Swedbank Economic Outlook August 2016

65

© Swedbank Swedbank Economic Outlook August 2016 Populism – the Achilles’ heel of the global recovery • Weak global growth – risks mainly related to politics • Swedish boom fades as structural challenges rises • Growth in the Baltics should pick up next year

Transcript of Swedbank Economic Outlook August 2016

© Swedbank

Swedbank Economic Outlook August 2016

Populism – the Achilles’ heel of the global recovery • Weak global growth – risks mainly related to politics

• Swedish boom fades as structural challenges rises

• Growth in the Baltics should pick up next year

© Swedbank

• The global economy

– Still reeling from the great recession

– Populism grows on the back of stagnant wages

– Only a very gradual normalisation of monetary

policy

• Sweden

– Dependent on its domestic sectors

– Housing shortage needs to be tackled

– Polarisation of the labour market

– The Riksbank continues to tiptoe

• Norway

– The worst is (probably) behind us

• Estonia: More mature and more slow

• Latvia: The breeze is yet to fill the sails

• Lithuania: Bronze in rowing and canoeing

Summary

2

Current themes

3

Populism grows as the world is

still reeling from the great

recession – rifts deepen among

countries in Europe

Lower growth, stagnant wages

and weaker productivity growth

is a pattern emerging in many

Western countries

Sweden faces difficulties ahead

with a increased polarization on

the labour market and an acute

housing shortage.

Source: Riksbank

© Swedbank

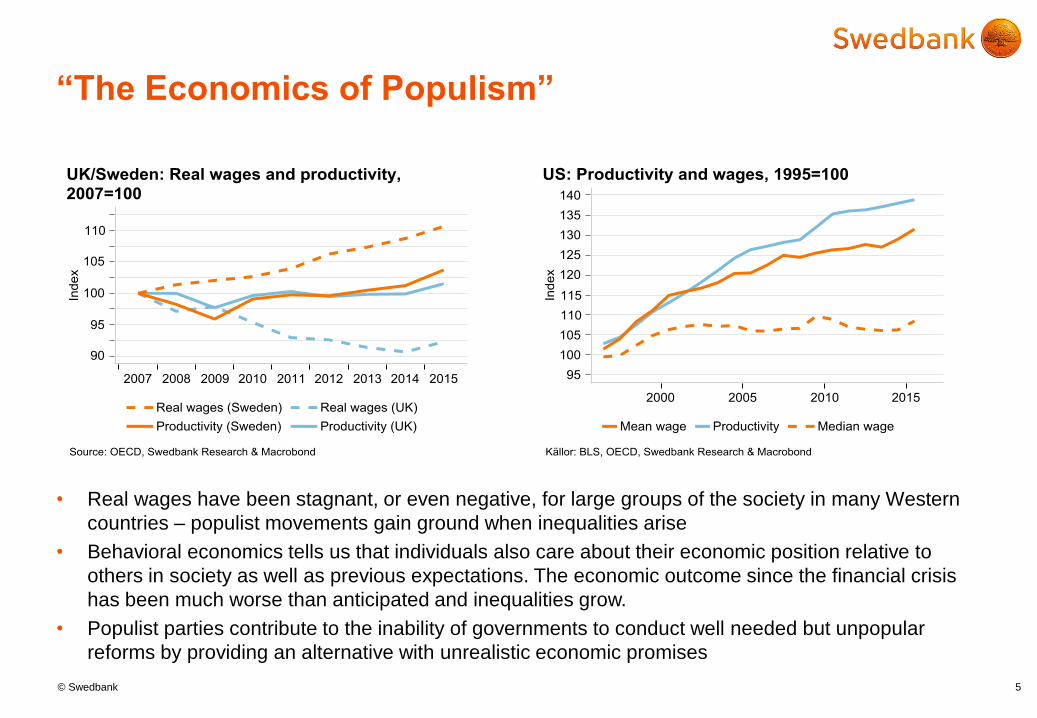

“The Economics of Populism”

4

• The past eight years represent the deepest global crisis since the depression in the 1930’s. Negative

chocks with lower real wages and high unemployment rate fules populist movements.

• Potential growth is significantly lower than what was forecasted before the financial crisis. The

difference between expected and actual outcome is startling.

• Structural challenges ahead related to lower productivity growth and an aging population emphasizes

the challenges of global growth ahead.

© Swedbank

“The Economics of Populism”

• Real wages have been stagnant, or even negative, for large groups of the society in many Western

countries – populist movements gain ground when inequalities arise

• Behavioral economics tells us that individuals also care about their economic position relative to

others in society as well as previous expectations. The economic outcome since the financial crisis

has been much worse than anticipated and inequalities grow.

• Populist parties contribute to the inability of governments to conduct well needed but unpopular

reforms by providing an alternative with unrealistic economic promises

5

© Swedbank

Global outlook: Weak economic growth, low interest

rates and populist movements

• We see global growth at about 3% per year in the next few years. In the US the business cycle is

maturing and we expect growth at around potential, while the euro area is still recovering from the

crisis

• Diverging growth in emerging markets – continued slowdown in China, better prospects in India

and weak re-emergence of growth in Russia and Brazil.

• The difference between expected growth before the financial crisis and actual income is startling.

Swedbank’s global GDP forecast1/

(annual percentage change)

2015 2018

USA 2,6 1,6 (2,4) 2,2 (2,6) 1,8

EMU countries 1,6 1,6 (1,5) 1,5 (1,6) 1,5

Germany 1,5 1,8 (1,3) 1,2 (1,3) 1,1

France 1,2 1,3 (1,3) 1,3 (1,6) 1,6

Italy 0,6 0,7 (0,9) 1,0 (1,2) 1,1

Spain 3,2 3,0 (3,0) 2,4 (2,4) 2,2

Finland 0,2 0,8 (0,7) 0,7 (0,9) 1,1

UK 2,2 1,6 (1,9) 0,7 (2,1) 1,4

Denmark 1,0 1,3 (1,5) 1,9 (2,1) 2,0

Norw ay 1,0 0,6 (0,6) 1,5 (1,4) 2,3

Japan 0,6 0,5 (0,7) 0,8 (0,6) 0,6

China 6,9 6,6 (6,6) 6,5 (6,5) 6,5

India 7,2 7,3 (7,2) 7,3 (7,7) 7,7

Brazil -3,9 -2,9 (-3,5) 0,3 (0,0) 1,6

Russia -3,7 -0,8 (-1,8) 1,5 (1,5) 2,0

Global GDP in PPP 2/ 3,1 3,0 (3,2) 3,3 (3,7) 3,4

1/ April 2016 f orecasts in parentheses.

2/ IMF weights (rev ised 2015). Sources: IMF and Swedbank.

2016f 2017f

6

© Swedbank

Global outlook: Gradual normalization of interest rates

7

• Subdued but positive growth numbers in the US and in the euro area will allow a very slow and

gradual normalization of monetary policy. Risks remain on the downside.

• The Fed’s policy is affected by a slow recovery in the rest of the world. We expect two rate hikes

per year in the US in 2017 and 2018.

• The ECB will taper its asset purchases in 2017 and make a first hike towards the end of 2018.

© Swedbank

Interest rates

• Interest rates forecast to

slowly rise

• Curves remain flat

• Embarking on a

normalization out of an

abnormal period

• How far can long-term

interest rates go?

Exchange rates

• Pound sterling depreciated

sharply after Brexit

• No action in G10 currencies

makes investors turn to EM

• Undervalued krona held

back by the Riksbank

Global outlook: Interest and exchange rates

8

Interest and exchange rate forecasts, %

Outcome Forecast

2016 2016 2017 2017 2018 2018

25-Aug 31 Dec 30 Jun 31 Dec 30 Jun 31 Dec

Policy rates

Federal Reserve, USA 0,50 0,75 0,75 1,00 1,25 1,50

European Central Bank 0,00 0,00 0,00 0,00 0,00 0,25

Bank of England 0,25 0,05 0,05 0,05 0,05 0,25

Norges Bank 0,50 0,50 0,50 0,50 0,50 0,75

Bank of Japan -0,10 -0,10 -0,10 -0,10 -0,10 -0,10

Government bond rates

Germany 2y -0,6 -0,6 -0,4 -0,3 0,5 0,6

Germany 5y -0,5 -0,5 -0,3 -0,2 0,6 0,8

Germany 10y -0,1 -0,1 0,1 0,2 0,9 1,0

US 2y 0,8 0,9 0,9 1,2 1,6 2,0

US 5y 1,2 1,3 1,4 1,5 1,9 2,4

US 10y 1,6 1,7 1,7 1,8 2,2 2,6

Exchange rates

EUR/USD 1,13 1,08 1,06 1,10 1,10 1,12

USD/CNY 6,7 6,8 6,9 6,7 6,8 7,0

EUR/NOK 9,67 9,11 8,91 8,90 8,73 8,73

USD/JPY 100 103 105 108 108 108

EUR/SEK 9,47 9,20 9,00 8,90 8,90 8,90

EUR/GBP 0,86 0,89 0,85 0,85 0,82 0,82

USD/RUB 65 60 59 58 55 52

Sources: M acrobond and Swedbank.

© Swedbank

Global: Central banks continue to use QE-stimuli

9

• The QE-programs continue.

• Risk that central banks will face a shortage of bonds to buy. Could cause an extension of

quantity (asset class).

© Swedbank

Global: Will the market liquidity prevail?

10

• The Riksbank is expected to have 43 per cent of outstanding SGB´s at end 2017

• Foreign ownership of outstanding government bonds has stabilised at around 40 percent in 2016

© Swedbank

Sweden Average is over

© Swedbank

Swedish growth dampens; dependence on domestic

demand remains large

12

• Investments and household consumptions drive growth

• Weak external demand and rising domestic cost pressures dampen net-exports

• Less fiscal policy stimulus as refugee inflow decreases

Swedbank's GDP Forecast - Sweden

Changes in volume, % 2015 2018f

Households' consumption expenditure 2.7 2.8 (2.9) 1.9 (2.1) 1.8

Government consumption expenditure 2.6 3.2 (3.7) 2.3 (2.6) 1.9

Gross f ixed capital formation 7.0 6.2 (5.0) 4.0 (4.4) 3.2

private, excl. housing 6.1 4.6 (4.1) 2.6 (3.7) 2.3

public 1.4 2.3 (4.6) 6.1 (6.4) 5.3

housing 16.6 14.9 (7.9) 6.6 (5.4) 4.4

Change in inventories 1/ 0.1 0.1 (0.0) 0.0 (0.0) 0.0

Exports, goods and services 5.9 2.8 (4.4) 3.8 (3.5) 3.0

Imports, goods and services 5.5 4.0 (5.3) 4.3 (4.8) 3.5

GDP 4.2 3.3 (3.3) 2.3 (2.3) 2.0

GDP, calendar adjusted 3.9 3.1 (3.0) 2.5 (2.6) 2.1

Domestic demand 1/ 3.6 3.6 (3.5) 2.4 (2.7) 2.1

Net exports 1/0.4 -0.4 (-0.2) -0.1 (-0.4) -0.1

1/ Contribution to GDP growth. Sources: Statistics Sweden and Swedbank

April 2016 forecast in parentheses.

2017f2016f

© Swedbank

Weak global growth since the financial crisis

• Eight years of weak global growth has affected households severely with stagnant or even negative

real wages. Inequalities rise in society.

• Global growth will continue to be weak, at about 3% per year. This does not imply no growth but

simply weaker than expected.

• Sweden depends heavily on domestic sectors to keep up economic growth. How can Sweden

achieve sound economic growth when the world is stagnating?

13

© Swedbank

Population growth and demographic changes are

driving growth

14

• Sweden’s population grows with a historically unforeseen pace

• The growth rate is higher for children and youth and the elderly than for the population on average

• Increased strain on municipalities and county councils

© Swedbank

Sluggish export performance

15

• Modest recovery in world market growth for Swedish exporters

• Uncertainties about export of services after UK Brexit

• Unfavourable competitiveness due to stronger krona and higher unit labour costs

• Sluggish growth in global investments and low commodity prices will limit the Swedish export

performance.

© Swedbank

Growth in investments decelerates from high levels

16

• Investment growth in housing decelerates due to growing capacity constrains (lack of labour)

• Public investments is expected to gear up driven by infrastructure (roads, railways) and from

municipalities.

• Investments in private business sector is expected to slow down from high level.

© Swedbank

Strong consumption growth but high household saving

persists

17

• Disposable income continues to grow, although at a slowing rate

• The strong job markets and low interest rates lend support

• The housing component grows during the forecast period in line with rising energy prices and interest

rates

• Households’ high level of savings persists

© Swedbank

Households show willingness to consume

18

• Strong retail sales supported by durable goods sales but higher comparative figures slowing growth

rates during the forecast period

• Consumption of durables slows down during the forecast period

– Saturation effect especially in strong car sales

© Swedbank

Household confidence vital for consumption

19

• Household confidence is crucial for consumption

• The declining micro index (households’ view on their own economy) is a worrying sign when it comes

to durables goods consumption

• Even parts of service consumption can be affected, not least “consumption of experiences”

© Swedbank

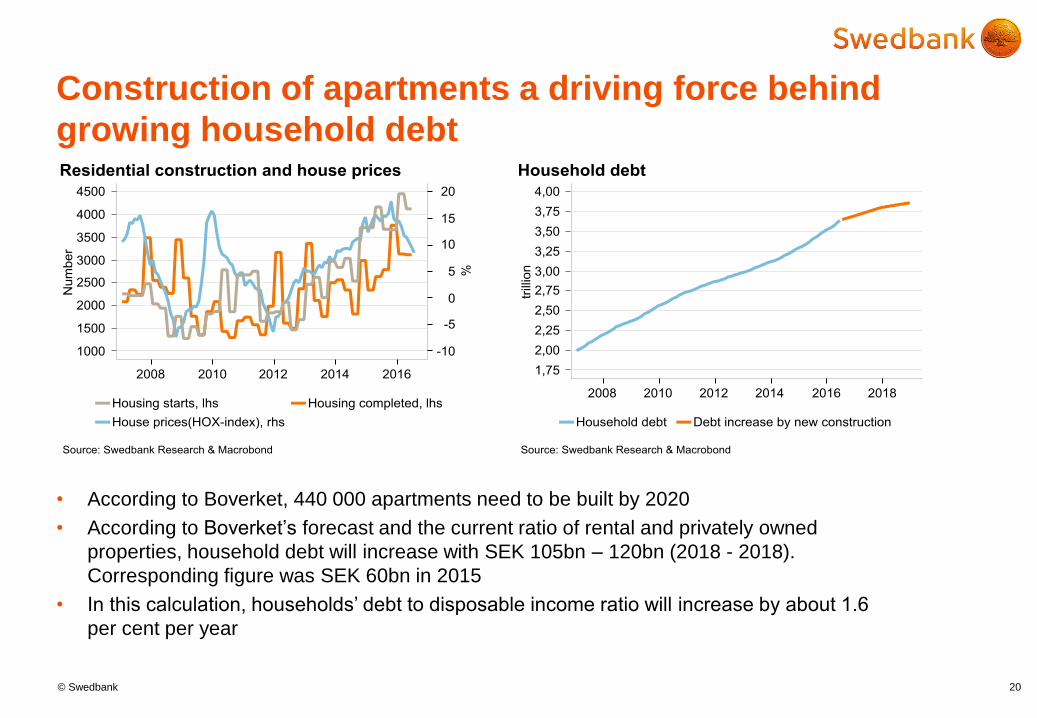

Construction of apartments a driving force behind

growing household debt

20

• According to Boverket, 440 000 apartments need to be built by 2020

• According to Boverket’s forecast and the current ratio of rental and privately owned

properties, household debt will increase with SEK 105bn – 120bn (2018 - 2018).

Corresponding figure was SEK 60bn in 2015

• In this calculation, households’ debt to disposable income ratio will increase by about 1.6

per cent per year

© Swedbank

Upcoming election is reflected in fiscal policy

21

• Strong growth and temporary factors lead to a budget surplus in 2016.

• Lower costs for migration but integration costs remain high. Central government budget likely to

include structural reforms and education efforts. Increased transfers to households likely.

• Deficit 2017 turns into surplus 2018. Politicians pressured by satisfying coalition partners.

• Slowdown in municipal bond issuance. The SNDO could further lower the issuance of government

bonds.

© Swedbank

The job market improves but increasing recruiting

problems become visible

22

• Employment continues to increase at a fast pace, with 210 000 in the years 2016-2018, but the

growth rate is slowing

• Even the workforce increases and the growth rate is maintained by newly arrived refugees

obtaining residence permits

• Unemployment rate falls to a low of 6.2 % at the end of 2017 and then rises to 6.4 % in 2018

• Hours worked increase considerably more than the number of employed persons this year

(assuming increased overtime and a falling share of the underemployed) The difference narrows

down in 2017-2018.

© Swedbank

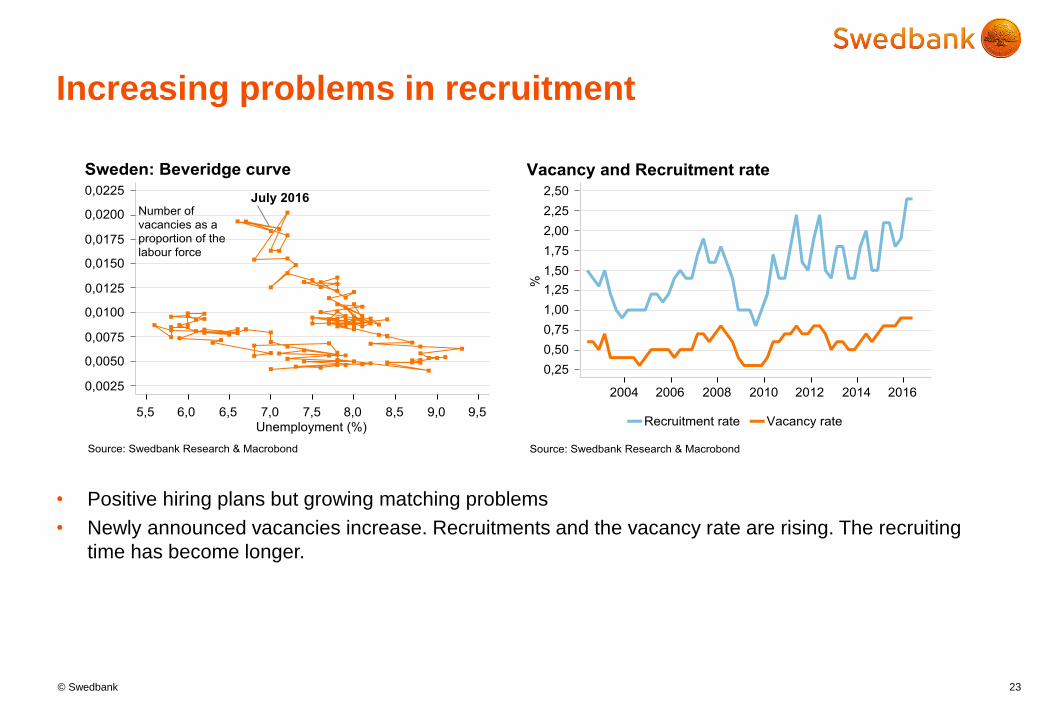

Increasing problems in recruitment

23

• Positive hiring plans but growing matching problems

• Newly announced vacancies increase. Recruitments and the vacancy rate are rising. The recruiting

time has become longer.

© Swedbank

Polarization between native and foreign born increases

24

© Swedbank

Slowly growing wage increases in line with the stronger

labour market

25

• The wage development in 2016 indicates unchanged centralized wage increases (about 2.3 %)

• One-year contracts support somewhat higher contracts next year if the labour shortage becomes even

more evident

• Continuing high tension inside the labour union movement. Can a centralized contract by LO emerge

again? Will the manufacturing sector’s dominance in wage setting hold in a strengthening domestic

economy?

• Wage increases in addition to the collective agreements regulations have become more common, but the

growth is slow and the old conventions for resource use have weakened. Increased non-wage labour

costs make labour costs grow.

© Swedbank

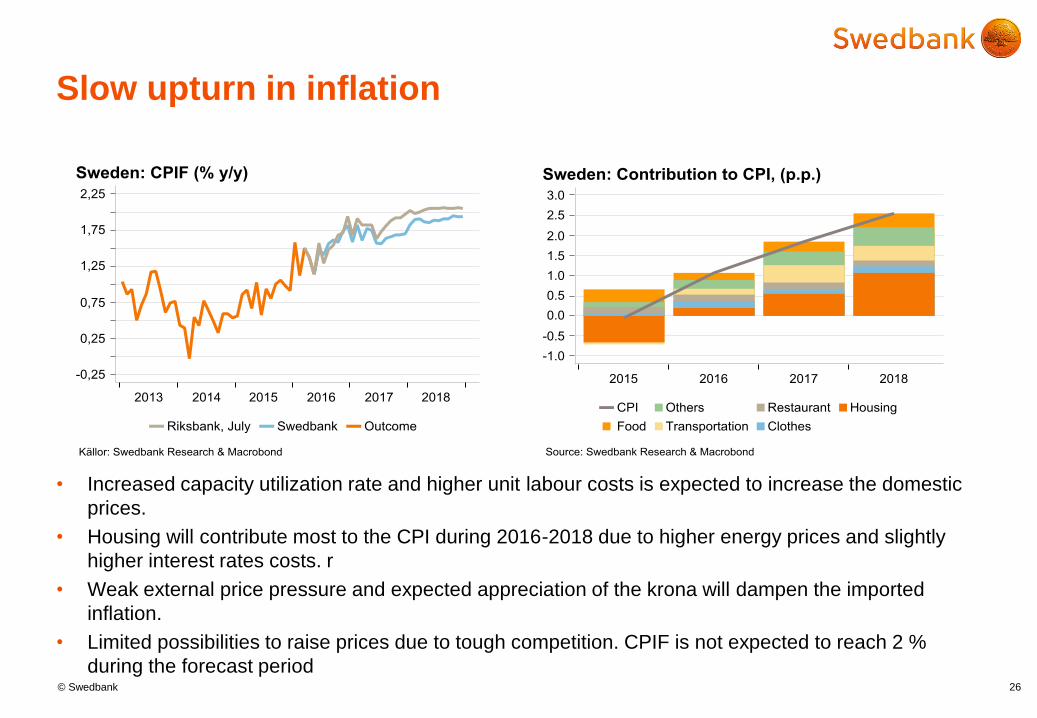

Slow upturn in inflation

26

• Increased capacity utilization rate and higher unit labour costs is expected to increase the domestic

prices.

• Housing will contribute most to the CPI during 2016-2018 due to higher energy prices and slightly

higher interest rates costs. r

• Weak external price pressure and expected appreciation of the krona will dampen the imported

inflation.

• Limited possibilities to raise prices due to tough competition. CPIF is not expected to reach 2 %

during the forecast period

© Swedbank

Domestic inflation rate and inflation expectations has

picked up while the imported inflation has declined

27

© Swedbank

Riksbank delays rate hikes until 2018

28

• The strong Swedish economy, the inflation and a weak krona give Riksbank breathing room in the

short run

• ECB decisive for monetary policy going forward

• Extension and thus, likely a broadening of QE likely as ECB extends its program

• The first rate hike will be delayed until February 2018 - but the negative rate reminds of the

necessity of an eventual rate increase

• The repo rate reaches zero per cent at the end of 2018

© Swedbank

Will the market liquidity prevail?

29

• The Riksbank is expected to have 43 per cent of outstanding SGB´s at end 2017

• Foreign ownership of outstanding government bonds has stabilised at around 40 percent in

2016

© Swedbank

Advanced economies Still in need of support

30

© Swedbank

EMU: Slow growth continues

31

• We expect growth to keep up at about 1.5%, in line with barometers and recent developments

• Economic consequences of Brexit likely small, but political risk has risen

• Even at this moderate growth rate, employment is rising and unemployment is falling steadily

• Monetary policy will remain exceptionally expansionary for quite some time. The scope for and

impact of further policy easing is limited

© Swedbank

EMU: Consumption and investments rising steadily

32

• Consumer confidence remains above average, but has fallen somewhat recently

• Suggests slower growth in private consumption ahead. Retail sales were close to flat in Q2

• Real investments have been rising continuously for two years, supported by credit growth

• Access to credit has improved and the banking sector has largely passed the stress tests,

serious concerns remain about capitalisation and profitability in some countries

© Swedbank

EMU: Growth remains uneven

33

• Growth remains uneven: Strong in Spain, fair in Germany, and zero in France and Italy in Q2

• PMIs indicate that the differing growth rates keep up

• Mixed picture for EMU also along other dimensions: Manufacturing has softened and

consumer confidence has weakened. But unemployment is falling almost everywhere and real

investments have been rising continuously for two years

© Swedbank

UK: Economically and politically weaker

34

• Referendum outcome to dampen growth going

forward. No recession predicted.

• Early indications suggest that domestic

demand will weaken significantly.

• Improving trade balance and policy stimulus

offsetting effects.

• BOE launched massive stimulus package in

Aug. (rate cut, QE & Term Funding Scheme).

• Rate cut in Nov. to 0.05%; hike in 2018. Yet

more stimuli possible.

• Political upheaval a major risk factor. Article 50

invoked in 2017 but could be delayed.

© Swedbank

Japan: Hanging on, for now

35

• Economic growth remains fragile and inflation far from the target. A fall in export and investment

volumes in Q2 reflects weaker global demand and a stronger yen. We expect growth to pick up

slightly next year. A tightening labour market, a supplementary budget, and the postponement of

the VAT hike will support domestic demand.

• The BoJ will probably fail to meet its current inflation target (2.0% by April 2018). Expanding

current instruments further would not have a meaningful impact on achieving the price target

(except, perhaps, expanding the maturity of the bonds to be bought, to make the BoJ’s life a bit

easier); however, something needs to be done, when prices fail to increase.

© Swedbank

US The cycle is maturing and the Fed is constrained

© Swedbank

US: Strong domestic demand the major growth engine

37

• Underlying growth stronger than headline figure suggests

• Inventory drawdown weighed heavily on Q2, expected to normalise during quarters ahead

• Buoyant household spending expected to continue to provide lion’s share of growth

– Supported by a tighter labour market with steady income improvements, low energy costs, consumer credit, as well as

wealth effects from housing market and stock market

© Swedbank

US: Firmer labour market, energy feed into inflation

38

• Increasingly less available slack in the labour market

• Wage inflation expected at present or higher level, will also pass-through to consumer prices

• Negative pressure on headline PCE & CPI from falling energy prices had disguised underlying

upward trend

© Swedbank

US: Signs of a maturing cycle

39

• Corporate profit levels would be expected to rise, and investments to drive growth, at this stage

• A cyclical peak likely approaching, economic growth slows thereafter

• Slow productivity growth – and a tight labour market limiting increases in the number of hours

worked – suggest lower trend growth ahead

© Swedbank

• Going forward, Fed will be faced with a

tough choice: – Incoming domestic data will confirm view that

normalisation of policy is appropriate, …

– … yet must consider what other central banks do or

risk cracking the economy

• Fed expected to balance these demands by

hiking the funds rate by 25 basis points once

this year, once in the fall of 2017 and twice

during 2018.

US: Fed is caught between a rock and a hard place

40

Domestic conditions will likely warrant a faster

normalisation

– Inflation rising

– Labour market tightening

– Domestic demand strong

– Asset prices increasing further

Interest rate differentials will constrain Fed

– Major CBs will be very dovish and large

interest rate differentials could make dollar

strengthen substantially

– Could imperil economic momentum and

further import deflation

© Swedbank

• Going forward, Fed will be faced with a

tough choice: – Incoming domestic data will confirm view that

normalisation of policy is appropriate, …

– … yet must consider what other central banks do or

risk cracking the economy

• Fed expected to balance these demands by

hiking the funds rate by 25 basis points once

this year, once in the fall of 2017 and twice

during 2018.

US: Fed is caught between a rock and a hard place

41

Domestic conditions will likely warrant a faster

normalisation

– Inflation rising

– Labour market tightening

– Domestic demand strong

– Asset prices increasing further

Interest rate differentials will constrain Fed

– Major CBs will be very dovish and large

interest rate differentials could make dollar

strengthen substantially

– Could imperil economic momentum and

further import deflation

Emerging Markets Financial flows have returned and economic fundamentals improve

42

© Swedbank

Emerging Markets - Hunt for yield

43

• Financial flows have returned

• Fundamentals not deteriorating in the same way as in 2015

• Less China fears with lot of economic policy support

• Political progress in India

• Bottom in sight for Brazil and Russia but structural shortcomings will prevent any meaningful

recoveries

© Swedbank

China – Economic policy supportive for growth

44

• Less fear but the economic momentum has moderated

• Growth driven by the property sector

• Economic policy is supportive

• The trade-weighted currency is 10 percent down and rates are record low

• We expect growth to moderate and economic policy to remain supportive

© Swedbank

Brazil – Bottom in sight but structural issues remain

45

• Brazil financial assets best performer this year

• A weaker USD and higher commodity prices have eased the pressure

• Structural issues remain and we doubt that the new government is able to push through with

necessary reforms

• The financial vulnerability has decreased on the back of less external deficit and large foreign

reserves

© Swedbank

India – Signs of green shoots

46

• Finally, some political progress

• The unified tax (GST) was approved in the upper house on Aug 2

• This is an important reform that is expected to raise potential growth by 1-2%

• However, many policy challenges remain such as land and labor reforms

• Credit growth remain weak as banks are still burdened with bad loans

© Swedbank

Russia: End of recession, but recovery will be modest

47

• Recession ended in 2Q 2016. Recovery is led

by industry, which gains from the weak rouble,

import substitution, and oil price rise. Growth

outlook remains volatile and patchy.

• CRB to continue cutting its policy rates (from

the current 10.5% to 9.50% by end 2016). RUB

to stabilize at 60-65 per USD.

• .

• GDP to fall 0.8% in 2016 followed by 1.5% and

2% expansion in 2017-18. It is about potential

as the fundamentals remain weak.

• Western sanctions against Russia: EU could

start easing in early 2017; most binding are the

US sanctions, but they will remain. Key Russia

risk is political, not economic.

© Swedbank

FX Central banks strive to keep currencies stable.

USD to see some limited scope for appreciation . Scandies remain range bound

© Swedbank

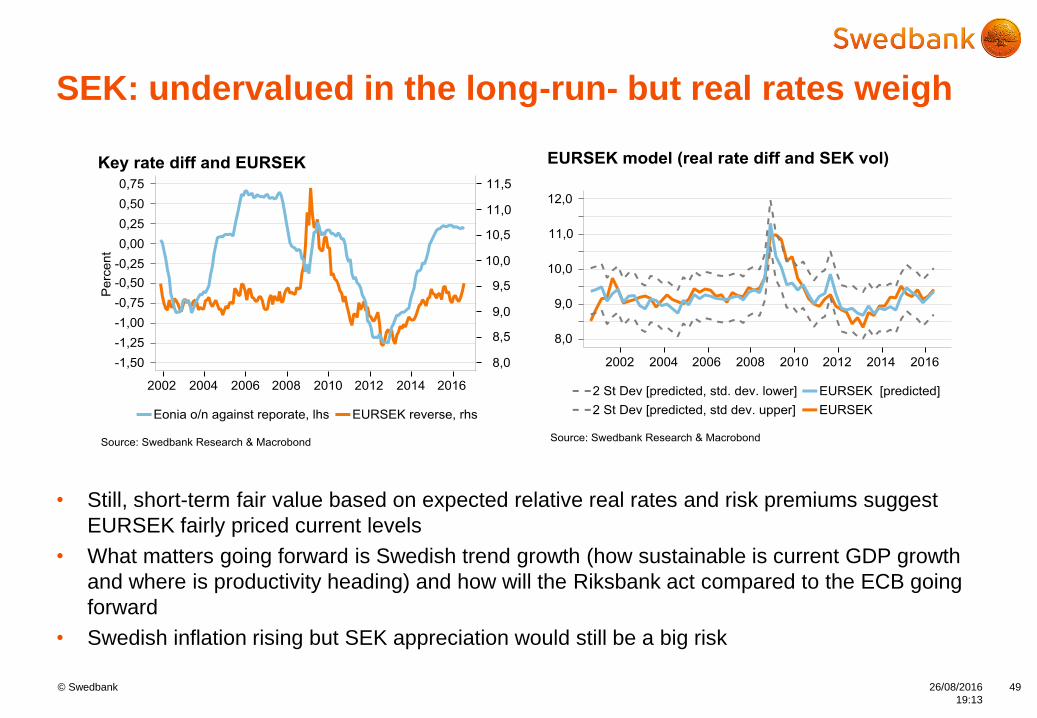

SEK: undervalued in the long-run- but real rates weigh

26/08/2016

19:13

49

• Still, short-term fair value based on expected relative real rates and risk premiums suggest

EURSEK fairly priced current levels

• What matters going forward is Swedish trend growth (how sustainable is current GDP growth

and where is productivity heading) and how will the Riksbank act compared to the ECB going

forward

• Swedish inflation rising but SEK appreciation would still be a big risk

© Swedbank

Some downside in EURUSD over the next 6m, target 1.08

50

• Fed Funds Futures suggest only a little more than one Fed hike priced over the next year

• The ECB not to cut the deposit rate but bond buying could continue beyond March next year.

May need to change QE limits to be able to continue buying. New forecast in September

• EURUSD downside is limited due to cautious Fed and valuation. Sharp USD appreciation

ahead of election could spark attacks on Fed from congress

© Swedbank

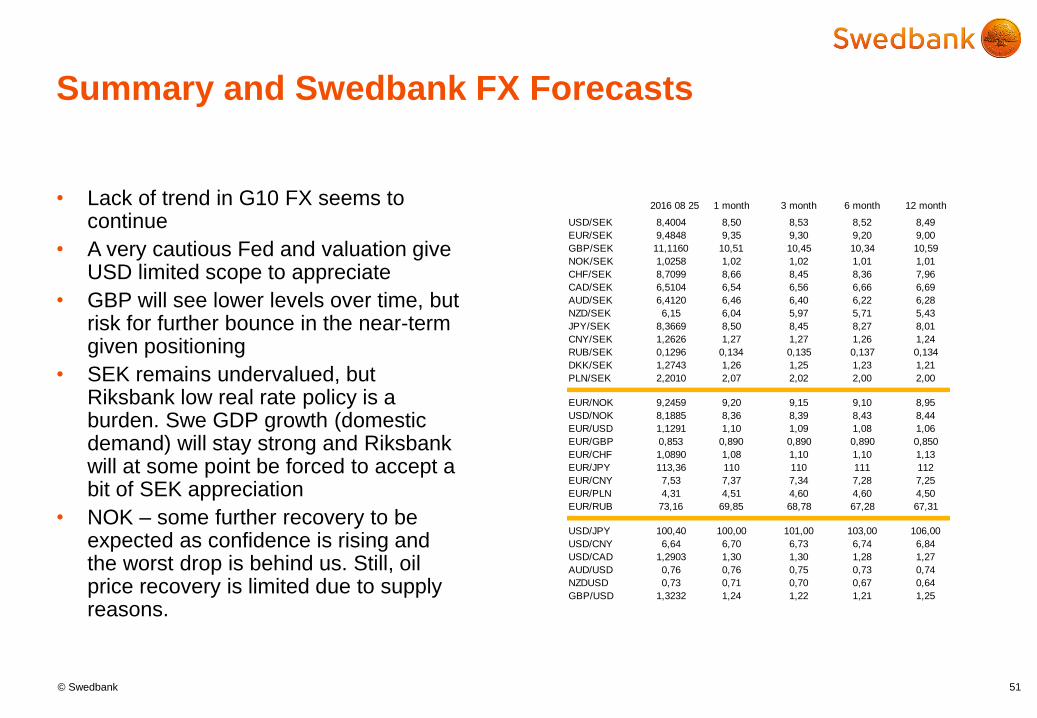

Summary and Swedbank FX Forecasts

• Lack of trend in G10 FX seems to continue

• A very cautious Fed and valuation give USD limited scope to appreciate

• GBP will see lower levels over time, but risk for further bounce in the near-term given positioning

• SEK remains undervalued, but Riksbank low real rate policy is a burden. Swe GDP growth (domestic demand) will stay strong and Riksbank will at some point be forced to accept a bit of SEK appreciation

• NOK – some further recovery to be expected as confidence is rising and the worst drop is behind us. Still, oil price recovery is limited due to supply reasons.

51

2016 08 25 1 month 3 month 6 month 12 month

USD/SEK 8,4004 8,50 8,53 8,52 8,49

EUR/SEK 9,4848 9,35 9,30 9,20 9,00

GBP/SEK 11,1160 10,51 10,45 10,34 10,59

NOK/SEK 1,0258 1,02 1,02 1,01 1,01

CHF/SEK 8,7099 8,66 8,45 8,36 7,96

CAD/SEK 6,5104 6,54 6,56 6,66 6,69

AUD/SEK 6,4120 6,46 6,40 6,22 6,28

NZD/SEK 6,15 6,04 5,97 5,71 5,43

JPY/SEK 8,3669 8,50 8,45 8,27 8,01

CNY/SEK 1,2626 1,27 1,27 1,26 1,24

RUB/SEK 0,1296 0,134 0,135 0,137 0,134

DKK/SEK 1,2743 1,26 1,25 1,23 1,21

PLN/SEK 2,2010 2,07 2,02 2,00 2,00

EUR/NOK 9,2459 9,20 9,15 9,10 8,95

USD/NOK 8,1885 8,36 8,39 8,43 8,44

EUR/USD 1,1291 1,10 1,09 1,08 1,06

EUR/GBP 0,853 0,890 0,890 0,890 0,850

EUR/CHF 1,0890 1,08 1,10 1,10 1,13

EUR/JPY 113,36 110 110 111 112

EUR/CNY 7,53 7,37 7,34 7,28 7,25

EUR/PLN 4,31 4,51 4,60 4,60 4,50

EUR/RUB 73,16 69,85 68,78 67,28 67,31

USD/JPY 100,40 100,00 101,00 103,00 106,00

USD/CNY 6,64 6,70 6,73 6,74 6,84

USD/CAD 1,2903 1,30 1,30 1,28 1,27

AUD/USD 0,76 0,76 0,75 0,73 0,74

NZDUSD 0,73 0,71 0,70 0,67 0,64

GBP/USD 1,3232 1,24 1,22 1,21 1,25

© Swedbank

Fixed Income US will lead the hiking cycle

52

© Swedbank

USA will lead the hiking cycle and the yield curve

remains flat

• Yield difference between the USA and the rest of the world will increase when US leads the hiking cycle

• Yield curves remain flat, even towards the end of the forecast period

• The hunt for yield will cap the potential steepening in the long end of the yield curve

© Swedbank

The low inflations prospects means lower long

rates beyond

• The low inflation environment is there to stay

• In the absence of visible inflations expectations the yield curve remains relatively flat

• The global savings surplus (global savings glut) in relation to investments will dampen the potential for

longer term rates to increase during the forecast horizon

© Swedbank

The Nordic and Baltic Countries

55

• Norway: The worst is behind us

• Denmark: Gradually reaching full capacity

• Finland: Domestic demand behind the

gradual recovery

• Estonia: More mature and more slow

• Latvia: The breeze is yet to fill the sails

• Lithuania: Bronze in rowing and canoeing

The Nordics Slowly coming out of a slump – brighter times ahead

56

© Swedbank

Norway: The worst is behind us

57

• Growth in the Mainland economy remains low but the worst is behind us

• After a steady rise through last year, unemployment is showing signs of stabilisation

• Overall household demand is keeping up and consumer confidence has risen markedly

• We expect Norges Bank to postpone the ‘planned’ September cut and see unchanged rates

through 2017 as the more likely outcome

• For the medium term, we remain positive on the NOK and the oil price

© Swedbank

Finland: Domestic demand behind the gradual recovery

58

• Investments are expected to increase, boosted primarily by residential construction sector

• The Competitiveness Pact, signed in June, is expected to reduce cost pressure on businesses, but

it suppresses consumption with the prevention of pay rises

• Finland has improved its cost-competitiveness, but accommodation with the changed structure of

exports and export markets has proved to be complicated and is unduly slow

• The unemployment rate hike seems to be contained and the employment rate is expected to rise

gradually

© Swedbank

Denmark: Gradually reaching full capacity

59

• Overall growth registered at 1.3% in 2014 and 1.0% in 2015, but was dragged down by a structural

decline in the extraction industries (primarily oil and gas in the North Sea).

• Domestic demand will remain strong, supported by primarily by household consumption.

• Employment increased by 1.5% in 2015 and continues to grow in 2016. Unemployment is currently

at 4.2%.

• Fiscal policy will need to become more contractionary to contain over-heating tendencies

• Households remain vulnerable to shifts in financing conditions and house price developments.

Household indebtedness is at record levels and the share of adjustable-rate mortgages is large.

The Baltics Stronger growth but still a long way to go

60

© Swedbank

Estonia: More mature and more slow

61

• GDP growth was revised down to 1.5% in 2016 due to the weaker-than-expected investments;

meanwhile, exports have started to grow and private consumption has been robust

• Foreign demand is expected to improve in 2016-2018: with the faster growth of exports, investments

are expected to recover and, in turn, will accelerate economic growth to 2.5 in 2017 and 2.7% in 2018

• The labour market remains tight: working age population shrinks, inactivity in the labour market will

decrease and the number of unemployed is expected to grow.

• Nominal wage growth will remain fast, but the recovery of consumer price inflation (2.5% in 2017 and

2% in 2018), real growth of net wages and private consumption will slow

© Swedbank

Latvia: The breeze is yet to fill the sails

62

• Investments disappoint in 2016, GDP growth

cut to 2.1%. EU funds’ inflow and corporate

credit growth will boost investments pushing

GDP growth to 3% and 3.3% in 2017-18.

• Construction sheds jobs, but unemployment

keeps falling. Low inflation and solid wage

growth to keep consumption growth at ca 4%.

• Exporters surprise positively in 2Q 2016.

Export growth expected at 2.5% this year and

4% in 2017-18. Current account may report

surplus this year (first time since 2010).

• Budget revenues benefit from squeezing tax

evasion. Government starts discussing tax and

other reforms to boost growth above 3%.

© Swedbank

Lithuania: Bronze in rowing and canoeing

63

• Like our athletes’ performance in the Rio Olympics,

economic growth is ok, but was weaker than expected.

• Growth is likely to pick up again: robust domestic

demand, recovering exports and investments

• Investments shrank, but are expected to recover with

the help of EU funds

• Household consumption growth remains strong, but

will moderate together with wage growth as of next

year

• Employment growth was surprisingly strong, but

unfavorable demographic trends will hurt –

employment is expected to start shrinking next year

• Wages are increasing rapidly due to increases in

minimum wage and growing competition for labour

• Inflation remains low due to low commodity prices, but

prices of goods will recover and push inflation up;

growth of prices of services is accelerating

• 2016 may turn out to be the first year when public

finances will be balanced

© Swedbank

Contact Information

64

Swedbank Research

Olof Manner

Head of Research

+46 (0)8 700 91 34

Macro Research Strategy

Anna Breman Knut Hallberg Nicole Bångstad Laura Galdikiené Madeleine Pulk

[email protected] [email protected] [email protected] [email protected] [email protected]

Group Chief Economist Senior Economist Junior Economist Senior Economist Head of Strategy and Allocation

+46 (0)8 700 91 42 +46 (0)8 700 93 17 +46 (0)8 700 97 39 +370 5258 2275 +46 (0)72 53 23 533

Harald-Magnus Andreassen Jörgen Kennemar Sihem Nekrouf Siim Isküll Anders Eklöf

[email protected] [email protected] [email protected] [email protected] [email protected]

Chief Economist Norway Senior Economist Economist, EA to Olof Manner Economist Chief FX Strategy

+47 23 11 82 60 +46 (0)8 700 98 04 +46 (0)8 5959 39 34 +372 888 79 25 +46 (0)8 700 91 38

Tõnu Mertsina Åke Gustafsson Øystein Børsum Agnese Buceniece Hans Gustafson

[email protected] [email protected] [email protected] [email protected] [email protected]

Chief Economist Estonia Senior Economist Senior Economist Economist Chief EM Strategy

+372 888 75 89 +46 (0)8 700 91 45 +47 99 50 03 92 +371 6744 58 75 +46 (0)8 700 91 47

Mārtiņš Kazāks Martin Bolander Helene Stangebye Olsen Linda Vildava Pär Magnusson

[email protected] [email protected] [email protected] [email protected] [email protected]

Deputy Chief Economist/Chief Economist Latvia Senior Economist Assistant to Swedbank Analys Norge Junior Economist Chief FI Strategy

+371 6744 58 59 +46 (0)8 700 92 99 +47 23 23 82 47 +371 6744 42 13 +46 (0)72 206 06 89

Nerijus Mačiulis Cathrine Danin Liis Elmik Johanna Högfeldt

[email protected] [email protected] [email protected] [email protected]

Chief Economist Lithuania Economist Senior Economist FX/FI Strategy

+370 5258 22 37 +46 (0)8 700 92 97 +372 888 72 06 +46(0)8 700 91 37

Magnus Alvesson Ingrid Wallin Johansson Vaiva Šečkutė

[email protected] [email protected] [email protected]

Head of Macro Research Economist Senior Economist

+46 (0)8 700 94 56 +46 (0)8 700 92 95 +370 5258 21 56

© Swedbank

General Disclaimer

This research report has been prepared by analysts of Swedbank Macro Research, a unit within Swedbank Large Corporates & Institutions,. The Macro Research department consists of research units in Estonia, Latvia, Lithuania, Norway and Sweden, and is responsible for preparing reports on global and home market economic developments.

Analyst’s certification

The analyst(s) responsible for the content of this report hereby confirm that notwithstanding the existence of any such potential conflicts of interest referred to herein, the views expressed in this report accurately reflect their personal and professional views.

Research reports are independent and based solely on publicly available information.

Issuer, distribution & recipients

This report by Swedbank Macro Research, a unit within Swedbank Research that belongs to Large Corporates & Institutions, is issued by the Swedbank Large Corporates & Institutions business area within Swedbank AB (publ) (“Swedbank”). Swedbank is under the supervision of the Swedish Financial Supervisory Authority (Finansinspektionen).

In no instance is this report altered by the distributor before distribution.

In Finland this report is distributed by Swedbank’s branch in Helsinki, which is under the supervision of the Finnish Financial Supervisory Authority (Finanssivalvonta).

In Norway this report is distributed by Swedbank’s branch in Oslo, which is under the supervision of the Financial Supervisory Authority of Norway (Finanstilsynet).

In Estonia this report is distributed by Swedbank AS, which is under the supervision of the Estonian Financial Supervisory Authority (Finantsinspektsioon).

In Lithuania this report is distributed by “Swedbank” AB, which is under the supervision of the Central Bank of the Republic of Lithuania (Lietuvos bankas).

In Latvia this report is distributed by Swedbank AS, which is under the supervision of The Financial and Capital Market Commission (Finanšu un kapitala tirgus komisija).

In the United States this report is distributed by Swedbank

First Securities LLC ('Swedbank First'), which accepts responsibility for its contents. This report is for distribution only to institutional investors. Any United States institutional investor receiving the report, who wishes to effect a transaction in any security based on the view in this document, should do so only through Swedbank First. Swedbank First is a U.S. broker-dealer, registered with the Securities and Exchange Commission, and is a member of the Financial Industry Regulatory Authority. Swedbank First is part of Swedbank Group.

For important U.S. disclosures, please reference: http://www.swedbanksecuritiesus.com/disclaimer/index.htm

In the United Kingdom this communication is for distribution only to and directed only at "relevant persons". This communication must not be acted on – or relied on – by persons who are not "relevant persons". Any investment or investment activity to which this document relates is available only to "relevant persons" and will be engaged in only with "relevant persons". By "relevant persons" we mean persons who:

• Have professional experience in matters relating to investments falling within Article 19(5) of the Financial Promotions Order.

• Are persons falling within Article 49(2)(a) to (d) of the Financial Promotion Order ("high net worth companies, unincorporated associations etc").

• Are persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) – in connection with the issue or sale of any securities – may otherwise lawfully be communicated or caused to be communicated.

Limitation of liability

All information, including statements of fact, contained in this research report has been obtained and compiled in good faith from sources believed to be reliable. However, no representation or warranty, express or implied, is made by Swedbank with respect to the completeness or accuracy of its contents, and it is not to be relied upon as authoritative and should not be taken in substitution for the exercise of reasoned, independent judgment by you.

Opinions contained in the report represent the analyst's present opinion only and may be subject to change. In the event that the analyst's opinion should change or a new analyst with a different opinion becomes responsible for our coverage, we shall endeavour (but do not undertake) to disseminate any such change, within the constraints of any regulations, applicable laws, internal procedures within Swedbank, or other circumstances.

Swedbank is not advising nor soliciting any action based upon this report. This report is not, and should not be construed as, an offer to sell or as a solicitation of an offer to buy any securities.

To the extent permitted by applicable law, no liability whatsoever is accepted by Swedbank for any direct or consequential loss arising from the use of this report.

Reproduction & dissemination

This material may not be reproduced without permission from Swedbank Research, a unit within Large Corporates & Institutions. This report is not intended for physical or legal persons who are citizens of, or have domicile in, a country in which dissemination is not permitted according to applicable legislation or other decisions.

Produced by Swedbank Research, a unit within Large Corporates & Institutions.

Address

Swedbank LC&I, Swedbank AB (publ), SE-105 34 Stockholm.

Visiting address: Landsvägen 40, 172 63 Sundbyberg

65