Strategic Advisors in Global Energy - World...

26

Strategic Advisors in Global Energy Strategic Advisors in Global Energy Strategic Advisors in Global Energy The Financial Crisis and its Impact on the Oil & Gas Industry Prepared for World Bank Energy Week by Lew Watts March 2009

Transcript of Strategic Advisors in Global Energy - World...

Strategic Advisors in Global Energy Strategic Advisors in Global Energy Strategic Advisors in Global Energy

The Financial Crisis and its Impact on the Oil & Gas Industry

Prepared for World Bank Energy Week by Lew Watts

March 2009

World Bank Energy Week 2009 | Page 2

The “Oil Century” was said to be ending A new demand scenario?

Constrained Growth Higher prices promote reduced demand and

modest substitution

Demand Destruction High prices and pinched supply curtail

demand

Energy Transition Pinched supply and technological innovation lead to abandoning of the internal combustion

engine

Economic Shock reduces demand temporarily, slows development and defers solutions

World Bank Energy Week 2009 | Page 3

But the Oil and Gas industry has been hit with a triple whammy ...

§ A massive deleveraging by financial institutions contributed to a collapse in the price of oil.

§ A global economic slowdown is creating a real decline in the demand for oil which will persist for some years.

§ The drying up of new credit availability and more restrictive terms will hamper the normal business financing of some players.

… and perhaps a fourth whammy ... § Accelerating momentum towards carbon regulation.

World Bank Energy Week 2009 | Page 4

Oil Prices and Structural Trends

Oil became a financial / investment vehicle as well as a physical commodity

Oil became a financial / investment vehicle as well as a physical commodity

WTI Prompt Month Price

$0

$20

$40

$60

$80

$100

$120

$140

$160

Jan99

Jan

00 Jan

01 Jan

02 Jan

03 Jan

04 Jan

05 Jan

06 Jan

07 Jan

08

"Traditional" Price Structure

Oil as a Financial Asset

Demand Shock, Lack of Spare Capacity

World Bank Energy Week 2009 | Page 5

8%

6%

4%

2%

0%

2%

4%

6%

2002

2003

2004

2005

2006

2007

2008

YOY change in US monthly gasoline demand

Signs of significant demand destruction

Source: PFC Energy Downstream Monitoring Service

Oil price

Income effect/ recession

World Bank Energy Week 2009 | Page 6

Massive value destruction in value

BP

Chevron

Encana

BHP ExxonMobil

HAL Lukoil

Repsol

INPEX

RD Shell

Surgutneftegaz

Husky

Formosa

Transocean

Tokyo Gas Apache

Devon

COP

Centrica

PTT

Reliance

BG

TOTAL ENI

StatoilHydro

Occidental

XTO Petrobras

Hess

Gazprom

CNOOC

Ecopetrol

Schlumberger

ONGC

Rosneft

3‐Ye

ar Growth in

Marke

t Cap

italization

1‐Year Growth in Market Capitalization

EOG

IOCs

NOCs

E&P

R&M

Service Companies

Gas Companies

Other

Sinopec

Petrochina

CNQ

From PFC Energy 50

World Bank Energy Week 2009 | Page 7

Implications to Oil & Gas Companies

1. Some exploration programs and development projects will not be economic at the lower prices and will be deferred or cancelled.

2. Some companies – IOCs, NOCs, Independents and Service Companies – will not be able to find funding, resulting in delays, defaults and consolidation. Cash is King—but so is Paper…

3. Irrespective of demand destruction, a supply crunch still looms in the next decade.

4. Huge uncertainty on potential carbon legislative frameworks, timing and exposure.

World Bank Energy Week 2009 | Page 8

Cuts, Delays, Consolidation ... and Opportunities

World Bank Energy Week 2009 | Page 9

IOCs may have limited access—but control bulk of investment

NOC reserves (limited equity access)

Reserves held by Russian companies

Full IOC access

NOC reserves (equity access) Others

Top 10 IOCs

Top 10 NOCS

Source: PFC Energy NOC Strategy Service, Upstream Competition Service

World Bank Energy Week 2009 | Page 10

Oil & Gas sector investment cuts accelerating

§ The credit crisis caught independents off guard and the oil price fall weakened all players’ finances

§ Upstream cuts: Independents, and some IOCs (and NOCs) – Some IOCs postponing projects to negotiate lower EPC costs – Many other players unable to find financing

§ Most affected: new source developments in OECD

Source: PFC Energy Market Intelligence Service

World Bank Energy Week 2009 | Page 11

Downstream project delays in Middle East (by end 2008)

§ Middle East had enormous plans for petrochemical and other downstream projects by 2015

§ These plans increasingly in doubt as project sponsors retrench from significant investment activity during a period of uncertainty

§ Most Downstream projects in pipeline threatened with cancelation or delay

Source: PFC Energy Market Intelligence Service

World Bank Energy Week 2009 | Page 12

Fewer LNG trains will be added in the future…

0

2

4

6

8

10

12

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

# trains Liquefaction Trains Added

3year avg

Source: PFC Energy Global LNG Service

World Bank Energy Week 2009 | Page 13

Lessons from 1998 – more consolidation?

§ Of 74 larger E&P Independents that produced a combined 6.5 mmboe/d in 1995, only 32 still existed in 2007

§ Most mergers were between independents and occurred in 1999 to 2002, when oil price was ~$1125

41 Independents Acquired, by Type of Acquirer

0 1 2 3 4 5 6 7 8

1998 2000 2002 2004 2006 Independent Major Other

Source: PFC Energy Upstream Competition Service

World Bank Energy Week 2009 | Page 14

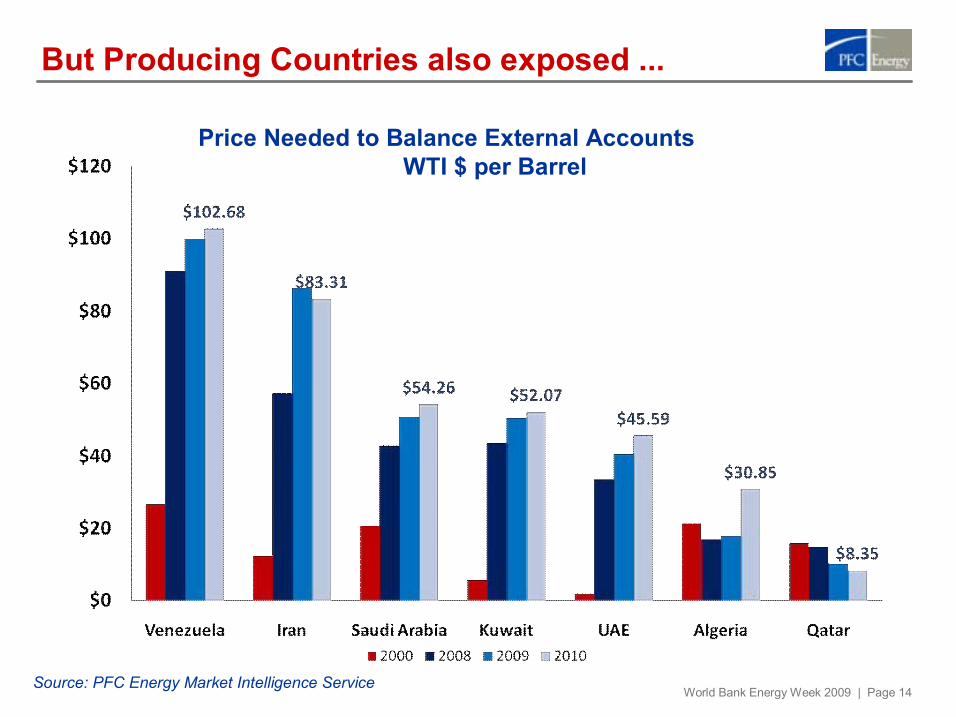

But Producing Countries also exposed ...

Price Needed to Balance External Accounts WTI $ per Barrel

Source: PFC Energy Market Intelligence Service

World Bank Energy Week 2009 | Page 15

Cracks in NOC landscape combined with financial stress also create opportunities

Cap

acity

Time 2002 2010

Low

High

Saudi Aramco, Petrobras, CNPC, CNOOC, StatoilHydro

Rosneft, Sinopec, Gazprom, Petronas, LNOC, Sonatrach, QP, NIOC, Pemex, Sonangol, ONGC, KMG

Capacity is a function of: • Government mandate & support • Ability to manage rising costs • Money • People • Technology • Project management

Pertamina, NNPC, KPC, PDVSA

Source: PFC Energy NOC Competition Service

World Bank Energy Week 2009 | Page 16

0

100

200

300

400

500

600

700

800

900

0 5 10 15 20 25 30 35 40

US 803 cars

S. Korea 230 cars

China 26 cars

UK 457 cars

PPP GDP 000/Capita

Cars/Capita (000)

India 9 cars

Meanwhile, oil demand will continue to increase ...

Japan 450 cars

Cars per 1000 People vs. GDP/capita Historical Data 1970 2007

Source: PFC Energy

Without major technological change—Pickens’ gasification and/or electrification of fleet—transportation drives oil demand growth

World Bank Energy Week 2009 | Page 17

Production crunch delayed, but still in our future

Source: PFC Energy Global Liquids Supply Forecast

2020 call on OPEC ~50–70 mmb/d, given 1.1% 2.4% growth

OPEC liquids

NonOPEC crude and NGLs

World Bank Energy Week 2009 | Page 18

1980 1985 1990 1995 2000 2005 4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

9,000

0 1980 1985 1990 1995 2000 2005

million metric

tons

C

0

200

400

600

800

1000

1200

1400

1980

Num

ber o

f articles on

carbo

n em

ission

s And then there is climate change ...

Montreal Protocol

Earth Summit

Kyoto

CA AB 32

An Inconvenient Truth Oscar

IPCC/Gore Nobel Prize

Bali Conference

The Hague

New Delhi

Milan

World Bank Energy Week 2009 | Page 19

Value of emissions: 2007 2012

World Bank Energy Week 2009 | Page 20

The cost of Carbon – threat or opportunity?

base case 2012

World Bank Energy Week 2009 | Page 21

The cost of Carbon – threat or opportunity?

Oil Sands CCS

World Bank Energy Week 2009 | Page 22

The Cost of Carbon – threat or opportunity?

Oil Sands CCS

Additional 10% in energy efficiency

World Bank Energy Week 2009 | Page 23

The cost of Carbon – threat or opportunity?

Flaring

Additional 10% in energy efficiency

Oil Sands CCS

World Bank Energy Week 2009 | Page 24

In conclusion

§ At least 3 major issues threaten the oil and gas industry

§ Except for a few IOCs, major cuts and project deferrals

§ But short term, three sets of opportunities: – Potential increased access to NOC reserves – Reduced contractor prices – Acquisitions by stronger players among Independents and ServCos

§ Carbon regulation will force action

§ Longer term, a major oil supply crunch looms

World Bank Energy Week 2009 | Page 25

Thank You

PFC Energy consultants are present in the following locations:

} Bahrain

} Beijing

} Buenos Aires

} Calgary

} Houston

} Kuala Lumpur

} Lausanne

} London

} Mumbai

} New York

} Paris

} San Francisco

} Washington, D.C.

Strategic Advisors in Global Energy

Main regional offices:

Asia

PFC Energy, Kuala Lumpur Level 27, UBN Tower #21 10 Jalan P. Ramlee 50250 Kuala Lumpur, Malaysia Tel (60 3) 21723400 Fax (60 3) 20723599

Europe

PFC Energy, France 19 rue du Général Foy 75008 Paris, France Tel (33 1) 47702900 Fax (33 1) 47705905

__

PFC Energy International, Lausanne 19, Boulevard de la Forêt 1009 Pully, Switzerland See Map Tel (41 21) 7211440 Fax: (41 21) 7211444

Middle East

PFC Energy, Bahrain Flat 72, Building 2334, Road 2830, Al Seef 428, King Mohammed VI Avenue P.O. Box 11118 Manama, Kingdom of Bahrain Tel (973) 17580775 Fax (973) 17 581776

North America

PFC Energy, Washington D.C. 1300 Connecticut Avenue, N.W. Suite 800 Washington, D.C. 20036, USA Tel (1 202) 8721199 Fax (1 202) 8721219

__

PFC Energy, Houston 4545 Post Oak Place, Suite 312 Houston, Texas 770273110, USA Tel (1 713) 6224447 Fax (1 713) 6224448

www.pfcenergy.com | [email protected] Main regional offices are shown in blue.