Singapore. Find Singapore Singapore Singapore: Singapore city.

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Strategy presentation, Singapore, 16 November 2012

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Disclaimer

Some of the statements contained in this presentation that are not historical facts are statements of future expectations and other forward-looking statements based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those in such statements. Such forward-looking statements are subject to various risks and uncertainties, which may cause actual results and performance of the Company’s business to differ materially and adversely from the forward-looking statements.

Should one or more of these risks or

uncertainties materialize, or should

underlying assumptions prove incorrect,

actual results may vary materially from

those described in this presentation as

anticipated, believed, or expected. SBM

Offshore NV does not intend, and does not

assume any obligation, to update any

industry information or forward-looking

statements set forth in this presentation to

reflect subsequent events or

circumstances.

2

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Agenda - Who we are, where we are - Transformation - Challenges and opportunities - Our Strategy

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Who we are, where we are

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

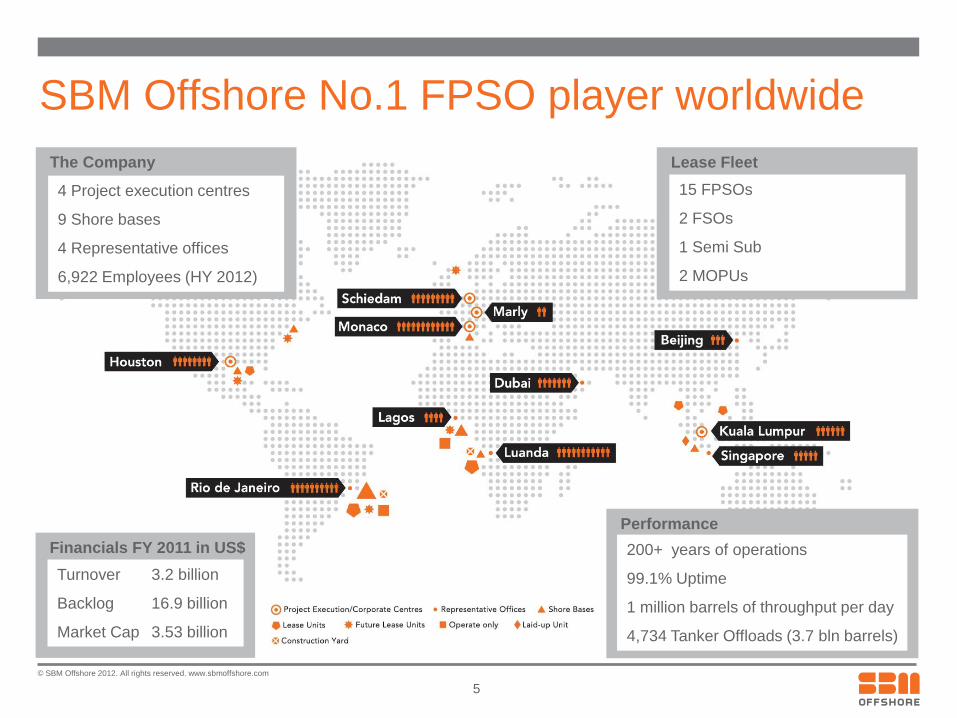

SBM Offshore No.1 FPSO player worldwide

Financials FY 2011 in US$

Turnover 3.2 billion

Backlog 16.9 billion

Market Cap 3.53 billion

Performance

200+ years of operations

99.1% Uptime

1 million barrels of throughput per day

4,734 Tanker Offloads (3.7 bln barrels)

The Company

4 Project execution centres

9 Shore bases

4 Representative offices

6,922 Employees (HY 2012)

Lease Fleet

15 FPSOs

2 FSOs

1 Semi Sub

2 MOPUs

5

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

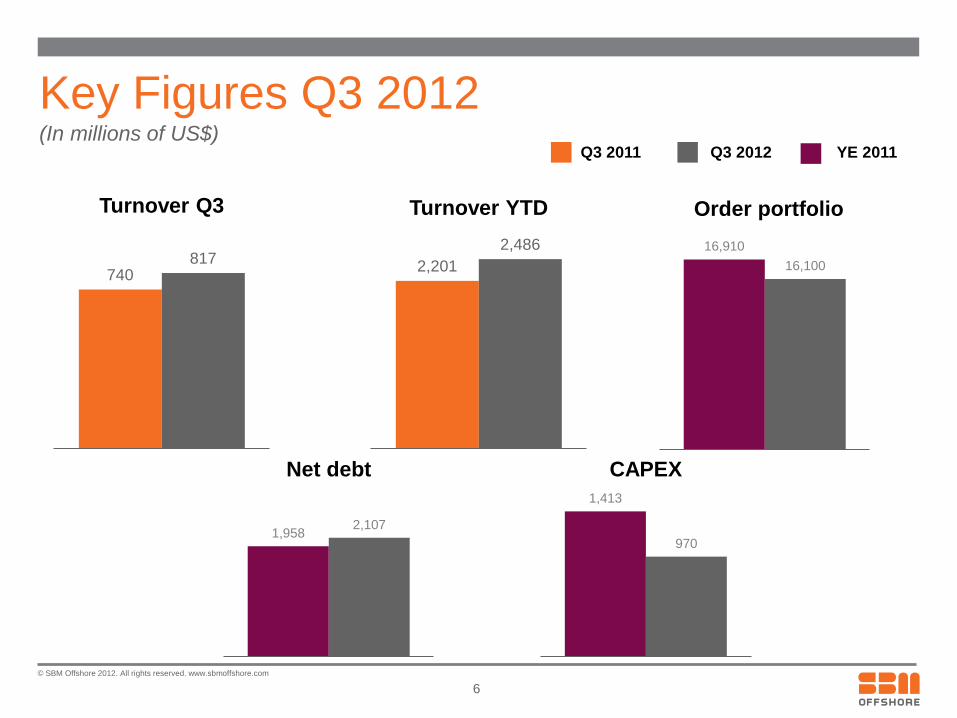

Key Figures Q3 2012 (In millions of US$)

Q3 2011 Q3 2012 YE 2011

6

740 817

Turnover Q3

2,201

2,486

Turnover YTD

16,910

16,100

Order portfolio

1,958 2,107

Net debt

1,413

970

CAPEX

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

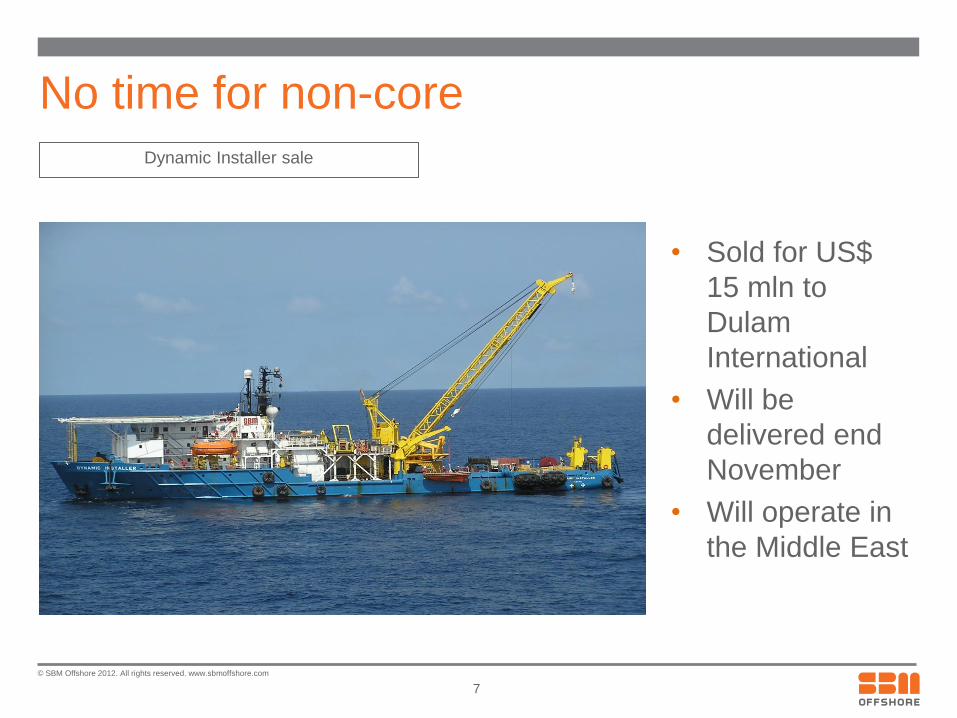

No time for non-core

• Sold for US$

15 mln to

Dulam

International

• Will be

delivered end

November

• Will operate in

the Middle East

7

Dynamic Installer sale

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

No time for non-core

• Gusto-MSC:

Sold for approximately US$ 185 mln

• Next step: Sale and lease back of real estate (offices) and potentially

other divestments

• Total: around US$ 400 mln

• Targeted schedule: within 6-12 months

8

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

First USPP and Ilhabela financing

• First US Private Placement project bond for SBM Offshore

• First US Private Placement project bond for a FPSO

• Cidade de Anchieta on hire since September 2012 for 18 year lease

contract

• US$ 500mn for 15 year maturity with 5.5% fixed coupon

• Duration of project bond in line with duration of lease contract

• Record US$ 1.05 billion financing secured for Cidade de Ilhabela

9

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

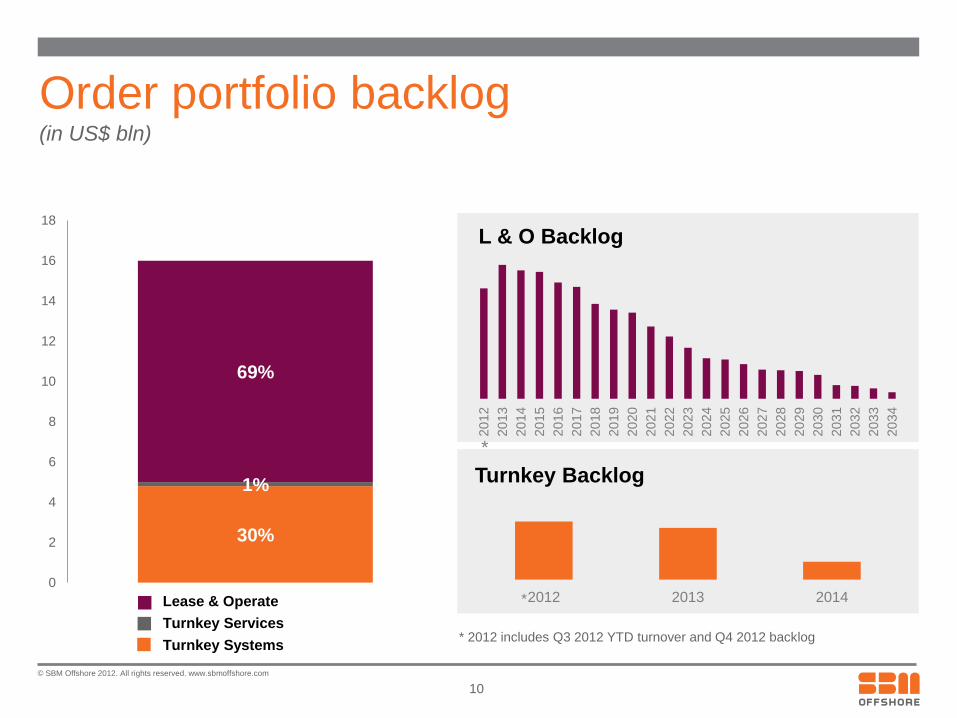

L & O Backlog

30%

1%

69%

0

2

4

6

8

10

12

14

16

18

*

* 2012 includes Q3 2012 YTD turnover and Q4 2012 backlog

10

Order portfolio backlog (in US$ bln)

Lease & Operate

Turnkey Systems

Turnkey Services

2012 2013 2014

Turnkey Backlog

*

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Transformation

11

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

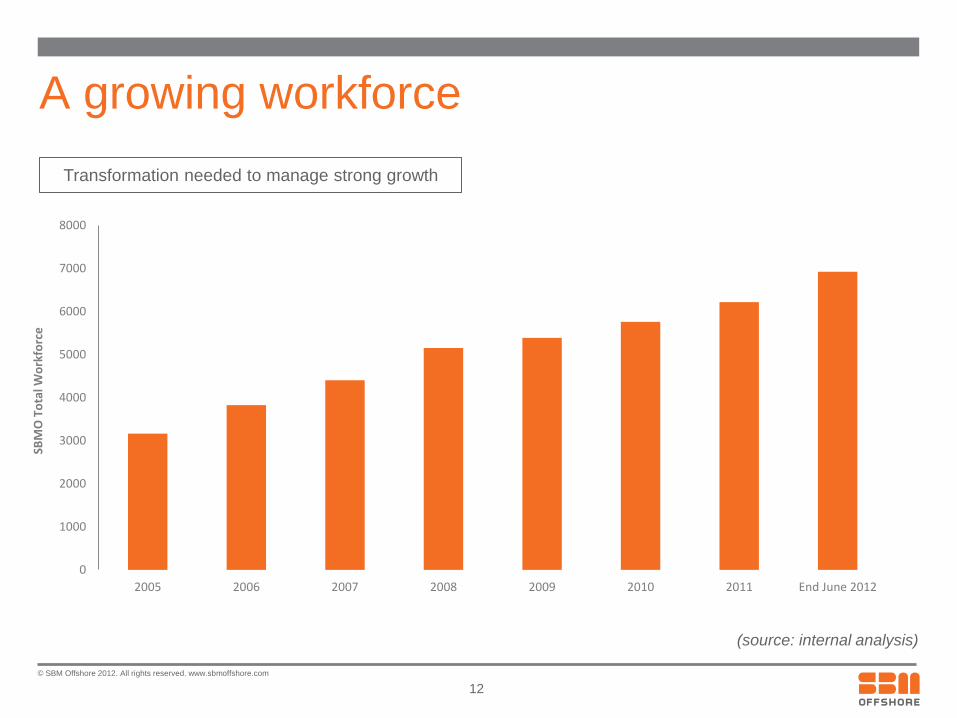

A growing workforce

12

(source: internal analysis)

Transformation needed to manage strong growth

0

1000

2000

3000

4000

5000

6000

7000

8000

2005 2006 2007 2008 2009 2010 2011 End June 2012

SBM

O T

ota

l Wo

rkfo

rce

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Growing production volume

13

(source: internal analysis)

Transformation needed to manage strong growth

700.00

750.00

800.00

850.00

900.00

950.00

1,000.00

2007 2008 2009 2010 2011

Th

ou

sa

nd

s

Average production in bl/day

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Group transformation in progress

14

FPSO strategy focus

Lead the industry transition towards improving risk/reward balance

New organisation profit

and cash flow

accountable

Strengthened

management team

Selective growth in

buoyant market

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Strengthened management team • The Board of Management

• Executive Committee: 5 Managing directors+ group functions

15

Wim Janse

MD SBM Monaco

Mike Wyllie

MD SBM PC (acting)

Bernard van Leggelo

MD SBM Houston Ivan Replumaz

MD SBM Kuala Lumpur

Yves Paletta

MD SBM Schiedam

Didier Beynet

Group HR director

Saskia Kunst

Group Strategy director

Erik van Kuijk

Group HSSE director

Bernard Verwilghen

Group Secretary

Oliver Kassam

Group Sales director

Bruno Chabas

CEO Peter van Rossum

CFO

Sietze Hepkema

CGCO

J.P. Laures

COO

Mike Wyllie

CTO

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

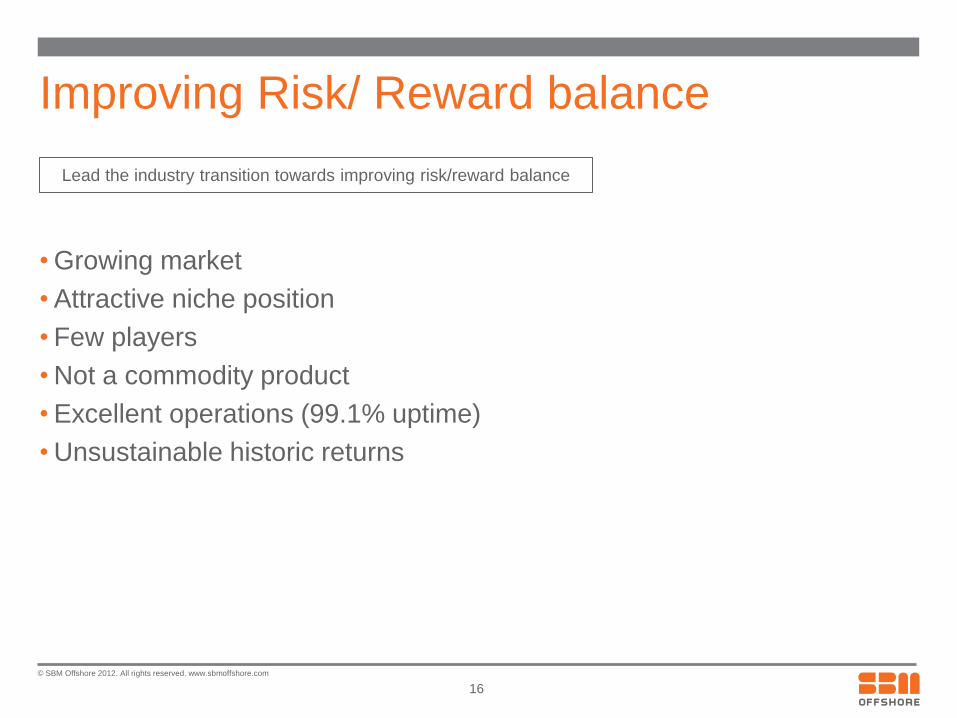

Improving Risk/ Reward balance

• Growing market

• Attractive niche position

• Few players

• Not a commodity product

• Excellent operations (99.1% uptime)

• Unsustainable historic returns

16

Lead the industry transition towards improving risk/reward balance

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Challenges and opportunities High demand for complex FPSOs Unsustainable industry returns

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

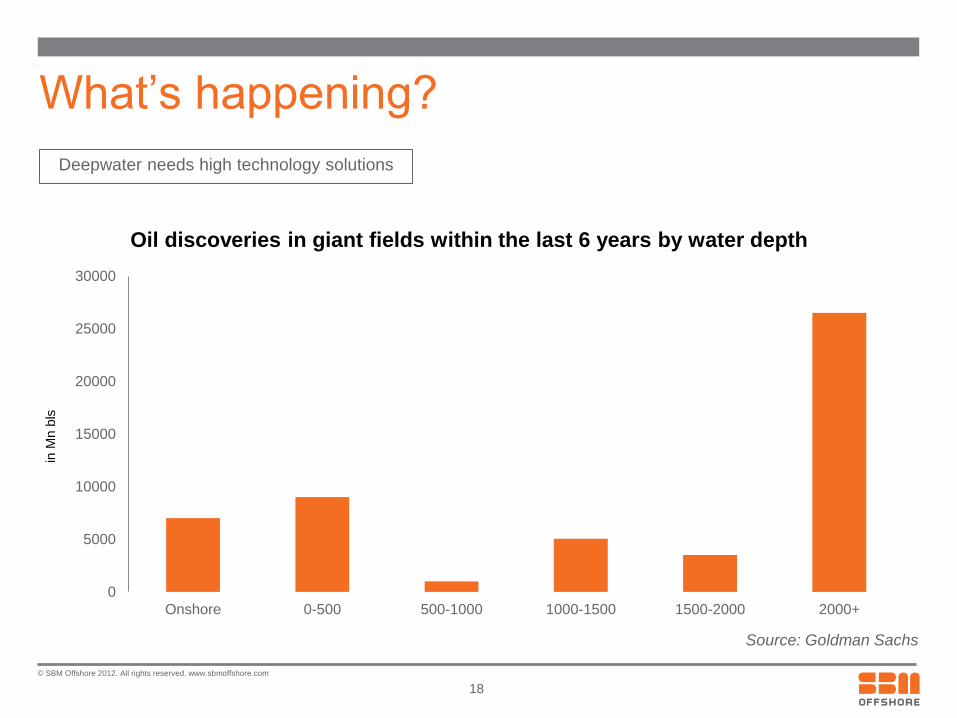

0

5000

10000

15000

20000

25000

30000

Onshore 0-500 500-1000 1000-1500 1500-2000 2000+

in M

n b

ls

Oil discoveries in giant fields within the last 6 years by water depth

What’s happening?

Source: Goldman Sachs

18

Deepwater needs high technology solutions

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

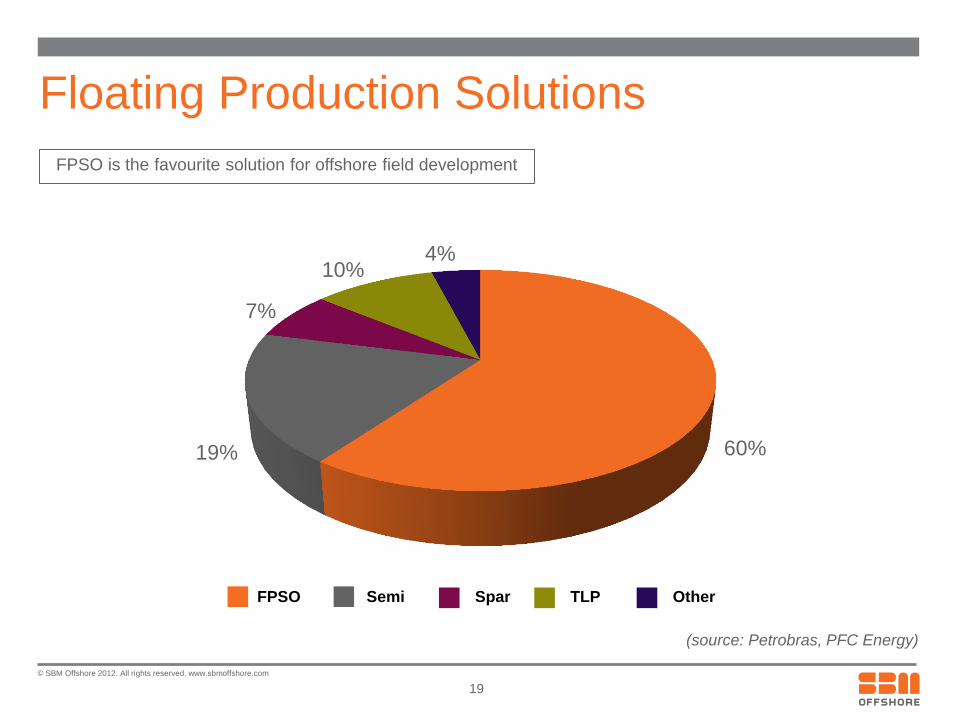

Floating Production Solutions

60% 19%

7%

10% 4%

19

(source: Petrobras, PFC Energy)

FPSO Semi Spar TLP Other

FPSO is the favourite solution for offshore field development

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

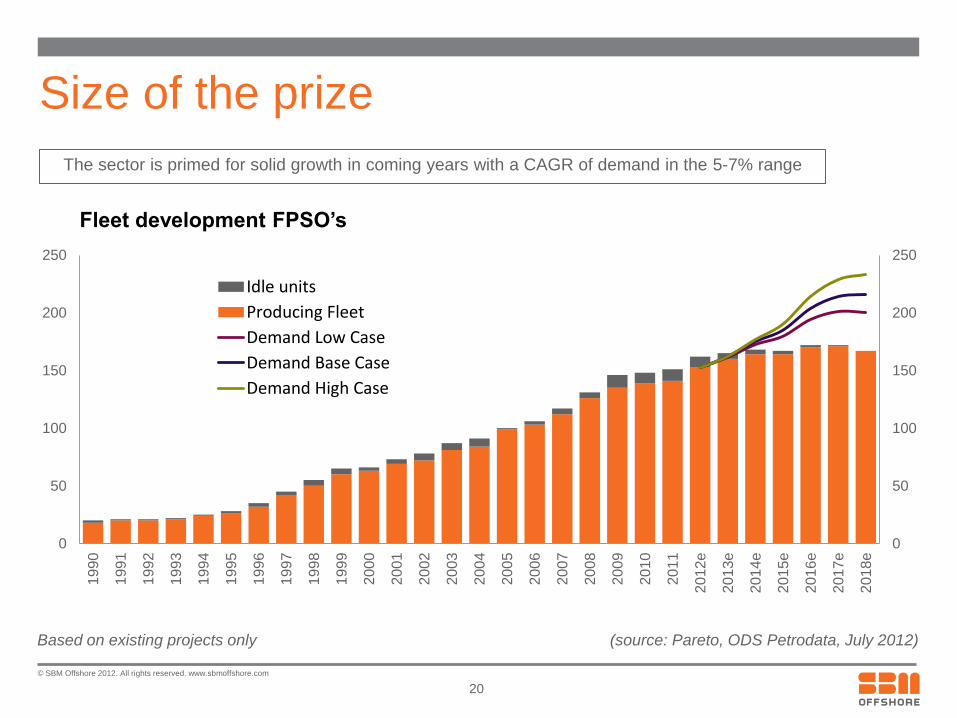

Size of the prize

20

Based on existing projects only (source: Pareto, ODS Petrodata, July 2012)

The sector is primed for solid growth in coming years with a CAGR of demand in the 5-7% range

0

50

100

150

200

250

0

50

100

150

200

250

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012e

2013e

2014e

2015e

2016e

2017e

2018e

Fleet development FPSO’s

Idle units

Producing Fleet

Demand Low Case

Demand Base Case

Demand High Case

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

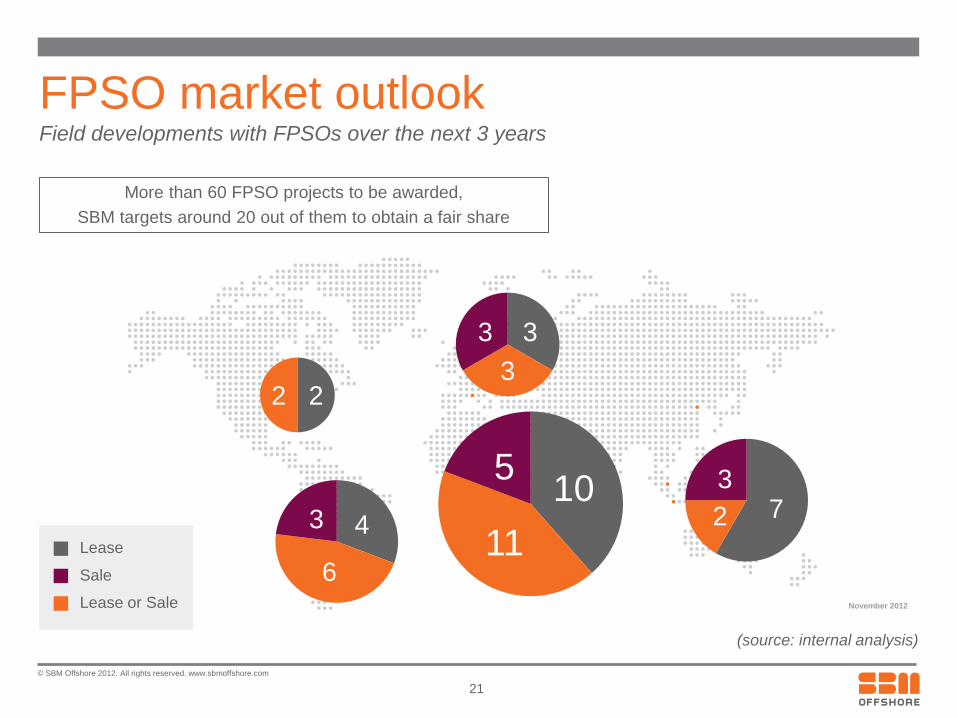

Field developments with FPSOs over the next 3 years

FPSO market outlook

November 2012

Lease

Sale

Lease or Sale

21

(source: internal analysis)

More than 60 FPSO projects to be awarded,

SBM targets around 20 out of them to obtain a fair share

10

11

5 7 2

3

4

6

3

3

3

3

2 2

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

0

4,000

8,000

12,000

16,000

20,000

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

To

psid

es W

eig

ht (t

on

)

Year of first oil

Rang Dong

Brasil Cachalote

Cd de Anchieta

FPSOs are getting heavier

22

Kuito

Espadarte

Xikomba

Falcon

Marlim

Sul

Serpentina

Cd de Paraty

Capixaba

P 57

Mondo Saxi

N’Goma

Cd de Ilhabela

Kikeh

Frade

BC 10 Aseng

(source: internal analysis)

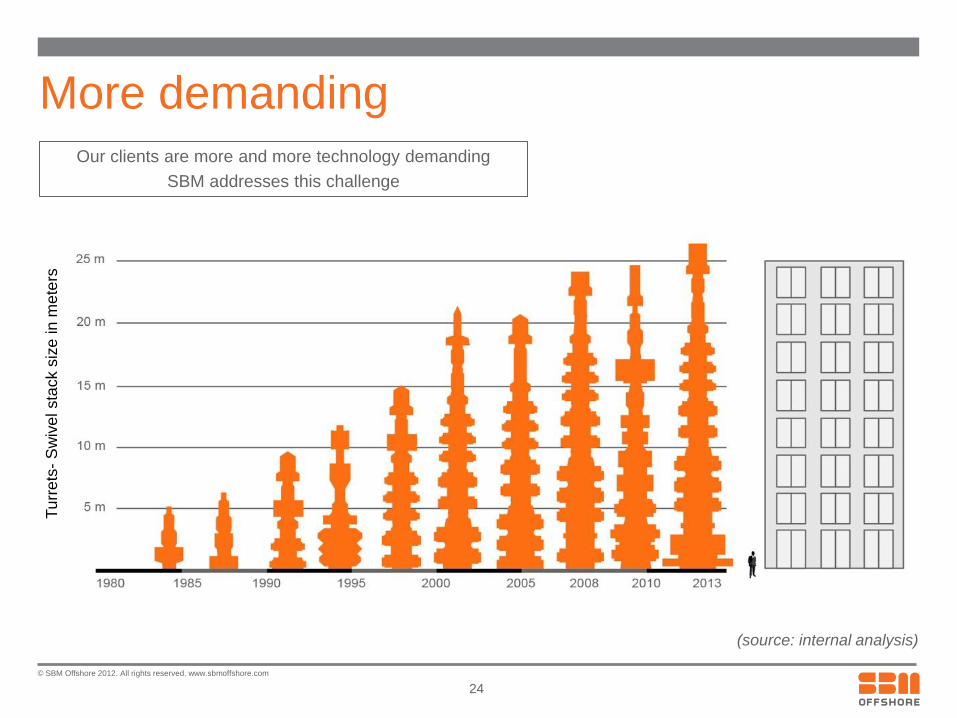

Our clients are more and more technology demanding

SBM addresses this challenge

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Getting complex

23

Our clients are more and more technology demanding

SBM addresses this challenge

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

More demanding

24

(source: internal analysis)

Turrets – Swivel stack size

Our clients are more and more technology demanding

SBM addresses this challenge

Tu

rre

ts-

Sw

ive

l sta

ck s

ize

in m

ete

rs

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Be ready for the next step

• Commercial

agreement with

CompactGTL

• Convert the

associated gas

into syncrude

• Co-mingle and

transport with the

natural crude

25

Work to adapt Gas to Liquids Technology to FPSO

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Industry leadership

• Focus on 3 areas:

FPSO

Topsides

Mooring

26

Maintain our technical edge

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

FPSOs are not a commodity

• Full life

production

solution

• Qualitative

differentiation

• Non

exchangeable

27

Bespoke solutions for full product lifecycle

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Challenges and opportunities High demand for complex FPSOs Unsustainable industry returns

28

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

FPSO: unsustainable industry ranking

-24.9%

-14.1%

-13.9%

-7.2%

-6.8%

-5.0%

-3.9%

-3.9%

-2.7%

1.9%

2.0%

2.2%

6.0%

9.5%

14.3%

14.6%

16.0%

16.5%

16.9%

20.3%

22.2%

24.4%

31.1%

-50.0% -40.0% -30.0% -20.0% -10.0% 0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

BW OFFSHORE

SBM OFFSHORE

HELIX ENERGY SOLUTIONS

TEEKAY

AP MOELLER-MAERSK

MODEC

JACOBS ENGINEERING GROUP

MCDERMOTT INTL

AKER SOLUTIONS

SUBSEA 7

KBR

FOSTER WHEELER

CHICAGO BRIDGE & IRON

FUGRO NV-CVA

TECHNIP

WORLEY PARSONS

AMEC

SAIPEM

WOOD GROUP (JOHN)

OIL STATES INTERNATIONAL

OCEANEERING INTL

FMC TECHNOLOGIES

PETROFAC

SBM OFFSHORE

BW OFFSHORE

TEEKAY

AP MOELLER-MAERSK

MODEC

TSR Peer Group Ranking 2007 – 1H2012, %CAGR

29

(source: Bloomberg, internal data)

Total Shareholders Return for FPSO industry negative

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

2007 2008 2009 2010 2011 5yr avg

SBMO Modec BWO Teekay Aker Floating Production Bluewater Group

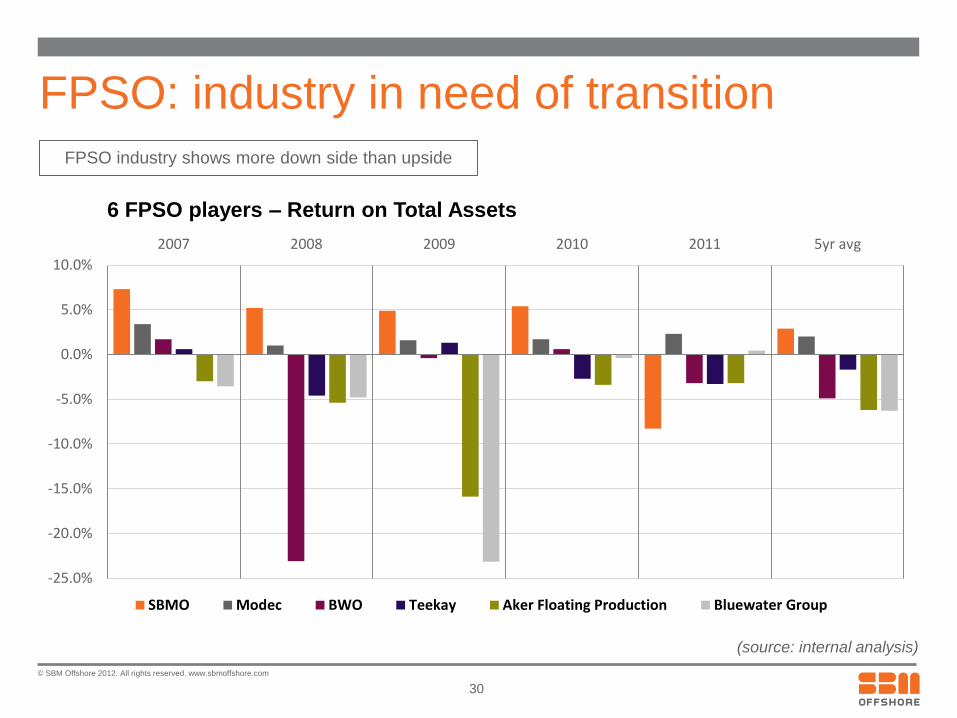

FPSO: industry in need of transition

6 FPSO players – Return on Total Assets

30

FPSO industry shows more down side than upside

(source: internal analysis)

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

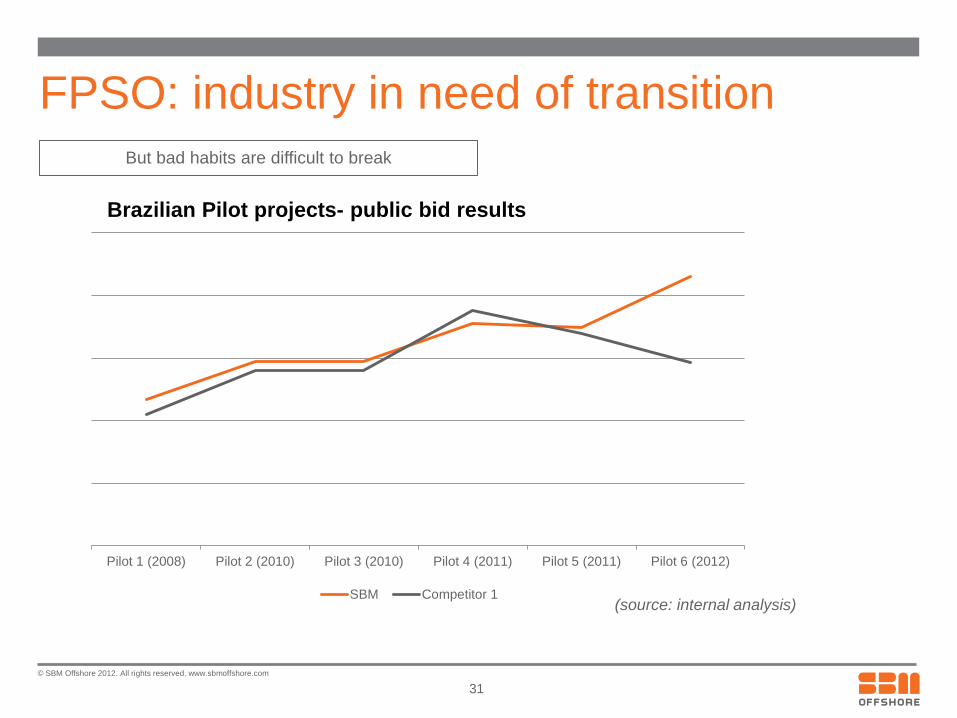

FPSO: industry in need of transition

Brazilian Pilot projects- public bid results

31

But bad habits are difficult to break

(source: internal analysis)

Pilot 1 (2008) Pilot 2 (2010) Pilot 3 (2010) Pilot 4 (2011) Pilot 5 (2011) Pilot 6 (2012)

SBM Competitor 1

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Our Strategy

32

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

33

FPSO

FPSO

FPSO

About our Strategy

The Company has refocused its product line on core

FPSO products and associated services. By focusing

on core products with historically good margins whilst

improving execution standards and project risk

profiles, the Company believes it will return to

delivering superior financial returns.

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

0

1

2

3

4

5

0 20000 40000 60000 80000 100000 120000 140000

Aw

ard

s w

on

Average production capacity (bpd) (Engineering complexity)

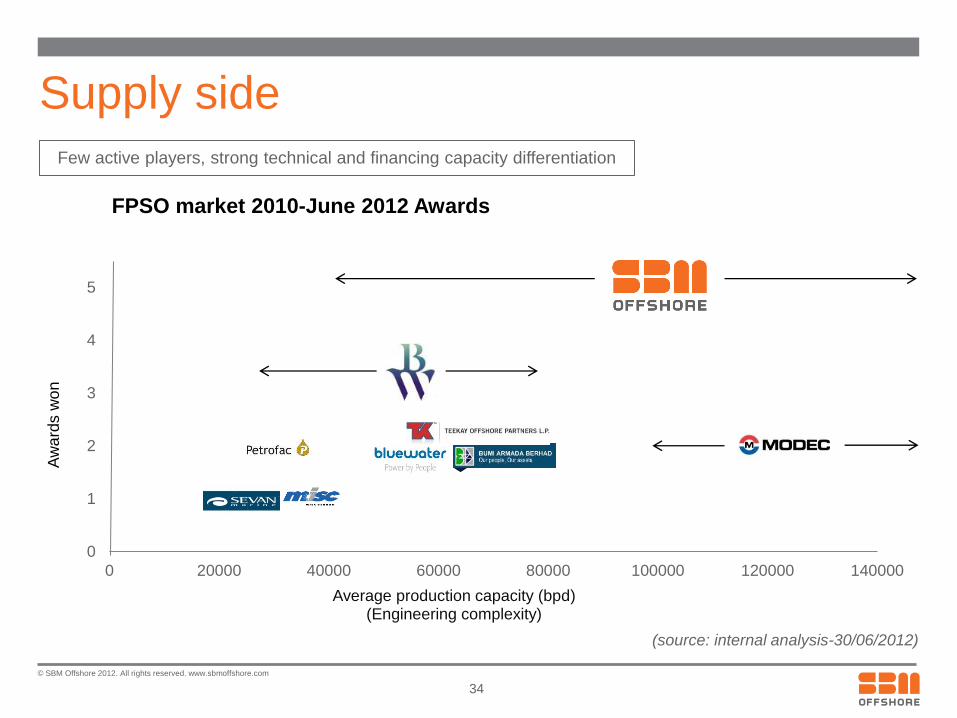

Supply side

34

(source: internal analysis-30/06/2012)

FPSO market 2010-June 2012 Awards

Few active players, strong technical and financing capacity differentiation

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

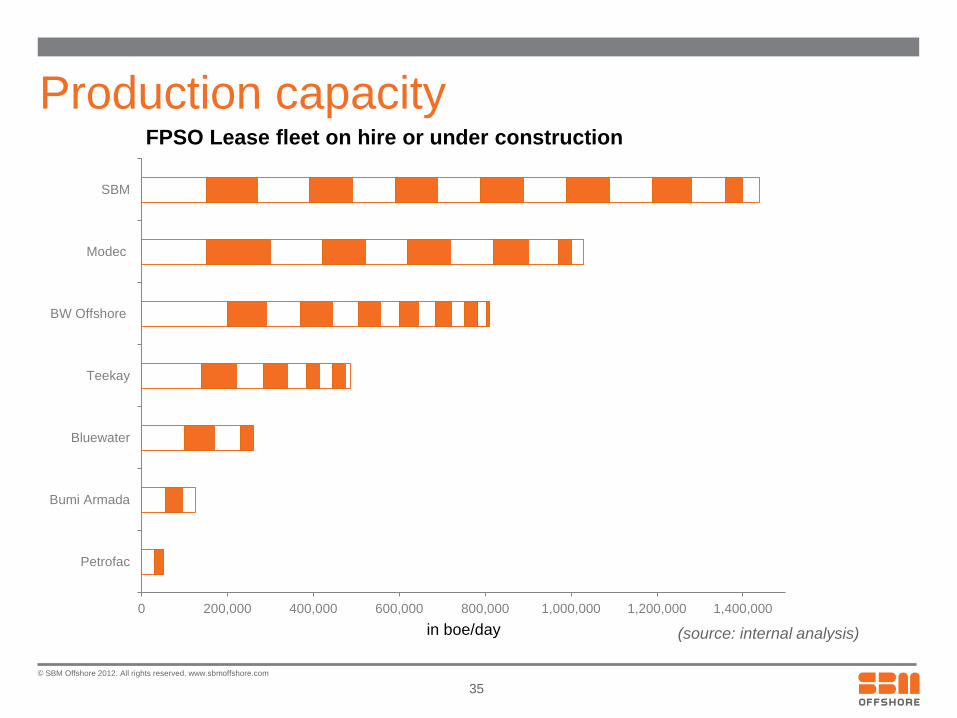

Production capacity

(source: internal analysis)

0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000

Petrofac

Bumi Armada

Bluewater

Teekay

BW Offshore

Modec

SBM

in boe/day

FPSO Lease fleet on hire or under construction

35

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

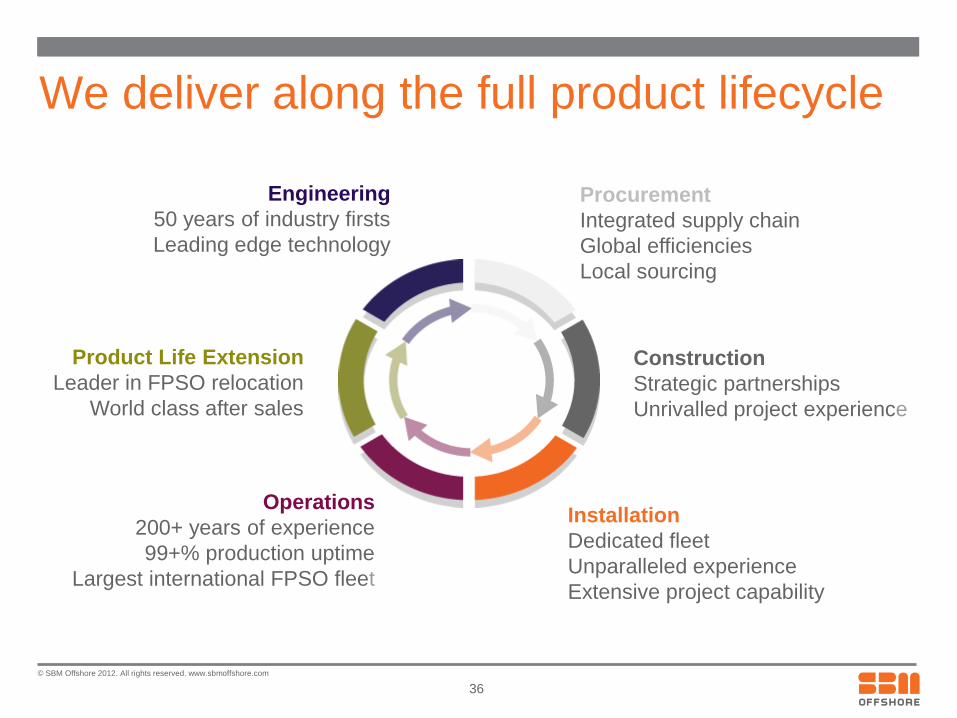

We deliver along the full product lifecycle

SBM Offshore - Running head. 6pt Arial Regular SBM Offshore - Running head. 6pt Arial Regular

Product Life Extension

Leader in FPSO relocation

World class after sales

Operations

200+ years of experience

99+% production uptime

Largest international FPSO fleet

Installation

Dedicated fleet

Unparalleled experience

Extensive project capability

Construction

Strategic partnerships

Unrivalled project experience

Procurement

Integrated supply chain

Global efficiencies

Local sourcing

Engineering

50 years of industry firsts

Leading edge technology

36

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Cidade de Anchieta

37

August 2012

April 2011

126 km

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

August 2011

38

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

October 2011

39

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

Year-end 2011

40

© SBM Offshore 2012. All rights reserved. www.sbmoffshore.com

41