Sustainable Finance and Fintech: progress and innovation ...

45

Sustainable Finance and Fintech: progress and innovation, 6 February 2020 1 Servizio Studi – Equity Research Sustainable Finance and Fintech: progress and innovation 6 February 2020 Sala Assemblee via Fratelli Gabba

Transcript of Sustainable Finance and Fintech: progress and innovation ...

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

1 Servizio Studi – Equity Research

Sustainable Finance and Fintech: progress and innovation

6 February 2020 Sala Assemblee via Fratelli Gabba

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

2 Servizio Studi – Equity Research

6 February 2020 Sala Assemblee via Fratelli Gabba

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

3 Servizio Studi – Equity Research

Summary

Centrale del Latte d’Italia 4 MailUp 24 CNH Industrial 6 NB Aurora 26 Elettra Investimenti 8 NEXI 28 Equita Group 10 Notorious Pictures 30 Ferrari 12 Piaggio 32 First Capital 14 Reply 34 Gefran 16 SIT 36 Grifal 18 Spactiv 38 Leone Film Group 20 TraWell 40 LU-VE 22

Disclaimer 42

Team 44

Please note: all the reccomandations, estimates and target prices refer to our latest published reports on every single stock available

on www.ubibanca.com/equity-research.

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

4 Servizio Studi – Equity Research

Centrale del Latte d’Italia 03 February 2020 – 5:30 PM SELL TARGET PRICE: 2.03 MARKET PRICE: 2.46

Food & Beverage

Data

Shares outstanding (m): 14.00

Market Cap. (EURm): 34.44

Enterprise Value (EURm): 121.70

Av. Daily Trad. Vol. (000): 7.6

Reuters/Bloomberg: CLI.MI CLI IM

52-Week Range (EUR): 2.4 2.9

Source: FactSet

Performance

1m 3m 12m

Absolute 1.7% -3.9% -9.9%

Rel. to FTSE IT 3.0% -6.3% -22.7%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile Centrale del Latte d’Italia is the third largest milk company in Italy after Parmalat and Granarolo and the market leader in the regions where it is present

(Piedmont, Liguria, Tuscany and Veneto). The group produces and distributes milk (fresh, ESL and UHT), milk derivatives, vegetable drinks, salads, cured meats, eggs and pasta. It has four plants, a fleet of >300 self-cooling vehicles, and 413

employees. Its four brands are well known and can demand a premium price and have increased their market shares in recent years (now at 7.7% in the fresh milk and 4% in UHT). As for distribution channels, >50% of revenues come from mass

retail, 36% from traditional trade and around 7% from private label. CLI was listed

on the Milan Stock Exchange in 2000 and moved to the STAR segment in 2001.

Recent development Despite the poor volume trend (value of production was down 1.3% in 3Q19

and 1.8% in 9M19) and soaring fresh milk price (+14.8% in 3Q19), CLI was able to increase EBITDA by 16% in 3Q19 (after the sharp slowdown of 1H19) thanks to effective cost cutting actions implemented in the past few months. However,

higher D&A costs led to breakeven at EBIT level while pre-tax result was negative for EUR0.45 million (EUR4.2 million in the first nine months) and net debt remained stable at EUR84.8 million (including EUR4.8 million for the adoption of

IFRS 16). The company guided for the last quarter of the year financial results similar to 3Q19, thus implying a revenues slowdown of around 2% in the full year

with an EBITDA margin around 4% (compared with 4.3% in 2018). Considering

that: 1) cash flow generation should remain negative in the full year, 2) the investment plan for the revamping of the Turin plant is proceeding, 3) the risk of breaking the existing covenants on the banks financing and on the 2017-24 bond, the company confirmed significant capital and financial strengthening within year-

end, which in our view could translate in a capital increase which could generate a significant dilution for existing shareholders. A capital increase of EUR5.0 million was already approved by the Board for Centrale del Latte di Vicenza.

Corporate Governance

Does the company have a combined Chairman/CEO? Yes

Percentage of independent directors 46.15% (6 out of 13)

Does the company have loyalty shares? No

Does major shareholders have a “shareholders pact” in place? Yes

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? No

CEO remuneration detail (fixed salary) EUR0.57 million

Chairman remuneration detail (fixed salary) EUR0.37 million

Is the share price included in the MBO criteria? No

Percentage of treasury shares 0.0%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? No

Social Responsibilities

Does the company publish a separated Sustainability report? No

Does the company have a Chief SRI/CSR officer (or a committee)? No

Does the Chief SRI/CSR officer votes in any of the committee? NA

Is the Investor Relation officer a different person from CFO (or other officers)?

Yes

Is the ESG strategy integrated in the Business Plan (or in the group strategy)?

No

Does the company have an ethical code? Yes

Percentage of female directors 38.46% (5 out of 13)

How is the cybersecurity issue managed? Not disclosed

SWOT Analysis

Strengths Weaknesses

• Leading position where it is present and strong brand awareness

• Increasing product diversification

• Low NWC and negative operating working capital

• Declining consumption of fresh and UHT milk in Italy

• Continuous price pressure from large distributors

• Lower innovation and marketing capacity than larger companies

Opportunities Threats

• The restructuring of the Turin production facility

• Cost synergies with Centrale del Latte di Firenze

• Agreement with Alibaba to distribute UHT milk in China

• Strong volatility of the raw milk price

• Private label competition and potential entry of large multinationals

• Strong price power of mass retail chains

2,200

2,700

3,200

CDL FTSE Italia All-Share

Fin, Centr. Latte Torino;

39,3%

Comune di

Firenze; 12,3%Fidi Toscana; 6,8%

Comune di

Pistoia; 5,3%

Free float; 36,3%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

5 Servizio Studi – Equity Research

Centrale del Latte d’Italia

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 183.14 180.36 185.33 193.24 ROE 0.6% -4.1% -3.7% -2.4%

EBITDA 7.79 7.21 7.72 9.35 Net Fin. Debt / Equity (x) 1.2 1.3 1.4 1.3

EBITDA margin 4.3% 4.0% 4.2% 4.8% Net Fin. Debt / EBITDA (x) 9.5 11.3 10.4 8.2

EBIT 0.85 -2.32 -1.56 -0.02 Capex / Sales 8.9% 8.4% 4.0% 3.0%

EBIT margin 0.5% -1.3% -0.8% -0.0% Pay Out Ratio 0.0% 0.0% 0.0% 0.0%

Profit before taxes -0.40 -4.18 -3.60 -2.01

Taxes 0.80 1.67 1.44 0.60

Net Income 0.40 -2.51 -2.16 -1.41

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS 0.03 -0.18 -0.15 -0.10

Growth Rates DPS 0.00 0.00 0.00 0.00

(%) 2018A 2019E 2020E 2021E BVPS 4.55 4.37 4.22 4.12

Growth Group Net Sales 0.5% -1.5% 2.8% 4.3%

Growth EBITDA 7.6% -7.5% 7.1% 21.2%

Growth EBIT 29.0% nm nm nm

Growth Net Profit nm nm nm nm Stock Market Ratios* *((Priced(Priced

(x) 2018A 2019E 2020E 2021E

P/E nm nm nm nm

P/OpCFPS 7.6 4.5 4.2 3.5

Balance Sheet P/BV 0.7 0.6 0.6 0.6

(EURm) 2018A 2019E 2020E 2021E Dividend Yield (%) 0.0% 0.0% 0.0% 0.0%

Capital Employed 137.52 142.50 139.52 133.95 EV/Sales

0.7 0.7 0.7 0.6

Shareholders’ Equity 63.72 61.22 59.06 57.65 EV/EBITDA 15.7 16.9 15.7 12.5

Net Financial Debt / (Cash) 73.80 81.29 80.46 76.30 EV/EBIT nm nm nm nm

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

6 Servizio Studi – Equity Research

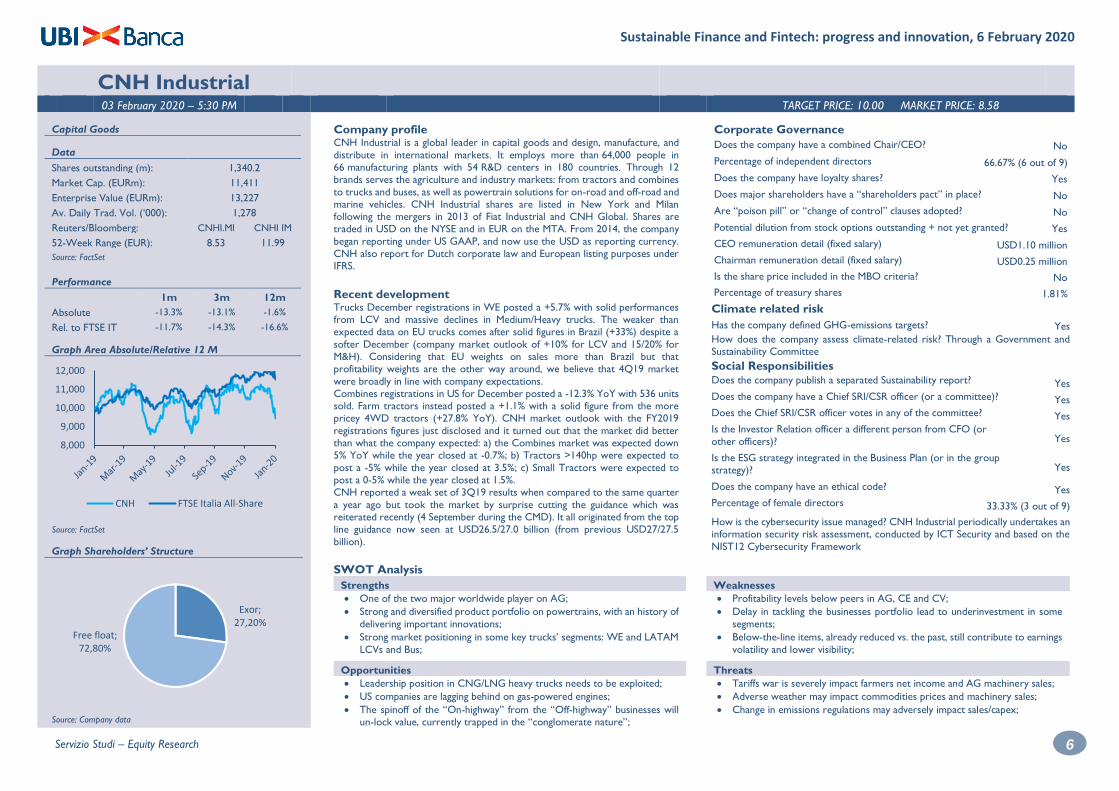

CNH Industrial 03 February 2020 – 5:30 PM TARGET PRICE: 10.00 MARKET PRICE: 8.58

Capital Goods

Data

Shares outstanding (m): 1,340.2

Market Cap. (EURm): 11,411

Enterprise Value (EURm): 13,227

Av. Daily Trad. Vol. (‘000): 1,278

Reuters/Bloomberg: CNHI.MI CNHI IM

52-Week Range (EUR): 8.53 11.99

Source: FactSet

Performance

1m 3m 12m

Absolute -13.3% -13.1% -1.6%

Rel. to FTSE IT -11.7% -14.3% -16.6%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile CNH Industrial is a global leader in capital goods and design, manufacture, and

distribute in international markets. It employs more than 64,000 people in 66 manufacturing plants with 54 R&D centers in 180 countries. Through 12 brands serves the agriculture and industry markets: from tractors and combines

to trucks and buses, as well as powertrain solutions for on-road and off-road and marine vehicles. CNH Industrial shares are listed in New York and Milan following the mergers in 2013 of Fiat Industrial and CNH Global. Shares are traded in USD on the NYSE and in EUR on the MTA. From 2014, the company

began reporting under US GAAP, and now use the USD as reporting currency.

CNH also report for Dutch corporate law and European listing purposes under IFRS.

Recent development Trucks December registrations in WE posted a +5.7% with solid performances from LCV and massive declines in Medium/Heavy trucks. The weaker than expected data on EU trucks comes after solid figures in Brazil (+33%) despite a

softer December (company market outlook of +10% for LCV and 15/20% for M&H). Considering that EU weights on sales more than Brazil but that profitability weights are the other way around, we believe that 4Q19 market

were broadly in line with company expectations. Combines registrations in US for December posted a -12.3% YoY with 536 units sold. Farm tractors instead posted a +1.1% with a solid figure from the more

pricey 4WD tractors (+27.8% YoY). CNH market outlook with the FY2019

registrations figures just disclosed and it turned out that the market did better than what the company expected: a) the Combines market was expected down 5% YoY while the year closed at -0.7%; b) Tractors >140hp were expected to

post a -5% while the year closed at 3.5%; c) Small Tractors were expected to post a 0-5% while the year closed at 1.5%. CNH reported a weak set of 3Q19 results when compared to the same quarter

a year ago but took the market by surprise cutting the guidance which was reiterated recently (4 September during the CMD). It all originated from the top line guidance now seen at USD26.5/27.0 billion (from previous USD27/27.5

billion).

Corporate Governance

Does the company have a combined Chair/CEO? No

Percentage of independent directors 66.67% (6 out of 9)

Does the company have loyalty shares? Yes

Does major shareholders have a “shareholders pact” in place? No

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? Yes

CEO remuneration detail (fixed salary) USD1.10 million

Chairman remuneration detail (fixed salary) USD0.25 million

Is the share price included in the MBO criteria? No

Percentage of treasury shares 1.81%

Climate related risk

Has the company defined GHG-emissions targets? Yes

How does the company assess climate-related risk? Through a Government and Sustainability Committee

Social Responsibilities

Does the company publish a separated Sustainability report? Yes

Does the company have a Chief SRI/CSR officer (or a committee)? Yes

Does the Chief SRI/CSR officer votes in any of the committee? Yes

Is the Investor Relation officer a different person from CFO (or

other officers)? Yes

Is the ESG strategy integrated in the Business Plan (or in the group strategy)? Yes

Does the company have an ethical code? Yes

Percentage of female directors 33.33% (3 out of 9)

How is the cybersecurity issue managed? CNH Industrial periodically undertakes an information security risk assessment, conducted by ICT Security and based on the

NIST12 Cybersecurity Framework

SWOT Analysis

Strengths Weaknesses

• One of the two major worldwide player on AG;

• Strong and diversified product portfolio on powertrains, with an history of

delivering important innovations;

• Strong market positioning in some key trucks’ segments: WE and LATAM

LCVs and Bus;

• Profitability levels below peers in AG, CE and CV;

• Delay in tackling the businesses portfolio lead to underinvestment in some

segments;

• Below-the-line items, already reduced vs. the past, still contribute to earnings

volatility and lower visibility;

Opportunities Threats

• Leadership position in CNG/LNG heavy trucks needs to be exploited;

• US companies are lagging behind on gas-powered engines;

• The spinoff of the “On-highway” from the “Off-highway” businesses will un-lock value, currently trapped in the “conglomerate nature”;

• Tariffs war is severely impact farmers net income and AG machinery sales;

• Adverse weather may impact commodities prices and machinery sales;

• Change in emissions regulations may adversely impact sales/capex;

Exor; 27,20%

Free float; 72,80%

8,000

9,000

10,000

11,000

12,000

CNH FTSE Italia All-Share

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

7 Servizio Studi – Equity Research

CNH Industrial

Income Statement Financial Ratios

(USDm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 29.706 28.520 29.422 30.480 ROE 21,1% 23,7% 16,8% 17,1%

EBITDA 2.671 2.495 2.666 2.873 Net Fin. Debt / Equity (x) 0,12 0,08 0,03 (0,01)

EBITDA margin 9,0% 8,7% 9,1% 9,4% Net Fin. Debt / EBITDA (x) 0,22 0,22 0,09 (0,02)

EBIT 2.101 1.891 2.088 2.298 Capex / Sales 2,0% 2,2% 3,5% 3,7%

EBIT margin 7,1% 6,6% 7,1% 7,5% Pay Out Ratio 25,2% 20,9% 30,5% 30,8%

Profit before taxes 1.566 1.373 1.702 1.995

Taxes (417) 165 (454) (532)

Net Income 1.068 1.503 1.220 1.429

Per Share Data

(USD) 2018A 2019E 2020E 2021E

EPS 0,79 1,11 0,90 1,06

Growth Rates DPS 0,198 0,232 0,275 0,325

(%) 2018A 2019E 2020E 2021E BVPS 3,7 4,7 5,4 6,2

Growth Group Net Sales 7,2% -4,0% 3,2% 3,6%

Growth EBITDA 15,1% -6,6% 6,9% 7,7%

Growth EBIT 28,2% -10,0% 10,4% 10,0%

Growth Net Profit n.m. 40,6% -18,8% 17,2% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E 15,1 8,5 10,5 8,9

P/OpCFPS 13,9 15,6 7,6 7,0

Balance Sheet P/BV 3,18 2,01 1,75 1,53

(USDm) 2018A 2019E 2020E 2021E Dividend Yield (%) 1,7% 2,5% 2,9% 3,5%

Capital Employed 23.710 24.594 24.582 24.703 EV/Sales

0,65 0,55 0,52 0,49

Shareholders’ Equity 5.043 6.312 7.246 8.338 EV/EBITDA 6,79 5,87 5,37 4,88

Net Financial Debt / (Cash) 600 537 227 (59) EV/EBIT 11,45 10,41 8,97 7,79

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

8 Servizio Studi – Equity Research

Elettra Investimenti 03 February 2020 – 5:30 PM TARGET PRICE: 11.81 MARKET PRICE: 8.60

Energy Services

Data

Shares outstanding (m): 3.8

Market Cap. (EURm): 33.0

Enterprise Value (EURm): 53.6

Av. Daily Trad. Vol. (000): 4.8

Reuters/Bloomberg: ELIN.MI ELIN IM

52-Week Range (EUR): 8.4 10.1

Source: FactSet

Performance

1m 3m 12m

Absolute 1.8% -3.4% -11.2%

Rel. to FTSE IT 3.1% -5.8% -23.8%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile Elettra Investimenti is an industrial holding company operating in Italy in the sector of electricity and thermal energy production from natural gas and

renewable sources according to the Distributed Generation approach (mainly cogeneration and trigeneration plants with 14 plants for a total 26MW capacity), in energy efficiency and car sharing. The strategy of Elettra Investimenti involves

strengthening the competitive position through the acquisition of third-party plants, the development of O&M business lines and energy efficiency, technological innovation in energy service. Elettra Investmenti has been listed on

the AIM market since April 2015 at EUR6.0 per share raising EUR4.3 million. In

the past four years the company grew substantially, doubling its size, thanks to acquisitions (Tholos in 2016, PHPower in 2017) and internal initiatives (UVAM, car sharing etc.), diversifying its product portfolio.

Recent development

Elettra Investimenti reported 1H19 results slightly above our estimates as for sales but below our expectations as for EBITDA margin which came to 13.6% vs. 18.1% in 1H18 and our 15.2% estimate. This is explained by the drop of the gross margin coming from the TEE trading (EUR1.64 million vs. EUR5.85 million in

1H18) and by higher labour cost (now at 10.4% of sales vs. 7.7% in 1H18) due to further hiring to sustain the company’s expansion. The good news is the strong increase of the gross margin coming from industrial activities which more than

doubled reaching EUR6.8 million compared with EUR3.4 million in the first half

of 2018 with an average margin of 29.9% vs. 23.5% in 1H18.In our view, this clearly shows that Elettra Investimenti is ready to replace the earnings coming from TEE, which will soften in future, with industrial activities which increased

sales by 59% in 1H19. Following 1H19 results and the sharp decrease of TEE contribution, we revised our estimates. For 2019, we slightly decreased our top line forecast, implying 15% sales growth in the second half of the year. However,

we lowered our EBITDA expectations incorporating the EBITDA slowdown reported in 1H19, implying a 16.2% EBITDA margin in the second half of the year. Altogether, our net profit is expected at EUR2.2 million, 50% below our

previous estimates.

Corporate Governance

Does the company have a combined Chair/CEO? Yes

Percentage of independent directors 28.57% (2 out of 7)

Does the company have loyalty shares? No

Does major shareholders have a “shareholders pact” in place? No

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? Yes

CEO remuneration detail (fixed salary) Not disclosed

Chairman remuneration detail (fixed salary) Not disclosed

Is the share price included in the MBO criteria? Not disclosed

Percentage of treasury shares 0.90%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? No

Social Responsibilities

Does the company publish a separated Sustainability report? No

Does the company have a Chief SRI/CSR officer (or a committee)? No

Does the Chief SRI/CSR officer votes in any of the committee? NA

Is the Investor Relation officer a different person from CFO (or other officers)?

Yes

Is the ESG strategy integrated in the Business Plan (or in the group strategy)?

Yes

Does the company have an ethical code? No

Percentage of female directors 42.9% (3 out of 7)

How is the cybersecurity issue managed? Not disclosed

SWOT Analysis

Strengths Weaknesses

• Profitable operating assets not related to incentives

• Current order backlog covers nearly 7 years of revenues

• Excellent M&A track record

• Limited size compared to main Italian peers

• Softening TEE market

• Complex Group’s structure

Opportunities Threats

• New “Exacto” platform for energy monitoring

• Development of new products

• Potential new acquisitions

• Possible changes in the regulatory framework

• Execution risk

• The current wide product portfolio could stress the management

8,000

9,000

10,000

11,000

12,000

Elettra FTSE Italia All-Share

Bombacci family; 81,9%

Treasury; 0,9%

Free float; 17,2%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

9 Servizio Studi – Equity Research

Elettra Investimenti

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 55.0 61.5 60.3 61.9 ROE 9.0% 14.1% 15.7% 16.0%

EBITDA 8.5 9.2 9.9 10.4 Net Fin. Debt / Equity (x) 1.0 1.1 1.2 1.2

EBITDA margin 15.4% 15.0% 16.4% 16.8% Net Fin. Debt / EBITDA (x) 1.7 2.0 2.1 2.2

EBIT 3.7 4.2 4.7 5.1 Capex / Sales 13.7% 11.6% 13.9% 15.5%

EBIT margin 6.8% 6.8% 7.8% 8.2% Pay Out Ratio 73.4% 68.9% 64.7% 65.8%

Profit before taxes 3.1 3.7 4.3 4.7

Taxes -1.8 -1.5 -1.6 -1.8

Net Income 1.3 2.2 2.7 2.9

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS 0.34 0.58 0.69 0.76

Growth Rates DPS 0.25 0.40 0.45 0.50

(%) 2018A 2019E 2020E 2021E BVPS 3.80 4.13 4.43 4.74

Growth Group Net Sales 17.0% 11.7% -1.9% 2.7%

Growth EBITDA -28.0% 8.6% 7.5% 5.0%

Growth EBIT -47.5% 11.8% 12.9% 7.3%

Growth Net Profit -70.6% 70.6% 19.6% 9.3% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E 29.5 14.8 12.4 11.3

P/OpCFPS 10.4 3.9 4.5 3.8

Balance Sheet P/BV 2.7 2.1 1.9 1.8

(EURm) 2018A 2019E 2020E 2021E Dividend Yield (%) 2.5% 4.7% 5.2% 5.8%

Capital Employed 30.2 34.9 38.5 42.3 EV/Sales

1.0 0.9 0.9 0.9

Shareholders’ Equity 14.6 15.9 17.0 18.2 EV/EBITDA 6.6 5.8 5.7 5.6

Net Financial Debt / (Cash) 14.8 18.2 20.8 23.4 EV/EBIT 15.1 12.9 11.9 11.6

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

10 Servizio Studi – Equity Research

Equita Group 03 February 2020 – 5:30 PM TARGET PRICE: 3.37 MARKET PRICE: 2.84

Investment Banking

Data

Shares outstanding (m): 45.5

Market Cap. (EURm): 129.1

Enterprise Value (EURm): NA

Av. Daily Trad. Vol. (‘000): 26.1

Reuters/Bloomberg: EQUI.I EQUI IM

52-Week Range (EUR): 2.43 3.27

Source: FactSet

Performance

1m 3m 12m

Absolute -0.4% 13.6% 7.2%

Rel. to FTSE IT 1.2% 12.4% -26.1%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile Equita is the leading boutique in Italy with distinctive features like the largest

trading floor in Italy, a top-ranked research team and clear positioning in the mid-

market segment. In the last ten years, Equita has grown its investment banking

division from scratch and also developed an Alternative Asset Management

(AAM) division business, which, starting from portfolio management, has grown

into private debt and private equity. The diversification effort included also the

entrance into retail trading on equities and bonds and the extension of the Global

markets activities to derivatives, ETFs and, more important, fixed incomes and

market making. Equita today operates three different business lines: a) Global

Markets (65% of 9M2019 Net Revenues); b) Investment Banking (27%); c) AAM

(8%). In 2017 it listed on the AIM segment and, in 2018, it moved to the STAR.

Recent development

Last November management presented a mid-long term business plan, in our view, to give more visibility on what the shape of the group will be once all the recent initiatives will reach a cruise speed: a) Global market: end-markets are still seen tough and the revenues growth toward the high end of the EUR30/34

million range (between 40% and 45% of total revenues) should be driven by cross-selling and diversification; b) IB: the plan assumes a EUR30/34 million revenues target (again 40-45% of total) which means at least doubling from the

EUR15 million expected for this year, but the 2022 target is more realistic if seen in the context of the EUR26 million achieved only one year ago; c) AAM: the launch of the SGR should ease the AuM growth towards the EUR2 billion

targeted with revenues being 10% of total (EUR8-11 million).

In the third quarter of 2019 Equita financials showed, finally, some signs of stabilization with a EUR1,6 million net profit, +4% vs. the 3Q18 figure. Revenues were up YoY thanks to market shares gains in Global Markets and despite negative m-t-m of Equita's SPAC. In the wording of the 3Q19 release, it seems

clear how management perceives a stabilization in market conditions, specifically in Investment Banking.

Corporate Governance

Does the company have a combined Chair/CEO? No

Percentage of independent directors 12.86% (3 out of 7)

Does the company have loyalty shares? Yes

Does major shareholders have a “shareholders pact” in place? Yes

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? Yes

CEO remuneration detail (fixed salary) EUR0.65 million

Chairman remuneration detail (fixed salary) EUR0.24 million

Is the share price included in the MBO criteria? No

Percentage of treasury shares 9.1%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? No

Social Responsibilities

Does the company publish a separated Sustainability report? No

Does the company have a Chief SRI/CSR officer (or a committee)? Yes

Does the Chief SRI/CSR officer votes in any of the committee? Yes

Is the Investor Relation officer a different person from CFO (or other officers)?

Yes

Is the ESG strategy integrated in the Business Plan (or in the group strategy)?

Yes

Does the company have an ethical code? Yes

Percentage of female directors 28.57% (2 out of 7)

How is the cybersecurity issue managed? Not disclosed

SWOT Analysis

Strengths Weaknesses

• Leading position in the cash-equity Italian market;

• Experienced management with an entrepreneurial attitude;

• High employees’ retention rates;

• Sales & Trading and Proprietary Trading businesses are volatile;

• Revenues are Italy-centric (i.e. from Italian customers/Italian assets/stocks);

• Its small size compared to International players/some Italian players;

Opportunities Threats

• Higher cross-selling;

• Development of AAM, which could add visibility to revenues;

• The company has enough resources to grow in-organically;

• Reputational risk;

• Key people risk (mitigated by shareholders pacts)

• Country risk.

2,200

2,700

3,200

3,700

Equita FTSE Italia All-Share

Management and

employees; 53,90%

Treasury shares; 9,10%

Free float; 37,00%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

11 Servizio Studi – Equity Research

Equita Group

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 59,8 52,5 57,6 61,7 RoE 13,8% 10,4% 13,0% 14,5%

Personnel Costs 27,4 24,2 26,0 28,0 RoTE 20,4% 14,8% 19,1% 21,6%

Administrative Expenses 16,8 16,6 16,8 16,9 Cost/Income 73,9% 77,6% 74,3% 72,7%

Profit Before Taxes 15,6 11,8 14,8 16,9 Comp/Revenues 45,8% 46,0% 45,2% 45,3%

% on Net Revenues 26,1% 22,4% 25,7% 27,3% RoE/CoE (x)

1,97 1,48 1,85 2,06

Income Taxes 4,5 3,7 4,5 5,1

Group Net Profit 11,0 8,1 10,3 11,7

Net Income Adjusted 12,0 8,1 10,3 11,7

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS Adjusted 0,26 0,18 0,23 0,26

Growth Rates DPS 0,22 0,20 0,22 0,25

(%) 2018A 2019E 2020E 2021E BVPS ex treasury 1,76 1,72 1,75 1,78

Growth Group Net Sales 10,9% -12,2% 9,7% 7,2%

Growth EBITDA 1,6% -24,5% 25,8% 13,8%

Growth EBIT 0,2% -26,3% 26,7% 13,8%

Growth Net Profit 6,6% -32,0% 26,7% 13,8% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E (x) 13,2 15,8 12,5 11,0

P/E Adjusted (x) 12,2 15,8 12,5 11,0

Balance Sheet P/BV (x) 1,8 1,6 1,6 1,6

(EURm) 2018A 2019E 2020E 2021E P/TBV (x) 2,2 2,0 2,0 2,0

Shareholders’ Equity 80,1 78,2 79,4 81,1 Dividend Yield (%) 6,9% 7,1% 7,7% 8,6%

RWA 218,2 212,9 224,9 236,2 RoE/CoE (x) 2,0 1,5 1,9 2,1

RoTE 20,4% 14,8% 19,1% 21,6% Payout 90,7% 111,9% 97,1% 95,0%

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

12 Servizio Studi – Equity Research

Ferrari 03 February 2020 – 5:30 PM TARGET PRICE: 180 MARKET PRICE: 152.5

Branded Goods

Data

Shares outstanding (m): 179.7

Market Cap. (EURm): 28,643

Enterprise Value (EURm): 27,427

Av. Daily Trad. Vol. (‘000): 429.0

Reuters/Bloomberg: RACE.MI RACE IM

52-Week Range (EUR): 96.7 158.7

Source: FactSet

Performance

1m 3m 12m

Absolute 3.1% 6.3% 40.4%

Rel. to FTSE IT 4.6% 5.1% 25.4%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile

Ferrari builds cars unique in terms of their performance, innovations, technology, driving pleasure and design. Those cars are acknowledged the world over as the pinnacle of Made in Italy achievement. Almost half of them are sold in Europe

with another third sold in US. The company has a record-braking presence in racing being the only constructor to have taken part in every single edition of the F1 championship since its launch (with 15 drivers’ world titles and 16

constructors’ world title). It employees almost 4,000 people and sells almost 10,000 cars in more than 60 countries through a dealer network that surpassed

the 200 stores mark.

Recent development

At the end of January Ferrari has been named the most influential brand of the world (for the second consecutive year) by Brand Finance. In a December 2019 interview, CEO Mr. Camilleri stated that Ferrari won't have its first fully electric model ready until after 2025 as the battery technology

requires more development, pushing back expectations. He also hinted at strong FY2019 results but statement was too generic to have a read-across from it. Ferrari reported a solid set of results in 3Q19 showing sound YoY growth (+13%

in units and +14% revenues for cars & spare parts), nice price/mix improvement (+5.1% to EUR286K), margins expansion (70bps at EBITDA level) and above all

impressive cash flow generation, despite heavy investments (EUR40 million

increase in R&D alone). The cash generation was probably the biggest surprise in this set of results: Net Industrial Debt reached the EUR369 million mark, in line with our estimates, but with more share buyback than expected (EUR93 million delta).

Corporate Governance

Does the company have a combined Chair/CEO? No

Percentage of independent directors 66.7% (8 out of 12)

Does the company have loyalty shares? Yes

Does major shareholders have a “shareholders pact” in place? Yes

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? Yes

CEO remuneration detail (fixed salary) EUR0.27 million

Chairman remuneration detail (fixed salary) EUR0.08 million

Is the share price included in the MBO criteria? Yes

Percentage of treasury shares 3.38%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? Through Governance and Sustainability Committee

Social Responsibilities

Does the company publish a separated Sustainability report? Yes

Does the company have a Chief SRI/CSR officer (or a committee)? Yes

Does the Chief SRI/CSR officer votes in any of the committee? Yes

Is the Investor Relation officer a different person from CFO (or

other officers)? Yes

Is the ESG strategy integrated in the Business Plan (or in the group strategy)?

Yes

Does the company have an ethical code? Yes

Percentage of female directors 33.33% (4 out of 12)

How is the cybersecurity issue managed? Compliance with GDPR, it adopted a progressive approach to ensure compliance with data protection law requirements,

such as the implementation of ICT and security systems

SWOT Analysis

Strengths Weaknesses

• Unmatchable brand image, the world's most recognizable brand;

• Unique racing heritage;

• Loyal and growing customer base composed of UHNWI.

• Exposure to exchange rate fluctuations;

• Product category not ideal to benefit from growth in Chinese's HNWI;

• 100% reliance on a single plant (Maranello, Modena only for chassis);

Opportunities Threats

• Personalization increasing more than we estimate;

• Volumes increases;

• Efficiencies higher than expected also on F1;

• Trade war may impact volumes or margins and, with a single plant, is impossible to balance-out also in the long run;

• Need to maintain a proper balance between exclusivity and growth;

• Lack of wins in F1;

104,000

124,000

144,000

164,000

Ferrari FTSE Italia All-Share

Exor; 24,0%

Piero Ferrari; 10,2%

Treasury shares; 4,2%

Free float; 61,6%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

13 Servizio Studi – Equity Research

Ferrari

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 3.419,9 3.721,3 4.182,4 4.735,9 ROE 58,1% 37,9% 33,0% 30,2%

EBITDA 1.134,5 1.280,6 1.460,0 1.715,7 Net Fin. Debt / Equity (x) (0,3) (0,2) 0,0 0,2

EBITDA margin 33,2% 34,4% 34,9% 36,2% Net Fin. Debt / EBITDA (x) (0,4) (0,3) 0,0 0,4

EBIT 826,0 925,6 1.033,7 1.213,5 Capex / Sales 18,6% 18,9% 17,8% 13,7%

EBIT margin 24,2% 24,9% 24,7% 25,6% Pay Out Ratio 24,6% 28,3% 30,0% 30,0%

Profit before taxes 803,0 883,3 1.012,8 1.202,8

Taxes (16,0) (176,8) (193,1) (233,7)

Net Income 787,0 706,5 819,7 969,1

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS 4,2 3,8 4,4 5,2

Growth Rates DPS 1,0 1,1 1,3 1,5

(%) 2018A 2019E 2020E 2021E BVPS 7,18 9,93 13,23 17,08

Growth Group Net Sales 0,1% 8,8% 12,4% 13,2%

Growth EBITDA 9,5% 12,9% 14,0% 17,5%

Growth EBIT 6,6% 12,1% 11,7% 17,4%

Growth Net Profit 46,5% (10,2%) 16,0% 18,2% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E 25,3 40,5 34,9 29,6

P/OpCFPS 38,8 27,8 26,9 18,3

Balance Sheet P/BV 14,7 10,6 8,0 6,2

(EURm) 2018A 2019E 2020E 2021E Dividend Yield (%) 1,0% 0,7% 0,9% 1,0%

Capital Employed 2.487 2.993 3.190 3.258 EV/Sales

5,8 7,5 6,6 5,7

Shareholders’ Equity 1.349 1.861 2.480 3.204 EV/EBITDA 17,4 21,7 18,8 15,6

Net Financial Debt / (Cash) (1.133) (1.127) (704) (49) EV/EBIT 23,9 30,1 26,5 22,1

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

14 Servizio Studi – Equity Research

First Capital 03 February 2020 – 5:30 PM TARGET PRICE: 16.80 MARKET PRICE: 12.00

Financial Holding

Data

Shares outstanding (m): 2.55

Market Cap. (EURm): 30.6

NAV (EURm): 46.5

Av. Daily Trad. Vol. (‘000): 1,2

Reuters/Bloomberg: FICM.MI FICM.IM

52-Week Range (EUR): 9.9 12.5

Source: FactSet

Performance

1m 3m 12m

Absolute -0.8% 0.8% 21.0%

Rel. to FTSE IT 0.5% -1.7% 4.4%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile First Capital S.p.A. is an investment holding company specialised in Public Equity and Private Equity Investments, focused on small-mid cap, with active approach

in managing investee companies. It was founded in February 2008 and has been listed on the AIM Italia since December 2010. Since the IPO, NAV/share total return has been 93% (as at the end of September 2019) while share total return

has been 50%. The main strategic investments are currently Tinexta and Intred; the other strategic investments are Orsero, ICF, Eukedos, Triboo and TPS. SPACs exposure amounts to around 10% of portfolio.

Recent development

1H19 results were outstanding: EUR13.7 million net profit and EUR47.1 million NAV (+38% YTD, EUR13 million in absolute term after EUR1.6 million dividend distribution). Net cash was EUR2.1 million at the end of June-19. In 1H19 the Group realized EUR7.2 million capital gains by adhering to the tender offer on

Bomi Italia (EUR1.5 million gain, >18% IRR) and by selling ca 1.6% stake in Tinexta (EUR5.4 million gain, >50% IRR) and LU-VE (EUR0.4 million gain, >45% IRR). In the meantime, Value First SICAF invested EUR3.9 million in ICF to acquire an

8.7% stake and increased the stake in Intred by 0.4% to 9.8%. In July, First Capital

announced its strategic decision to enter into private equity investments by promoting a club deal through First Private Investment; on 30 September it joined Space Capital Club with an initial soft commitment of EUR15 million.

Corporate Governance

Does the company have a combined Chair/CEO? No

Percentage of independent directors 44% (4 out of 9)

Does the company have loyalty shares? No

Does major shareholders have a “shareholders pact” in place? No

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? No

CEO remuneration detail (fixed salary) EUR0.155 million

Chairman remuneration detail (fixed salary) EUR0.04 million

Is the share price included in the MBO criteria? No

Percentage of treasury shares 2.84%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? No

Social Responsibilities

Does the company publish a separated Sustainability report? No

Does the company have a Chief SRI/CSR officer (or a committee)? No

Does the Chief SRI/CSR officer votes in any of the committee? No

Is the Investor Relation officer a different person from CFO (or other officers)?

Yes

Is the ESG strategy integrated in the Business Plan (or in the group

strategy)? No

Does the company have an ethical code? Yes

Percentage of female directors 11% (1 out of 9)

How is the cybersecurity issue managed? Not disclosed

SWOT Analysis

Strengths Weaknesses

• Leading position in AIM/small caps fund management segment

• Strong track record of investment management team

• Quality of the strategic portfolio

• Full exposure to the Italian stock market

• Stock performance is highly correlated to stock market performance

• Systematic liquidity risk in small cap investments

Opportunities Threats

• Business diversification into private equity investments

• Business diversification into SICAV management

• P.I.R. 2.0 potential effect on stock market

• Increasing compliance requirements

• Increasing competition

• Potential lack of investment opportunities

9,50010,50011,50012,50013,500

First Capital FTSE Italia All-Share

Strategy Invest; 28,1%

Next Holding; 29,0%

CHUI; 9,1%

Treasury; 2,6%

Free Float; 31,2%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

15 Servizio Studi – Equity Research

First Capital

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Dividends 0,38 0,65 0,67 0,69 Debt/Equity 0,16 -0,16 -0,18 -0,20

Other financial income 0,07 0,07 0,07 0,07 Cost/Income nm 19,2% 51,3% 52,0%

Trading profit/(loss) -1,02 15,35 2,37 2,37 ROI -5,8% 32,5% 3,4% 3,4%

Total income -0,57 16,07 3,11 3,13 ROE -6,0% 27,1% 2,4% 2,4%

D&A -0,02 -0,10 -0,10 -0,10 Pay Out Ratio 90,0% 5,4% 60,9% 63,4%

Operating (cost)/income -1,46 -3,08 -1,60 -1,63

Financial charges -0,25 -0,28 -0,12 -0,12

Pre-tax profit -2,29 12,61 1,29 1,28

Taxes 0,24 -0,16 -0,16 -0,16 Per Share Data

Net profit -2,05 12,45 1,13 1,12 (EUR) 2018A 2019E 2020E 2021E

EPS -0,80 4,87 0,44 0,44

DPS 0,25 0,26 0,27 0,28

BVPS 13,35 17,98 18,16 18,34

Balance Sheet Stock Market Ratios

(EURm) 2018A 2019E 2020E 2021E (x) 2018A 2019E 2020E 2021E

Capital Employed 39,44 38,75 38,05 37,36 P/E -12,0 2,3 27,1 27,4

Shareholders’ Equity 34,09 45,92 46,40 46,85 P/BV 0,7 0,6 0,7 0,7

Net Financial Debt / (Cash) 5,35 -7,18 -8,35 -9,50 Div Yield 2,6% 2,3% 2,2% 2,3%

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

16 Servizio Studi – Equity Research

Gefran 03 February 2020 – 5:30 PM TARGET PRICE: 8.98 MARKET PRICE: 6.40

Electrical equipment

Data

Shares outstanding (m): 14.4

Market Cap. (EURm): 91.4

Enterprise Value (EURm): 108.4

Av. Daily Trad. Vol. (000): 34.8

Reuters/Bloomberg: GFRN.MI GE IM

52-Week Range (EUR): 5.8 8.3

Source: FactSet

Performance

1m 3m 12m

Absolute -6.9% -7.8% -18.1%

Rel. to FTSE IT -5.7% -10.1% -29.7%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile Gefran is a leading industrial company specialized in three divisions: 1) Sensors

for industrial applications (44% of sales in 2018), typically for large industrial machine makers supplying the plastic industry, packaging industry, automotive, and white goods companies; 2) Systems and components for automation (27% of

sales) including the production of complete electric panels for the plastic industry, and 3) Motion Controls division (29% of sales) which produces a complete range of electric drives to regulate the speed of AC and DC motors and is specialised in inverters for industrial applications and for domestic lifts

which are progressively replacing hydraulic and mechanical devices. The company

has 10 production sites, nearly 800 employees and 70% of sales outside Italy (mainly EU, China and the US). Gefran is vertically integrated, from R&D (2 R&D

centers, with investments approaching 5% of revenues p.a.) to the commercialization of its products (100,000 references) and has a leading position for plastic processing applications. Gefran, 60% controlled by the founder’s

family, which still manages the company, was listed in 1998 and entered the STAR segment in 2001. Recently the CEO resigned and should be replaced by the end of April 2020.

Recent development The first nine months of 2019 were challenging for Gefran, which was impacted by the slowdown of the high-margin Sensors division while the order intake declined. From a geographical standpoint, all regions went down in 9M19 (Asia

by 2.7%, EU by 3.4% and other European countries by 33%) with the sole

exception of Americas (North America was up by 34% and Latam by 10.5%). Lastly, Italy positive performance (+10.1%) can be entirely ascribed to the change in scope of consolidation (consolidation of Elettropiemme). The EBITDA margin

declined to 14.3% from 15.3% in 9M18 also due to higher personnel costs while the net debt rose to EUR14.9 million (>EUR10 million more than Dec-18) mainly because of the lower cash flow, substantial investments, the dividend distribution

and the application of IFRS16. Against this backdrop, the management confirmed its guidance for higher revenues and EBITDA margin in line with 2018, implying a recovery in the last quarter of the year.

Corporate Governance

Does the company have a combined Chair/CEO? Yes

Percentage of independent directors 33.3% (3 out of 9)

Does the company have loyalty shares? No

Does major shareholders have a “shareholders pact” in place? No

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? No

CEO remuneration detail (fixed salary) EUR0.36 million

Chairman remuneration detail (fixed salary) EUR0.31 million

Is the share price included in the MBO criteria? No

Percentage of treasury shares 0.19%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? The company underwent an "Energetic Audit" in order to assess the efficiency of the use of energetic resources and it committed to solve the critical issues emerged

Social Responsibilities

Does the company publish a separated Sustainability report? Yes

Does the company have a Chief SRI/CSR officer (or a committee)? Yes

Does the Chief SRI/CSR officer votes in any of the committee? Yes

Is the Investor Relation officer a different person from CFO (or

other officers)? No

Is the ESG strategy integrated in the Business Plan (or in the group strategy)?

Yes

Does the company have an ethical code? Yes

Percentage of female directors 33.3% (3 out of 9)

How is the cybersecurity issue managed? Not disclosed

SWOT Analysis

Strengths Weaknesses

• Low exposure to the Italian market (70% revenues outside Italy)

• Strong and consistent product innovation, with R&D at >5% of revenues

• Solid financial structure and attractive dividend yield

• Limited size compared to international peers

• Part of the products are now commodities, competing just on selling prices

• Persistent losses for the Motion Control division

Opportunities Threats

• Growing reference market, in particular sensors

• Potential acquisitions in new segments and/or markets

• Arrival of the new CEO

• Weaker Chinese market

• Currency fluctuations

• High competition and low entry barriers in some segments

5,000

6,000

7,000

8,000

9,000

10,000

Gefran FTSE Italia All-Share

Fingefran; 56,7%

Franceschetti Ennio; 3,5%Lazard;

2,6%

Free float; 37,2%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

17 Servizio Studi – Equity Research

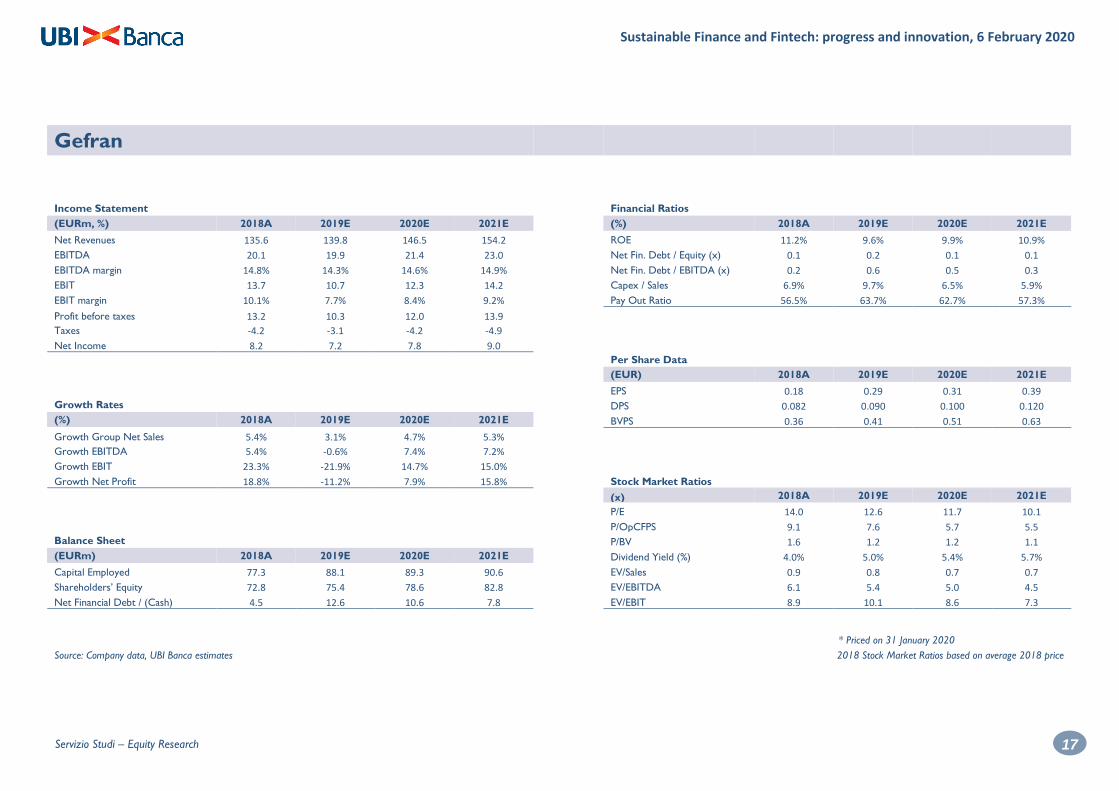

Gefran

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 135.6 139.8 146.5 154.2 ROE 11.2% 9.6% 9.9% 10.9%

EBITDA 20.1 19.9 21.4 23.0 Net Fin. Debt / Equity (x) 0.1 0.2 0.1 0.1

EBITDA margin 14.8% 14.3% 14.6% 14.9% Net Fin. Debt / EBITDA (x) 0.2 0.6 0.5 0.3

EBIT 13.7 10.7 12.3 14.2 Capex / Sales 6.9% 9.7% 6.5% 5.9%

EBIT margin 10.1% 7.7% 8.4% 9.2% Pay Out Ratio 56.5% 63.7% 62.7% 57.3%

Profit before taxes 13.2 10.3 12.0 13.9

Taxes -4.2 -3.1 -4.2 -4.9

Net Income 8.2 7.2 7.8 9.0

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS 0.18 0.29 0.31 0.39

Growth Rates DPS 0.082 0.090 0.100 0.120

(%) 2018A 2019E 2020E 2021E BVPS 0.36 0.41 0.51 0.63

Growth Group Net Sales 5.4% 3.1% 4.7% 5.3%

Growth EBITDA 5.4% -0.6% 7.4% 7.2%

Growth EBIT 23.3% -21.9% 14.7% 15.0%

Growth Net Profit 18.8% -11.2% 7.9% 15.8% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E 14.0 12.6 11.7 10.1

P/OpCFPS 9.1 7.6 5.7 5.5

Balance Sheet P/BV 1.6 1.2 1.2 1.1

(EURm) 2018A 2019E 2020E 2021E Dividend Yield (%) 4.0% 5.0% 5.4% 5.7%

Capital Employed 77.3 88.1 89.3 90.6 EV/Sales

0.9 0.8 0.7 0.7

Shareholders’ Equity 72.8 75.4 78.6 82.8 EV/EBITDA 6.1 5.4 5.0 4.5

Net Financial Debt / (Cash) 4.5 12.6 10.6 7.8 EV/EBIT 8.9 10.1 8.6 7.3

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

18 Servizio Studi – Equity Research

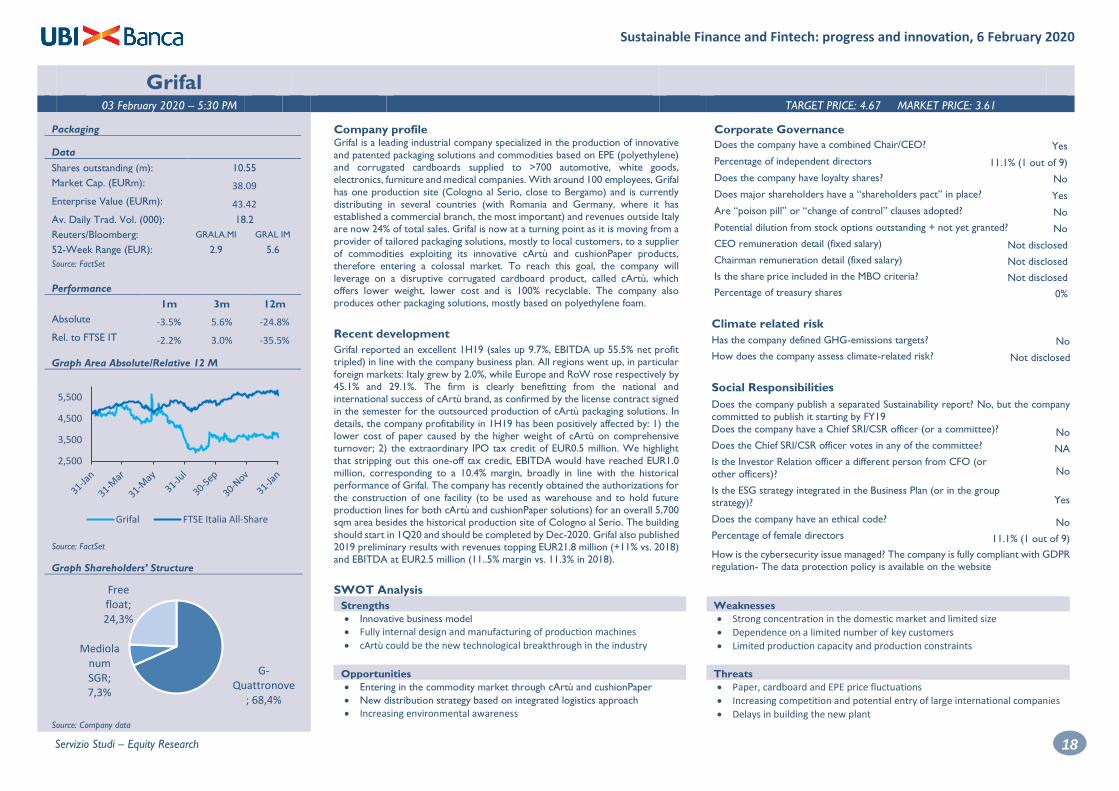

Grifal 03 February 2020 – 5:30 PM TARGET PRICE: 4.67 MARKET PRICE: 3.61

Packaging

Data

Shares outstanding (m): 10.55

Market Cap. (EURm): 38.09

Enterprise Value (EURm): 43.42

Av. Daily Trad. Vol. (000): 18.2

Reuters/Bloomberg: GRALA.MI GRAL IM

52-Week Range (EUR): 2.9 5.6

Source: FactSet

Performance

1m 3m 12m

Absolute -3.5% 5.6% -24.8%

Rel. to FTSE IT -2.2% 3.0% -35.5%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile Grifal is a leading industrial company specialized in the production of innovative

and patented packaging solutions and commodities based on EPE (polyethylene) and corrugated cardboards supplied to >700 automotive, white goods, electronics, furniture and medical companies. With around 100 employees, Grifal

has one production site (Cologno al Serio, close to Bergamo) and is currently distributing in several countries (with Romania and Germany, where it has established a commercial branch, the most important) and revenues outside Italy are now 24% of total sales. Grifal is now at a turning point as it is moving from a

provider of tailored packaging solutions, mostly to local customers, to a supplier

of commodities exploiting its innovative cArtù and cushionPaper products, therefore entering a colossal market. To reach this goal, the company will

leverage on a disruptive corrugated cardboard product, called cArtù, which offers lower weight, lower cost and is 100% recyclable. The company also produces other packaging solutions, mostly based on polyethylene foam.

Recent development

Grifal reported an excellent 1H19 (sales up 9.7%, EBITDA up 55.5% net profit tripled) in line with the company business plan. All regions went up, in particular

foreign markets: Italy grew by 2.0%, while Europe and RoW rose respectively by 45.1% and 29.1%. The firm is clearly benefitting from the national and international success of cArtù brand, as confirmed by the license contract signed in the semester for the outsourced production of cArtù packaging solutions. In

details, the company profitability in 1H19 has been positively affected by: 1) the lower cost of paper caused by the higher weight of cArtù on comprehensive turnover; 2) the extraordinary IPO tax credit of EUR0.5 million. We highlight

that stripping out this one-off tax credit, EBITDA would have reached EUR1.0 million, corresponding to a 10.4% margin, broadly in line with the historical performance of Grifal. The company has recently obtained the authorizations for

the construction of one facility (to be used as warehouse and to hold future production lines for both cArtù and cushionPaper solutions) for an overall 5,700 sqm area besides the historical production site of Cologno al Serio. The building

should start in 1Q20 and should be completed by Dec-2020. Grifal also published 2019 preliminary results with revenues topping EUR21.8 million (+11% vs. 2018) and EBITDA at EUR2.5 million (11..5% margin vs. 11.3% in 2018).

Corporate Governance

Does the company have a combined Chair/CEO? Yes

Percentage of independent directors 11.1% (1 out of 9)

Does the company have loyalty shares? No

Does major shareholders have a “shareholders pact” in place? Yes

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? No

CEO remuneration detail (fixed salary) Not disclosed

Chairman remuneration detail (fixed salary) Not disclosed

Is the share price included in the MBO criteria? Not disclosed

Percentage of treasury shares 0%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? Not disclosed

Social Responsibilities

Does the company publish a separated Sustainability report? No, but the company

committed to publish it starting by FY19

Does the company have a Chief SRI/CSR officer (or a committee)? No

Does the Chief SRI/CSR officer votes in any of the committee? NA

Is the Investor Relation officer a different person from CFO (or

other officers)? No

Is the ESG strategy integrated in the Business Plan (or in the group strategy)?

Yes

Does the company have an ethical code? No

Percentage of female directors 11.1% (1 out of 9)

How is the cybersecurity issue managed? The company is fully compliant with GDPR regulation- The data protection policy is available on the website

SWOT Analysis

Strengths Weaknesses

• Innovative business model

• Fully internal design and manufacturing of production machines

• cArtù could be the new technological breakthrough in the industry

• Strong concentration in the domestic market and limited size

• Dependence on a limited number of key customers

• Limited production capacity and production constraints

Opportunities Threats

• Entering in the commodity market through cArtù and cushionPaper

• New distribution strategy based on integrated logistics approach

• Increasing environmental awareness

• Paper, cardboard and EPE price fluctuations

• Increasing competition and potential entry of large international companies

• Delays in building the new plant

2,500

3,500

4,500

5,500

Grifal FTSE Italia All-Share

G-Quattronove

; 68,4%

Mediolanum SGR; 7,3%

Free float; 24,3%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

19 Servizio Studi – Equity Research

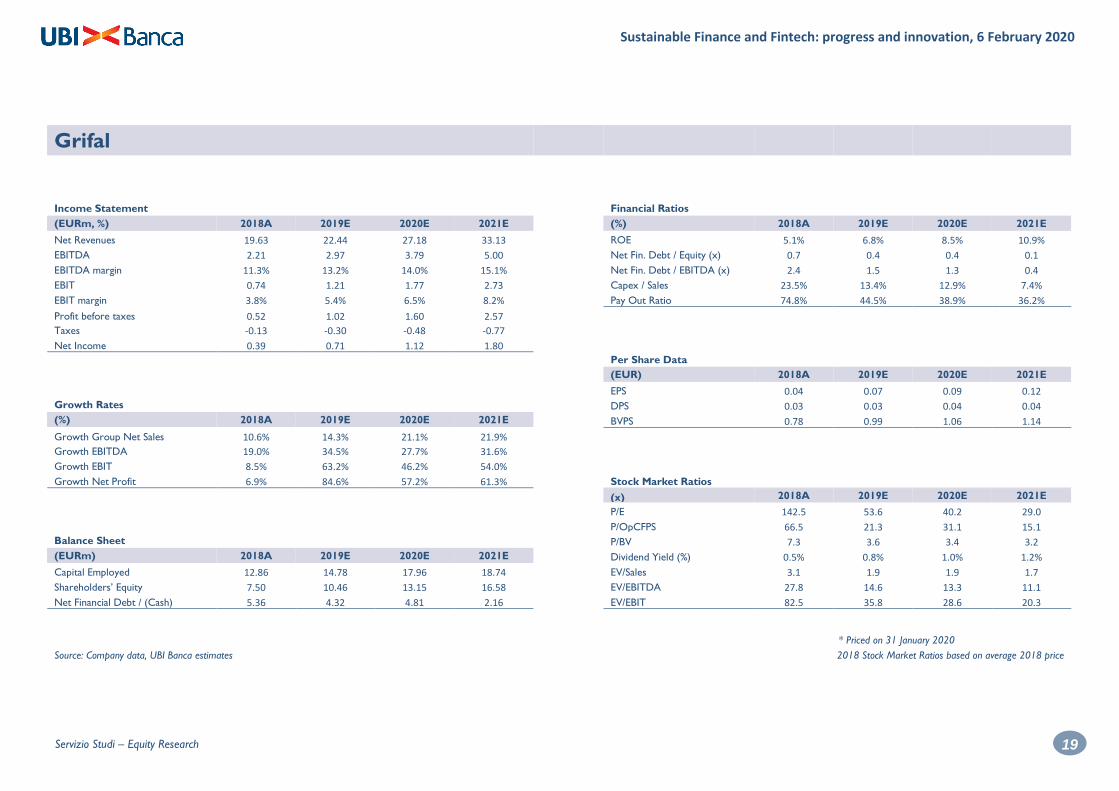

Grifal

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 19.63 22.44 27.18 33.13 ROE 5.1% 6.8% 8.5% 10.9%

EBITDA 2.21 2.97 3.79 5.00 Net Fin. Debt / Equity (x) 0.7 0.4 0.4 0.1

EBITDA margin 11.3% 13.2% 14.0% 15.1% Net Fin. Debt / EBITDA (x) 2.4 1.5 1.3 0.4

EBIT 0.74 1.21 1.77 2.73 Capex / Sales 23.5% 13.4% 12.9% 7.4%

EBIT margin 3.8% 5.4% 6.5% 8.2% Pay Out Ratio 74.8% 44.5% 38.9% 36.2%

Profit before taxes 0.52 1.02 1.60 2.57

Taxes -0.13 -0.30 -0.48 -0.77

Net Income 0.39 0.71 1.12 1.80

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS 0.04 0.07 0.09 0.12

Growth Rates DPS 0.03 0.03 0.04 0.04

(%) 2018A 2019E 2020E 2021E BVPS 0.78 0.99 1.06 1.14

Growth Group Net Sales 10.6% 14.3% 21.1% 21.9%

Growth EBITDA 19.0% 34.5% 27.7% 31.6%

Growth EBIT 8.5% 63.2% 46.2% 54.0%

Growth Net Profit 6.9% 84.6% 57.2% 61.3% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E 142.5 53.6 40.2 29.0

P/OpCFPS 66.5 21.3 31.1 15.1

Balance Sheet P/BV 7.3 3.6 3.4 3.2

(EURm) 2018A 2019E 2020E 2021E Dividend Yield (%) 0.5% 0.8% 1.0% 1.2%

Capital Employed 12.86 14.78 17.96 18.74 EV/Sales

3.1 1.9 1.9 1.7

Shareholders’ Equity 7.50 10.46 13.15 16.58 EV/EBITDA 27.8 14.6 13.3 11.1

Net Financial Debt / (Cash) 5.36 4.32 4.81 2.16 EV/EBIT 82.5 35.8 28.6 20.3

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

20 Servizio Studi – Equity Research

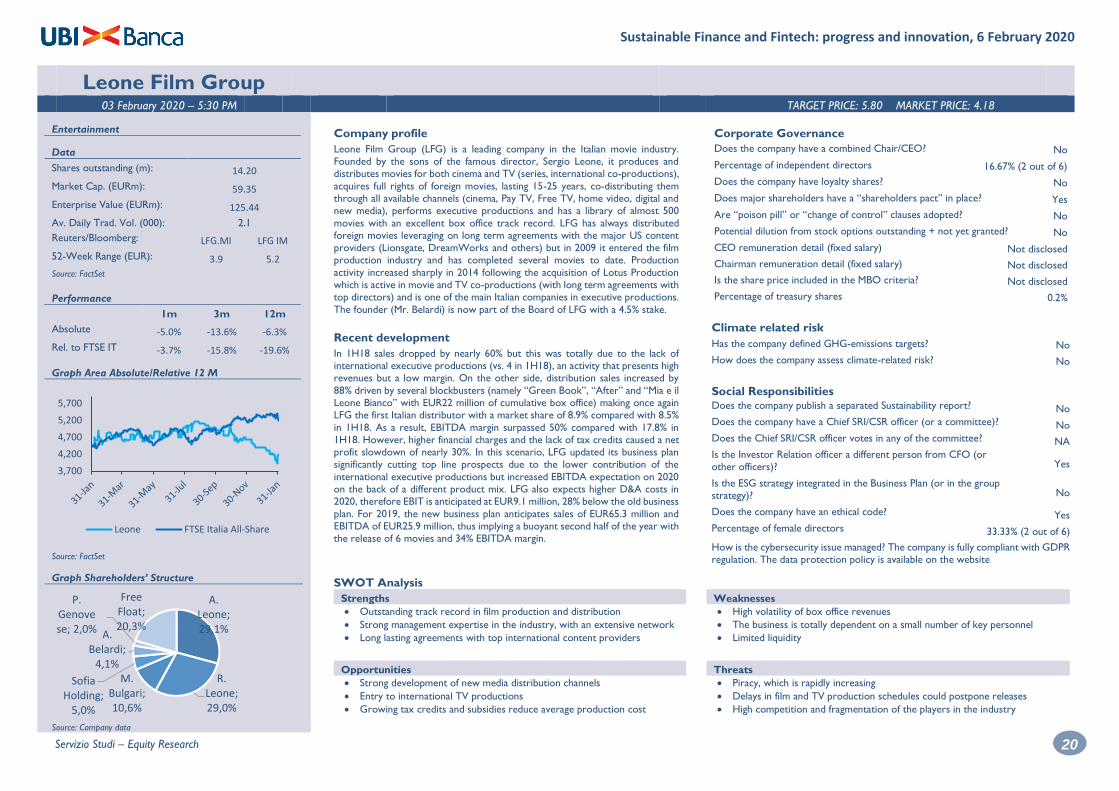

Leone Film Group 03 February 2020 – 5:30 PM TARGET PRICE: 5.80 MARKET PRICE: 4.18

Entertainment

Data

Shares outstanding (m): 14.20

Market Cap. (EURm): 59.35

Enterprise Value (EURm): 125.44

Av. Daily Trad. Vol. (000): 2.1

Reuters/Bloomberg: LFG.MI LFG IM

52-Week Range (EUR): 3.9 5.2

Source: FactSet

Performance

1m 3m 12m

Absolute -5.0% -13.6% -6.3%

Rel. to FTSE IT -3.7% -15.8% -19.6%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile

Leone Film Group (LFG) is a leading company in the Italian movie industry. Founded by the sons of the famous director, Sergio Leone, it produces and distributes movies for both cinema and TV (series, international co-productions),

acquires full rights of foreign movies, lasting 15-25 years, co-distributing them through all available channels (cinema, Pay TV, Free TV, home video, digital and new media), performs executive productions and has a library of almost 500

movies with an excellent box office track record. LFG has always distributed foreign movies leveraging on long term agreements with the major US content

providers (Lionsgate, DreamWorks and others) but in 2009 it entered the film production industry and has completed several movies to date. Production

activity increased sharply in 2014 following the acquisition of Lotus Production which is active in movie and TV co-productions (with long term agreements with top directors) and is one of the main Italian companies in executive productions.

The founder (Mr. Belardi) is now part of the Board of LFG with a 4.5% stake.

Recent development

In 1H18 sales dropped by nearly 60% but this was totally due to the lack of international executive productions (vs. 4 in 1H18), an activity that presents high revenues but a low margin. On the other side, distribution sales increased by

88% driven by several blockbusters (namely “Green Book”, “After” and “Mia e il Leone Bianco” with EUR22 million of cumulative box office) making once again

LFG the first Italian distributor with a market share of 8.9% compared with 8.5%

in 1H18. As a result, EBITDA margin surpassed 50% compared with 17.8% in 1H18. However, higher financial charges and the lack of tax credits caused a net profit slowdown of nearly 30%. In this scenario, LFG updated its business plan significantly cutting top line prospects due to the lower contribution of the

international executive productions but increased EBITDA expectation on 2020 on the back of a different product mix. LFG also expects higher D&A costs in 2020, therefore EBIT is anticipated at EUR9.1 million, 28% below the old business

plan. For 2019, the new business plan anticipates sales of EUR65.3 million and EBITDA of EUR25.9 million, thus implying a buoyant second half of the year with the release of 6 movies and 34% EBITDA margin.

Corporate Governance

Does the company have a combined Chair/CEO? No

Percentage of independent directors 16.67% (2 out of 6)

Does the company have loyalty shares? No

Does major shareholders have a “shareholders pact” in place? Yes

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? No

CEO remuneration detail (fixed salary) Not disclosed

Chairman remuneration detail (fixed salary) Not disclosed

Is the share price included in the MBO criteria? Not disclosed

Percentage of treasury shares 0.2%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? No

Social Responsibilities

Does the company publish a separated Sustainability report? No

Does the company have a Chief SRI/CSR officer (or a committee)? No

Does the Chief SRI/CSR officer votes in any of the committee? NA

Is the Investor Relation officer a different person from CFO (or other officers)?

Yes

Is the ESG strategy integrated in the Business Plan (or in the group strategy)?

No

Does the company have an ethical code? Yes

Percentage of female directors 33.33% (2 out of 6)

How is the cybersecurity issue managed? The company is fully compliant with GDPR regulation. The data protection policy is available on the website

SWOT Analysis

Strengths Weaknesses

• Outstanding track record in film production and distribution

• Strong management expertise in the industry, with an extensive network

• Long lasting agreements with top international content providers

• High volatility of box office revenues

• The business is totally dependent on a small number of key personnel

• Limited liquidity

Opportunities Threats

• Strong development of new media distribution channels

• Entry to international TV productions

• Growing tax credits and subsidies reduce average production cost

• Piracy, which is rapidly increasing

• Delays in film and TV production schedules could postpone releases

• High competition and fragmentation of the players in the industry

3,700

4,200

4,700

5,200

5,700

Leone FTSE Italia All-Share

A. Leone; 29,1%

R. Leone; 29,0%

M. Bulgari; 10,6%

Sofia Holding;

5,0%

A. Belardi;

4,1%

P. Genovese; 2,0%

Free Float; 20,3%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

21 Servizio Studi – Equity Research

Leone Film Group

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 128.14 68.51 87.35 105.22 ROE 15.6% 10.0% 13.8% 14.0%

EBITDA 30.47 25.53 39.20 47.11 Net Fin. Debt / Equity (x) 1.1 1.2 1.2 1.1

EBITDA margin 23.8% 37.3% 44.9% 44.8% Net Fin. Debt / EBITDA (x) 1.6 2.3 1.7 1.5

EBIT 6.65 6.08 9.55 10.66 Capex / Sales 18.1% 39.4% 43.3% 38.1%

EBIT margin 5.2% 8.9% 10.9% 10.1% Pay Out Ratio 18.8% 27.1% 17.5% 15.2%

Profit before taxes 6.54 4.62 7.16 8.23

Taxes 0.25 0.09 0.14 0.16

Net Income 6.79 4.71 7.31 8.39

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS 0.48 0.33 0.51 0.59

Growth Rates DPS 0.09 0.09 0.09 0.09

(%) 2018A 2019E 2020E 2021E BVPS 3.07 3.31 3.73 4.24

Growth Group Net Sales 9.3% -46.5% 27.5% 20.5%

Growth EBITDA 3.6% -16.2% 53.5% 20.2%

Growth EBIT 22.7% -8.6% 57.1% 11.6%

Growth Net Profit 73.9% -30.6% 55.2% 14.8% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E 10.0 12.6 8.1 7.1

P/OpCFPS 4.2 2.8 1.8 1.5

Balance Sheet P/BV 1.6 1.3 1.1 1.0

(EURm) 2018A 2019E 2020E 2021E Dividend Yield (%) 1.9% 2.2% 2.2% 2.2%

Capital Employed 93.01 105.14 118.54 128.94 EV/Sales

0.9 1.7 1.4 1.2

Shareholders’ Equity 43.57 47.00 53.03 60.14 EV/EBITDA 3.9 4.6 3.2 2.7

Net Financial Debt / (Cash) 49.42 58.14 65.51 68.80 EV/EBIT 17.7 19.4 13.1 12.1

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

22 Servizio Studi – Equity Research

LU-VE 03 February 2020 – 5:30 PM TARGET PRICE: 17.82 MARKET PRICE: 13.65

Heat exchangers, refrigeration

Data

Shares outstanding (m): 22.2

Market Cap. (EURm): 303.5

Enterprise Value (EURm): 462.6

Av. Daily Trad. Vol. (000): 28.1

Reuters/Bloomberg: LUVE.MI LUVE IM

52-Week Range (EUR): 10.0 14.6

Source: FactSet

Performance

1m 3m 12m

Absolute 6.6% 32.5% 36.5%

Rel. to FTSE IT 8.1% 29.3% 17.0%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile LU-VE is a leading producer of heat exchangers and ventilated products for non-

residential applications with revenues of EUR307 million in 2018, 16 plants (of which 7 outside Italy), 12 commercial branches abroad, and a total of 2,655 employees at Dec-18. It is also present in the niche segments of close control

and glass doors. The group, founded and still managed by Liberali family, has reported average top line growth of about 10% in the past five years and strongly expanded abroad in the past few years thanks to the acquisition of Spirotech in India, Zyklus in the US and Al Air, a true game changing-acquisition finalized in

2019 which added >EUR100 million sales. Because of its lean cost structure,

healthy operating leverage and the quality recognized by its customers, the company has maintained EBITDA margins close to 12% in the past five years. LU-

VE was listed on the AIM market following the business combination with the SPAC Industrial Star for Italy 1 in Jul-15 and moved to the MTA market segment in 2018.

Recent development

LU-VE reported a remarkable product sales growth in 2019: sales were up 29% (+38% in 4Q19), broadly in line with our forecasts. Organic growth was also

positive with an increase of 6.7% in the entire 2019 and of around 5% in 4Q19 despite the macro economic slowdown in Europe. Based on our estimates, Al Air should have reported around EUR60 million in the past eight months (this acquisition, for total consideration was EUR67.1 million corresponding to 6.5x

2018 EBITDA including an earn-out based on 2019 EBITDA, was consolidated from May 2019), implying around EUR100 million revenues in the full year, in line with LU-VE expectations. Order backlog at Dec-19 increased by 78.2% and by

13.6% organically, thus providing a positive kickoff for 2020. 1H19 was strong: EBITDA adjusted grew by >40% with 180 bps improvement in margin and all the companies acquired performed well (Spirotech was up 25%, Zyklus sales were

up 39% with EBITDA margin >15%, Al Air added EUR13.6 million of revenues in two months). In addition, all the projects underway (new plant in Poland, plant relocation in China, plant expansion in India, new plant in the US) are in line or

ahead of schedule and this should pave the way for further margins improvement in future.

Corporate Governance

Does the company have a combined Chair/CEO? No

Percentage of independent directors 15.4% (2 out of 13)

Does the company have loyalty shares? Yes

Does major shareholders have a “shareholders pact” in place? Yes

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? Yes

CEO remuneration detail (fixed salary) EUR0.36 million

Chairman remuneration detail (fixed salary) EUR0.25 million

Is the share price included in the MBO criteria? No

Percentage of treasury shares 0.62%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? LU-VE minimizes the environmental impact of its production processes, implementing policies of energy efficiency, reduction of emissions, water consumption and of waste generation.

Social Responsibilities

Does the company publish a separated Sustainability report? Yes

Does the company have a Chief SRI/CSR officer (or a committee)? Not disclosed

Does the Chief SRI/CSR officer votes in any of the committee? Not disclosed

Is the Investor Relation officer a different person from CFO (or

other officers)? Yes

Is the ESG strategy integrated in the Business Plan (or in the group strategy)?

Yes

Does the company have an ethical code? Yes

Percentage of female directors 23.1% (3 out of 13)

How is the cybersecurity issue managed? Not disclosed

SWOT Analysis

Strengths Weaknesses

• Innovative products and low exposure to the Italian market

• High entry barriers

• Outstanding acquisition track record

• Net debt, after the acquisition of Ail Air, needs to be reduced

• High weight of goodwill (23% of the capital employed at Dec-18)

• Limited liquidity and free float

Opportunities Threats

• Synergies and cross selling opportunities from Al Air

• New plant in Poland should increase EBITDA margin

• Expansion in the US market thanks to Zyklus

• Raw material fluctuations (mostly copper and aluminum)

• Currency fluctuations (in particular RUB and USD)

• Integration costs of Al Air

9,00010,00011,00012,00013,00014,00015,000

LUVE FTSE Italia All-Share

Liberali family50,3%

Faggioli family17,6%

Free Float

32,2%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

23 Servizio Studi – Equity Research

LU-VE

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 306.9 399.6 472.1 491.1 ROE 10.8% 11.8% 14.7% 13.8%

EBITDA 36.6 47.8 58.9 62.9 Net Fin. Debt / Equity (x) 0.4 0.9 0.8 0.6

EBITDA margin 11.9% 12.0% 12.5% 12.8% Net Fin. Debt / EBITDA (x) 1.7 3.1 2.4 2.0

EBIT 19.7 27.0 37.1 39.9 Capex / Sales 9.0% 6.3% 3.2% 3.1%

EBIT margin 6.4% 6.8% 7.9% 8.1% Pay Out Ratio 36.1% 34.0% 26.1% 28.9%

Profit before taxes 17.4 23.8 34.3 37.1

Taxes -1.3 -4.8 -7.9 -9.3

Net Income 15.4 18.3 25.6 26.9

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS 0.69 0.82 1.15 1.21

Growth Rates DPS 0.25 0.28 0.30 0.35

(%) 2018A 2019E 2020E 2021E BVPS 6.40 6.97 7.84 8.75

Growth Group Net Sales 13.6% 30.2% 18.2% 4.0%

Growth EBITDA 25.9% 30.7% 23.2% 6.7%

Growth EBIT 39.7% 37.1% 37.1% 7.7%

Growth Net Profit 173.1% 18.9% 39.6% 5.3% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E 14.6 16.6 11.9 11.3

P/OpCFPS 10.7 11.8 7.2 6.3

Balance Sheet P/BV 1.6 2.0 1.7 1.6

(EURm) 2018A 2019E 2020E 2021E Dividend Yield (%) 2.5% 2.0% 2.2% 2.6%

Capital Employed 208.9 304.9 317.1 324.4 EV/Sales

8.1 9.7 7.7 7.0

Shareholders’ Equity 142.2 155.0 174.3 194.6 EV/EBITDA 15.1 17.1 12.3 11.0

Net Financial Debt / (Cash) 63.6 146.3 138.9 125.4 EV/EBIT 1.4 1.5 1.4 1.4

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

24 Servizio Studi – Equity Research

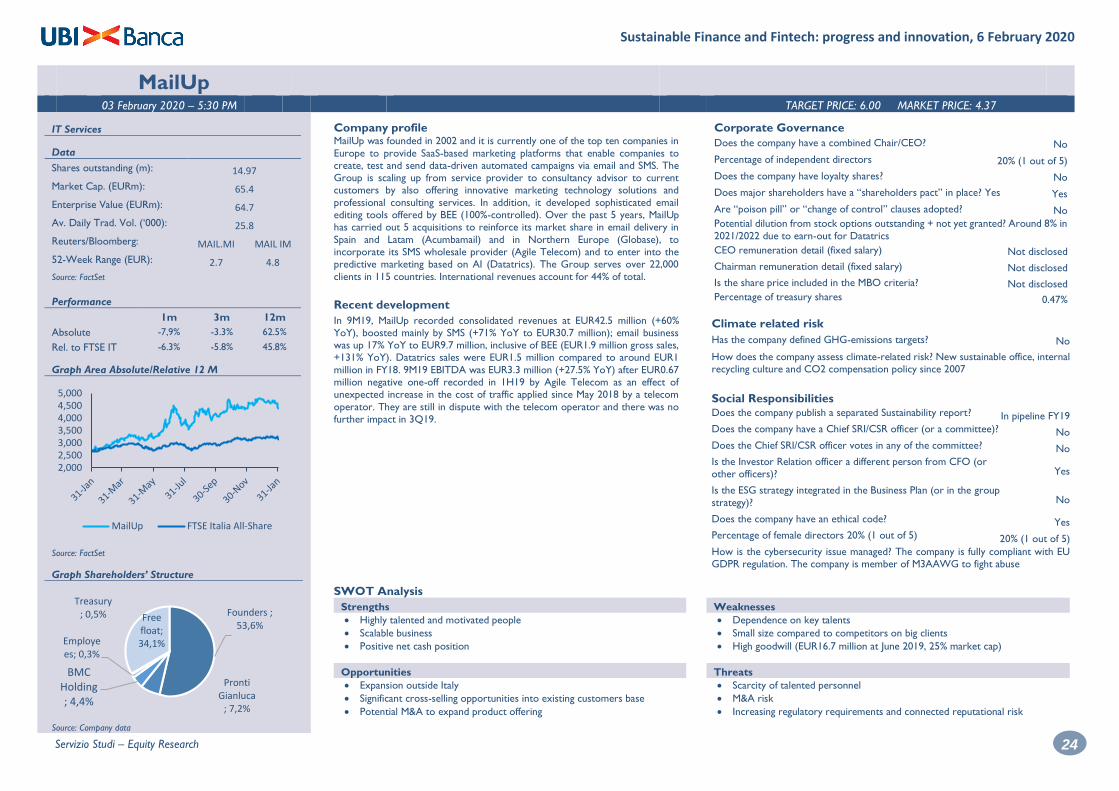

MailUp 03 February 2020 – 5:30 PM TARGET PRICE: 6.00 MARKET PRICE: 4.37

IT Services

Data

Shares outstanding (m): 14.97

Market Cap. (EURm): 65.4

Enterprise Value (EURm): 64.7

Av. Daily Trad. Vol. (‘000): 25.8

Reuters/Bloomberg: MAIL.MI MAIL IM

52-Week Range (EUR): 2.7 4.8

Source: FactSet

Performance

1m 3m 12m

Absolute -7,9% -3.3% 62.5%

Rel. to FTSE IT -6.3% -5.8% 45.8%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile MailUp was founded in 2002 and it is currently one of the top ten companies in

Europe to provide SaaS-based marketing platforms that enable companies to create, test and send data-driven automated campaigns via email and SMS. The Group is scaling up from service provider to consultancy advisor to current customers by also offering innovative marketing technology solutions and

professional consulting services. In addition, it developed sophisticated email editing tools offered by BEE (100%-controlled). Over the past 5 years, MailUp has carried out 5 acquisitions to reinforce its market share in email delivery in

Spain and Latam (Acumbamail) and in Northern Europe (Globase), to

incorporate its SMS wholesale provider (Agile Telecom) and to enter into the predictive marketing based on AI (Datatrics). The Group serves over 22,000

clients in 115 countries. International revenues account for 44% of total.

Recent development

In 9M19, MailUp recorded consolidated revenues at EUR42.5 million (+60% YoY), boosted mainly by SMS (+71% YoY to EUR30.7 million); email business was up 17% YoY to EUR9.7 million, inclusive of BEE (EUR1.9 million gross sales, +131% YoY). Datatrics sales were EUR1.5 million compared to around EUR1

million in FY18. 9M19 EBITDA was EUR3.3 million (+27.5% YoY) after EUR0.67 million negative one-off recorded in 1H19 by Agile Telecom as an effect of unexpected increase in the cost of traffic applied since May 2018 by a telecom

operator. They are still in dispute with the telecom operator and there was no

further impact in 3Q19.

Corporate Governance

Does the company have a combined Chair/CEO? No

Percentage of independent directors 20% (1 out of 5)

Does the company have loyalty shares? No

Does major shareholders have a “shareholders pact” in place? Yes Yes

Are “poison pill” or “change of control” clauses adopted? No

Potential dilution from stock options outstanding + not yet granted? Around 8% in

2021/2022 due to earn-out for Datatrics

CEO remuneration detail (fixed salary) Not disclosed

Chairman remuneration detail (fixed salary) Not disclosed

Is the share price included in the MBO criteria? Not disclosed

Percentage of treasury shares

0.47%

Climate related risk

Has the company defined GHG-emissions targets? No

How does the company assess climate-related risk? New sustainable office, internal recycling culture and CO2 compensation policy since 2007

Social Responsibilities

Does the company publish a separated Sustainability report? In pipeline FY19

Does the company have a Chief SRI/CSR officer (or a committee)? No

Does the Chief SRI/CSR officer votes in any of the committee? No

Is the Investor Relation officer a different person from CFO (or other officers)?

Yes

Is the ESG strategy integrated in the Business Plan (or in the group

strategy)? No

Does the company have an ethical code? Yes

Percentage of female directors 20% (1 out of 5) 20% (1 out of 5)

How is the cybersecurity issue managed? The company is fully compliant with EU GDPR regulation. The company is member of M3AAWG to fight abuse

SWOT Analysis

Strengths Weaknesses

• Highly talented and motivated people

• Scalable business

• Positive net cash position

• Dependence on key talents

• Small size compared to competitors on big clients

• High goodwill (EUR16.7 million at June 2019, 25% market cap)

Opportunities Threats

• Expansion outside Italy

• Significant cross-selling opportunities into existing customers base

• Potential M&A to expand product offering

• Scarcity of talented personnel

• M&A risk

• Increasing regulatory requirements and connected reputational risk

2,0002,5003,0003,5004,0004,5005,000

MailUp FTSE Italia All-Share

Founders ; 53,6%

Pronti Gianluca

; 7,2%

BMC Holding ; 4,4%

Employees; 0,3%

Treasury; 0,5% Free

float; 34,1%

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

25 Servizio Studi – Equity Research

MailUp

Income Statement Financial Ratios

(EURm, %) 2018A 2019E 2020E 2021E (%) 2018A 2019E 2020E 2021E

Net Revenues 39,0 59,9 71,3 83,1 ROE 15,6% 12,9% 18,8% 24,7%

EBITDA 3,8 4,8 7,3 9,6 Net Fin. Debt / Equity (x) -0,4 -0,1 -0,2 -0,2

EBITDA margin 9,7% 8,0% 10,2% 11,6% Net Fin. Debt / EBITDA (x) -1,7 -0,4 -0,5 -0,6

EBIT 1,9 2,4 4,5 6,4 Capex / Sales 8,5% 6,4% 6,2% 6,0%

EBIT margin 4,9% 4,0% 6,3% 7,7% Pay Out Ratio 0,0% 0,0% 0,0% 0,0%

Profit before taxes 1,9 2,4 4,5 6,4

Taxes -0,7 -1,1 -1,8 -2,3

Net Income 1,3 2,7 4,1 4,9

Per Share Data

(EUR) 2018A 2019E 2020E 2021E

EPS 0,08 0,09 0,18 0,27

Growth Rates DPS 0 0 0 0

(%) 2018A 2019E 2020E 2021E BVPS 1,07 1,15 1,34 1,61

Growth Group Net Sales 47,8% 53,5% 19,0% 16,6%

Growth EBITDA 30,0% 27,8% 50,7% 32,3%

Growth EBIT 45,9% 27,1% 85,6% 42,8%

Growth Net Profit 143,9% 103,2% 49,0% 21,8% Stock Market Ratios

(x) 2018A 2019E 2020E 2021E

P/E 27,8 48,9 24,0 16,1

P/OpCFPS 3,1 4,2 3,8 3,3

Balance Sheet P/BV 2,19 3,79 3,27 2,72

(EURm) 2018A 2019E 2020E 2021E Dividend Yield (%) 0,0% 0,0% 0,0% 0,0%

Capital Employed 9,6 15,4 16,4 18,2 EV/Sales

0,76 1,08 0,89 0,73

Shareholders’ Equity 15,9 17,3 20,0 24,0 EV/EBITDA 7,8 13,4 8,7 6,3

Net Financial Debt / (Cash) -6,4 -1,9 -3,5 -5,9 EV/EBIT 15,6 26,9 14,1 9,5

* Priced on 31 January 2020

Source: Company data, UBI Banca estimates 2018 Stock Market Ratios based on average 2018 price

Sustainable Finance and Fintech: progress and innovation, 6 February 2020

26 Servizio Studi – Equity Research

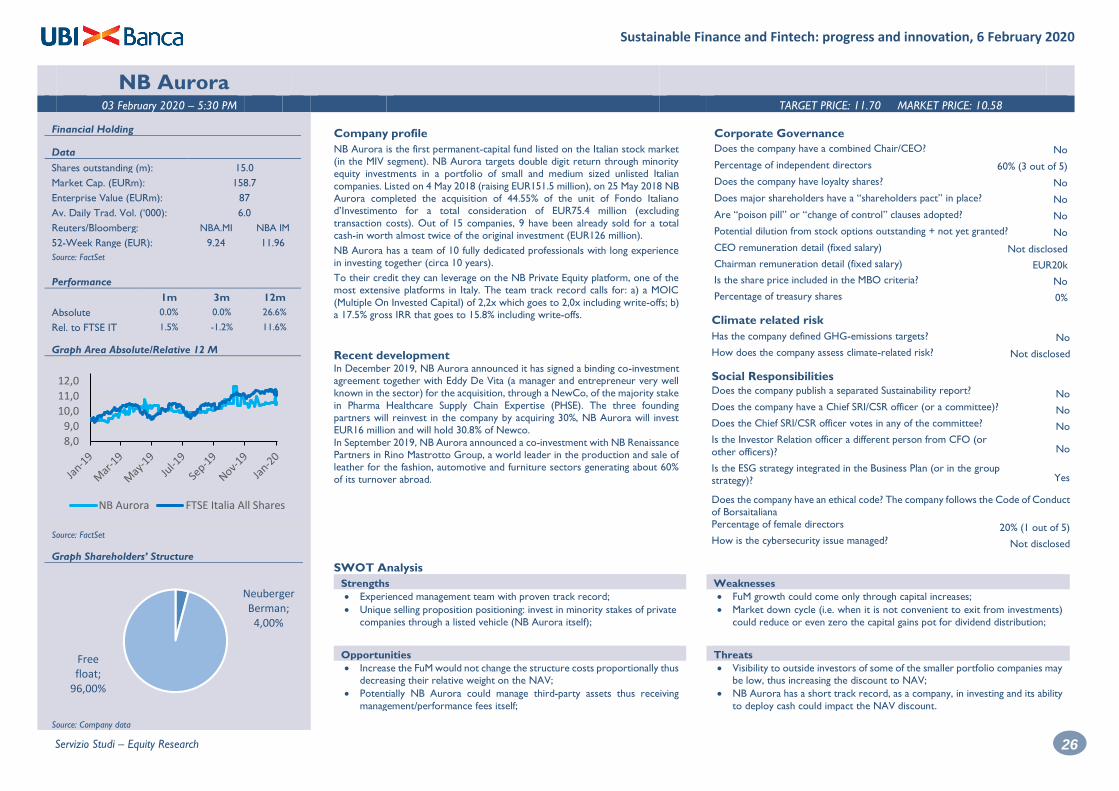

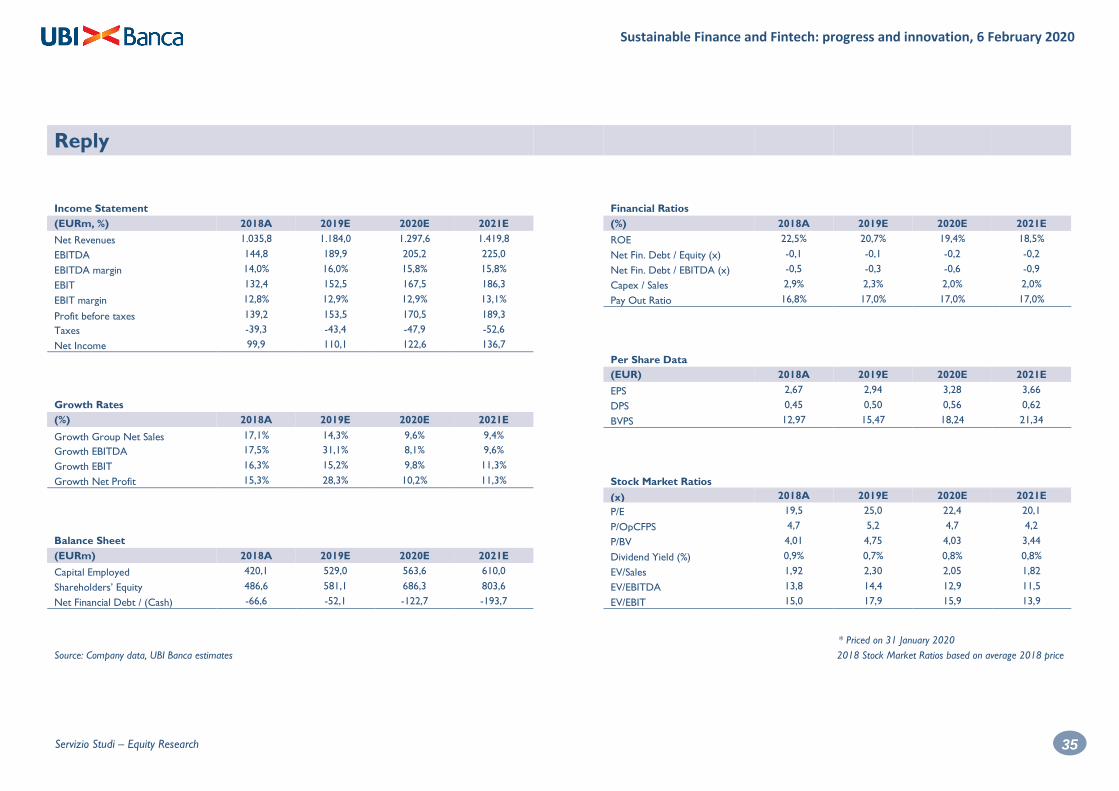

NB Aurora 03 February 2020 – 5:30 PM TARGET PRICE: 11.70 MARKET PRICE: 10.58

Financial Holding

Data

Shares outstanding (m): 15.0

Market Cap. (EURm): 158.7

Enterprise Value (EURm): 87

Av. Daily Trad. Vol. (‘000): 6.0

Reuters/Bloomberg: NBA.MI NBA IM

52-Week Range (EUR): 9.24 11.96

Source: FactSet

Performance

1m 3m 12m

Absolute 0.0% 0.0% 26.6%

Rel. to FTSE IT 1.5% -1.2% 11.6%

Graph Area Absolute/Relative 12 M

Source: FactSet

Graph Shareholders’ Structure

Source: Company data

Company profile