The Agricultural Outlook: USDA’s Commodity …The Agricultural Outlook: USDA’s Commodity...

76

The Agricultural Outlook: USDA’s Commodity Analysis Program and Current Market Prospects Gerald A. Bange Chairperson World Agricultural Outlook Board Office of the Chief Economist U.S. Department of Agriculture Presented to John Deere Executives Moline, Illinois July 22, 2008

Transcript of The Agricultural Outlook: USDA’s Commodity …The Agricultural Outlook: USDA’s Commodity...

The Agricultural Outlook: USDA’s Commodity Analysis Program and Current Market Prospects

Gerald A. BangeChairperson

World Agricultural Outlook BoardOffice of the Chief Economist

U.S. Department of Agriculture

Presented toJohn Deere Executives

Moline, IllinoisJuly 22, 2008

2

Topics for Discussion

• USDA’s Analytical Program• Commodity Situation and Outlook• Impact of Renewable Energy• Fuel vs. Food Debate• Prospects for World Agricultural Growth

3

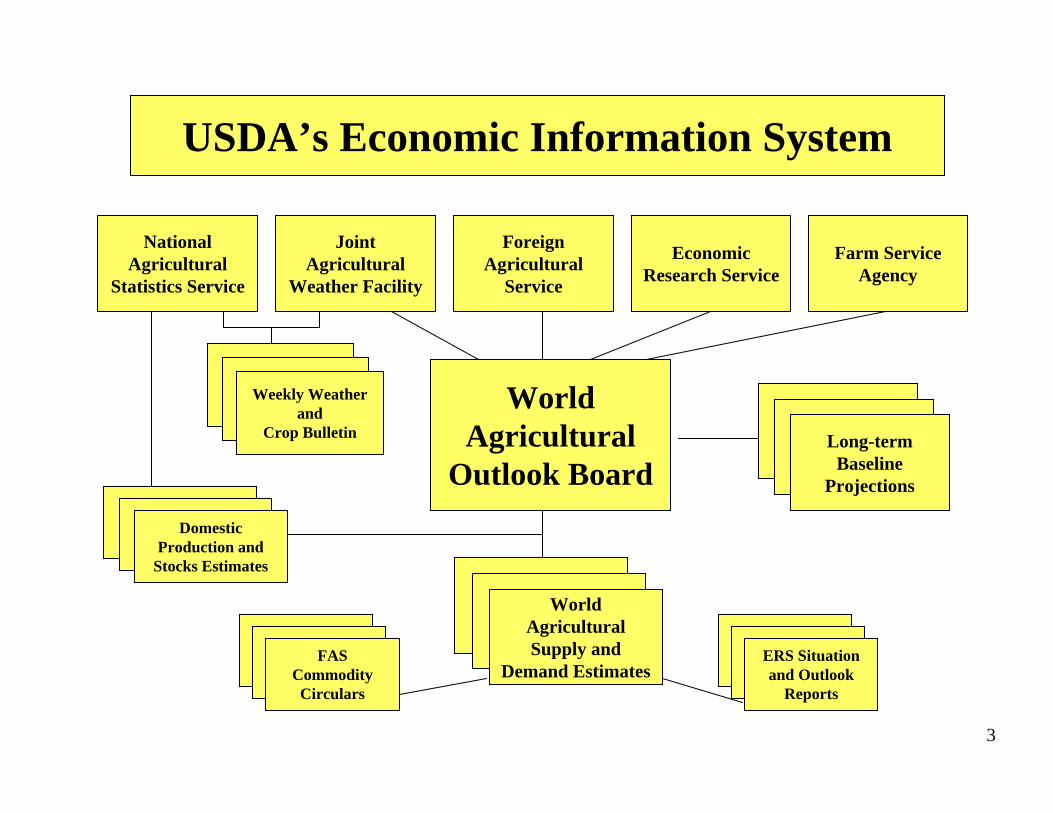

USDA’s Economic Information System

Farm Service Agency

Joint Agricultural

Weather Facility

Foreign Agricultural

Service

Economic Research Service

National Agricultural

Statistics Service

ERS Situation and Outlook

Reports

Weekly Weatherand

Crop Bulletin

World Agricultural

Outlook BoardDomestic

Production and Stocks Estimates

World Agricultural Supply and

Demand EstimatesFAS

Commodity Circulars

Long-term Baseline

Projections

4

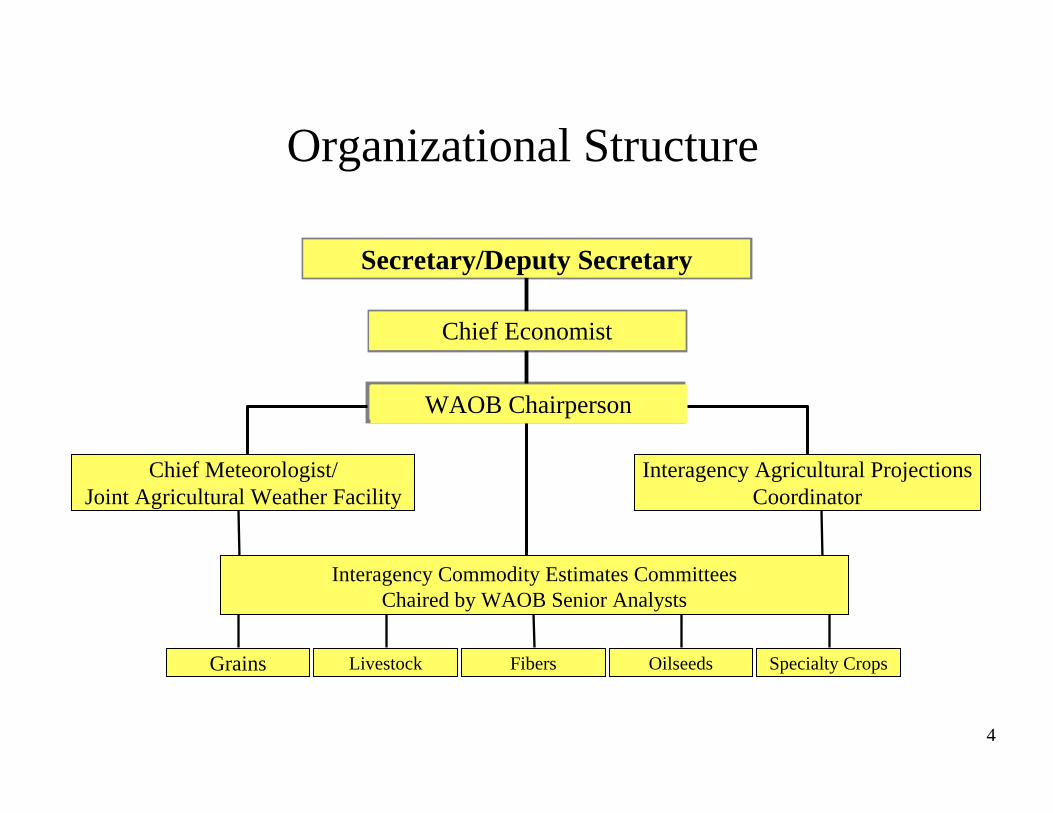

Interagency Agricultural Projections Coordinator

Chief Economist

Secretary/Deputy Secretary

Organizational Structure

WAOB Chairperson

Chief Meteorologist/Joint Agricultural Weather Facility

Grains OilseedsLivestock Fibers Specialty Crops

Interagency Commodity Estimates CommitteesChaired by WAOB Senior Analysts

5

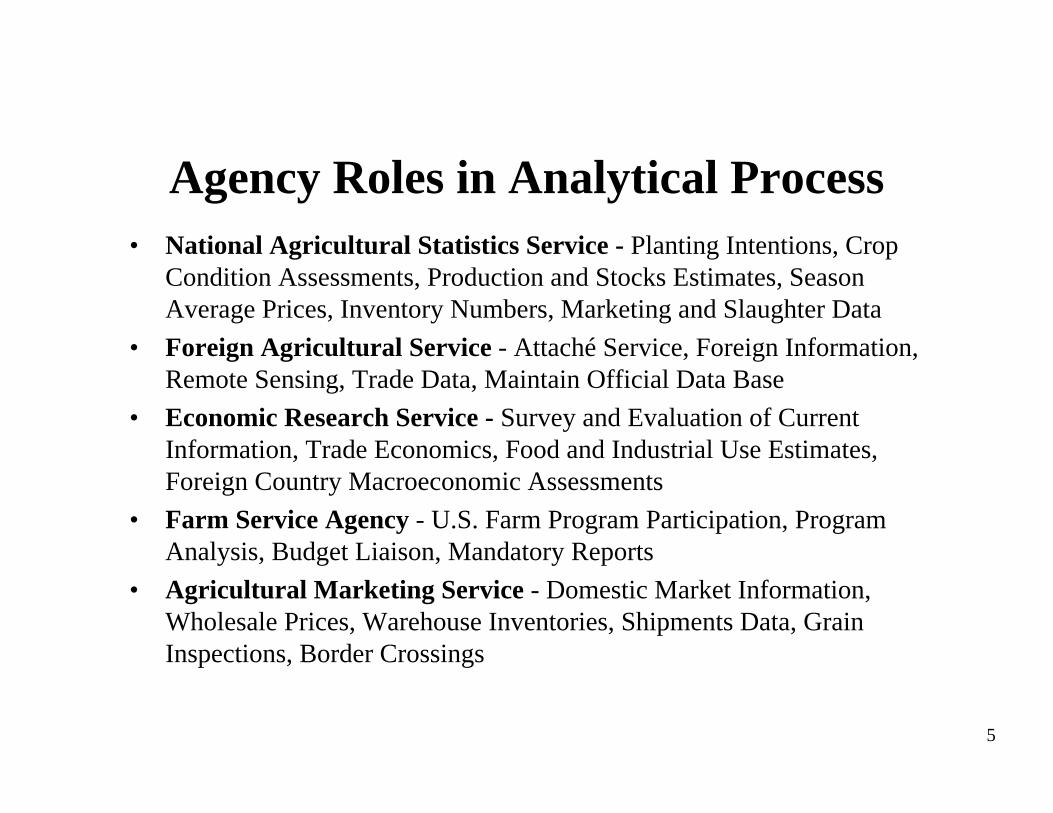

Agency Roles in Analytical Process• National Agricultural Statistics Service - Planting Intentions, Crop

Condition Assessments, Production and Stocks Estimates, Season Average Prices, Inventory Numbers, Marketing and Slaughter Data

• Foreign Agricultural Service - Attaché Service, Foreign Information, Remote Sensing, Trade Data, Maintain Official Data Base

• Economic Research Service - Survey and Evaluation of Current Information, Trade Economics, Food and Industrial Use Estimates,Foreign Country Macroeconomic Assessments

• Farm Service Agency - U.S. Farm Program Participation, Program Analysis, Budget Liaison, Mandatory Reports

• Agricultural Marketing Service - Domestic Market Information, Wholesale Prices, Warehouse Inventories, Shipments Data, Grain Inspections, Border Crossings

6

World Agricultural Outlook Board

• Chairs Interagency Committees– Commodity Supply and Demand Estimates– Agricultural Projections

• Clears USDA Outlook Reports• Directs Weather Analysis

– Joint Agricultural Weather Facility– World Meteorological Organization Liaison

• Coordinates Climate and Remote Sensing Activities– Landsat Imagery– Meteorological Satellite Data

7

Goals of USDA’s Analytical Program

• Objectivity– Provide unbiased information

• Reliability– Based on sound data and analysis

• Timeliness– Fast flow to users

8

Economic and Trend Analysis

U.S. and World

Weather

Travel Reports

Remote Sensing

Official Country Reports

AttachéReports

USDA’s Economic

Information System

9

Commodity Situation and Outlook (Overview)

• Strong Demand Worldwide – Income growth in developing countries – India, China, etc.– Japan and other Asian markets active buyers despite high

prices– Weak U.S. dollar

• Rising Petroleum Prices • Increased Production of Renewable Fuels

– Corn for ethanol in the United States– Oilseeds for biodiesel in the European Union

10

Projected Growth Rates

2.8

6.8

8.8

1.4

1.5

1.7

2009 Average20102008

3.23.63.1World

7.47.67.9India

9.28.410.5China

1.72.11.5Japan

2.02.22.2EU-27

2.23.31.6U.S.

Source: Oxford Economics

11

Overview(continued)

• Tight Grain and Soybean Stocks– U.S wheat stocks at 60-year low– World wheat stocks at 26-year low– Corn stocks forecast to decline sharply in 2008/09– U.S. soybean acres dropped sharply in 2007/08,

stocks reduced from record beginning levels as use exceeds production by 450+ million bushels

– South American soybean acres increased only modestly in 2007/08

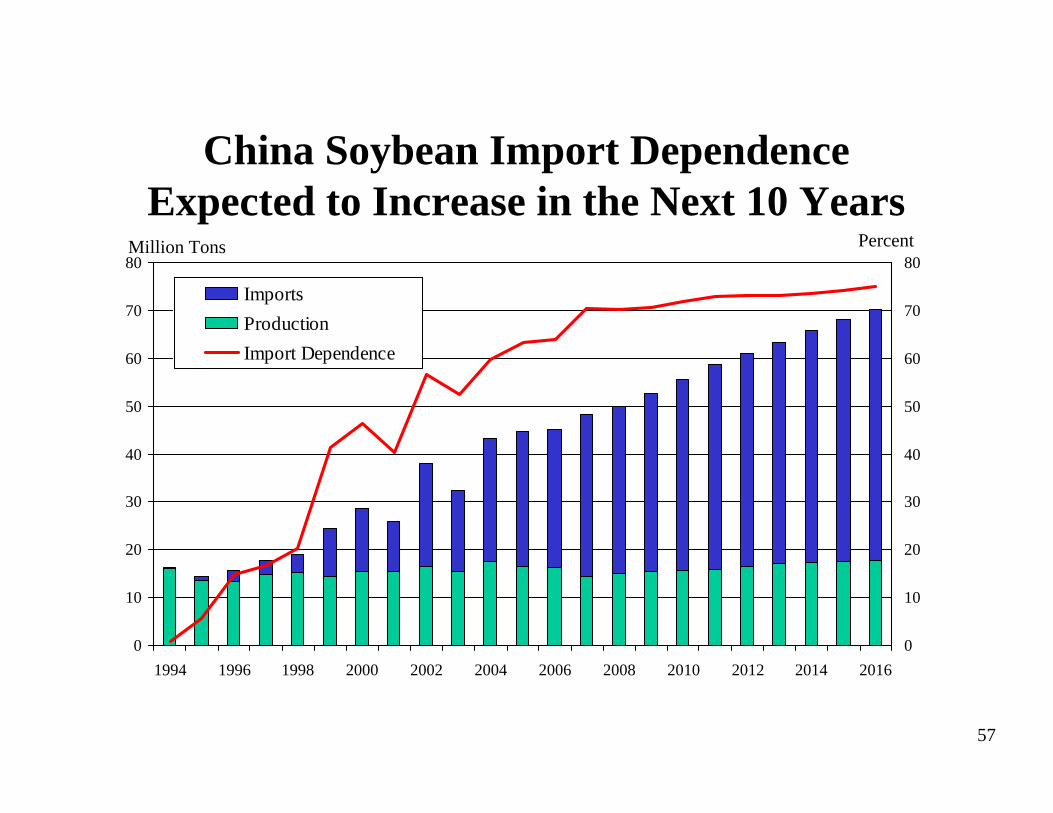

– China imports of soybeans forecast record high

12

Overview(continued)

• World Wheat Consumption has exceeded Production in 7 of the last 8 years– Yields below trend in major exporting countries for the

past 2 years– Australia recorded 2 back-to-back crop failures – lost

more than one full year’s output– E.U. crops below par – U.S. yields below trend– Canadian crops below average

13

Overview(continued)

• Restrictions on World Exports– Ukraine, Russia, and Kazakhstan curtailed grain

exports– Argentina shut-off export registrations on corn and

wheat and raised taxes on soybean exports– Thailand, Vietnam, India, Egypt, Cambodia, and China

imposed various restraints on rice exports– Australian rice exportable supplies down sharply due to

drought

14

Overview(continued)

• Rising Input Costs– Fuel prices up sharply– Fertilizer prices at record highs

• Strong global demand with higher incomes, improved cultural practices and more cultivated area amid rising prices for agricultural commodities

• U.S. dependency on fertilizer imports is growing –domestic production accounts for less than half of nitrogen needs

– Feed prices rising

15

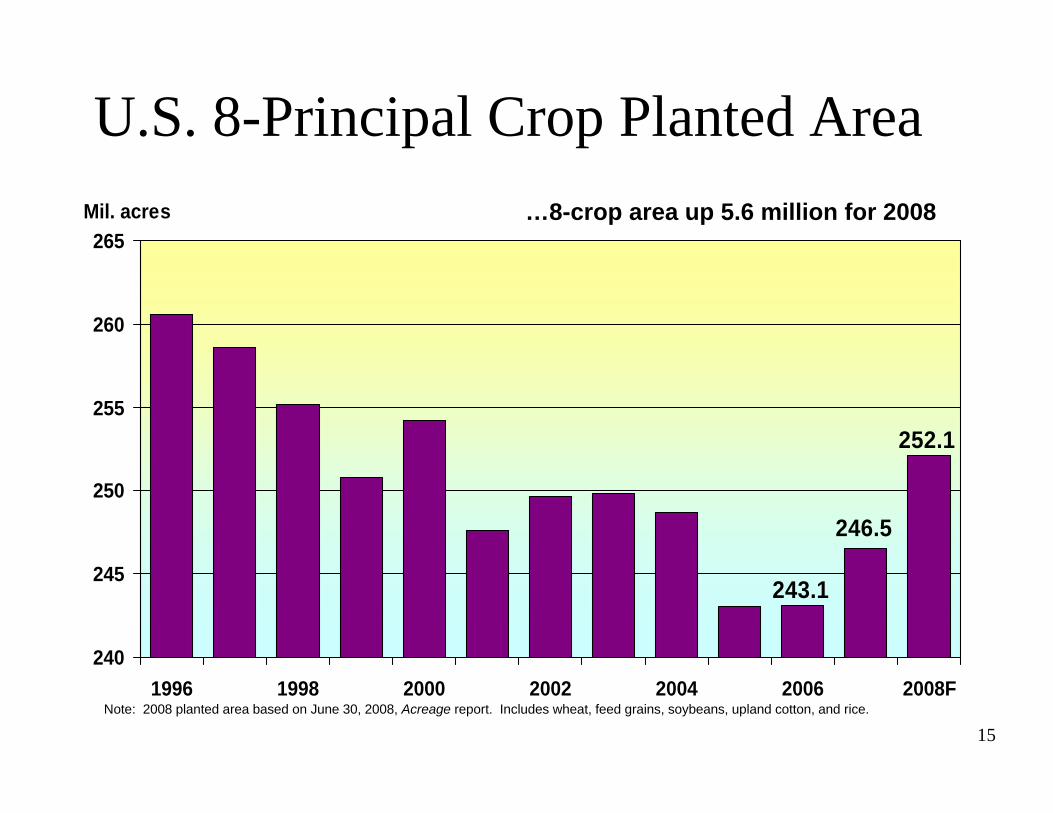

243.1

246.5

252.1

240

245

250

255

260

265

1996 1998 2000 2002 2004 2006 2008F

Mil. acres

Note: 2008 planted area based on June 30, 2008, Acreage report. Includes wheat, feed grains, soybeans, upland cotton, and rice.

U.S. 8-Principal Crop Planted Area…8-crop area up 5.6 million for 2008

16

60.4

63.5

50

55

60

65

70

75

80

1996 1998 2000 2002 2004 2006 2008F

Mil. acres

Note: 2008 planted area based on June 30, 2008, Acreage report.

U.S. Wheat Planted Area…wheat acres up 3.1 million for 2008

17

U.S. Wheat Supply and DemandChange from

2007/08Percent

Planted area (million acres) 60.4 63.5 5.0Harvested area (million acres) 51.0 56.6 10.9Yield (bushels per acre) 40.5 43.5 7.4

Million bushelsBeginning stocks 456 306 -33.0Production 2,067 2,461 19.1Imports 108 100 -7.4

Total supply 2,631 2,866 8.9Food use 950 960 1.1Seed 88 84 -4.7Feed and residual 20 285 1,323.5

Domestic use 1,058 1,329 25.6Exports 1,267 1,000 -21.1

Total use 2,325 2,329 0.2Ending stocks 306 537 75.8

PercentStocks to use ratio 13.1 23.1

Dollars per bushelAverage market price 6.48 6.75/8.25 15.7

2007/08 estimate

2008/09 forecast

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

18

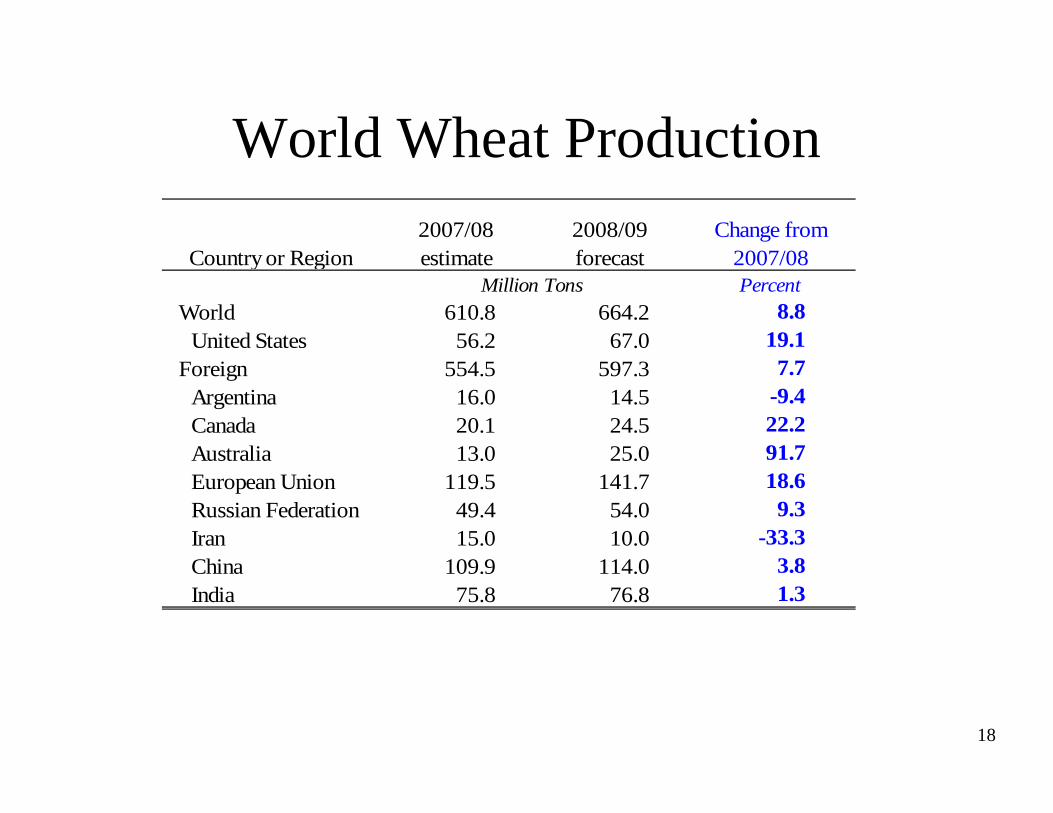

World Wheat Production

Country or Region2007/08 estimate

2008/09 forecast

Change from 2007/08

Million Tons PercentWorld 610.8 664.2 8.8

United States 56.2 67.0 19.1Foreign 554.5 597.3 7.7

Argentina 16.0 14.5 -9.4Canada 20.1 24.5 22.2Australia 13.0 25.0 91.7European Union 119.5 141.7 18.6Russian Federation 49.4 54.0 9.3Iran 15.0 10.0 -33.3China 109.9 114.0 3.8India 75.8 76.8 1.3

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

19

This Time Last Year.

20

Filling

Maturing

Maturing

Flowering

21Northern Poland 08-July-2008

22

Iran WheatYear Area Yield Production

Million hectares Tons/hectare Million tons2003/04 6.4 2.10 13.42004/05 6.6 2.21 14.62005/06 7.0 2.06 14.32006/07 6.5 2.23 14.52007/08 6.9 2.17 15.0

2008/09 f 5.9 1.71 10.0

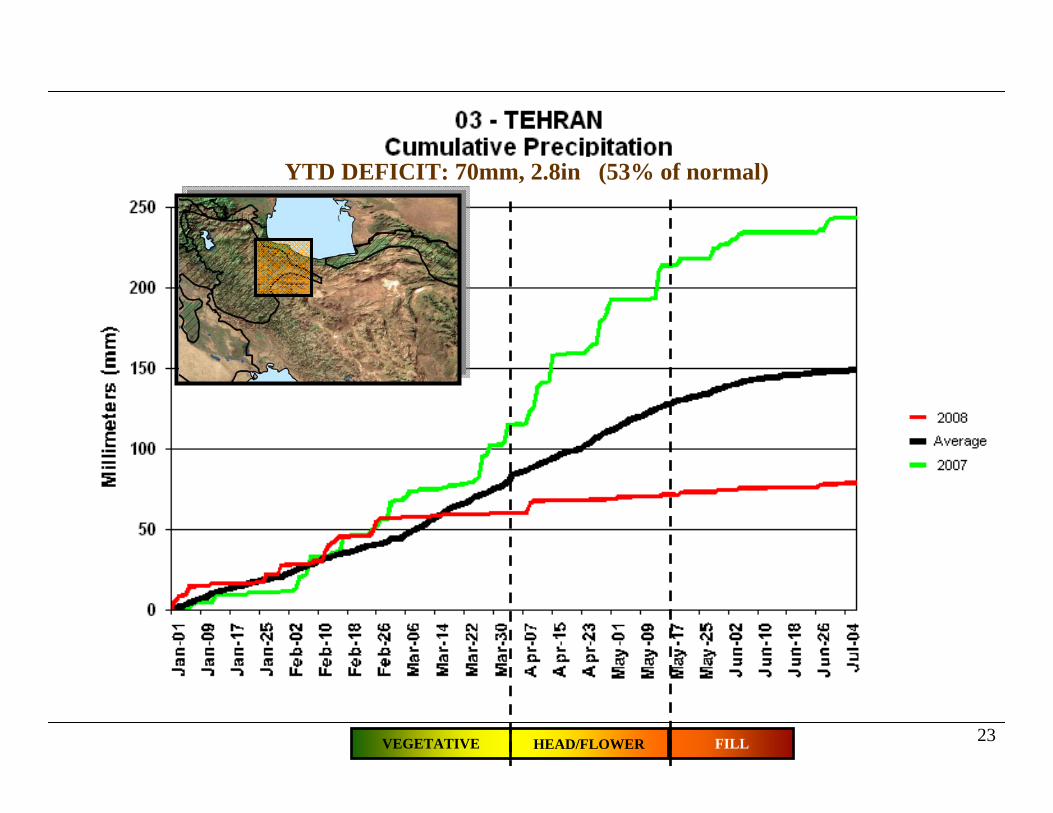

23FILLHEAD/FLOWERVEGETATIVE

YTD DEFICIT: 70mm, 2.8in (53% of normal)

24

NW

CENTRAL

CENTRAL

EAST

CASPIAN

SEA

PERSIAN

GULF

IRAN:Vegetative Index

Difference from Last YearMay 10, 2008

SPOT NDVI: Compared to Last Year

Worse thanlast year

Better thanlast year

NoDiff

Foreign Agricultural ServiceOffice of Global Analysis

IPA Division

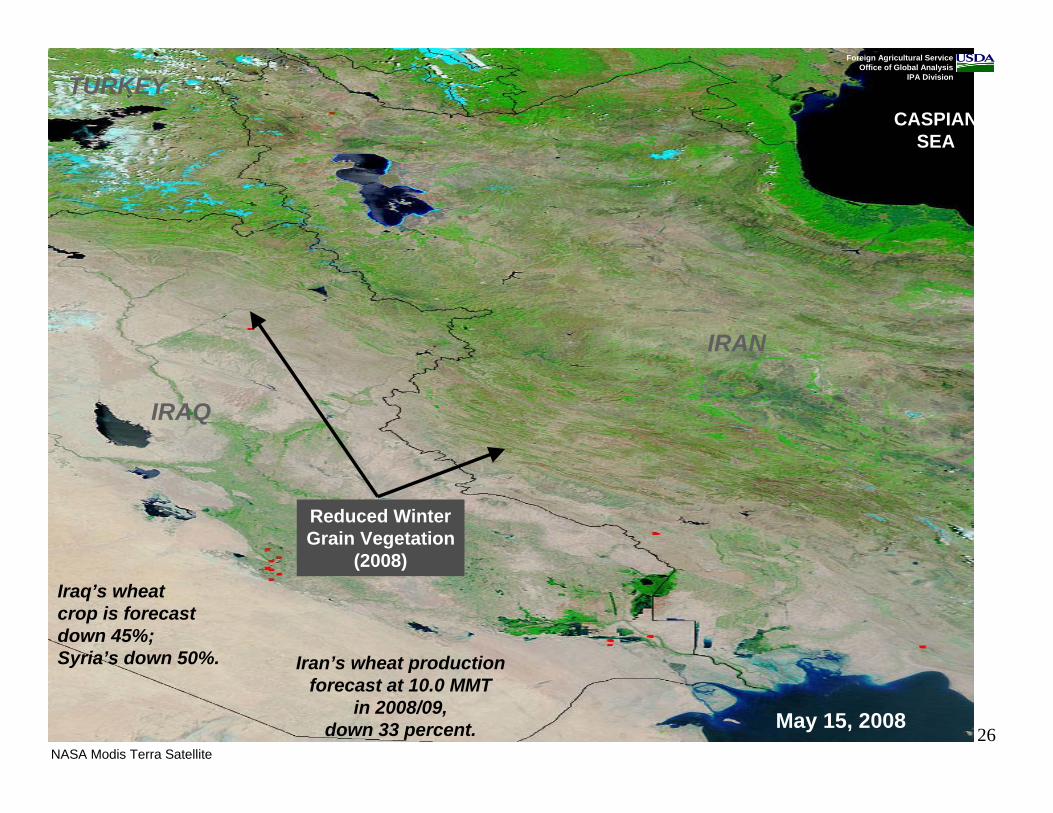

25May 6, 2007

IRAQ

IRAN

TURKEY

Normal WinterGrain Vegetation

(2007)

CASPIANSEA

Iran produced anestimated 15.0 MMTof wheat in 2007/08

NASA Modis Terra Satellite

Foreign Agricultural ServiceOffice of Global Analysis

IPA Division

26May 15, 2008

IRAQ

IRAN

TURKEYCASPIAN

SEA

Reduced WinterGrain Vegetation

(2008)

Iran’s wheat productionforecast at 10.0 MMT

in 2008/09,down 33 percent.

Iraq’s wheat crop is forecast down 45%;Syria’s down 50%.

NASA Modis Terra Satellite

Foreign Agricultural ServiceOffice of Global Analysis

IPA Division

27

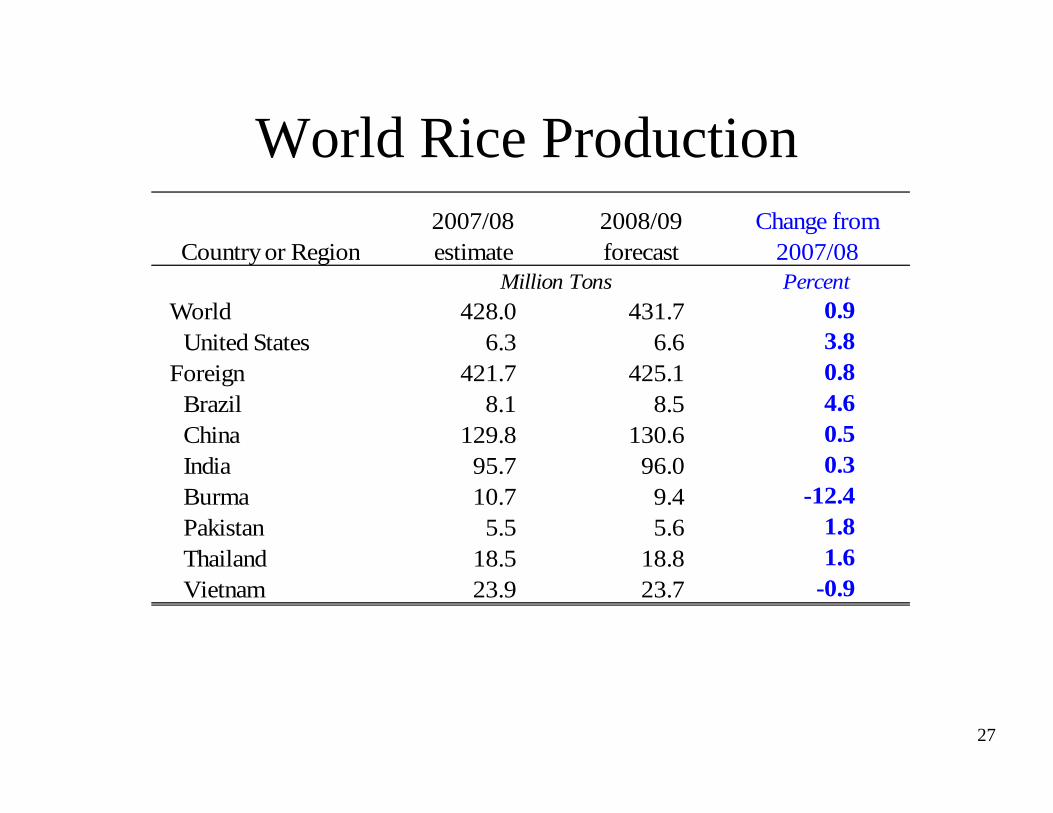

World Rice Production

Country or Region2007/08 estimate

2008/09 forecast

Change from 2007/08

Million Tons PercentWorld 428.0 431.7 0.9

United States 6.3 6.6 3.8Foreign 421.7 425.1 0.8

Brazil 8.1 8.5 4.6China 129.8 130.6 0.5India 95.7 96.0 0.3Burma 10.7 9.4 -12.4Pakistan 5.5 5.6 1.8Thailand 18.5 18.8 1.6Vietnam 23.9 23.7 -0.9

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

28

Burma: Rice Land Distribution

Landsat Satellite-derived Rice Area Map (Geocover 2000) – 30 Meter Resolution

Foreign Agricultural ServiceOffice of Global AnalysisIPA Division

Ayeyarwady 2.0

Yangon 0.6

Bago 1.1

Mon 0.3

Subtotal 4.0

Others 3.0

Total 7.0

Total Rice Area (MHa)

Wet Season Rice Accounts for85% of Total Rice Production

Bay of

Bengal

AndamanSea

Yangon

Bago

Mon

Ayeyarwady

Rakhine

Kayah

Kayin

Magway

RiceCultivation

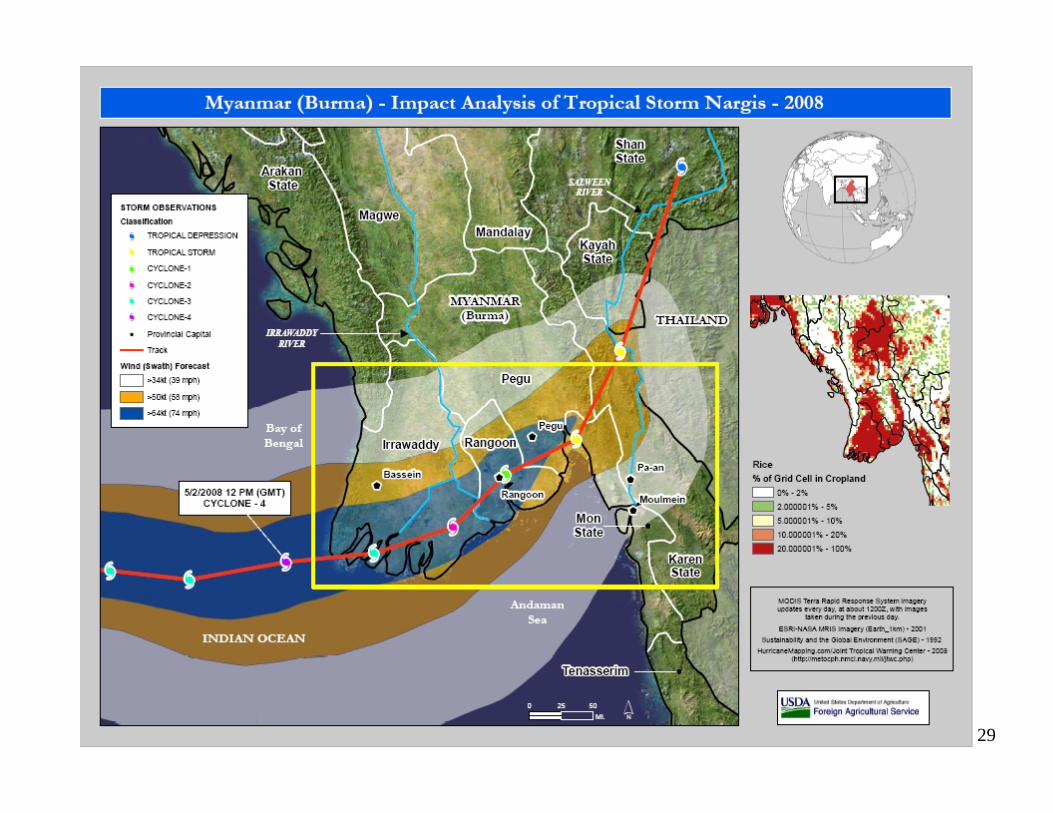

29

30

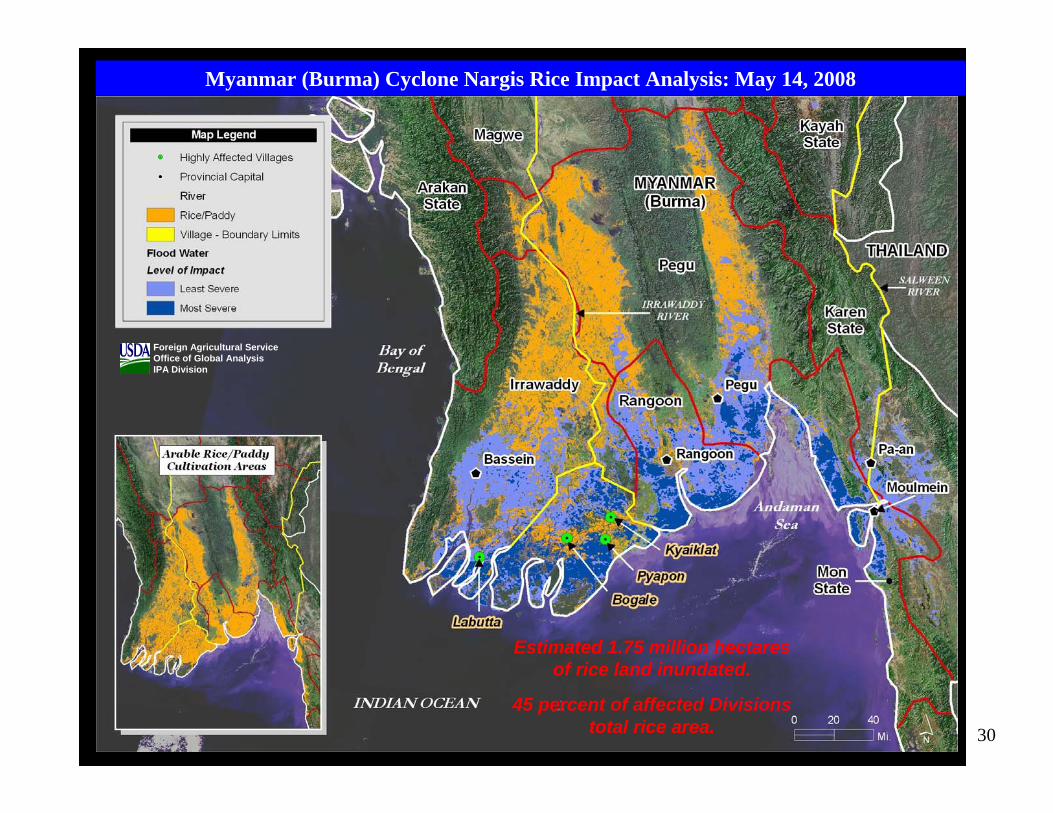

Foreign Agricultural ServiceOffice of Global AnalysisIPA Division

Estimated 1.75 million hectaresof rice land inundated.

45 percent of affected Divisionstotal rice area.

Myanmar (Burma) Cyclone Nargis Rice Impact Analysis: May 14, 2008

31

U.S. Rice Supply and DemandRough Equivalent of Rough and Milled Rice

Change from 2007/08Percent

Planted area (million acres) 2.76 2.90 4.9Harvested area (million acres) 2.75 2.88 4.8Yield (pounds per acre) 7,185 7,121 -0.9

Million cwtBeginning stocks 39.3 26.1 -33.6Production 197.5 205.0 3.8Imports 23.0 23.5 2.2

Total supply 259.8 254.6 -2.0Domestic use 124.7 126.0 1.1Exports 109.0 107.0 -1.8

Total use 233.7 233.0 -0.3Ending stocks 26.1 21.6 -17.2

PercentStocks/use 11.2 9.3

Dollars/cwtAverage market price 12.8 16.30/17.30 31.3

2007/08 estimate

2008/09 forecast

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

32

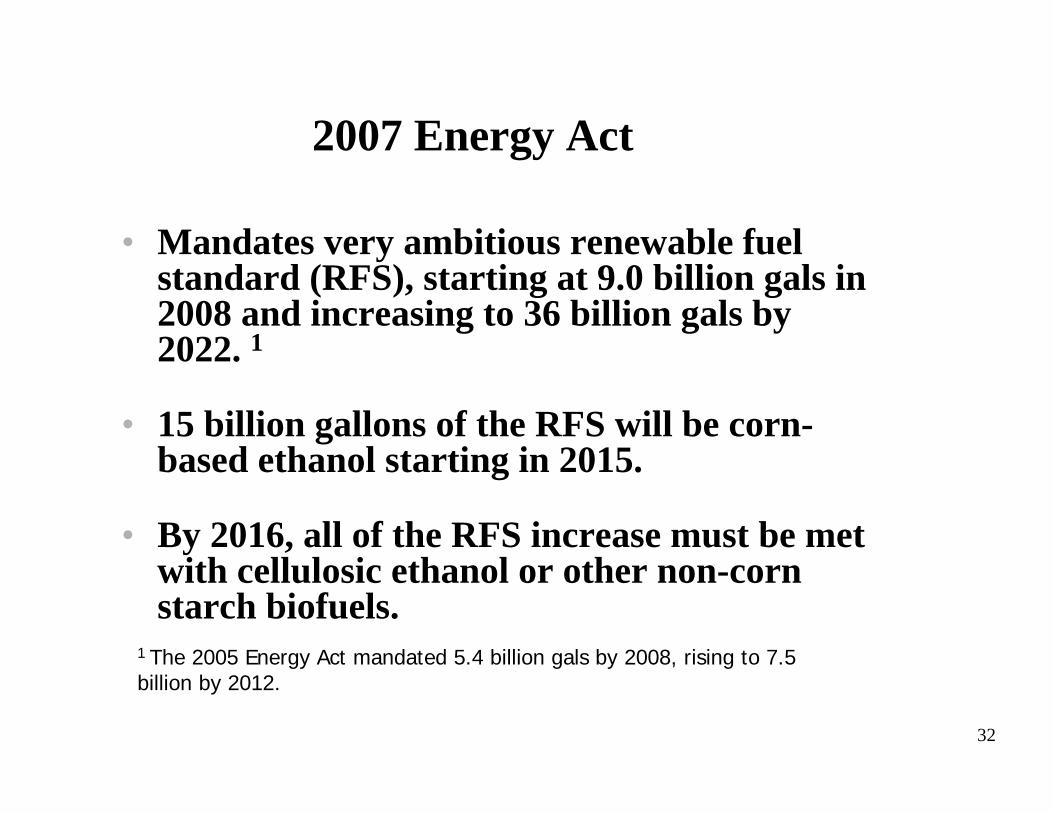

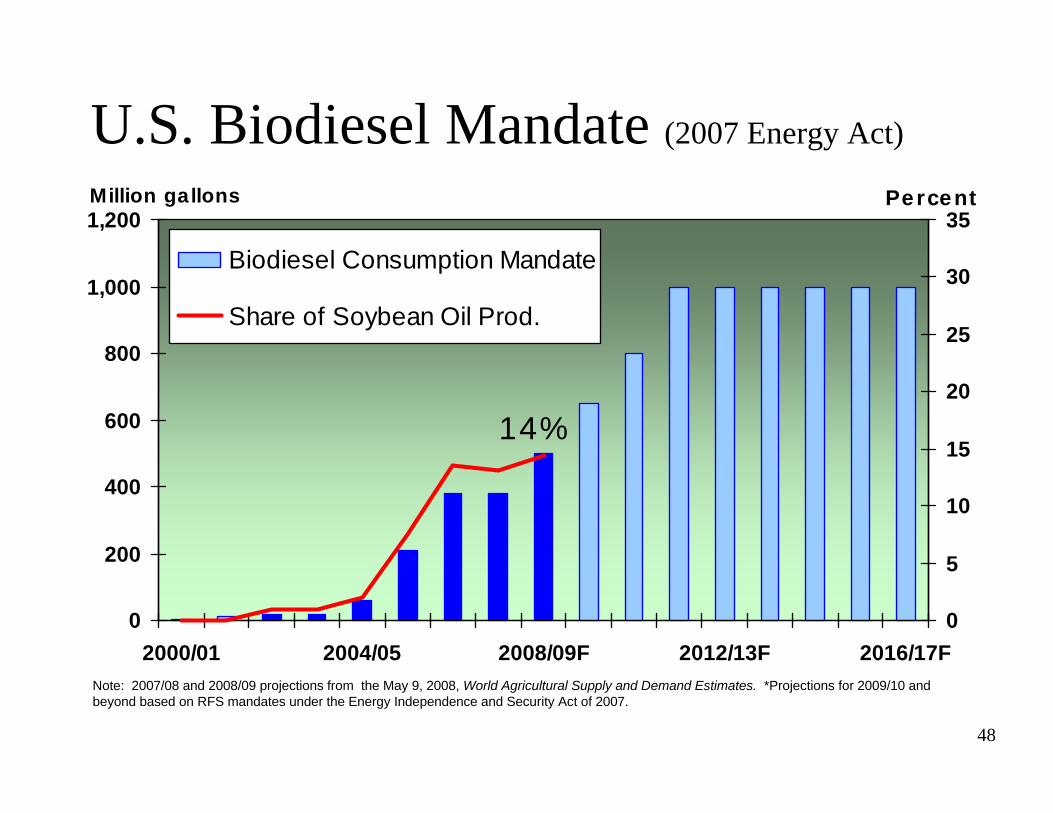

2007 Energy Act

• Mandates very ambitious renewable fuel standard (RFS), starting at 9.0 billion gals in 2008 and increasing to 36 billion gals by 2022. 1

• 15 billion gallons of the RFS will be corn-based ethanol starting in 2015.

• By 2016, all of the RFS increase must be met with cellulosic ethanol or other non-corn starch biofuels.

1 The 2005 Energy Act mandated 5.4 billion gals by 2008, rising to 7.5 billion by 2012.

33

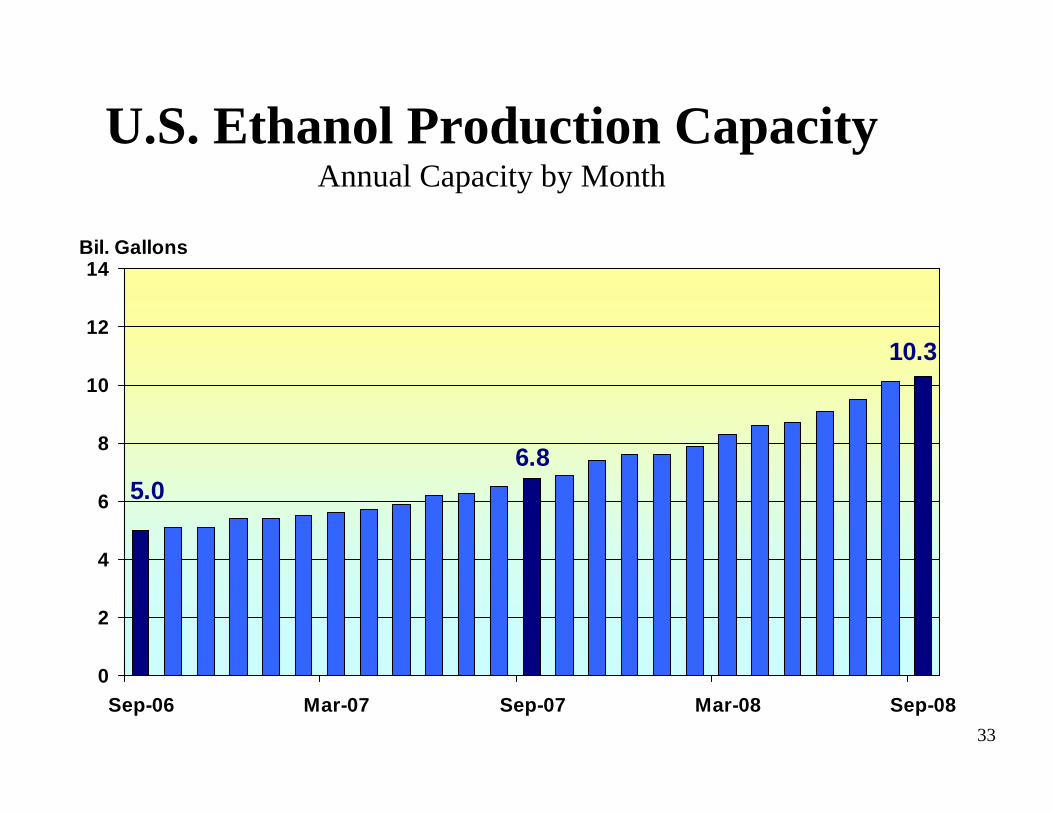

U.S. Ethanol Production CapacityAnnual Capacity by Month

6.8

10.3

5.0

0

2

4

6

8

10

12

14

Sep-06 Mar-07 Sep-07 Mar-08 Sep-08

Bil. Gallons

34

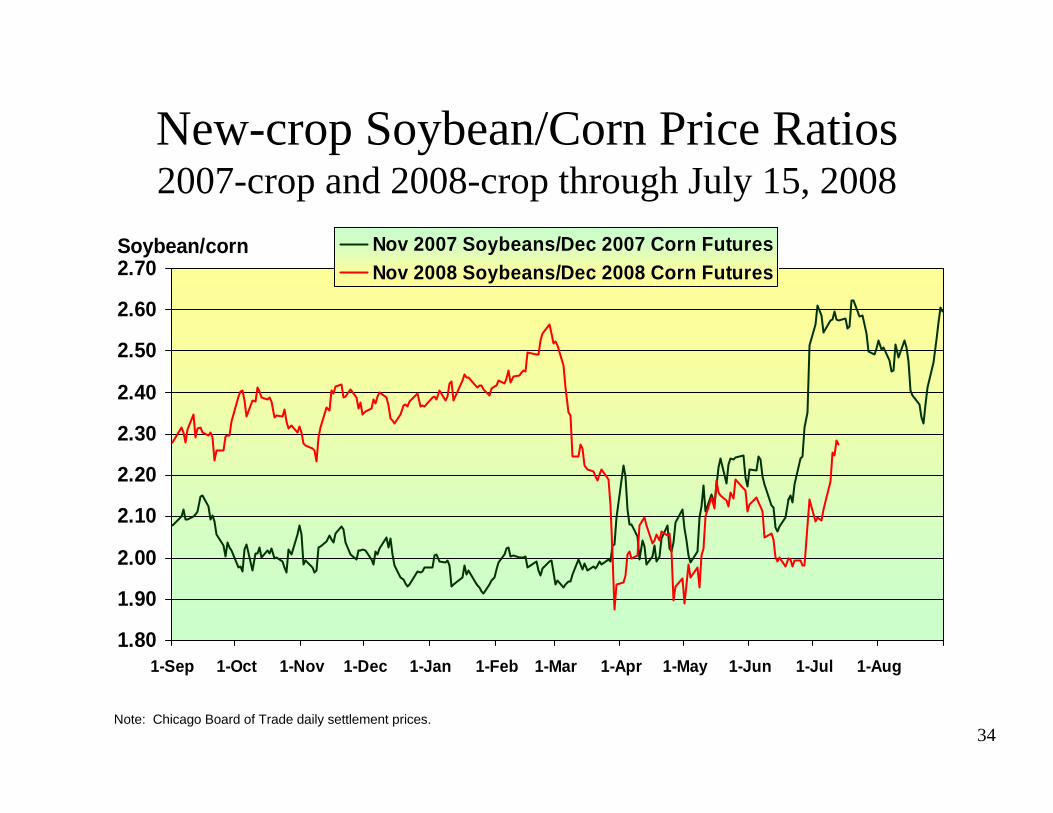

New-crop Soybean/Corn Price Ratios2007-crop and 2008-crop through July 15, 2008

1.80

1.90

2.00

2.10

2.20

2.30

2.40

2.50

2.60

2.70

1-Sep 1-Oct 1-Nov 1-Dec 1-Jan 1-Feb 1-Mar 1-Apr 1-May 1-Jun 1-Jul 1-Aug

Soybean/corn Nov 2007 Soybeans/Dec 2007 Corn FuturesNov 2008 Soybeans/Dec 2008 Corn Futures

Note: Chicago Board of Trade daily settlement prices.

35

87.3

93.6

74.5

63.6

55

60

65

70

75

80

85

90

95

100

1996 1998 2000 2002 2004 2006 2008F

Mil. acres

Corn Soybeans

Note: 2008 planted area based on June 30, 2008, Acreage report.

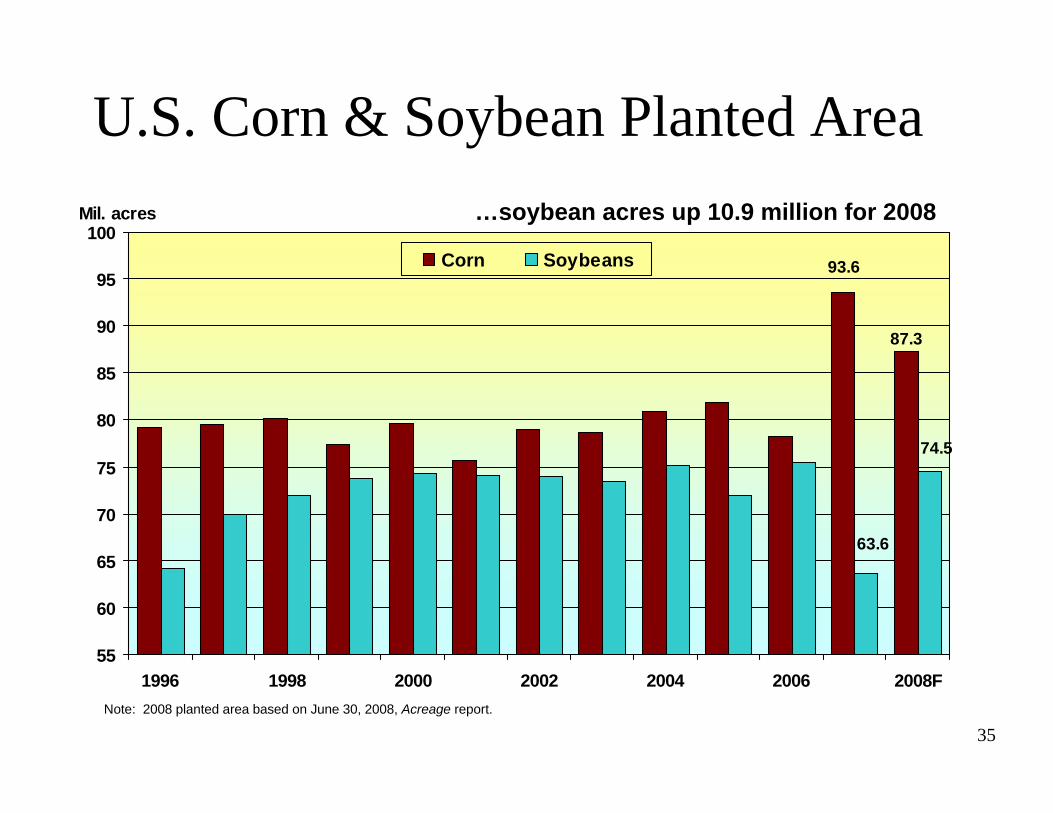

U.S. Corn & Soybean Planted Area…soybean acres up 10.9 million for 2008

36

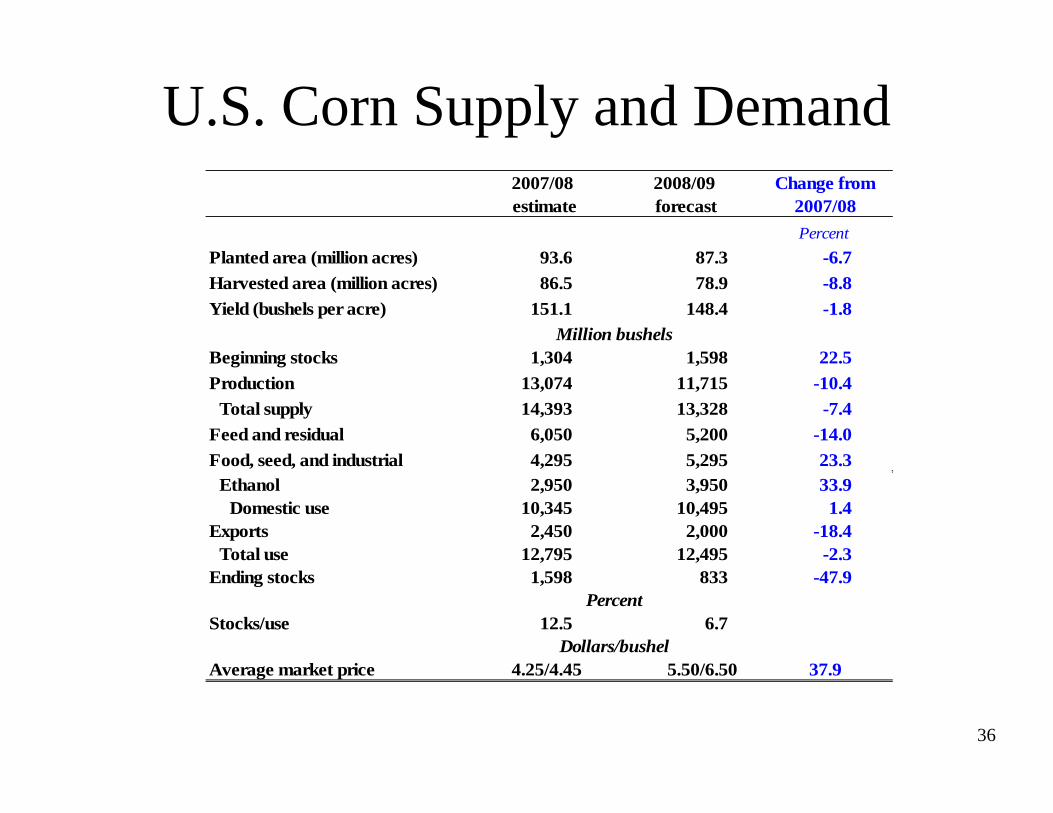

U.S. Corn Supply and DemandChange from

2007/08Percent

Planted area (million acres) 93.6 87.3 -6.7Harvested area (million acres) 86.5 78.9 -8.8Yield (bushels per acre) 151.1 148.4 -1.8

Million bushelsBeginning stocks 1,304 1,598 22.5Production 13,074 11,715 -10.4

Total supply 14,393 13,328 -7.4Feed and residual 6,050 5,200 -14.0Food, seed, and industrial 4,295 5,295 23.3

Ethanol 2,950 3,950 33.9Domestic use 10,345 10,495 1.4

Exports 2,450 2,000 -18.4Total use 12,795 12,495 -2.3

Ending stocks 1,598 833 -47.9Percent

Stocks/use 12.5 6.7Dollars/bushel

Average market price 4.25/4.45 5.50/6.50 37.9

2007/08 estimate

2008/09 forecast

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

37

1.60

2.10

2.60

3.10

3.60

4.10

4.60

5.10

5.60

6.10

6.60

1990/91 1996/97 2002/03 2008/09F

$/bushel

0

5

10

15

20

25

30PercentFarm Price Stocks/Use Avg. S/U (90-07)

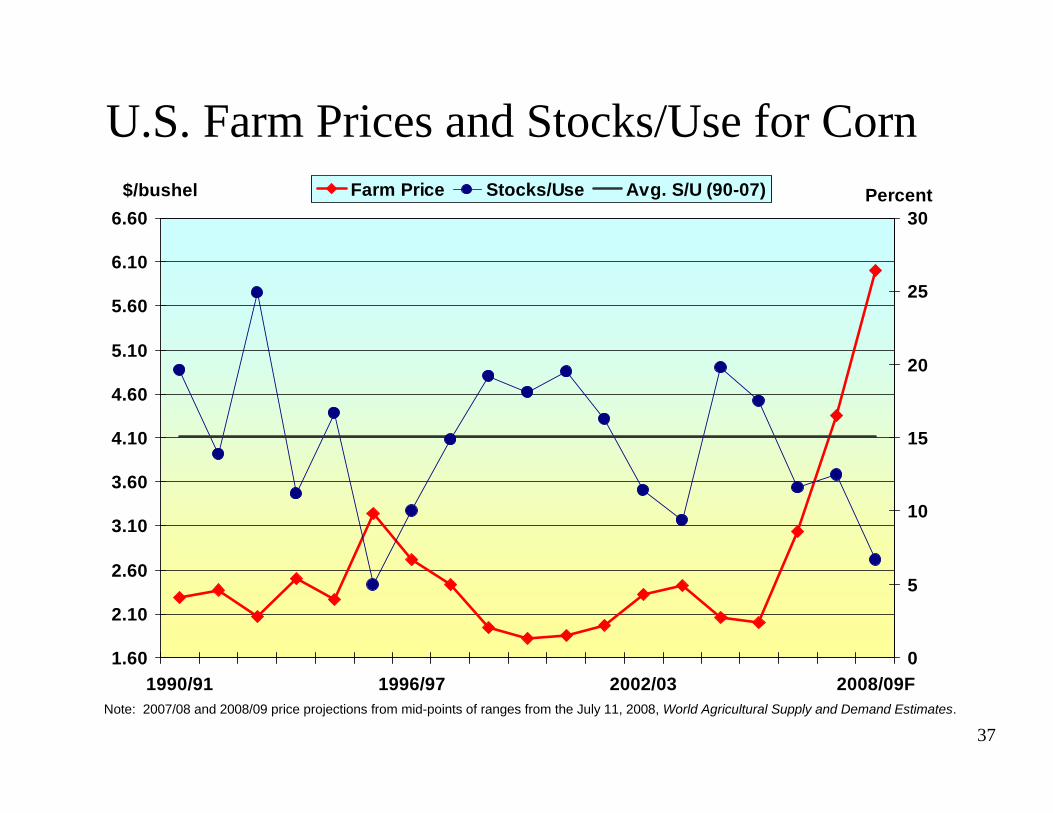

U.S. Farm Prices and Stocks/Use for Corn

Note: 2007/08 and 2008/09 price projections from mid-points of ranges from the July 11, 2008, World Agricultural Supply and Demand Estimates.

38

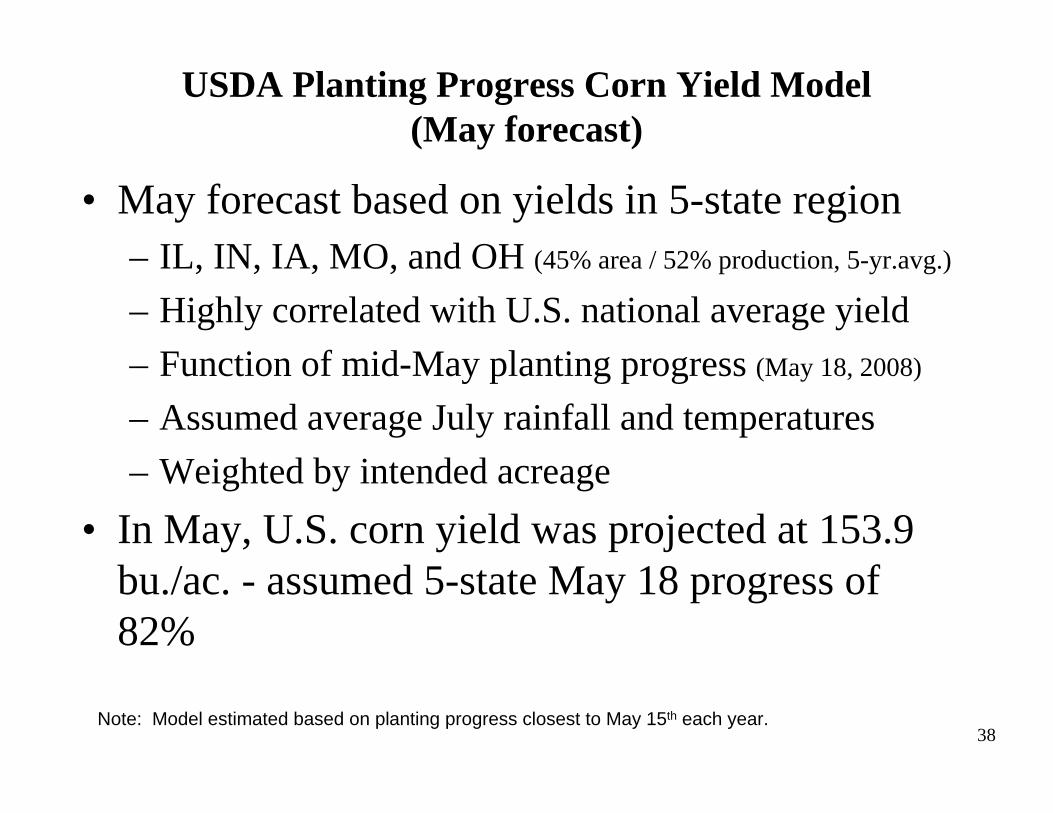

USDA Planting Progress Corn Yield Model(May forecast)

• May forecast based on yields in 5-state region– IL, IN, IA, MO, and OH (45% area / 52% production, 5-yr.avg.)

– Highly correlated with U.S. national average yield– Function of mid-May planting progress (May 18, 2008)

– Assumed average July rainfall and temperatures– Weighted by intended acreage

• In May, U.S. corn yield was projected at 153.9 bu./ac. - assumed 5-state May 18 progress of 82%

Note: Model estimated based on planting progress closest to May 15th each year.

39

U.S. Corn Trend Yields

100

110

120

130

140

150

160

170

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008F

Bu./ac.

Yield 90-07 Trend May 9 WASDE

May forecast 153.9 based on planting progress

40

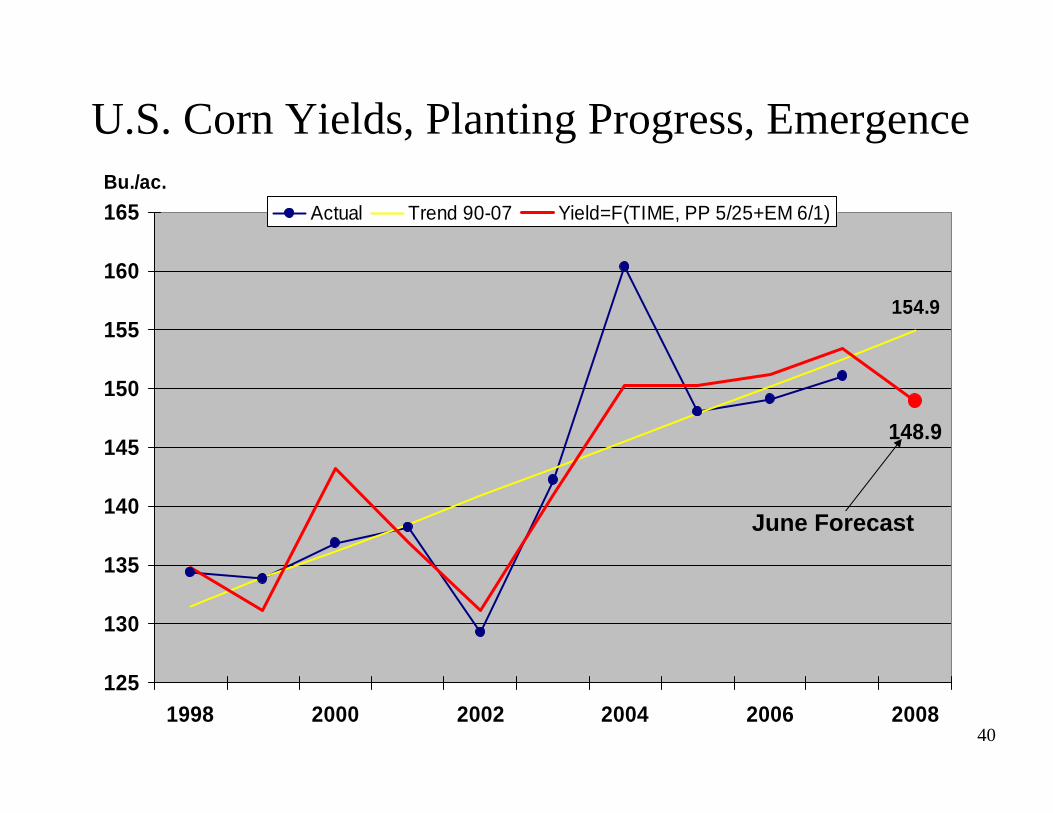

U.S. Corn Yields, Planting Progress, Emergence

154.9

148.9

125

130

135

140

145

150

155

160

165

1998 2000 2002 2004 2006 2008

Bu./ac.Actual Trend 90-07 Yield=F(TIME, PP 5/25+EM 6/1)

June Forecast

41

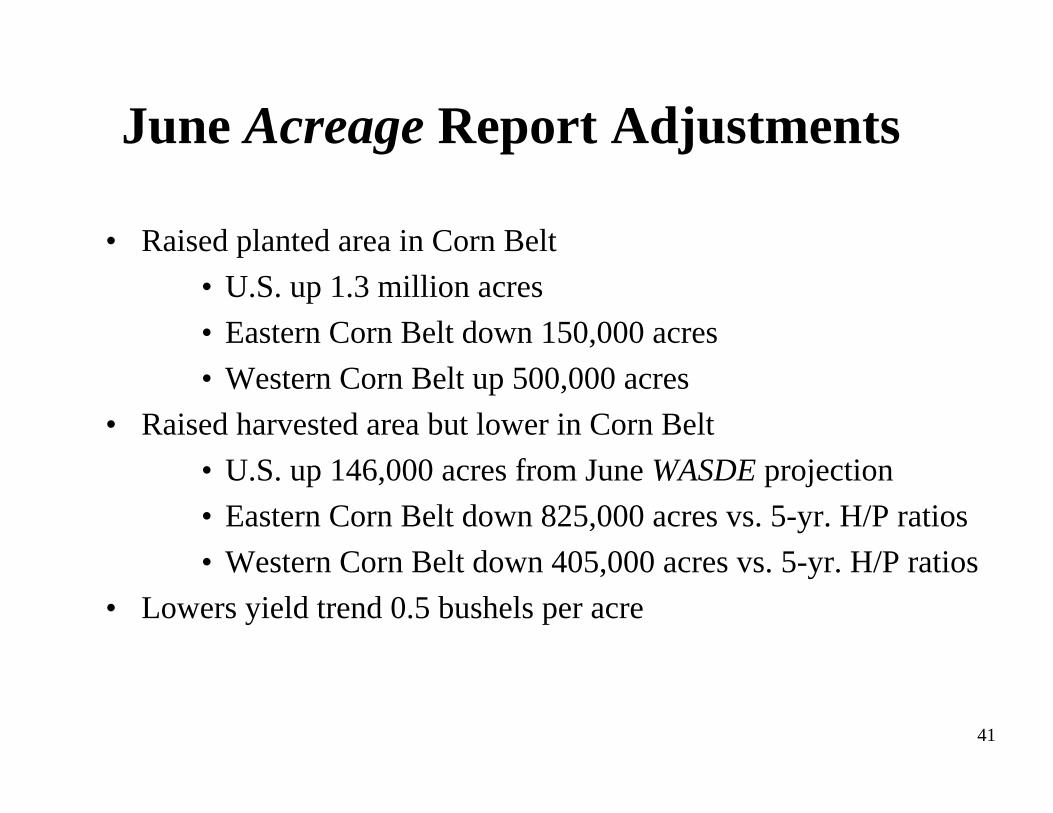

June Acreage Report Adjustments

• Raised planted area in Corn Belt• U.S. up 1.3 million acres• Eastern Corn Belt down 150,000 acres• Western Corn Belt up 500,000 acres

• Raised harvested area but lower in Corn Belt• U.S. up 146,000 acres from June WASDE projection• Eastern Corn Belt down 825,000 acres vs. 5-yr. H/P ratios• Western Corn Belt down 405,000 acres vs. 5-yr. H/P ratios

• Lowers yield trend 0.5 bushels per acre

42

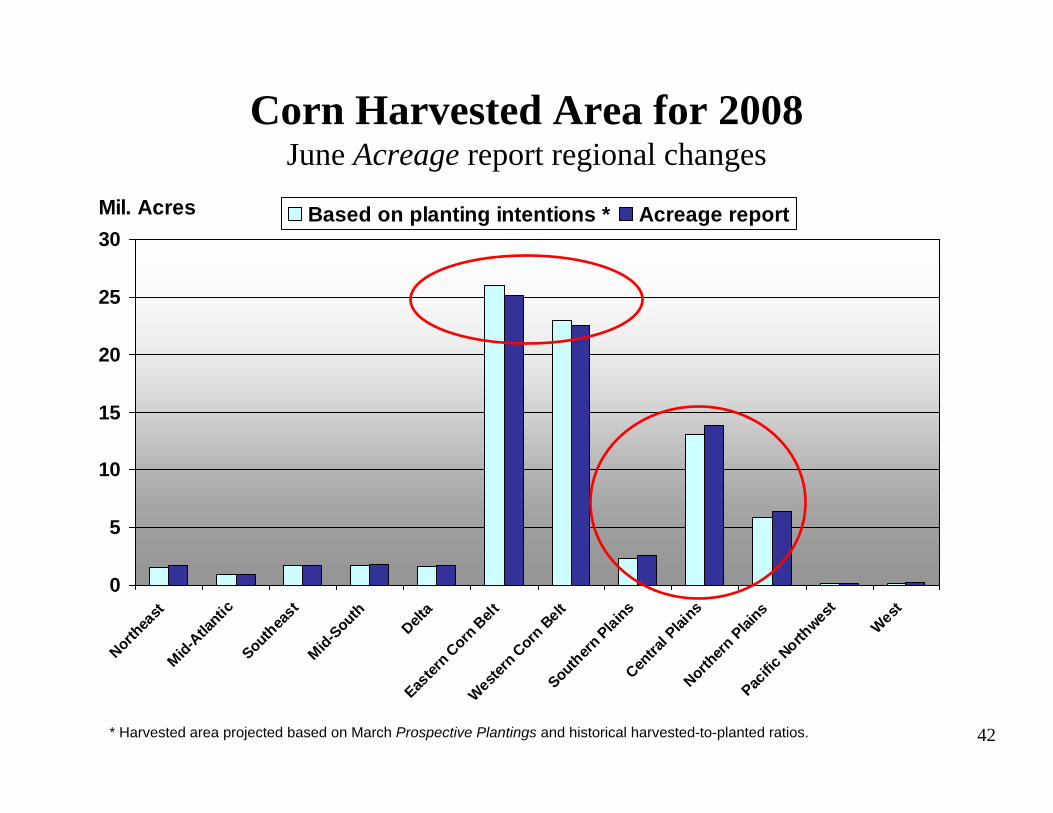

Corn Harvested Area for 2008June Acreage report regional changes

0

5

10

15

20

25

30

Northea

stMid-A

tlantic

Southea

stMid-S

outh

Delta

Easter

n Corn

Belt

Western

Corn

Belt

Southern

PlainsCen

tral P

lains

Northern

Plai

nsPac

ific N

orthwest

West

Mil. Acres Based on planting intentions * Acreage report

* Harvested area projected based on March Prospective Plantings and historical harvested-to-planted ratios.

43

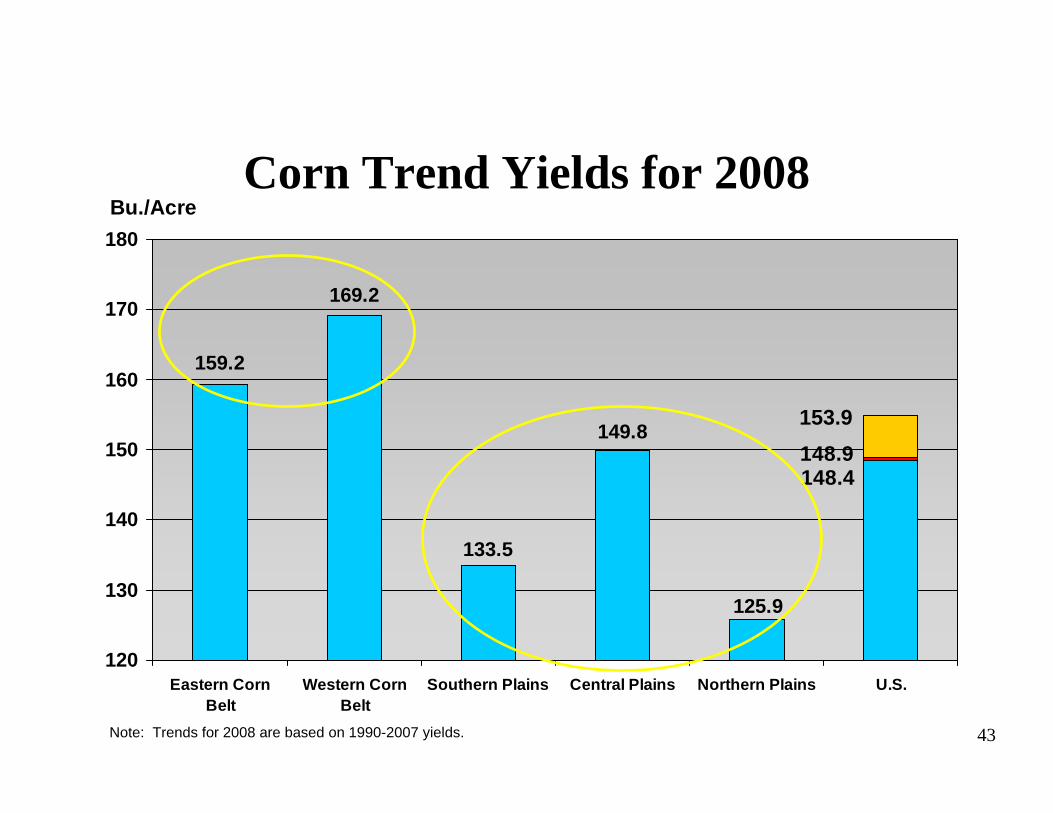

148.4

159.2

169.2

133.5

149.8

125.9

148.9

120

130

140

150

160

170

180

Eastern CornBelt

Western CornBelt

Southern Plains Central Plains Northern Plains U.S.

Bu./AcreCorn Trend Yields for 2008

153.9

Note: Trends for 2008 are based on 1990-2007 yields.

44

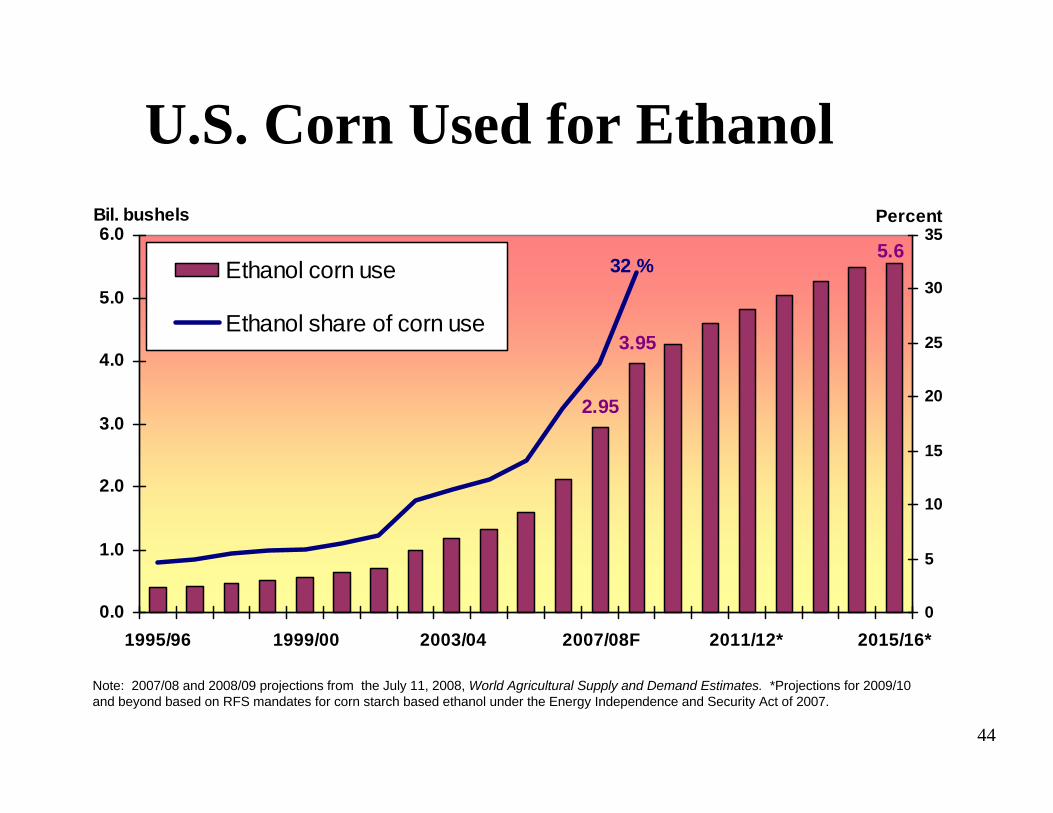

3.95

2.95

5.632 %

0.0

1.0

2.0

3.0

4.0

5.0

6.0

1995/96 1999/00 2003/04 2007/08F 2011/12* 2015/16*

Bil. bushels

0

5

10

15

20

25

30

35Percent

Ethanol corn use

Ethanol share of corn use

Note: 2007/08 and 2008/09 projections from the July 11, 2008, World Agricultural Supply and Demand Estimates. *Projections for 2009/10 and beyond based on RFS mandates for corn starch based ethanol under the Energy Independence and Security Act of 2007.

U.S. Corn Used for Ethanol

45

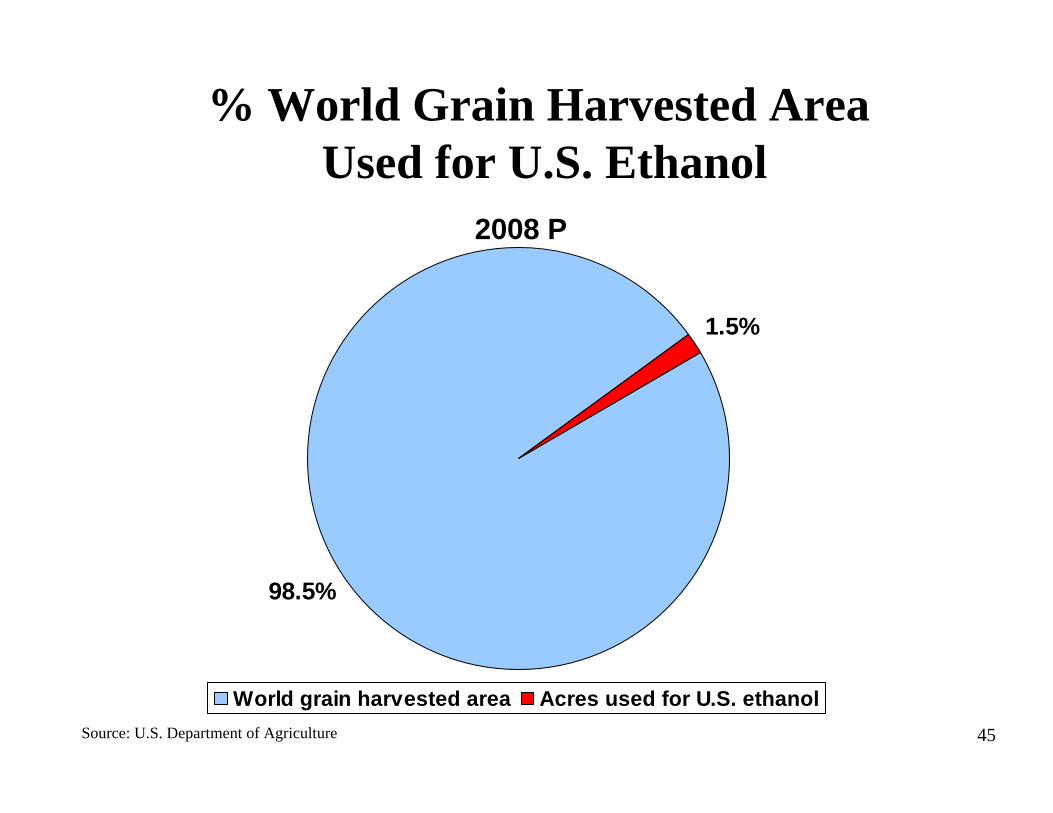

% World Grain Harvested AreaUsed for U.S. Ethanol

2008 P

98.5%

1.5%

World grain harvested area Acres used for U.S. ethanolSource: U.S. Department of Agriculture

46

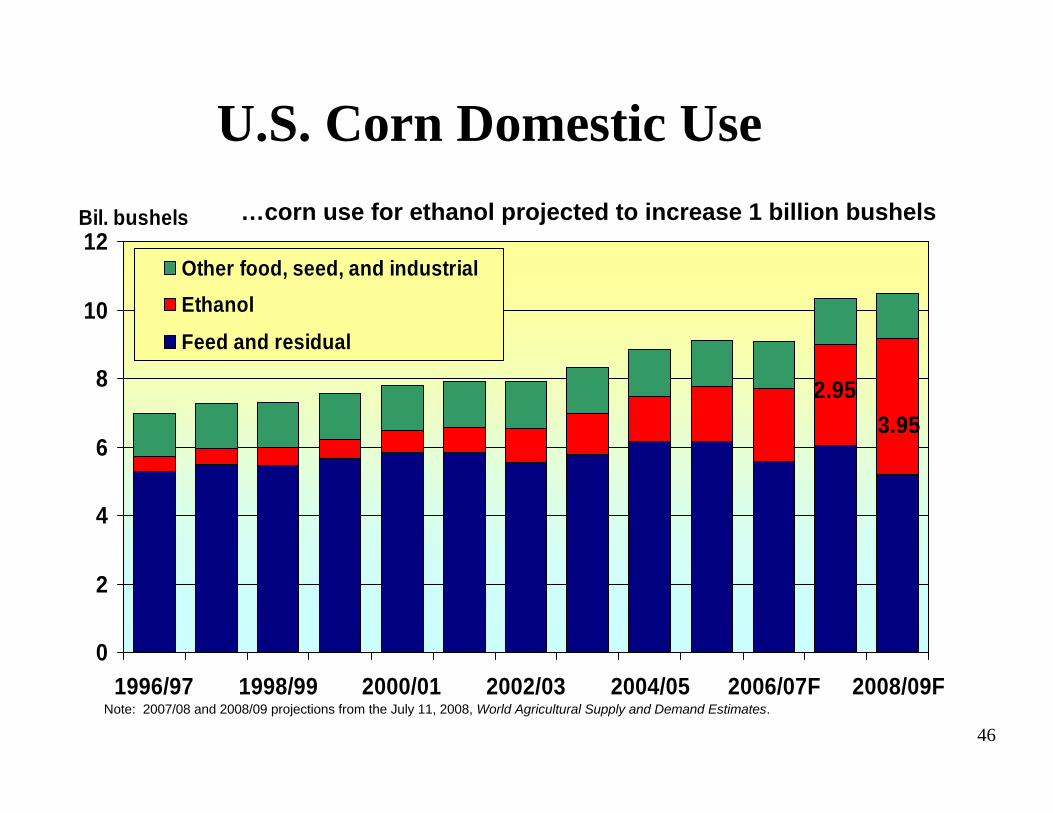

2.953.95

0

2

4

6

8

10

12

1996/97 1998/99 2000/01 2002/03 2004/05 2006/07F 2008/09F

Bil. bushels

Other food, seed, and industrialEthanol

Feed and residual

U.S. Corn Domestic Use

Note: 2007/08 and 2008/09 projections from the July 11, 2008, World Agricultural Supply and Demand Estimates.

…corn use for ethanol projected to increase 1 billion bushels

47

U.S. Feed and Residual Use (Sep-Aug)

0

50

100

150

200

1990/91 1993/94 1996/97 1999/00 2002/03 2005/06 2008/09

Mil. MT Corn Other feed grains Wheat DDGS

Note: 2007/08 and 2008/09 projections from the July 11, 2008, World Agricultural Supply and Demand Estimates.

48

U.S. Biodiesel Mandate (2007 Energy Act)

0

200

400

600

800

1,000

1,200

2000/01 2004/05 2008/09F 2012/13F 2016/17F0

5

10

15

20

25

30

35

Biodiesel Consumption Mandate

Share of Soybean Oil Prod.

Million gallons Percent

14%

Note: 2007/08 and 2008/09 projections from the May 9, 2008, World Agricultural Supply and Demand Estimates. *Projections for 2009/10 and beyond based on RFS mandates under the Energy Independence and Security Act of 2007.

49

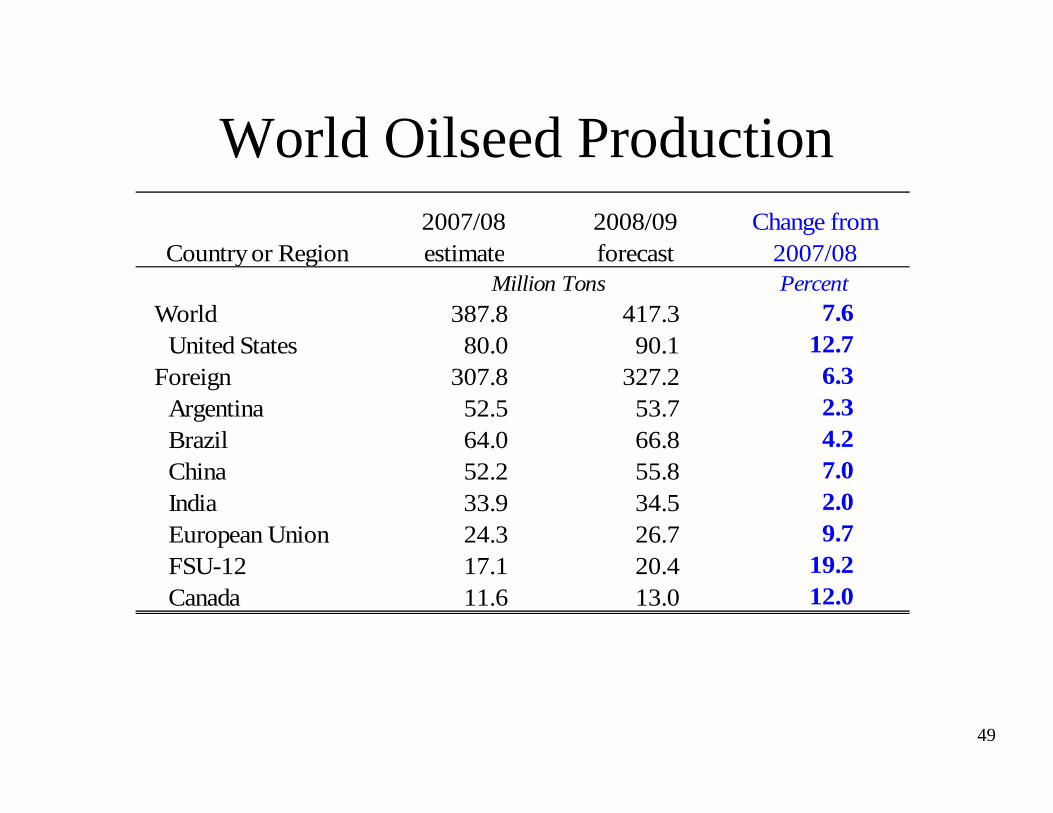

World Oilseed Production

Country or Region2007/08 estimate

2008/09 forecast

Change from 2007/08

Million Tons PercentWorld 387.8 417.3 7.6

United States 80.0 90.1 12.7Foreign 307.8 327.2 6.3

Argentina 52.5 53.7 2.3Brazil 64.0 66.8 4.2China 52.2 55.8 7.0India 33.9 34.5 2.0European Union 24.3 26.7 9.7FSU-12 17.1 20.4 19.2Canada 11.6 13.0 12.0

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

50

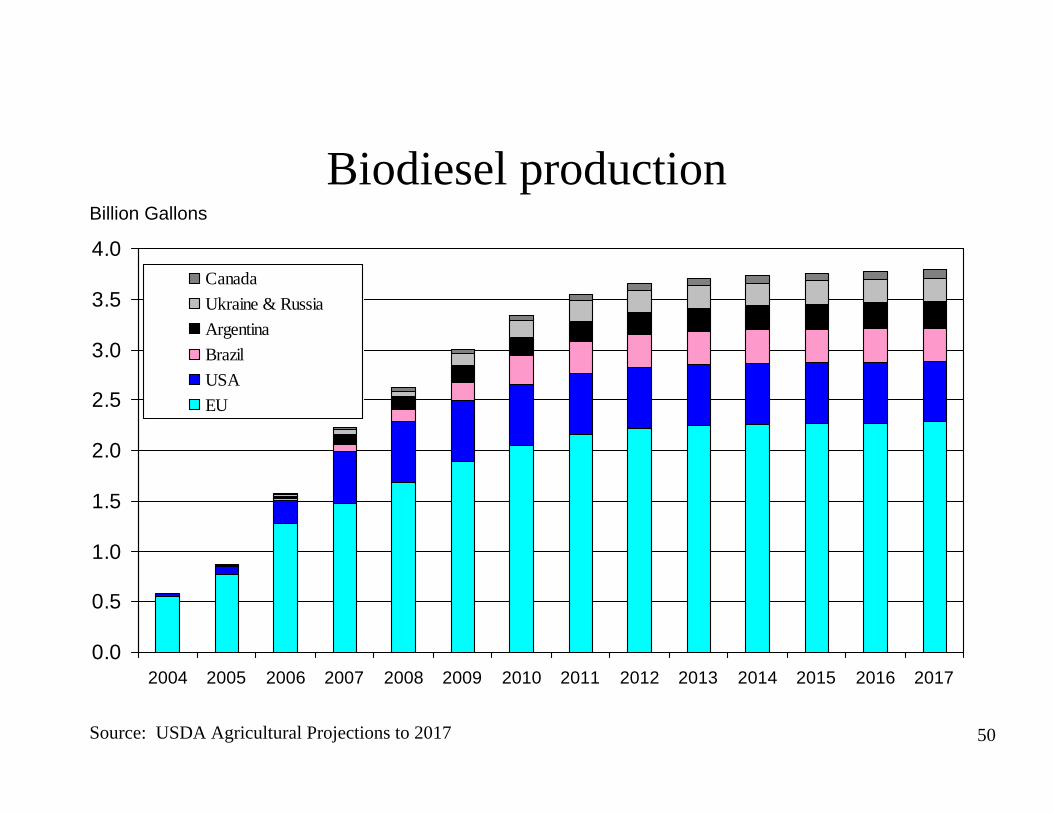

Biodiesel production

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

CanadaUkraine & RussiaArgentinaBrazilUSAEU

Billion Gallons

Source: USDA Agricultural Projections to 2017

51

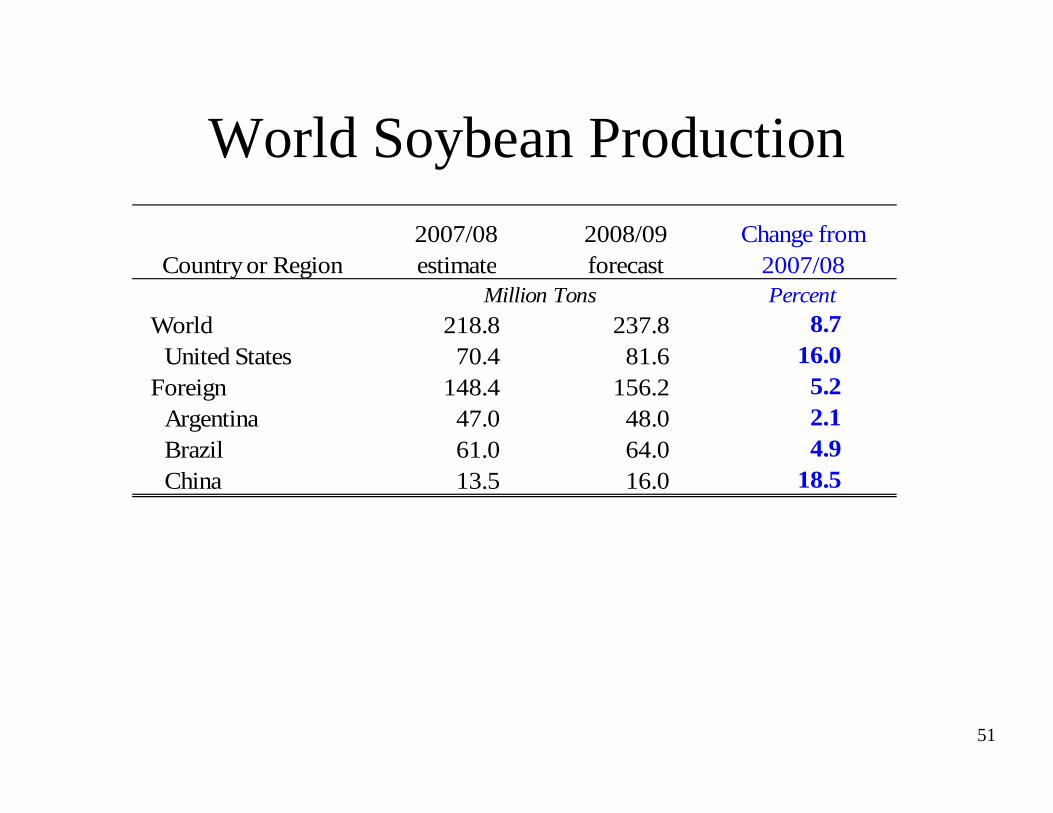

World Soybean Production

Country or Region2007/08 estimate

2008/09 forecast

Change from 2007/08

Million Tons PercentWorld 218.8 237.8 8.7

United States 70.4 81.6 16.0Foreign 148.4 156.2 5.2

Argentina 47.0 48.0 2.1Brazil 61.0 64.0 4.9China 13.5 16.0 18.5

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

52

U.S. Soybean Supply and DemandChange from

2007/08Percent

Planted area (million acres) 63.6 74.5 17.1Harvested area (million acres) 62.8 72.1 14.8Yield (bushels per acre) 41.2 41.6 1.1

Million bushelsBeginning stocks 574 125 -78.2Production 2,585 3,000 16.0Imports 10 10 0.0

Total Supply 3,169 3,135 -1.1Crush 1,840 1,830 -0.5Seed and Residual 59 166 182.2

Domestic use 1,899 1,996 5.1Exports 1,145 1,000 -12.7

Total Use 3,044 2,996 -1.6Ending stocks 125 140 11.5

PercentStocks/use ratio 4.1 4.7

Dollars/bushelAverage market price 10.15 12.00/13.50 25.6

2007/08 estimate

2008/09 forecast

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

53

U.S. Soybean Oil Supply and DemandChange from

2007/08Million pounds Percent

Beginning stocks 3,085 2,930 -5.0Production 21,345 20,860 -2.3Imports 50 50 0.0

Total supply 24,480 23,840 -2.6Domestic use 18,400 18,500 0.5

Methyl ester 2,800 3,000 7.1Exports 3,150 2,650 -15.9

Total use 21,550 21,150 -1.9Ending stocks 2,930 2,690 -8.2

Cents per poundAverage market price 54.50 59.00/63.00 11.9

2007/08 estimate

2008/09 forecast

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

54

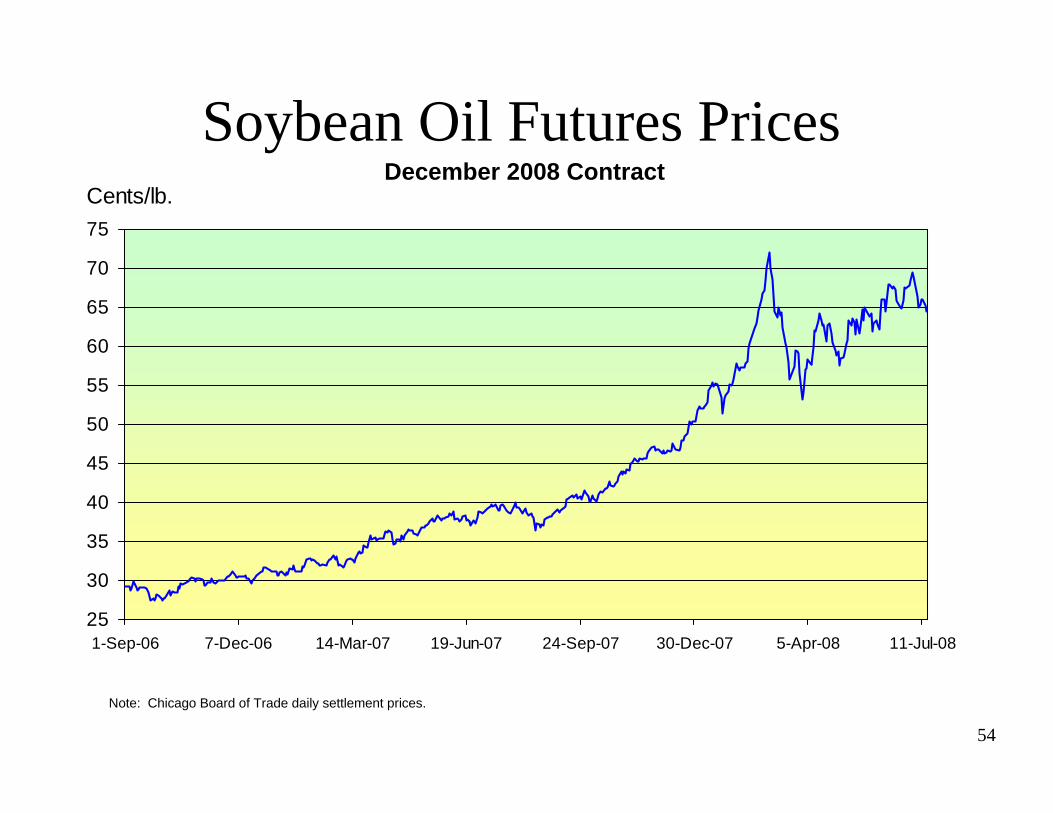

Soybean Oil Futures Prices

25

30

35

40

45

50

55

60

65

70

75

1-Sep-06 7-Dec-06 14-Mar-07 19-Jun-07 24-Sep-07 30-Dec-07 5-Apr-08 11-Jul-08

Cents/lb.

Note: Chicago Board of Trade daily settlement prices.

December 2008 Contract

55

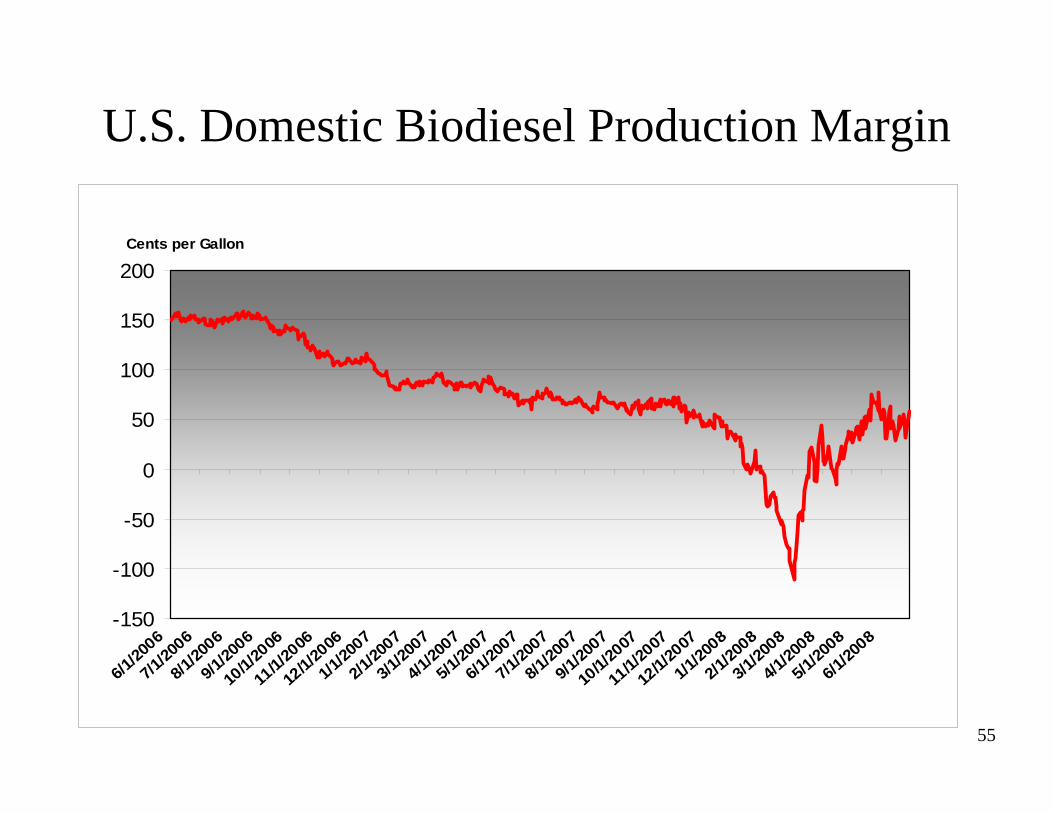

U.S. Domestic Biodiesel Production Margin

-150

-100

-50

0

50

100

150

200

6/1/20

06

7/1/20

06

8/1/20

06

9/1/20

06

10/1/

2006

11/1/

2006

12/1/

2006

1/1/20

07

2/1/20

07

3/1/20

07

4/1/20

07

5/1/20

07

6/1/20

07

7/1/20

07

8/1/20

07

9/1/20

07

10/1/

2007

11/1/

2007

12/1/

2007

1/1/20

08

2/1/20

08

3/1/20

08

4/1/20

08

5/1/20

08

6/1/20

08

Cents per Gallon

56

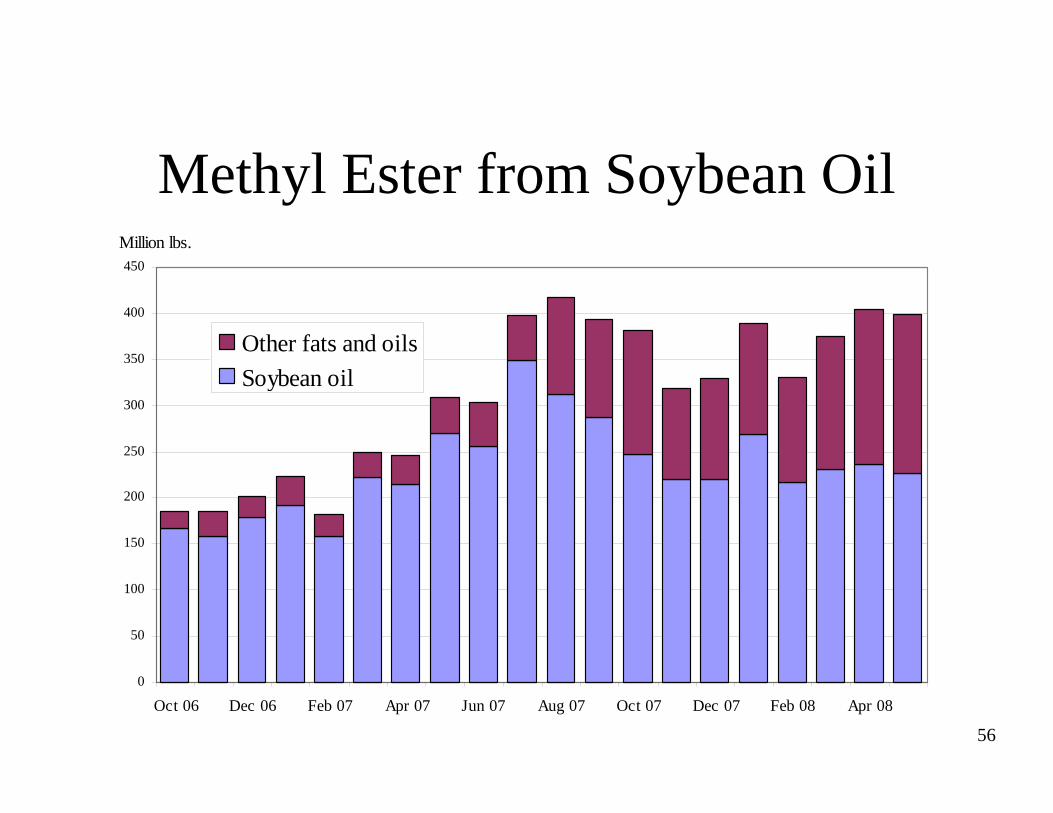

Methyl Ester from Soybean Oil

0

50

100

150

200

250

300

350

400

450

Oct 06 Dec 06 Feb 07 Apr 07 Jun 07 Aug 07 Oct 07 Dec 07 Feb 08 Apr 08

Other fats and oilsSoybean oil

Million lbs.

57

China Soybean Import Dependence Expected to Increase in the Next 10 Years

0

10

20

30

40

50

60

70

80

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 20160

10

20

30

40

50

60

70

80

ImportsProductionImport Dependence

Million Tons Percent

58

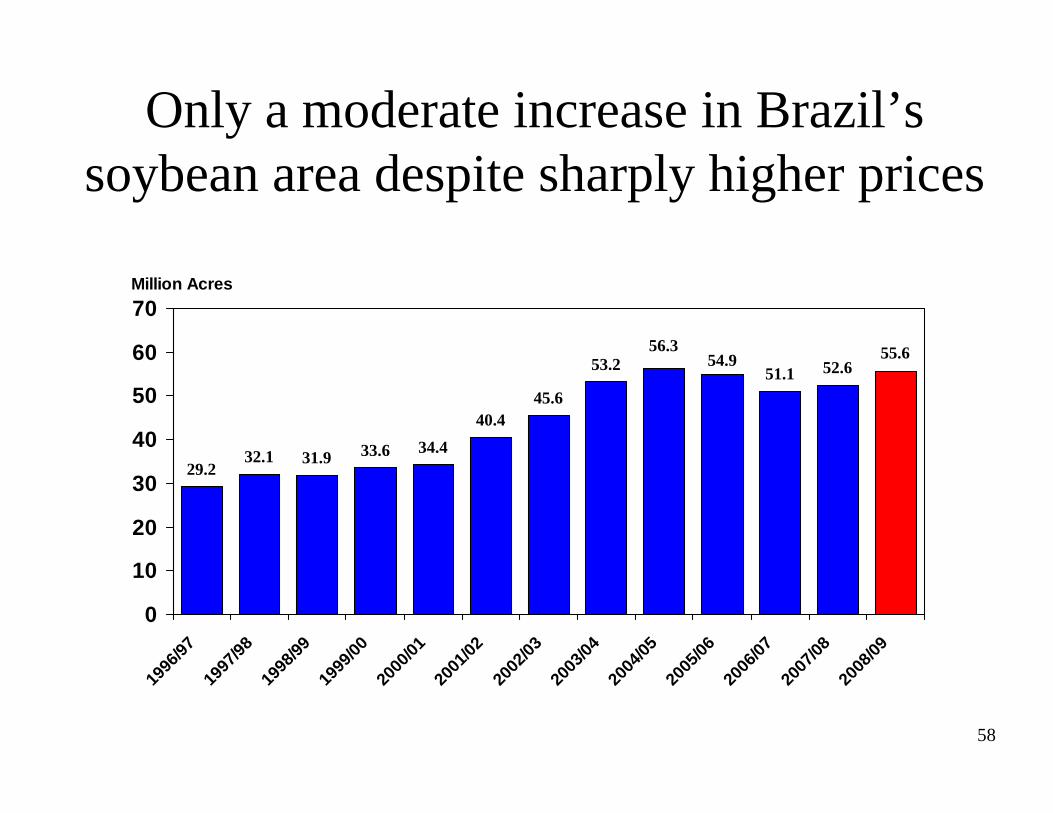

Only a moderate increase in Brazil’s soybean area despite sharply higher prices

29.232.1 31.9 33.6 34.4

40.445.6

53.2 51.1 52.654.956.3 55.6

0

10

20

30

40

50

60

70

1996

/9719

97/98

1998

/9919

99/00

2000

/0120

01/02

2002

/0320

03/04

2004

/0520

05/06

2006

/0720

07/08

2008

/09

Million Acres

59

Effect of Dollar Devaluation on Brazil Soybean Price

5

10

15

20

25

30

35

40

Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08

Reals Per Bushel2004 Rate Current Rate

$13.50/bu

$7.60/bu

$5.50/bu

60

0

25

50

75

100

125

150

175

200

225

250

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

U.S. Brazil Argentina

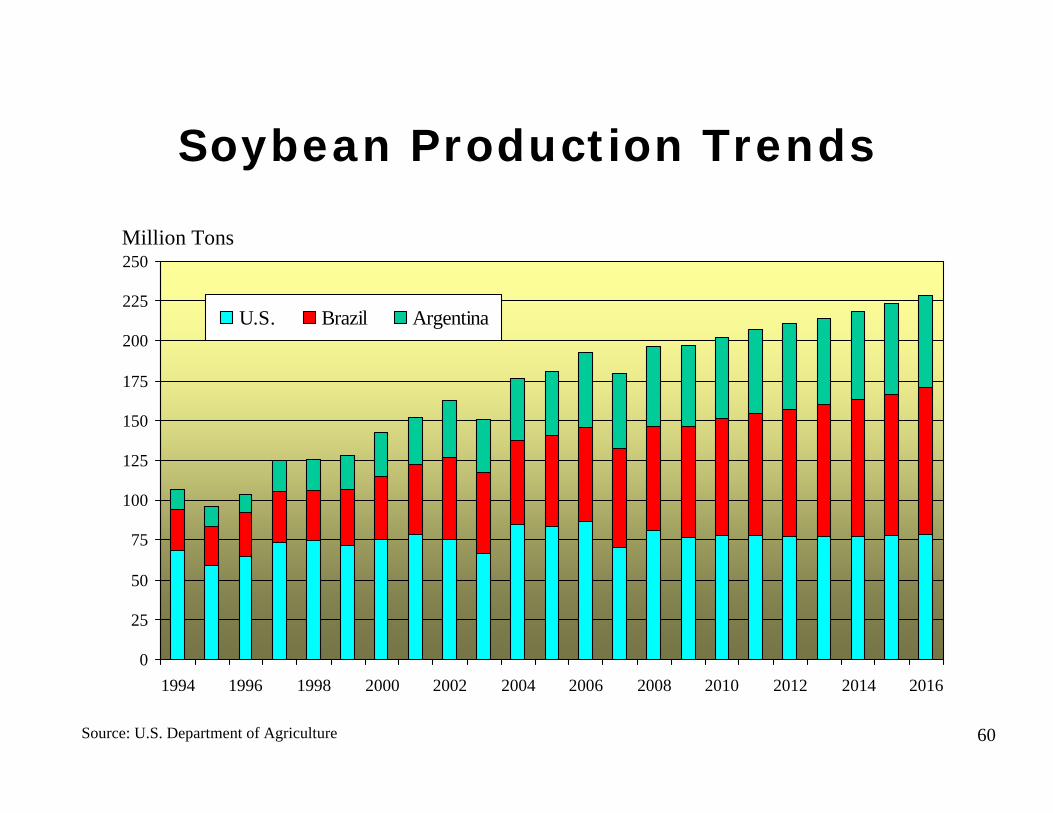

Soybean Production Trends

Million Tons

Source: U.S. Department of Agriculture

61

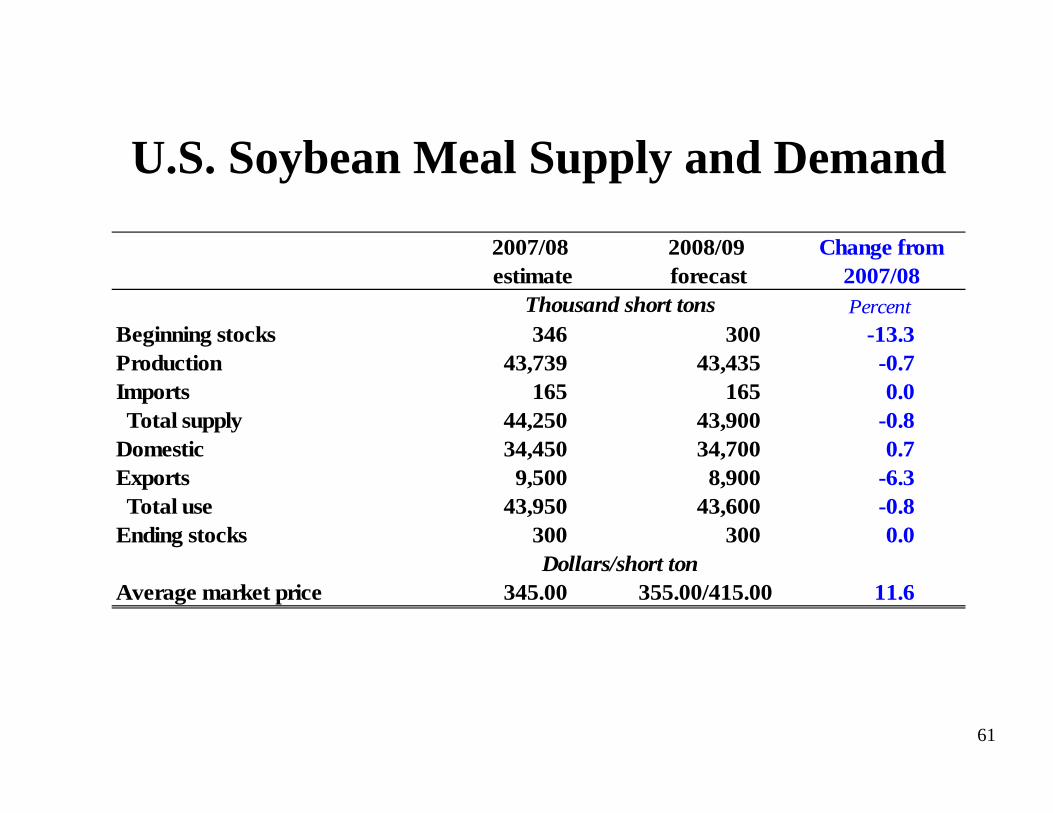

U.S. Soybean Meal Supply and Demand

Change from 2007/08

Thousand short tons PercentBeginning stocks 346 300 -13.3Production 43,739 43,435 -0.7Imports 165 165 0.0 Total supply 44,250 43,900 -0.8Domestic 34,450 34,700 0.7Exports 9,500 8,900 -6.3 Total use 43,950 43,600 -0.8Ending stocks 300 300 0.0

Dollars/short tonAverage market price 345.00 355.00/415.00 11.6

2007/08 estimate

2008/09 forecast

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

62

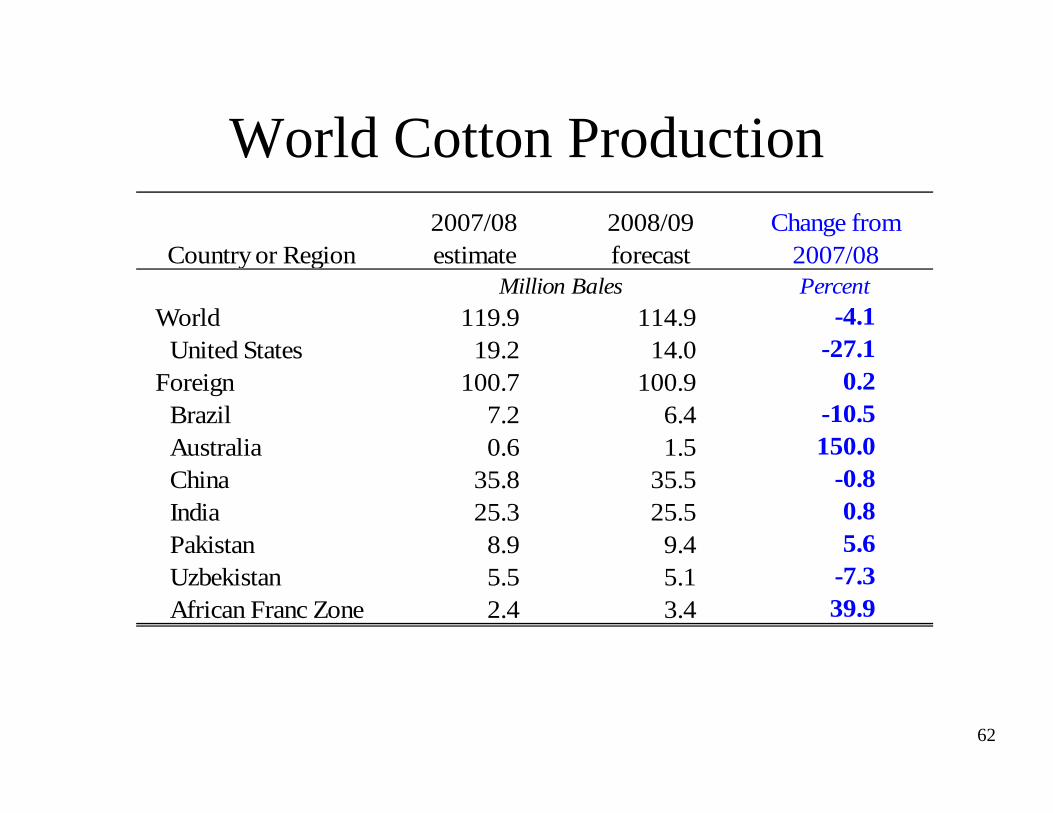

World Cotton Production

Country or Region2007/08 estimate

2008/09 forecast

Change from 2007/08

Million Bales PercentWorld 119.9 114.9 -4.1

United States 19.2 14.0 -27.1Foreign 100.7 100.9 0.2

Brazil 7.2 6.4 -10.5Australia 0.6 1.5 150.0China 35.8 35.5 -0.8India 25.3 25.5 0.8Pakistan 8.9 9.4 5.6Uzbekistan 5.5 5.1 -7.3African Franc Zone 2.4 3.4 39.9

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

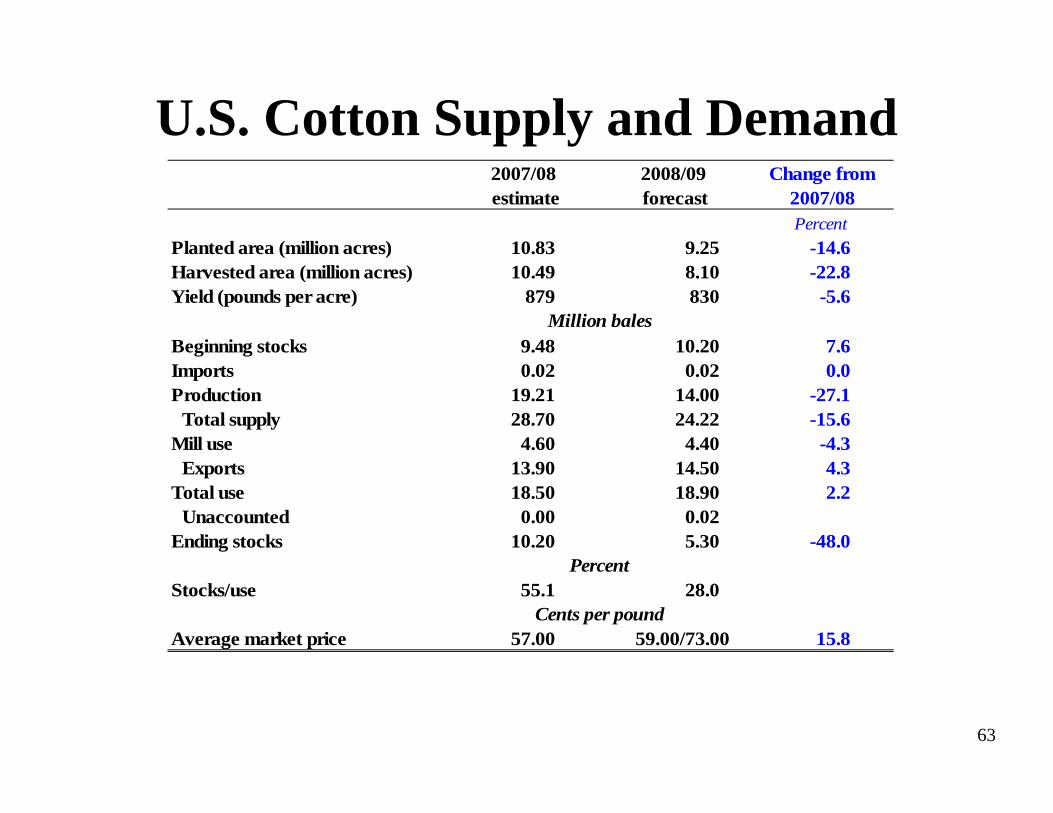

63

U.S. Cotton Supply and DemandChange from

2007/08Percent

Planted area (million acres) 10.83 9.25 -14.6Harvested area (million acres) 10.49 8.10 -22.8Yield (pounds per acre) 879 830 -5.6

Million balesBeginning stocks 9.48 10.20 7.6Imports 0.02 0.02 0.0Production 19.21 14.00 -27.1

Total supply 28.70 24.22 -15.6Mill use 4.60 4.40 -4.3

Exports 13.90 14.50 4.3Total use 18.50 18.90 2.2

Unaccounted 0.00 0.02Ending stocks 10.20 5.30 -48.0

PercentStocks/use 55.1 28.0

Cents per poundAverage market price 57.00 59.00/73.00 15.8

2007/08 estimate

2008/09 forecast

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

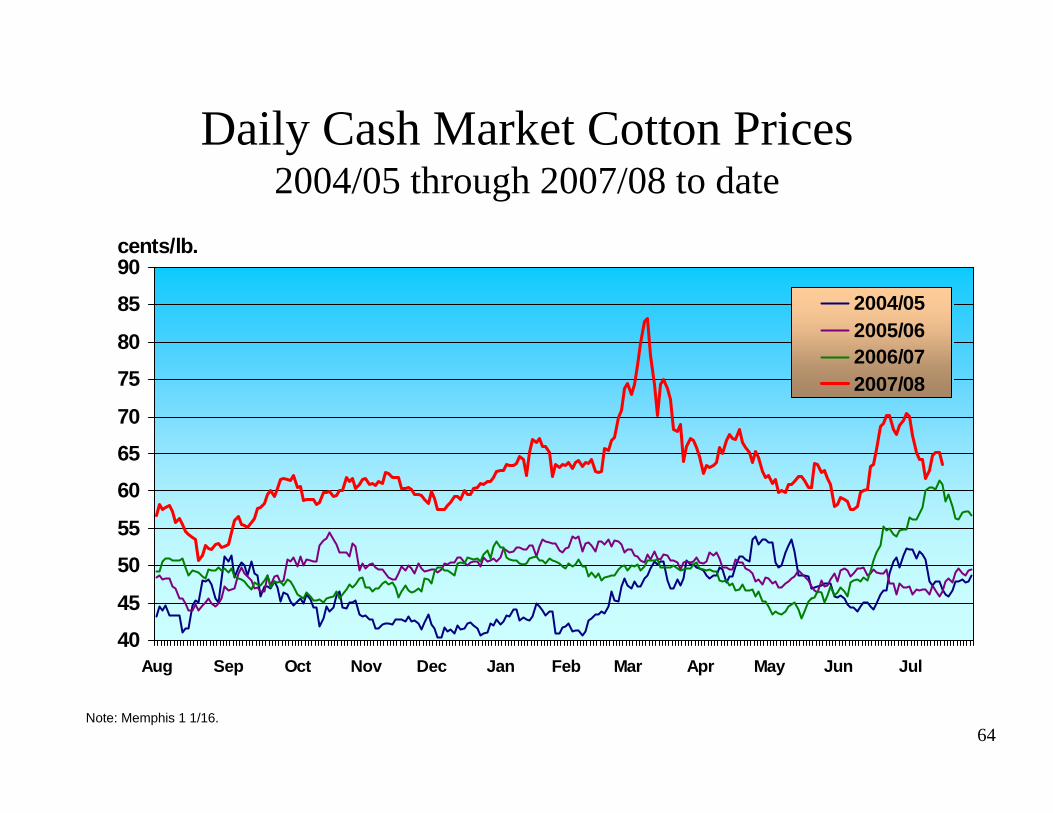

64Note: Memphis 1 1/16.

Daily Cash Market Cotton Prices2004/05 through 2007/08 to date

40

45

50

55

60

65

70

75

80

85

90

Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul

cents/lb.

2004/052005/062006/072007/08

65

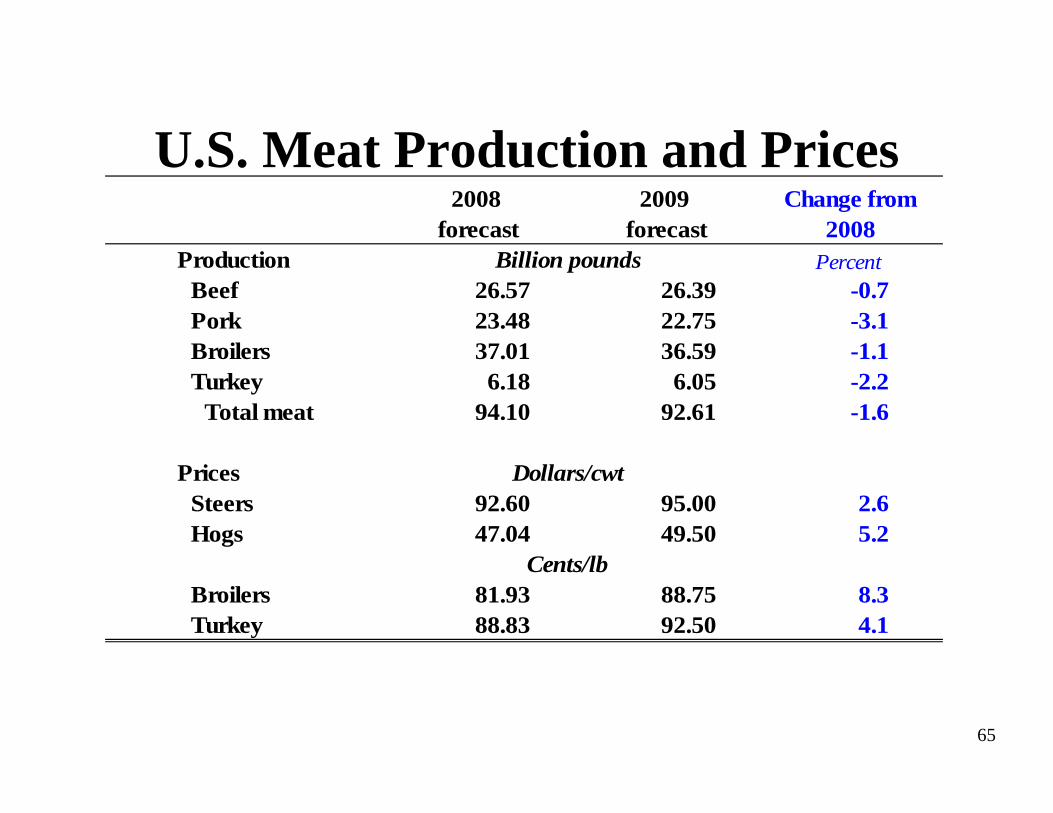

U.S. Meat Production and PricesChange from

2008Production Billion pounds Percent

Beef 26.57 26.39 -0.7Pork 23.48 22.75 -3.1Broilers 37.01 36.59 -1.1Turkey 6.18 6.05 -2.2

Total meat 94.10 92.61 -1.6

Prices Dollars/cwtSteers 92.60 95.00 2.6Hogs 47.04 49.50 5.2

Cents/lbBroilers 81.93 88.75 8.3Turkey 88.83 92.50 4.1

2008 forecast

2009 forecast

Indicates an increase in the estimate or forecast from the previous month.Indicates a decrease in the estimate or forecast from the previous month.

66

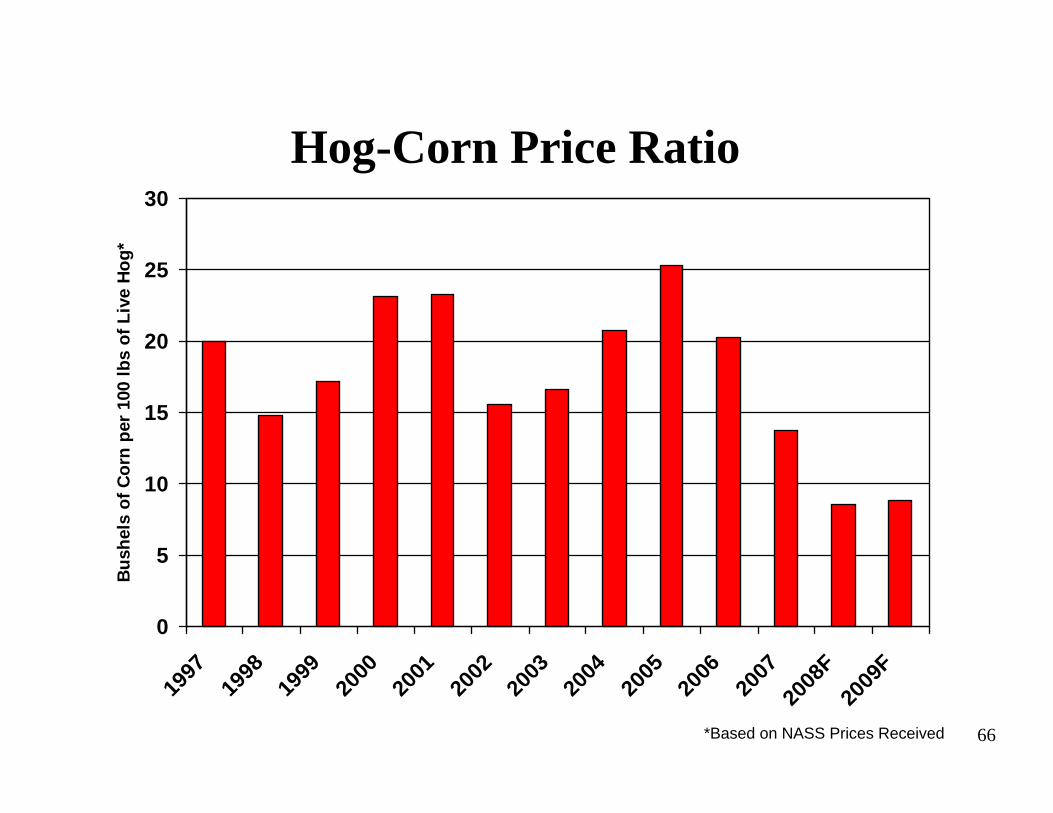

Hog-Corn Price Ratio

0

5

10

15

20

25

30

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

F20

09F

Bush

els

of C

orn

per 1

00 lb

s of

Liv

e Ho

g*

*Based on NASS Prices Received

67

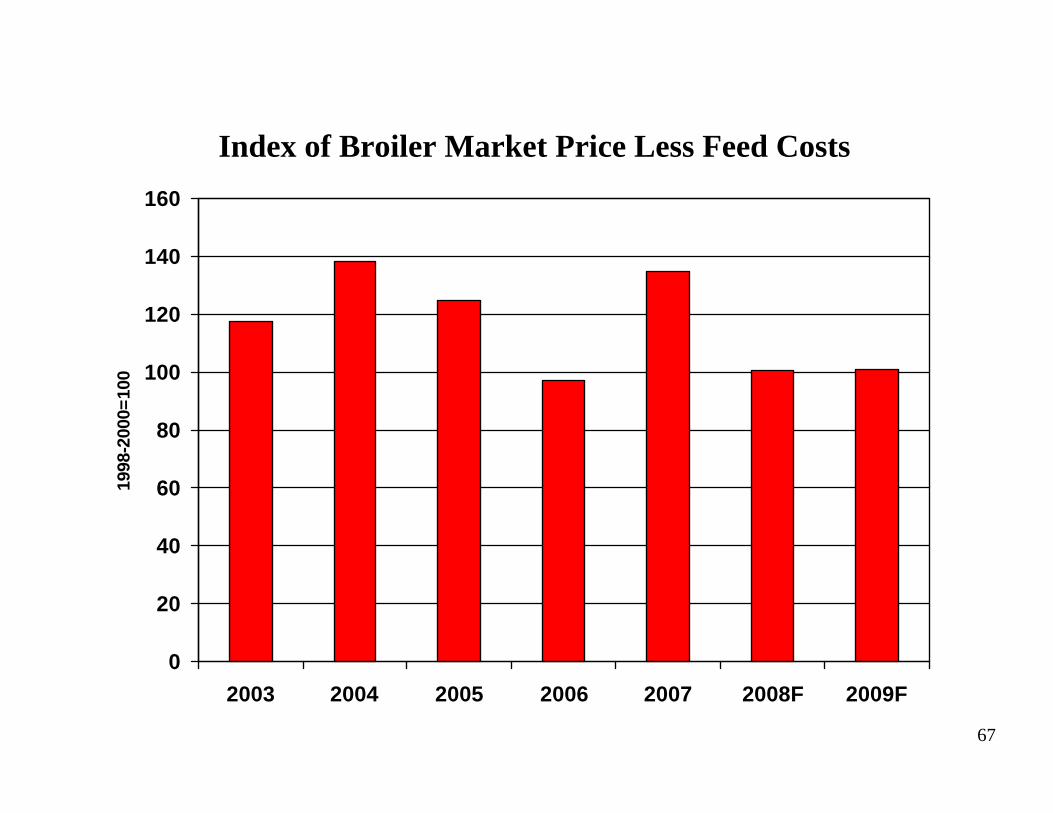

Index of Broiler Market Price Less Feed Costs

0

20

40

60

80

100

120

140

160

2003 2004 2005 2006 2007 2008F 2009F

1998

-200

0=10

0

68

CPI for FoodYear-over-year Change

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008

Percent

69

World Population and Population Growth

0

2

4

6

8

10

12

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 20500.0

0.5

1.0

1.5

2.0

2.5

Billions of persons (midyear)

Growth rate

Billions Percent

Source: U.S. Bureau of the Census

70

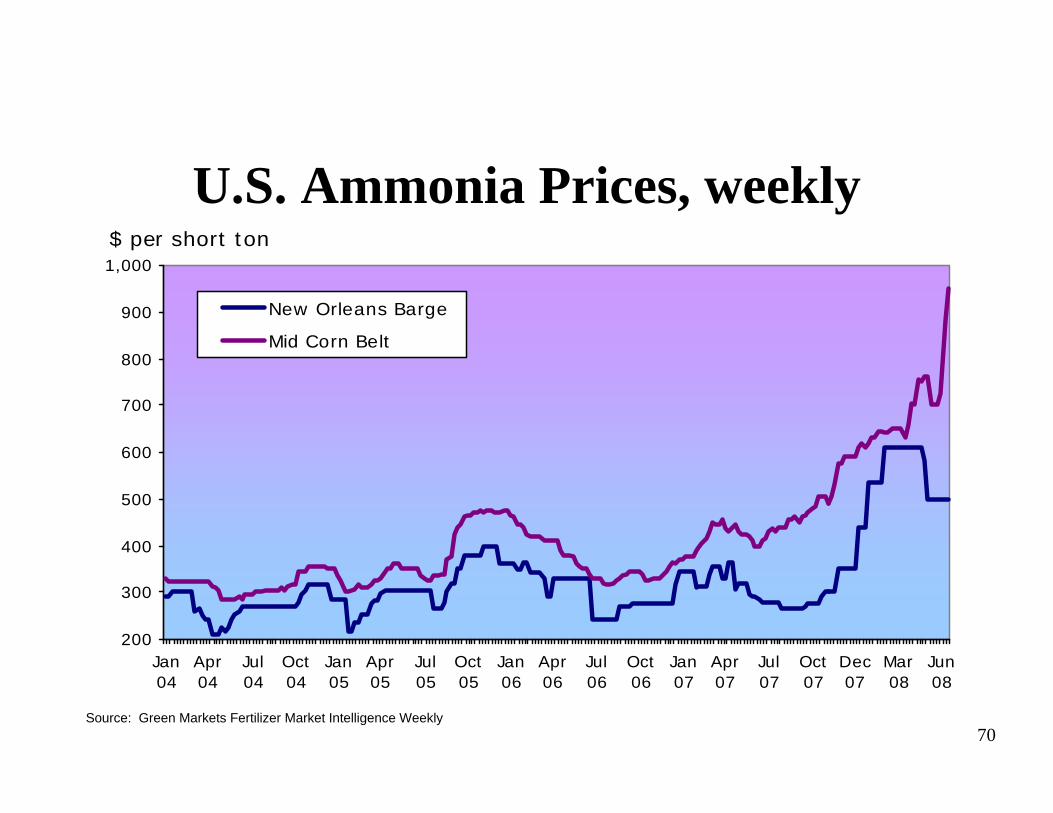

200

300

400

500

600

700

800

900

1,000

Jan04

Apr04

Jul04

Oct04

Jan05

Apr05

Jul05

Oct05

Jan06

Apr06

Jul06

Oct06

Jan07

Apr07

Jul07

Oct07

Dec07

Mar08

Jun08

New Orleans Barge

Mid Corn Belt

$ per short ton

Source: Green Markets Fertilizer Market Intelligence Weekly

U.S. Ammonia Prices, weekly

71

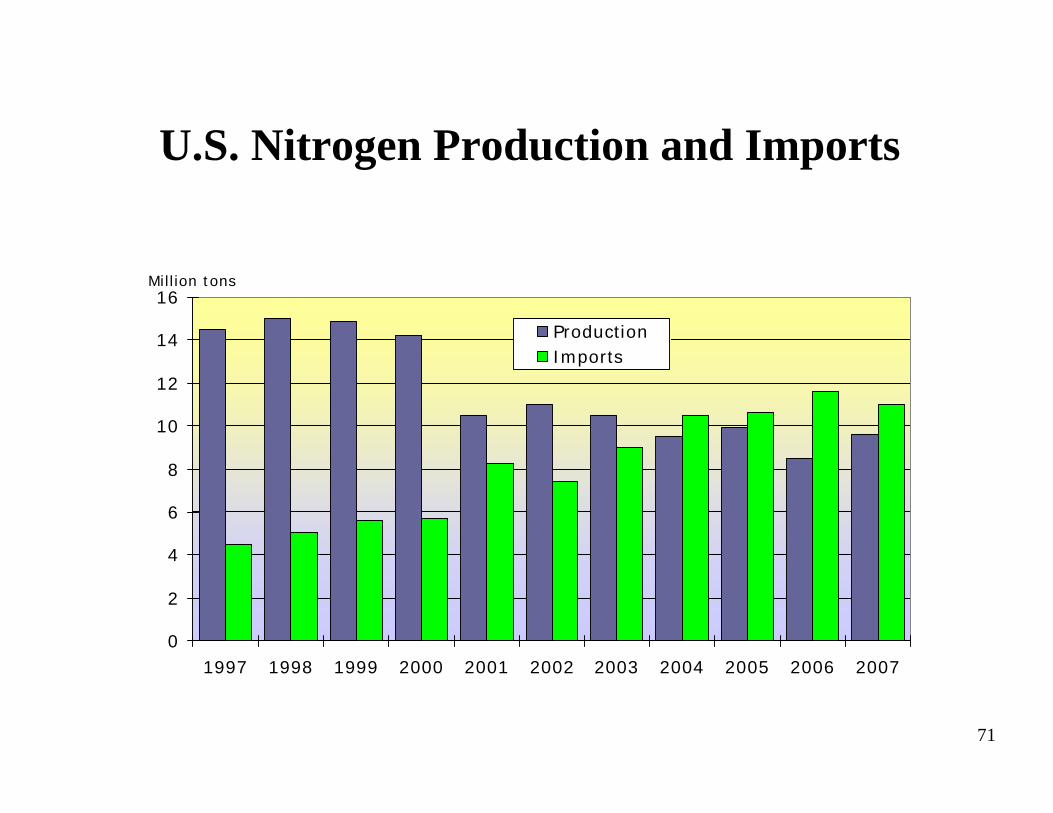

U.S. Nitrogen Production and Imports

0

2

4

6

8

10

12

14

16

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

ProductionImports

Million tons

72

Global Area PlantedIncluding to Plant Biofuel Feedstocks

0

100

200

300

400

500

600

700

800

900

1,000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

HistoryProjectedPlanted to Biofuels

Million hectares

1Crops include:Wheat, Rice, Corn, Barley, Sorghum, Other cereals, Soybeans,Rapeseed, Sunseed, Cotton

Source: Ron Trostle, “Global Agricultural Supply and Demand: Factors Contributing to the Recent Increase in Food Commodity Prices,”USDA, Economic Research Service, May 2008. http://www.ers.usda.gov/Publications/WRS0801/WRS0801.pdf

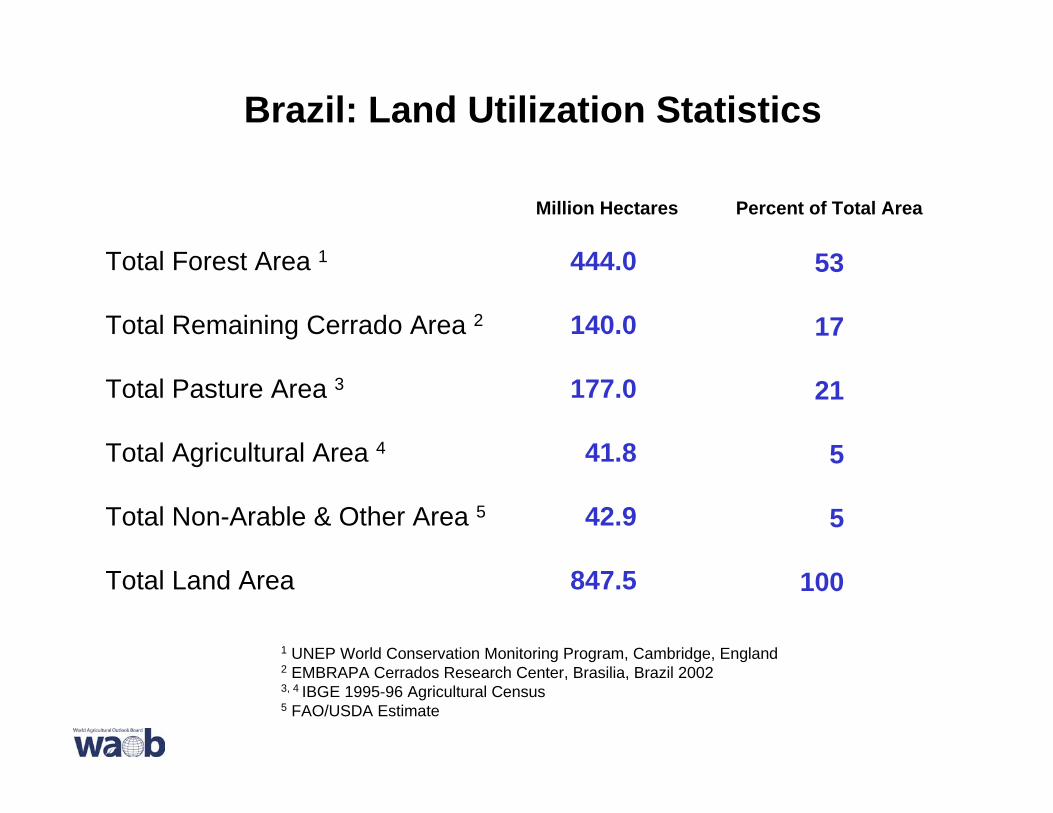

Brazil: Land Utilization Statistics

Total Forest Area 1

Total Remaining Cerrado Area 2

Total Pasture Area 3

Total Agricultural Area 4

Total Non-Arable & Other Area 5

Total Land Area

Million Hectares Percent of Total Area

1 UNEP World Conservation Monitoring Program, Cambridge, England2 EMBRAPA Cerrados Research Center, Brasilia, Brazil 20023, 4 IBGE 1995-96 Agricultural Census5 FAO/USDA Estimate

444.0

140.0

177.0

41.8

42.9

847.5

53

17

21

5

5

100

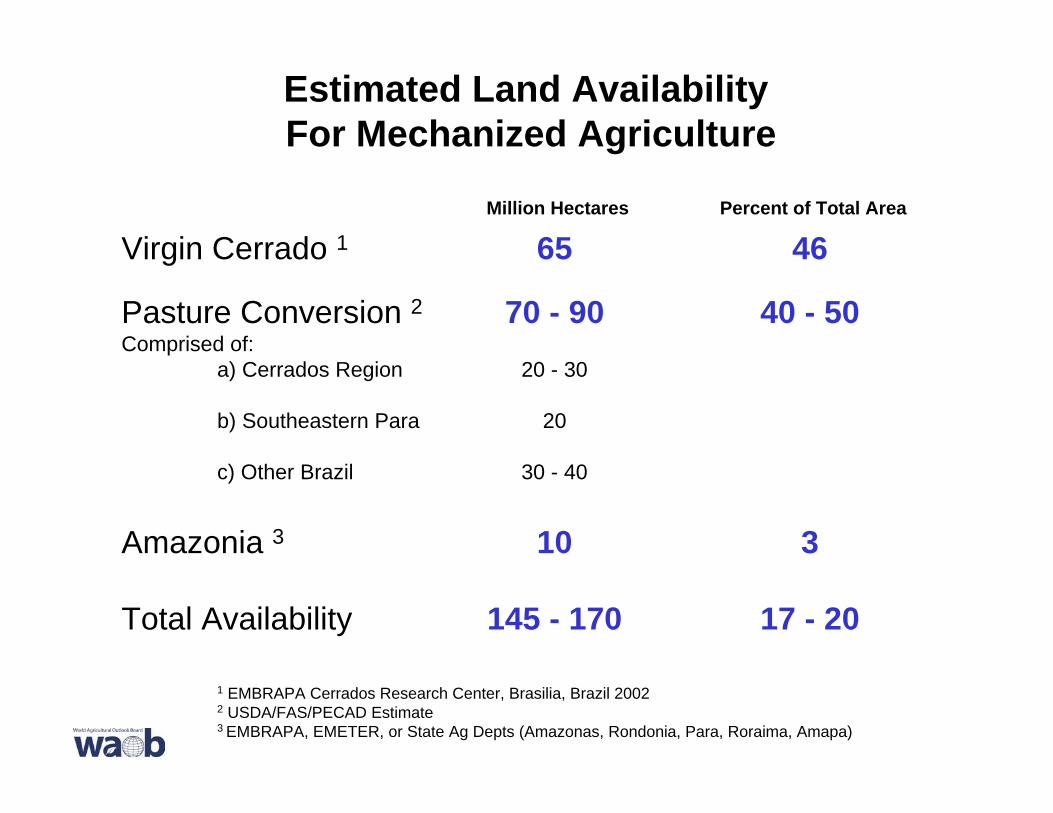

Estimated Land Availability For Mechanized Agriculture

Virgin Cerrado 1

Pasture Conversion 2Comprised of:

a) Cerrados Region

b) Southeastern Para

c) Other Brazil

Amazonia 3

Total Availability

Million Hectares

65

70 - 9020 - 30

20

30 - 40

10

145 - 170

Percent of Total Area

46

40 - 50

3

17 - 20

1 EMBRAPA Cerrados Research Center, Brasilia, Brazil 20022 USDA/FAS/PECAD Estimate3 EMBRAPA, EMETER, or State Ag Depts (Amazonas, Rondonia, Para, Roraima, Amapa)

Feb. 26-27,

End