The response values are placed in a vector ( ), and the

predictor values are placed in the design matrix [ ], where is the value of the jth

predictor variable for the ith unit. The model assumes that the conditional mean of Y given X

is a linear function of X, whereas the conditional variance of the error term given X is a

known matrix Ω. This is usually written as

⌈( | )⌉ ⌈( | )⌉

Eq. 28

Here β is a vector of unknown “regression coefficients” that must be estimated from

the data.Suppose b is a candidate estimate for β. Then the residual vector for b will be

Y − Xb. Generalized least squares, which is two steps from Ordinary Least Squares, method

estimates β by minimizing the squared Mahalanobis9 length of this residual vector:

( ) ( )

Eq. 29

8 Generalized Least Square requires two following assumptions. The first is the covariance of error is diagonal,

and the second is the structure of error covariance of error is observable 9 Descriptive statistic that provides a relative measure of data point‟s distance (residual) from a common point.

27

Since the objective is a quadratic form in b, the estimator has an explicit formula:

( )

Eq. 30

The GLS estimator is unbiased, consistent, efficient, and asymptotically normal:

√ ( ) → ( ( ) )

Eq. 31

GLS is equivalent to applying ordinary least squares to a linearly transformed version

of the data. To see this, factor , for instance using the Cholesky decomposition. Then

if we multiply both sides of the equation by , we get an equivalent linear

model where , and . In this

model , - ( ) . Thus we can efficiently estimate β by applying OLS to

the transformed data, which requires minimizing:

( ) ( ) ( ) ( )

Eq. 32

This has the effect of standardizing the scale of the errors and “de-correlating” them.

Since OLS is applied to data with homoscedastic errors, the Gauss–Markov theorem10

applies, and therefore the GLS estimate is the best linear unbiased estimator for β. Or in other

words, it can be said to be essentially useful, through transformation, to change from

heteroscedastic to homoscedastic.

3.3.1.2. Fixed Effect Model

Fixed Effect Model is a statistical model that represents the observed quantities in terms of

explanatory variables that are treated as if the quantities were non-random (Peter, Patrick,

Yee, and Scott, 2002). This is in contrast to random effects models and mixed models in

10

Stating that a linear regression model has expected zero errors and are uncorrelated as well as having equal

variances.

28

which either all or some of the explanatory variables are treated as if they arise from random

causes. Contrast this to the biostatistics definitions, as biostatisticians use "fixed" and

"random" effects to respectively refer to the population-average and subject-specific effects

(and where the latter are generally assumed to be unknown, latent variables).

Fixed effect model can be mathematically explained as follow:

Eq. 33

where is the dependent variable observed for individual i at time k, is the time-variant

regressor matrix, is the observed time-invariant11

individual effect and is the error

term. Unlike , cannot be observed by the econometrician. Common examples for

time-invariant effects are innate ability for individuals or historical and institutional

factors for countries. The fixed effect model allows to be correlated with the regressors

matrix . Strict exogeneity, however, is still required.

Since is not observable, it cannot be directly controlled for. The Fixed Effect

model eliminates by demeaning the variables using the within transformation:

( ) ( ) ( )

Eq. 34

Where

∑

and

∑

. Since is constant, and hence the effect

is eliminated. The fixed effect estimator is then obtained by an OLS regression of on

. Another alternative to the within transformation is to add a dummy variable for each

individual i. This is numerically, but not computationally, equivalent to the fixed effect

model and only works if T, the number of time observations per individual, is much larger

than the number of individuals in the panel.

11

Time-variant individual means identifier specific characteristic of is fixed.

29

3.3.1.3. Random Effect Model

Random Effect Model is intended to differ between individual or period effect, so that

intercept of the equation is the average of the intercept of the overall observations (Peter,

Patrick, Yee, and Scott, 2002). In statistics, a random effect(s) model, also called a variance

components model, is a kind of hierarchical linear model. It assumes that the dataset being

analyzed consists of a hierarchy of different populations whose differences relate to that

hierarchy. In econometrics, random effects models are used in the analysis of hierarchical or

panel data when one assumes no fixed effects (i.e. no individual effects). The random effect

model can be mathematically expressed as follow

Eq. 35

where all variables are defined as above. At first glance this appears the same as equation

(general model), but there are differences. First, the random effects model assumes that the

effects of , and on do not change over time. This is why (not subscript)

replaces and replaces . Second, the random effects model assumes that is a

random latent variable that is uncorrelated with , , and . Considering the type of

unmeasured time-invariant variables that might appear in (e.g. intelligence, personality with

all other explanatory variables in the analysis. If this assumption or the assumption of the

same coefficients over time is incorrectly imposed, either can bias the estimated effects that

we find. Another assumption of the random effects model is that the error variance does not

change over time (

). Violation of this assumption can lead to inaccuracy of the

estimates (Bollend and Brand, 2008).

One common estimator of the coefficients and variances of the error and time-

invariant latent variable is the feasible Generalized Least Square (GLS) estimator (e.g. Hasio,

2003; and Woldridge, 2002). In this approach, an estimate of the variance of and of are

used to form the “weight matrix” for GLS estimation. If the preceding assumptions hold, then

this procedure has desirable large sample properties such as consistency, asymptotic

unbiasedness, and readily available significance tests. It also provides an estimate and test of

30

whether there are latent time-invariant variables ( ) such that zero variance of

implies their absence. A maximum likelihood estimator of the random effects model also is

possible under the assumption that and come from a normal distribution (Hsiao, 2003).

One or both of these estimators are available in statistical software such as SAS (e.g.

TSCSREG) or STATA (xtreg). However, the use of these procedures presupposes that the

assumptions of the random effect model hold, with the assumption that the latent time-

invariant variable is uncorrelated with all observed covariates being the most problematic

assumption. The fixed effect model removes this restriction.

Implicit in the summary-statistics of Random Effect Model approach is the two-level

model

Eq. 36

Eq. 37

where is the true mean effect for the subject , is the sample mean effect for subject

and is the true effect for the population.

The Summary-Statistic (SS) approach is of interest because it is computationally

much simpler to implement than the full random effects model of equation 1. This is because

it is based on the sample mean value, , rather than on all of the samples . This is

important for neuroimaging as in a typical functional imaging group study there can be

thousands of images, each containing tens of thousands of voxels. In the first level we

consider the variation of the sample mean for each subject around the true mean for each

subject. The corresponding variance is , -

, where

is the within-subject variance.

At the second level we consider the variation of the true subject means about the population

means where about the population mean where , - the between-subject variance.

We also have , - , - . Consequently,

31

Eq. 38

The population mean is then estimated as

∑

Eq. 39

This estimate has a mean [ ] and a variance given by

[ ] ,∑

-

[∑

] ,∑

-

Eq. 40

Thus, the variance of the estimate of the population mean contains contributions from

both the within-subject and between-subject variances. Importantly, both [ ]

and [ ] are identical to the maximum-likelihood estimates derived earlier. This

validates the summary-statistic approach lies in the fact that what is brought forward to the

second-level is a sample mean. It contains an element of within-subject variability which

when operated on at the second level produces just the right balance of within and between

subject variance.

32

3.3.2. Determining the Best Model

In panel analysis using Ordinary Least Square estimation technique, there are some following

statistical tests to determine the best model of an analysis such as Chow Test, LM test and

Hausman Test (Nachrowi, 2006) as follow:

3.3.2.1. Chow Test

The Chow test is a statistical and econometric test of whether the coefficients in two linear

regressions on different data sets are equal. The Chow test was invented by economist

Gregory Chow in 1960. In econometrics, the Chow test is most commonly used in time series

analysis to test for the presence of a structural break. In program evaluation, the Chow test is

often used to determine whether the independent variables have different impacts on different

subgroups of the population (Doughterty and Christoper, 2007).

The Chow Test can be mathematically explained as follow:

Eq. 41

and

Eq. 42

The null hypothesis of the Chow test asserts that , , and , there is

the assumption that the model errors are independent and identically distributed from a

normal distribution with unknown variance

Let be the sum of squared residuals from the combined data, be the sum of

squared residuals from the first group, and be the sum of squared residuals from the

second group. and are the number of observations in each group and k is the total

number of parameters. Then the Chow test statistics is:

33

Chow Stat ( ( )) ( )⁄

( ) ( )⁄

Eq. 43

The test statistic follows the F distribution with k and ( ) degrees of

freedom.Related to determine to use either Pooled Least Square of Fixed Effect Model

estimation, then reject the null hypothesis ( ) if the p-value is less than the

critical value.

3.3.2.2. LM Test

The Lagrange Multiplier (LM) test is a general principle for testing hypotheses about

parameters in a likelihood framework (Cook and Demets, 2007). The hypothesis under test is

expressed as one or more constraints on the values of parameters. To perform an LM test

only estimation of the parameters subject to the restrictions is required. This is in contrast

with Wald tests, which are based on unrestricted estimates, and likelihood ratio tests which

require both restricted and unrestricted estimates.

The name of the test is motivated by the fact that it can be regarded as testing whether

the Lagrange multipliers involved in enforcing the restrictions are significantly different from

zero. The term “Lagrange multiplier” itself is a wider mathematical word coined after the

work of the eighteenth century mathematician Joseph Louis Lagrange. The LM testing

principle has found wide applicability to many problems of interest in econometrics.

Moreover, the notion of testing the cost of imposing the restrictions, although originally

formulated in a likelihood framework, has been extended to other estimation environments,

including method of moments and robust estimation. Statistically, it can be explained as

follow:

Let ( ) be a log-likelihood function of a parameter vector , and let the score

function and the information matrix be

( )

34

Eq. 44

( ) , ( )

-

Let be the maximum likelihood estimator (MLE) of subject to an vwctor of

constraints ( ) . If we consider the Lagrangian function

( ) ( )

Eq. 45

where is an vector of Lagrange multipliers, the first-order conditions for are

( ) ( )

( )

Eq. 46

where ( ) ( )

The Lagrange Multiplier test statistic is given by

Eq. 47

where ( ), ( ), and ( ). The term is the score form of the statistic

is the Lagrange multiplier form of the statistic. They correspond to two different

interpretations of the same quantity.

35

The score function ( ) is exactly equal to zero when evaluated at the unrestricted MLE

of , but not when evaluated at ( ). If the constraints are true we would expect both and to

be small quantities, so that the region of rejection of the null hypothesis ( ) is

associated with large values of LM. Under suitable regularity conditions, the large-sample

distribution of the LM statistic converges to a chi-square distribution with degrees of

freedom, provided the constraints ( ) are satisfied. This result is used to determine

asymptotic rejection intervals and p-values for the test. Breusch Pagan Lagrange Multiplier

LM test is intended to determine the best model between Pooled Least Square (PLS) and

Random Effect Model (REM).

3.3.2.3. Hausman Test

Consider the linear model y = bX + e, where y is univariate and X is vector of regressors, b is

a vector of coefficients and e is the error term (Greene, 2008). We have two estimators for b:

b0 and b1. Under the null hypothesis, both of these estimators are consistent, but b1 is

efficient (has the smallest asymptotic variance), at least in the class of estimators containing

b0. Under the alternative hypothesis, b0 is consistent, whereas b1 isn‟t.

Then the Wu–Hausman statistic is

( ) ( ( ) ( ))

( )

Eq. 48

Where + denotes the Moore–Penrose pseudoinverse12

. This statistic has asymptotically the

chi-squared distribution with the number of degrees of freedom equal to the rank of matrix

Var(b0) − Var(b1). If we reject the null hypothesis, b1 is inconsistent. This test can be used to

check for the endogeneity of a variable (by comparing instrumental variable (IV) estimates to

ordinary least squares (OLS) estimates). It can also be used to check the validity of extra

instruments by comparing IV estimates using a full set of instruments Z to IV estimates that

use a proper subset of Z. Note that in order for the test to work in the latter case, we must be

12

Moore-Penrose Pseudoinverse is defined for any matrix and is unique. It brings great notational and

conceptual clarity to the study of solutions to arbitrary systems of linear equations and linear least squares

problems (Soderstorm, Torsten; Stewart, G.W. (1974)

36

certain of the validity of the subset of Z and that subset must have enough instruments to

identify the parameters of the equation. Hausman also showed that the covariance between an

efficient estimator and the difference of an efficient and inefficient estimator is zero.

Related to determine to choose either fixed effect or random effect through hausman

test. The null hypothesis states that is is uncorrelated with the variables in , then

random effects is the appropriate estimator, while if correlated with the variables in ,

then fixed effects is the appropriate estimator. The Hausman test can be statistically

explained by the following model:

[ - ], ( ) ( )- [ -

]

Eq. 49

3.4. Parameter Estimation

3.4.1. Ordinary Least Square

The least square method is widely used to find or estimate the numerical values of the

parameters to fit a function to a set of data and to characterize the statistical properties of

estimates. It exists with several variations (Abdi, 2003). Ordinary least square is a

generalized linear modeling technique that may be used to model a single response variable

which has been recorded on at least an interval scale. It can be applied to single or multiple

explanatory variables and also categories explanatory that have been appropriately coded. At

a very basic level, the relationship between a continuous response variable (Y) and a

continuous explanatory variable (X) may be represented using a line of best-fit. If this

relationship is linear, it may be appropriately represented mathematically using the straight

equation .

In addition to the model parameters and confidence intervals for , it is useful to laso

have an indication of how well the model fits the data. It can be determined by comparing the

observed the scores of Y (the values of Y predicted by the regression equation). The

37

difference between the two variables (the deviation, or residual as it is also called) provides

an indication of how well the model predicts each data point. The sum of all squared

residuals is known as the residual sum of squares (RSS) and provides a measure of model-fit

for an OLS regression model. A poorly fitting model will deviate markedly from the data and

will consequently have a relatively large RSS and vice versa (a perfectly fitting model will

have an RSS equal to zero, as there will be no deviation between observed and expected

values of Y).

It is important to understand how the RSS statistic (Hutchseson, 2011) operates as it

is used to determine the significance of individual and groups of variables in a regression

model. For a simple OLS regression model, the effect of the explanatory variable can be

assessed by comparing the RSS statistic for the full regression model with that

for the null model . The difference in deviance between the nested models can be tested

for significance using an F-test computed from the following equations:

( )(

)

Eq. 50

where p represents the null model, , p+q represents the model , and df are

the degrees of freedom associated with the designated model. It can be seen from equation

that the F-statistic is simply based on the difference in the deviances between the two models

as a fraction of the deviance of the full model, whilst taking account of the number of

parameters.

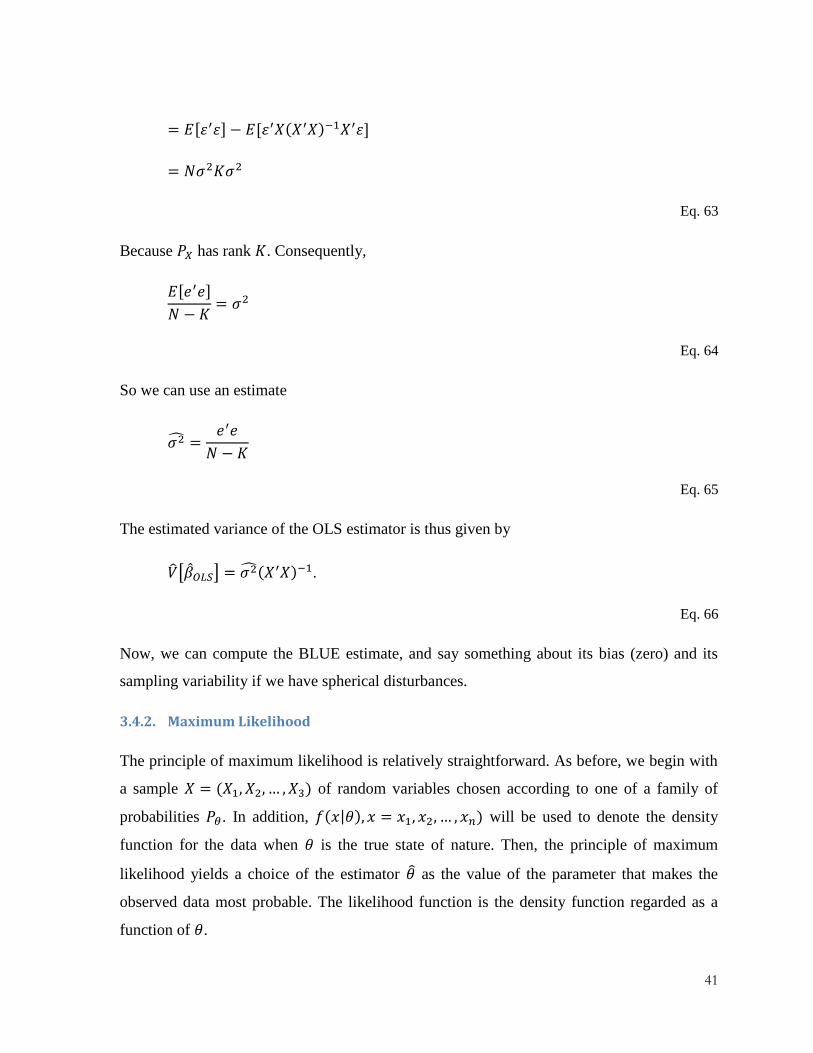

In order to explain the efficient Ordinary Least Square, we start by the following

equations:

Eq. 51

, -

38

Eq. 52

, -

Eq. 53

is full-rank and contains . In this case, OLS is BLUE. So we can get an estimated

parameter vector

( )

Eq. 54

Its bias is

[( ) ] ,( ) ( )

,( ) - ( )

Eq. 55

The variance of the estimated parameter vector is the expectation of the square of the

quality in square brackets:

[ ] ,( )( ) -

,( ) ( ) -

( ) , - ( )

( ) ( )

( ) ( )

( )

Eq. 56

39

Additionally, in order to get a precise estimate, we can assume [ ] ( )

in three pieces. The first is the variance of is the variance of conditional on . Less

variation of around the regression line yields greater precision. The second is is the

number of observations. It shows up, implicitly, inside . This is easiest to see if has just

one column: in the case, ( ) ∑ ( )

which for drawn from some density ( )

has an expectation that increases linearly with . So, [ ] goes inversely proportionally

with . The thord is is related to the covariance matrix the vectors . If

each column of is mean-zero, then is the covariance matrix of the columns of . For

this reason, if has a lot of variance, then is bigger, so ( ) is smaller, so [ ] is

smaller and estimate is more precise. Here is not observed. However, we have a

sample analog, the sample residual :

Eq. 57

So we can further exactly explain how relate to by the following equation.

( )

, ( ) -

, ( ) - , ( ) -

, ( ) -

, ( ) -

Eq. 58

is a linear transformation of . However, although, ( ) - is an

matrix, it is not a full rank matrix; its columns are related. Indeed, the weighting matrix

is all driven by the identity matrix, which has rank , and the matrix , which only has

columns. The full matrix , ( ) - has rank .

40

Matrices like , ( ) - and ( ) are called projection matrices, and

they come up a lot. For any matrix , denote its projection matrix ( ) and its

error projection as ( ) . These are convenient. We can write the OLS

estimate of as

,

Eq. 59

And the OLS residual as

Eq. 60

and also

Eq. 61

We say stuff like “The matrix projects onto . These matrices have a few useful

properties such as being symmetric and idempotent, which means they equal their own

square, .

Compute in terms of :

Eq. 62

so,

, - , -

, -

41

, - , ( ) -

Eq. 63

Because has rank . Consequently,

, -

Eq. 64

So we can use an estimate

Eq. 65

The estimated variance of the OLS estimator is thus given by

[ ] ( ) .

Eq. 66

Now, we can compute the BLUE estimate, and say something about its bias (zero) and its

sampling variability if we have spherical disturbances.

3.4.2. Maximum Likelihood

The principle of maximum likelihood is relatively straightforward. As before, we begin with

a sample ( ) of random variables chosen according to one of a family of

probabilities . In addition, ( | ) ) will be used to denote the density

function for the data when is the true state of nature. Then, the principle of maximum

likelihood yields a choice of the estimator as the value of the parameter that makes the

observed data most probable. The likelihood function is the density function regarded as a

function of .

42

( | ) ( | )

Eq. 67

The maximum likelihood estimator (MLE)

( ) ( | )

Eq. 68

In a large sample, the maximum likelihood estimators have many desirable properties.

However, especially for high dimensional data, the likelihood can have many local maxima.

Thus, finding the global maximum can be a major computational challenge.

This class of estimators has an important property. If ( ) is a maximum likelihood

estimate for , then ( ( )) is a maximum likelihood estimate for ( ). For example, if

is a parameter for the variance and is the maximum likelihood estimator, then √ is the

maximum likelihood for the standard deviation. The flexibility in estimation criterion seen

here is not available in the case of unbiased estimators. Typically, maximizing the score

function, ( | ), the logarithm of the likelihood, will be easier.

3.4.3. Generalized Method of Moment

Generalized Method of Moment (GMM) is a general estimation principle. Estimators are

derived from so-called moment conditions (Nielsen, 2005). There are some motivations to

apply GMM, firstly, many estimators can be seen a s special cases of GMM unifying

framework for comparison. Secondly, maximum likelihood estimators have the smallest

variance in the class of consistent and asymptotically normal estimators; however, we need a

full description of the data generating process and correct specification. Unlike maximum

likelihood, GMM does not require complete knowledge of the distribution of the data. Only

specified moments derived from an underlying model are needed for GMM estimation.

In some cases in which the distribution of the data is known, MLE can be

computationally very burdensome whereas GM can be computationally very easy. The log-

normal stochastic volatility model is one example. In models for which there are more

43

moment conditions than model parameters, GMM estimation provides a straightforward way

to test the specification of the proposed model. This is an important feature that is unique to

GMM estimation. GMM is an alternative based on minimal assumptions. The last, GMM

estimation is often possible where a likelihood analysis is extremely difficult. We only need a

partial specification of the models for rational expectations. A moment condition is a

statement involving the data and the parameters:

( ) , ( )-

Eq. 69

where is a K x 1 vector of parameters; ( ) is an R dimensional vector of (non-linear)

functions; contains model variables; and contains instruments.

If we knew the expectation that we could solve the equation in (*) to find . If there

is a unique solution, so that

, ( )- if and only if

Eq. 70

Then we say that the system is identified. Identification is essential for doing econometrics as

applied for “is the model constructed so that is unique (identification) and are the data

informative enough to determine (empirical identification). In many applications, the

moment condition has the specific form as follow.

( ) ( )

Eq. 71

Where the R instruments in the are multiplied by the disturbance term, ( ). It can be

assumed as the equivalent of an error term. The moment condition becomes.

( ) , ( ) -

44

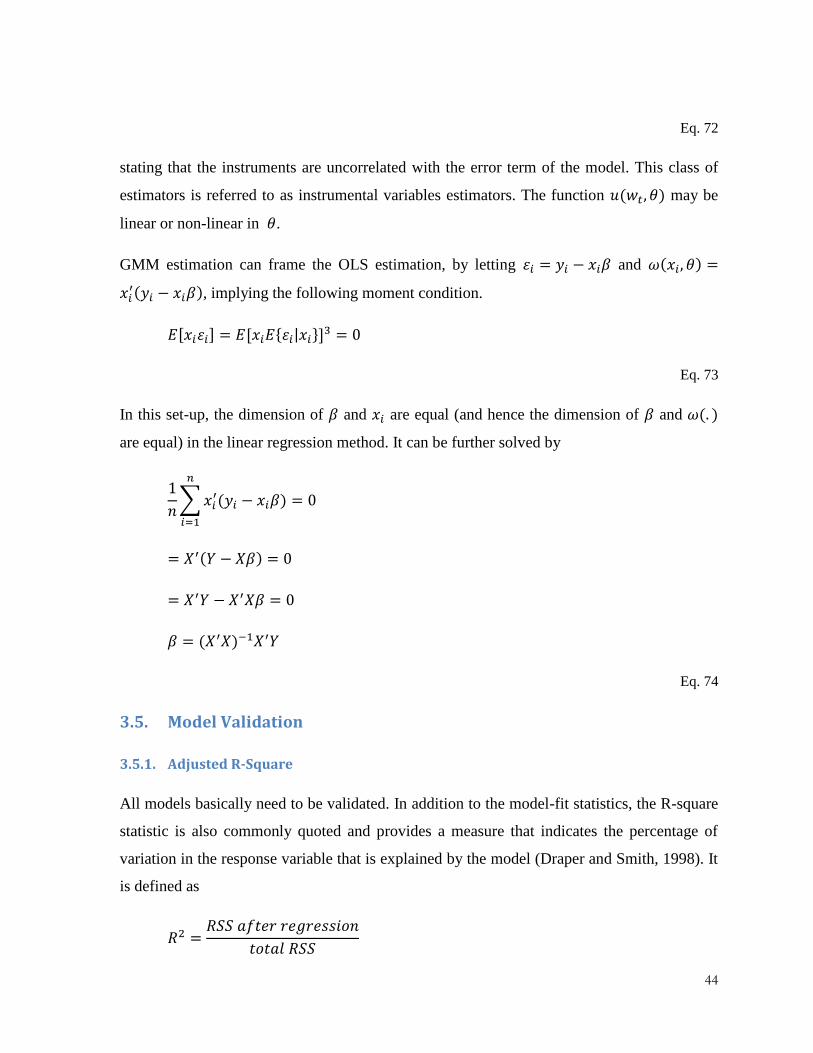

Eq. 72

stating that the instruments are uncorrelated with the error term of the model. This class of

estimators is referred to as instrumental variables estimators. The function ( ) may be

linear or non-linear in .

GMM estimation can frame the OLS estimation, by letting and ( )

( ), implying the following moment condition.

, - , * | +-

Eq. 73

In this set-up, the dimension of and are equal (and hence the dimension of and ( )

are equal) in the linear regression method. It can be further solved by

∑

( )

( )

( )

Eq. 74

3.5. Model Validation

3.5.1. Adjusted R-Square

All models basically need to be validated. In addition to the model-fit statistics, the R-square

statistic is also commonly quoted and provides a measure that indicates the percentage of

variation in the response variable that is explained by the model (Draper and Smith, 1998). It

is defined as

45

Eq. 75

And basically gives the percentage of the deviance in the response variable that can

be accounted for by adding the explanatory variable to the model. Although R-square is

widely used, it will always increase as variables added to the model (the deviance can only

go down when additional variables are added to a model). One solution to this problem is to

circulate an adjusted R-square statistic ( ), which takes into account the number of terms

entered into the model and does not necessarily increase as more terms are added. Adjusted

R-square can be derived using the following equation:

( )

Eq. 76

where n is the number of cases used to construct the model and k is the number of terms in

the model (not including the constant).

3.5.2. Marginal Cost of Information

3.5.2.1. Akaike Information Criterion (AIC)

The Akaike information criterion (1973) is a measure of the relative quality of a statistical

model, for a given set of data. As such, AIC provides a means for model selection. AIC deals

with the trade-off between the goodness of fit and the complexity of the model. It is founded

on information entropy: it offers a relative estimate of the information lost when a given

model is used to represent the process that generates the data. Burnham and Anderson (2002)

suggested that Akaike Information Criterion (AIC) is a way of selecting a model from a set

of models. The chosen model is the one that minimizes the Kullback-Leibler distance

between the model and the truth. It's based on information theory, but a heuristic way to

think about it is as a criterion that seeks a model that has a good fit to the truth but few

parameters. It is defined as:

( ( ))

Eq. 77

46

where likelihood is the probability of the data given a model and K is the number of free