Tax cute in tough times - who really gains?

25

Tax cuts in tough times – who really gains? Gavin Kelly – Resolution Foundation Matthew Whittaker – Resolution Foundation Tim Montgomerie – The Times Polly Toynbee – The Guardian Stephen Tall – Lib Dem Voice Gary Gibbon – Channel 4 #taxcuts

-

Upload

resolutionfoundation -

Category

Economy & Finance

-

view

354 -

download

0

Transcript of Tax cute in tough times - who really gains?

Tax cuts in tough times – who really gains?

Gavin Kelly – Resolution Foundation

Matthew Whittaker – Resolution Foundation

Tim Montgomerie – The Times

Polly Toynbee – The Guardian

Stephen Tall – Lib Dem Voice

Gary Gibbon – Channel 4#taxcuts

Tax cuts in tough times –

who really gains?

November 2014

Gavin Kelly & Matthew Whittaker

Been here before:

• Promises of tax cuts often precede post-election tax rises

But also an especially challenging context:

• Fall in living standards politics tax cuts

• Big deficit and fiscal constraint economics tax rises

Pre-election promises

All parties are pointing to some tax cuts

Different scale

Different sources of funding

(with distributional implications)

Shared rhetoric of supporting households on low to middle incomes/ low paid

Shared ‘candour deficit’ about tax rises/implications of fiscal tightening

Assessing the current debateSome differences, some similarities

Focused on tax cuts for low earners?

What about NI (‘forgotten’ tax payers)

Focused on disposable income of low to middle income families?

What about Universal Credit

Silence on both.....

Assessing the current debateSome shared blind spots

Our starting point?

• Even if tightening overall: still case for tax reform

• Context means distributional choices matter even more

• All proposals must be fully funded

Caveats• Raising living standards clearly depend on wider factors

• Narrow focus today on personal tax/in-work benefits

• If fiscal position deteriorates further then all bets off...

Presenting the alternativesSome important caveats

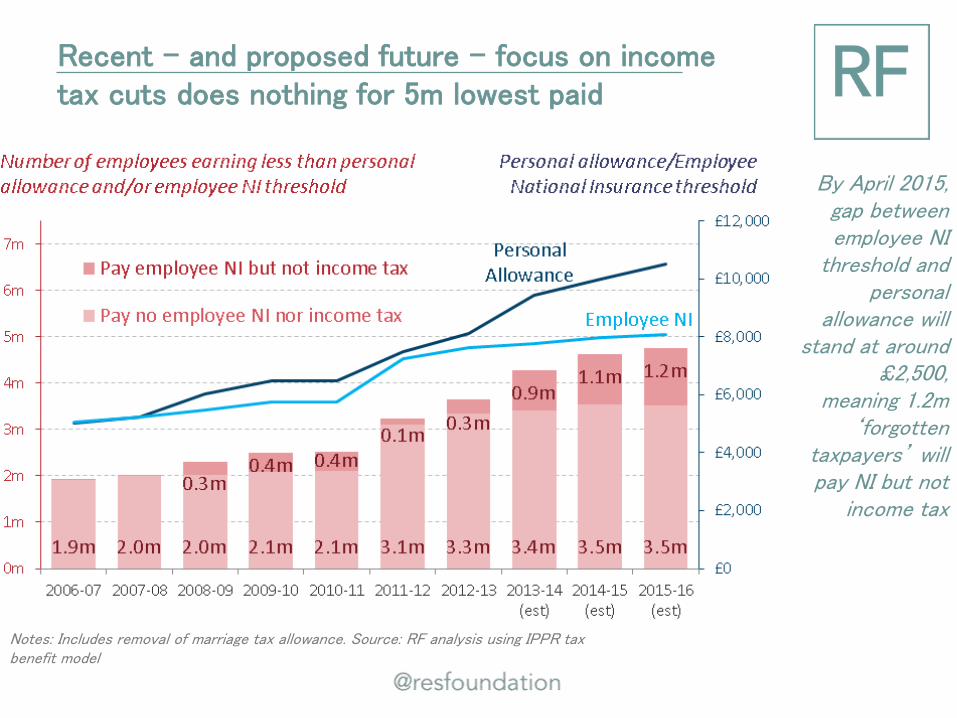

Recent – and proposed future – focus on incometax cuts does nothing for 5m lowest paid

Each increase in the personal allowance has increased the

number of employees who

no longer benefit from

further movements

Notes: Includes removal of marriage tax allowance. Source: RF analysis using IPPR tax benefit model

Recent – and proposed future – focus on incometax cuts does nothing for 5m lowest paid

By April 2015, gap between employee NI

threshold and personal

allowance will stand at around

£2,500

Notes: Includes removal of marriage tax allowance. Source: RF analysis using IPPR tax benefit model

Recent – and proposed future – focus on incometax cuts does nothing for 5m lowest paid

By April 2015, gap between employee NI

threshold and personal

allowance will stand at around

£2,500, meaning 1.2m

‘forgotten taxpayers’ will pay NI but not

income tax

Notes: Includes removal of marriage tax allowance. Source: RF analysis using IPPR tax benefit model

Lib Dem approach provides biggest proportional gain in deciles 6-8 in 2020-21

Based on increasing

personal allowance to

£12.5k in April 2020 and removing

marriage tax allowance

Notes: Includes removal of marriage tax allowance. Source: RF analysis using IPPR tax benefit model

Conservative approach provides biggest proportional gain in deciles 7-9 in 2020-21

Based on increasing

personal allowance to

£12.5k in April 2020 and

raising higher rate threshold

to £50k

Source: RF analysis using IPPR tax benefit model

UKIP approach provides biggest proportional gain in deciles 7-9 in 2020-21

Based on increasing

personal allowance to

£13.5k in April 2020 (it might

be FAR higher) and introducing a 35p tax band that stretches from £47k to £61k by 2020

Notes: We model £13.5k PA in 2020, but UKIP’s proposal could be interpreted as equating to a level closer to £16k by then. 35p band is promised between existing higher rate threshold and £55k, we assume it rises with inflation over the course of the parliament. Source: RF analysis using IPPR tax benefit model

Labour approach provides biggest proportional gain in deciles 6-8 in 2020-21

10p band on the first £300

of income above the

personal allowance in 2016 (rising

with inflation for rest of

parliament). Labour say:

paid for by removing

marriage tax allowance

Notes: Includes removal of marriage tax allowance. Source: RF analysis using IPPR tax benefit model

Proposals vary hugely in size (and in regressivity) – but all skewed upwards

Modelled proposals vary from a cost of £900m to (at least) £13bn,

but households in the top half of the income

distribution consistently do

best

Source: RF analysis using IPPR tax benefit model

Clear majority of gains go to households in the top half of the distribution

Notes: Distribution of gains per £1 spent on the different proposals as modelled in 2020-21. Source: RF analysis using IPPR tax benefit model

Based on the distribution of costs

across household income deciles

Bottom half of households account for no morethan a quarter of the cost in all cases

Notes: Distribution of gains per £1 spent on the different proposals as modelled in 2020-21. Source: RF analysis using IPPR tax benefit model

Of every £1 spent, the bottom 50% account for

25p under the Lib Dems

24p under Labour

19p under UKIP

18p under the Conservatives

Top fifth of households account for between one-third and one-half

Notes: Distribution of gains per £1 spent on the different proposals as modelled in 2020-21. Source: RF analysis using IPPR tax benefit model

Of every £1 spent,the top 20% account for

31p under the Lib Dems

34p under Labour

43p under UKIP

46p under the Conservatives

Focusing support on work allowances underUC is more targeted

Based on a 20% increase in

‘lower’ work allowances and corresponding

cash increases in ‘higher’

work allowances

Source: RF analysis using IPPR tax benefit model

Combined – and funded – package provides more progressive outcome

Based on a 20% increase in

work allowances and realignment of

NI threshold and PA

Paid for via 3-year freeze in

PA; 2-year freeze in basic

rate limit; extension of NI to workers over

the state pension age

Source: RF analysis using IPPR tax benefit model

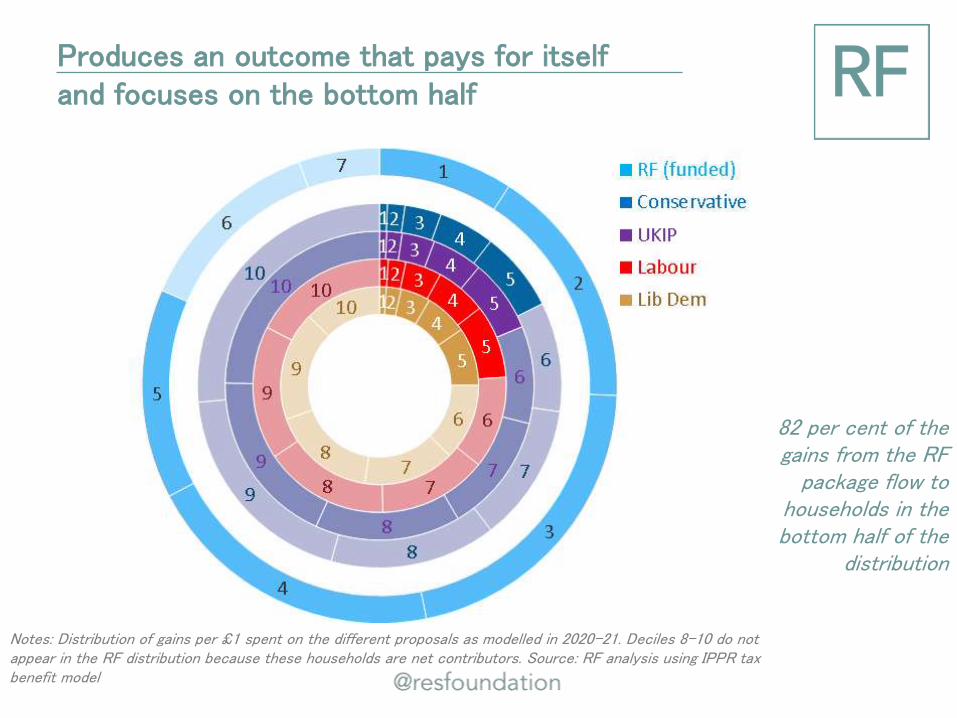

Produces an outcome that pays for itself and focuses on the bottom half

Notes: Distribution of gains per £1 spent on the different proposals as modelled in 2020-21. Deciles 8-10 do not appear in the RF distribution because these households are net contributors. Source: RF analysis using IPPR tax benefit model

Produces an outcome that pays for itself and focuses on the bottom half

Notes: Distribution of gains per £1 spent on the different proposals as modelled in 2020-21. Deciles 8-10 do not appear in the RF distribution because these households are net contributors. Source: RF analysis using IPPR tax benefit model

82 per cent of the gains from the RF

package flow to households in the bottom half of the

distribution

• Unlike party promises, benefits enjoyed by low to middle income households, working-age, families with children and those earning less than £10.5k

Very different set of outcomes from theparty approaches

• Unlike party promises, benefits enjoyed by low to middle income households, working-age, families with children and those earning less than £10.5k

• Other benefits include:

– Reduced effective tax rates for some lower earners

– Major simplification of tax system

– Pre-requisite for integration of NI with income tax

Very different set of outcomes from theparty approaches

• Parties’ focus on income tax cuts are hard to justify during fiscally tough times

• They all miss the purported target. No rationale for benefiting those above £10.5k while ignoring those on £8k

• UC work allowances provide more targeted support

• As part of a majoritarian package that prioritises work allowances, raising the NI threshold is clearly better than raising the personal allowance and simplifies tax system

Other packages could be pursued – but the principle of prioritising UC remains

Tax cuts in tough times – who really gains?

Gavin Kelly – Resolution Foundation

Matthew Whittaker – Resolution Foundation

Tim Montgomerie – The Times

Polly Toynbee – The Guardian

Stephen Tall – Lib Dem Voice

Gary Gibbon – Channel 4#taxcuts