SWBC Lending Solutions Copyright 2015 - SWBC Page...

16

SWBC Lending Solutions Copyright 2015 - SWBC Page 1 This engagement letter serves as a contract between the vendor listed and SWBC Lending Solutions and must be completed or Supervised and signed by the appraiser listed. The fee and due date are not negotiable after the case terms have been accepted by the vendor. If the report is not completed per the instruction outlined in this letter on or before the above agreed upon due date, Client or SWBC Lending Solutions reserves the right to reduce fees or cancel the assignment without payment any time thereafter. You must set your appointment no later than 24 hours after receiving this request and submit the inspection date through Appraisal Port. If there are any problems gaining access to the property or meeting the appraisal due date notify us immediately. DELIVERY OF APPRAISAL The appraisal report is expected to be uploaded no more than 48 hours (2 business days) after inspection, regardless of the due date. HOT LINE - (949) 206-0445 APPRAISAL INDEPENDENCE EMAIL – [email protected] SWBC Lending Solutions requires any appraiser on our panel that has experienced coercion, bribery or other similar actions designed to cause the appraiser to base appraisal value of a property on factors other than the appraiser's independence judgment to stop work immediately on the associated file and notify us of the volition. UAD COMPLIANCE UAD Requirements for Entering the Subject Property's Address: The appraiser must enter the subject property's USPS address into the Subject section of the appraisal report following USPS mailing format standards (Street Number, Street Name, City, State, and ZIP Code.) Unit number for condominium appraisals: A condominium's unit number must be entered in the Unit Number field of the appraisal report. If the appraiser determines that a unit number is not available for a property known to be a condominium, the appraiser must put a "-"in the Unit Number field. The “-“symbolizes that the appraiser has researched the property address and was unable to identify a unit number. The address and unit number must be provided consistently for the subject property throughout the appraisal. Variations of the subject property address : Variations in the subject property address may be found because the property is (1) new construction, (2) lacks a USPS address, (3) USPS address is a P.O. Box or (4) USPS address conflicts with the legal address in public records. When these variations are found by the appraiser, take the following steps: If the subject property is new construction, address is a P.O. Box or lacks a USPS address, enter the subject property's physical address as best as possible using the USPS format. When the USPS address conflicts with the legal address in public records, identify and comment on the conflict in the addendum to the appraisal report.

Transcript of SWBC Lending Solutions Copyright 2015 - SWBC Page...

SWBC Lending Solutions Copyright 2015 - SWBC Page 1

This engagement letter serves as a contract between the vendor listed and SWBC Lending Solutions and must be

completed or Supervised and signed by the appraiser listed. The fee and due date are not negotiable after the case

terms have been accepted by the vendor. If the report is not completed per the instruction outlined in this letter on or before the above agreed upon due date, Client or SWBC Lending Solutions reserves the right to reduce fees or cancel the

assignment without payment any time thereafter. You must set your appointment no later than 24 hours after receiving this request and submit the inspection date through Appraisal Port. If there are any problems

gaining access to the property or meeting the appraisal due date notify us immediately.

DELIVERY OF APPRAISAL

The appraisal report is expected to be uploaded no more than 48 hours (2 business days) after inspection, regardless of the due date.

HOT LINE - (949) 206-0445 APPRAISAL INDEPENDENCE EMAIL – [email protected]

SWBC Lending Solutions requires any appraiser on our panel that has experienced coercion, bribery or other similar actions designed to cause the appraiser to base appraisal value of a property on factors other than the appraiser's independence judgment to stop

work immediately on the associated file and notify us of the volition.

UAD COMPLIANCE

UAD Requirements for Entering the Subject Property's Address: The appraiser must enter the subject property's USPS

address into the Subject section of the appraisal report following USPS mailing format standards (Street Number, Street Name, City, State, and ZIP Code.)

Unit number for condominium appraisals: A condominium's unit number must be entered in the Unit Number field of the appraisal report. If the appraiser determines that a unit number is not available for a property known to be a

condominium, the appraiser must put a "-"in the Unit Number field. The “-“symbolizes that the appraiser has researched the property address and was unable to identify a unit number. The address and unit number must be provided

consistently for the subject property throughout the appraisal.

Variations of the subject property address: Variations in the subject property address may be found because the property is (1) new construction, (2) lacks a USPS address, (3) USPS address is a P.O. Box or (4) USPS address conflicts

with the legal address in public records. When these variations are found by the appraiser, take the following steps:

If the subject property is new construction, address is a P.O. Box or lacks a USPS address, enter the subject

property's physical address as best as possible using the USPS format. When the USPS address conflicts with the legal address in public records, identify and comment on the conflict in

the addendum to the appraisal report.

SWBC Lending Solutions Copyright 2015 - SWBC Page 2

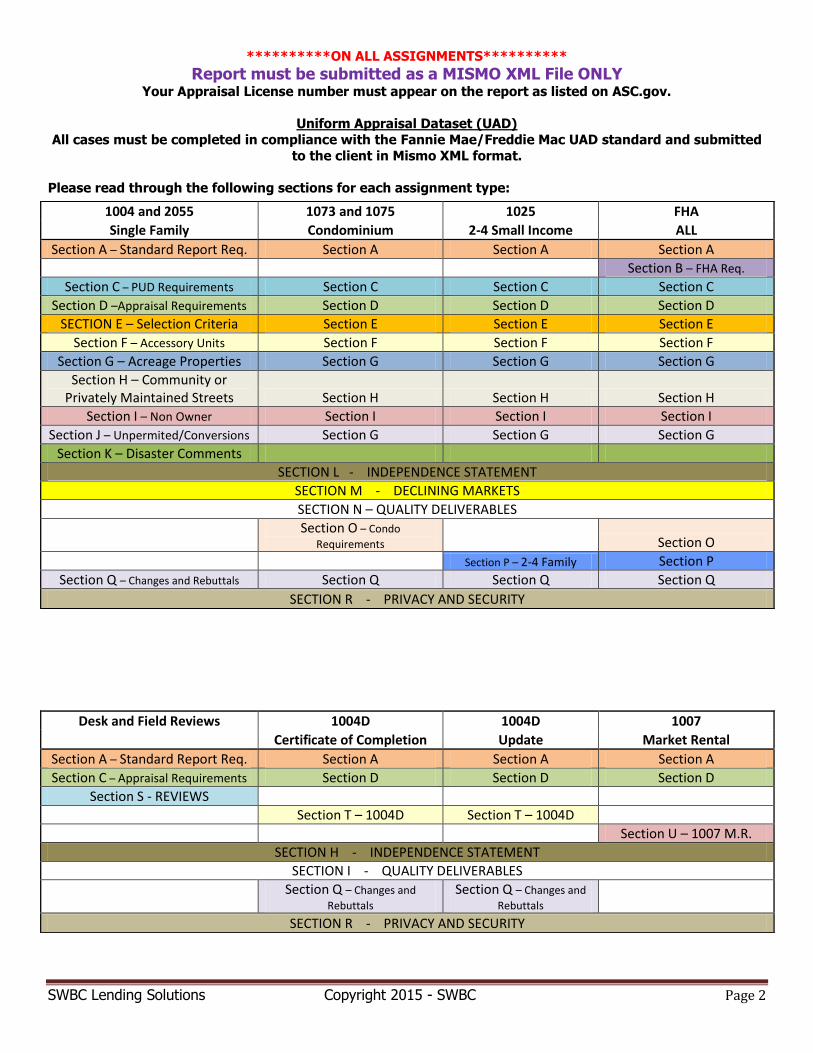

**********ON ALL ASSIGNMENTS**********

Report must be submitted as a MISMO XML File ONLY Your Appraisal License number must appear on the report as listed on ASC.gov.

Uniform Appraisal Dataset (UAD)

All cases must be completed in compliance with the Fannie Mae/Freddie Mac UAD standard and submitted

to the client in Mismo XML format.

Please read through the following sections for each assignment type:

1004 and 2055 1073 and 1075 1025 FHA

Single Family Condominium 2-4 Small Income ALL

Section A – Standard Report Req. Section A Section A Section A

Section B – FHA Req.

Section C – PUD Requirements Section C Section C Section C

Section D –Appraisal Requirements Section D Section D Section D

SECTION E – Selection Criteria Section E Section E Section E

Section F – Accessory Units Section F Section F Section F

Section G – Acreage Properties Section G Section G Section G

Section H – Community or Privately Maintained Streets Section H Section H Section H

Section I – Non Owner Section I Section I Section I

Section J – Unpermited/Conversions Section G Section G Section G

Section K – Disaster Comments

SECTION L - INDEPENDENCE STATEMENT

SECTION M - DECLINING MARKETS

SECTION N – QUALITY DELIVERABLES

Section O – Condo

Requirements

Section O

Section P – 2-4 Family Section P

Section Q – Changes and Rebuttals Section Q Section Q Section Q

SECTION R - PRIVACY AND SECURITY

Desk and Field Reviews 1004D 1004D 1007

Certificate of Completion Update Market Rental

Section A – Standard Report Req. Section A Section A Section A

Section C – Appraisal Requirements Section D Section D Section D

Section S - REVIEWS

Section T – 1004D Section T – 1004D

Section U – 1007 M.R.

SECTION H - INDEPENDENCE STATEMENT

SECTION I - QUALITY DELIVERABLES

Section Q – Changes and

Rebuttals Section Q – Changes and

Rebuttals SECTION R - PRIVACY AND SECURITY

SWBC Lending Solutions Copyright 2015 - SWBC Page 3

SECTION A - STANDARD REPORT REQUIREMENTS

“Experience, Integrity, and Transparency”

Loan Number must be noted at the top right hand corner of the form.

Copy of your License and E/O must be attached to your report.

DO NOT include an invoice within your appraisal report.

Use the USPS address for the subject

All appraisals must conform to the requirements stated or referenced in this engagement letter, including the

applicable requirements in the current edition of the Uniform Standards of Professional Appraisal Practice (USPAP).

All reports must be submitted on the appropriate, most recent Fannie Mae,/Freddie Mac form.

All reports must be consistent throughout and be well supported. A comprehensive value conclusion is expected. A

comment like “all comparables have been given equal weight” is not enough. A detailed analysis on how the comps

were selected, adjustments, and your final value conclusion was derived is required.

Always ensure the client name on the report is the lender as specified in the order (Not SWBC Lending Solutions).

SWBC Lending Solutions should only be stated as the AMC in the client name field on the Signature/Certification Page.

Appraiser Independence Statement (See Below) must accompany every assignment.

Appraiser must have access to local MLS and must be used in comparable selection.

PHOTOGRAPHS: (Granular, blurred, pixilated or obstructed view photos will not be acceptable)

Required where applicable:

Front of property / Rear of property / Side elevations / Street Scene / Kitchen / All Bathrooms / All Bedrooms including Den or

Office / Main Living Area(s) / Basement (finished or unfinished) / Pools or other amenities / View(s) (ie: water view, mountain view,

city view, recreational area(s), power lines or any external obsolescence) / Examples of Physical Deterioration (If Present) /

Examples of recent updates: (ie: Restoration, Remodeling & Renovation) / Photos of specific items which contributory value given

(ie: Custom features, Barn, Tack room, horse facilities, Guest house, Casita, Workshop, Detached garage, Boat house, )

MLS photos- are NOT acceptable. In the case where a comparable sale(s) where access is not permitted such as a guarded gate

or blocked access the appraiser may provide the MLS photo; however, a photo of the obstruction must also be provided.

Final or Appraisal Update Photographs - The Client requires a new front exterior photo, a new rear exterior & street scene

photo. Additional photos are required of items of which the “subject to condition” was placed upon.

Aerial Photos - An aerial photo of the subject and the market area is best practice and should be included in the appraisal

addenda. The aerial photo should be or sufficient sale to show the subject property and immediate neighborhood and any external

obsolescence, or appraiser must provide comments if the photo is limited or subject is not clearly shown.

PERSONS, FAMILY PHOTOS, PERSONAL PHOTOS, RELIGIOUS OBJECT must be removed or blurred. Please try and take

photos that do not show these items.

NOTE: STOP and notify SWBC Lending Solutions if the subject is a manufactured home or double wide.

NOTE: California – Please ask borrower if CO Detector has been installed when setting up your inspection. Carbon Monoxide

Detector (CA) - If the subject does not have a Carbon monoxide detector, the report must be made subject to installation of a carbon

monoxide detector. "As of July 1, 2011, the state of California enacted the Carbon Monoxide Poisoning Prevention Act SB183. This

act requires all single family homes with an attached garage or a fossil fuel source to install working carbon monoxide alarms."

NOTE: HAWAII

The Appraiser is required to provide a lava zone map for properties on the Big Island of Hawaii. The subject property location must

be identified within the appropriate zone on the map.

*Note: properties located in lava zones 1 or 2 on the Big Island of Hawaii are ineligible.

SWBC Lending Solutions Copyright 2015 - SWBC Page 4

SECTION B - FHA REQUIREMENTS

• FHA Number must be at the top right hand corner of “ALL” pages of your report

• An affirmative statement that “ The subject property meets all FHA Requirements in Sections 4150.1 & 4150.2” is required or

the appraisal must be completed “Subject To Repairs” to bring it to Average or Better Condition and so that the property will in fact

meet FHA Minimum Property Standards.

• HUD INTENDED USER STATEMENT REQUIRED - Appraiser must state that the lender client and FHA/HUD is the intended user.

• If the subject structure was built prior to 1978 all chipped and peeling paint on any and all buildings on the property must be conditioned

for scraped and painting per HUD Requirements - pictures of all areas that need repair required.

• That the appraiser has completed a 'head and shoulders' inspection of the crawl space and attic areas - Photos are only required if an

issue is being addressed. Appraiser MUST provide photos of attic and crawl space!

• The Appraiser has tested all of the Mechanical Systems and found them to be in working order; or outline any issues found.

Water, Wells, Septic and Sewage Systems:

Water, well, septic and sewage systems must meet community standards, be adequate, be in service and be accepted by area

residences.

If Public water and /or sewage facilities are not available then private well and septic facilities must be available and utilized by the

subject property. The private facilities must be viable and adequate to service the subject property.

Generally, the private well and septic facilities must be located on the subject property site. However, off-site private facilities are

acceptable if the inhabitants of the subject property have the right to use and access the off-site facilities and there is an adequate,

legally binding agreement for use, access and maintenance.

The appraiser must comment when the viability, adequacy or market acceptance of or access to the well and septic facilities are an

issue. If not an issue, the appraiser should demonstrate market acceptance by selecting comparables (sales, listings, rentals) with

same/similar characteristics.

For FHA appraisals on properties with private well and private septic the Client requires that the appraiser indicate on the Sketch,

the distance between the:

1. Well & septic tank

2. Well & septic drain field. * If any of this information was not available, please explain.

Builders Certification Builders Certification (92541 form), the appraiser must receive a fully executed form HUD-

92541 before performing the appraisal on proposed or under construction properties less than one year old and

never occupied. The appraiser must review Item One and note in the appraisal report any discrepancies between the

information in Item One and the actual conditions observed on site. The appraiser must take into consideration the

effects of any site conditions on the value of the property.

• If the subject is on well and septic: The distance between the well and septic system, distance between well and septic drain field is at

least 75 feet, please mark and show measurements on the Building Sketch page. The distance of the well is at least 10 feet from the

property line and . If access to city water and/or sewer is available, please provide the hook-up fee requirements, if not available please

so state.

• In addition to front, back, and street exterior photos, FHA requires photos of each side of the subject.

SECTION C - PUD INFORMATION AND ANALYSIS

When the subject is in a PUD, the appraisal must contain

1. Legal name of PUD.

2. HOA dues and assessments.

3. Description of common elements and condition of amenities.

4. Address how the subject's development compares in its amenities and cost to surrounding PUD developments.

5. When using non-PUD comparables provide an analysis to support the inclusion of non-PUD comparables, and address the impact the

subject's deed restriction have on its marketability and value compared with the non-PUD comparables.

SWBC Lending Solutions Copyright 2015 - SWBC Page 5

SECTION D - STANDARD APPRAISAL REQUIREMENTS

Scope of Work The scope of work for this appraisal is defined by the complexity of this appraisal assignment and the reporting requirements of this appraisal report form, including the following definition of market value,

statement of assumptions and limiting conditions, and certifications. The appraiser must, at a minimum:

(1) perform a complete visual inspection of the interior and exterior areas of the subject property (2) inspect the neighborhood (3) inspect each of the comparable sales from at least the street (4) research verify, and analyze data from reliable public and/or private sources (5) report his or her analysis, opinions, and conclusions in this appraisal report.

All assignments must include the UAD definitions in the addendum for all UAD reports.

All assignments must include the Fannie Mae 1004MC form.

Provide total days on market, list date, contract date, original list price for the subject and all comparable sales.

All assignments must include the” COST APPROACH” for “all” interior appraisals and must include a fully developed opinion of site

value.

On all assignments, present and adjust a minimum of three closed sales within 6 months and two current listings and/or under contract

(Pending) sales on the market grid. (Include listing history and days on the market).

All walkthrough assignments require the room locations to be labeled on the floor sketch. (i.e. BR, BA, KIT, LR, DR, etc.)

The sketch must include “ALL” improvements, with dimensions, including but not limited to patios, outbuildings, pools, tennis courts,

etc. Also, basement must be included in sketch addendum.

All walkthrough assignments must include photos for any condition, feature or amenity for which adjustments have been made (e.g.

view, pool, outbuildings, deferred maintenance or other positive or adverse factors).

All walkthrough assignments require interior photographs of the main living areas that include but are not limited to the living room,

kitchen, all bedroom(s), all bathroom(s), and basement.

All walkthrough assignments require a photo of “all” OUTBUILDINGS and an estimated replacement cost for each structure. Comment

whether the foundation of each outbuilding is permanent or the structure is portable.

All photos must be clear, current, in color, and well-framed. They must be specifically labeled (subject interior or subject

exterior and similar vague labels are not acceptable).

Plat Map is required on all assignments. If plat map is unavailable then please indicate and why.

SECTION E - CRITERIA USED FOR SELECTION OF COMPARABLE SALES / SEARCH RESULTS

Appraisers are required by USPAP to include their search criteria documented in their work file. SWBC Lending Solutions believes by being

transparent with this information appraiser independence is strengthened because there are fewer opportunities to second guess appraiser's

comparables selection and at the same time let the reader understand the scope of research completed by the appraiser. SWBC Lending Solutions

believes that including this information initially will reduce second touches by the appraiser and increase underwriter efficiency and reduce

unnecessary revision requests.

SWBC Lending Solutions therefore requires the appraiser to state the search criteria used when researching sales as possible comparables and the

resulting number of potential comparables. When the appraiser determines the initial output is not sufficient and extends the criteria the appraiser

should note the revised search criteria and the resulting number of potential comparables. Sequential searches should all be documented to show

the increasing number of sales analyzed by the appraiser. Only the final list of property addresses considered by the appraiser needs to be listed.

Example: Search criteria included properties that sold within 6 months, were within one half mile of the subject and were within 10% +/- of the

subject's living area. The results of the search produced only one property. The search was extended to twelve months and two miles and 20%

+/- of the subject's living area. The result of the search produced three sales, one pending sale and two listings. The final search criteria were

twelve months, five miles and 25% +/- of the subject's living area. The search criteria resulted in six sales, two pending, and four listings.

Note: The listings of street addresses can be hand typed, MLS outputs or property records outputs. Only the street addresses are required to be

shown, this data may be provided as a one line CMA report; however, greater detail is permissible.

SWBC Lending Solutions Copyright 2015 - SWBC Page 6

SECTION F - ACCESSORY UNITS AND SECOND KITCHENS

A single family home may contain an accessory dwelling unit (ADU), also referred to as a "mother-in-law unit" or "guest apartment." ADUs are self-contained living units (including a private bath and kitchen) that have their own direct access from the outside. An ADU can be either attached or detached and above or below grade. ADUs should only be included in the GLA if they are attached and have direct interior access. ADUs with only exterior access are to be reported, and valued, separately from GLA.

An attached non-permitted second unit (Guest Unit or ADU) should not be valued but the area should be included in the area calculations as if the kitchen components have been removed. The report should be "as is" as long as the appraiser describes the functional obsolescence for the cost of removing the kitchen and returning the structure to its original state.

A detached non-permitted second unit (Guest unit or ADU) should not be valued unless the appraiser can find three similar non-permitted units to demonstrate the acceptance of the non-permitted unit in the market and zoning does not prohibit a second unit (e.g., illegal use)

Properties with accessory dwelling units must be appraised in conformity with local zoning requirements and must accurately report the property's highest and best use. The decision to appraise as a single family with ADU or a 2-unit property will depend on the zoning classification and property characteristics. The appraisal report must indicate whether the unit is legally conforming and whether it is typical for the area. The appraisal report must provide a complete description of the unit. The sales comparison analysis should include at least one comparable sale with an accessory dwelling unit. However, in instances where the ADU is legal but comparable sales cannot be obtained, the appraiser must explain the reason for the deviation and clearly describe the basis for inclusion and valuation.

SECTION G - Acreage Properties

When the assignment includes large acreage or multi-parcels, the appraiser must determine if it is residential in nature. The Lender does not

impose limits on acreage or the percentage of the value to which the excess land is attributed when the property meets these conditions:

The property is common and customary to the market, and supported by comparable sales.

The property is not a Texas Homestead 50(a)(6) property

The property is residential in nature

The property is not used for income producing purposes; the appraiser must comment fully on the excess land and compare it to

properties with like characteristics.

The property must be serviced by adequate utilities and roads which meet local standards.

The property must be accessible for year-round use.

Ineligible rural properties include properties with these characteristics:

Secured by agriculture type land (i.e., farms, orchards or ranches)

Undeveloped land

·Secured for land development purposes

Appraisal should value the subject property based on the typical property size as found through the comparable sales and consider the remainder

excess land. The appraiser is required to describe and include the full parcel even when excess land is considered.

SWBC Lending Solutions Copyright 2015 - SWBC Page 7

SECTION I - NON OWNER- OCCUPIED PROPERTY REQUIREMENTS When completing an appraisal report of a non-owner occupied property, a FNMA Form 1007, Single Family Comparable Rent Schedule is required. Also, the FNMA Form 216, Operating Income Statement is required on all income producing properties. The fee for the appropriate form (s) must be included in the fee prior to starting the assignment.

1. Non-owner occupied SFR: requires FNMA Forms 1007 and 216

2. All 1007 reports require rental comparable photos. MLS photos for rent comparables will be accepted.

3. Small Income Property: report must include FNMA Form 216

4. LET SWBC Lending Solutions SUPPORT KNOW IMMEDIATELY IF THE PROPERTY IS NON-OWNER OCCUPIED SO THE FEE CHANGES CAN BE MADE.

SECTION H - Community Owned or Privately Maintained Streets

If the property is located on a community-owned or privately-owned and maintained street, an adequate, legally enforceable agreement or

covenant for maintenance of the street is required. The agreement or covenant should include the following provisions and be recorded in the

land records of the appropriate jurisdiction:

Responsibility for payment of repairs, including each party's representative share,

Default remedies in the event a party to the agreement or covenant fails to comply with his or her obligations, and

The effective term of the agreement or covenant, which in most cases should be perpetual and binding on any future owners.

Note: If the property is located within a state that has statutory provisions that define the responsibilities of property owners for the

maintenance and repair of a private street, no separate agreement or covenant is required

If the property is not located in a state that imposes statutory requirements for maintenance, and either there is no agreement or covenant for

maintenance of the street, or an agreement or covenant exists but does not meet the requirements listed above, the property is not eligible for

lending.

The appraiser is not required to provide a copy of the Maintenance agreement, but must report that the subject meets the aforementioned

requirements.

SWBC Lending Solutions Copyright 2015 - SWBC Page 8

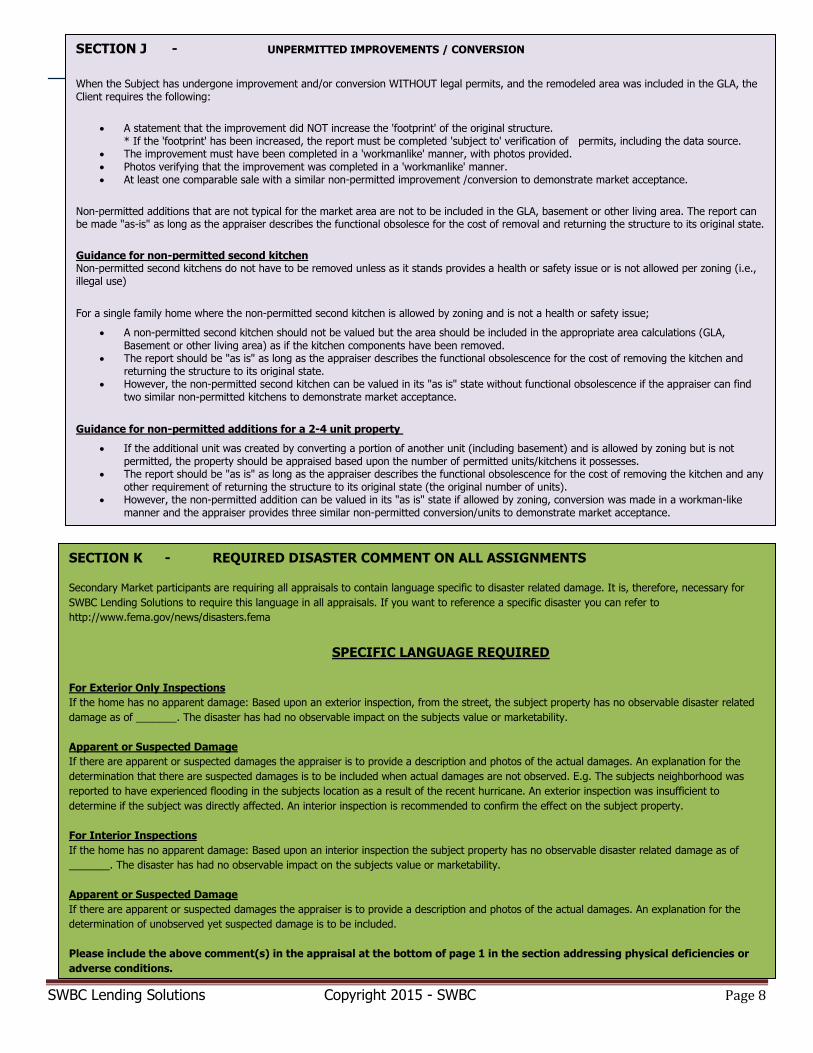

SECTION K - REQUIRED DISASTER COMMENT ON ALL ASSIGNMENTS

Secondary Market participants are requiring all appraisals to contain language specific to disaster related damage. It is, therefore, necessary for

SWBC Lending Solutions to require this language in all appraisals. If you want to reference a specific disaster you can refer to

http://www.fema.gov/news/disasters.fema

SPECIFIC LANGUAGE REQUIRED

For Exterior Only Inspections

If the home has no apparent damage: Based upon an exterior inspection, from the street, the subject property has no observable disaster related

damage as of _______. The disaster has had no observable impact on the subjects value or marketability.

Apparent or Suspected Damage

If there are apparent or suspected damages the appraiser is to provide a description and photos of the actual damages. An explanation for the

determination that there are suspected damages is to be included when actual damages are not observed. E.g. The subjects neighborhood was

reported to have experienced flooding in the subjects location as a result of the recent hurricane. An exterior inspection was insufficient to

determine if the subject was directly affected. An interior inspection is recommended to confirm the effect on the subject property.

For Interior Inspections

If the home has no apparent damage: Based upon an interior inspection the subject property has no observable disaster related damage as of

_______. The disaster has had no observable impact on the subjects value or marketability.

Apparent or Suspected Damage

If there are apparent or suspected damages the appraiser is to provide a description and photos of the actual damages. An explanation for the

determination of unobserved yet suspected damage is to be included.

Please include the above comment(s) in the appraisal at the bottom of page 1 in the section addressing physical deficiencies or

adverse conditions.

SECTION J - UNPERMITTED IMPROVEMENTS / CONVERSION

When the Subject has undergone improvement and/or conversion WITHOUT legal permits, and the remodeled area was included in the GLA, the Client requires the following:

A statement that the improvement did NOT increase the 'footprint' of the original structure. * If the 'footprint' has been increased, the report must be completed 'subject to' verification of permits, including the data source.

The improvement must have been completed in a 'workmanlike' manner, with photos provided. Photos verifying that the improvement was completed in a 'workmanlike' manner. At least one comparable sale with a similar non-permitted improvement /conversion to demonstrate market acceptance.

Non-permitted additions that are not typical for the market area are not to be included in the GLA, basement or other living area. The report can be made "as-is" as long as the appraiser describes the functional obsolesce for the cost of removal and returning the structure to its original state.

Guidance for non-permitted second kitchen Non-permitted second kitchens do not have to be removed unless as it stands provides a health or safety issue or is not allowed per zoning (i.e., illegal use)

For a single family home where the non-permitted second kitchen is allowed by zoning and is not a health or safety issue;

A non-permitted second kitchen should not be valued but the area should be included in the appropriate area calculations (GLA, Basement or other living area) as if the kitchen components have been removed.

The report should be "as is" as long as the appraiser describes the functional obsolescence for the cost of removing the kitchen and returning the structure to its original state.

However, the non-permitted second kitchen can be valued in its "as is" state without functional obsolescence if the appraiser can find two similar non-permitted kitchens to demonstrate market acceptance.

Guidance for non-permitted additions for a 2-4 unit property

If the additional unit was created by converting a portion of another unit (including basement) and is allowed by zoning but is not permitted, the property should be appraised based upon the number of permitted units/kitchens it possesses.

The report should be "as is" as long as the appraiser describes the functional obsolescence for the cost of removing the kitchen and any other requirement of returning the structure to its original state (the original number of units).

However, the non-permitted addition can be valued in its "as is" state if allowed by zoning, conversion was made in a workman-like manner and the appraiser provides three similar non-permitted conversion/units to demonstrate market acceptance.

SWBC Lending Solutions Copyright 2015 - SWBC Page 9

SECTION M - DECLINING MARKETS Refer to and utilize Fannie Mae Guidelines regarding defining and reporting declining markets. All reports indicating a declining market should include the following:

• Three closed sales within 90 days of the date of the appraisal. Explain if unavailable.

• Two listings and/or pending sales (pending sales are preferable).

• If time adjustments are not applied, the reason must be explained in the analysis.

• Time adjustments should be applied based on the contract date of the sales.

SECTION L - INDEPENDENCE STATEMENT Must Accompany Every Assignment (Please place above cost approach on page 3) No, employee, director, officer or agent of the lender, or any other third party acting as a joint venture partner, independent contractor, appraisal management company, or partner on behalf of the lender has influenced or attempted to influence the development, reporting, result or review of this assignment through coercion, extortion, collusion, compensation, instruction, inducement, intimidation, bribery or in any other manner. I have not been contacted by anyone other than the intended user (lender/client as identified on the first page of the report), borrower, or designated contact to make an appointment to enter the property. I agree to immediately report any unauthorized contacts either personally by phone or electronically.

SWBC Lending Solutions Copyright 2015 - SWBC Page 10

SECTION N - QUALITY CONTROL DELIVERABLES

At SWBC Lending Solutions, We strive to deliver a premium quality appraisal to the lenders that we service. Below is a list of standards that we

utilize in order to not only meet, but exceed the expectations of our clients.

Subject Section

• Properly identify all information concerning the legal descriptive for the subject property identify if the property is for a purchase,

refinance or other (describe) purpose.

• If the property is a purchase, please indicate all marketing that the property has gone through including but not limited to canceled,

expired, hold, pending and/or sold statuses. Please fully identify the times spent throughout each status and if there were any reductions in pricing.

• If the property is a purchase you MUST indicate that a contract for sale was reviewed and analyzed AND, you must indicate if there were

or were not any items which may affect the sales price. Neighborhood Section

• Identify the neighborhood appropriately. Check built up rate vs. Present land use percentage. Consider Urban, Suburban and Rural ratings in conjunction with your comparable search. Consider distances to support facilities, employment.

• Neighborhood boundaries are to be defined based on the subject property’s neighborhood and not based on the extended market area.

Properly define only the homogeneous neighborhood.

• Market conditions within the neighborhood section can encompass the range of properties throughout the neighborhood. This is opposed to the 1004MC, which should only include properties comparable to the subject property.

Site Section

• Site dimensions should be utilized if at all available (even if irregular). Appraiser is to check calculations against the reported size in public records/assessor role to determine accuracy.

• Plat map to be submitted for every appraisal and is publicly available in most instances. Please utilize your city/county sources and/or

subscription services to make available. Identify subject parcel.

• Please accurately report the “Specific Zoning Classification” and at minimum report the basic minimal lot size and minimal density requirements (units/acre). Residential or R1 for every report is not acceptable. Please familiarize yourself with city/county codes/regulations of area you service. This is a significant source of determination for the test of “Zoning Compliance”.

• Please describe any adverse site requirements (double check when adding your location map). Within the section which asks if there are

any adverse site conditions – Report what directly surrounds the subject property (Ex. Similar quality SFR’s to N,S,E with similar SFR across the street to the West).

• If the subject property exceeds the size of a typical “city size lot”, or over 1 acre, please describe the topography of the site, what is on

the site, if the site is likely to be divisible, and what the lot utility is. Subject Section

• Adequately identify the subject property. Please reflect “actual” effective age of property based on upgrades. If effective age greatly differs from actual age, identify all upgrades that have been made paying particular attention to: electrical, plumbing, heating, cooling, roofing, doors, windows, siding, foundation, flooring, kitchens, and baths.

• Report any physical, functional, or external depreciation to the subject property. All Depreciations are also to be reflected in the Cost

Approach and within the Sales Comparison Approach. Functional obsolescence concerning floor plan MUST be reflected in the Sketch by drawing interior walls.

Gross Living Area

The appraiser is to measure the exterior of the subject property to determine the gross living area. Interior dimensions are permitted for

condos and townhouses. Only areas that are attached and have continuous interior access, and are suitable for year round occupancy,

can be included in Gross Living Area (GLA). Living areas that are detached from the main structure, do not have direct interior access, or

are partially or fully below grade, are to be fully described and reported separately from the Gross Living Area.

To ensure consistency in the sales comparison analysis, appraisers must compare above-grade areas to above-grade areas and below-

grade areas to below-grade areas. In extreme instances appraisers may deviate from this approach if the style of the subject property or

any of the comparables does not lend itself to such comparisons. However, in such instances, the appraiser must explain the reason for

the deviation and clearly describe the comparisons that were made.

The appraiser is to reconcile any substantial difference between their measured living area and the living area reported on public records.

SWBC Lending Solutions Copyright 2015 - SWBC Page 11

SECTION N - QUALITY CONTROL DELIVERABLES (Continued)

Additions

When the appraiser determines an addition to the original structure is present, they are expected to describe the added improvements,

and comment on:

Whether the appraiser was able to confirm the existence of permits,

The conformity of the addition in both quality and functional utility to the original improvements,

The effects on marketability and compliance with local zoning laws including the consequences of being out of compliance

within the municipality.

When the additions or modifications create "Health and Safety" issues or are not allowed by zoning the appraisal is to be made

"subject-to" remediation of the item, or removal of the addition, depending on severity of the issue.

If zoning does not allow the non-permitted addition (e.g., a single family with a guest unit; a 3 or 4 unit when only a 2-unit is allowed),

the property is not acceptable for financing and the AMC should stop the inspection process to notify the AMC.

Permits

The appraiser is to document if they have verified the addition was built with permits and their source of information. Permitted

additions should be included in the GLA (if they meet the definition of GLA above), or as basement or additional living area as

appropriate. Non-permitted additions are only to be included in the GLA if all three of the following conditions are met:

They were constructed in a "workmanlike" manner,

Non-permitted additions are typical for the market area,

The appraiser is able to demonstrate market acceptance by the use of comparable sales with similar non-permitted additions.

Sales Comparison Analysis

• The known days on market should be included for each comparable provided

• Comparable properties currently offered for sale and comparable sales in the subject neighborhood within the past 12 months. This section resides above gridded comparables #1- #3. This data within these two spaces should be populated with data “comparable” to the subject property – meaning this data should be the data considered in your research of comparables for the subject property. This should not be data which shows “market trends” for the neighborhood, or for an extended marketing area. Also, this data should not be set by a predetermined value (Ex.$ 500,000-$700,000). This data should be the data reflected from the 1004MC data set. If it is not the same data set used from the 1004MC, please explain differences.

• All adjustments to comparables should be based on paired sales analysis from comparables which bracket the attributes of the subject

property. If bracketed comparables are not available forcing “across the board” adjustments to the comparables, please explain how these adjustments were derived.

• All adjustments should be made based on actual differences in value as supported by comparables. Differences should not be reduced

in order to avoid making comments concerning exceeding FNMA guidelines, and they should not be based upon anticipated underwriting expectations.

• Please identify and explain any line item adjustments which exceed 10% and/or identify any comparables which exceed 15% net or

25% gross adjustments. Also explain why it was necessary to utilize these comparables which exceed typical FNMA adjustment guidelines.

• Identify and explain – if all comparables net adjusted positively or negatively, if the value range of adjusted comparables exceeds 10%,

if final value is above or below unadjusted range of comparables.

• If time adjustments are necessary - make time adjustments based on contract date and clearly identify how the time adjustment was derived and applied.

• Appraiser to include closing document numbers for each sold comparable. If this data is not available due to non-disclosure . Please add

a comment indicating why they are not available.

• Identify any sales concessions – although these are commonly overlooked, concessions can have a significant impact on values. Identify, report, apply, and explain accordingly. If marketing time or contract date is reported in this section on the form, a comment will need to be reported concerning sales concessions for all comparables within the sales comparison analysis.

SWBC Lending Solutions Copyright 2015 - SWBC Page 12

SECTION N - QUALITY CONTROL DELIVERABLES

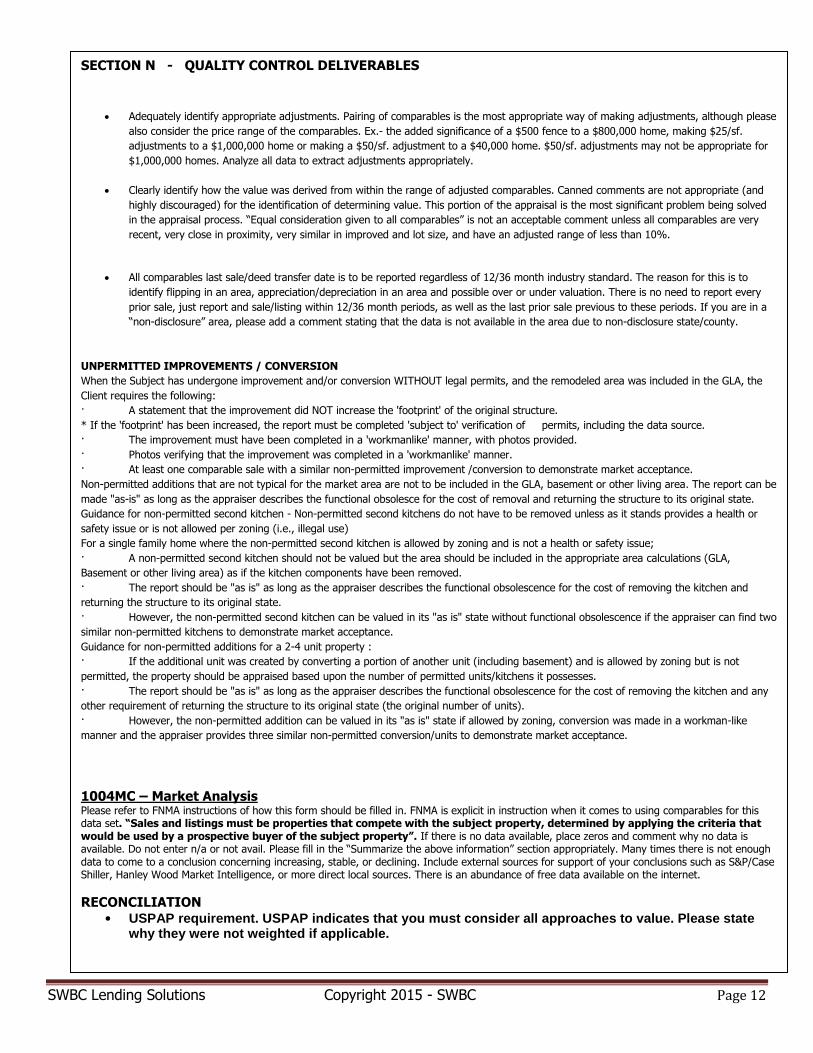

Adequately identify appropriate adjustments. Pairing of comparables is the most appropriate way of making adjustments, although please

also consider the price range of the comparables. Ex.- the added significance of a $500 fence to a $800,000 home, making $25/sf.

adjustments to a $1,000,000 home or making a $50/sf. adjustment to a $40,000 home. $50/sf. adjustments may not be appropriate for

$1,000,000 homes. Analyze all data to extract adjustments appropriately.

Clearly identify how the value was derived from within the range of adjusted comparables. Canned comments are not appropriate (and

highly discouraged) for the identification of determining value. This portion of the appraisal is the most significant problem being solved

in the appraisal process. “Equal consideration given to all comparables” is not an acceptable comment unless all comparables are very

recent, very close in proximity, very similar in improved and lot size, and have an adjusted range of less than 10%.

All comparables last sale/deed transfer date is to be reported regardless of 12/36 month industry standard. The reason for this is to

identify flipping in an area, appreciation/depreciation in an area and possible over or under valuation. There is no need to report every

prior sale, just report and sale/listing within 12/36 month periods, as well as the last prior sale previous to these periods. If you are in a

“non-disclosure” area, please add a comment stating that the data is not available in the area due to non-disclosure state/county.

UNPERMITTED IMPROVEMENTS / CONVERSION

When the Subject has undergone improvement and/or conversion WITHOUT legal permits, and the remodeled area was included in the GLA, the

Client requires the following:

· A statement that the improvement did NOT increase the 'footprint' of the original structure.

* If the 'footprint' has been increased, the report must be completed 'subject to' verification of permits, including the data source.

· The improvement must have been completed in a 'workmanlike' manner, with photos provided.

· Photos verifying that the improvement was completed in a 'workmanlike' manner.

· At least one comparable sale with a similar non-permitted improvement /conversion to demonstrate market acceptance.

Non-permitted additions that are not typical for the market area are not to be included in the GLA, basement or other living area. The report can be

made "as-is" as long as the appraiser describes the functional obsolesce for the cost of removal and returning the structure to its original state.

Guidance for non-permitted second kitchen - Non-permitted second kitchens do not have to be removed unless as it stands provides a health or

safety issue or is not allowed per zoning (i.e., illegal use)

For a single family home where the non-permitted second kitchen is allowed by zoning and is not a health or safety issue;

· A non-permitted second kitchen should not be valued but the area should be included in the appropriate area calculations (GLA,

Basement or other living area) as if the kitchen components have been removed.

· The report should be "as is" as long as the appraiser describes the functional obsolescence for the cost of removing the kitchen and

returning the structure to its original state.

· However, the non-permitted second kitchen can be valued in its "as is" state without functional obsolescence if the appraiser can find two

similar non-permitted kitchens to demonstrate market acceptance.

Guidance for non-permitted additions for a 2-4 unit property :

· If the additional unit was created by converting a portion of another unit (including basement) and is allowed by zoning but is not

permitted, the property should be appraised based upon the number of permitted units/kitchens it possesses.

· The report should be "as is" as long as the appraiser describes the functional obsolescence for the cost of removing the kitchen and any

other requirement of returning the structure to its original state (the original number of units).

· However, the non-permitted addition can be valued in its "as is" state if allowed by zoning, conversion was made in a workman-like

manner and the appraiser provides three similar non-permitted conversion/units to demonstrate market acceptance.

1004MC – Market Analysis Please refer to FNMA instructions of how this form should be filled in. FNMA is explicit in instruction when it comes to using comparables for this data set. “Sales and listings must be properties that compete with the subject property, determined by applying the criteria that would be used by a prospective buyer of the subject property”. If there is no data available, place zeros and comment why no data is available. Do not enter n/a or not avail. Please fill in the “Summarize the above information” section appropriately. Many times there is not enough data to come to a conclusion concerning increasing, stable, or declining. Include external sources for support of your conclusions such as S&P/Case Shiller, Hanley Wood Market Intelligence, or more direct local sources. There is an abundance of free data available on the internet.

RECONCILIATION • USPAP requirement. USPAP indicates that you must consider all approaches to value. Please state

why they were not weighted if applicable.

SWBC Lending Solutions Copyright 2015 - SWBC Page 13

SECTION O - CONDOMINIUM REQUIREMENTS

• ASK BORROWER/REALTOR/OWNER TO HAVE DEVELOPMENT ASSOCIATION INFORMATION AVAILABLE TO YOU WHEN SETTING APPT. TO EXPEDITE THE PROCESS-(Ex. # of units, phases, rented, for sale, sold, amenities, pending litigation, etc).

• Site size should be identified considering entire condo development. Density of site will be based upon the size of site divided by the number of units – please identify in units/acre. Please identify when this information is not obtainable.

• Please accurately report the “Specific Zoning Classification” and at minimum report the basic minimal lot size and minimal density

requirements (units/acre). Residential or R1 for condominiums is not applicable. Familiarize yourself with city/county codes/regulations of area you service. This is a significant source of determination for the test of “Zoning Compliance”.

• Please describe any adverse site requirements (double check when adding your location map). Within the section which asks if there

are any adverse site conditions – Report what directly surrounds the subject development (Ex. Similar quality SFR’s to N,S,E with similar SFR across the

• street to the West).

• Project information – Contacting Management Agency or HOA is necessary to verify details of development. Please discuss attempts to reach one of these agencies if appraiser is not able to. Report number of phases/units accordingly and identify source of information. If reporting 1 phase because phase information is not available, please report you are doing this and attempts at gaining this information. “# of units rented” is a critical portion of information and should be very accurate so that the loan can be properly underwritten. Explain how this information was obtained. Provide information contact and phone number.

• Condition - Be specific indicating individual unit numbers/conditions. Pay special attention to the location of the individual unit within

the project.

• Photos are required for all items being valued. Typically condominiums have some type of common area. Submit photos representative of Clubhouse/rec. room, common pool/spa, tennis courts, or any other common amenity.

• Selection of Condo Comparables – At minimum, two sold comparables within the development, and two sold

comparables outside the subject development (from competing development(s)) are to be utilized. Also, at least one pending sale or listing (same development) should be added to show current asking prices. Due to the current economic stigma of condominiums, we have found this comparable selection to provide the strongest support of value for the majority of lenders. This applies to new or existing constructed condominium complexes.

Condominiums with Commercial Space: The Lender will finance properties within a condominium project that includes commercial space. The appraiser must determine the percentage of commercial space in the project. If the commercial space represents more than 20% of the total square footage for the project, the appraiser must also:

State whether the amount of the commercial space is common for the local market Address whether the commercial space has an impact on the residential nature of the project Identify three projects with similar square footage of commercial space. Their actual commercial square footage does not need to be

itemized. (The appraiser is not required to provide the percentage of commercial space for the three projects. The appraiser is not required to use comparables located within one of these three projects. The appraiser must identify, in an addendum, three projects by providing their respective addresses).

Site Condominiums A site condominium is defined as a single family, totally detached dwelling (no shared garages or any other attached buildings) encumbered by a declaration of condominium covenants or condominium form of ownership. The appraiser must adhere to the following guidelines when completing an appraisal for a site Condo (Detached Condominium):

FHA/VA is to be completed on form FNMA1073/FHLMC 465 Non-FHA/Non-VA may also be completed on FNMA 1004/FHLMC 70 when the appraiser includes an adequate description of the project and information about the homeowners' association fees and the quality of the project maintenance.

Required information when form 1073/465 not used: Leave the checkbox blank adjacent to PUD. / The total number of units, the number of units completed, and number of units sold / Description of what comprises the common areas / The name of the HOA, Management Group or builder if in control of HOA / Does any single entity own more than 10% of the units in the project? / Are any common elements leased to or by the HOA? / Is the project adequately maintained? / What is the HOA fee and what does it cover?

SWBC Lending Solutions Copyright 2015 - SWBC Page 14

SECTION Q Changes to appraisals or Rebuttals – Please make changes as soon as possible! Occasionally you may be asked to make changes to your appraisal based on typographical error, omissions from appraisal, or a need for additional commentary. At SWBC Lending Solutions we utilize an automated review system as well as an Internal Review Staff who will work with you in order to provide a Quality product which meet client requirements. You may receive an automated and/or manual correction request. We ask that you make these corrections within 24 hours in order to meet important deadlines. Prior to submission to lender, these changes can typically be made and returned to SWBC Lending Solutions. After the appraisal has been submitted to the lender, we ask that you make your changes to the appraisal and add a comment section at the end of your comment addendum stating the effective date of changes and exactly what was changed. Example – Changes as of 01/01/2010: Based on submission of a legal subdivision from title, the site size has been corrected. The additional lot (lot 6) originally valued has been excluded from this appraisal. The additional lot was not of significant size which would require additional comparables. All comparables site sizes have been readjusted at $1.00/sf., resulting in a value change from $210,000 to $200,000. Effective date of appraisal will remain the same. Date of Signature and report will be 01/01/2010 or date of change. “Changes to appraisals” also applies to value rebuttals. CONDITION DEFICIENIES When the Subject is in C5 or C6 (below average) condition, the Client requires the report be made 'subject to’ the required repairs/inspections necessary to bring the subject up to C4 (average) condition AND that the following be provided:

A description of the repair/inspection items. An itemized cost to cure estimate for the repair items. A Subject overall condition rating which reflects the 'as-improved' condition of the property. Comparable sales that reflect the 'as-improved' condition of the property. Demonstrative photos of observations which indicate needed repair(s)/inspection(s).

* NOTE: If during the inspection it becomes evident that the Subject condition deficiencies are such that repair is NOT financially feasible take photograph evidence of the deficiencies. Stop & Notify the AMC. *The Client requires that the Subject property be habitable and free of any health and/or safety hazards OR the report must be made 'subject to' the repair and/or expert inspection of the specific deficiency. This would include any deficiencies that affect Safety, Security or Structural Soundness, such as:

Bedroom windows with security bars, with no safety release latches, in rooms with no other outside access. Upper level door with no balcony or steps. Obvious deterioration/destruction from water, insects, etc. Other similar conditions that adversely affect the safety and livability of the property.

SECTION P - 2-4 Small Income Property Appraisal (1025) Rental Analysis

• Provide at least two rent comparables for each unit type within the subject property. Pay particular attention to rent/sf. and rent/bedroom. You will have to calculate these indicators, although this is what reviewers and underwriters are very particular about.

• Please thoroughly explain how you derived the opinion of market rent for the subject property. Also, when forecasting market rents for

the subject property pay particular attention to current restrictions in being able (legally) to raise rents (ex. rent control, leasing restrictions).

Gross Rent Multiplier

• GRM must be supported. Be careful when weighting your comparable sales when determining your GRM. Two unit GRM’s for instance are typically higher than three and more units. You should make every effort to utilize similar unit properties when determining your GRM. Please provide detailed analysis as to how the GRM was extracted from the market, how the comparable GRM’s mare weighted and why, and how the final estimate was determined in the income approach to value.

Units of Comparison

• Carefully analyze unadjusted and adjusted units of comparison (price per unit/room/GBA, bedroom). Comment on how units of comparison were selected from within the range of comparables. If units of comparison are reconciled outside of the range of adjusted units of comparison, explanation will need to be made and supported. It is necessary to comment on which units of comparison are weighted most heavily and why.

SWBC Lending Solutions Copyright 2015 - SWBC Page 15

SECTION R - PRIVACY AND DATA SECURITY

You represent and warrant that you have, and covenant that for so long as you retain Personally Identifiable Information (Personally Identifiable Information has the meaning of nonpublic personal information under the Gramm-Leach-Bliley Act (Pub. L. 106-102 (1999) (GLBA)) you will continue to have, adequate administrative, technical, and physical safeguards to (A) ensure the security and confidentiality of such Personally Identifiable Information (as defined under the GLBA as implemented); (B) protect against any anticipated or reasonably likely threats or hazards to the security or integrity of such Personally Identifiable Information; (C) protect against unauthorized access to or use of such Personally Identifiable Information; (D) ensure the proper disposal of Personally Identifiable Information and (E) without limiting the generality of items (A) through (D) preceding, comply with the requirements contained in Section 501(b) of the GLB Act and the Interagency Guidelines Establishing Information Security Standards adopted by federal bank regulatory agencies, including the OCC and Board of Governors of the Federal Reserve System. In addition, you represent and warrant that the manner in which Personally Identifiable Information is maintained, transported and transmitted will comply with applicable state laws imposing data security requirements, including 201 CMR 17.00 et seq., Massachusetts Standard for the Protection of Personal Information of Residents of the Commonwealth. In addition to the prior representations and warranties, you agree to: a) Develop, implement and maintain, at your own expense, a proven system or methodology to audit for compliance with your administrative,

technical, and physical safeguards. b) Not share Client Information with any subcontractor or third party. c) DO NOT DISCUSS APPRAISAL FEES OR VALUE CONCLUSION with borrowers, realtors, or any parties other than SWBC

Lending Solutions. d) If required by the terms of this Service Engagement Letter or Applicable Law to store the client Confidential Information or any modification

thereto and Supplier is the primary source for such data, you must ensure a back-up or alternate copy of such data exists. Backup copies shall be maintained in a physically secured environment.

e) Ensure documents created which contain the client Confidential Information are labeled in accordance with your data classification labeling. f) Maintain documents within a physically secure facility. You must employ commercially reasonable controls to prevent unauthorized access

and establish tracking mechanism to establish physical access to the Information. When documentation is not in use it shall be locked away in a cabinet, ideally with fire resistant capability

g) Destroy paper documentation using a commercial shred product, into confetti-sized pieces. h) No electronic copies may be made or maintained of client Information. You must immediately notify SWBC Lending Solutions if you discover there has been a material breach of, or a serious attempt to breach, your security safeguards required by this Section [Internal cite to above requirements], or if the security of Personally Identifiable Information has been or may be compromised for any reason (including unauthorized access to and unauthorized attempts to access Personally Identifiable Information by colleagues, coworkers or any other internal or external individuals or entities (Personnel necessary to perform the obligations under this Service Engagement Letter for which such Personally Identifiable Information was disclosed. You must ensure that Personnel cannot attempt to access, or allow access to, any Personally Identifiable Information that they are not permitted to access in connection with the provision of Services under this Service Engagement Letter.

SECTION S - REVIEWS

Desk Review

Complete of Form 2006 Provide analysis and conclusions Client is looking for AS IS or Other Discuss Market Conditions

Field Review

Complete on form 2000 Provide your own value Provide subject exterior photos and your own comp photos. (not MLS photos)

SWBC Lending Solutions Copyright 2015 - SWBC Page 16

SECTION T - 1004D

Certificate of Completion

Describe ALL improvements completed or not completed Provide photos of each item (completed or not completed) If FHA assignment you must address how subject now meets HUD minimum property standards

Update of Value

You must provide support for current market condition 1004MC is required and should be consistent with your conclusion Provide exterior photo of subject

SECTION U - 1007 Market Rent

PROVIDE OWN PHOTOS (Not MLS)