Taxes and recordkeeping for small farms

44

Taxes and Recordkeeping for Small Farms Hawkins, Yarber & Chambers, CPA’s Gabe Chambers, CPA, MBA

-

Upload

bronwen-elizabeth-madden -

Category

Business

-

view

110 -

download

1

Transcript of Taxes and recordkeeping for small farms

Taxes and Recordkeeping for

Small FarmsHawkins, Yarber & Chambers, CPA’s

Gabe Chambers, CPA, MBA

Questions/Topics Requested

Minimum farm income requirements

Chances of being audited

Record-keeping requirements

What is considered a farm expense?

How to handle losses

Having kids/family members work on the farm

Farm vs Hobby The IRS presumes that an activity is carried on for profit if it makes a profit

during at least three of the last five tax years, including the current year — at least two of the last seven years for activities that consist primarily of breeding, showing, training or racing horses.

Does the time and effort put into the activity indicate an intention to make a profit?

Does the taxpayer depend on income from the activity?

If there are losses, are they due to circumstances beyond the taxpayer’s control or did they occur in the start-up phase of the business?

Has the taxpayer changed methods of operation to improve profitability?

Does the taxpayer or his/her advisors have the knowledge needed to carry on the activity as a successful business?

Has the taxpayer made a profit in similar activities in the past?

Does the activity make a profit in some years?

Can the taxpayer expect to make a profit in the future from the appreciation of assets used in the activity?

Source:http://www.kiplinger.com/tool/taxes/T055-S001-calculator-what-s-your-risk-of-a-tax-audit

Audit

We are seeing a lot more notices than full audits (knock on wood)

Risk Factors

Self-Employed-Business or farm

Large fluctuations in income or expenses

Large losses with not much revenue

Not reporting income e.g. 1099’s not reported

Large earned income credit (huge area of tax fraud)

How to avoid an audit

Make sure all reported items are reported on the tax return

Be consistent with reporting

Show some profit eventually

Importance of Records

Benefits of recordkeeping

Kinds of records to keep

How long to keep records

Accounting tools

Accounting methods

Best practices

Benefits of Recordkeeping

Business / Personal Use

Business analysis

Easily track important information

Income

Expenses

Compare Periods

Month-month/year-year

Organize records

Keep invoices, receipts etc.

Reconcile bank accounts

CPA / Tax / IRS Use

Tax return preparation

Clean books will save tax prep $

Thorough books will save TAX $

Tax planning

Can save you significant $

Audit

Not exactly the time you want to find out the tax return doesn’t match the “books”

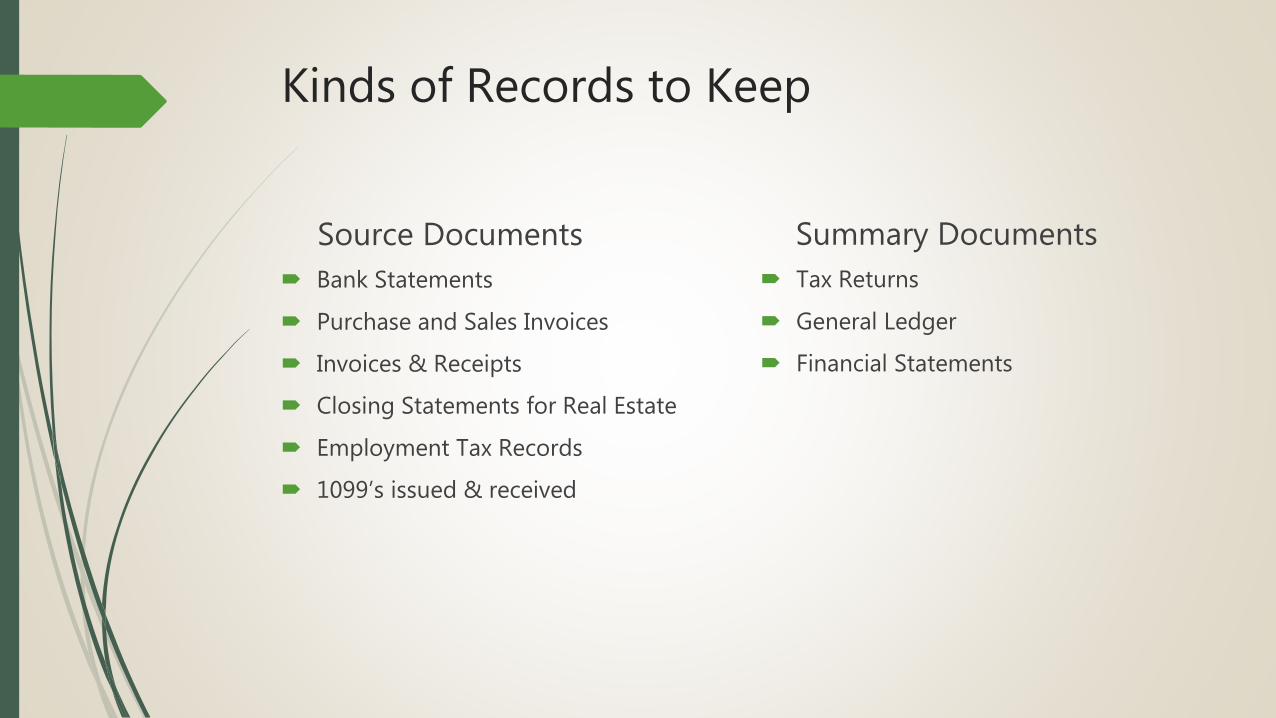

Kinds of Records to Keep

Source Documents

Bank Statements

Purchase and Sales Invoices

Invoices & Receipts

Closing Statements for Real Estate

Employment Tax Records

1099’s issued & received

Summary Documents

Tax Returns

General Ledger

Financial Statements

How Long to Keep Records

General Rule

Keep all records for at least 3 years after filing tax return or 2 years after tax was paid

Employment Taxes for Farm Employees

Keep all employment tax records for at least 4 years after the date the tax becomes due or is paid, whichever is later.

Social Security

Social Security recommends keeping W-2’s until you begin collecting social security

Since farmers’ social security is based on self-employment tax, it might be good to keep a copy of your tax return until you make sure they have computed it correctly

Assets

Keep record of the purchase until the sale of the asset is reported and then follow the general rule

How Long to Keep Records

Example

Built barn in 2005 for $20,000

Annual depreciation of $1,000 for 20 years

If you get audited in 2015 and cannot produce records for purchase, IRS can disallow annual deduction for 2013, 2014, 2015 and going forward.

Assuming a 30% tax rate, this loss of deduction could cost $3,600+

Accounting Tools

Accounting software such as QuickBooks or Quicken

Will provide the most business management tools

Easy to use after learning curve

Excel or spreadsheet software

Cheap

Easy to use if you keep it simple

Columnar Pad

Work great if used properly

Box of receipts and adding machine

Simple but labor intensive

Bottom line: Anything will work if it is maintained!

Accounting Methods

Cash

Most farmers use cash accounting

Recognize income when money changes hands

Simplest method

Cannot hold checks or postpone receipt (Example 1)

Can have deferred payment contract (Example 2)

Accrual

Income matching principle

Example: Sell grain produced in 2016. Payment not received until 2017.

Cash method: Income reported in ’17 related expenses reported in ‘16

Accrual method: Income reported in ’16 same as related expenses

Method of accounting is selected upon filing of first tax return and cannot be changed without IRS approval

Accounting Methods

Example 1: Frances Jones, a farmer who uses the cash method of accounting, was entitled to receive a $10,000 payment on a grain contract in December 2016. She was told in December that her payment was available. She requested not to be paid until January 2017. Frances must include this payment in her 2016 income because it was made available to her in 2016

Example 2: You are a farmer who uses the cash method and a calendar tax year. You sell grain in December 2016 under a bona fide arm’s length contract that calls for payment in 2017. You include the proceeds from the sale in your 2017 gross income since that is the year payment is received. However, if the contract states that you have the right to the proceeds from the buyer at any time after the grain is delivered, you must include the sales price in your 2016 income, even if payment is received in the following year.

Best Practices

I recommend a separate bank account for the farm

Easier to keep farm and personal separate

Keep asset purchases separate from others in a permanent file

Use the filing/recordkeeping system that you will maintain

Just like a diet: use the one that works for you

Keep all records at least 5 years

Questions over Recordkeeping or Accounting Methods?

Farm Income

Farm Income

Schedule F

Farm Products raised for sale

Livestock, produce, grain, etc.

Farm products bought for resale

Patronage Dividends (1099-PATR)

All taxable unless personal portion can be determined

Ag Program Payments

Custom Hire / Machine Work

Other - Fuel Tax Credit

Subject to SE Tax & normal tax rate

Form 4797

Sale of depreciated assets

Generally depreciation is recaptured and subject to normal tax rate

Sale amount over original cost is taxed at capital gains rate (15% max)

Sale of raised livestock

Cattle & Horses held 24+ months

Other livestock held 12+ months

Used for draft, breeding, dairy or sporting

Capital Gains Rates (15% Max)

NO SE TAX

Farm Income – Misc.

Income Averaging

Used if income fluctuates significantly from year to year

Calculates tax using prior 3 years rates

Weather Related Sales

You can show that you would not have sold the additional animals under “normal” conditions

The weather condition must be in an area eligible for assistance i.e. Federal Disaster

Example: You live in federally declared drought disaster area and because of the drought you sold 135 head when you would have normally sold 100 you can postpone recognition of sale to next year

Barter Income is generally reportable to FMV of items received

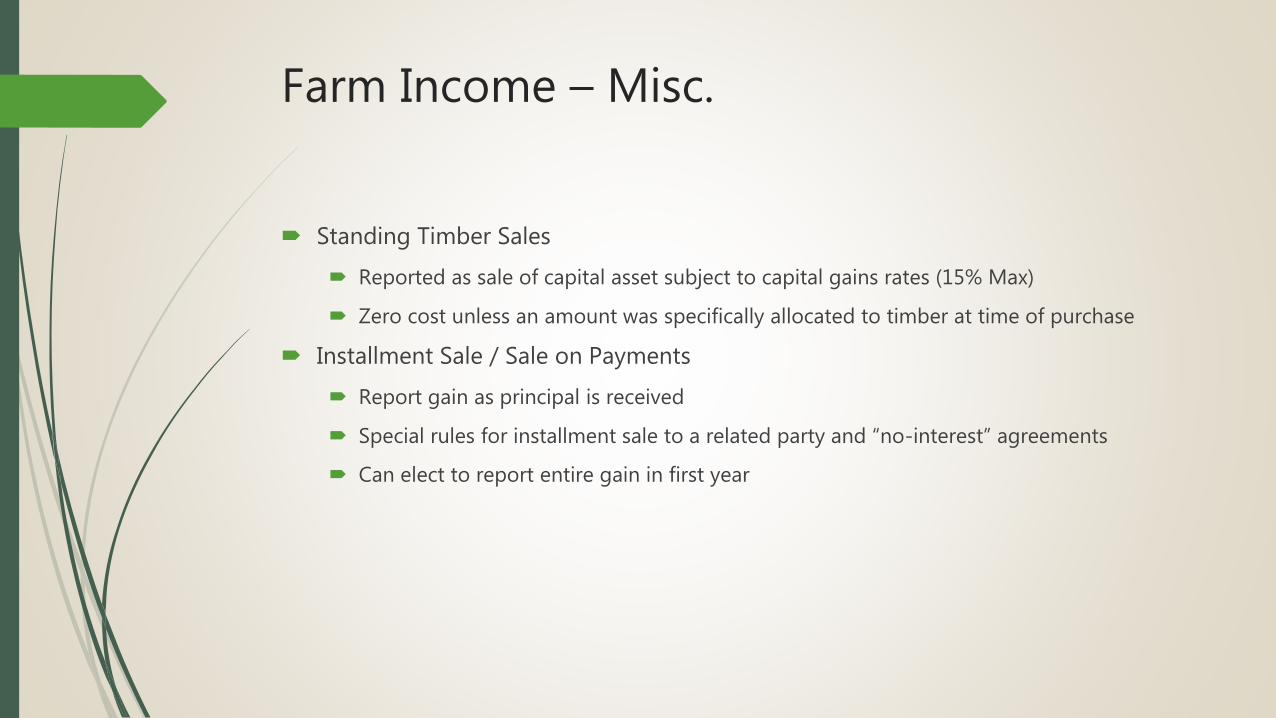

Farm Income – Misc.

Standing Timber Sales

Reported as sale of capital asset subject to capital gains rates (15% Max)

Zero cost unless an amount was specifically allocated to timber at time of purchase

Installment Sale / Sale on Payments

Report gain as principal is received

Special rules for installment sale to a related party and “no-interest” agreements

Can elect to report entire gain in first year

Farm Expenses

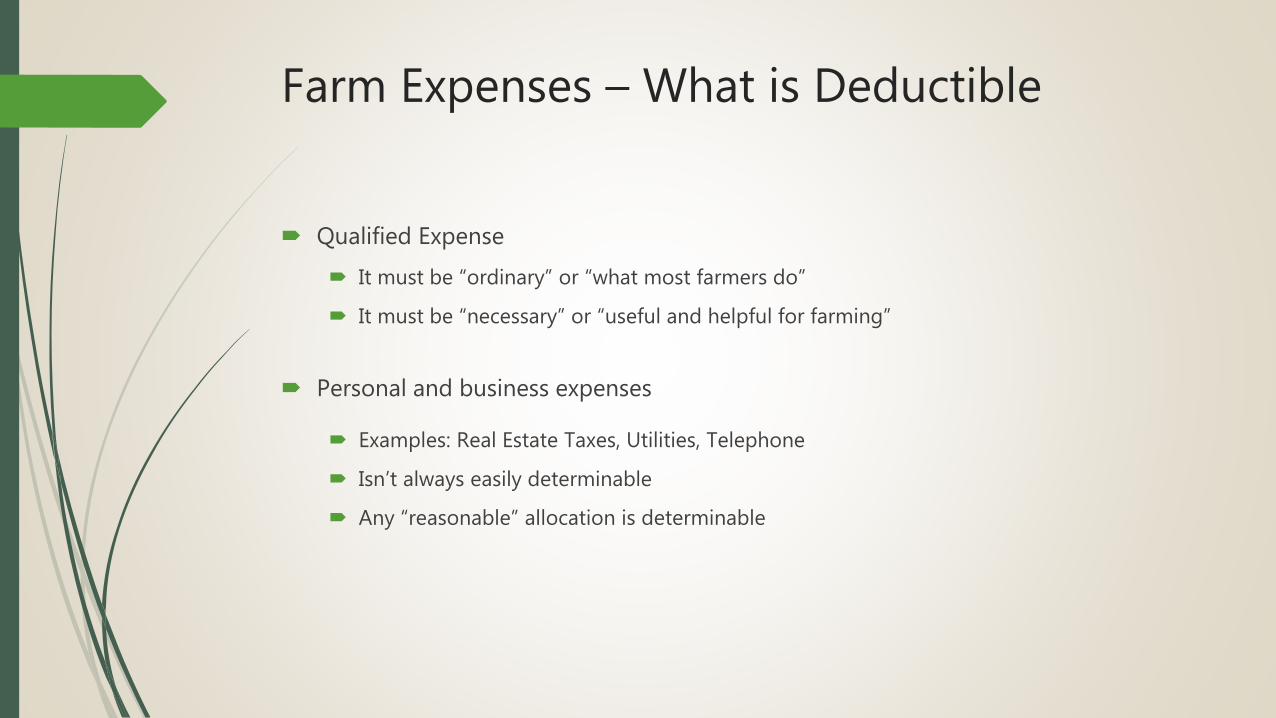

Farm Expenses – What is Deductible

Qualified Expense

It must be “ordinary” or “what most farmers do”

It must be “necessary” or “useful and helpful for farming”

Personal and business expenses

Examples: Real Estate Taxes, Utilities, Telephone

Isn’t always easily determinable

Any “reasonable” allocation is determinable

Farm Expenses

Farm Expenses – Car & Truck ExpensesMileage vs. Actual

Mileage

53.5 cents per mile

24 cents per mile of depreciation

Continue to deduct even when basis is zero

Mileage log is required

Keep maintenance records to substantiate mileage

Apps will track mileage

MileIQ & QuickBooks Self-Employed

Actual Expenses

Includes gas, tires, repairs, etc.

Depreciation is limited to cost

Can use Sec. 179 (expense) and 50% Bonus in 1st year to maximize benefit

If available for personal use, deduction can be limited to business use % that should be substantiated by mileage log

Farm Expenses - Travel

Travel Expenses

Deductible assuming they meet the ordinary and necessary requirements

Include hotels, airfare, taxi’s, etc.

Only business related expenses are deductible

Travel Meals

Can only deduct 50% of expenses on taxes

Only deductible if it is necessary to stop for substantial rest during business trip

Can use per Standard Meal Allowance (most localities are $51/day)

Amounts for specific locations are available at www.gsa.gov/perdiem

Subject to specific rules regarding partial days away

Farm Expenses - Employees

General Rules

Ag Employees are subject to Social Security (6.2%) and Medicare (1.45%)

Farmers report withholding annually on Form 943 and can make payment annually if liability is less than $2,500

Subject to Unemployment (Federal and State)if either:

Paid wages of $20,000 in any calendar quarter in current or prior year

Employed 10 or more farmworkers during at least some part of a day (whether or not at the same time) during any 20 or more different weeks in 2016 or 20 or more different weeks in 2017

Employees must be issued a W-2

Farmers can provide employee benefits, e.g., health insurance, retirement, etc.

Farm Expenses – Family Employees

Spouse

Subject to Social Security and Medicare Taxes but not Unemployment Taxes

Verify this is employment, not partners

Tax planning

If there is self-employment profit, some can be shifted to spouse for Social Security Coverage

Children

Must be a bona fide employer/employee relationship

Children under 18 are not subject to social security, Medicare or unemployment

Children under 21 are not subject to unemployment

Tax Planning

Wages paid to children less than $6,300 are not subject to income tax for children

This also gives them earned income to be able to contribute to ROTH IRA, i.e., tax deferred college savings

Paying your children can be a nice tax savings

Farm Expenses – Contract Labor

Determine employee or contract labor

Do you control what, when, and where, e.g., what they do, when they get paid, etc.

Are they doing similar work for other people?

If you classify an employee as an independent contractor and you have no reasonable basis for doing so, you may be held liable for employment taxes for that worker

1099’s

Must be issued for payments of $600 or more to individuals (e.g. accountants, contractors, veterinarians, etc.) for services or rents in the course of business

Tip: Get payee information by requesting a W-9 before issuing payment

Deduction can be disallowed if 1099’s are not issued

Farm Expenses - Depreciation

What can be depreciated

Property owned by you used in the business

Have a determinable useful life beyond current year

Examples: Livestock purchased for breeding, equipment, barns, etc.

What cannot be depreciated

Land

Property placed in service and disposed in same year

Depreciation starts on the “Placed-in-Service” date

The date the property is ready and available for a specific use

Not the purchase date or the date it was first used

Depreciation is “recaptured” as ordinary income at the time of sale

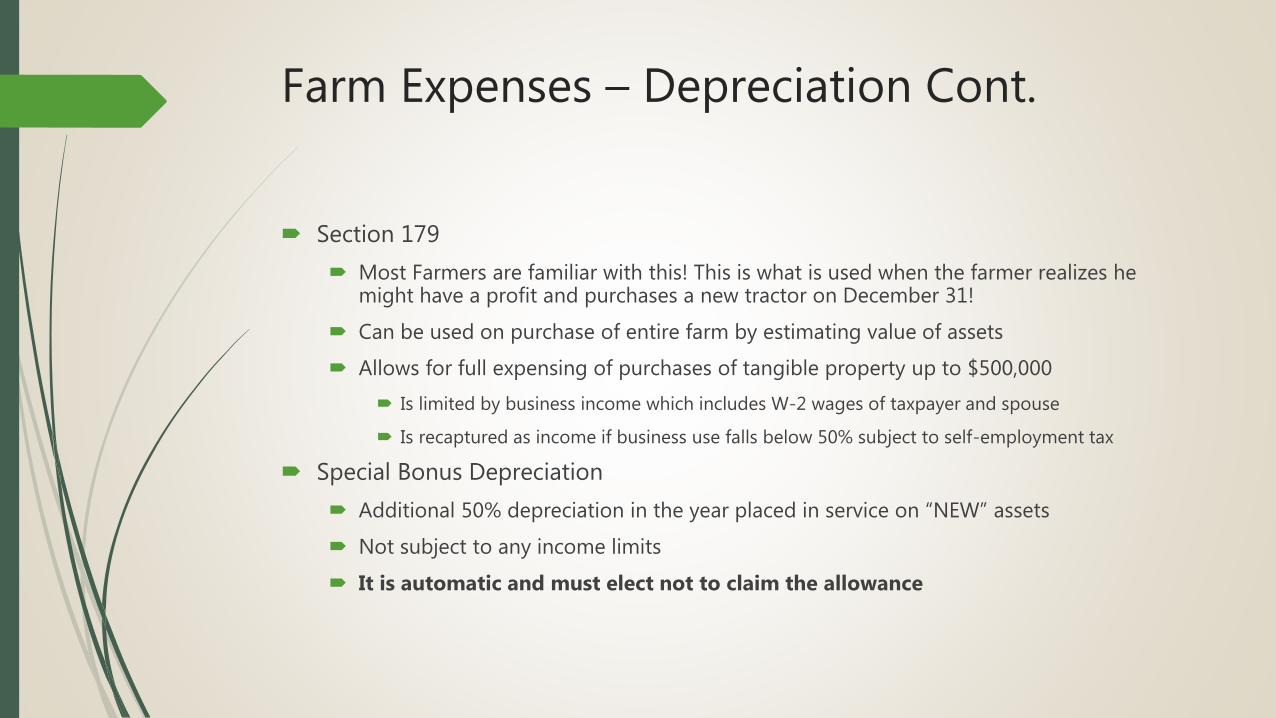

Farm Expenses – Depreciation Cont.

Section 179

Most Farmers are familiar with this! This is what is used when the farmer realizes he might have a profit and purchases a new tractor on December 31!

Can be used on purchase of entire farm by estimating value of assets

Allows for full expensing of purchases of tangible property up to $500,000

Is limited by business income which includes W-2 wages of taxpayer and spouse

Is recaptured as income if business use falls below 50% subject to self-employment tax

Special Bonus Depreciation

Additional 50% depreciation in the year placed in service on “NEW” assets

Not subject to any income limits

It is automatic and must elect not to claim the allowance

Farm Expenses – Depreciation Cont.

Annual Depreciation is calculated on useful life

Example: Farm equipment is purchased for 10,000. Since this is 7year property, you multiply$10,000 by 10.71% to get this year's depreciation of $1,071. For next year, your depreciationwill be $1,913 ($10,000 × 19.13%)

Self-Employment Tax

Farm Misc. – Self-Employment Tax

Regular Method

Calculated at 15.3% (12.4% for Social Security and 2.9% for Medicare)

Need $5,040 ($1,260x4) of self-employment income to earn the max of four SS credits/year.

All self employment income is combined for the calculation

A loss on a farm can reduce income from other business or partnership

Farm Optional Method

Allows you to get SS credits

Increases your earned income which can increase credits e.g. EIC

Bases self-employment earning off of 2/3 of gross farm income up to $5,040

½ of SE tax is deducted against taxable income

Farm Return Due Dates

Resources

Publication 225 – Farmer’s Tax Guide

Publication 51 (Circular A) – Agricultural Employer’s Tax Guide

Publication 463 – Travel, Entertainment, Gift & Car Expenses