A Practitioner's Guide to Insurance Coverage Disputes in Missouri

Sue or Settle? Strategic Thinking for Insurance Coverage Disputes

(CLM018)

Speakers:

Ash Kilada, PepsiCo, Inc.

David F. Klein, Pillsbury Winthrop Shaw Pittman LLP

Learning Objectives

At the end of this session, you will:

• Know the legal and commercial considerations that drive the decision whether to litigate or compromise major insurance claims

• Understand the key strategic considerations driving settlement, the variables shaping negotiations, the potential formal or informal negotiating forums, and the tools at your disposal to get a settlement done

• Know how to manage litigation or settlement negotiations to minimize cost and maximize recovery

Section IThe Major Coverage Dispute

The Best Disputes are the Ones Avoided Improve contract certainty – know your policy

• Involve coverage counsel when reviewing policy terms and conditions

• Ask for clarification, wording enhancements up front

• Stress test loss scenarios through your policy language

• Choose your insurance partners carefully (brokers and insurers)

• Understand dispute provisions in your policy (arbitration, choice of law, etc.)

Identify and head off potential disputes before they occur:

• If a claim appears likely to be controversial, try to involve your broker early

• Get the underwriter involved

• Set reasonable expectations early with your internal management

The Day of Reckoning

You have been waiting for weeks to hear from insurers about that major claim

The loss is large enough to be reported on the company’s 10(k)

Your boss has been asking about insurance proceeds almost daily

Operational people have been assuming the cash will come in the door

A thin envelope comes in the mail . . . .

What do you do?

When Bad News Comes, Inhale . . . Review the insurer’s denial letter in light of the policy language

Review any applicable legal decisions with inside or outside counsel

Discuss objectively with the insurer’s claims staff

• Understand their basis for denial

• Do they understand the facts and your argument for coverage?

Understand all the intangible factors

• Is the problem an overly aggressive claims person or insurer’s coverage counsel?

Is the insurer making a statement to your broker?

• Is the insurer having a bad year? Or trying to avoid setting a precedent?

• Is there a chance of getting a better result talking to your account

manager/underwriter, or higher level management?

Features of a Major Coverage Dispute Underlying loss – very substantial

Ongoing/future exposure

• Financial

• Institutional

Legal uncertainty

Factual disputes

Impasse

• Denial of claim

• Insurer inaction

• Collateral disputes (indemnifiable loss, defense costs/rates)

Example #1: A D&O Claim D&O insurer denies legal costs of responding to a U.S. Attorney subpoena are

covered defense costs under its policy

Underlying loss is uncertain:

• Subpoena imposes some legal costs, but no immediate damages

Ongoing/future exposure:

• Future risk is very substantial—includes securities investigation, potential class action lawsuits, liability of directors, officers and company

• Insurer may have institutional commitment to policy interpretation

Legal uncertainty/factual issues:

• Is an investigative subpoena a “claim” within the meaning of the policy?

Impasse:

• Insurer declines coverage

• Note that a second claim for coverage may be possible as SEC investigation or third-party claims develop

Example #1: D&O Claim OptionsConsideration Do Nothing Sue Settle

Loss Absorb loss Win/lose on line-item basis

Partial recovery

Future Exposure Can pursue later claim as investigation unfolds

May or may not resolve if you win/lose

Possible accord as to future coverage

Legal Uncertainty No resolution Resolution if litigated to conclusion

Skip resolution of legal claims

Impasse Interim insurer win Interim win or interim/total loss

Narrower range of outcomes (partial recovery)

Example #2: An Environmental Claim Insurers have denied coverage or reserved rights under historic CGL policies

on a major environmental claim spanning sites in many jurisdictions

Underlying loss is very substantial:

• Company has 10 environmental sites in 4 states

Ongoing/future exposure:

• Overall remediation costs may reach $100M

• Insurers have institutional commitment to legal positions

Legal uncertainty/factual issues:

• Insurers cite qualified pollution exclusions, assert that administrative actions do not constitute

“suits” seeking “damages,” and contend that common-law allocation principles require the

insured to bear 2/3 of the liability

Impasse:

• All have denied claims or reserved rights with no indication that they will proceed to adjust

the losses or pay your attorney fees to deal with regulator agencies

Example #2: Environmental Claim OptionsConsideration Do Nothing Sue Settle

Loss Absorb loss All or nothing outcome (or settle)

Partial recovery

Future Exposure Absorb future risk Resolve ripe claims only (possibly set precedent)

Resolve past and future claims

Legal Uncertainty No resolution Resolution if litigated to conclusion

Skip resolution of legal claims

Impasse Insurer win Wide range of outcomes (from 0% to 100%)

Narrower range of outcomes (partial recovery)

Example #3: A First Party Loss with Business Interruption Property insurer asserts flood sublimit caps coverage for massive property and

business interruption loss

Underlying loss is very substantial:

• Property damage is $40M

Ongoing/future exposure:

• Business interruption may reach $200M

• Insurer may have institutional commitment to policy interpretation

Legal uncertainty/factual issues:

• Flood sublimit

• Expect line-item disputes over property damage loss

• Expect disputes over quantum of covered business interruption loss

Impasse:

• Insurer is willing to pay $5M of $240M loss

Example #3: First Party Loss OptionsConsideration Do Nothing Sue Settle

Loss Absorb loss Win/lose on line-item basis (or settle)

Partial recovery

Future Exposure Absorb future risk Win/lose (or settle)

Partial recovery

Legal Uncertainty No resolution Resolution if litigated to conclusion

Skip resolution of legal claims

Impasse Insurer win Wide range of outcomes (from $5M - $240M)

Narrower range of outcomes (partial recovery)

Section II How to Decide What to Do

Sue or Settle? Deciding how to respond to an insurance dispute requires a balancing of

commercial and legal considerations

• Importance to the company

• Importance to the insurer

• Financial cost of litigation versus settlement

• Cost of litigation versus settlement in corporate time and resources

• Securing venue

• The risks and rewards of upping the ante

• The risk of making bad law

• Timing to resolution

• Likelihood of success (uncertainty of the merits)

• Publicity

How to you balance your thinking about these factors?

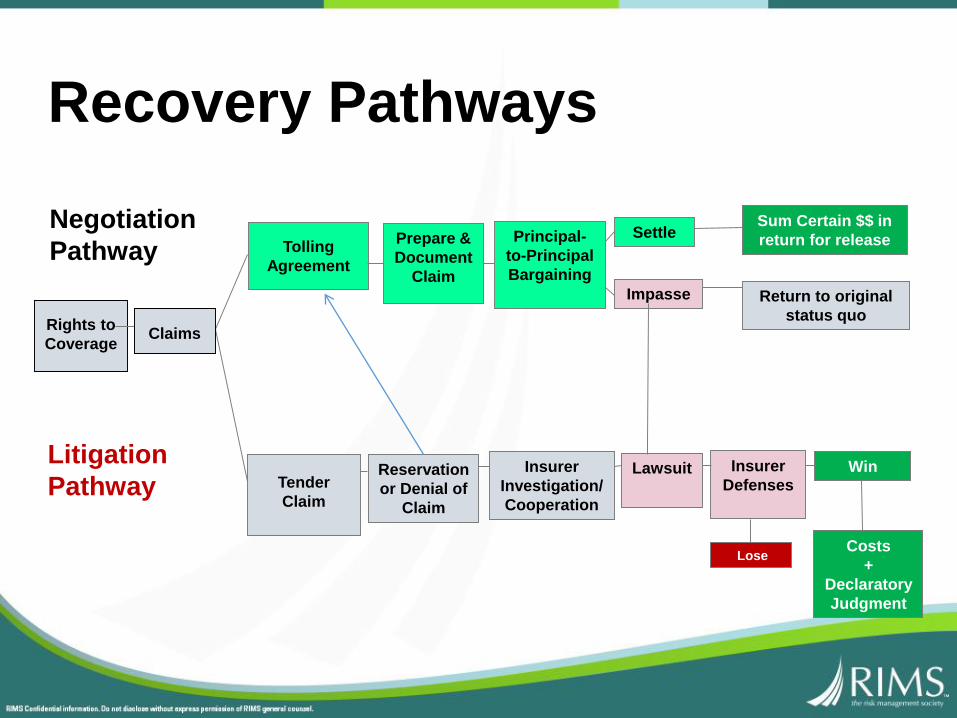

Recovery Pathways

Rights to

Coverage

Tolling

Agreement

Prepare &

Document

Claim

Principal-

to-Principal

Bargaining

Settle

Impasse

Sum Certain $$ in

return for release

Tender

Claim

Reservation

or Denial of

Claim

Insurer

Investigation/

Cooperation

Lawsuit Insurer

Defenses

Return to original

status quo

Lose

Win

Costs

+

Declaratory

Judgment

Negotiation

Pathway

Litigation

Pathway

Claims

Litigation Pathway

Pros Cons

May be necessary to vindicate importance

to company

Institutional importance to insurer may

prolong litigation

Holds open chance of winning “top dollar” May lead to no recovery

Increases pressure on insurers Expensive – may lead to net loss

In multi-jurisdiction case, may secure most

favorable forum

In cases involving large “future cost”

component, victory may be only partial: $

+ declaratory judgment

Allows discovery of insurer data that may

support coverage

Potential corporate disruption—discovery,

litigation holds, depositions

May leader to higher $ settlement Once begun, often difficult to settle

In multi-insurer cases, a strategic goal is to

“peal off” early settlers to increase

pressure on remaining insurers

In multi-insurer cases, insurers enjoy

advantage of sharing litigation costs

Litigation Pathway: When May It Make Sense?

When forum-selection may be case-dispositive

When upside potential greatly exceeds litigation cost

When upside potential exceeds coverage risk

When upside potential is worth a significant investment of corporate time and resources

When claim facts are manageable (discrete facts, few corporate witnesses)

When only one or two insurers are involved to bear costs

When early disposition of one or two issues may increase claim value

When court disposition of legal question is a pressure point

When insurer will not compromise

Negotiation Pathway

Pros Cons

Allows company to monetize uncertain

claims at “fair” value—avoiding risk of no

recovery

Cannot achieve “top dollar”

Shorter cycle time to resolution Insurer may abuse process to delay

resolution

Less demand on corporate resources Less pressure on insurer

In some complex cases, allows liquidation

of both past a future losses without

multiple litigation

May require surrender of future coverage

rights

Conducted on an orderly, confidential basis

with set meetings at agreed times

Lack of access to the insurer’s “black box”

Lower cost, more adaptable to alternative

fee structures

Imposes less pain on insurer, too

In multi-insurer cases, reverses insurers’

economic advantages in litigation

In multi-jurisdiction case, fails to secure

choice of forum

Negotiation Pathway: When May It Make Sense?

When risk of “no recovery” is unacceptable

When litigation cost may be disproportionate to upside potential

When coverage risk is high—applicable law is uncertain

When management of corporate resources dictates

When claim facts are very complex or uncertain (multiple claims and witnesses, unknown or old facts)

When multiple insurers are involved

When adverse publicity is a concern

When time to recovery is important

A Decision-Analytic MatrixFactor Litigation Settlement

Importance to company May dictate litigation for

cultural reasons

May dictate settlement if

“all/nothing” risk

unacceptable

Likelihood of success Favored if likelihood of

success is high

Favored if legal or factual risk

is high

Cost Very costly Less costly

Resources More resources required Less required—but not none!

Time Usually takes longer Favored if time to resolution

is important

Pressure on insurer Places more immediate

pressure on insurer

Less pressure—but can sue

later

Securing a forum Requires litigation Standstill & Tolling Preserves

both parties’ opportunities

Economic pressure More on policyholder More on insurers (in multi-

insurer cases)

Using Decision Analysis:$10M D&O Case

Likelihood Value

Forum?Subpoena

Covered?

75% 60% 6,000,000 Chance of80% Recovery

25% 20% zeroChance ofNo Recovery

50% 10% 1,000,000 20% Years to

50% 10% zero Recovery

100% 7,000,000 2% Interest Rate

Expenses (2,000,000)

Nominal Net Value 5,000,000 PV 4,711,612

90% Chance of90% 4,500,000 Recovery

Chance ofNo Recovery

10% 10% zeroYears to

100% 4,500,000 Recovery

Expenses (500,000) 2% Interest Rate

Nominal Net Value 4,000,000 PV 3,921,569

Issues

90%

10%

1

Branch Outcomes Final Outcomes

70%

30%

3

LITIGATE

Win: Illinois

Lose: New York

Win: Yes

Lose: No

Win: Yes

Lose: No

NEGOTIATE

Succeed: NegotiatedSettlement at 50% of

Incurred Costs

Fail: Move to Litigation

Decision Analysis: $100M Environmental Claim

Likelihood Value

Forum?As

Damages?

Pollution

ExclusionAllocation

100% 64.00% 64,000,000 80%

0% Chance of100% Recovery

80% 20%

0% 16.00% zero Chance ofNo Recovery

0% 0.00% zero20% Years to

100% 20.00% zero Recovery

100% 64,000,000 2% Interest Rate

Expenses (5,000,000)

Nominal Net Value 59,000,000 PV 53,438,118

Chance of90% Recovery

90% 49,500,000 Chance ofNo Recovery

10% 10% zeroYears to

100% 49,500,000 Recovery

Expenses (2,000,000) 2% Interest Rate

Nominal Net Value 47,500,000 PV 46,109,812

Branch Outcomes Final Outcomes

64.00%

36.00%

Issues

5

90%

10%

1.5

LITIGATE

Win: Washington

Lose: California

Win

Lose

Lose

NEGOTIATE

Fail: Move to Litigation

Win

Lose

Win

Lose

Win

Discount for General Coverage

Defense: 25%

Succeed: Overall discount of 55%(1-0.4)*(1-0.25)=0.45

Discount for Pollution

Exclusion: 40%= +

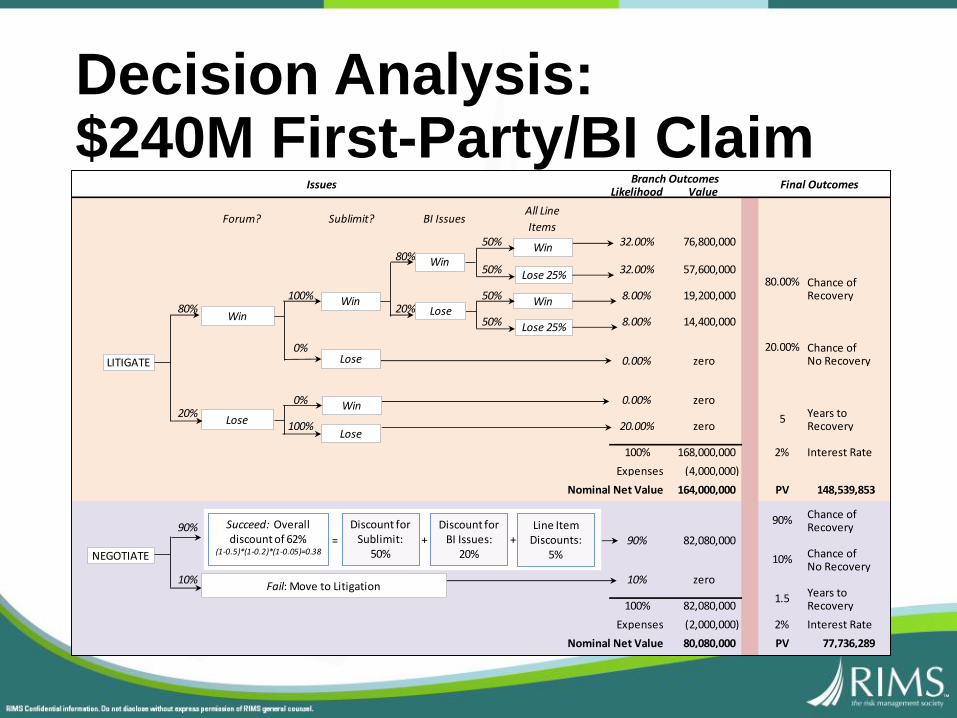

Decision Analysis:$240M First-Party/BI Claim

Likelihood Value

Forum? Sublimit? BI IssuesAll Line

Items50% 32.00% 76,800,000

80%50% 32.00% 57,600,000

Chance of100% 50% 8.00% 19,200,000 Recovery

80% 20%50% 8.00% 14,400,000

0% Chance of0.00% zero No Recovery

0% 0.00% zero20% Years to

100% 20.00% zero Recovery

100% 168,000,000 2% Interest Rate

Expenses (4,000,000)

Nominal Net Value 164,000,000 PV 148,539,853

Chance of90% Recovery

90% 82,080,000 Chance ofNo Recovery

10% 10% zeroYears to

100% 82,080,000 Recovery

Expenses (2,000,000) 2% Interest Rate

Nominal Net Value 80,080,000 PV 77,736,289

Issues

10%

1.5

80.00%

90%

Branch Outcomes Final Outcomes

20.00%

5

LITIGATE

Win

Lose

Win

Lose

Lose

Win

Lose

Win

Lose 25%

Win

Win

Lose 25%

NEGOTIATE

Fail: Move to Litigation

Succeed: Overall discount of 62%

(1-0.5)*(1-0.2)*(1-0.05)=0.38

Discount for Sublimit:

50%= +

Discount for BI Issues:

20%

Line Item Discounts:

5%+

Section IIIManaging Litigation and/or

Negotiations

Managing Litigation Open and maintain clear communications with counsel

• Understand their theory of the case—ask questions!

• Understand case status, calendar, and how it affects you

• Set up regular updates

Prepare your company for litigation

• Understand and implement litigation holds

• Depositions and discovery—understand who must participate, the timing, and the resources required

• Understand that your counsel may influence, but cannot control, the calendar—the court’s calendar comes first

• Consider and have a plan to deal with public relations issues

Managing Litigation (cont’d)

Managing costs

• Have counsel prepare a budget showing expected and potential tasks, professionals providing services, rates and expected timeline

• Counsel should explain contingencies that may change the budget and what effect those contingencies could have

• In regular meetings with counsel, set aside time to track performance against budget, discuss developments that may increase costs, and consider approaches that may introduce efficiencies

• Your budget seldom includes the impact of stays, expansive discovery orders, and appeals, all of which can blow the budget

• Expect the unexpected—build a contingency into your budget

Managing Negotiations Like litigation, negotiations have to be managed to minimize

costs and maximize recovery

The key is preparation

• Marshal available data—thoroughly (leverage informational advantages over insurers)

• Analyze facts and law

• Come to a realistic internal assessment of strengths and weaknesses

• Set realistic financial goals before negotiations

Create a space where negotiating is “safe” for both sides

• Standstill and tolling agreements

• Confidentiality

• Make your case—credibly and diplomatically—while acknowledging risk

• Understand insurer needs (information, reinsurance, avoiding adverse precedents)

Managing Negotiations (cont’d)

• Negotiate with intermediaries, not through them

• Your participation represents corporate buy-in and authority—don’t just speak “through counsel”

• Insist on participating in strategic decisions with your counsel

• Rely on mediators for information about your case—but remember who your counsel is

• Maintain litigation option

• The other side needs to see you have counsel capable of bringing suit

• The other side needs to know your counsel has done his homework just as if litigation were a step away

• But no need to threaten litigation explicitly (especially if you don’t mean it)

• And the corollary: Don’t sue unless you are prepared to see litigation through to the end

Managing Negotiations (cont’d)

Managing Costs

• Discuss at the outset with your counsel

• Set specific expectations, budgets and targets

• Take a phased approach and measure costs against pre-determined milestones

• Maintain communications with counsel at regular intervals

• Explore alternative fee options

Take-Aways Avoid disputes - understand your coverage and negotiate up front,

also choose your counterparties carefully

Identify potential disputes early and work with the broker and/or

underwriter before formally tendering the claim

Understand the tangibles and intangibles of the dispute and look

for ways around a logjam

Evaluate the potential outcomes and set reasonable internal

expectations

Don’t assume litigation is the only answer—explore the pros and

cons of a negotiated alternative

Consider decision analytic tools—and professional advice—in

exploring the value of litigation and settlement alternatives

![Chapter 23 SETTLING INSURANCE COVERAGE DISPUTES · VALUING THE COVERAGE CLAIM FOR PURPOSES OF SETTLEMENT ... 23.05[1] Settlements May Include Any or All Known and Unknown Policies](https://static.fdocuments.in/doc/165x107/5f92e9160a1bca1a0f0fa66e/chapter-23-settling-insurance-coverage-valuing-the-coverage-claim-for-purposes-of.jpg)