Swiss Equities Conference - Credit Suisse · Jakarta Cape Town Johannesburg Athens Mumbai Lisbon...

27

Swiss Equities Conference Credit Suisse: Private Banking update New York September 28, 2006 Walter Berchtold, CEO Private Banking

-

Upload

nguyenkiet -

Category

Documents

-

view

214 -

download

0

Transcript of Swiss Equities Conference - Credit Suisse · Jakarta Cape Town Johannesburg Athens Mumbai Lisbon...

Swiss Equities Conference

Credit Suisse: Private Banking update

New YorkSeptember 28, 2006

Walter Berchtold, CEO Private Banking

Swiss Equities ConferenceSlide 2

Disclaimer

Cautionary statement regarding forwardCautionary statement regarding forwardCautionary statement regarding forwardCautionary statement regarding forward----looking informationlooking informationlooking informationlooking information

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995.

Forward-looking statements involve inherent risks and uncertainties, andwe might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements.

A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in"Risk Factors" in our Annual Report on Form 20-F for the fiscal yearended December 31, 2005 filed with the US Securities and Exchange Commission, and in other public filings and press releases.

We do not intend to update these forward-looking statements except as may be required by applicable laws.

Swiss Equities ConferenceSlide 3

Credit Suisse: Key facts & Figures as of 30 June 2006

� Global financial services company with presence in Europe, Middle East, Africa, Americas, and Asia

� 44,100 employees1)

� Registered shares are listed in Switzerland and as American Depositary Shares in New York

� CHF 7.5 bn pre-tax income

� CHF 1,371 bn AuM

� 25.4% Return on Equity

1) Banking businesses only

Swiss Equities ConferenceSlide 4

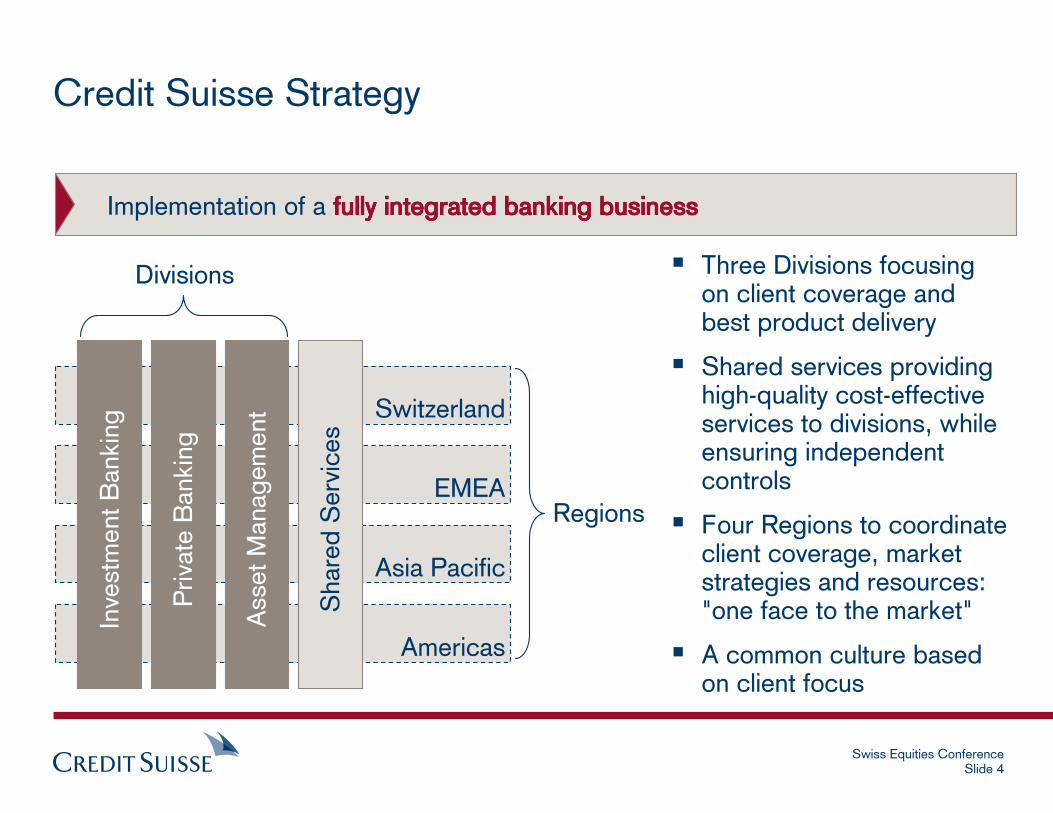

Credit Suisse Strategy

� Three Divisions focusingon client coverage andbest product delivery

� Shared services providing high-quality cost-effective services to divisions, whileensuring independent controls

� Four Regions to coordinate client coverage, market strategies and resources: "one face to the market"

� A common culture basedon client focus

Switzerland

EMEA

Asia Pacific

Americas

Inve

stm

ent B

ankin

g

Priva

te B

ankin

g

Asset M

anag

em

ent

Share

d S

erv

ices

Divisions

Regions

Implementation of a fully integrated banking businessfully integrated banking businessfully integrated banking businessfully integrated banking business

Swiss Equities ConferenceSlide 5

Private Banking: Key Facts and Figures as of 30 June 2006

1) Excluding Shared Services headcount allocation of approx. 6,000 FTEs

� 2.5 million clients

– ~630,000 WM

– ~1,900,000 CRB

� 15,000 employees1)

� Global franchise

� CHF 6.0 bn net revenue

� CHF 2.4 bn pre-tax income

� CHF 859 bn AuM

� CHF 165 bn loans

Swiss Equities ConferenceSlide 6

Pretax Income (in CHF m)

1) Annualized

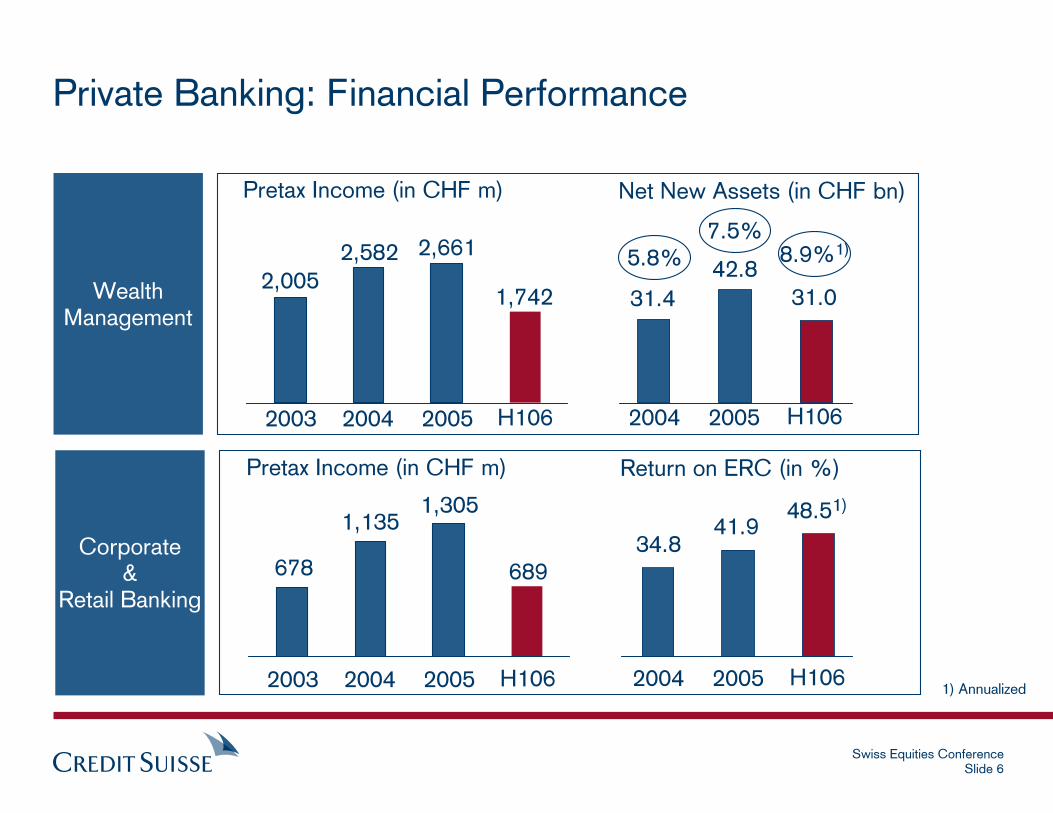

Private Banking: Financial Performance

Net New Assets (in CHF bn)

5.8%7.5%

Pretax Income (in CHF m) Return on ERC (in %)

2,005

2,582 2,661

1,742 31.4

42.8

31.0

34.841.9

48.51)

678

1,1351,305

689

WealthManagement

Corporate &

Retail Banking

2003 2004 2005 H106 2004 2005 H106

8.9%1)

2003 2004 2005 H106 2004 2005 H106

Swiss Equities ConferenceSlide 7

Wealth Management vs Brokerage: More Comprehensive Business Model; Higher Margins

� Gross margin 100-120 bps

� Cost-income 50-70%

� Compensation: Salary plus bonus

Wealth management Wealth management Wealth management Wealth management

� Comprehensive advisory, e.g. financial planning

� Discretionary mandates / fiduciary services

� Broad range of investment products, e.g. third party

� Wealth-related services, e.g. tax & inheritance consulting, trusts

� Broad range of lending products

BrokerageBrokerageBrokerageBrokerage

� Securities investments (advice, execution)

� Selected proprietary investment products

� Equity research

� Custody services

� Selective lending

� Gross margin 50-70 bps

� Cost-income 80-95%

� Compensation: Commission -based

Market Characteristics

Swiss Equities ConferenceSlide 8

CS is a Leading Global Player in Wealth Management

121

203

224

246

260

353

355

466

659

982UBS

Credit Suisse

Citigroup

Merrill Lynch

HSBC

Deutsche Bank

JP Morgan

BNP Paribas

ABN Amro

Julius Baer

Global AuM of competitors 2005 (CHF bn), excl. brokerage business

Source: CS estimates

Swiss Equities ConferenceSlide 9

Increasing Global Wealth Management Franchise

Service locations

Los Angeles

MiamiNassau

San Francisco

Dallas

ChicagoBoston

AtlantaNew York

Mexico

Caracas

Bogotá

Lima

SantiagoBuenos Aires

Montevideo

São PauloRio de Janeiro

Moscow

Cairo

Istanbul

Dubai

St. Petersburg

Abu Dhabi

Beijing

Shanghai

TaipeiGuangzhouHong Kong

Bangkok

Singapore

Jakarta

Cape Town

Johannesburg

Athens

Mumbai

Lisbon

Madrid

ParisZurich

ViennaFrankfurt

London

Guernsey

Gibraltar

Milan

Luxembourg

BeirutDoha

Baltimore

Monaco

Sydney1)

1) as of Nov 1, 2006; Status: 12 September, 2006

� Switzerland: 75 service locations

� Germany: 14 service locations

� Italy: 32 service locations

� France: 3 service locations

� Spain: 3 service locations

Melbourne1)

Swiss Equities ConferenceSlide 10

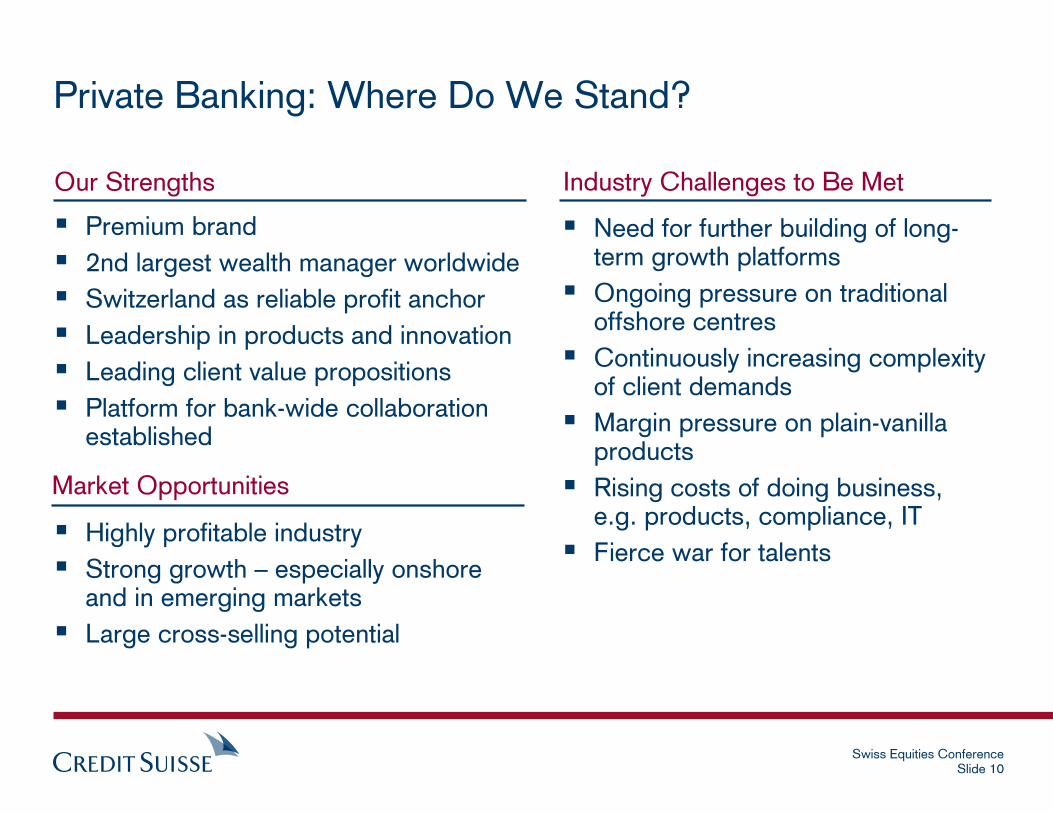

� Premium brand

� 2nd largest wealth manager worldwide

� Switzerland as reliable profit anchor

� Leadership in products and innovation

� Leading client value propositions

� Platform for bank-wide collaboration established

� Need for further building of long-term growth platforms

� Ongoing pressure on traditional offshore centres

� Continuously increasing complexity of client demands

� Margin pressure on plain-vanilla products

� Rising costs of doing business, e.g. products, compliance, IT

� Fierce war for talents

Our Strengths Industry Challenges to Be Met

Private Banking: Where Do We Stand?

Market Opportunities

� Highly profitable industry

� Strong growth – especially onshore and in emerging markets

� Large cross-selling potential

Swiss Equities ConferenceSlide 11

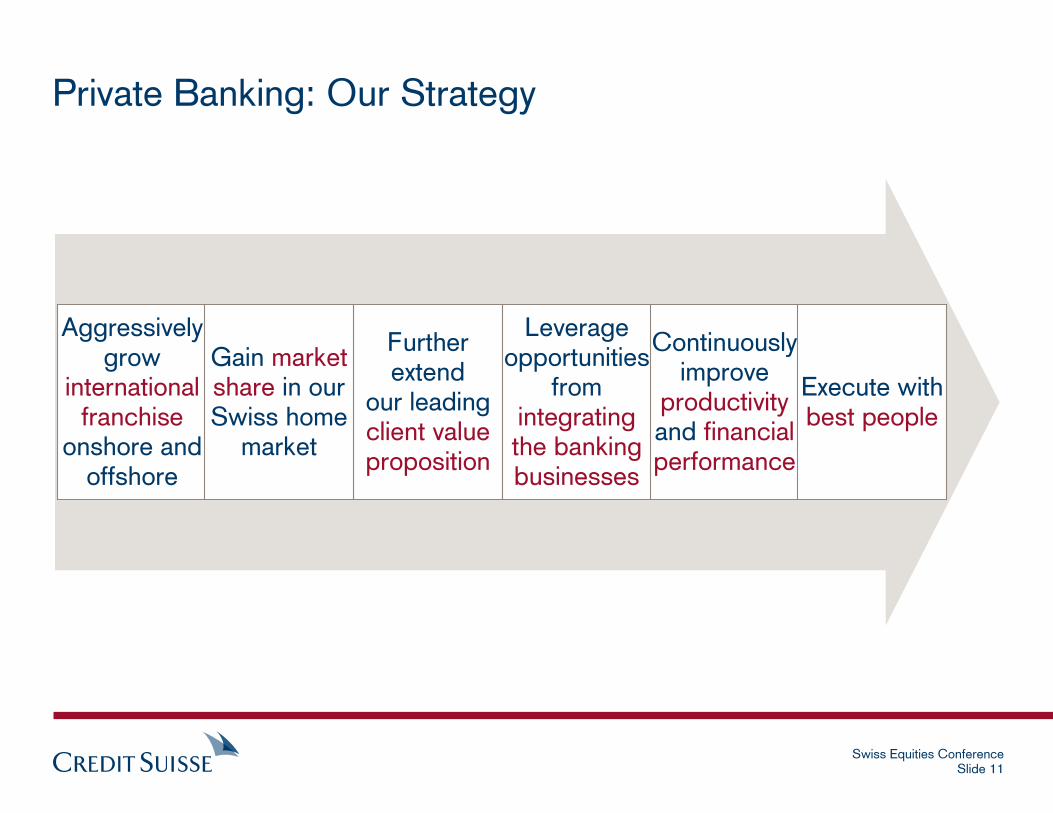

Private Banking: Our Strategy

Further extend

our leading client value proposition

Aggressively grow

international franchise

onshore and offshore

Gain market share in our Swiss home

market

Leverage opportunities

from integrating the banking businesses

Continuously improve

productivityand financial performance

Execute with best people

Swiss Equities ConferenceSlide 12

Markets: Asia-Pacific

� Explore opportunities in China; build Shanghai branch and explore JV opportunities

� Leverage Singapore and Hong Kong hubs, upgrade IT platform

� Build on and expand onshore presence, e.g. Indonesia and Australia

35

50

+43%

2004 2005

� NNA: ~19% annual growth

� Margins: stable environment

Way Forward

AuM (in CHF bn) Expected Development

Swiss Equities ConferenceSlide 13

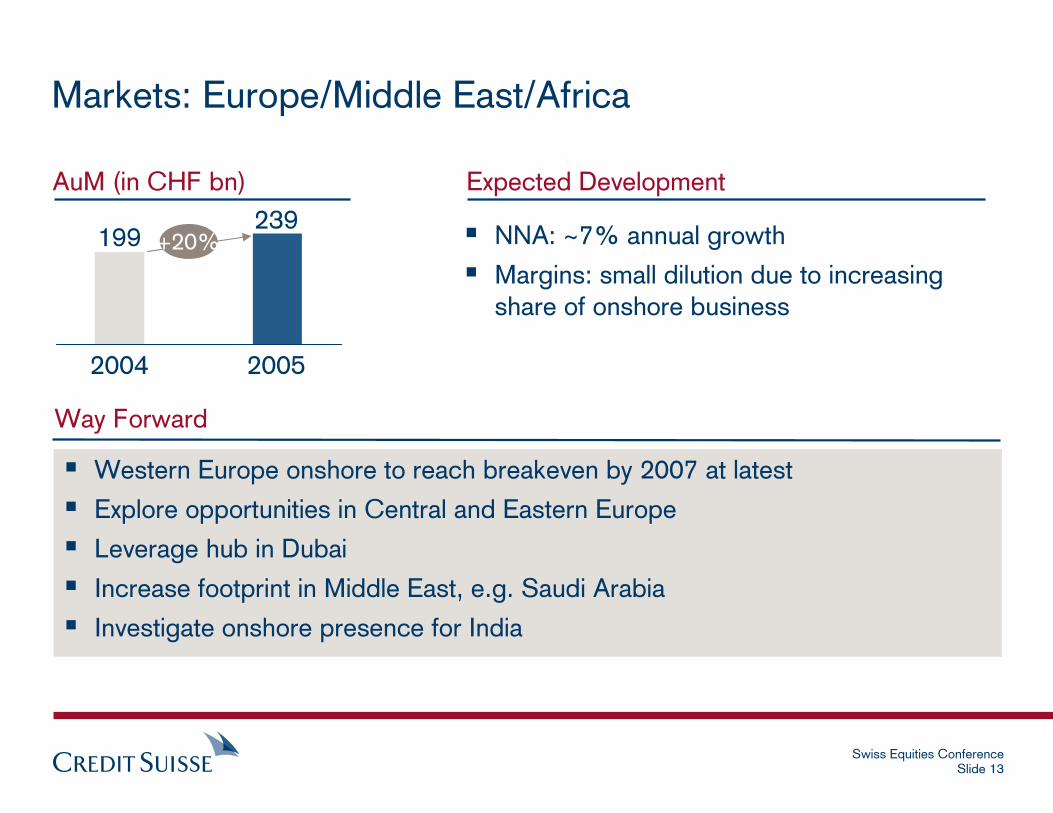

Markets: Europe/Middle East/Africa

Way Forward

� Western Europe onshore to reach breakeven by 2007 at latest

� Explore opportunities in Central and Eastern Europe

� Leverage hub in Dubai

� Increase footprint in Middle East, e.g. Saudi Arabia

� Investigate onshore presence for India

199239

+20% � NNA: ~7% annual growth

� Margins: small dilution due to increasing share of onshore business

2004 2005

AuM (in CHF bn) Expected Development

Swiss Equities ConferenceSlide 14

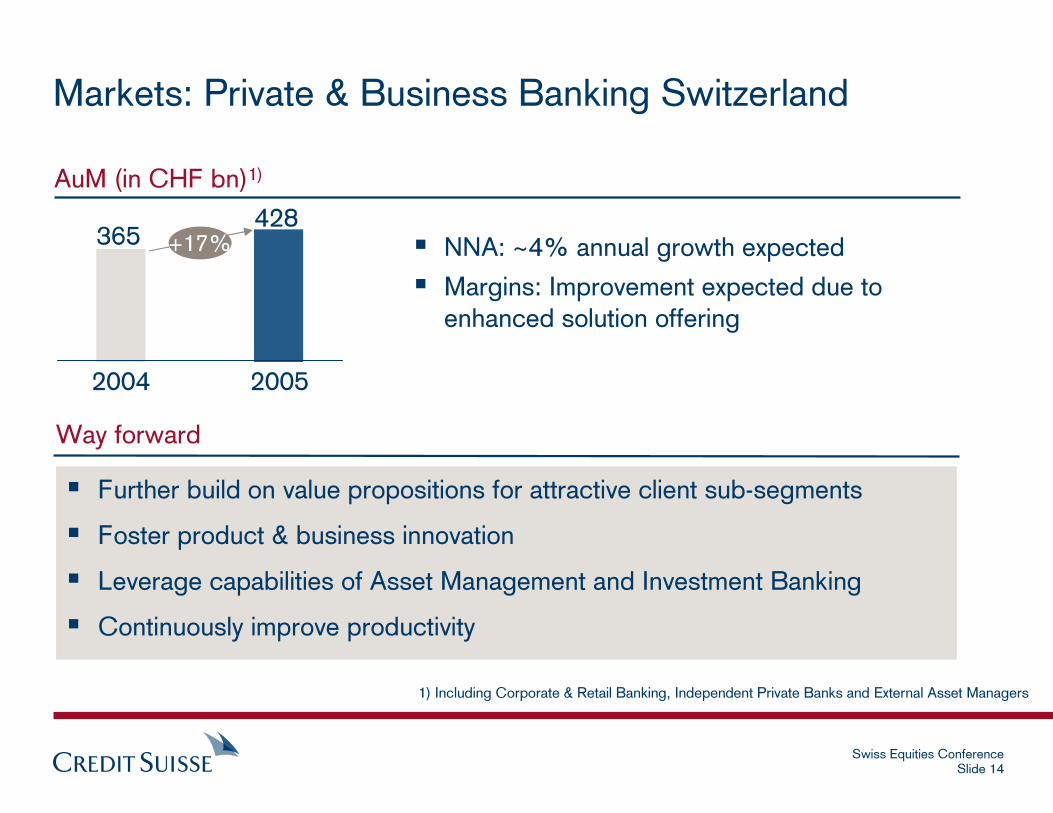

Markets: Private & Business Banking Switzerland

� Further build on value propositions for attractive client sub-segments

� Foster product & business innovation

� Leverage capabilities of Asset Management and Investment Banking

� Continuously improve productivity

365428

+17%

1) Including Corporate & Retail Banking, Independent Private Banks and External Asset Managers

� NNA: ~4% annual growth expected

� Margins: Improvement expected due to enhanced solution offering

2004 2005

AuM (in CHF bn)1)

Way forward

Swiss Equities ConferenceSlide 15

Markets: Americas

� Build comprehensive Wealth Management in US

� Strengthen footprint in Latin America, e.g. onshore presence in Brazil

� Explore onshore opportunities in other countries

92 +23% � NNA: ~10% annual growth

� Margins: improvement expected given transformation toward comprehensive wealth management business model in US

2004 2005

AuM (in CHF bn)

Way Forward

113

Expected Development

Swiss Equities Conference

Credit Suisse: Private Banking AmericasNew YorkSeptember 28, 2006

Anthony DeChellis, Head of PB Americas

Swiss Equities ConferenceSlide 17

Private Banking presence in Americas

USA highlights (as per Aug 2006)

Clients Clients Clients Clients

� > CHF 5mn average AuM

Relationship mangersRelationship mangersRelationship mangersRelationship mangers

� > CHF 1.2mn average revenue per experienced relationship manager

Size of business Size of business Size of business Size of business

� AuM: CHF 83.3 bn

Footprint Footprint Footprint Footprint

� Offices in 9 major regional wealth centers

� Offices in 8 major regional locationsService locations

Los Angeles

MiamiNassau

San Francisco

Dallas

ChicagoBoston

AtlantaNew York

Mexico

Caracas

Bogotá

Lima

SantiagoBuenos Aires

Montevideo

São PauloRio de Janeiro

Baltimore

Latin America footprint

Swiss Equities ConferenceSlide 18

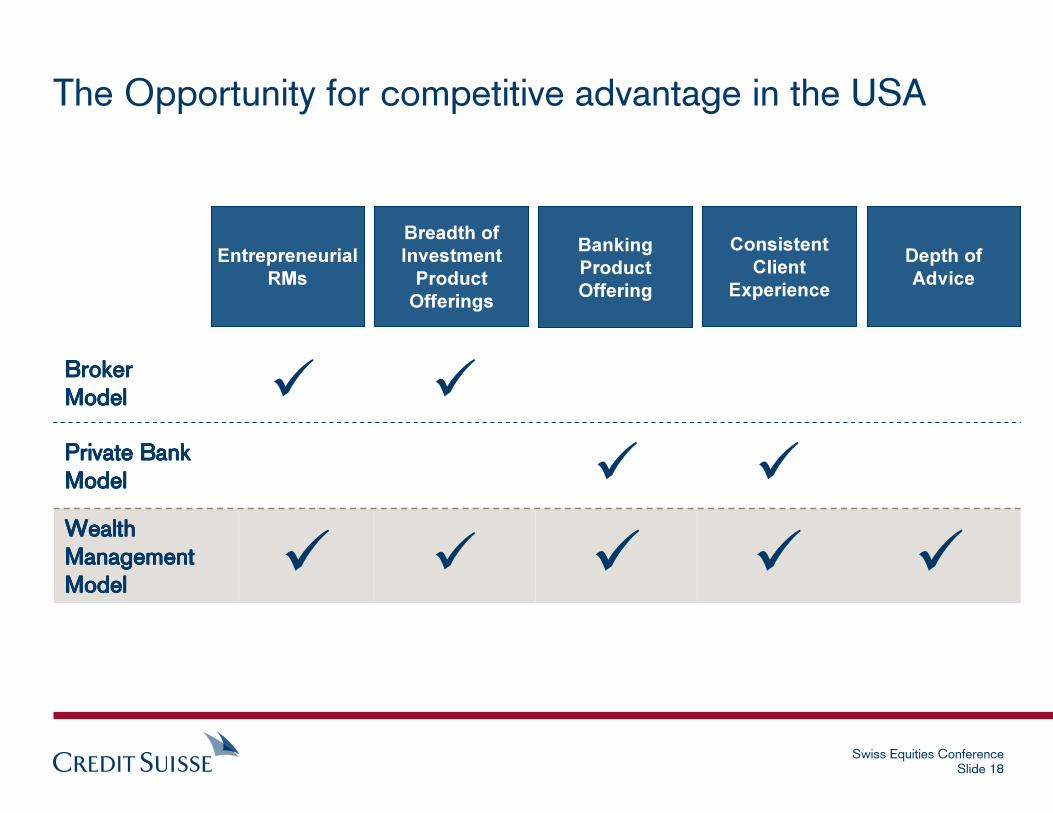

The Opportunity for competitive advantage in the USA

�

�

����Wealth Wealth Wealth Wealth

Management Management Management Management

ModelModelModelModel

�

�

�Private Bank Private Bank Private Bank Private Bank

ModelModelModelModel

Broker Broker Broker Broker

ModelModelModelModel

Entrepreneurial

RMs

Breadth of

Investment

Product

Offerings

Consistent

Client

Experience

Depth of

Advice

Banking

Product

Offering

Swiss Equities ConferenceSlide 19

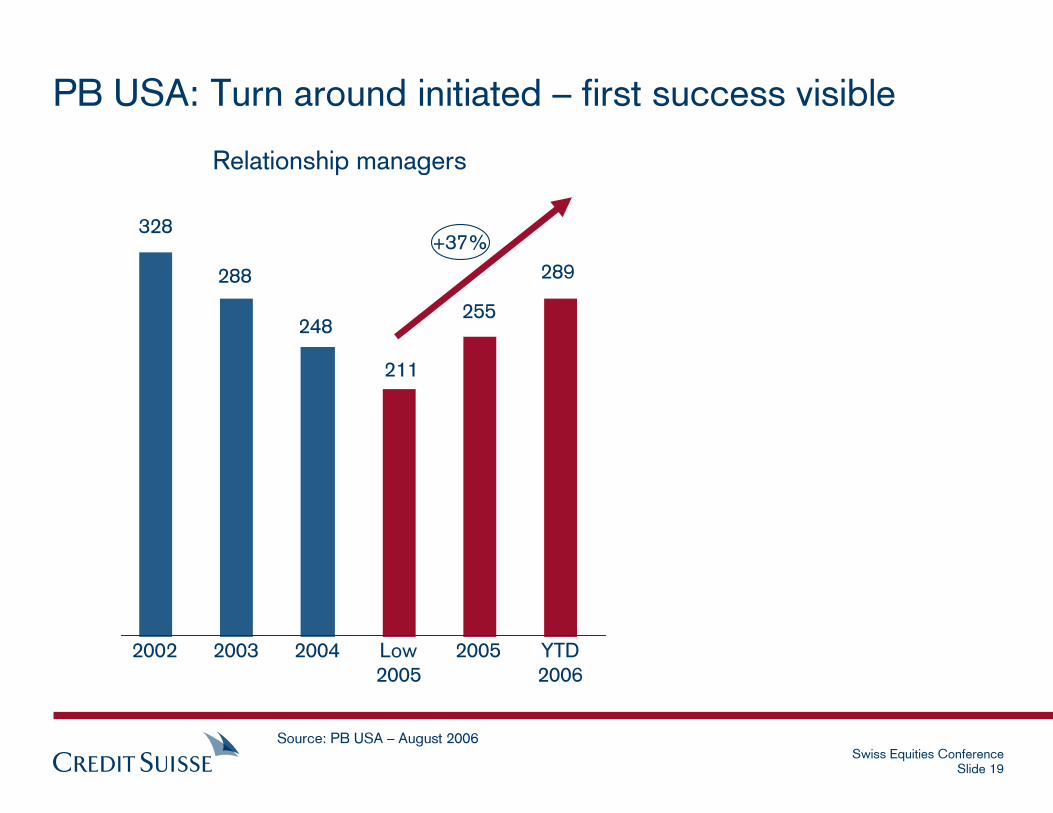

PB USA: Turn around initiated – first success visible

Source: PB USA – August 2006

+37%

211

255

289

20032002 2004 Low

2005

2005 YTD

2006

288

328

248

Relationship managers

Swiss Equities ConferenceSlide 20

PB USA: Turn around initiated – first success visible

Source: PB USA – August 2006

+37%

211

255

289

20032002 2004 Low

2005

2005 YTD

2006

288

328

248

+560%

1.4

6.5

10.0

2004 2005 YTD

2006

Relationship managers NNA (CHF bn)

Swiss Equities ConferenceSlide 21

Our vision for Private Banking USAOur vision for Private Banking USA

� Preeminent wealth manager in US (top 5 player) Preeminent wealth manager in US (top 5 player) Preeminent wealth manager in US (top 5 player) Preeminent wealth manager in US (top 5 player) � Best client experience for UHNW segmentBest client experience for UHNW segmentBest client experience for UHNW segmentBest client experience for UHNW segment� Employer of choice for bestEmployer of choice for bestEmployer of choice for bestEmployer of choice for best----inininin----class class class class RMsRMsRMsRMs

Best-in-Class RMs

and Specialists

Consistent Value

Creation

State-of-the-Art Products and

Support

Prestigious UHNW

Positioning

Leveraging IB and AM

Platform

and

Resources

PeopleClient

ExperienceBrandOne Bank

PB USA

Vision

Swiss Equities ConferenceSlide 22

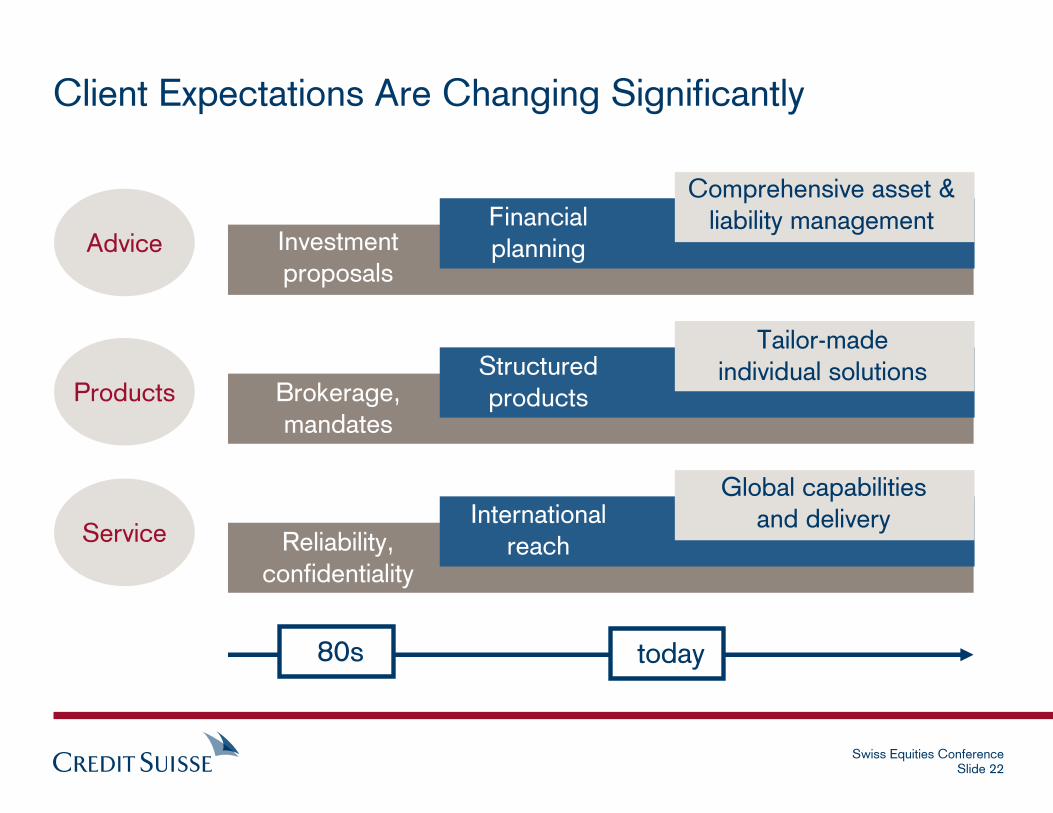

Client Expectations Are Changing Significantly

Advice

Products

Service

today

Investment proposals

Financial planning

Brokerage, mandates

Structured products

Tailor-made individual solutions

Reliability, confidentiality

International reach

Global capabilities and delivery

80s

Comprehensive asset & liability management

Swiss Equities ConferenceSlide 23

Client Value: Key Building Blocks for True Client Focus

� Relationship managers& specialists

� Products and solutions

� Processes and tools

� Client experience

Analysis Delivery

� Client needs/ Voice of the Customer

� Client profitability and wallet share

� Competitivepositioning

Clear, unique and valuable set of offerings and services for a defined, attractive client group

Design

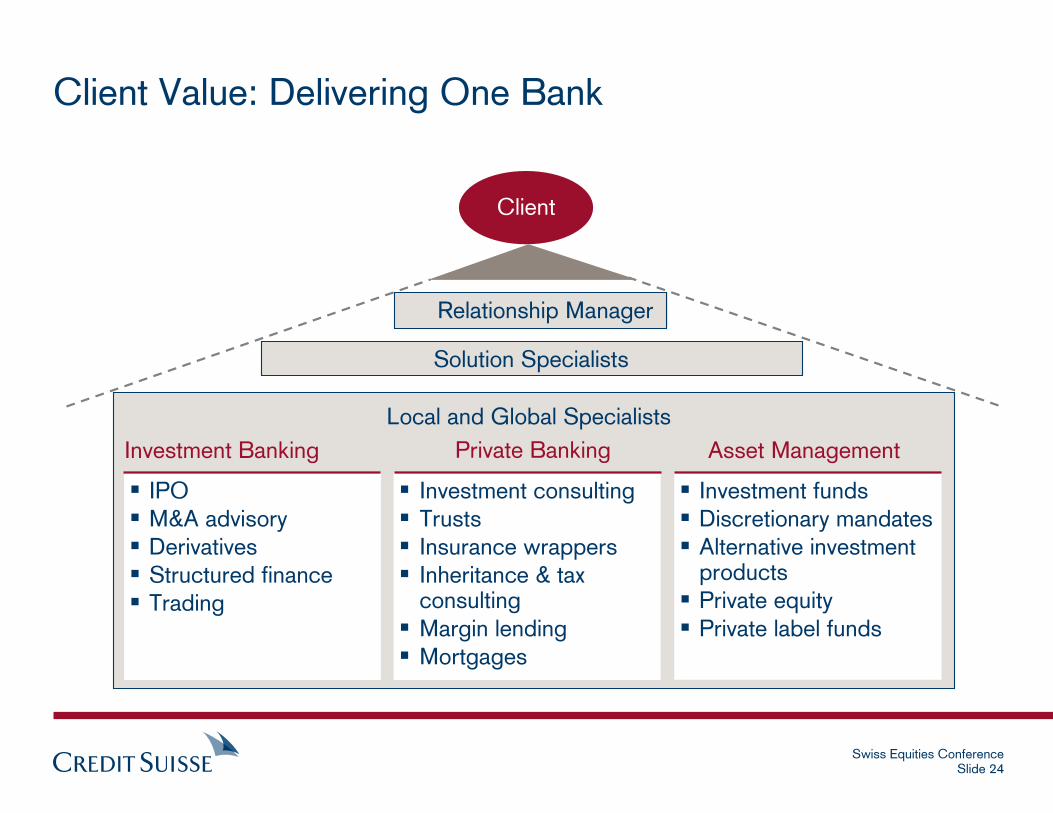

Swiss Equities ConferenceSlide 24

Client

� Investment funds� Discretionary mandates� Alternative investment

products� Private equity

� Private label funds

� IPO� M&A advisory� Derivatives� Structured finance� Trading

Client Value: Delivering One Bank

Investment Banking

� Investment consulting� Trusts� Insurance wrappers� Inheritance & tax

consulting

� Margin lending� Mortgages

Asset ManagementPrivate Banking

Solution Specialists

Relationship Manager

Local and Global Specialists

Swiss Equities ConferenceSlide 25

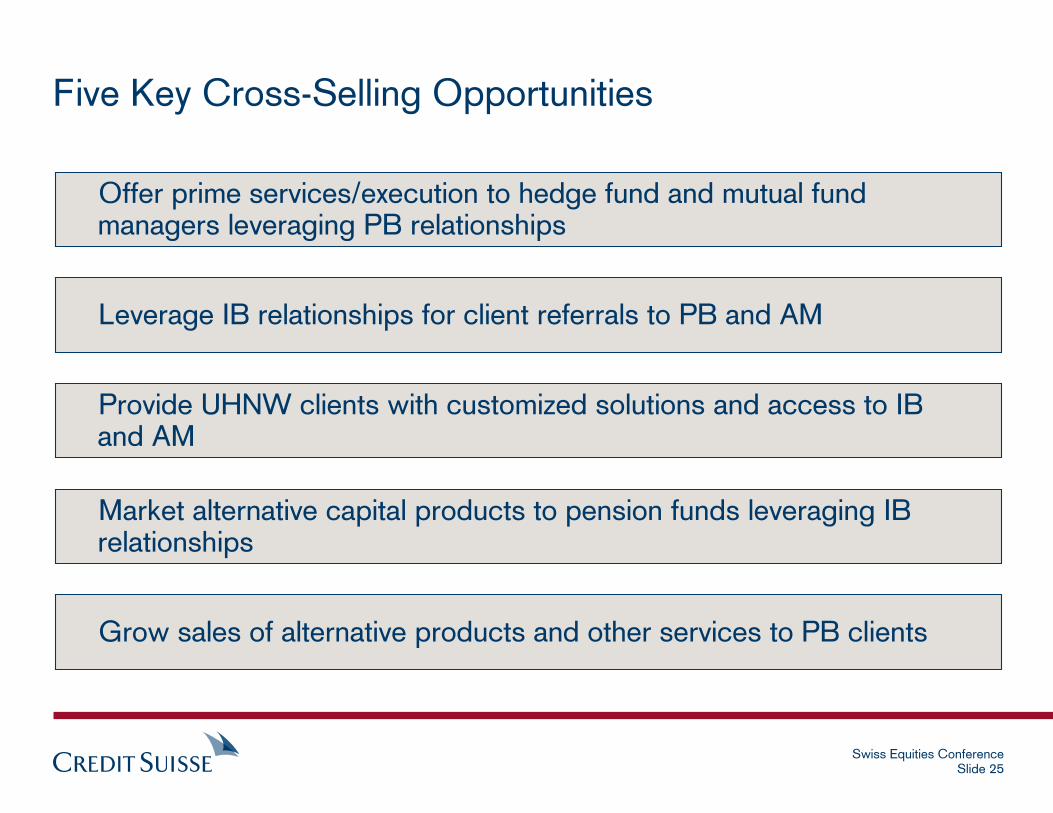

Five Key Cross-Selling Opportunities

Leverage IB relationships for client referrals to PB and AM

Provide UHNW clients with customized solutions and access to IB and AM

Market alternative capital products to pension funds leveraging IB relationships

Grow sales of alternative products and other services to PB clients

Offer prime services/execution to hedge fund and mutual fund managers leveraging PB relationships

Swiss Equities ConferenceSlide 26

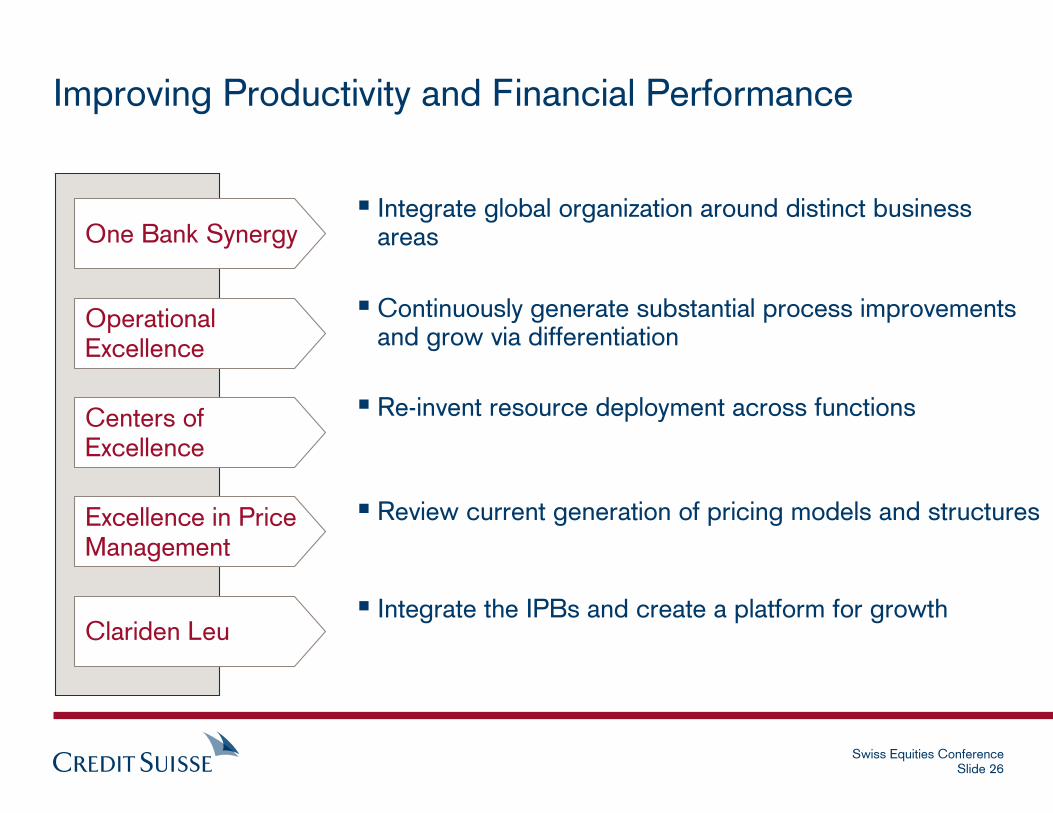

Improving Productivity and Financial Performance

Operational Excellence

One Bank Synergy

Excellence in Price Management

Clariden Leu

Centers of Excellence

� Re-invent resource deployment across functions

� Continuously generate substantial process improvements and grow via differentiation

� Integrate global organization around distinct business areas

� Review current generation of pricing models and structures

� Integrate the IPBs and create a platform for growth

Swiss Equities ConferenceSlide 27