Strategic Management: Indian Luggage Industry

13

Strategic Management Submitted by: Aditya Khare Aditya Thakare Cheena Pasrija Joydeepta Biswas Indian Luggage Industry

-

Upload

aditya-khare -

Category

Leadership & Management

-

view

192 -

download

0

Transcript of Strategic Management: Indian Luggage Industry

Strategic Management

Submitted by:

Aditya Khare Aditya Thakare Cheena Pasrija Joydeepta Biswas

Indian Luggage Industry

Contents

• Overview

• Industry Analysis – PEST

• Porter’s Analysis

• VIP – Company Analysis

• VIP – SWOT Analysis

• VIP – Competitor Analysis

• Issues

• Recommendations and Implications

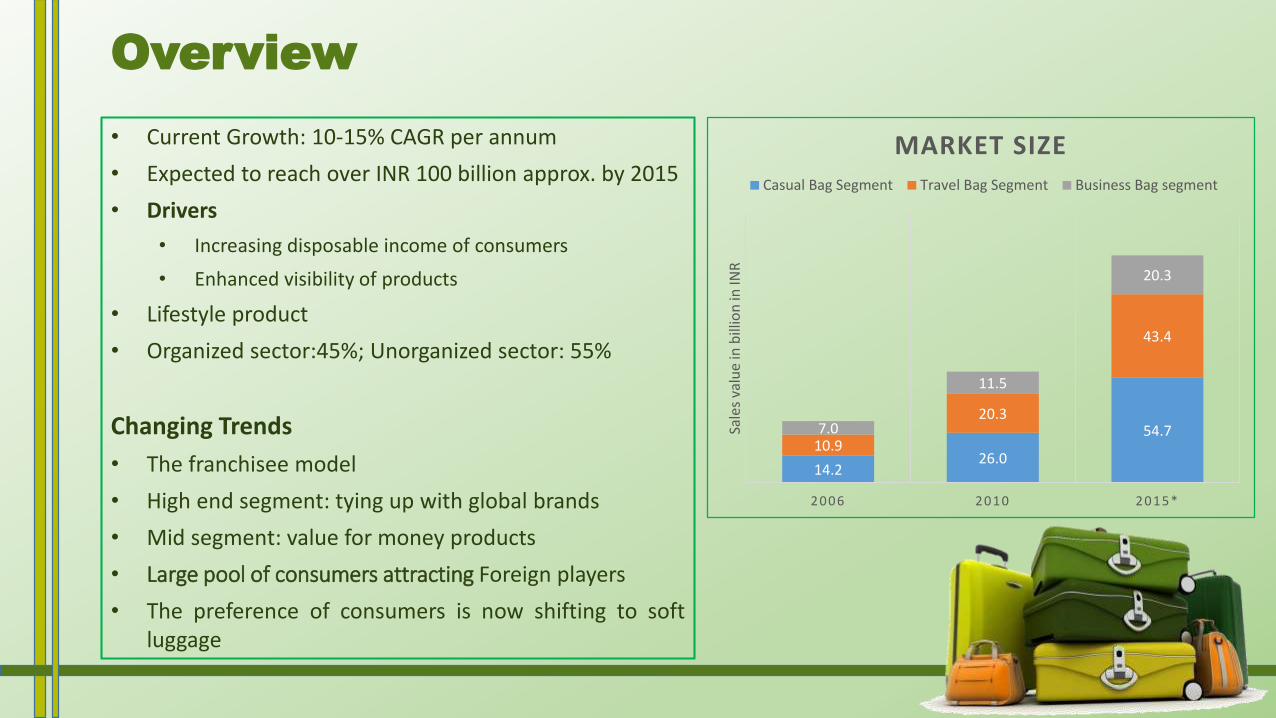

• Current Growth: 10-15% CAGR per annum

• Expected to reach over INR 100 billion approx. by 2015

• Drivers

• Increasing disposable income of consumers

• Enhanced visibility of products

• Lifestyle product

• Organized sector:45%; Unorganized sector: 55%

Changing Trends

• The franchisee model

• High end segment: tying up with global brands

• Mid segment: value for money products

• Large pool of consumers attracting Foreign players

• The preference of consumers is now shifting to softluggage

Overview

14.226.0

54.710.9

20.3

43.4

7.0

11.5

20.3

2006 2010 2015*

Sale

s va

lue

in b

illio

n in

INR

MARKET SIZE

Casual Bag Segment Travel Bag Segment Business Bag segment

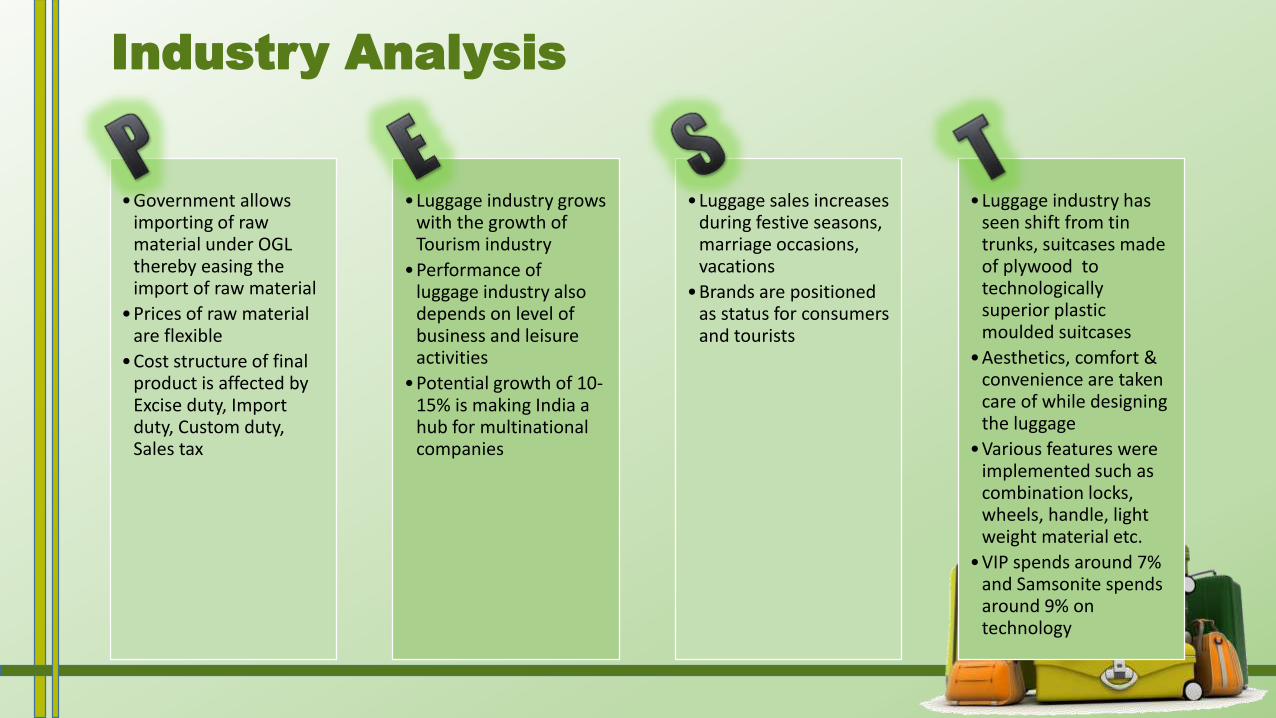

•Government allows importing of raw material under OGL thereby easing the import of raw material

•Prices of raw material are flexible

•Cost structure of final product is affected by Excise duty, Import duty, Custom duty, Sales tax

•Luggage industry grows with the growth of Tourism industry

•Performance of luggage industry also depends on level of business and leisure activities

•Potential growth of 10-15% is making India a hub for multinational companies

•Luggage sales increases during festive seasons, marriage occasions, vacations

•Brands are positioned as status for consumers and tourists

•Luggage industry has seen shift from tin trunks, suitcases made of plywood to technologically superior plastic moulded suitcases

•Aesthetics, comfort & convenience are taken care of while designing the luggage

•Various features were implemented such as combination locks, wheels, handle, light weight material etc.

•VIP spends around 7% and Samsonite spends around 9% on technology

Industry Analysis

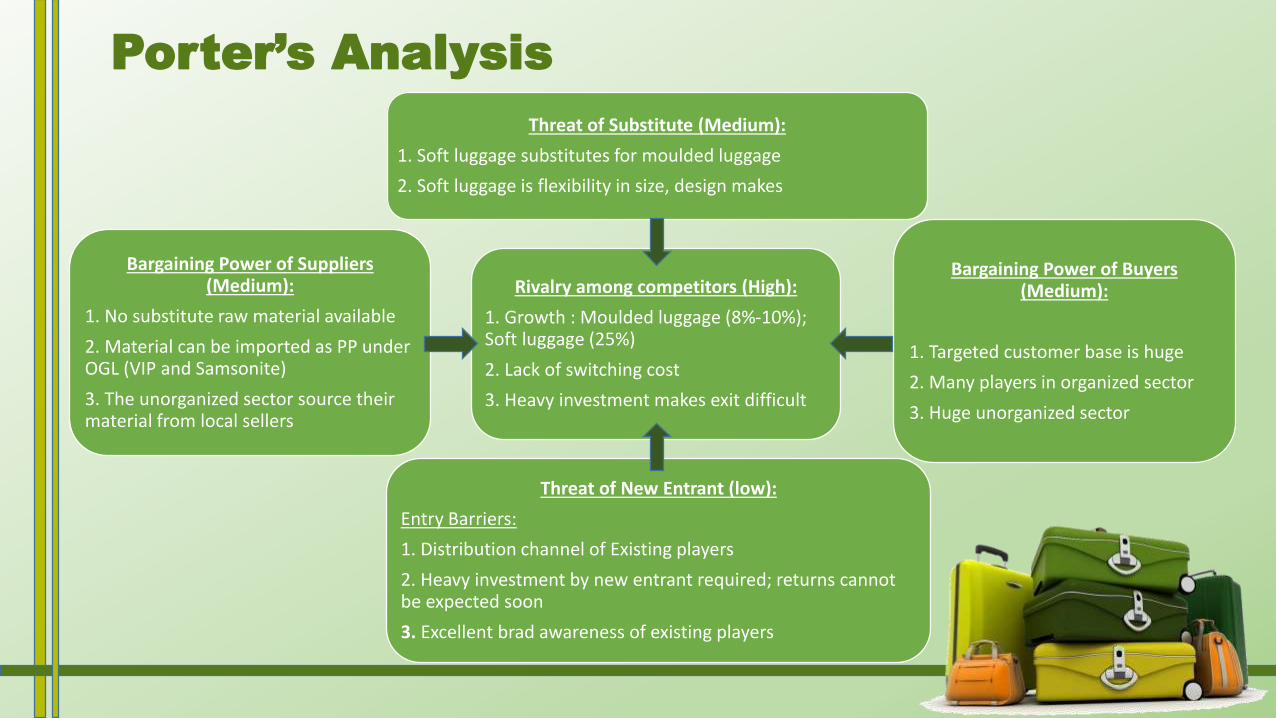

Rivalry among competitors (High):

1. Growth : Moulded luggage (8%-10%); Soft luggage (25%)

2. Lack of switching cost

3. Heavy investment makes exit difficult

Threat of Substitute (Medium):

1. Soft luggage substitutes for moulded luggage

2. Soft luggage is flexibility in size, design makes

Bargaining Power of Buyers (Medium):

1. Targeted customer base is huge

2. Many players in organized sector

3. Huge unorganized sector

Threat of New Entrant (low):

Entry Barriers:

1. Distribution channel of Existing players

2. Heavy investment by new entrant required; returns cannot be expected soon

3. Excellent brad awareness of existing players

Bargaining Power of Suppliers (Medium):

1. No substitute raw material available

2. Material can be imported as PP under OGL (VIP and Samsonite)

3. The unorganized sector source their material from local sellers

Porter’s Analysis

• VIP has dependably been a business pioneerand a class characterizing brand

• Six different brands

Carlton, VIP bags, Skybags, Caprese, Aristocat and Alfa

• Partnered with Oglivy to handle advertisingand public relations of all the brands

• In the organised segment, VIP Industries is themarket leader with 60 to 65 per cent shareacross all the brands

• Distribution is their strength

VIP Industries

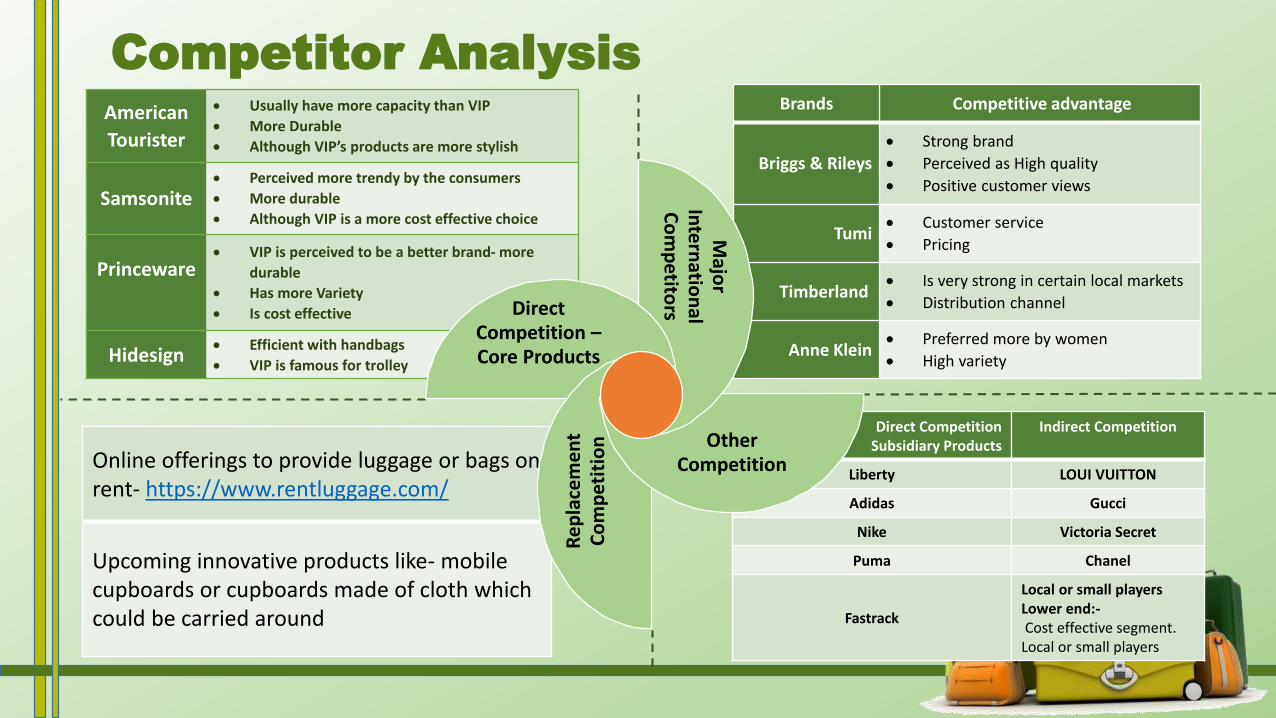

• Only a few companies competing againstVIP – American Tourister and Samsonitebeing the major ones

• Only brand to have a presence in Rural andSemi-Rural market

• Gradually taking a step forward in E-commerce sector

• Strong retail presence

• Plan for re-entering the kid’s bag market

• Launch of Eco-friendly bags, Acura

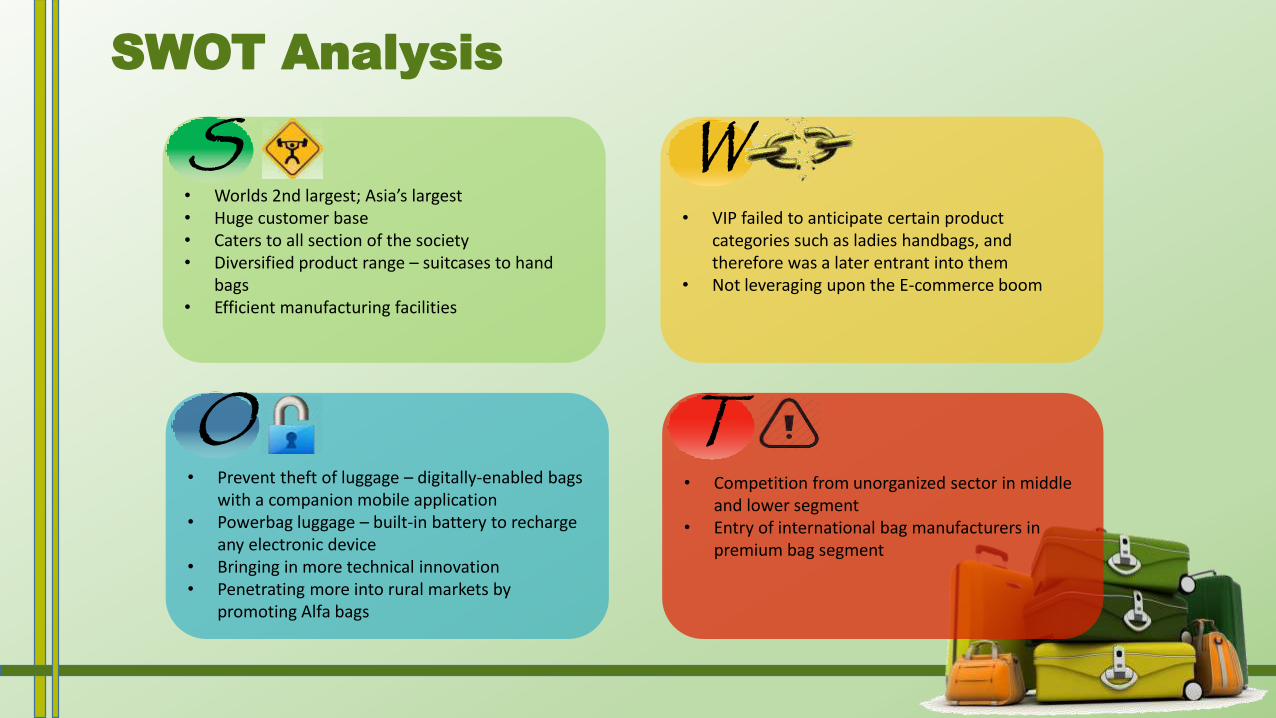

• Prevent theft of luggage – digitally-enabled bags with a companion mobile application

• Powerbag luggage – built-in battery to recharge any electronic device

• Bringing in more technical innovation• Penetrating more into rural markets by

promoting Alfa bags

• Worlds 2nd largest; Asia’s largest• Huge customer base• Caters to all section of the society• Diversified product range – suitcases to hand

bags• Efficient manufacturing facilities

• VIP failed to anticipate certain product categories such as ladies handbags, and therefore was a later entrant into them

• Not leveraging upon the E-commerce boom

• Competition from unorganized sector in middle and lower segment

• Entry of international bag manufacturers in premium bag segment

T

W

O

S

SWOT Analysis

American

Tourister

Usually have more capacity than VIP

More Durable

Although VIP’s products are more stylish

Samsonite Perceived more trendy by the consumers

More durable

Although VIP is a more cost effective choice

Princeware VIP is perceived to be a better brand- more

durable

Has more Variety

Is cost effective

Hidesign Efficient with handbags

VIP is famous for trolley

Online offerings to provide luggage or bags on rent- https://www.rentluggage.com/

Upcoming innovative products like- mobile cupboards or cupboards made of cloth which could be carried around

Direct CompetitionSubsidiary Products

Indirect Competition

Liberty LOUI VUITTON

Adidas Gucci

Nike Victoria Secret

Puma Chanel

Fastrack

Local or small players Lower end:-Cost effective segment.

Local or small players

Brands Competitive advantage

Briggs & Rileys Strong brand

Perceived as High quality

Positive customer views

Tumi Customer service

Pricing

Timberland Is very strong in certain local markets

Distribution channel

Anne Klein Preferred more by women

High variety

Majo

r In

tern

ation

al C

om

petito

rs

Other Competition

Re

pla

cem

en

t C

om

pet

itio

n

Direct Competition –Core Products

Competitor Analysis

• Increasing Consumerism

• Better understanding of product quality and increased disposable incomes

• Increased fashion quotient

• Increasing western influence

• Increasing Competition in Domestic Market

• Indian luggage market growing and hence drawing attention

• Perceived threats- Samsonite and American Tourister

• Emerging threats- Calonge, Dandy, Hidesign

• Prevailing unorganised sector

• Franchising

• Initially big retailers

• Gradually moving to franchisee model

Issues

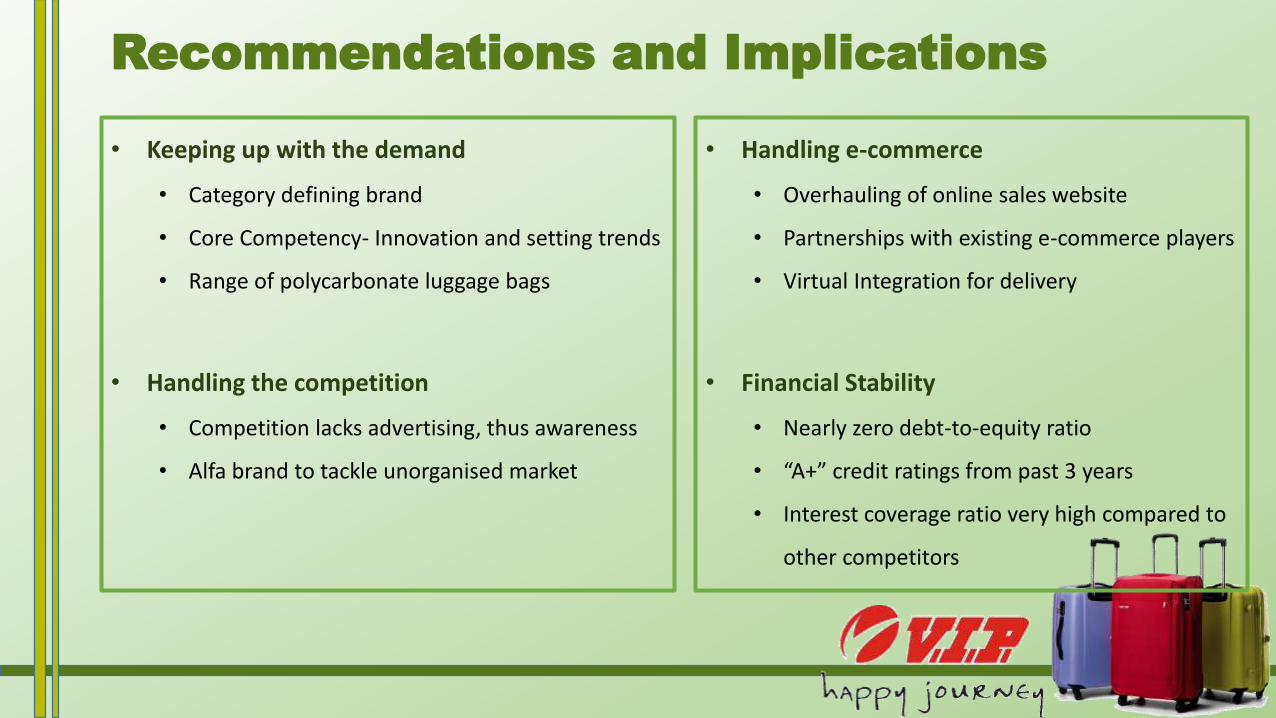

Recommendations and Implications

• Keeping up with the demand

• Category defining brand

• Core Competency- Innovation and setting trends

• Range of polycarbonate luggage bags

• Handling the competition

• Competition lacks advertising, thus awareness

• Alfa brand to tackle unorganised market

• Handling e-commerce

• Overhauling of online sales website

• Partnerships with existing e-commerce players

• Virtual Integration for delivery

• Financial Stability

• Nearly zero debt-to-equity ratio

• “A+” credit ratings from past 3 years

• Interest coverage ratio very high compared to

other competitors

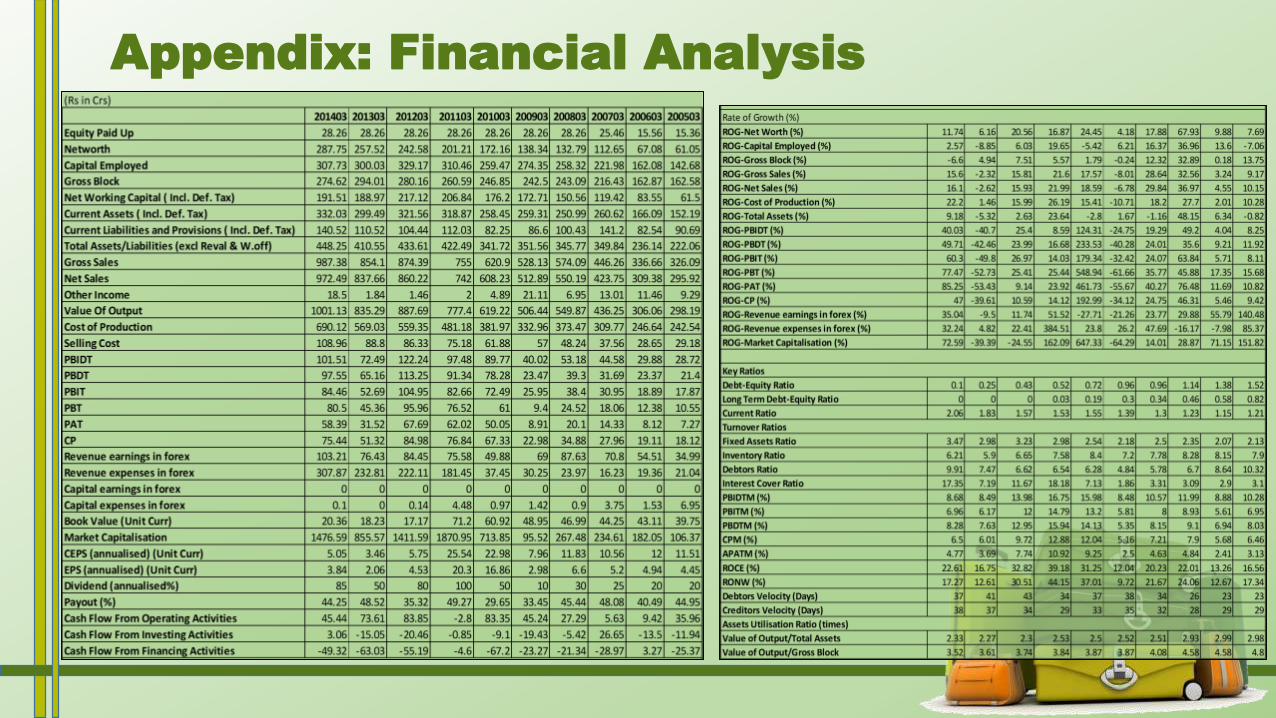

Appendix: Financial Analysis

Appendix: Futuristic Suitcases