Subsumationinto Dual GST€¦ · 6.Invoice Value if full input tax credit available to the...

50

Transcript of Subsumationinto Dual GST€¦ · 6.Invoice Value if full input tax credit available to the...

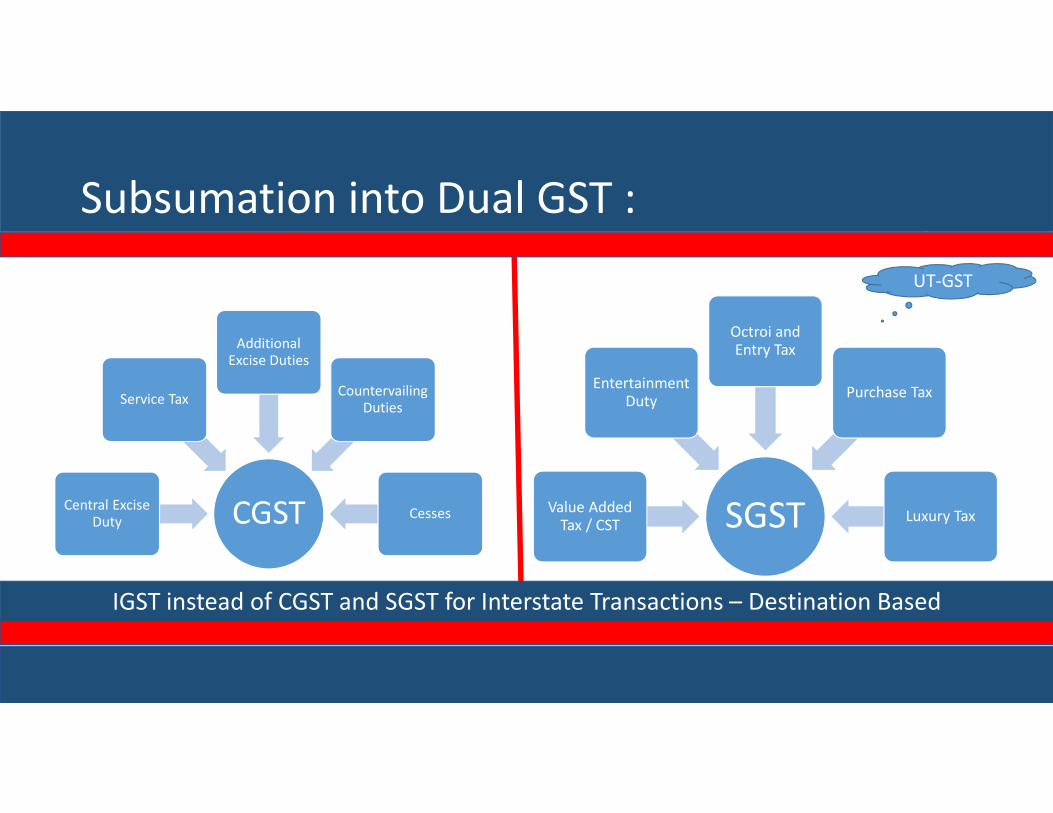

Subsumation into Dual GST :

CGSTCentral Excise Duty

Service Tax

Additional Excise Duties

Countervailing Duties

Cesses SGSTValue Added Tax / CST

Entertainment Duty

Octroi and Entry Tax

Purchase Tax

Luxury Tax

IGST instead of CGST and SGST for Interstate Transactions – Destination Based

UT-GST

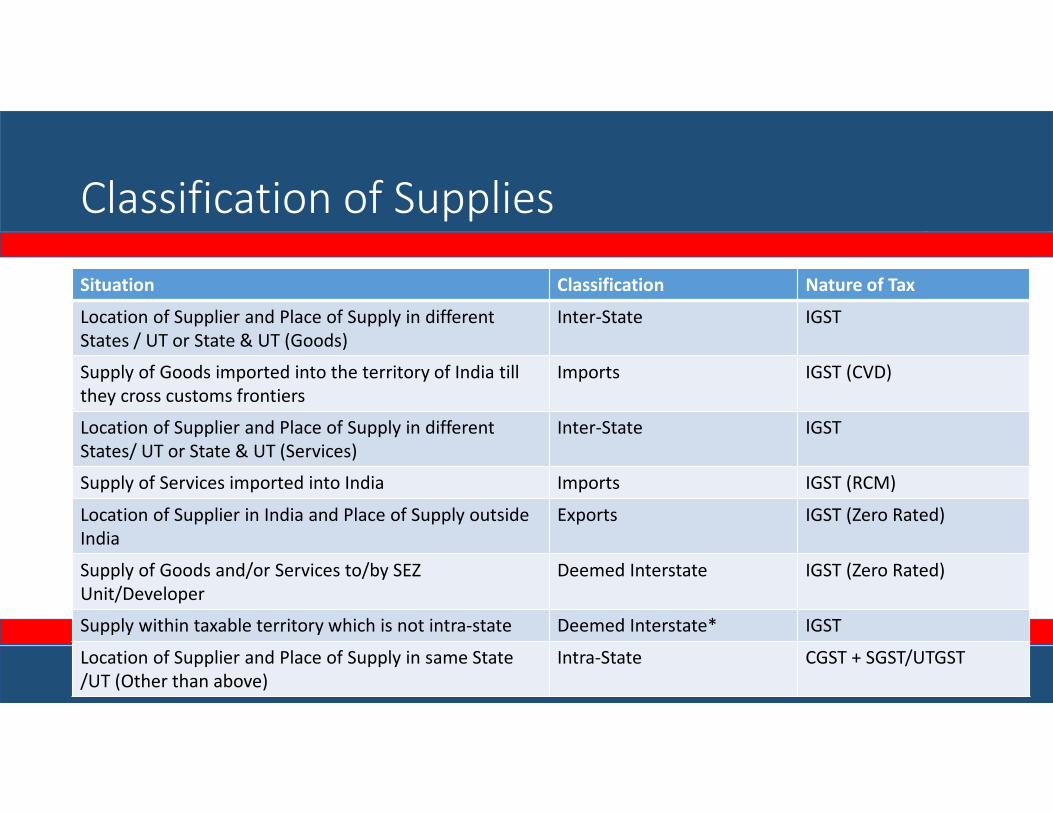

Classification of Supplies

Situation Classification Nature of Tax

Location of Supplier and Place of Supply in different

States / UT or State & UT (Goods)

Inter-State IGST

Supply of Goods imported into the territory of India till

they cross customs frontiers

Imports IGST (CVD)

Location of Supplier and Place of Supply in different

States/ UT or State & UT (Services)

Inter-State IGST

Supply of Services imported into India Imports IGST (RCM)

Location of Supplier in India and Place of Supply outside

India

Exports IGST (Zero Rated)

Supply of Goods and/or Services to/by SEZ

Unit/Developer

Deemed Interstate IGST (Zero Rated)

Supply within taxable territory which is not intra-state Deemed Interstate* IGST

Location of Supplier and Place of Supply in same State

/UT (Other than above)

Intra-State CGST + SGST/UTGST

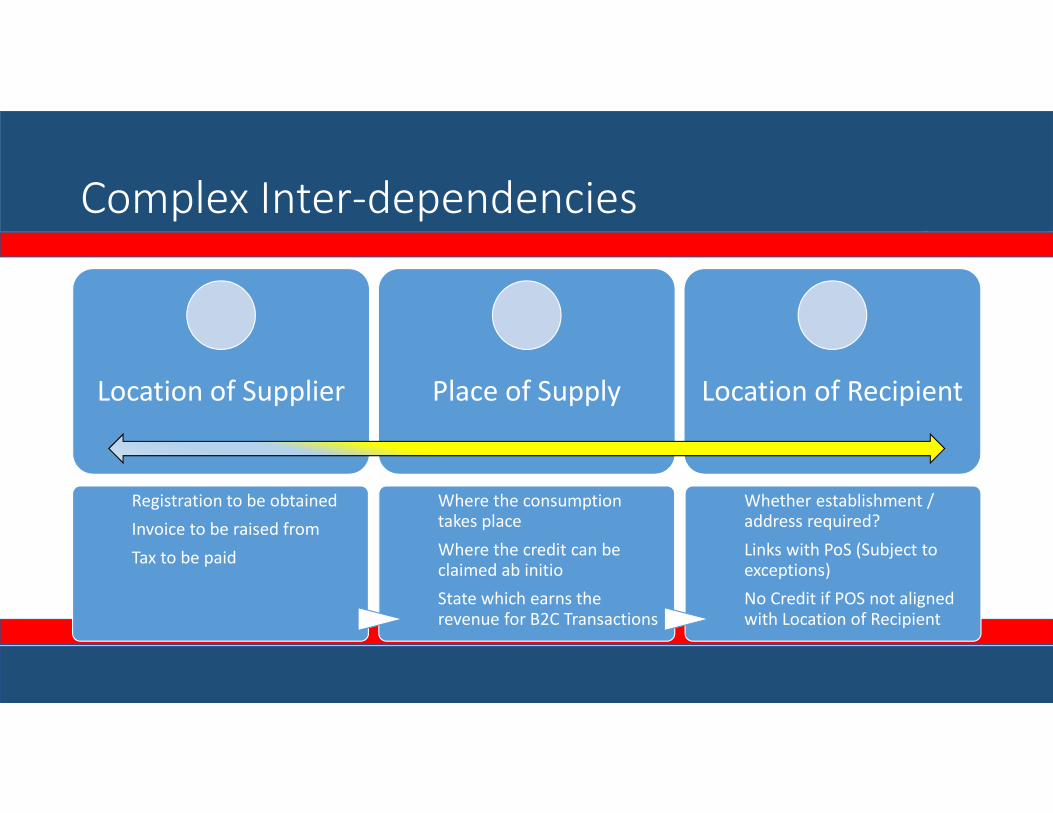

Complex Inter-dependencies

Location of Supplier Place of Supply Location of Recipient

Registration to be obtained

Invoice to be raised from

Tax to be paid

Where the consumption takes place

Where the credit can be claimed ab initio

State which earns the revenue for B2C Transactions

Whether establishment / address required?

Links with PoS (Subject to exceptions)

No Credit if POS not aligned with Location of Recipient

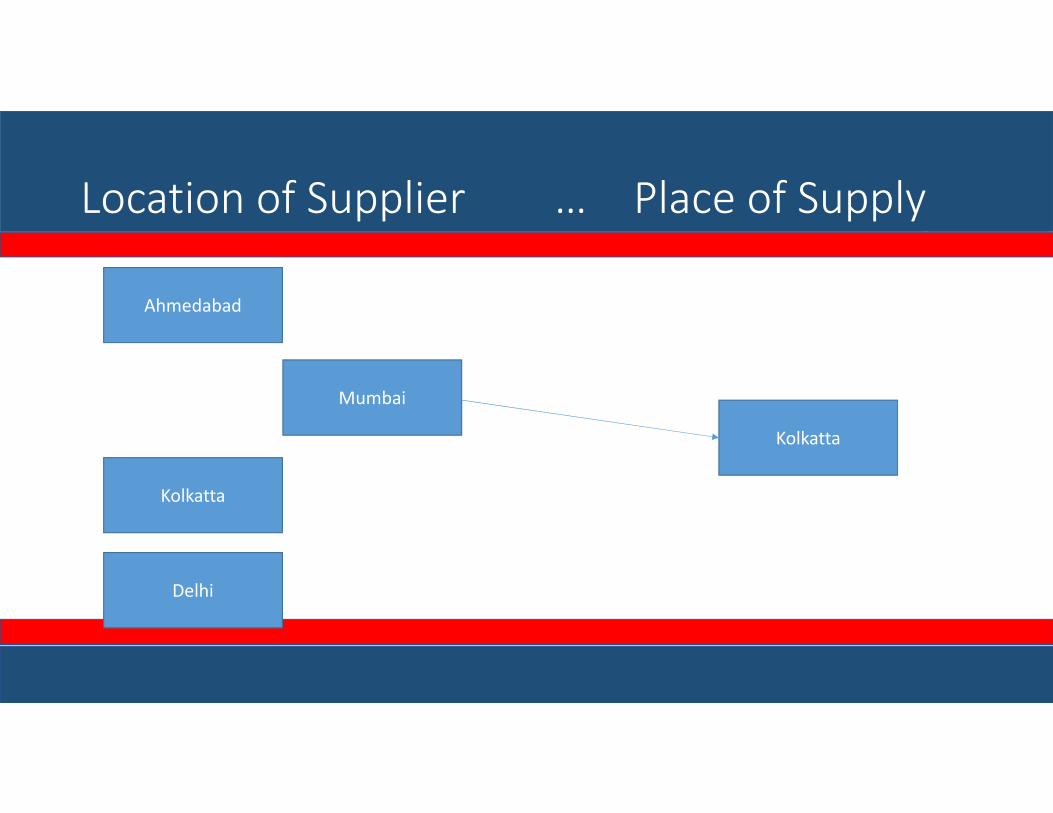

Location of Supplier – Case Study

• CA firm has head office in Mumbai and branch offices in Ahmedabadand Delhi. The Mumbai office has entered into an audit engagementwith a client located in Kolkatta. The junior members for theengagement will be deputed from Ahmedabad branch office to theclient location in Kolkatta. The audit report will be reviewed by seniormembers located in Mumbai and ultimately signed off by an auditpartner located in Delhi.

• What is the location of supplier?

Location of Supplier … Place of Supply

Ahmedabad

Mumbai

Kolkatta

Delhi

Kolkatta

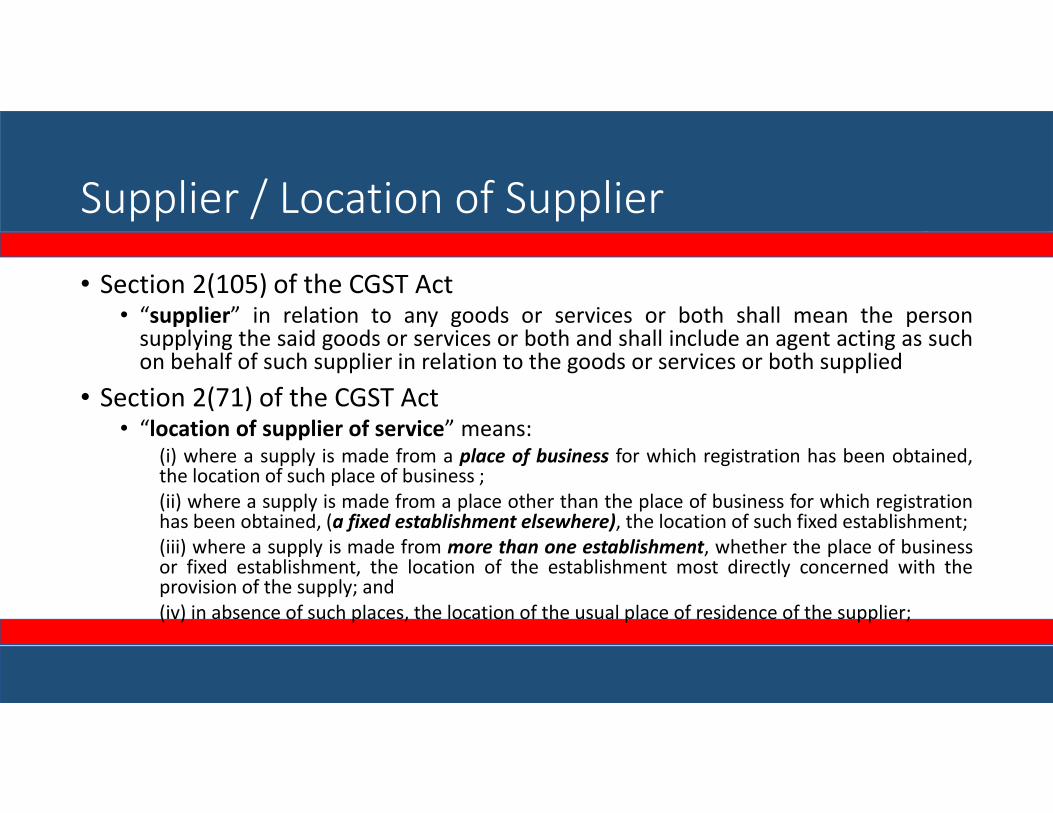

Supplier / Location of Supplier

• Section 2(105) of the CGST Act• “supplier” in relation to any goods or services or both shall mean the person

supplying the said goods or services or both and shall include an agent acting as suchon behalf of such supplier in relation to the goods or services or both supplied

• Section 2(71) of the CGST Act• “location of supplier of service” means:

(i) where a supply is made from a place of business for which registration has been obtained,the location of such place of business ;

(ii) where a supply is made from a place other than the place of business for which registrationhas been obtained, (a fixed establishment elsewhere), the location of such fixed establishment;

(iii) where a supply is made from more than one establishment, whether the place of businessor fixed establishment, the location of the establishment most directly concerned with theprovision of the supply; and

(iv) in absence of such places, the location of the usual place of residence of the supplier;

Some Related Definitions…

• Fixed Establishment – Section 2(50)• “fixed establishment” means a place (other than the registered place of

business) which is characterised by a sufficient degree of permanence andsuitable structure in terms of human and technical resources to supplyservices, or to receive and use services for its own needs;

• Place of Business – Section 2(85)• place of business” includes

(a) a place from where the business is ordinarily carried on, and includes a warehouse, agodown or any other place where a taxable person stores his goods, supplies or receivesgoods or services or both; or

(b) a place where a taxable person maintains his books of account; or

(c) a place where a taxable person is engaged in business through an agent, by whatevername called;

Location of Supplier … Place of Supply

Ahmedabad

Mumbai

Kolkatta

Delhi

Kolkatta

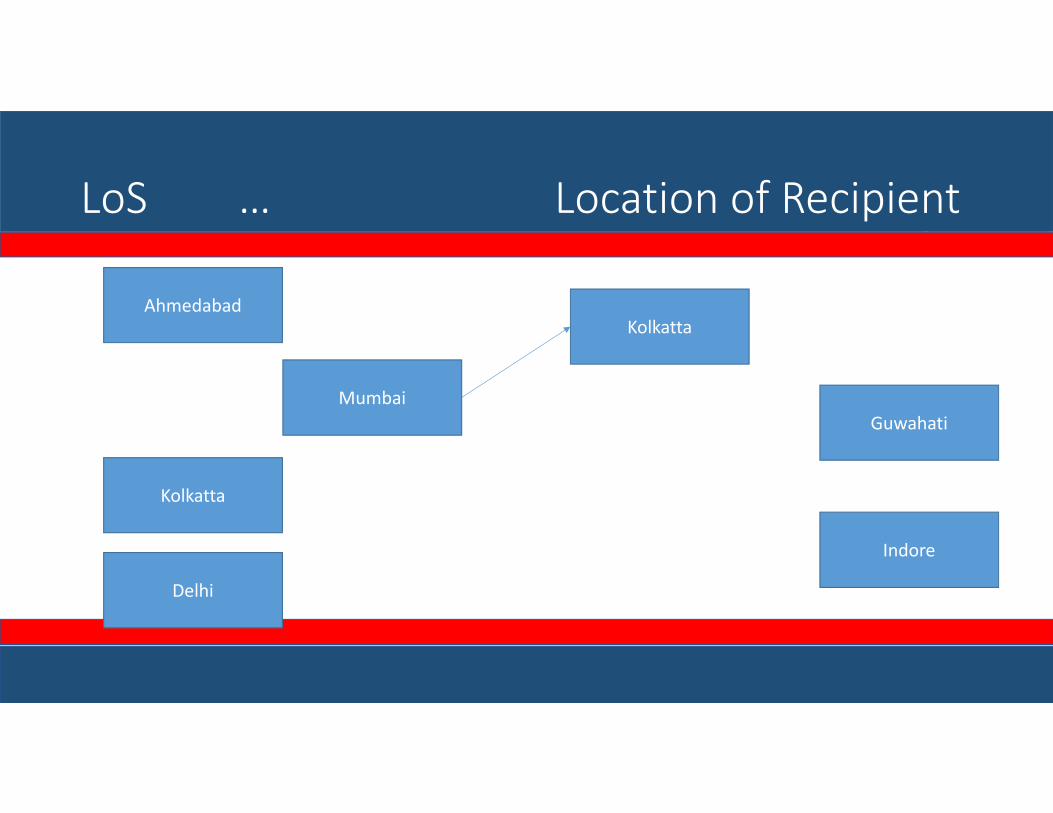

Location of Recipient – Case Study

• In the earlier example, the client has corporate office in Kolkatta,factory in Guwahati and registered office is located in Indore

• What is the location of recipient?

LoS … Location of Recipient

Ahmedabad

Mumbai

Kolkatta

Delhi

Kolkatta

Guwahati

Indore

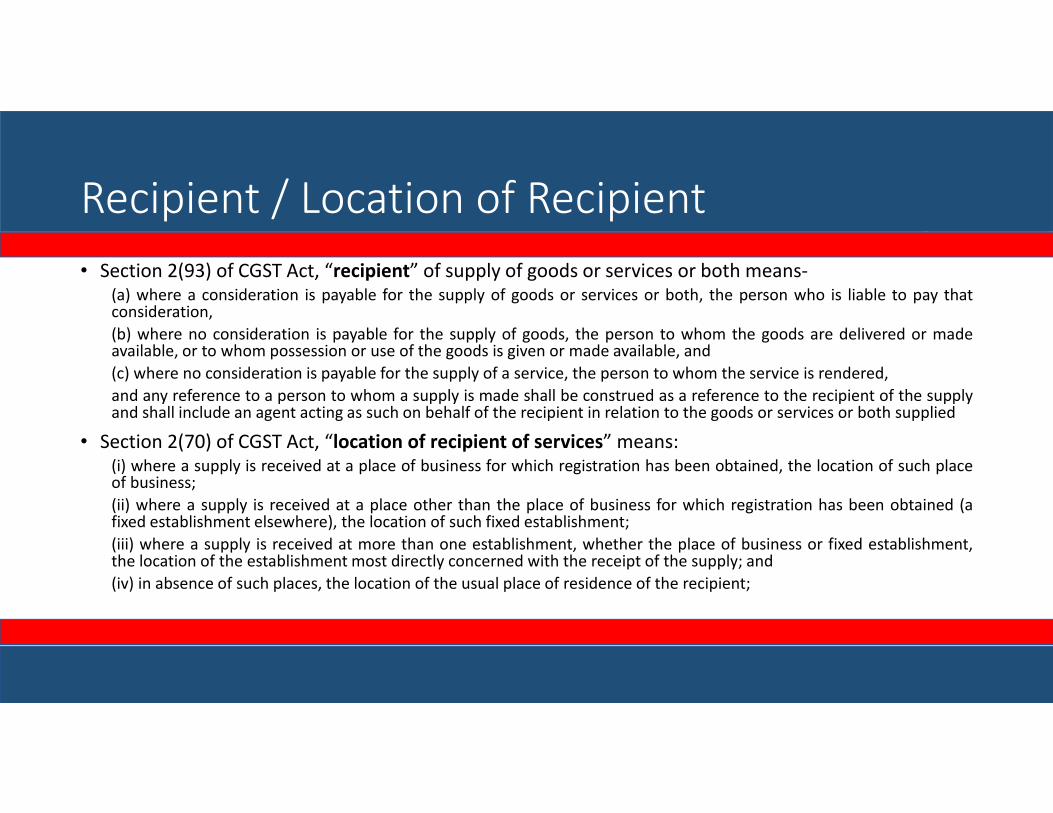

Recipient / Location of Recipient

• Section 2(93) of CGST Act, “recipient” of supply of goods or services or both means-(a) where a consideration is payable for the supply of goods or services or both, the person who is liable to pay thatconsideration,

(b) where no consideration is payable for the supply of goods, the person to whom the goods are delivered or madeavailable, or to whom possession or use of the goods is given or made available, and

(c) where no consideration is payable for the supply of a service, the person to whom the service is rendered,

and any reference to a person to whom a supply is made shall be construed as a reference to the recipient of the supplyand shall include an agent acting as such on behalf of the recipient in relation to the goods or services or both supplied

• Section 2(70) of CGST Act, “location of recipient of services” means:(i) where a supply is received at a place of business for which registration has been obtained, the location of such placeof business;

(ii) where a supply is received at a place other than the place of business for which registration has been obtained (afixed establishment elsewhere), the location of such fixed establishment;

(iii) where a supply is received at more than one establishment, whether the place of business or fixed establishment,the location of the establishment most directly concerned with the receipt of the supply; and

(iv) in absence of such places, the location of the usual place of residence of the recipient;

LoS … Location of Recipient

Ahmedabad

Mumbai

Kolkatta

Delhi

Kolkatta

Guwahati

Indore

State Specific Law: Fallout for service providers

Registration Numbers

Output TaxInput Tax

CreditRCM Tax

Invoice SeriesPayment &

ReturnsTrial Balances

Audits &Assessments

Concept of Supply

• GST is applicable on all forms of supplies of goods or servicesfor a consideration

• It includes deemed supplies (even without consideration)

• Free Supplies to related persons

• Interstate branch transfers

• Goods {Raw Materials, Finished Goods, Capital Assets, Collaterals, etc.}

• Services {Income / Expenses}

• Supplies of goods by Principal to Agents & vice – versa

Supply of Services across branches : Case Study

Ahmedabad

Mumbai

Kolkatta

Delhi

Kolkatta

Guwahati

Indore

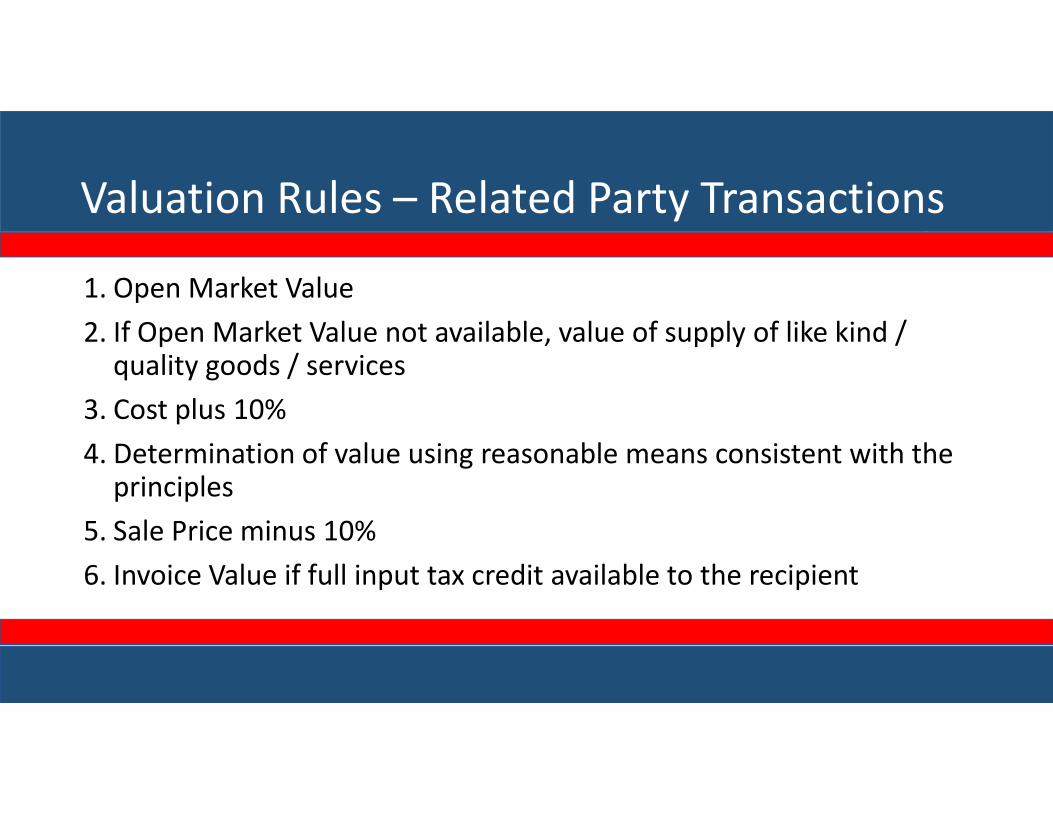

Valuation Rules – Related Party Transactions

1. Open Market Value

2. If Open Market Value not available, value of supply of like kind / quality goods / services

3. Cost plus 10%

4. Determination of value using reasonable means consistent with the principles

5. Sale Price minus 10%

6. Invoice Value if full input tax credit available to the recipient

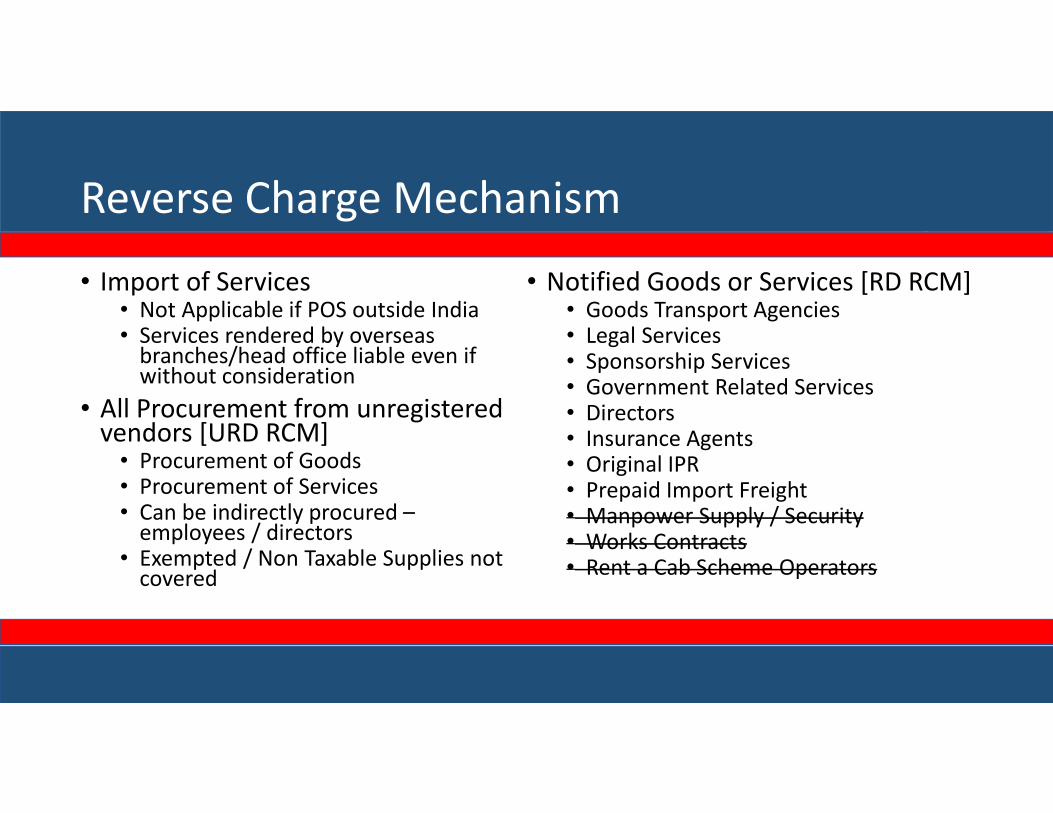

Reverse Charge Mechanism

• Import of Services• Not Applicable if POS outside India• Services rendered by overseas

branches/head office liable even if without consideration

• All Procurement from unregistered vendors [URD RCM]

• Procurement of Goods• Procurement of Services• Can be indirectly procured –

employees / directors• Exempted / Non Taxable Supplies not

covered

• Notified Goods or Services [RD RCM]• Goods Transport Agencies• Legal Services• Sponsorship Services• Government Related Services• Directors• Insurance Agents• Original IPR• Prepaid Import Freight• Manpower Supply / Security• Works Contracts• Rent a Cab Scheme Operators

RCM – Some Examples

• Refreshment Costs - Taxable

• Conveyance Costs – Mostly Exempted / Registered

• Printing and Stationery – Taxable

• Minor Repairs & Maintenance – Taxable

• Miscellaneous Expenses – Taxable

• Apprentices – Pseudo Employment??

• Payments to CPE Study Circles – Whether Exempted ??

RCM – Compliance Requirements

• Raise a Self Generated Invoice at the time of receiving the services

• Issue a Payment Voucher at the time of making the payment

• Upload the details on GST Portal (invoice wise) at the time of payment

• If the payment is within 60 days, TOS is the date of payment

• Claim Credit if eligible

Rate of Tax & Classification

• Rate of Tax

• 0 – 5 – 12 – 18 – 28 + CESS

• HSN/SAC Classification Important

Sr. No. Service Code Service Description

1. 997156 Financial Consultancy Services

2. 998221 Financial Auditing Services

3. 998222 Accounting and Bookkeeping Services

4. 998231 Corporate Tax Consulting and Preparation Services

5. 998232 Individual Tax Preparation and Planning services

6. 998311 Management Consulting Services

7. 999293 Commercial Training and Coaching Services

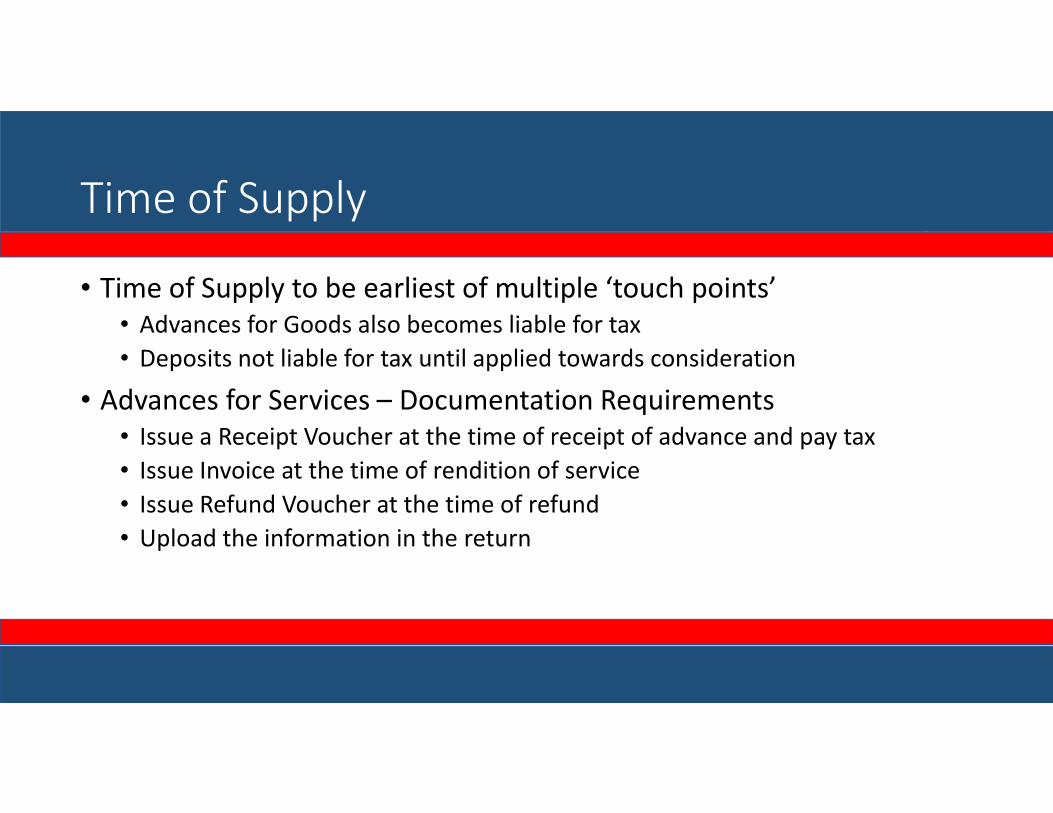

Time of Supply

• Time of Supply to be earliest of multiple ‘touch points’

• Advances for Goods also becomes liable for tax

• Deposits not liable for tax until applied towards consideration

• Advances for Services – Documentation Requirements

• Issue a Receipt Voucher at the time of receipt of advance and pay tax

• Issue Invoice at the time of rendition of service

• Issue Refund Voucher at the time of refund

• Upload the information in the return

Small Professionals : Impact

• Facility of payment of tax on receipt basis for small professionals no longer exists

• Moving Forward

• Will need to discharge tax at the time of invoicing or completion of service

• Need for discipline in raising invoices

• No adjustment on account of bad debts

• Need for ensuring proper engagement letters and pre-decision on fees

• Credit Notes for non provision/deficiency of services

• Transition

• Service Tax will be payable as and when amounts are realized

Valuation

• Value is generally the transaction value

• Arms’ Length Pricing in case of Related Parties

• Can you provide PRO BONO Services to relatives ?

• Role of Credit Notes

• Non Provision of Service / Deficiency in provision of Service

• Subject to acceptance by the recipient of service on GST Portal

• Has to be issued by September of next financial year

Exemptions

• Threshold of Rs. 20 lakhs / 10 lakhs*

• Exemption not applicable if registered

• Auto Migrated Assessees need to apply for cancellation if they do not intend to continue (within 30 days)

• Not applicable if engaged in

• Interstate Supply

• Optional Composition Scheme upto Rs. 75lakhs (not for service providers)

IGST : Domestic Place of Supply Rules

• PoS Rule for Services

• General Rule - Destination Principle – Classification as B2B vs. B2C important

• Exceptions – Source and Hybrid Principles

• Impact on Claim of Credit in B2B Cases

• Hotel Stay for Travel at Client Locations

Input Credit – Essential Conditions

You should receive

Goods/ Services

Tax Invoice

Pay the vendor within 180 days

Vendor should

Have Paid the tax

Have uploaded the tax to the customers account

Credit should not be

Blocked

Subject to apportionment

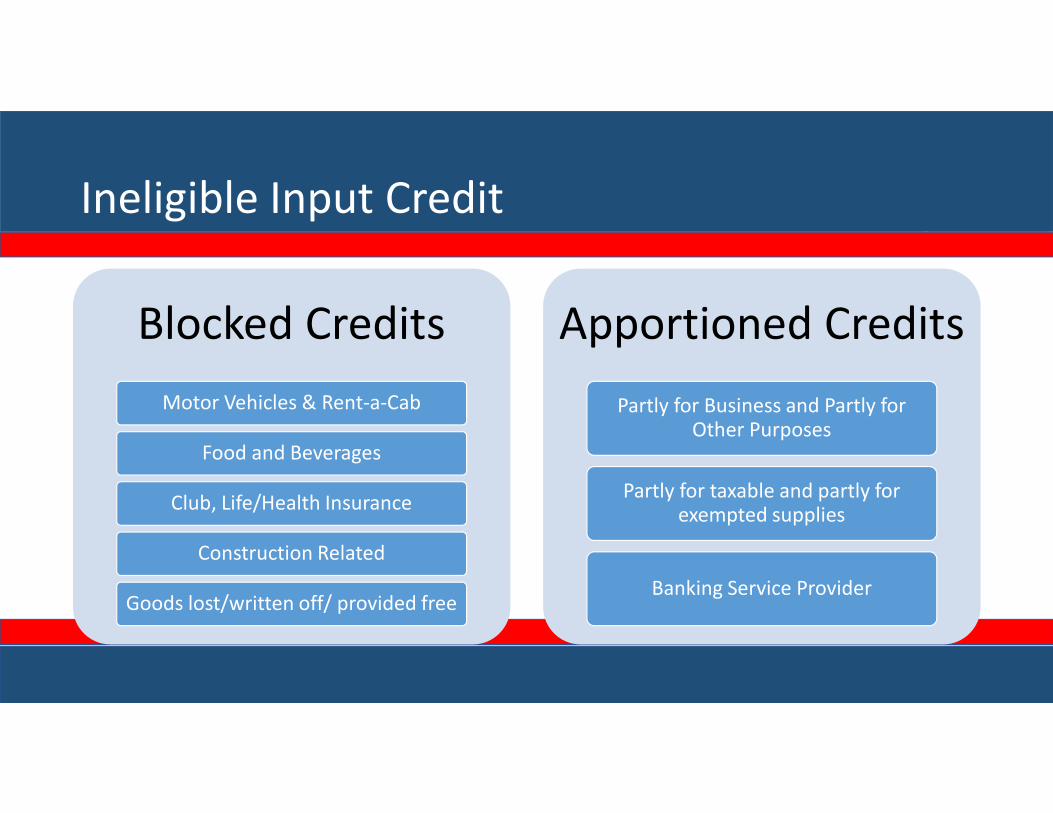

Ineligible Input Credit

Blocked Credits

Motor Vehicles & Rent-a-Cab

Food and Beverages

Club, Life/Health Insurance

Construction Related

Goods lost/written off/ provided free

Apportioned Credits

Partly for Business and Partly for Other Purposes

Partly for taxable and partly for exempted supplies

Banking Service Provider

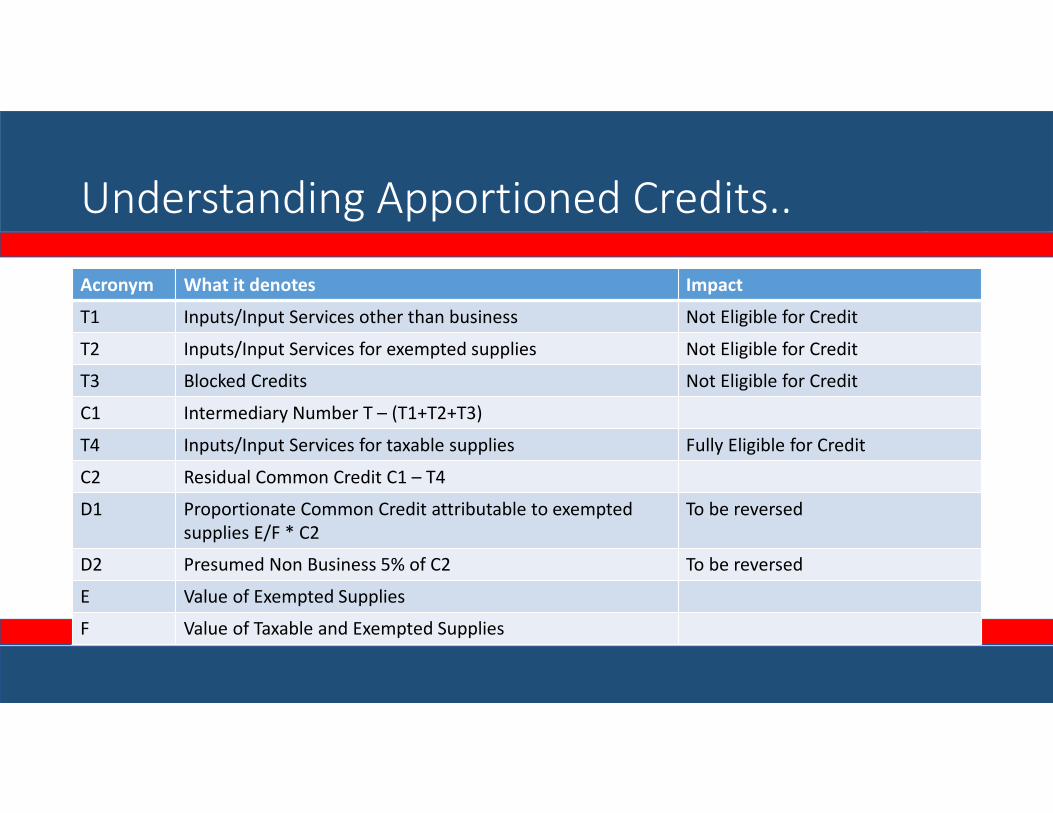

Understanding Apportioned Credits..

Acronym What it denotes Impact

T1 Inputs/Input Services other than business Not Eligible for Credit

T2 Inputs/Input Services for exempted supplies Not Eligible for Credit

T3 Blocked Credits Not Eligible for Credit

C1 Intermediary Number T – (T1+T2+T3)

T4 Inputs/Input Services for taxable supplies Fully Eligible for Credit

C2 Residual Common Credit C1 – T4

D1 Proportionate Common Credit attributable to exempted

supplies E/F * C2

To be reversed

D2 Presumed Non Business 5% of C2 To be reversed

E Value of Exempted Supplies

F Value of Taxable and Exempted Supplies

Monthly Return Filing Process

GSTR-1: Details of Outward supplies of goods and/or services

GSTR 1: Details

of Outward

supplies

Step 1

GSTR 2A: Auto-

populated in

GSTR-2A of

recipients

Step 2

GSTR 2: On the basis of

above GSTR-2A, details

of inward supplies

added, corrected or

deleted by recipient to

be disclosed under

GSTR-2, including URD-

RCM details

Step 3

GSTR-1A : The details of inward

supplies added, corrected or

deleted by the recipient shall be

made available to the supplier

Step 410

11

15

16

Supplier will accept or

reject the modifications

Step 5

17

GSTR-1 will be amended

to the extent

modifications are

accepted by supplier.

Step 617

GSTR 3

Step 8

Part A of GSTR 3

Part A of GSTR 3

20

Make

Payment

Step 7

20

Part B of

GSTR 3

Monthly Return Process : Caveats

• No Revised Return permitted

• Rectifications permitted

• In the same cycle only if sponsored by the recipient

• Only in the subsequent cycle if unmatched by the recipient

• Not permitted for matched transactions – Section 37(3)

• Locking of GSTR1 between 10th and 15th – Proviso to Section 37(1)

• Understanding the broad contents…

Broad Contents of GSTR Returns

• GSTR1 : Outward Supplies

• B2B – Line Level Upload

• B2CIL – Line Level Upload

• Others – Aggregate Upload (Rate/POS)

• GSTR2 – Inward Supplies

• B2B (RD) including RD_RCM – Line Level Upload (Matching Process)

• B2B (URD_RCM) – Line Level Upload (Entry Process)

• Others - Aggregate

GSTR1

4. B2B

5. B2CIL

6. Zero Rated

7. B2CS (Net of CN)

8. Nil/Exempt/Non GST

9. Amendments (incl CN) 4-5-6

10. Amendments 7

11. Advances

12. Document Summary

13. HSN Summary

GSTR2

3. B2B

4. RCM

5. Imports

6. Amendments

7. Composition/Exempt/Non GST

8. ISD Credit

9. TDS/TCS Credit

10. Advance RCM

11. ITC Reversal/Reclaim

12. Output Tax Addition/Reclaim

13. HSN Summary

GSTR3

3. Turnover of outward supplies

4. Breakup of Taxable Outward Supplies

5. RCM

6. Input Tax Credit

7. Output Tax Adjustments

8. Tax Liability (Total)

9-15 Payments and Adjustments

1A 2A

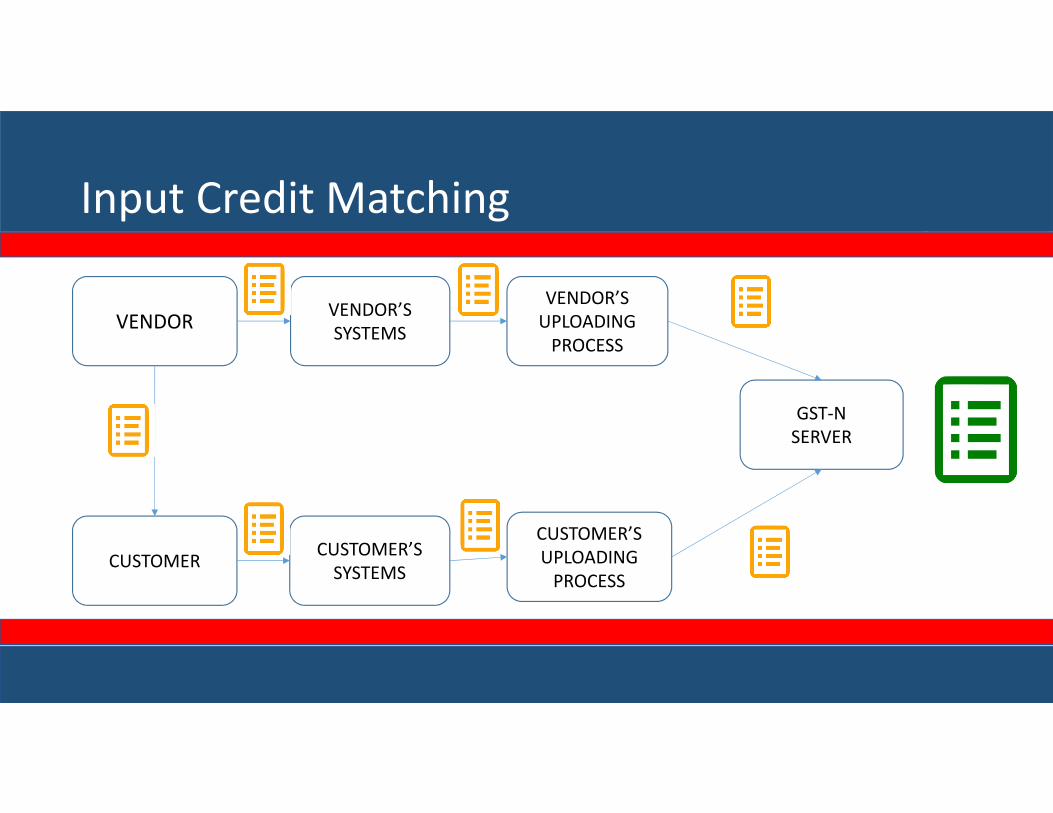

Input Credit Matching

VENDOR

CUSTOMERCUSTOMER’S

SYSTEMS

VENDOR’S

SYSTEMS

VENDOR’S

UPLOADING

PROCESS

CUSTOMER’S

UPLOADING

PROCESS

GST-N

SERVER

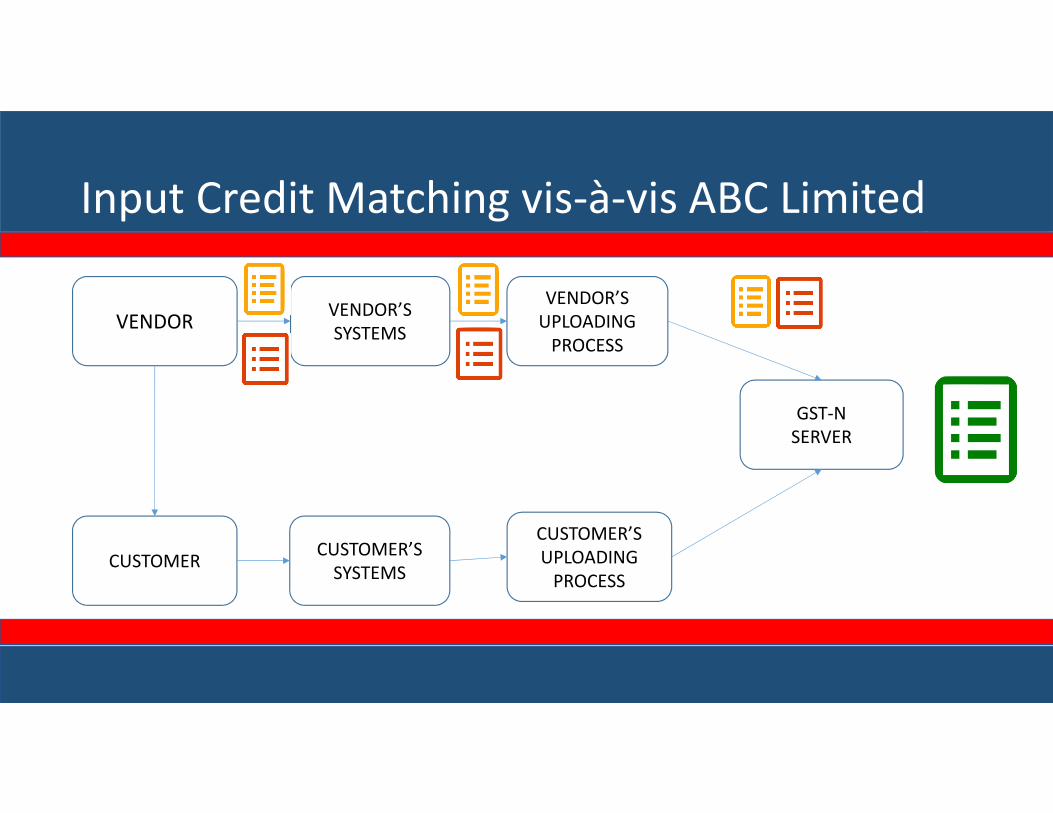

Unilateral Errors and Rectifications..

An invoice 1 is issued in the name of ABC Limited . Immediately on issuance of the invoice, it is realized that the invoice is wrongly issued. But system does not permit cancellation of invoices. So a credit note 1 issued in the name of ABC Limited and another invoice 2 is issued in the name of PQR Limited

• Should Invoice 1 be uploaded?

• Should Credit Note 1 be uploaded?

• Should Invoice 2 be uploaded?

Input Credit Matching vis-à-vis ABC Limited

VENDOR

CUSTOMERCUSTOMER’S

SYSTEMS

VENDOR’S

SYSTEMS

VENDOR’S

UPLOADING

PROCESS

CUSTOMER’S

UPLOADING

PROCESS

GST-N

SERVER

No Clarity on Place of Supply

An invoice 1 is issued in the name of ABC Limited, Mumbai on 20-July instead of ABC Limited, Delhi. ABC Limited, Delhi does not see invoice 1 in its’ GSTR2A so self claims the credit. When the invoice is reflected in GSTR1A, it is realized that there was an error. The error is accepted in GSTR 1A. In accounts, a credit note 1 issued in the name of ABC Limited, Mumbai and another invoice 2 is issued in the name of ABC Limited, Delhi.

• Invoice 1 was already uploaded in favour of ABC Limited, Mumbai

• Through GSTR1A, the invoice is accepted (through rectification mode) for ABC Limited, Delhi

• Should Credit Note 1 be uploaded

• Should Invoice 2 be uploaded

• What happens if inadvertently ABC Limited, Mumbai accepts the transaction

Invoices : Care to take…

• Unilateral Errors and Cancellations

• Error Resolution through GSTR1A

• Already matched erroneous invoices on GSTR Portal

• Incorrect tagging / non tagging of RCM

• Wrong Amounts populated

• Delayed identification of B2B Nature of transaction

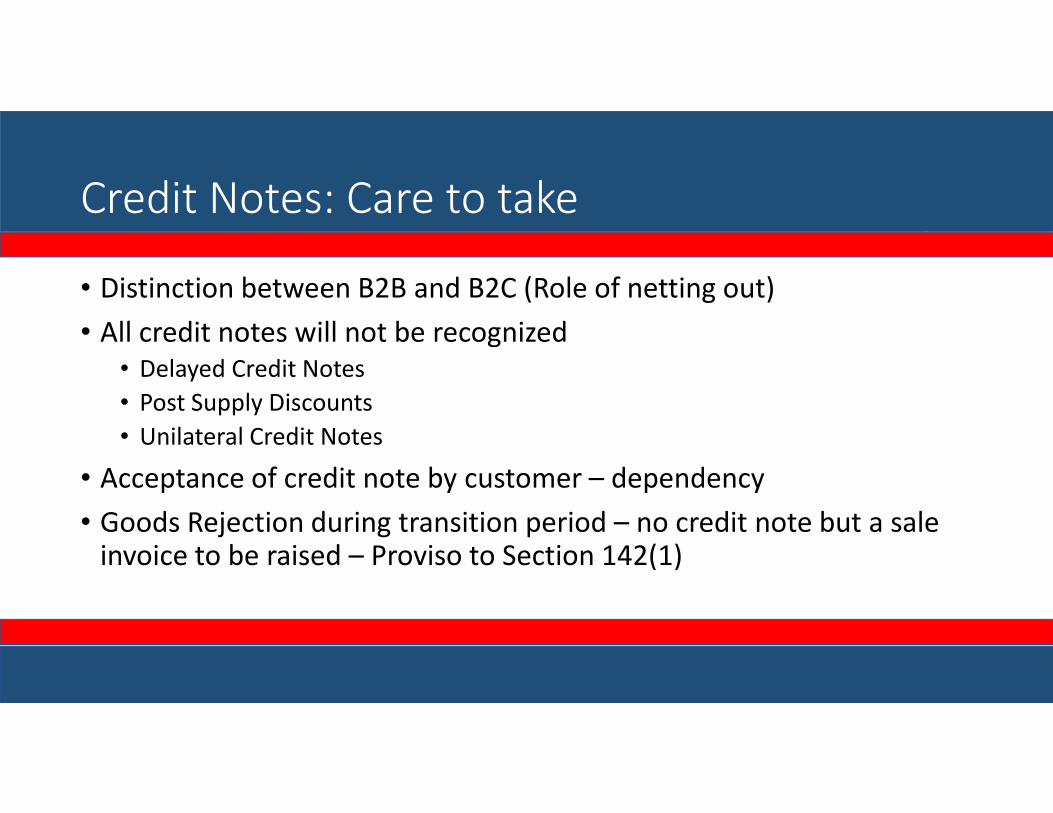

Credit Notes: Care to take

• Distinction between B2B and B2C (Role of netting out)

• All credit notes will not be recognized

• Delayed Credit Notes

• Post Supply Discounts

• Unilateral Credit Notes

• Acceptance of credit note by customer – dependency

• Goods Rejection during transition period – no credit note but a sale invoice to be raised – Proviso to Section 142(1)

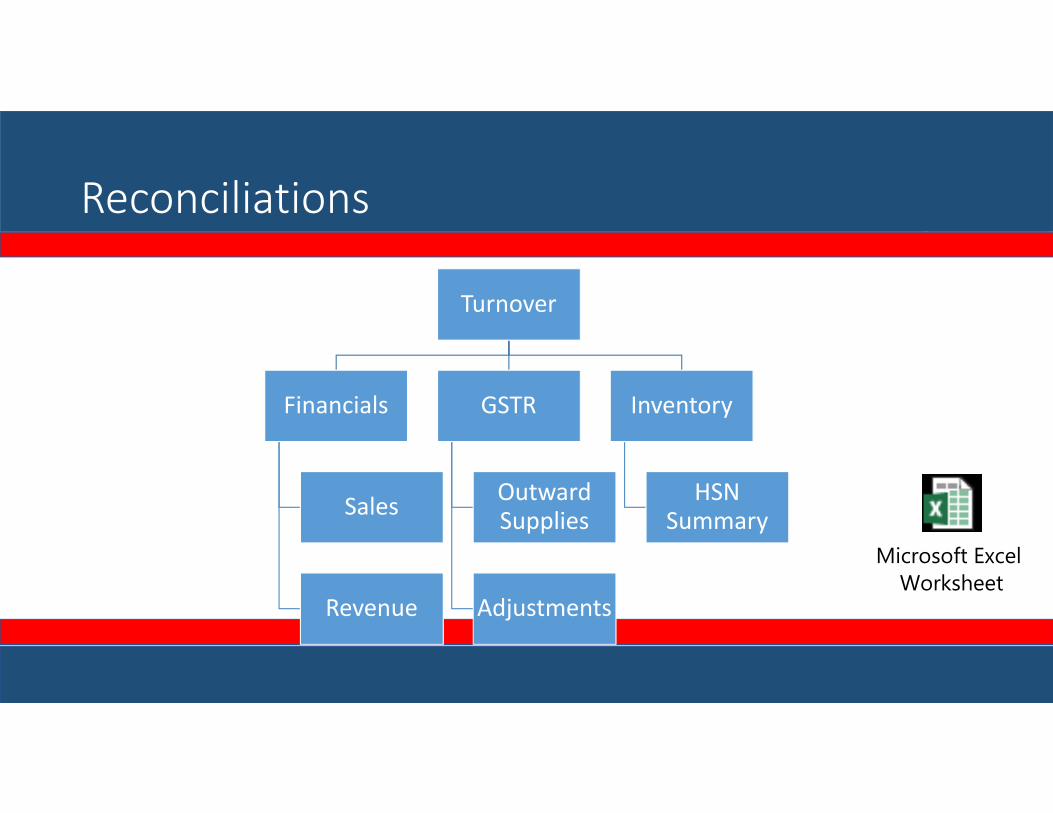

Reconciliations

Turnover

Financials

Sales

Revenue

GSTR

Outward Supplies

Adjustments

Inventory

HSN Summary

Microsoft Excel

Worksheet

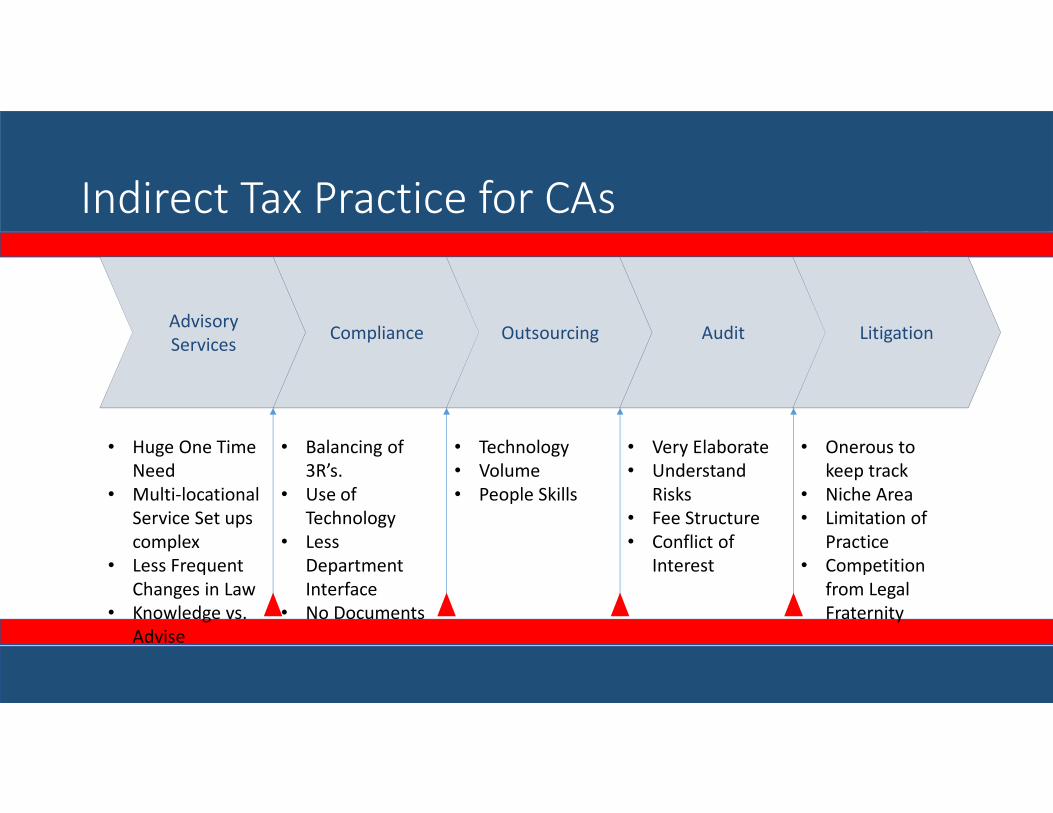

Indirect Tax Practice for CAs

Advisory

Services

• Balancing of

3R’s.

• Use of

Technology

• Less

Department

Interface

• No Documents

• Very Elaborate

• Understand

Risks

• Fee Structure

• Conflict of

Interest

• Onerous to

keep track

• Niche Area

• Limitation of

Practice

• Competition

from Legal

Fraternity

• Huge One Time

Need

• Multi-locational

Service Set ups

complex

• Less Frequent

Changes in Law

• Knowledge vs.

Advise

Compliance Outsourcing Audit Litigation

• Technology

• Volume

• People Skills

Compliance Practice for CAs : Way Forward

• ABC Limited has currently appointed separate excise consultant, VAT consultant and service tax consultant.

• Will he need three different consultants in GST?

• Can he keep three different consultants in GST? What will be the role of each of them?

• Will there be a need for state level consultants?

• Common Law across the country

• Most activities on common portal

• Law being State level, local nuances may still play a role

• What are the relevant skill sets in GST Regime?

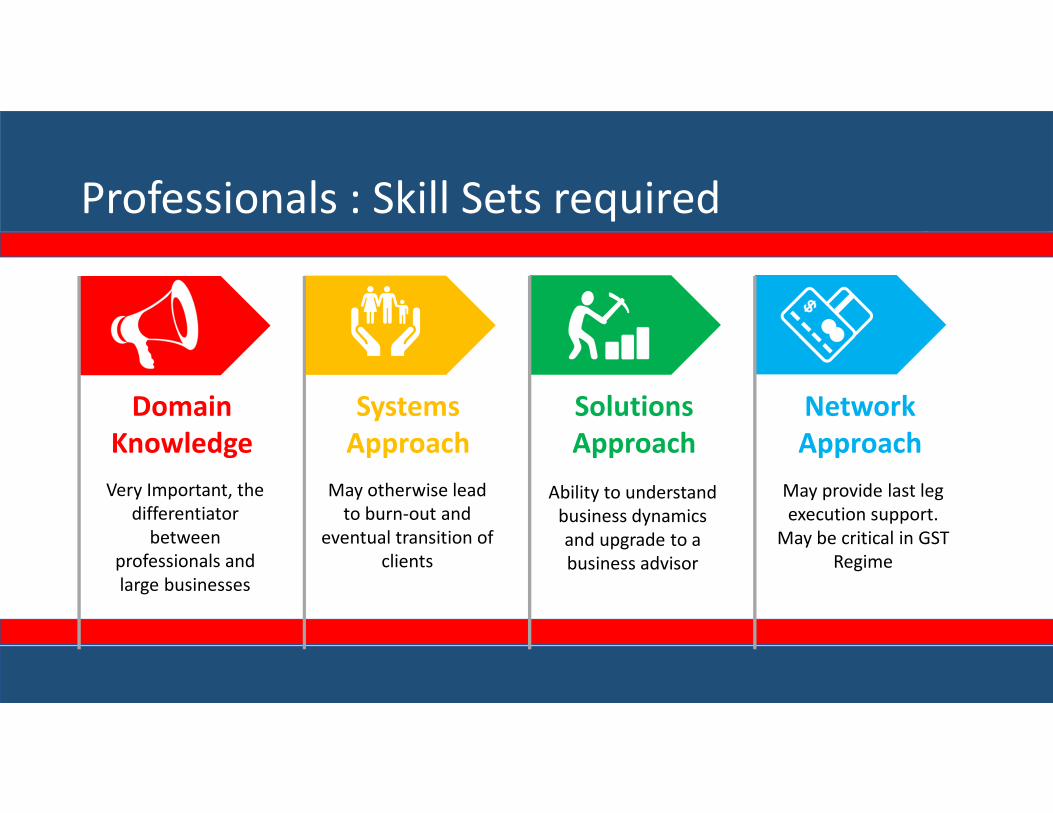

Professionals : Skill Sets required

Network

Approach

Domain

Knowledge

Solutions

Approach

Systems

Approach

Very Important, the

differentiator

between

professionals and

large businesses

May otherwise lead

to burn-out and

eventual transition of

clients

Ability to understand

business dynamics

and upgrade to a

business advisor

May provide last leg

execution support.

May be critical in GST

Regime

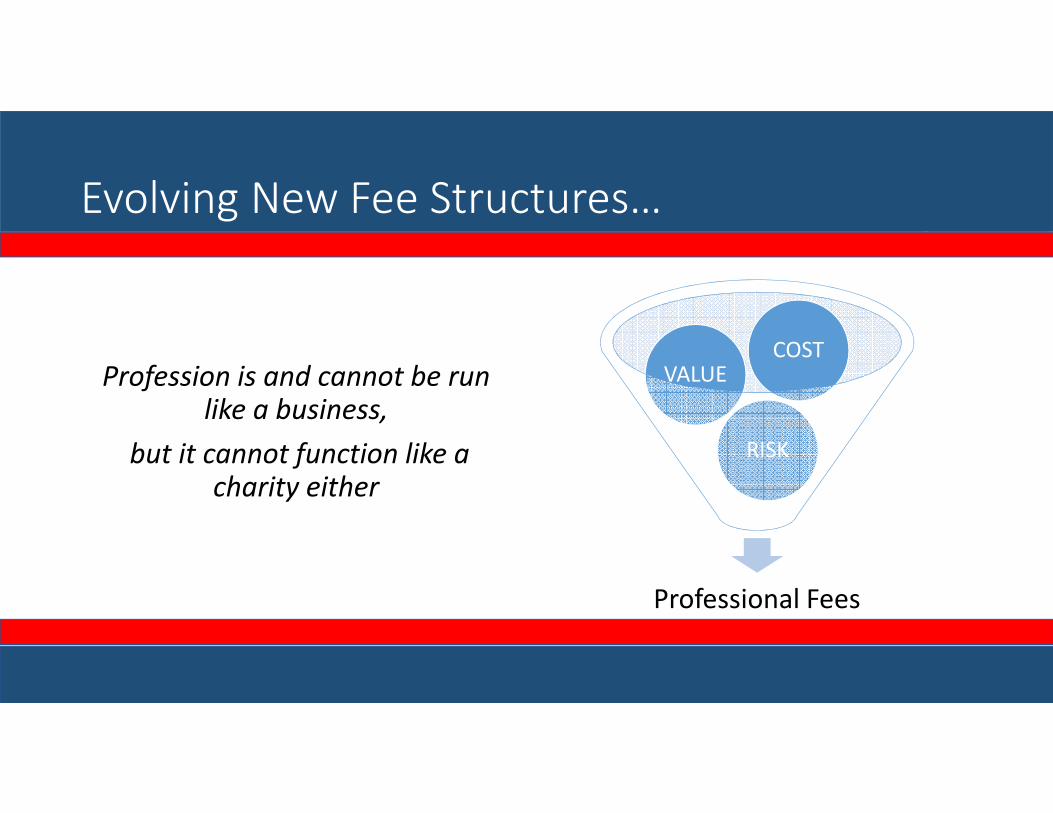

Evolving New Fee Structures…

Profession is and cannot be run

like a business,

but it cannot function like a

charity either

Professional Fees

RISK

VALUECOST

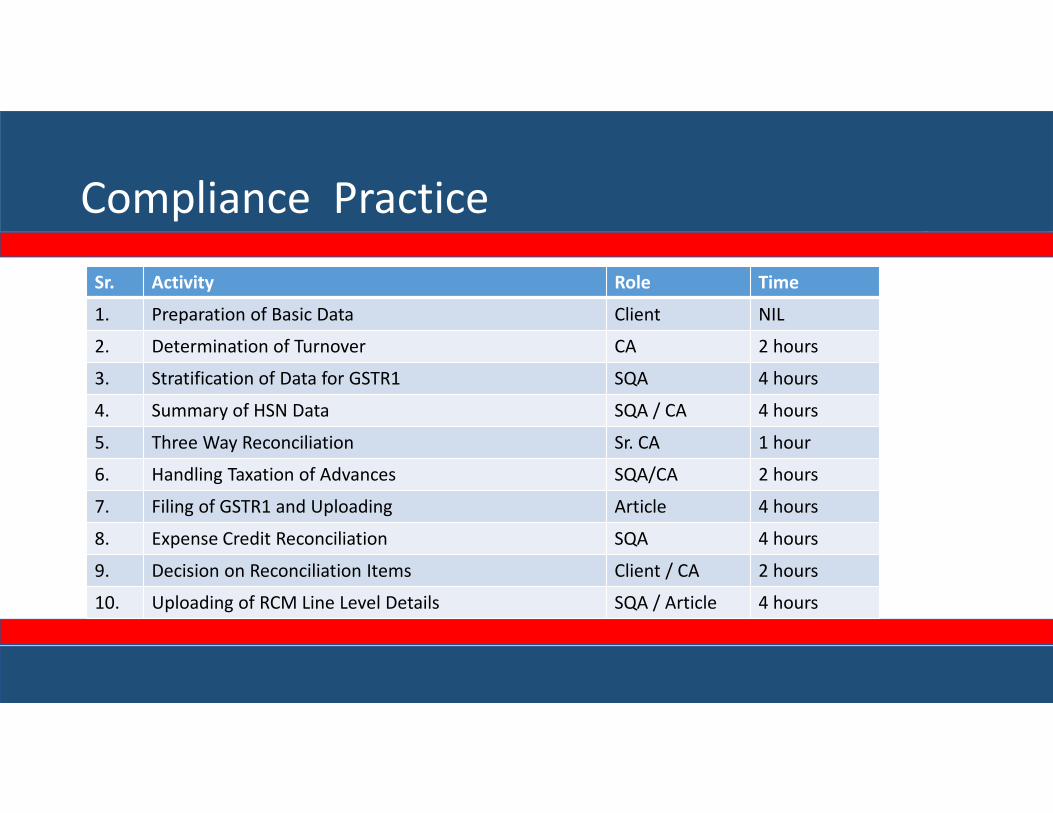

Compliance Practice

Sr. Activity Role Time

1. Preparation of Basic Data Client NIL

2. Determination of Turnover CA 2 hours

3. Stratification of Data for GSTR1 SQA 4 hours

4. Summary of HSN Data SQA / CA 4 hours

5. Three Way Reconciliation Sr. CA 1 hour

6. Handling Taxation of Advances SQA/CA 2 hours

7. Filing of GSTR1 and Uploading Article 4 hours

8. Expense Credit Reconciliation SQA 4 hours

9. Decision on Reconciliation Items Client / CA 2 hours

10. Uploading of RCM Line Level Details SQA / Article 4 hours

Compliance Practice (Contd.)

Sr. Activity Role Time

11. Decision on Claim of Credits Client / CA 2 hours

12. Uploading of GSTR 2 Article/SQA 2 hours

13. Income Reconciliation based on GSTR1A CA 1 hour

14. Decision on Reconciliation Items Client/CA 1 hour

15. Uploading of GSTR 1A Article/SQA 1 hour

16. Finalisation of GSTR 3 Article/SQA 1 hour

17. ITC Mismatch Report and Action Points thereon CA 1 hour

18. Reconciliation of Provisional Credits and Reversals and

Re-credits

CA/Sr. CA 2 hours

19. Review of Above Steps and Advisory CA/Sr. CA 4 hours

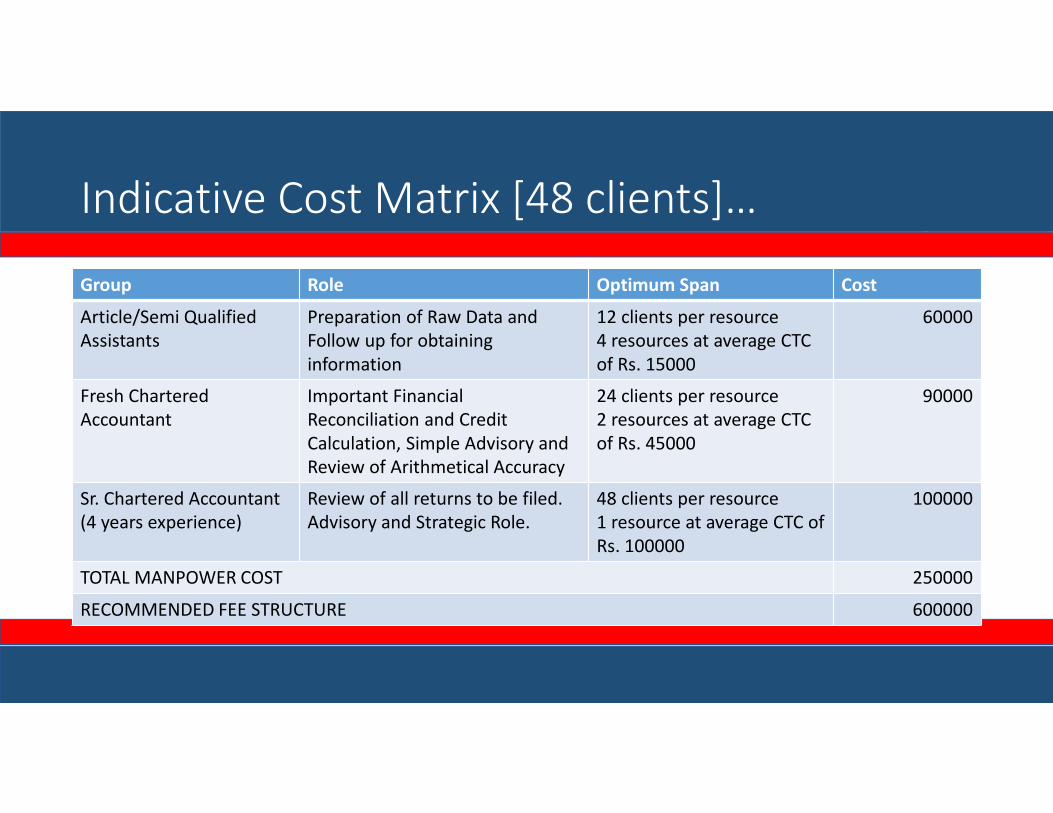

Indicative Cost Matrix [48 clients]…

Group Role Optimum Span Cost

Article/Semi Qualified

Assistants

Preparation of Raw Data and

Follow up for obtaining

information

12 clients per resource

4 resources at average CTC

of Rs. 15000

60000

Fresh Chartered

Accountant

Important Financial

Reconciliation and Credit

Calculation, Simple Advisory and

Review of Arithmetical Accuracy

24 clients per resource

2 resources at average CTC

of Rs. 45000

90000

Sr. Chartered Accountant

(4 years experience)

Review of all returns to be filed.

Advisory and Strategic Role.

48 clients per resource

1 resource at average CTC of

Rs. 100000

100000

TOTAL MANPOWER COST 250000

RECOMMENDED FEE STRUCTURE 600000

Marrying Cost and Value

Category No. of

Clients

Total Per Client

Per Month

A 5 200000 40000

B 10 200000 20000

C 33 200000 6000

Total 48 600000

• How to drive VALUE ??

• Learn to say NO, at least once in a while

• Always remember

• 50 x 20,000 > 200 x 4,000

What are the risks??

• Successful GSTR Filing Dependent on

• Quality of Data Entry by Client

• Processing of Data at CA End

• Timely Confirmation by Client

• Network and Server Dependencies

• Any aberration to be known to

• Client’s tax team

• Client’s Sales team

• Client’s Client’s tax and procurement teams

• Who is the person to be blamed ??