The Accounting Review -...

52

Securitization and Insider Trading Stephen Ryan Stern School of Business New York University (212) 998-0020 (office) [email protected] Jennifer Wu Tucker Fisher School of Accounting University of Florida (352) 273-0214 (office) [email protected] Ying Zhou School of Business University of Connecticut (860) 486-3019 (office) [email protected] July 2015 Forthcoming, The Accounting Review We thank Stephen Asare, Gauri Bhat (discussant), Stephen V. Brown, Michael Donohoe, Leslie Hodder (the editor), Kathy Rupar, Stanley Veliotis, James Vincent, Dushyant Vyas, two anonymous reviewers, and participants of the 2011 American Accounting Association Annual Meeting and the accounting workshops at the University of Florida, Fordham University, University of International Business and Economics, Shanghai University of Finance and Economics, and Yale University.

Transcript of The Accounting Review -...

Securitization and Insider Trading

Stephen Ryan Stern School of Business

New York University (212) 998-0020 (office)

Jennifer Wu Tucker Fisher School of Accounting

University of Florida (352) 273-0214 (office)

Ying Zhou School of Business

University of Connecticut (860) 486-3019 (office)

July 2015

Forthcoming, The Accounting Review We thank Stephen Asare, Gauri Bhat (discussant), Stephen V. Brown, Michael Donohoe, Leslie Hodder (the editor), Kathy Rupar, Stanley Veliotis, James Vincent, Dushyant Vyas, two anonymous reviewers, and participants of the 2011 American Accounting Association Annual Meeting and the accounting workshops at the University of Florida, Fordham University, University of International Business and Economics, Shanghai University of Finance and Economics, and Yale University.

Securitization and Insider Trading

ABSTRACT: Securitizations are complex and opaque transactions. We hypothesize that bank insiders trade on private information about banks’: (1) securitization-related recourse risks, (2) not-yet-reported current-quarter securitization income, and (3) securitization-based business model sustainability. We provide evidence that proxies for each of these types of insider information are positively associated with insider trading. Specifically, we find that net insider sales in the 2001Q2-2007Q2 pre-financial crisis quarters predict not-yet-reported non-performing securitized loans and securitization income for those quarters and that net insider sales during 2006Q4 predict write-downs of securitization-related assets during the 2007Q3-2008Q4 crisis period. We find that net insider sales are more negatively associated with banks’ subsequent stock returns in their securitization quarters than in other quarters. In supplemental analysis, we show that the above findings are driven by trades by banks’ CEOs and CFOs, and that insiders avoid larger stock price losses through 10b5-1 plan sales than through non-plan sales. Keywords: Securitization, insider trading, opacity, banks. Data availability: All data are available from public sources.

1

I. INTRODUCTION

We examine whether bank insiders exploit private information about an important type of

complex structured-finance transaction, securitization, by trading for personal gain. Financial

reporting requirements portray banks’ securitization-related risks in limited fashions, rendering

these risks opaque to users of financial reports. We expect that bank insiders, particularly top

executives, have informational advantages about these risks that enable profitable trading.

In a typical securitization, the issuer (assumed to be a bank) transfers financial assets to a

special-purpose entity (SPE), which sells asset-backed securities (ABS), i.e., claims to the future

cash flows generated by the securitized assets, to outside investors. The SPE conveys the cash

received from investors to the bank. Banks engage in securitizations for the economic purposes of

transferring risks of the securitized assets and raising funds. Banks for which securitization is a

business model, rather than one-off transactions, generally aim to earn income from securitizations

and to use the cash received to originate securitizable assets on an ongoing basis. Banks also

engage in securitizations for accounting purposes. While the applicable accounting rules have been

tightened over time, banks continue to account for most securitizations as sales with the

securitization SPEs unconsolidated. This accounting leaves the SPEs’ borrowings off the banks’

balance sheets and enables them to report gains on sale that front-load income compared to the

alternative of earning interest income on the securitized assets over time.

We examine securitizations instead of other types of complex financial transactions (e.g.,

hedging) for three reasons. First, securitization is the most common type of structured-finance

transaction. At the end of March 2007, the outstanding principal of ABS in the US equaled $8.9

trillion, compared to $5.4 trillion of corporate bonds and $4.5 trillion of US Treasuries (Cheng,

Dhaliwal, and Neamtiu 2011). Although securitization volume for most asset classes other than

2

agency mortgages fell dramatically during the financial crisis, volume has begun to rebound as the

US economy and financial markets recover.1 Second, banks’ securitization-based business models

worked well before but poorly during the crisis, allowing us to examine large realizations of

downside risks on banks’ existing exposures to these transactions. Third, banks’ public quarterly

regulatory reports contain detailed and standardized data about their securitizations.

Securitization is a contractually and economically complex transaction for which the

issuing banks may be exposed to three types of risk. First, banks always retain some risk of

providing recourse on previously securitized assets (“recourse risks”). Securitizations of credit

risky assets typically create risk-layered tranches of securities and other contractual asset and

liability interests in the securitized assets. Issuing banks often retain risky and illiquid residual

securities to “credit enhance” the senior securities sold to outside investors. Alternatively, banks

may provide non-contractual (“implicit”) recourse. In essentially all securitizations, banks provide

contractual representations and warranties that the securitized assets have the characteristics

specified in the securitization prospectus. Banks violating representations and warranties are

required to buy back the assets at par or other specified amounts if requested by the purchaser.

Although historically viewed as distinct from recourse, buybacks of impaired securitized assets at

prices above fair value due to actual or alleged violations effectively amount to recourse. Second,

banks are exposed to uncertainty about their securitization income for the current period. This

income depends on the prices that investors are willing to pay for the sold ABS and the estimated

fair values of banks’ retained interests. Banks typically do not publicly disclose securitization

1 In 2006, the issuance of mortgage-related ABS was $2.6 trillion (including $1.4 trillion of non-agency mortgages) and of other ABS was $268 billion. By 2010, the issuance of mortgage-related ABS had fallen to $2.0 trillion (including only $69 billion of non-agency mortgages) and of other ABS to $106 billion. In 2013, the issuance of mortgage-related ABS was $2.0 trillion (including $108 billion of non-agency mortgages) and of other ABS was $189 billion. See http://www.sifma.org/research/statistics.aspx.

3

income for a quarter until they file their financial and regulatory reports midway through the

subsequent quarter. Third, banks for which securitization is a business model are exposed to

uncertainty about the sustainability of this model, which requires continuing access to financing

on acceptable terms that can evaporate quickly in credit crunches.

Our study is motivated by and contributes to both the securitization and insider trading

literatures. The former literature finds that securitizations accounted for as sales have attributes of

both secured borrowings and sales (Niu and Richardson 2006; Landsman, Peasnell, and

Shakespeare 2008; Chen, Liu, and Ryan 2008). Issuers time these securitizations to window-dress

their balance sheets and manipulate reported earnings (Dechow and Shakespeare 2009; Dechow,

Myers, and Shakespeare 2010).2 Due to their complex economics and accounting, securitizations

contribute to banks’ opacity (Cheng et al. 2011). We extend this literature, especially Cheng et al.,

by examining how bank insiders exploit their securitization-related information advantages

through trading. The later literature finds that insiders trade before significant price movements

and the public disclosure of earnings (Lakonishok and Lee 2001; Ke, Huddart, and Petroni 2003).

Few studies in this literature examine specific sources of insiders’ information advantage,

however. A notable exception is Aboody and Lev (2000), who identify research and development

(R&D) as a source of private information and find higher insider trading profits at R&D-intensive

firms than at other firms. By examining specific sources of insiders’ private information,

researchers can identify and test for direct links between that information and insiders’ trading.

Such tests help policymakers identify gaps in required disclosures and thereby limit insider trading.

We extend this literature by examining securitizations as a source of bank insiders’ private

information.

2 Barth and Taylor (2010) question whether Dechow et al.’s (2010) findings are attributable to earnings management.

4

To mitigate self-selection issues, our full sample includes bank holding companies only if

they report securitized assets outstanding or non-zero securitization income in at least one quarter

during our full sample period of 2001Q2-2007Q2. We view securitization as a feasible choice for

these “Securitization Banks.” We identify subsamples that correspond to the three types of

securitization-related risks about which we expect insiders to have private information. The

“Recourse Risk” subsample includes all bank-quarters with securitized assets outstanding at the

end of the quarter; insiders in this subsample have private information about the banks’ recourse

risks. The “Securitization Income” subsample includes all bank-quarters with non-zero

securitization income reported for the current quarter or the previous quarter; insiders in this

subsample have private information about the banks’ securitization income. The “Crisis”

subsample includes all banks with non-zero securitized assets outstanding or securitization income

in 2006Q4 on the verge of the financial crisis;3 insiders in this subsample have private information

about the (non)sustainability of the banks’ securitization business models.

We develop three hypotheses about the association between bank insiders’ securitization-

related private information and their insider trading that we test using the relevant subsamples and

proxies for bank insiders’ private information about the specific risks involved. First, we

hypothesize that bank insiders’ securitization-related private information in a quarter is

contemporaneously positively associated with their trading volume in that quarter. We test this

hypothesis using the Recourse Risk and Securitization Income subsamples. In the Recourse Risk

subsample analysis, we proxy for insiders’ private information about recourse risks using quarter-

end securitized assets, non-performing securitized loans, and retained securities, as well as charge-

3 The financial crisis unfolded in waves, with the first wave (the subprime crisis) arriving with the announcement of significant losses on subprime mortgage-related positions by New Century Financial and HSBC Holdings on February 4, 2007 (Ryan 2008).

5

offs of securitized loans during the quarter. In the Securitization Income subsample analysis, we

proxy for insiders’ private information about current-quarter securitization income using the

absolute value of unexpected securitization income. As predicted, we find that these proxies are

positively associated with bank insiders’ trading volume. This association is stronger for trades by

banks’ CEOs and CFOs, who are more likely to possess private information, than by other insiders,

and for the type of securitized assets most subject to implicit recourse, revolving consumer loans,

than for other types of securitized assets.4

Second, we hypothesize that net insider sales during a quarter predict unexpected values of

specified securitization-related performance measures for that quarter or subsequent quarters that

are reported after quarter end. This hypothesis differs from the first in examining the direction of

insider trades as well as the predictive implications of these trades. We test this hypothesis using

all three subsamples. In the Recourse Risk subsample analysis, we examine whether net insider

sales predict unexpected non-performing securitized loans for the quarter. We find a significant

positive association for trades by CEOs and CFOs but not by other insiders. In the Securitization

Income subsample analysis, we examine whether net insider sales predict unexpected

securitization income for the quarter. We find a significantly negative association, again driven by

CEO/CFO trades. In contrast, we do not find any association between net insider sales and

unexpected non-securitization income. In the Crisis subsample analysis, we examine whether net

insider sales in 2006Q4 predict write-downs of securitization-related assets during the financial

crisis period of 2007Q3-2008Q4, our proxy for the breakdown of banks’ securitization-related

business model during the crisis,5 and find this is the case. Hence, bank insiders appear to trade on

4 See Chen et al. (2008) for discussion of how implicit recourse applies only to certain types of securitized assets. 5 Ideally, we would use decreases in securitization volume and/or income (rather than write-downs of preexisting securitization-related exposures) during the financial crisis as proxies for the breakdown of banks’ securitization-related business model during the crisis. Such alternative proxies are difficult to develop and employ effectively,

6

specific types of securitization-related private information. In contrast, we do not find any relation

between net insider sales and write-downs of non-securitization assets during the crisis.

Third, we hypothesize that bank insiders profit from trading on securitization-related

private information. Using the Recourse Risk and Securitization Income subsamples, we find

economically and statistically significant negative abnormal stock returns for the three and six

months after insider sales. For example, the median six-month stock return is -2.4% (-3.9%) for

the Recourse Risk (Securitization Income) subsample. Abnormal returns after insider purchases

are consistently positive in both subsamples, but exhibit smaller magnitudes than after sales. The

Recourse Risk and Securitization Income subsamples exhibit significantly more negative

abnormal returns after insider sales than does a Control subsample that is comprised of

Securitization Banks’ quarters without securitization activity. Furthermore, abnormal returns are

significantly more negative after sales by CEOs and CFOs than by other insiders. Hence, bank

insiders appear to avoid significant losses by selling shares before unfavorable securitization-

related news becomes public.

The Crisis subsample provides a vivid example of insiders selling early to avoid losses.

Banks’ securitization-based business models became compromised as the performance of

subprime mortgages and other types of credit risky assets began to deteriorate before the financial

crisis and the availability of financing evaporated early in the crisis. Due to banks’ central role in

originating, holding, and securitizing these credit risky assets, bank managers were among the first

market participants to observe these adverse events. Crisis subsample banks experienced an

average raw return of -64.8% during 2007-2008, 31.7% more negative than the market and 4.7%

however, due to limitations of Y-9C report data (e.g., amounts for unaffected agency and highly affected non-agency mortgage securitizations are not disaggregated), the occurrence of non-trivial apparent “fire sale” securitization volume during the crisis, and the attrition of the 33 Crisis subsample observations as the crisis unfolds.

7

more negative than similarly sized banks. Net insider sales by bank insiders in the Crisis subsample

totaled $1.19 billion in 2006Q4, over twice the amount in any other sample quarter; these sales

enabled the insiders to avoid losses of $0.99 billion during the crisis.

We conduct two supplemental analyses. First, we investigate the role of litigation risk in

securitization-related insider sales. Beginning in October 2000, the SEC allows insider sales under

10b5-1 plans that provide insiders with affirmative defenses against allegations of insider trading.

Prior research finds that insiders avoid larger losses through 10b5-1 plan sales than through non-

plan sales, consistent with these plans being used for private-information-based trades (Jagolinzer

2009; Shon and Veliotis 2013). We observe that 98.3% of plan sales for our full sample occur in

securitization quarters when we expect bank insiders to possess securitization-related private

information. We find that the significant negative stock returns after insider sales in securitization

quarters are driven by plan sales rather than by non-plan sales. Moreover, plan sales constitute

47% of sales by banks’ CEOs and CFOs but only 23% of sales by other bank insiders, enabling

CEOs and CFOs to avoid more losses than do other insiders. Hence, bank insiders appear to sell

shares under 10b5-1 plans to provide cover for information-based trades, thereby mitigating

litigation risk.

Second, we test the claim that insider trading benefits investors by impounding insiders’

private information more quickly into stock prices (Manne 1970; Boudreaux 2009) using the future

earnings response coefficient (FERC) framework (Collins, Kothari, Shanken and Sloan 1994;

Tucker and Zarowin 2006). We find that securitization and insider trading each separately reduce

the informativeness of price with respect to future earnings and that insider trading does not alter

the effect of securitization on this price informativeness. Hence, we find no evidence that

securitization-related insider trading benefits investors.

8

We believe our findings have implications for policy makers and investors. Our findings

suggest that complex structured-finance transactions such as securitizations require greater

scrutiny from the SEC in enforcing insider trading rules and from investors in analyzing banks’

financial reports. In addition to their current approach of requiring firms to describe existing

securitizations in detail, the SEC and FASB should consider requiring MD&A or financial

statement note disclosures that reveal bank managers’ information about the likelihood of banks’

future losses from providing recourse on securitizations and the sustainability of their

securitization-based business models.

The rest of the paper is organized as follows. Section II develops our hypotheses. Section

III describes the sample and data. Section IV presents the research designs and test results. Section

V provides supplemental analyses. Section VI concludes.

II. HYPOTHESIS DEVELOPMENT

Since the effective date of SFAS 125 in 1997, banks account for securitizations in which

they cede control over the securitized assets as sales rather than as secured borrowings.6 Although

the FASB tightened the requirements for sale accounting with SFAS 140 and SFAS 166, in

practice banks continue to account for most securitizations as sales (Dechow et al. 2010). Under

sale accounting, banks initially recognize retained interests at fair value.7 For illiquid interests,

banks must estimate fair value using internally developed or vendor models that banks do not (and

6 For simplicity, we assume that banks do not consolidate securitization SPEs, as is usually the case, although the issuance of SFAS 167 made consolidation of certain types of SPEs (e.g., credit card master trusts and asset-backed commercial paper conduits) more common starting in 2010. Sale accounting with consolidation of securitization SPEs effectively yields secured-borrowing accounting for the consolidated entity. 7 The types of retained interests that GAAP requires to be recognized at fair value at the time of sale have expanded over time. SFAS 125 and SFAS 140 required initial fair value measurement only for retained liability interests. SFAS 156 added servicing rights and SFAS 166 added all other asset interests. Before SFAS 166, GAAP required retained asset interests not required to be fair valued to be initially recognized at relative-fair-value-based allocations of the amortized cost basis of the securitized assets at the time of sale.

9

likely cannot feasibly) fully describe in their financial reports. Holding a transaction constant, the

valuation of retained interests directly and fully determines securitization income for that

transaction: a dollar higher fair value assigned to a retained asset (liability) yields a dollar higher

(lower) securitization gain on sale. For example, underestimation of default rates at the time of

securitization increases the fair value of any retained junior securities and decreases the fair value

of any recourse liability, thereby increasing the gain on sale.

SFAS 140, effective in 2001, requires banks to disclose considerable information about

their securitizations including: (1) the cash received and gains on sale recognized from securitizing

assets by major asset type; (2) the fair value of each type of retained interests at the end of each

reporting period; and (3) the sensitivity of these valuations to changes in key estimates. SFAS 166

and SFAS 167, effective in 2010, expanded these required disclosures, especially about continuing

involvements with securitized assets. Oz (2013) finds that these additional disclosures have

improved the information available to investors.

Despite these findings, significant aspects of securitization remain opaque to investors due

to four limitations of securitization disclosures. First, banks describe securitized assets in

aggregated and incomplete fashions in their financial reports and even in their securitization

prospectuses. For example, securitization prospectuses often include statistics about the

underwriting criteria (e.g., credit scores and loan-to-value ratios) that banks used in originating the

securitized assets but rarely provide information about risk layering (e.g., the combination of low

credit scores with high loan-to-value ratios).8 Second, banks’ financial reports contain very little

8 The SEC revised Regulation AB in August 2014, effective October 2014, to require extensive additional standardized asset-level disclosures about securitization pools in securitization prospectuses and on an ongoing basis. These additional disclosures pertain to contractual features of the securitization that affect the payment waterfall; credit-risk-relevant attributes of the securitized assets such as geography, property value, and loan-to-value ratio; the post-securitization performance of the securitized assets; and post-securitization loss mitigation efforts. These disclosures clearly improve the information available to investors. Due to their recency, however, the effects of these enhanced disclosure requirements have not yet been empirically evaluated.

10

information about recourse risks associated with contractual representations and warranties and

non-contractual implicit recourse (Niu and Richardson 2006; Landsman et al. 2008; Chen et al.

2008; Dou, Liu, Richardson, and Vyas 2014). Third, the volume and profitability of current-period

securitizations are uncertain because they depend on (1) economic conditions such as the

receptivity of financial markets to securitization; (2) banks’ choices about whether to conduct and

how to structure securitizations, given their financing needs and risk tolerance; and (3) banks’

exercise of discretion in fair valuing retained interests and recording securitization income. Fourth,

financial reports provide little information about the sustainability of banks’ securitization-based

business models. Bank insiders likely have information advantages about all of these aspects of

securitization, but the extant literature provides no empirical evidence about whether insiders

exploit these advantages by trading for personal gain.

Prior research finds that insiders exploit their information advantages by trading. For

example, insider net purchases predict future stock returns (Lakonishok and Lee 2001) and insider

sales predict breaks in strings of consecutive quarterly earnings increases three to nine quarters

before the breaks occur (Ke et al. 2003). Because a firm’s stock price impounds all information

about the firm and its earnings measure the firm’s overall operating performance, these studies are

largely silent about the specific types of private information on which insiders trade. Identifying

these types of information is important for two reasons. First, it helps researchers determine the

control variables (e.g., risk factors or alternative sources of information) to include in empirical

models to alleviate concerns that reported results are attributable to omitted correlated variables.

Second, this identification clarifies the determinants of insider trading and thus the policy

implications of the research. For example, Aboody and Lev (2000) identify R&D as a specific

source of insider information and provide evidence that insiders’ trading profits are substantially

11

larger at R&D-intensive firms than at other firms, consistent with R&D activities providing

insiders with information advantages. Aboody and Lev conclude that requiring additional

disclosures of firms’ ongoing and planned R&D activities would mitigate those advantages.

We propose three hypotheses about the associations between bank insiders’ securitization-

related private information and their trading. Each of these hypotheses reflects our expectation that

insiders receive securitization-related information before its public release and that they exploit

this private information by profitably trading. Although insiders’ private information is inherently

unobservable, our study takes a step further than extant research by testing these hypotheses using

subsamples and proxies intended to capture the private information that bank insiders possess

about three types of securitization-related risks: (1) recourse risks, (2) uncertainty about current-

period securitization income, and (3) uncertainty about securitization-based business model

sustainability. We state all hypotheses as alternatives. Online Appendix A summarizes the

hypotheses and indicates the tables that report the corresponding test results and supplemental

analyses.

We first hypothesize a positive contemporaneous association between the amount of bank

insiders’ securitization-related private information and their trading volume:

H1: Bank insiders’ securitization-related private information is positively associated

with their trading volume during the quarter.

This hypothesis is similar to Cheng et al.’s (2011) hypothesis of a positive contemporaneous

association between a bank’s securitization activity and measures of its information asymmetry.

We next hypothesize that the direction and magnitude of insider trading during a quarter

predict not-yet-reported securitization-related accounting performance measures (e.g.,

securitization income) for that quarter or subsequent quarters. Although we examine both insider

12

sales and insider purchases, we expect the association to be stronger for insider sales because the

major concerns raised by securitization pertain to downside risks: Will recourse be triggered? Will

securitizations occur in the current quarter and be profitable? Is the securitization-based business

model sustainable? Because most insider trades are sales, for simplicity we state this and our third

hypotheses in terms of net insider sales (insider sales minus insider purchases).

H2: Net insider sales during quarters are negatively associated with banks’ not-yet-

reported securitization-related accounting performance for those quarters or subsequent quarters.

Tests of this hypothesis can provide more direct evidence of whether insiders trade on valuable,

private securitization-related information than do tests of our first hypothesis.

Lastly, we hypothesize that insider sales (purchases) are followed by stock price decreases

(increases), more so in banks’ securitization quarters, when insiders likely possess more

securitization-related private information, than in other quarters.

H3. Net insider sales in banks’ quarters with securitization activity are more strongly

negatively associated with the banks’ subsequent abnormal stock returns than are net insider sales in the banks’ other quarters.

III. DATA

Although securitization occurs in many industries, as in most prior research our sample

includes only bank holding companies (“banks”). Our sample period begins in 2001Q2 when the

Federal Reserve Board included Schedule HC-S, “Servicing, Securitization and Asset Sale

Activities,” in banks’ quarterly regulatory Y-9C reports. Banks with more than $150 million ($500

million) in total assets before (after) March 2006 must file these reports. Schedule HC-S requires

banks to report detailed and standardized data about their securitizations accounted for as sales in

13

which they retain servicing rights or provide credit enhancement. As in Cheng et al. (2011), we

end the sample period in 2007Q2 for the Recourse Risk and Securitization Income subsample

analyses that examine insider trading during periods when banks’ securitization-based business

models appeared to perform well. We extend the sample period for our Crisis subsample analysis

of the breakdown of those business models during the financial crisis.

Panel A of Table 1 summarizes the sample selection for the full sample. We require bank-

quarter observations to have available Y-9C filings and non-missing PERMCO in the Federal

Reserve Bank of New York’s file that matches Y-9C filings to CRSP,9 yielding 11,513 initial

observations. To mitigate self-selection, we restrict the full sample to banks with securitized assets

outstanding or non-zero securitization income in at least one quarter of our sample period.

Although this restriction excludes 8,402 observations of banks for which securitization does not

appear to be a feasible choice, the remaining 3,111 observations for “Securitization Banks”

constitute 85.8% of the market capitalization of all banks on average during our sample period.

We exclude 472 observations with missing CUSIP, which is necessary to merge Y-9C data with

insider trading data from Thomson Reuters’ Insider Filing Data Feed. Following Seyhun (1992),

Rozeff and Zaman (1998), Piotroski and Roulstone (2005), and Cheng and Lo (2006), we limit

insider trades to open market purchases and sales, which are most likely to reflect insiders’ private

information.10 The Thomson Reuters database does not contain data for 639 bank-quarters; it is

unclear whether this is attributable to absence of insider trading or database incompleteness. We

exclude these observations following Lakonishok and Lee (2001), Frankel and Li (2004), and

Piotroski and Roulstone (2005). The resulting full sample includes 2,000 bank-quarters for 130

9 http://www.newyorkfed.org/research/banking_research/datasets.html. 10 Most other insider trades are between the insiders and their firms. These trades tend to be driven by stock option grants and other stock-based forms of compensation.

14

unique banks, with the number of banks in a quarter varying from a maximum of 98 in 2004Q1 to

a minimum of 67 in 2006Q3 and 2007Q1-2 (untabulated).

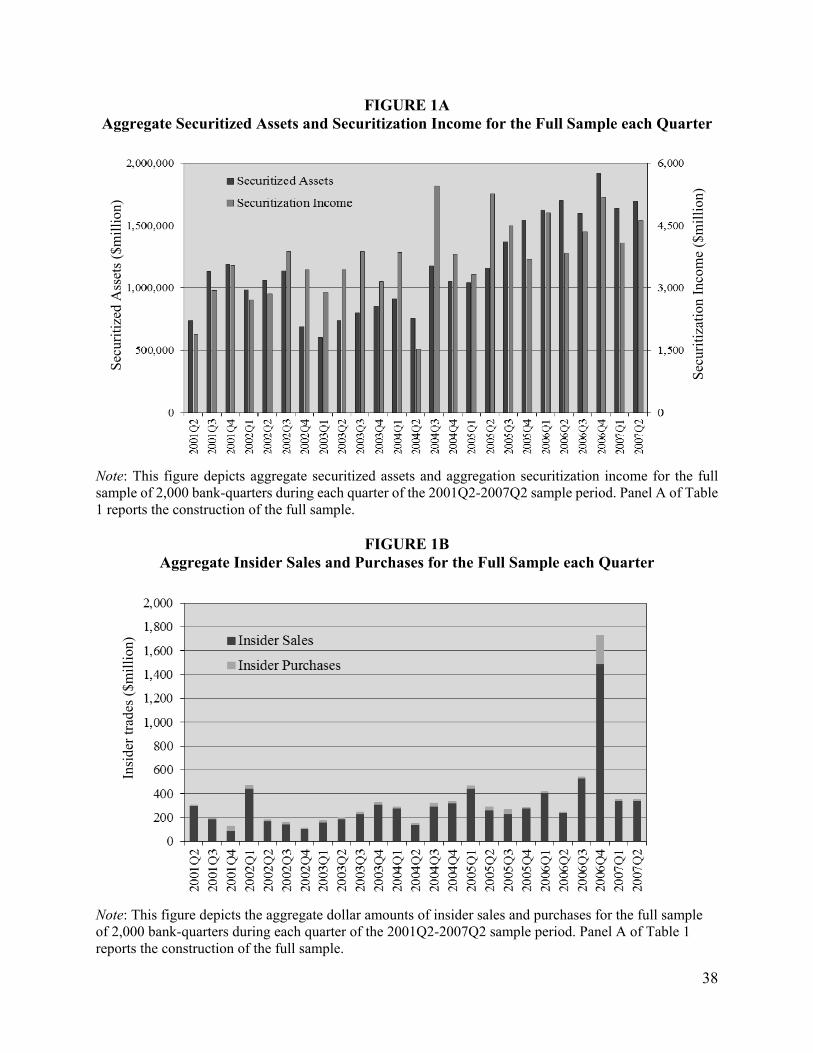

Figure 1A depicts aggregate securitized assets outstanding and securitization income for

the full sample for each quarter of the 2001Q2-2007Q2 sample period. Aggregate securitized

assets generally increase over this period, peaking at $1.9 trillion in 2006Q4. Aggregate

securitization income fluctuates considerably over time, with the maximum being $5.5 billion in

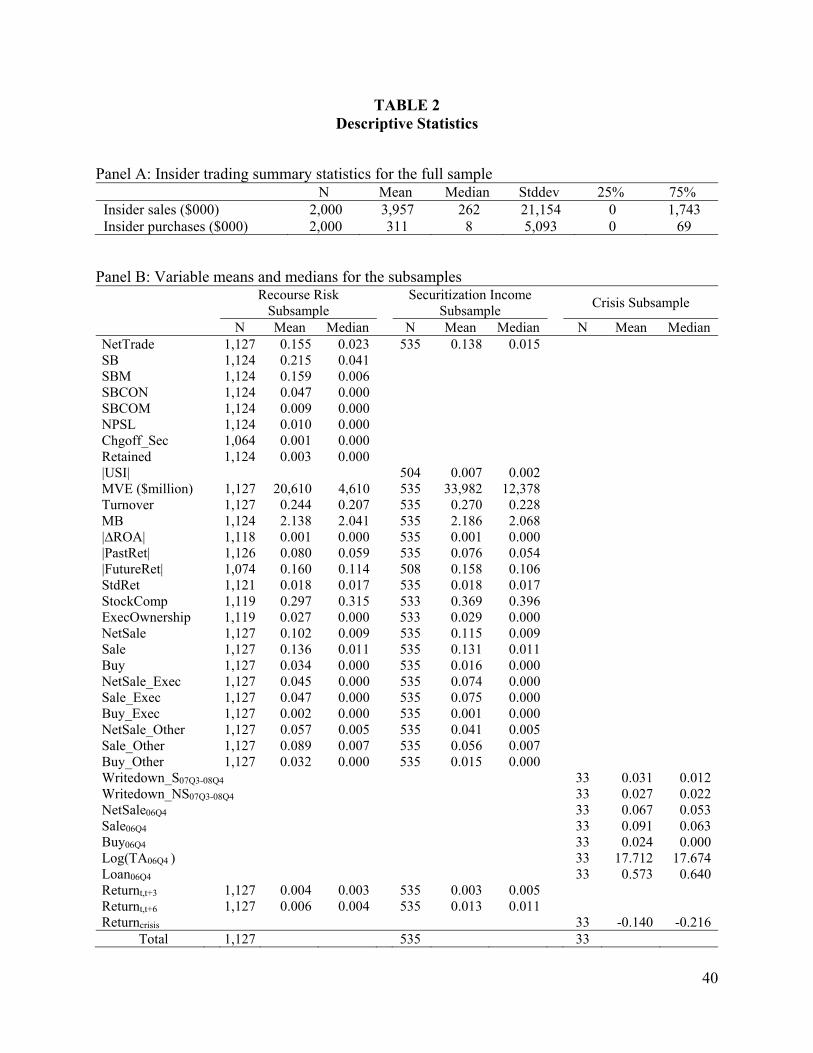

2004Q3. Panel A of Table 2 reports summary statistics for insider sales and purchases calculated

as the number of shares traded multiplied by the trade price. Consistent with prior research, insider

sales are a large multiple of insider purchases (about 13 [33] based on the mean [median] of the

variables). Figure 1B depicts the total dollar amount of insider sales and purchases for the full

sample during each quarter of the sample period. Insider trading varies moderately over time

except for 2006Q4, when the amount is about two and half times higher than in any other quarter,

indicating unusually active insider trading on the verge of the financial crisis.

We identify three subsamples of the full sample in which bank insiders likely possess

specific types of securitization-related private information. Panels B-D of Table 1 summarize the

selection processes for these “securitization-treatment” subsamples. The Recourse Risk subsample

includes the 1,127 bank-quarters reporting a positive balance of securitized assets at the end of the

quarter, with the number of banks in a quarter varying from a maximum of 58 in 2001Q3 to a

minimum of 33 in 2007Q1 (untabulated). Because Schedule HC-S includes only securitizations

accounted for as sales in which banks retain servicing rights or provide credit enhancement, banks

reporting securitized assets generally are exposed to recourse risks. The Securitization Income

subsample includes the 535 bank-quarters with non-zero securitization income in either the current

quarter or the previous quarter, with the number of banks in a quarter varying from a maximum of

15

29 in 2001Q4 to a minimum of 15 in 2006Q3 (untabulated). Of the Securitization Income

subsample observations, 89.3% also belong to the Recourse Risk subsample. 11 The Crisis

subsample includes the 33 banks reporting either a positive balance of securitized assets or non-

zero securitization income in the fourth quarter of 2006 on the verge of the financial crisis; all of

these observations appear in one or both of the Recourse Risk and Securitization Income

subsamples.

We refer to the bank-quarter observations in the full sample that do not belong to either the

Recourse Risk or Securitization Income subsamples as the Control subsample. We contrast the

Recourse Risk and Securitization Income subsamples to the Control subsample in the analyses of

the profitability of insider trading. We do not contrast the Crisis subsample to the Control

subsample, however, because we do not expect the time-distributed Control sample observations

to be comparable to banks with securitization exposures in a single quarter on the verge of the

financial crisis.

IV. PRIMARY ANALYSES

Tests of Hypothesis 1

H1 predicts that the amount of bank insiders’ securitization-related private information is

positively associated with insider trading volume during the quarter. We test this hypothesis by

estimating this equation using the Recourse Risk and Securitization Income subsamples:

NetTradet = a0 + a1Securitizationt + a2 log(MVEt) + a3 log(Turnovert) + a4MBt

+ a5|ΔROAt| + a6|PastRett| + a7|FutureRett| + a8 StdRett + a9StockCompt

11 Securitization income in a quarter may be zero for banks with non-zero securitized assets in the quarter, and vice versa, for various reasons. For example, some banks have positive securitized assets in a quarter from securitizations in prior quarters but conduct no securitizations and thus earn no securitization income in the current quarter. Some banks record zero securitization income despite conducting securitizations in a quarter. Some banks conduct securitizations during a quarter for which they do not retain servicing rights or provide credit enhancement and so do not disclose the securitized assets on Schedule HC-S.

16

+ a10ExecOwnershipt + a11StockCompt*ExecOwnershipt + et. (1) Following Piotroski and Roulstone (2004), the dependent variable is NetTrade, the absolute dollar

amount of sales minus purchases by all of the bank’s insiders during the quarter, multiplied by 100

for presentation purposes, and divided by beginning-of-quarter market value of equity.12 NetTrade

is unaffected by equal increments to insider sales and purchases for a bank in a quarter, and thus

treats such increments as having perfectly offsetting implications.

The primary explanatory variable, Securitization, stands in for our proxies for bank

insiders’ securitization-related private information, which differ across the subsample analyses. In

the Recourse Risk subsample analysis, we proxy for this information using four variables

identified by Cheng et al. (2011): (1) quarter-end securitized assets, SB, which captures the size of

the exposure to recourse risks; (2) quarter-end non-performing securitized loans, NPSL, and (3)

net charge-offs of securitized loans during the quarter, Chgoff_Sec, two variables that capture the

recent performance of the securitized assets; and (4) quarter-end retained securities from

securitizations, Retained, which captures the extent of the primary form of credit enhancement.

We expect banks’ recourse risks to increase with each of these proxies. Bank insiders’ private

information involves knowing the values of these variables before their public disclosure as well

as the implications of the variables for the likelihood that the bank provides recourse on the

securitized assets and the amount of losses resulting from that provision.

In the Securitization Income subsample analysis, to develop the proxy for the amount of

bank insiders’ securitization-related private information, we first estimate this equation predicting

securitization income, SI:

12 Piotroski and Roulstone (2004) scale their measure by trading volume. We scale instead by beginning-of-quarter market value of equity because trading volume trends upward strongly over time with the growth in high-frequency trading after their sample period ends in 2000.

17

SIt = a0 + a1SIt-1 + a2SBt-1 + a3Q1t +a4Q2t + a5Q3t + year fixed effects + et. (2)

On the right hand side of Equation (2), we include securitization income for the previous quarter,

which we expect to be the best predictor of current-quarter securitization income. Following

Dechow et al. (2010), we divide securitization income by beginning-of-quarter book value of

equity. We include beginning-of-quarter securitized assets to capture the strong tendency for banks

that have previously conducted securitizations to continue to do so. Finally, we include fiscal

quarter dummies to control for seasonality and year fixed effects to control for macroeconomic

and financial market factors. We measure unexpected securitization income, USI, as the estimated

residual in Equation (2) and use the absolute value of unexpected securitization income, |USI|, as

the proxy for the amount of bank insiders’ securitization-related private information. Because this

proxy plays a more central role in the test of H2 than in the test of H1, we discuss the estimation

of Equation (2) in the section devoted to the test of H2.

Following Piotroski and Roulstone (2004) and Cheng and Lo (2006), we control for the

following variables in Equation (1). We control for the natural logarithm of banks’ beginning-of-

quarter market value of equity, log(MVE), which we expect to be negatively associated with insider

trading because larger firms tend to have stronger corporate governance and higher media scrutiny.

We control for banks’ stock liquidity using the natural logarithm of trading volume divided by

beginning-of-quarter number of shares outstanding, log(Turnover), because liquidity affects

insiders’ ability to trade without moving the price. We control for beginning-of-quarter market-to-

book ratio, MB, and for the absolute value of the change in quarterly net income from the previous

quarter to the current quarter divided by beginning-of-quarter total assets, |ΔROA|, because we

expect insiders of banks with higher growth and more variable profitability to have greater

18

information advantages. We control for the absolute value of the bank’s stock return in the previous

quarter minus the index return of banks of similar size, |PastRet|, because prior research finds that

insiders are more likely to trade after larger price movements.

We also control for the absolute value of the bank’s return minus the average return of

banks of similar size in the 12 months following the current quarter, |FutureRet|, to capture

insiders’ private information about banks’ future performance unrelated to securitization (Ke et al.

2003). We control for the standard deviation of daily stock returns in the 12 months before the

current quarter begins, StdRet, because managers may trade to reduce their exposure to bank risks

other than recourse risks. We control for the fraction of the bank’s shares owned by its reportable

executives at the end of the most recent fiscal year, ExecOwnership, and for the dollar value of

restricted stock and option grants divided by total compensation in the most recent fiscal year

averaged across these executives, StockComp, because managers with high stock ownership or

recent stock-based compensation tend to trade to reduce this exposure (Cziraki 2015; Ofek and

Yermack 2000). We further include the interaction of ExecOwnership and StockComp to capture

the effect of the combination of stock ownership and stock-based compensation on insiders’

tendency to trade. We are able to calculate ExecOwnership and StockComp using data from

ExecuComp for 995 observations (about 50% of the full sample); we hand-collect data for the

remaining observations from the banks’ proxy statements.

Panel B of Table 2 reports descriptive statistics for the variables in Equation (1). In the

Recourse Risk subsample, securitized assets (undeflated SB) on average equal a sizeable 21.5% of

total assets. The other recourse-risk proxies have considerably smaller values. In the Securitization

Income subsample, securitization income (undeflated SI) equals 34.3% of net income on average

19

(untabulated). Many of the variables have skewed distributions, as evidenced by the large

differences between their means and medians.

Panel C of Table 2 reports pairwise Pearson and Spearman correlations for the full sample.

Because of data skewness, we discuss only the Spearman correlations. NetTrade is negatively and

insignificantly correlated with SB and |USI|, respectively, apparently inconsistent with H1. These

correlations are likely driven by bank size: log(MVE) is highly negatively correlated with NetTrade

but highly positively correlated with SB and |USI|.

Panel A of Table 3 reports the estimation of Equation (1) using robust regression to mitigate

the effects of the data skewness. Robust regression iteratively reweights observations until the

estimated coefficients converge. This method is superior to traditional methods of dealing with

outliers, such as winsorization and truncation, because it identifies and assigns weights to outliers

in a multivariate distribution (Anderson 2008; Leone et al. 2012). The first four columns of the

panel use the Recourse Risk subsample with the four proxies for bank insiders’ securitization-

related private information about recourse risks included one at a time. Consistent with H1, the

coefficients on SB, NPSL, Chgoff_Sec, and Retained are significantly positive at 0.004 (t=2.18),

0.094 (t=2.84), 1.841 (t=4.44), and 0.320 (t=3.15), respectively. The fifth column uses the

Securitization Income subsample with |USI| as the proxy for uncertainty about current-quarter

securitization income. Again consistent with H1, the coefficient on |USI| is significantly positive

at 0.848 (t=14.43). The control variables log(MVE), log(Turnover), and MB have consistently

significant coefficients of the predicted signs across the models, except for the positive but

insignificant coefficient on MB in the Securitization Income subsample analysis. The coefficients

on the other control variables are less consistently significant with the predicted sign.13 Overall,

13 We expect the coefficient on |ΔROA| to be positive. Results in the Recourse Risk subsample analysis are largely consistent with this expectation, but this coefficient is insignificant in the Securitization Income subsample analysis.

20

the results reported in Panel A of Table 3 indicate that insiders trade more when they possess better

securitization-related private information.

We refine the above analyses in two ways to probe our interpretation of the positive

estimated coefficients on the Securitization proxies in Equation (1) as attributable to bank insiders

trading on securitization-related private information. First, we decompose insider trades into those

by CEOs and CFOs versus by other insiders, because prior research provides evidence that CEOs

and CFOs possess better private information than other insiders. For example, Cheng and Lo

(2006) find that the number of bad-news earnings forecasts is more strongly positively associated

with planned purchases by CEOs than by other insiders. Shon and Veliotis (2013) find a significant

positive association between firms meeting or beating analyst earnings expectations and planned

sales after earnings announcements only by CEOs and CFOs. Based on this research, we expect

H1 holds more strongly for trades by CEOs and CFOs than by other insiders. In untabulated tests,

we jointly estimate two regressions, one with trades by CEOs and CFOs as the dependent variable

and the other with trades by other insiders as the dependent variable, using seemingly unrelated

regression. We find that the coefficients on the Securitization proxies are significantly more

positive in the CEO/CFO regression than in the other-insider regression.

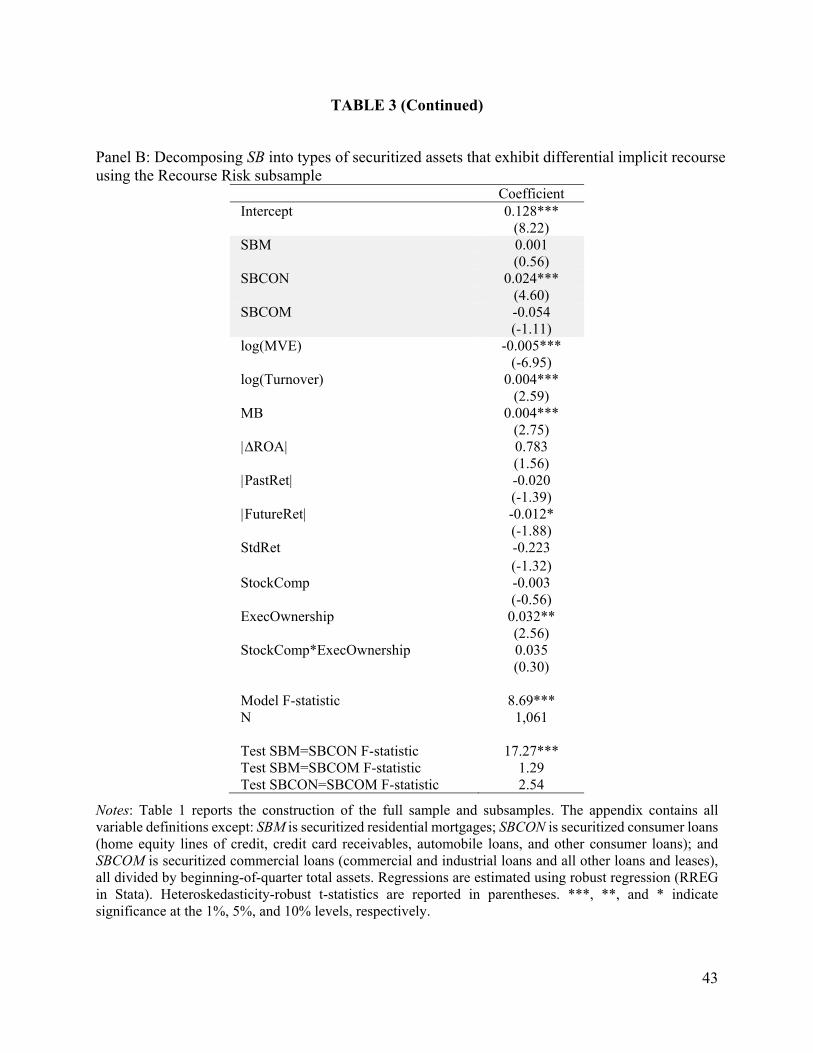

Second, we decompose securitized assets into types that we expect differentially expose

banks to implicit recourse. Chen et al. (2008) argue, based on structural differences across

securitizations of different types of loans and empirical research examining banks’ provision of

implicit recourse, that banks provide implicit recourse in securitizations of revolving consumer

The coefficient on |PastRet| is weakly significantly negative in most of the models. We expect the coefficient on |FutureRet| to be positive and find a weakly positive coefficient in the Securitization Income subsample analysis but a negative coefficient in the Recourse Risk subsample analysis. The coefficient on StdRet is insignificant. The coefficient on ExecOwnership is significantly positive as expected in the Recourse Risk subsample analysis, but not in the Securitization Income subsample analysis. The interaction term of StockComp and ExecOwnership is significantly positive only in the Securitization Income subsample analysis.

21

loans (e.g., credit card receivables and home equity lines of credit) due to the use of master trusts

and early amortization provisions, but not in securitizations of mortgages and most other types of

loans.14 We expect bank insiders’ information advantages to be stronger about implicit recourse

than about contractual recourse. Accordingly, we expand Equation (1) by decomposing SB into

securitized residential mortgages, SBM, consumer loans, SBCON, and commercial loans, SBCOM.

We expect more positive coefficients on SBCON than on SBM or SBCOM.

Panel B of Table 2 reports that, as a percentage of banks’ total assets (SB), SBM averages

15.9% (74.0%), SBCON averages 4.7% (21.9%), and SBCOM averages only 0.9% (4.2%). Panel

B of Table 3 reports the estimation of the expansion of Equation (1) replacing SB with SBM,

SBCON, and SBCOM. As expected, the coefficient on SBCON is significantly positive and

significantly higher than the coefficient on SBM (F=17.27). Likely due to SBCOM’s small

magnitude, the coefficient on SBCOM has a large standard error that renders all differences of

coefficients involving SBCOM insignificant. The results of these refined analyses provide further

support for our interpretation of the positive coefficients on the Securitization proxies in the

estimation of Equation (1) as attributable to bank insiders trading on their securitization-related

private information.

Tests of Hypothesis 2

H2 predicts that higher net insider sales in a quarter indicate that securitization-related

accounting performance for that quarter or subsequent quarters will, when subsequently reported,

be found to be worse on average. We test this hypothesis by examining the association of net

14 Residential mortgages and other consumer loans generally are homogeneous, whereas commercial loans generally are heterogeneous. All else being equal, bank insiders’ information advantage should be greater for heterogeneous loans than for homogeneous loans. Because commercial loan securitizations are relatively small, we do not focus on this source of insiders’ information advantage.

22

insider sales with three securitization-related performance measures using the most relevant

subsamples. First, we examine the unexpected component of non-performing securitized loans

(UNPSL), a timely measure of the performance of securitized loans and thus of the likelihood and

expected cost of banks providing recourse, using the Recourse Risk subsample. We model

expected NPSL below. Second, we examine the unexpected component of securitization income

(USI, the residual in Equation (2)) using the Securitization Income subsample. Finally, we examine

write-downs of securitization-related assets during the financial crisis, our measure of the

breakdown of banks’ securitization-based business models during the crisis, using the Crisis

subsample. Unlike for the first two performance measures, we do not model the expected

component of these write-downs because they should be largely unpredictable if banks accurately

measure securitization-related assets each quarter and because the infrequency of write-downs

before the crisis makes it difficult to implement an expectation model. We include additional

control variables in this test, however, to compensate for the absence of an expectation model for

write-downs.

The expectation model for NPSL is:15

NPSLt = a0 + a1NPSLt-1 + a2SBt-1 + a3Q1t + a4Q2t + a5Q3t + year fixed effects + et. (3)

We include lagged NPSL on the right hand side of Equation (3) to capture serial correlation in the

performance of securitized loans, which we expect to arise for various reasons including: (1)

different loan types exhibit different levels of delinquencies (Ryan 2007, Exhibit 5.6); (2) different

15 We obtain similar results testing H2 using the residual from the estimation of a modified version of Equation (3) in which we define the dependent variable as the change in NPSL from the beginning of quarter t to the end of quarter t+2 plus the sum of loan charge-offs during quarters t, t+1, and t+2. If charge-offs during a period equal zero, the change in NPSL equals the amount of loans that become delinquent, net of any cure of prior delinquencies, during the period. Charge-offs decrease NPSL by the book value of the charged-off loans. Thus, the change in NPSL plus charge-offs during a period reflect loans that either become delinquent, net of cure, or that migrate from delinquency to charge-offs during the period.

23

banks exhibit different underwriting quality; and (3) different pools of securitized loans exhibit

different risk attributes such as geographical and industry concentrations. We include lagged SB

to capture the mathematical fact that, holding delinquency rates constant, banks with higher

securitized assets have higher NPSL. We again include fiscal quarter dummies to control for

seasonality and year fixed effects to control for macroeconomic and financial market factors.

Panel A of Table 4 reports the estimation of Equation (3) using the Recourse Risk

subsample. As expected, the coefficient on lagged NPSL is significantly positive. The coefficient

on SB is insignificant, however, suggesting that lagged NPSL adequately captures both the

delinquency rate and the securitized assets subject to that rate. UNPSL is the estimated residual in

this equation.

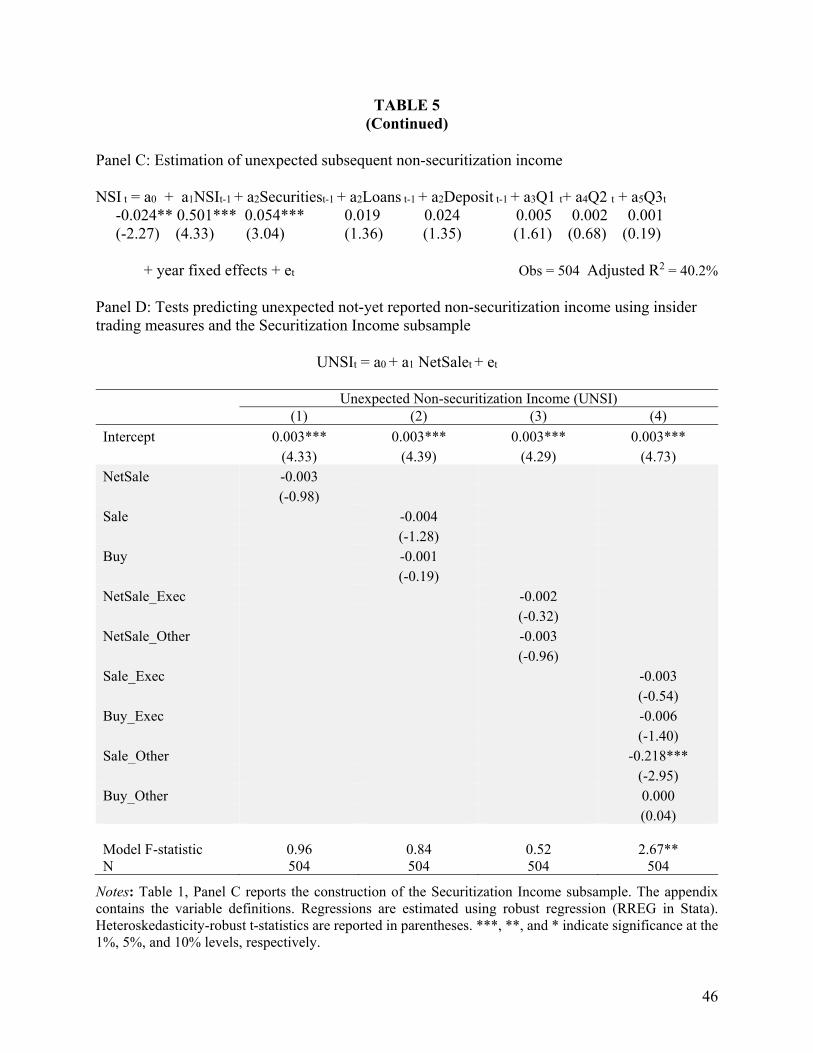

Panel A of Table 5 reports the estimation of Equation (2) using the Securitization Income

subsample. As expected, the coefficients on SI and SB are both significantly positive.

We test H2 by regressing the securitization-related performance measures UNPSL and USI

on NetSale:

UNPSLt = b0 + b1 NetSalet + et. (4) USIt = b0 + b1 NetSalet + et. (5)

We also estimate expanded versions of Equations (4) and (5) in which NetSale is decomposed into

one or both of Sale versus Buy and trades by CEOs and CFOs versus by other insiders.

Panel B of Table 4 reports the robust-regression estimation of Equation (4) using the

Recourse Risk subsample. NetSale is the sole explanatory variable in Column 1 and is decomposed

in Columns 2-4. In Columns 1 and 2, NetSale and its Sale and Buy components have insignificant

coefficients, inconsistent with H2. Decomposing NetSale, Sale, and Buy into trades by CEOs and

24

CFOs (NetSale_Exec, Sale_Exec, and Buy_Exec) versus by other insiders (NetSale_Other,

Sale_Other, and Buy_Other) in Columns 3 and 4, we find significantly positive coefficients on

NetSale_Exec and Sale_Exec but insignificant coefficients on the other variables. These results

indicate that trades by CEOs and CFOs, especially sales, predict the unexpected component of

subsequently reported NPSL for the quarter, consistent with H2 and with top executives having

and trading on private information about the performance of securitized loans.

Panel B of Table 5 presents the robust-regression estimation of Equation (5) using the

Securitization Income subsample and the same decompositions of NetSale and column structure

as in Panel B of Table 4.16 In Column 1, the coefficient on NetSale is significantly negative,

indicating that NetSale predicts unexpectedly low securitization income for the quarter, consistent

with H2. Decomposing NetSale into Sale and Buy in Column 2 shows that the significant

association reported in Column 1 is driven by insider sales, not purchases. In Columns 3 and 4, we

find significantly negative coefficients on NetSale_Exec and Sale_Exec and a significantly positive

coefficient on Buy_Exec, but insignificant coefficients on the trades by other insiders, indicating

that the significant association reported in Column 1 is driven by trades of CEOs and CFOs. These

results are consistent with H2 and with top executives having and trading on private information

about current-quarter securitization income.

To rule out the possibility that the ability of NetSale to predict the unexpected component

of securitization income simply reflects bank insiders trading on their private information about

16 The timing of the arrival of securitization news for a quarter varies across banks, coming from as early as the earnings announcement date to as late as the Y-9C filing date, which is required to be no later than 45 days after the quarter end. In our primary tests, we measure insider trades within the quarter. To test the sensitivity of our results to this choice and to better align the measure of insider trades with the subsequent arrival of securitization news, we alternatively measure insider trades from one day after the earnings announcement for the previous quarter to one day before the earnings announcement for the current quarter. The use of this alternative insider trading window does not alter the results, reflecting the fact that 95% of the trades in this alternative window occur during the fiscal quarter involved.

25

the bank’s bottom-line net income (Ke et al. 2003), we conduct parallel analysis using non-

securitization income, NSI, defined as net income minus securitization income divided by

beginning-of-quarter book value of equity (Dechow et al. 2010). Panel C of Table 5 reports the

estimation of an expectation model for NSI that parallels Equation (2) for SI. We measure the

unexpected component of NSI as the residual from this estimation, UNSI. Panel D of Table 5

reports the robust-regression estimation of Equation (6) replacing USI with UNSI. Columns 1-3

report that this estimation yields insignificant associations of UNSI with NetSale, its Buy and Sale

components, and its NetSale_Exec and NetSale_Other components. Column 4 reports a significant

negative coefficient on Sale_Other, however, indicating that other insiders sell shares before the

release of negative news about NSI. The contrasting results for USI and UNSI suggest that

securitization is an especially significant source of information advantage for bank insiders,

particularly top executives.

We also test H2 using write-downs of securitization-related assets during 2007Q3-2008Q4

by the Crisis subsample of 33 banks. We collect data on these write-downs from Bloomberg’s

WDCI (Write-Down and Capital Infusion) database, which contains material quarterly write-

downs by type reported by financial institutions during the crisis. For banks not covered by WDCI,

we hand collect these write-downs from their Form 10-K filings. In aggregate, Crisis subsample

banks reported total asset write-downs of $291 billion during the 2007Q3-2008Q4 period we

examine.17 WDCI distinguishes 18 types of write-downs, all of which largely or entirely involve

financial instruments.18 We classify these write-down types as securitization-related versus non-

securitization-related as follows. The only apparent non-securitization-related asset is loans held

17 For two sample banks that were acquired during 2007Q3-2008Q4, we calculate write-downs only up to the quarter before the acquisition to exclude discretionary “cleaning the decks” write-downs that often are recorded upon the arrival of new management. 18 For example, the WDCI help function indicates that write-downs of goodwill are not included.

26

for investment; this classification implies that banks do not currently intend to securitize the loans.

We define write-downs of non-securitization-related assets, Writedown_NS07Q3-08Q4, as cumulative

excess loss provisions for these loans divided by loans held for investment at quarter-end

2006Q4.19 WDCI includes an unspecified category that we do not treat as either securitization

related or non-securitization related; our results are not affected by this choice. We define write-

downs of securitization-related assets, Writedown_S07Q3-08Q4, as the sum of WDCI’s 16 other types

of write-downs divided by the sum of trading securities, available-for-sale securities, held-to-

maturity securities, and loans held for sale at quarter-end 2006Q4.20

We regress Writedown_S07Q3-08Q4 on net insider sales during 2006Q4, NetSale06Q4. We

include two control variables: (1) the logarithm of total assets at quarter-end 2006Q4, TA06Q4, to

capture size-related effects; and (2) loans held for investment divided by total assets at quarter-end

2006Q4, Loan06Q4, to capture banks’ willingness and ability to hold loans on balance sheet.

Writedown_S07Q3-08Q4 = c0 + c1NetSale06Q4 + c2log(TA06Q4) + c3Loan06Q4 + e. (6)

We also estimate an expanded version of Equation (6) in which NetSale06Q4 is decomposed into

Sale06Q4 and Buy06Q4.21 The mean of NetSale06Q4 is $36 million, which equals Sale06Q4 of $43

million minus Buy06Q4 of $7 million (untabulated). For comparison purposes, we estimate Equation

(6) with Writedown_NS07Q3-08Q4 as the dependent variable. The means of Writedown_S07Q3-08Q4 and

Writedown_NS07Q3-08Q4 are $3.4 billion and $3.9 billion, respectively (untabulated).

19 The WDCI help function indicates that its write-downs for loan held for investment equal the excess of the bank’s provision for loan losses during the quarter over its provision for loan losses in 2006Q4. 20 The asset types that contribute most to Writedown_S07Q3-08Q4 are collateralized debt obligations (28%), subprime residential mortgage-backed securities (16%), collateralized loan obligations (11%), and commercial mortgage-backed securities (8%). 21 Because of the small size of the Crisis subsample, we do not decompose insider trades into those by CEOs and CFOs versus other insiders.

27

Columns 1 and 2 (3 and 4) of Table 6 report Tobit estimation of Equation (6) with

Writedown_S07Q3-08Q4 (Writedown_NS07Q3-08Q4) as the dependent variable. 22 Even though the

sample includes only 33 observations, yielding low-power tests, Column 1 reports a significantly

positive coefficient of 0.159 (t=2.43) on NetSale06Q4, and Column 2 reports a significantly positive

coefficient on Sale06Q4 of 0.140 (t=2.10) and a significantly negative coefficient on Buy06Q4

of -0.233 (t=-2.31). These results are consistent with H2 that insider sales (purchases) on the verge

of the crisis predict larger (smaller) write-downs of securitization-related assets during the crisis.

In contrast, the coefficients on the insider trading variables in Columns 3 and 4 are insignificant,

inconsistent with trading by bank insiders on the verge of the financial crisis pertaining to the

deterioration of banks’ traditional banking activities such as lending.

Tests of Hypothesis 3

H3 predicts that net insider sales in Securitization Banks’ quarters with securitization

activity indicate subsequent negative abnormal stock returns more strongly than do net insider

sales in these banks’ other quarters. We test this hypothesis using two approaches: (1) calculating

median abnormal stock returns after individual insider trades following Aboody and Lev (2000)

and (2) estimating multivariate regression models at the bank-quarter level following Lakonishok

and Lee (2001).23 In each approach, we compare the abnormal returns for the Recourse Risk and

Securitization Income subsamples to those for the Control subsample.

In the individual trade-level approach, following Jagolinzer (2009) we calculate buy-and-

hold abnormal stock returns for the three and six months following each insider trade during a

quarter. We do not examine Jagolinzer’s one-month return window because it often excludes

22 Untabulated robust-regression (linear) estimation of Equation (6) yields the same inferences. 23 Aboody and Lev (2000) also use a rolling calendar-time portfolio approach that is inappropriate for our study due to our relatively short sample period.

28

banks’ first disclosure of securitization information in a quarter, which may occur as late as the

required filing of regulatory Y-9C reports by 45 days after quarter end.24 We calculate abnormal

stock returns as a bank’s buy-and-hold return minus the buy-and-hold return for a size-stratified

banking-industry index over the same window. Specifically, we sort banks into above- versus

below-median size groups in each quarter based on the banks’ beginning-of-quarter market

capitalization. We calculate average returns for each group for each day during the quarter. The

index return for a bank in a quarter is the return during the quarter for the group to which the bank

belongs at the beginning of the quarter. This index return removes returns attributable to common

factors affecting comparable banks, an improvement over prior research that typically uses a

market index return (Aboody and Lev 2000; Ke et al. 2003; Jagolinzer 2009).25

Panel A (Panel B) of Table 7 reports median abnormal stock returns for the three- and six-

month windows after sales and purchases by all insiders, CEOs and CFOs only, and other insiders

for the Recourse Risk (Securitization Income) and corresponding Control subsample. Statistically

significant median abnormal returns are in boldface. The “between-group test statistic” indicates

the significance of differences between the median abnormal returns for the securitization-

treatment and Control subsamples. If insiders trade solely for liquidity or portfolio-rebalancing

purposes, we expect median abnormal returns to be zero. If insiders instead trade on private

information, we expect median abnormal returns to be negative (positive) after insider sales

(purchases).

In the top part of Panel A examining trades by all insiders, abnormal stock returns are

significantly negative after insider sales and significantly positive after insider purchases in both

24 Aboody and Lev (2000) also examine a 12-month windows for which we find insignificant results, likely due to the noise resulting from extending the window. 25 Our results are similar or stronger using a market index or overall bank index.

29

the three- and six-month return windows in the Recourse Risk subsample. In the Control

subsample, abnormal stock returns are significantly negative after insider sales but insignificant

after insider purchases in both return windows. Insider trading is significantly more profitable in

the Recourse Risk subsample than in the Control subsample for the three- and six-month windows

after purchases and the six-month window after sales, consistent with H3, although the difference

in returns between the Recourse Risk and Control subsamples in the three-month window after

sales is insignificant. Overall, these results suggest that trades by insiders of Securitization Banks

are more likely to be based on private information in quarters with securitization activity than in

other quarters.

The middle (bottom) portion of Panel A reports the same analyses for trades by CEOs and

CFOs (other insiders). While sales and purchases by CEOs and CFOs and other insiders are all

profitable, trades by CEOs and CFOs are considerably more profitable than trades by other

insiders. For example, the abnormal stock return in the six-month window is -4.6% for sales by

CEOs and CFOs compared to -1.3% for sales by other insiders, and 4.3% for purchases by CEOs

and CFOs compared to 0.0% for purchases by other insiders. As for trades by all insiders, trades

by CEOs and CFOs are more profitable in the Recourse Risk subsample than in the Control

subsample for the three- and six-month windows after purchases and the six-month window after

sales. In contrast, trades by other insiders do not exhibit consistently different profitability across

the Recourse Risk and Control subsamples. These results are consistent with our expectation that

top executives such as CEOs and CFOs have better securitization-related private information and

thus trade more profitably than other insiders.

Panel B (Panel C) of Table 7 reports similar analyses of median abnormal stock returns

following trades by bank insiders for the Securitization Income and Control subsamples (the Crisis

30

subsample). To conserve space, we do not discuss these results, which yield similar inferences as

the Panel A results. The significance of the results for the Crisis subsample is striking given the

small size of this sample.

Online Appendix B reports the details of our bank-quarter-level multivariate regression

models, which yield similar inferences as the individual trade-level approach. Briefly, for the

Recourse Risk, Securitization Income, and Control subsamples, we regress 3-month and 6-month

abnormal stock returns on either NetSale or Sale and Buy as well as control variables. For both of

these securitization-treatment subsamples, we find that the coefficients on NetSale and Sale are

significantly negative and the coefficient on Buy is significantly positive, consistent with insider

trading in securitization quarters being profitable. In contrast, for the Control subsample the

coefficients on these insider trading variables are all insignificant. For the Crisis subsample, we

regress abnormal stock returns during the financial crisis period from January 1, 2007 to April 30,

2009 on the same sets of insider trading variables in 2006Q4. Again despite the small sample size,

we find that the coefficient on NetSale (Sale) is significantly negative at the 10% level in a one-

tailed (two-tailed) test, weak evidence of profitable insider trading on the verge of the crisis.

V. SUPPLEMENTAL ANALYSES

Litigation Risk and 10b5-1 Plans

Although a matter of ongoing interpretation and dispute, insider trading is in principle

prohibited, being subject to SEC enforcement and litigation under SEC Rule 10b-5 issued in 1942

pursuant to the SEC’s authority under Section 10(b) of the Securities Exchange Act of 1934. Ke

et al. (2003) provide evidence that insiders avoid litigation by reverting their stock sales to normal

levels two quarters before informational events. SEC Rule 10b5-1, issued in August 2000, defines

illegal insider trading as insiders possessing non-public information when they trade. Section (c)

31

of this rule provides an affirmative defense for transactions under pre-arranged trading plans,

referred to as “10b5-1 plans.” Jagolinzer (2009) finds that insiders sell their shares under these

plans from one to six months before firms report unexpectedly poor performance and that plan

sales avoid larger losses than do non-plan sales. Shon and Veliotis (2013) find that CEOs and

CFOs manipulate earnings to meet or beat market expectations before plan sales. These studies

suggest that 10b5-1 plans are often used by insiders to reduce their litigation risk by providing

cover for their private-information-based trading.

We examine the extent to which insiders in our sample trade under 10b5-1 plans and

whether plan sales avoid larger losses than do non-plan sales. As do Shon and Veliotis (2013), we

obtain data on insiders’ trades under 10b5-1 plans from j3sg.com,26 which begins coverage on July

1, 2003, when insiders were first required to file Form 4 electronically after trading. Insiders are

not required to disclose whether their trades are under a 10b5-1 plan, however, or the details of

any plan.27 All plan trades by insiders of our sample banks are sales.

Panel A of Table 8 reports the dollar amount of plan sales by all insiders, by CEOs and

CFOs, and by other insiders of Securitization Banks in each quarter of 2003Q3-2007Q2 and in

total across this period. Plan sales constitute 47% of sales by CEOs and CFOs but only 23% of

sales by other insiders. Over 98% of plan sales by insiders occur in banks’ quarters with

securitization activity (untabulated), i.e., in the Recourse Risk or Securitization Income

subsamples, even though these quarters comprise fewer than 60% of the banks’ quarters. These

statistics suggest that CEOs and CFOs are more concerned than other insiders about litigation risk

26 The j3sg.com database is less comprehensive than the Thomson Reuters database used in our earlier analyses. For example, for the period over which the two databases overlap, the number of bank-quarters (dollar amount of insider trades) in the j3sg.com database is 63.7% (55.8%) of that in the Thomson Reuters database. 27 Jagolinzer (2009) observes that 18% of plan trades are not disclosed as such and that insiders predominantly use 10b5-1 plans for sales, not purchases.

32

but that both types of insiders use 10b5-1 plans to provide cover for private-information-based

sales.

To investigate whether insiders use 10b5-1 plans to mitigate litigation risk, we exploit the

fact that a large stock price drop following an insider trade increases the insider’s exposure to

litigation (Lev and de Villiers 1994). In Panel B of Table 8, we report the median abnormal stock

returns in the three and six months after plan sales and non-plan sales in the same quarters by all

insiders, by CEOs and CFOs only, and by other insiders. The panel reports significantly negative

median abnormal stock returns in both return windows after plan sales, but insignificant (in one

case significantly positive) returns after non-plan sales, by all three groups of insiders. The

abnormal returns after plan sales are significantly more negative than those after non-plan sales.

Moreover, the stock returns after plan sales by CEOs and CFOs are considerably more negative

than those after plan sales by other insiders (untabulated). These results suggest that insiders,

especially CEOs and CFOs, use 10b5-1 plans to provide cover for their trading on securitization-

related private information.

Does Insider Trading Benefit Investors through Enhanced Price Informativeness?

This details of analysis are reported in Online Appendix C. Briefly, we expand the future

earnings response coefficient (FERC) framework (Collins, Kothari, Shanken and Sloan 1994;

Tucker and Zarowin 2006) to include interactions of the explanatory variables with securitized

assets, SB, an indicator for high insider trading volume, and the interaction of these two variables.

We find that securitization and insider trading each separately reduce the informativeness of price

with respect to future earnings and that insider trading does not alter the effect of securitization on

this price informativeness. Hence, we find no evidence that securitization-related insider trading

benefits investors.

33

VI. CONCLUSION

Securitizations are complex and opaque transactions about which bank insiders have

significant information advantages. We investigate whether and if so how insiders exploit specific

types of securitization-related private information by trading for personal gain. For our sample of

Securitization Banks, we find that the amount of securitization-related insider information is

positively associated with insider trading volume during the quarter, more so for trades by CEOs

and CFOs than by other insiders and for the type of securitized assets most subject to implicit

recourse. Net sales by CEOs and CFOs predict subsequent unexpected high levels of non-

performing securitized loans and low levels of securitization income subsequently reported for the

quarter, as well as large write-downs of securitization-related assets during the financial crisis,

indicating that CEOs and CFOs trade on their securitization-related private information. We find

that insiders profit more from trading in their bank’s securitization quarters than in other quarters

and this finding is driven by trades by CEOs and CFOs instead of other insiders. Moreover, insiders

tend to use Rule 10b5-1 plan sales in securitization quarters to shield themselves from the litigation

risk, and they are able to avoid substantially larger negative stock returns under plan sales than

under non-plan sales. We find no evidence that insider trading improves the informativeness of

price with respect to future earnings.

Our results suggest that securitization is an especially significant source of information

advantage for bank insiders, especially top executives such as CEOs and CFOs. Securitization-

related insider trading appears to benefit bank insiders, particularly top executives, but not

investors. Our findings should be of interest to investors and policymakers involved in the

regulation of securitizations and other complex financial transactions.

34

References

Aboody, D., and B. Lev. 2000. Information asymmetry, R&D, and insider gains. Journal of Finance 55 (6): 2747-2766.