SUNFLOWER SEED MARKET VALUE CHAIN …webapps.daff.gov.za/AmisAdmin/upload/Sunflower Market...1...

29

1 SUNFLOWER SEED MARKET VALUE CHAIN PROFILE 2014 Department of Agriculture, Forestry and Fisheries . Directorate Marketing Private Bag X 15 Arcadia 0007 Tel: 012 319 8455/6 Fax: 012 319 8131 Email: [email protected]

Transcript of SUNFLOWER SEED MARKET VALUE CHAIN …webapps.daff.gov.za/AmisAdmin/upload/Sunflower Market...1...

1

SUNFLOWER SEED MARKET VALUE CHAIN PROFILE

2014

Department of Agriculture, Forestry and Fisheries .

Directorate Marketing Private Bag X 15

Arcadia 0007

Tel: 012 319 8455/6 Fax: 012 319 8131

Email: [email protected]

2

TABLE OF CONTENTS

1. DESCRIPTION OF THE INDUSTRY ............................................................................... 3

1.1 Production Areas ..................................................................................................... 3 1.2 Production Trends ................................................................................................... 4

2. MARKET STRUCTURE .................................................................................................. 5

2.1. Domestic Market ..................................................................................................... 5 2.2. Producer prices ....................................................................................................... 7

2.3. Exports ................................................................................................................... 7 2.3.1. Share Analysis ............................................................................................... 13

2.4. Imports ................................................................................................................. 15

2.5. Processing ............................................................................................................ 17 3. MARKET VALUE CHAIN .............................................................................................. 20

4. MARKET INTELLIGENCE ............................................................................................ 21

4.1. Tariffs ..................................................................................................................... 21 4.2. Performance of the South African sunflower seed industry.......................................... 24

5. STRATEGIC CHALLENGES AND OPPORTUNITIES ......................................................... 28

6. OTHER INFORMATION ............................................................................................... 28

7. ACKNOWLEDGEMENTS ............................................................................................. 29

3

1. DESCRIPTION OF THE INDUSTRY

Sunflower seed is primarily used for the manufacturing of sunflower oil and oilcake. In South Africa sunflower is well adapted in both hot and dry climate. The seed can be consumed after the hull has been removed as a snack or used for production of different oils. Most of the seed produced is marketed locally to expressers, animal feed manufacturers and for seed. Sunflower is the third largest grain crop produced in South Africa after maize and wheat. For the period between 2004 and 2013, an average of about 643 thousand tons sunflower seed were produced per annum while the gross value was approximated at 1.93 billion Rand per annum. The gross value of sunflower seed produced in South Africa has been relatively volatile for the past ten years. From Figure 1 below there is an indication of cyclical behavior with regard the gross value of production, which can be associated with the cycle of the producer prices received for sunflower seed. During 2013 marketing year, sunflower seed production contributed approximately 5.42% to field crops’ total gross value of production.

Source: Statistics and Economic Analysis

1.1 Production Areas

Sunflower seed is produced mostly in the eight provinces out of the nine provinces. Traditionally, the North West and Free State Provinces produced a significant amount of sunflower seed. Sunflower seed can be planted from the beginning of November to the end of December, which is almost the same time for maize plantings. The general observation from Table 1 below is that during the five year period between 2009 and 2013 production of sunflower seed has experienced a downturn in almost all the major producing provinces. The Free State Province has consistently experienced a downward trend in sunflower seed production during this period except in 2011 and 2013, while another major producer the North West Province has also had a similar experience. The same trend is observed in other provinces such as the Limpopo and Mpumalanga.

Figure 1: Sunflower Seed - Gross Value of Agricultural Production

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Marketing Year

Gro

ss V

alu

e (

R'0

00

)

4

Table 1: Sunflower seed production by provinces

Province Production in 2009 (tons)

Production in 2010 (tons)

Production in 2011 (tons)

Production in 2012 (tons)

Production in 2013 (tons)

Western Cape

700 200 0 0 0

Eastern Cape 780 160 220 0 0

Northern Cape

1000 1 700 680 100 100

Free State 363 000 277 500 434 000 247000 296800

Limpopo 90 000 67 500 98 000 85000 79500

Mpumalanga 370 700 12 800 12000 135001 9900

Gauteng 9 820 4 900 4 800 3 900 4700

North West 298 000 175 240 310 300 172500 166000

Source: Statistics and Economic Analysis The actual production of sunflower seed during the 2012/13 production season is depicted in Figure 2 and shows that the Free State and North West provinces are the major producers of sunflower seed with a share of 53% and 30% of the total production respectively, followed by Limpopo, Mpumalanga and Gauteng provinces. Very small quantities of sunflower seed were produced in the Western, Eastern and Northern Cape provinces of South Africa.

Source: Statistics and Economic Analysis 1.2 Production Trends

According to Figure 3, the hectares planted for sunflower seed have been volatile for the past ten years and this was followed by fluctuations in production volumes. The figure further indicates that an average of 643 thousand hectares of sunflower seed were planted per annum resulting in

Figure 2: Sunflower seed production by province 2012/13

Free State

53%

Limpopo

14%

Mpumalanga

2%

Gauteng

1%

North West

30%

5

average production volumes of about 487 thousand tons. Both area planted and total production of sunflower seed experienced substantial increase during the 2007/’08 season as compared to the past four seasons, followed by a slight decline in 2008/09 and 2009/10 seasons. Both area planted and total production shows substantial increase in 2010/11 production season, followed by slight decline in 2011/12. This was then followed by a drastic increase in production of sunflower seeds in 2012/13. Generally, production of sunflower seeds has been fluctuating during the past 10 years.

Source: Statistics and Economic Analysis

2. MARKET STRUCTURE

2.1. Domestic Market The processing of sunflower seed is highly capital intensive and requires high technology and specialized knowledge. The refining process produces sunflower oil which is used mostly for human consumption. Most of the large refineries are situated in Gauteng and Kwazulu Natal. The greatest importance of sunflower production is the extraction of oil from the seed. Figure 4 below indicates domestic producer sales and exports of sunflower seed from 2003/04 to 2012/13 marketing years. The figure indicates that exports of sunflower seed were minimal throughout the period under analysis and this explains that South Africa is not a major exporter of sunflower seed. The lower volumes of sunflower seed exports are also attributed to the fact that our processing capacity in the country is big enough to accommodate most of sunflower seed produced locally. In actual fact South Africa remains a net importer of sunflower seed over the past few years. The figure indicates that domestic producer sale of sunflower seed remained dominant throughout the period under analysis. The period under analysis closed with moderate of sunflower sales in the domestic market in 2012/13.

Figure 3: Area Planted & Total Production

0

100000

200000

300000

400000

500000

600000

700000

2003

/'04

2004

/'05

2005

/'06

2006

/'07

2007

/'08

2008

/'09

2009

/'10

2010

/'11

2011

/'12

2012

/'13

Production Years

Are

a P

lan

ted

(H

a)

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

To

tal P

rod

uct

ion

(T

on

s)

Area Planted (ha) Total Production(tons)

6

Source: Statistics and Economic Analysis Figure 5 below shows sunflower seed processing from 2004 to 2013. The figure indicates that the quantity of sunflower seed processed into oil is generally higher than the quantities utilized for seed, animal feed manufacturing and other uses. The quantity of sunflower seed utilized for oil and oilcakes was very low during the year 2007 compared to other years mainly as a result of lower levels of local production at the time. This increased slightly during the years 2008 and 2009 as the local production increased. The period under analysis closed with moderate volume of sunflower seed processing.

Source: Statistics and Economic Analysis

Figure 4: Sunflwer Seed - Domestic Producer Sales Vs Exports

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

2003/'04

2004/'05

2005/'06

2006/'07

2007/'08

2008/'09

2009/'10

2010/11

2011/12

2012/13

Marketing Year

Tons

Producer sales (tons) Exports (tons)

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Vo

lum

e (

Ton

s)

Period (Years)

Figure 5: Sunflower seed processing

Oil & Oilcake Seed & Feed Other

7

2.2. Producer prices Figure 6 below shows producer prices for sunflower seed from 2003/04 to 2012/13. The period under analysis opened with lower price of R1 826.88/ton and the prices continued to decrease dramatically between 2003/04 and 2004/05. The producer prices for the product in question started to pick up in 2005/06 and continued to increase until a peak was reached in 2007/08. The figure further indicates that the price declined dramatically in 2008/09. This was followed by an increase from 2009/10 production season until the highest price was achieved during the closing season of the period under analysis (2012/13). The period under review closed with high level of producer prices (R4 840.53/ton) in 2012/13.

Source Statistics and Economic Analysis

2.3. Exports The major importers of sunflower seed originating from South Africa are Kenya, Pakistan France, Botswana, Uganda and Namibia. During the year 2013, Kenya acquired about 53.8% of South Africa’s total sunflower seed exports, followed by Pakistan and France with 14.5% and 9.3% respectively. Figure 7 below shows value of sunflower seed exports by different province of South Africa for the period between the year 2004 and 2013. The figure indicates that exports from KwaZulu-Natal province were dominant throughout the period under analysis with the exception was only in 2011 where Gauteng province emerged to be the largest exporter of sunflower. The figure further indicates that the exports of sunflower seed from other province remained minimal throughout the period under review. Between 2004 and 2007 exports of sunflower seed from KwaZulu-Natal Province were greater than those from any other province in the Republic with greater export values recorded during this period. Exports of sunflower seed from Gauteng were very low during the years 2009 and 2010 while those from KZN were slightly higher at the time. The figure further

0

1000

2000

3000

4000

5000

6000

Ran

ds/

Ton

Years

Figure 6: Sunflower Seed Producer Prices

8

indicates that the period closed with Kwazulu-Natal provinces accumulating higher exports of sunflower seed in 2013.

Source: Quantec Easy Data The trend for sunflower seed exports from Western Cape Province is shown in Figure 8 below. In the Western Cape Province sunflower seed exports occur mostly through the City of Cape Town Metropolitan municipality. The figure indicates that there were no exports of sunflower seed from the Eden district municipality from 2007 and 2011. It is also clear from the figure that City of Cape Town was the largest contributor to the Western Cape’s total value of sunflower exports in 2013 followed by Eden District.

Source: Quantec Easy Data

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Western Cape 33133 3757763 106072 178029 307339 292990 102295 1460912 3530285 6710013

Kwazulu-Natal 2527687 9123582 7462307 8715573 59631548 46685514 5701666 0 20378213 15250068

North West 156890 0 0 1099 0 0 0 9229215 428606 699

Gauteng 4810981 1117406 620343 484315 4.24E+08 590031 365211 443805 1967206 4118468

Other 0 117 1077 4000 0 40345 811 183574 5783 0

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

400000000

450000000

Exp

ort

Valu

e (

Ran

d)

Period (Years)

Figure 7: Value of sunflower seed exports by provinces

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

City of Cape Town Metro 33032 30572 92778 178029 307339 292990 102284 1460912 2746189 4441809

Cape Winelands DM 101 18542 0 0 0 0 11 0 0 0

Eden District 0 3708650 13294 0 0 0 0 0 784096 2268204

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

4500000

5000000

Exp

ort

s V

alu

e (

Ran

d)

Period (Years)

Figure 8: Value of sunflower exports from Western Cape

9

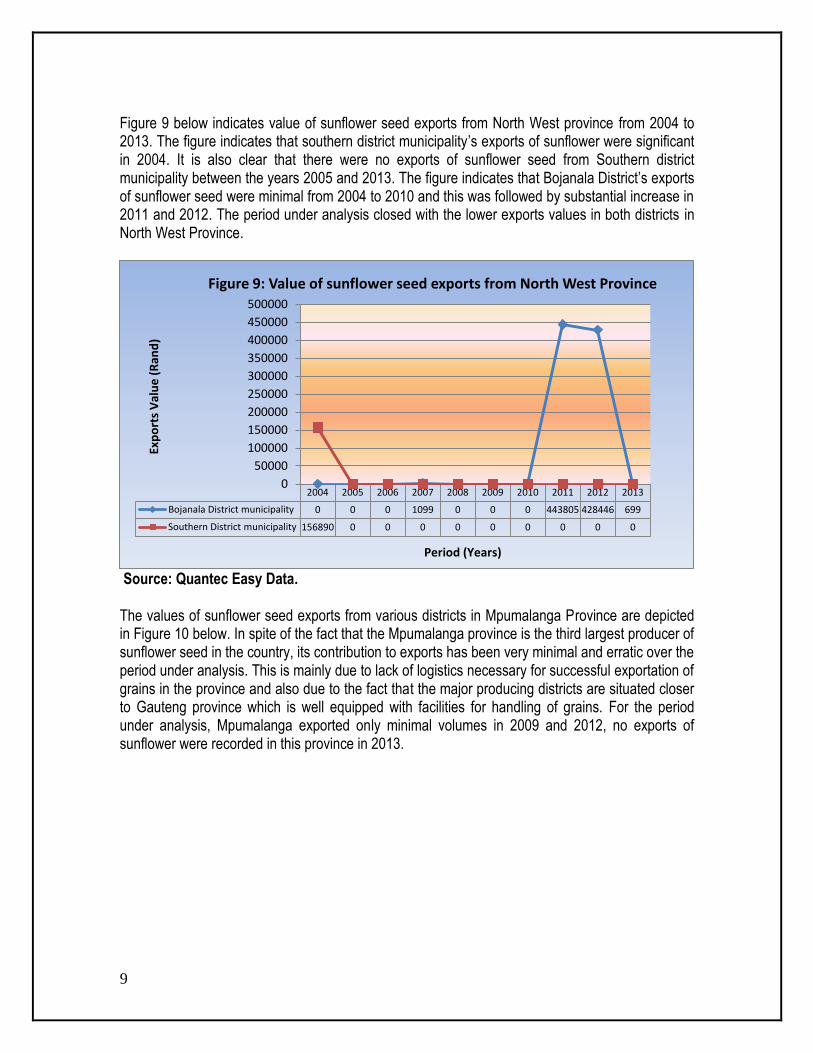

Figure 9 below indicates value of sunflower seed exports from North West province from 2004 to 2013. The figure indicates that southern district municipality’s exports of sunflower were significant in 2004. It is also clear that there were no exports of sunflower seed from Southern district municipality between the years 2005 and 2013. The figure indicates that Bojanala District’s exports of sunflower seed were minimal from 2004 to 2010 and this was followed by substantial increase in 2011 and 2012. The period under analysis closed with the lower exports values in both districts in North West Province.

Source: Quantec Easy Data. The values of sunflower seed exports from various districts in Mpumalanga Province are depicted in Figure 10 below. In spite of the fact that the Mpumalanga province is the third largest producer of sunflower seed in the country, its contribution to exports has been very minimal and erratic over the period under analysis. This is mainly due to lack of logistics necessary for successful exportation of grains in the province and also due to the fact that the major producing districts are situated closer to Gauteng province which is well equipped with facilities for handling of grains. For the period under analysis, Mpumalanga exported only minimal volumes in 2009 and 2012, no exports of sunflower were recorded in this province in 2013.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Bojanala District municipality 0 0 0 1099 0 0 0 443805 428446 699

Southern District municipality 156890 0 0 0 0 0 0 0 0 0

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

Exp

ort

s V

alu

e (

Ran

d)

Period (Years)

Figure 9: Value of sunflower seed exports from North West Province

10

Source: Quantec Easy Data Figure 11 below, indicates the value of sunflower seed exports from KwaZulu-Natal province form 2004 to 2013. The figure indicates that the value of sunflower seed exports from the Kwazulu-Natal province fluctuated considerably between the year 2004 and 2012 with the lowest levels having occurred during the year 2004. Sunflower seed exports from the UMzinyathi district started increasing in 2005 and this continued until a peak was reached in 2008 which was about 60 million Rand. The figure further reveals that the period under analysis closed with very low values of sunflower seed from KwaZulu-Natal, particularly those from UMzinyathi and eThekwini.

Source: Quantec Easy Data

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Gert Sibande DM 0 0 0 0 0 0 0 0 0 0

Nkangala DM 0 0 0 0 0 5863 0 0 160 0

0

1000

2000

3000

4000

5000

6000

7000 Ex

po

rts

Val

ue

(R

and

)

Period (Years)

Figure 10: Value of Sunflower Seed Exports from Mpumalanga Province

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

UMgungundlovu District 0 0 4200 0 0 0 320 11 504777 0

Umzinyathi District 2498904 7806150 7458107 8685914 59631548 46685514 5701308 9229204 19870959 15237031

eThekwini Metro 28783 1317432 0 29659 0 0 0 0 2478 12876

Uthungulu District 0 0 0 0 0 0 38 0 0 161

0

10000000

20000000

30000000

40000000

50000000

60000000

70000000

Exp

ort

s V

alu

e (

Ran

ds)

Period (Years)

Figure 11: Value of Sunflower Seed Exports from KZN Province

11

Figure 12 below indicate the value of sunflower seed exports from Gauteng province from 2004 to 2013. The figure indicates that City of Johannesburg Metro and Ekurhuleni metro opened with moderate value of exports of sunflower seed while the other district opened with lower levels of sunflower seed exports. The figure further indicates that sunflower seed exports arise mainly from the City of Johannesburg Metropolitan Municipality while those from the other three districts namely, Sedibeng, West Rand and Metsweding have been very low and irregular over the period between 2004 and 2013. The value of sunflower seed exports originating from the City of Johannesburg municipality peaked during the year 2008 and then declined substantially between 2009 and 2013. Exports from the other three districts have been considerably lower during the period under review. Gauteng Province, in spite of not being a major producer of sunflower seed is an exporter of sunflower oil because of larger number of traders who are situated in the province as well as the availability of Randfontein Grain Market in the Province.

Source: Quantec Easy Data Figure 13 shows volume of sunflower exports to various regions in the world from 2004 to 2013. The period under analysis opened with moderate volumes of sunflower exports from South Africa to various regions. The figure further indicates that sunflower seed exports from South Africa to various regions/continents were very low and unreliable over the period under analysis, mainly due to relatively lower levels of local production. Sunflower seed from South Africa is exported mainly to Africa, Asia and Europe and intermittently to the Americas and Oceania. The exports to these regions fluctuated considerably over the past ten years with a peak in exports destined to Europe and Asia in the year 2008. The period under review closed with lower volumes of sunflower seed exports.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Sedibeng District 0 0 2018 7158 1848 0 2477 2692 6258 706

West Rand District 114213 1060727 511429 446363 1119 16475 243897 706 1534518 3837035

Ekurhuleni Metro 2652377 10192 12197 11168 11342 552294 20589 108517 102572 63364

City of Johannesburg Metro 2044391 46487 94699 19626 4.24E+08 19503 93789 57178 317796 128519

City of Tshwane Metro 0 0 0 0 0 1759 4458 14481 6063 88048

Metsweding District 0 0 0 0 0 0 0 0 0 795

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

400000000

450000000

Exp

ort

s V

alu

e (

Ran

d)

Period (Years)

Figure 12: Value of sunflower seed exports from Gauteng Province

12

Source: Quantec Easy Data Figure 14 below summarizes the trend of sunflower seed exports from South Africa to other African countries. The figure indicates that SADC and Eastern Africa are the major recipients of South African sunflower seed exports. On the African continent we export our sunflower seed to Eastern Africa, Northern Africa and SADC with insignificant amounts of exports going to Northern Africa Rest and Eastern Africa. In the Eastern Africa, we export our sunflower mainly to Kenya and Uganda while Zimbabwe remains the major importer of sunflower seed originating from South Africa in the SADC region. During the years 2008 and 2009, larger amounts of sunflower seed exports from South Africa were destined to Northern Africa followed by exports to SADC and the Eastern Africa Rest respectively. Exports sunflower seed from South Africa to the African continent have also declined during the year 2010 and this was followed by a slight increase 2011. The situation with exports to Africa is very similar to the situation that was observed with regard to exports to the rest of the world. The period under review closed with lower levels of sunflower seed exports to Eastern Africa and Northern Africa.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Africa 39.355 496.11 333.15 335.62 1305.2 1187.2 157.42 383.4 383.4 257.89

Americas 62.72 75.619 4.193 23.768 81.441 21.207 0.637 20.551 20.551 1.776

Asia 246.97 214.46 172.29 146.76 18005 0.034 10.55 119.81 119.81 172.95

Europe 92.009 39.867 2.94 3.145 60084 0.165 1.986 51.253 51.253 66.576

Oceania 0 0.016 0 0 0 0 0 0 0 0

0

10000

20000

30000

40000

50000

60000

70000 Ex

po

rt V

olu

me

(To

ns)

Preiod (Years)

Figure 13: Volume of sunflower seed exports to various regions

13

Source: Quantec Easy Data

2.3.1. Share Analysis

Table 2: Contribution of various provinces to the total SA sunflower seed exports (%)

Year 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Province

Western Cape

0.44 26.84 1.29 1.89 0.06 0.62 1.66 12.91 13.42 25.72

Eastern Cape

0.00 0.00 0.00 0.00 0.00 0.00 0.00

0.00 0.00 0.00

Free State 0.00 0.00 0.01 0.04 0.00 0.00 0.00 0.00 0.00 0.00

Kwazulu- Natal

33.57 65.17 91.11 92.88 12.32 98.06 92.41 0.00 77.47 58.47

North-West 2.08 0.00 0.00 0.01 0.00 0.00 0.00 81.55 1.63 0.00

Gauteng 63.90 7.98 7.57 5.16 87.61 1.24 5.92 3.92 7.48 15.79

Limpopo 0.00 0.00 0.00 0.00 0.00 0.072 0.01 1.62 0.00 0.00

Mpumalanga 0.00 0.00 0.00 0.00 0.00 0.012 0.00 0.00 0.00 0.00

Source: Calculated from Quantec easy data Table 2 above confirms the earlier observation that Gauteng, Kwazulu-Natal and Western Cape Provinces are the major exporters of sunflower seed in South Africa, while exports from Limpopo and Mpumalanga remained minimal throughout the period under analysis. Gauteng Province commanded the greatest share of South Africa’s total sunflower seed exports during the years 2004 and 2008 while KwaZulu-Natal Province became be the largest exporter of sunflower seed from 2005 to 2013 exception was in 2008 and 2011. The table further indicates that KwaZulu-Natal Province accounted for 58.47% of South Africa’s total sunflower seed exports in 2013 while the contribution of other provinces remained minimal.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Eastern Africa 24.796 120.95 176.99 124.95 388.33 99.755 116.58 262.61 247.1 203.19

Middle Africa 0.003 0.96 0.151 0 0.006 0 0 0.09 0 0.001

Northern Africa 0.008 215.62 118 200 762.03 849.21 0.034 0.034 110.44 0.03

Western Africa 0.05 4.786 4.342 0.778 1.246 0.602 1.151 0.592 1.021 1.143

SADC 14.498 153.8 33.668 9.893 153.59 237.64 39.662 19.184 24.84 53.523

0 100 200 300 400 500 600 700 800 900

Exp

ort

Vo

lum

e (

Ton

)

Period (Years)

Figure 14: Volume of sunflower seed exports to Africa

14

Table 3: Contribution of various districts in Gauteng Province to the provincial sunflower seed exports (%)

Year 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

District

Sedibeng 0.00 0.00 0.32 1.47 0.00 0.00 0.68 1.47 0.32 0.02

West Rand 2.37 94.92 82.44 92.16 0.00 2.79 66.78 0.38 78.00 93.17

Ekurhuleni 55.13 0.91 1.96 2.30 0.00 93.60 5.63 59.11 5.21 1.54

City of Johannesburg

42.49 4.16 15.26 4.05 100 3.31 25.68 31.15 16.15

3.12

City of Tshwane

0.00 0.00 0.00 0.00 0.00 0.29 1.22 7.89 0.31

2.18

Source: Calculated from Quantec easy data Table 3 indicates contribution of different districts to Gauteng province’s total value of groundnuts exports. The figure indicates that the West Rand district, City of Johannesburg and Ekurhuleni are the major exporters of sunflower seed in Gauteng province while contribution in City of Tshwane and Sedibeng district are minimal. On average, West Rand is the major contributor to Gauteng’s total sunflower seed exports followed by City of Johannesburg. City of Tshwane Metropolitan District only recorded sunflower seed exports between the years 2009 and 2013. The table further indicates that West Rand accumulated higher share between 2005 and 2007 whereas City of Tshwane accumulated zero percent during this period. The table further indicates that West Rand district was responsible for about 93.17% of Gauteng’s total value of exports in 2013. Table 4: Contribution of various districts in KwaZulu-Natal Province to the provincial sunflower seed exports (%)

Year 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

District

UMgungundlovu

0.00 0.00 0.06 0.00 0.00 0.00 0.01 0.01 2.48

0.00

UMzinyathi 98.86 85.56 99.94 99.66 0.00 100 99.99 99.99 97.51 99.9

ILembe 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

EThekwini 1.13 14.43 0.00 0.34 0.00 0.00 0.00 0.00 0.012 0.01

Source: Calculated from Quantec easy data Table 4 indicates contribution of various districts in KwaZulu-Natal province to the provincial sunflower seed exports from 2004 to 2013. The figure indicates that in Kwazulu-Natal province, the UMzinyathi district commanded the greatest share of sunflower seed exports throughout the period under analysis with very fractional exports recorded for the EThekwini district in 2007, 2012 and 2013. During the 2013 season UMzinyathi district accounted for 99.9% of sunflower seed exports from the KwaZulu-Natal, with the remaining 0.01% originating from EThekwini district.

15

2.4. Imports

South Africa imports sunflower seed from the following regions: Europe, Asia, the Americas and Africa particularly from the SADC region. Figure 15 indicates that over the past ten years South Africa has been importing sunflower seed consistently from Africa, the Americas, Europe and Oceania. The major sunflower seed import market for South Africa is Europe followed by Africa and the Americas. On average, South Africa imports about 18 680 tons of sunflower seed annually from Europe while imports from Africa and Asia are about 1164 tons and 357 tons per annum, respectively. Figure 15 shows that, during the year 2013, South Africa’s imports of sunflower seed originated mainly from Europe followed by those from Africa and Asia. However, imports from all five regions have been insignificant over the period under review, until imports from Europe peaked in 2009. The period under analysis closed with high volumes of sunflower seed from Europe.

Source: Quantec Easy data Figure 16 below indicates volume of sunflower seed imports from Africa for the period ranging from 2004 to 2013. The figure indicates that the period under analysis opened with moderate volumes of sunflower seed imports. The figure further indicates that on the African continent South Africa imports its sunflower seed mainly from SADC region which might be attributed to the SADC Free Trade Agreement which facilitates flow of commodities among SADC countries at no tariff charges. In the SADC region, sunflower seed imports originate mainly from countries such as Malawi and Mozambique, with fractional and erratic quantities originating from DRC, Angola and Zimbabwe. The highest volumes of imports from SADC were experienced during the year 2007 when about 4000 tons were imported by South Africa from the region. The figure furthers indicates that less was imported from Eastern Africa throughout the period under analysis.

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Africa 418 399.32 559.68 3973.6 680.82 532.5 1818.5 503.5 1587.2 1175.8

Americas 0.843 0.589 27.55 235.42 289.96 486.05 80.136 176.58 83.068 174.83

Asia 415.45 464.1 409.36 686.55 307.15 396.81 430.16 252.37 92.44 114.38

Europe 17260 1.391 17.52 45.48 52.087 87627 23183 25502 776.64 32341

Oceania 3.272 11.275 13.605 42.11 32.559 176.04 0.58 0 0 0.84

0 10000 20000 30000 40000 50000 60000 70000 80000 90000

100000

Imp

ort

s V

olu

me

(To

n)

Period (Years)

Figure 15: Volume of sunflower seed imports from various regions

16

Source: Quantec Easy data Figure 17 below shows volume of sunflower seed imports originating from Oceania from 2004 to 2013. The period under review opened with lower imports of sunflower from Oceania. The figure further indicates that sunflower seed imports originating from Oceania are mainly from Australia. However, the volume of sunflower seed imports from this region was very low in 2004 primarily due to the fact that greater volumes of sunflower seed were imported from Europe during that year, while on the other hand the local production was also relatively higher. The figure furthers indicates that less was imported from Polynesia and New Zealand throughout the period under analysis.

Source: Quantec Easy Data

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Eastern Africa Rest 10 0 0 0 0 0 0 0 0 0

SADC 408 399 560 3974 681 533 1818 504 1587 1176

Malawi 249 399 560 3968 564 510 1818 432 1562 1176

Mozambique 159 0 0 0 81 0 0 72 25 0

0

500

1000

1500

2000

2500

3000

3500

4000

4500 Im

po

rts

Vo

lum

e (

Ton

)

Period (Years)

Figure 16: Volume of sunflower seed imports from africa

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Australia 3.27 11.28 13.61 41.97 32.56 176.04 0.03 0.00 0.00 0.84

Polynesia 0.00 0.00 0.00 0.14 0.00 0.00 0.00 0.00 0.00 0.00

New Zealand

0.00 0.00 0.00 0.00 0.00 0.00 0.55 0.00 0.00 0.00

0.00 20.00 40.00 60.00 80.00

100.00 120.00 140.00 160.00 180.00 200.00

Imp

ort

s V

olu

me

(To

ns)

Period (Years)

Figure 17: Volume of sunflower seed imports from Oceania

17

Figure 18 indicates volume of sunflower seed imports originating from Europe 2004 to 2013. The principal exporters of sunflower seed to South Africa in Europe are Romania and European Union respectively. Figure 18 shows that the highest volume of sunflower seed imports from Europe originated from Eastern Europe in 2004 and again in 2009. The figure further shows that sunflower seed imports from the European Union were dominant throughout the period under analysis. It is also clear that that there were no imports of sunflower seed from Eastern Europe between 2005 and 2008.

Source: Quantec Easy Data

2.5. Processing

Sunflower seed provides 40-50% of oil, which is mostly processed to cooking oil. The oil is used on a daily basis in households, restaurants and various food industries. Sunflower is the basic raw material for the preparation of margarine and spreads, used daily by millions of people. Some pet food also contains oilseed raw material. In desperate times sunflower oil can also be converted to diesel for use in diesel engines as bio-fuel. Figure 19: The production of oil Source: Grain SA

0 10000 20000 30000 40000 50000 60000 70000 80000 90000

100000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Imp

ort

Vo

lum

e (

Ton

s)

Period (Years)

Figure 18: Volume of sunflower seed imports from Europe

Eastern Europe European Union France Romania

Production of

Sunflower Press

Hexane Oilcake of

Sunflower

Crude oil Refining Sunflower

Oil

18

During pressing there are two different methods of extracting oil from the oilseeds i.e. production of crude oil and production of oil cakes from hexane. Sunflower seed provides 40 – 50% of oil and about 40% of oilcake, which is processed to cooking oil and for animal feed respectively, see the (Figure 19) above. Other oil products include margarine, fuel in diesel engines and other foods. The sunflower seed also produces oil cake, which is widely used for animal feeds (as sunflower oilcake meal) because of its high protein content. Sunflower oil is marketed in the form of refined oil for domestic and industrial cooking as well as baking processes. In South Africa, the main crushers of sunflower seed are Nola Industries, Epic and Epko. Pressing plants with relatively smaller crushing capacity in the country are Sealake Industries, Elangeni Oil & cake Mills and Capital Oil Mills. According to the South African Oil Processors Association there are thirteen oil refineries in South Africa, namely Capital Oil Mills, Continental Oil Mills, Elangeni Oil & Cake Mills, Epic Foods, Epko Oil Seed Crushing, Hentiq 1320, Nedan Oil Mills, Nola Industries, Sealake Industries, Sun Oil Refineries, Sunola Oil Mills, UBR and Willowton Oil Mills. Figure 20 below indicates that when sunflower seed is crushed the oil is extracted from the seed and the oilcake that remains is then used to manufacture animal feeds in the form of sunflower oilcake meal. The oil can be used as cooking oil or if hydrogenated it becomes margarine that is used by households. The oil can also find its usage in the biofuel industry to manufacture biodiesel that is used in automotive engines or it can be blended with other vegetable oils to manufacture other foods. Figure 20: The uses of sunflower seed.

19

Source: Adapted from Grain SA

Sunflower

Seed

OIL

OILCAKE

FUEL IN DIESEL

ENGINES

COOKING OIL

MARGARINE

OTHER FOODS: Massage blends with

Vegetable oils

ANIMAL FEEDS

20

3. MARKET VALUE CHAIN

There are five main levels that can be identified in the sunflower seed-to-sunflower oil value chain: sunflower seed producers, crushers of seed, refineries of crude oil, the wholesalers and retailers, and finally the consumers as shown in Figure 22 below:

Figure 21: Sunflower Seed market value chain. Producers of sunflower seed usually deliver their produce to seed expressers who crush the seed to produce crude oil and oilcake. The crude oil can then be used by refineries to produce various products as explained in Figure 22 while the oilcake is used by animal feed manufacturers to manufacture a concentrate in the form of sunflower oilcake meal. Refineries may also import crude oil from the international market and, their products and those of the animal feed manufacturers are packaged, labeled and sent to wholesalers and retails who in turn will sell to consumers.

Sunflower seed

Producers

Crushers/Expressers

of Seed

Refineries of Crude

Oil

Wholesalers &

Retailers

Consumers

Imports of

Crude Oil

Animal feed

Manufacture

rs

21

4. MARKET INTELLIGENCE

4.1. Tariffs

South Africa applies the following tariffs to the imports of sunflower seed arising from the following trading partners: Table 5

EXPORTING COUNTRY

TRADE REGIME DESCRIPTION

APPLIED TARIFF

ESTIMATED TOTAL AD VALOREM EQUIVALENT TARIFF 2013

Slovakia MFN duties (Applied 9.40% 9.40%

Preferential tariff for European Union Countries

0.00% 0.00%

Argentina MFN duties (Applied) 9.40% 9.40%

Bulgaria MFN duties (Applied 9.40% 9.40%

Preferential tariff for European Union Countries

0.00% 0.00%

China MFN duties (Applied) 9.40% 9.40%

Belgium MFN duties (Applied) 9.40% 9.40%

Preferential tariff for European Union Countries

0.00% 0.00%

India MFN duties (Applied) 9.40% 9.40%

Netherlands MFN duties (Applied) 9.40% 9.40%

Preferential tariff for European Union Countries

0.00% 0.00%

Malawi Preferential tariff for SADC countries

0.00% 0.00%

Israel MFN duties (Applied) 9.40% 9.40%

United States of America

MFN duties (Applied) 9.40% 9.40%

Source: ITC Market Access Map Table 5 indicates that South Africa charges 9.40% tariff on imports of sunflower seed from other countries, but all the European Union Countries (such as Belgium, Slovakia, Bulgaria and Netherlands) and SADC countries receive preferential treatment of not having to pay any tariff when they export sunflower seed to South Africa. This is because of SADC Free Trade Agreement and the EU-SA Trade, Development and Cooperation Agreement that exist between South Africa and EU.

22

The following countries apply the following tariffs to the exports of sunflower seed originating from South Africa: Table 6

Importers Selected product codes

Product description

Trade regime description

Applied tariffs

Total ad valorem equivalent tariff (estimated)

France 1206001000 Sunflower seeds, whether or not broken

MFN duties (Applied)

0.00% 0.00%

Kenya 12060000 Sunflower seeds, whether or not broken

MFN duties (Applied)

10.00% 10.00%

Sudan 12060000 Sunflower seeds, whether or not broken

General tariff

25.00% 25.00%

Republic of Korea

1206000000 Sunflower seeds, whether or not broken

MFN duties (Applied)

25.00% 25.00%

Netherlands 1206001000 Sunflower seeds, whether or not broken

MFN duties (Applied)

0.00% 0.00%

Pakistan 12060000 Sunflower seeds, whether or not broken

MFN duties (Applied)

0.00% 0.00%

Argentina 12060010 Sunflower seeds, whether or not broken

MFN duties (Applied)

0.00% 0.00%

Zimbabwe 12060000 Sunflower seeds, whether or not broken

MFN duties (Applied)

5.00% 5.00%

Denmark 1206009100 Sunflower seeds, whether or not broken

MFN duties (Applied)

0.00% 0.00%

23

Importers Selected product codes

Product description

Trade regime description

Applied tariffs

Total ad valorem equivalent tariff (estimated)

Sunflower seeds

Mozambique 12060010 Sunflower seeds, whether or not broken

MFN duties (Applied)

2.50% 2.50%

Preferential Tariff for South Africa

0.00% 0.00%

Source: ITC Market Access Map Table 6 indicates that countries such as France, Netherlands, Pakistan, Argentina and Denmark charge no tariffs on imports of sunflower seed from the rest of the world.. South African sunflower seed exports face tariff barriers in countries such as Kenya, Sudan, Republic of Korea, Argentina, and Zimbabwe. Kenya generally charge higher tariffs at the level of 10.00% ad valorem on the imports of sunflower seed originating from South Africa. Republic of Korea and Sudan charge much higher tariffs at the level of 25.00% on their imports sunflower seed originating from South Africa.

24

4.2. Performance of the South African sunflower seed industry

Figure 22

Source: ITC Trade Map

25

Figure 22 above shows that South Africa’s sunflower seed imports from Netherlands, United States of America and Israel increased significantly between the years 2009 and 2013. South Africa increased its imports of sunflower seed from USA, Netherlands and Israel at a faster pace than these countries’ groundnuts export growth to the rest of the world. Over the same period, imports of sunflower from Romania, China, Argentina, India and Turkey declined significantly. Table 7 below and the figure on the next page (Figure 23) show the major export destinations of sunflower seed produced in South Africa. On average South Africa’s sunflower seed exports to the world have grown by 15% in value terms and 23% in volume terms between 2009 and 2013. During 2013 South Africa exported sunflower seed mainly to Kenya, Pakistan, France and Botswana. A total of 1 821 tons of sunflower seed originating from South Africa were exported to the world during 2013, of which 157 tons went to Kenya. Table 7: Importing markets for sunflower seed (120600) exported by SA in 2013

Importers

Trade Indicators

Exported value 2013 (USD thousand)

Share in South Africa's exports (%)

Exported quantity 2013

Unit value (USD/unit)

Exported growth in value between 2009-2013 (%, p.a.)

Exported growth in quantity between 2009-2013 (%, p.a.)

Exported growth in value between 2012-2013 (%, p.a.)

World 5,848 100 1,821 3,211 15 23 82

Kenya 3,408 58.3 157 21,707 196 96 227

Pakistan 850 14.5 170 5,000 170 71

France 546 9.3 64 8,531 285 68

Botswana 340 5.8 1,049 324

Uganda 194 3.3 40 4,850 -48 -18

Namibia 91 1.6 88 1,034

Mozambique 89 1.5 9 9,889 39 1 493

Swaziland 88 1.5 189 466

Zambia 85 1.5 39 2,179 31 39 1600

Source: ITC Trade Map During 2013 Kenya and Pakistan commanded the greatest share of sunflower seed exports originating from South Africa. During the same year, Kenya alone absorbed 58.3% of South Africa’s total sunflower seed exports followed by Pakistan with 14.5%.

26

Figure 23

Source: ITC Trade Map

27

Table 8: Supplying markets for sunflower seed (120600) imported by SA in 2013

Exporters

Trade Indicators

Imported value 2013 (USD thousand)

Share in South Africa's imports (%)

Imported quantity 2013

Unit value (USD/unit)

Imported growth in value between 2009-2013 (%, p.a.)

Imported growth in quantity between 2009-2013 (%, p.a.)

Imported growth in value between 2012-2013 (%, p.a.)

World 17,546 100 34,464 509 -25 -34 530

Romania 14,100 80.4 31,654 445 -54 9

Bulgaria 984 5.6 665 1,480 - - 69

United States of America

774 4.4 90 8,600 71 70 129

Malawi 516 2.9 1,176 439 40 16 -41

Argentina 466 2.7 85 5,482 -24 -31 99

Botswana 225 1.3 654 344 - -

China 188 1.1 94 2,000 -30 -36 29

France 150 0.9 20 7,500 17 30

Turkey 77 0.4 15 5,133 -2 -18 2467

Source: ITC Trade Map During the year 2013 South Africa imported a total of 34 464 tons of sunflower seed from the world. These imports originated mainly from Romania, Bulgaria, United Stated of America and Malawi. Romania commanded the greatest share in South Africa’s sunflower seed imports followed by Bulgaria, USA and Malawi respectively. Imports of sunflower seed from United State of America increased by 70% in value between the years 2012 and 2013. Sunflower seed imports from Bulgaria to South Africa increased by 69% in value over the same period.

28

he figure on the previous page shows that if South Africa is to diversify its sunflower seed imports, the biggest markets exist in Turkey, Russian Federation, republic of Moldova Slovakia, Ukraine and France. Other markets exist in countries such as China, Argentina and India since these countries recorded a positive growth in exports to the rest of the world between 2009 and 2013.

5. STRATEGIC CHALLENGES AND OPPORTUNITIES

As mentioned in the description sunflower seed production is very suitable for South African climatic conditions and is performing well for income generation to the rest of the agricultural sector. According to the FPMC report in 2003 the crushing capacity is not fully utilized by the companies therefore, there is an opportunity for any role player in the industry to crush seed, sell the crude oil at a lower price than the import parity price and still manage to realize profit. The challenge is how to get new role players in the industry as it is highly capitalized and requires sophisticated technology. There is a lack of black economic empowerment in this industry and also in the seed trade industry in general. Lack of funding to purchase equipment to get projects off the ground is often cited as one of the major obstacles to transformation. The fact that the growth season of sunflower is short, added to its drought tolerance; it can serve as an ideal alternative crop on low-potential soils when it is late to plant maize.

6. OTHER INFORMATION

In the agricultural sector, food safety is very important. As result the oilseed industry is also expected to adhere to o several regulations in this regard. The regulations include: Foodstuffs, Cosmetics and Disinfectants Act of 1972 (Act 54 of 1972) Health Act of 1977 (Act 63 of 1977) Fertilizers, Farm Feeds Agricultural Remedies A of 1947 (Act 31 of 1947) Agricultural Products Standards Act of 1990 (Act 119 of 1990)

29

7. ACKNOWLEDGEMENTS

The following organizations and references are acknowledged: Animal Feed Manufacturers Association Tel: (012) 663 9097 www.afma.co.za Grains South Africa Tel: (056) 515 0918 Fax: (056) 515 1517 www.grainsa.co.za Directorate Statistics and Economic Analysis Tel: (012) 319 8453 Fax: (012) 319 8031 www.nda.agric.za Quantec Easydata www.quantec.co.za ITC Market Access Map http://www.macmap.org/SouthAfrica ITC Trade Map http://www.trademap.org. Disclaimer: This document and its contents have been compiled by the Department of Agriculture, Forestry and Fisheries for the purpose of detailing the sunflower seed industry. Anyone who uses the information as contained in this document does so at his/her own risk. The views expressed in this document are those of the Department with regard to the industry, unless otherwise stated. The Department therefore accepts no liability that may be incurred resulting from the use of this information.