Starbucks in Consumer FoodService - PUREpure.au.dk/portal/files/6292/bilag_2.pdf · Starbucks in...

23

Starbucks in Consumer FoodService November 2008

Transcript of Starbucks in Consumer FoodService - PUREpure.au.dk/portal/files/6292/bilag_2.pdf · Starbucks in...

Starbucks in Consumer FoodService

November 2008

2

© Euromonitor International >Starbucks – CFS

Strategic Evaluation

Competitive Positioning

Market Assessment

Recommendations

3

© Euromonitor International >Starbucks – CFSStrategic Evaluation

Key Company Facts

Starbucks

Name Starbucks Corp

Headquarters USA

Regional Involvement

North America, Western Europe,

Eastern Europe, Latin America,

Asia Pacific, Australasia, Middle

East and Africa

Sector Involvement Cafés/Bars

World % value share

(2007)2.9 share of Cafes/Bars

Value growth % (2006-

2007)24.5

Global leader in Cafés/Bars

Starbucks operates solely as a coffee specialist and

dominates the category, with a value share of 39% in

2007.

With a strong and growing international presence,

Starbucks is the top specialist coffee shop operator in

Asia Pacific, Latin America, North America and Western

Europe.

Starbucks’s largest presence is in the US, with around

70% of its total outlets in the country in 2007. The

company’s value share in chained specialist coffee

shops in the US is a remarkable 88%, and 67% when

including both chained and independents.

Operating income increased by nearly 18% in fiscal

2007, but the operating margin slightly dipped from

11.5% to 11.2% due in part to an increase in the cost of

goods, particularly dairy, higher rents and distribution

costs.

The US segment’s financial results slowed in 2007,

with lower levels of same-store sales. While some of

this was offset by two price increases, store traffic

overall has slowed as consumers faced increasing

prices for food and fuel.

Operating income up but margin down

4

© Euromonitor International >Starbucks – CFSStrategic Evaluation

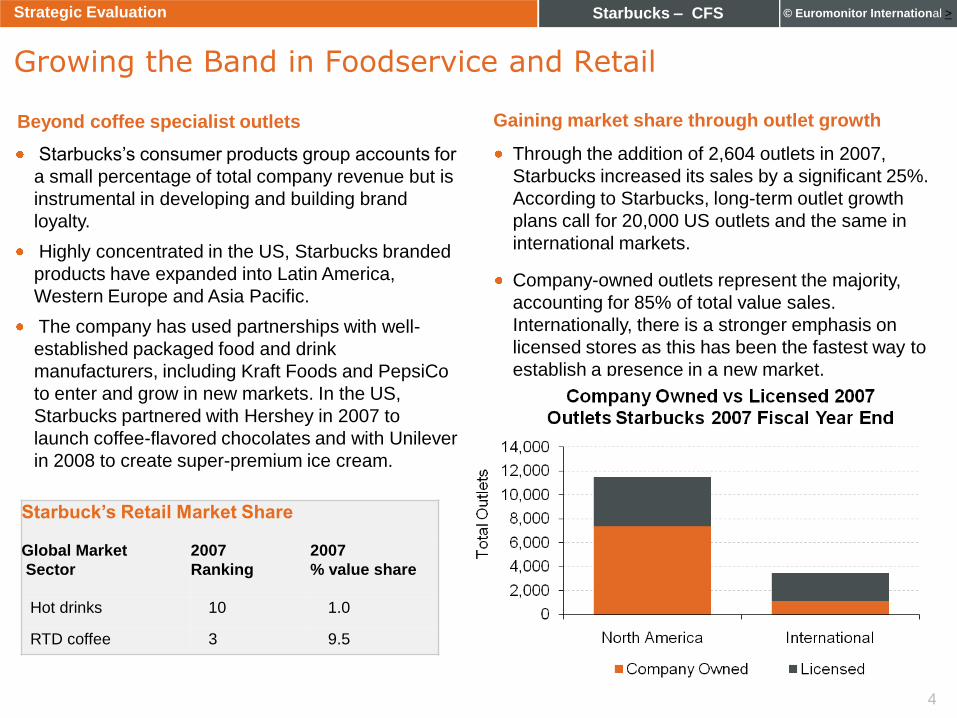

Growing the Band in Foodservice and Retail

Beyond coffee specialist outlets

Starbucks’s consumer products group accounts for

a small percentage of total company revenue but is

instrumental in developing and building brand

loyalty.

Highly concentrated in the US, Starbucks branded

products have expanded into Latin America,

Western Europe and Asia Pacific.

The company has used partnerships with well-

established packaged food and drink

manufacturers, including Kraft Foods and PepsiCo

to enter and grow in new markets. In the US,

Starbucks partnered with Hershey in 2007 to

launch coffee-flavored chocolates and with Unilever

in 2008 to create super-premium ice cream.

Through the addition of 2,604 outlets in 2007,

Starbucks increased its sales by a significant 25%.

According to Starbucks, long-term outlet growth

plans call for 20,000 US outlets and the same in

international markets.

Company-owned outlets represent the majority,

accounting for 85% of total value sales.

Internationally, there is a stronger emphasis on

licensed stores as this has been the fastest way to

establish a presence in a new market.

Gaining market share through outlet growth

Starbuck‟s Retail Market Share

Global Market

Sector

2007

Ranking

2007

% value share

Hot drinks 10 1.0

RTD coffee 3 9.5

5

© Euromonitor International >Starbucks – CFSStrategic Evaluation

Operating Philosophy

Reliance on fixed price contracts

Starbucks’s socially responsible foundation will

continue to be favourable particularly as a

greater number of consumers themselves become

more environmentally-conscious.

The company continues to publish an annual

Social Responsibility Report while other fast

food operators have only recently started to act

and market their corporate social responsibility

moves.

Central to Starbucks‟s socially responsible

philosophy is its C.A.F.E.. (Coffee and Farmer

Equity) Practices. These practices were designed

to ensure the coffee the company purchases is

produced in a responsible way.

Starbucks also places a strong emphasis on

excellent employee relations, referring to all

employees as partners.

These efforts have helped to shield the brand from

the typical scrutiny that most large multinational

chains receive. With aggressive international

growth plans in place these efforts will need to

continue.

Expanding globally and responsibly

Starbucks controls the impact of increased commodity

costs by entering into fixed price contracts or price

to be fixed contracts with coffee suppliers.

While these coffee contracts have shielded the

company historically, a stronger threat now stems

from increased dairy and other food costs.

Starbucks large global position should shield the

coffee specialist from experiencing too much damage

in terms of operating margin, but it has had to

implement two price increases in the US to

counteract these costs.

The US accounts for 75% of the companies total

dairy expense. As dairy prices can change

significantly in the short term this has impacted profit

margins in 2007 and will likely have a similar impact in

full year 2008.

Passing on rising costs through an increase in menu

prices is an unfavourable option as mounting food

and fuel costs have and will continue to impact

consumers‟ discretionary spending into 2009.

Starbucks will look to new product launches to

attract existing and new customers to increase their

frequency as well as their value per transaction.

6

© Euromonitor International >Starbucks – CFSStrategic Evaluation

SWOT – Starbucks

Opportunities

WeaknessesStrengths

Threats

Brand RecognitionLicensed International

Outlets

Asia Expansion Local Competition

Global Presence

Expanding Popularity

of Coffee

UK Market Reliance

Diluted Brand

The Starbucks brand is

well recognised and

synonymous with

premium coffee, helping

to attract consumers

looking for consistency

and convenience.

The company has

been the first chained

specialist coffee

operator in many

markets and continues

to benefit from its first

mover advantage.

While licensing

international outlets has

helped the company

quickly increase market

presence it does

weaken its overall

control.

Starbucks has 70% of

its outlets in the US,

where economic

conditions are currently

poor and the

competition from fast

food operators is

mounting.

China presents a unique

opportunity for Starbucks

as the coffee drinking

culture is still

undeveloped.

As the result of

Starbucks’s success and

quick expansion,

premium coffee

beverages are in high

demand and are

projected to continue to

be a popular affordable

luxury for most

consumers.

Competition continues to

escalate with

local/regional coffee

specialists increasing

their presence and fast

food operators

expanding their offerings

to attract consumers

seeking premium coffee

products.

As the company

continues to expand in

size so does the

authenticity and

premium platform on

which Starbucks has

relied upon to bolster

demand.

7

© Euromonitor International >Starbucks – CFSStrategic Evaluation

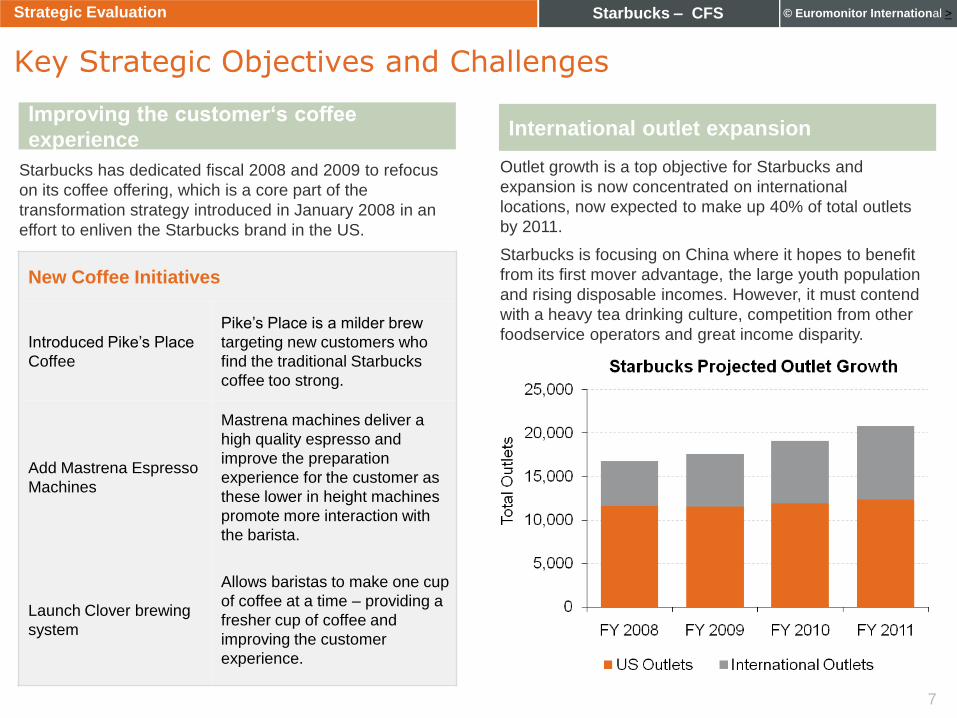

Key Strategic Objectives and Challenges

Improving the customer„s coffee

experienceInternational outlet expansion

Starbucks has dedicated fiscal 2008 and 2009 to refocus

on its coffee offering, which is a core part of the

transformation strategy introduced in January 2008 in an

effort to enliven the Starbucks brand in the US.

Outlet growth is a top objective for Starbucks and

expansion is now concentrated on international

locations, now expected to make up 40% of total outlets

by 2011.

Starbucks is focusing on China where it hopes to benefit

from its first mover advantage, the large youth population

and rising disposable incomes. However, it must contend

with a heavy tea drinking culture, competition from other

foodservice operators and great income disparity.

New Coffee Initiatives

Introduced Pike’s Place

Coffee

Pike’s Place is a milder brew

targeting new customers who

find the traditional Starbucks

coffee too strong.

Add Mastrena Espresso

Machines

Mastrena machines deliver a

high quality espresso and

improve the preparation

experience for the customer as

these lower in height machines

promote more interaction with

the barista.

Launch Clover brewing

system

Allows baristas to make one cup

of coffee at a time – providing a

fresher cup of coffee and

improving the customer

experience.

8

© Euromonitor International >Starbucks – CFSStrategic Evaluation

Defining the Experience

Health and wellness focus

Maintaining the “third” place atmosphere

Generating customer loyalty

Faced with an increasing amount of scrutiny regarding the

healthy position of its beverages and food items,

particularly in the US, Starbucks is focused on improving

its healthy product offering. The company has launched a

new beverage selection including Sorbetto’s and the

Vivanno smoothies, with the option to add Matcha Green

Tea Powder, as well as a selection of better-for-you

breakfast products in the US in 2008.

Starbucks has also changed its standard milk from full fat

to 2% fat in many of its markets. Additionally, it branded a

new selection of beverages using non-fat milk and sugar-

free syrup as “Skinny” in the US, the UK and Ireland.

Looking to maintain and build upon its loyal consumer

base, Starbucks launched a loyalty card programme in

2008. This card and other promotional initiatives will be

used to advertise new food and drink items encouraging

consumers to increase their store visits.

With plans to expand the loyalty card worldwide, cards

now exist in Hong Kong, Mexico and the UK with stand-

alone programmes in place in Japan, Spain and other

international markets.

Not traditionally a central part of Starbucks’s strategy,

loyalty programmes will become even more essential for

building customer loyalty and for tracking consumer

preferences in new markets as a result of increasing

levels of competition.

Starbucks is focused on maintaining its successful third

place positioning – a place between home and

work/school. While the US market has seen an

expanding number of outlets with drive-throughs,

Starbucks’s third place emphasis is an integral part of its

international market expansion strategy.

New US Breakfast Product Line

Starbucks Perfect Oatmeal

Power Protein Plate

Berry Stella

Apple Bran Muffin

Chewy Fruit and Nut Bar

Multigrain Roll with Spreads

9

© Euromonitor International >Starbucks – CFS

Strategic Evaluation

Competitive Positioning

Market Assessment

Recommendations

10

© Euromonitor International >Starbucks – CFSCompetitive Positioning

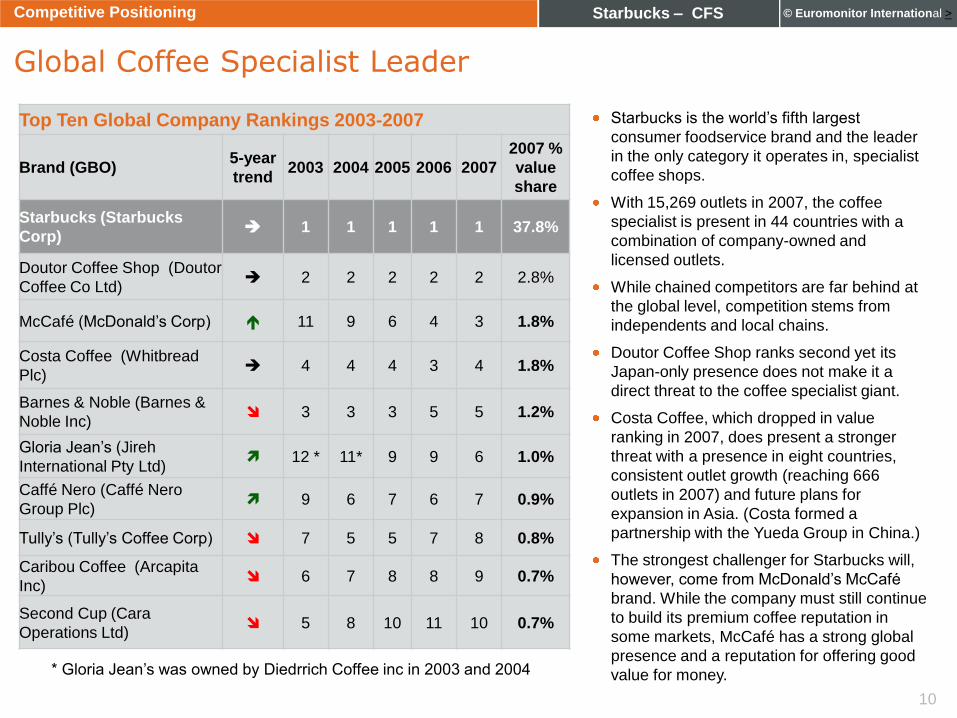

Global Coffee Specialist Leader

Top Ten Global Company Rankings 2003-2007

Brand (GBO)5-year

trend2003 2004 2005 2006 2007

2007 %

value

share

Starbucks (Starbucks

Corp) 1 1 1 1 1 37.8%

Doutor Coffee Shop (Doutor

Coffee Co Ltd) 2 2 2 2 2 2.8%

McCafé (McDonald’s Corp) 11 9 6 4 3 1.8%

Costa Coffee (Whitbread

Plc) 4 4 4 3 4 1.8%

Barnes & Noble (Barnes &

Noble Inc) 3 3 3 5 5 1.2%

Gloria Jean’s (Jireh

International Pty Ltd) 12 * 11* 9 9 6 1.0%

Caffé Nero (Caffé Nero

Group Plc) 9 6 7 6 7 0.9%

Tully’s (Tully’s Coffee Corp) 7 5 5 7 8 0.8%

Caribou Coffee (Arcapita

Inc) 6 7 8 8 9 0.7%

Second Cup (Cara

Operations Ltd) 5 8 10 11 10 0.7%

Starbucks is the world’s fifth largest

consumer foodservice brand and the leader

in the only category it operates in, specialist

coffee shops.

With 15,269 outlets in 2007, the coffee

specialist is present in 44 countries with a

combination of company-owned and

licensed outlets.

While chained competitors are far behind at

the global level, competition stems from

independents and local chains.

Doutor Coffee Shop ranks second yet its

Japan-only presence does not make it a

direct threat to the coffee specialist giant.

Costa Coffee, which dropped in value

ranking in 2007, does present a stronger

threat with a presence in eight countries,

consistent outlet growth (reaching 666

outlets in 2007) and future plans for

expansion in Asia. (Costa formed a

partnership with the Yueda Group in China.)

The strongest challenger for Starbucks will,

however, come from McDonald’s McCafé

brand. While the company must still continue

to build its premium coffee reputation in

some markets, McCafé has a strong global

presence and a reputation for offering good

value for money.* Gloria Jean’s was owned by Diedrrich Coffee inc in 2003 and 2004

11

© Euromonitor International >Starbucks – CFSCompetitive Positioning

Competition Expands Beyond Coffee Specialists

Starbucks competes increasingly against a number of

categories, as foodservice operators try to capitalise on

the popularity of premium coffee and breakfast on-the-go.

While the most direct competition stems from coffee

specialist shops, fast food competitors also pose a threat

with their strong brand recognition, reputation as a

breakfast/snack destination and global presence.

Fast food operators are increasingly becoming, for

consumers, a one-stop location for premium coffee,

breakfast, snacks in addition to their typical lunch/dinner

focus.

Bakery products fast food brands perhaps offer the

strongest threat to Starbucks as they already are a

morning destination for many consumers. While the

largest global brands, Dunkin’ Donuts and Tim Hortons

have the strongest presence in North America, other

smaller chains including Paris Baguette and Mister Donut

are quite popular in Asia.

Starbucks has historically set itself apart from fast food

operators by serving speciality coffee, but the slowdown

in the global economy will likely intensify the competition

as consumers seek out the better value over a name

brand.

Starbucks hopes its recent new breakfast menu will help

attract those consumers who have been drawn to these

fast food outlets for both their speciality coffee and

expanding breakfast selection.

Leading Competitive Bakery Products Fast Food

Brands - 2007 Outlets*

Dunkin’ Donuts 7,386

Tim Hortons 3,223

Mister Donut 1,778

Paris Baguette 1,650

Expanded Beverage Offerings Fast Food Brands

McDonald’s

To introduce speciality coffee beverages to all

US locations by the end of 2009.

Internationally looks to expand the McCafé

brand. In 2007 there were already 1,370

outlets worldwide.

Wendy’s

Began testing a line of ice coffee drinks in

several US states in 2008, including a

variation on the Frosty, called Frosty-cino.

Subway

Sandwich specialist Subway launched a new

concept called the Subway Café in

Washington D.C. in 2008 serving sandwiches,

gelato as well as speciality coffee drinks.

* Excludes sandwich specialist

12

© Euromonitor International >Starbucks – CFSCompetitive Positioning

Chained vs Independent Coffee Specialist Shops

With 71,516 total specialist coffee shops, chained players account for the majority, with Starbucks by far the

market leader.

The independent sector, with 28,065 outlets in 2007, has a strong outlet presence yet its share of total value

is much smaller at 24%.

This high concentration of chains in specialist coffee shops, really as a result of Starbucks’s position, is

unique as other café/bars and full-service restaurants have a much higher percentage of independents in

both value and outlets.

Almost half of the world’s independent specialist coffee shops are located in Asia Pacific, mainly Vietnam

where small local specialist coffee shops target only a select customer group such as musicians, financial

professionals etc. with a unique style or product selection.

Independents continue to hold their own and have seen consecutive growth in outlets and value with a value

increase of 7% in 2007.

Starbucks’s expansion has likely helped independents as the brand has attracted new consumers to

speciality coffee.

The strongest competitive threat for Starbucks, however, will come from local and smaller international

chains which have also benefited from the growing demand for specialist coffee.

13

© Euromonitor International >Starbucks – CFSCompetitive Positioning

When it Comes to Market Value, Starbucks Takes the Lead

Top Coffee Specialist Brands – Total Outlets

14

© Euromonitor International >Starbucks – CFS

Strategic Evaluation

Competitive Positioning

Market Assessment

Recommendations

15

© Euromonitor International >Starbucks – CFSMarket Assessment

Foodservice Value Growth: Starbucks vs The Market

A Starbucks has been the growth driver of specialist coffee shops through its own expansion and by

creating a coffee culture that did not exist in most markets.

B Despite a slowdown in US store traffic in 2007, the addition of over 2,600 outlets worldwide helped

the company achieve another year of over 20% growth.

16

© Euromonitor International >Starbucks – CFSMarket Assessment

Opportunities Across All Regions

Only the North American market is nearing maturity - future value growth reliant on successful new product launches.

Western Europe is the most promising market, yet Starbucks must contend with strong competition from local chains.

While Asia Pacific’s projected compound annual growth rate (CAGR) is not as optimistic as other regions, North

America the only exception, the region is projected to add nearly US$2 billion in value, second only to Western

Europe.

Opportunity Zone

17

© Euromonitor International >Starbucks – CFSMarket Assessment

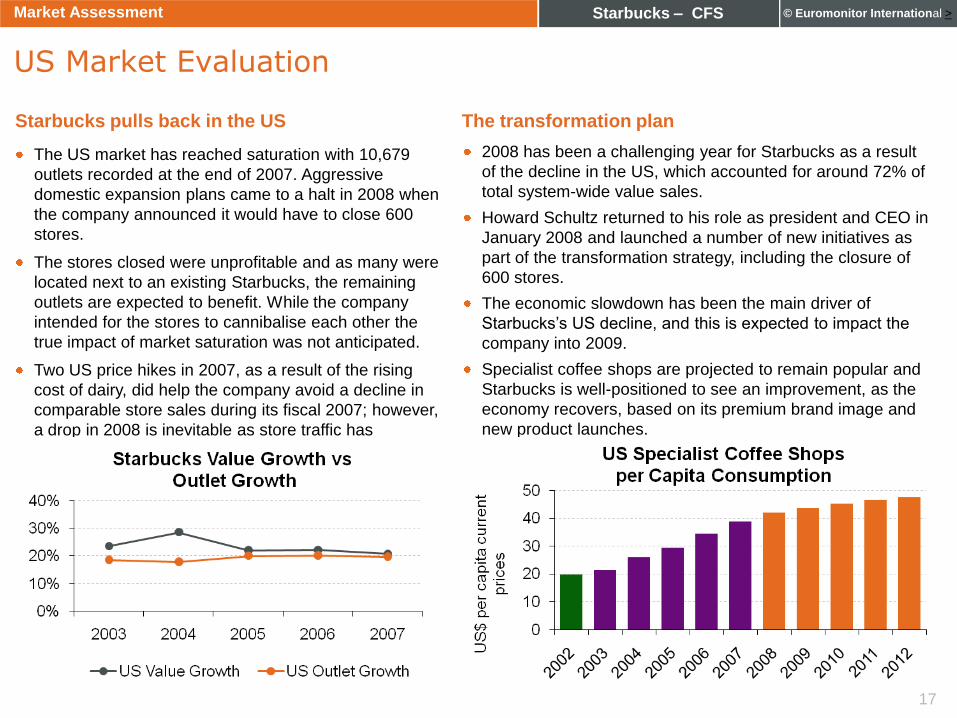

US Market Evaluation

The US market has reached saturation with 10,679

outlets recorded at the end of 2007. Aggressive

domestic expansion plans came to a halt in 2008 when

the company announced it would have to close 600

stores.

The stores closed were unprofitable and as many were

located next to an existing Starbucks, the remaining

outlets are expected to benefit. While the company

intended for the stores to cannibalise each other the

true impact of market saturation was not anticipated.

Two US price hikes in 2007, as a result of the rising

cost of dairy, did help the company avoid a decline in

comparable store sales during its fiscal 2007; however,

a drop in 2008 is inevitable as store traffic has

continued to decline.

Starbucks pulls back in the US

2008 has been a challenging year for Starbucks as a result

of the decline in the US, which accounted for around 72% of

total system-wide value sales.

Howard Schultz returned to his role as president and CEO in

January 2008 and launched a number of new initiatives as

part of the transformation strategy, including the closure of

600 stores.

The economic slowdown has been the main driver of

Starbucks’s US decline, and this is expected to impact the

company into 2009.

Specialist coffee shops are projected to remain popular and

Starbucks is well-positioned to see an improvement, as the

economy recovers, based on its premium brand image and

new product launches.

The transformation plan

18

© Euromonitor International >Starbucks – CFSMarket Assessment

Obstacles Facing the US Segment

Obstacle Starbucks Reaction and the Implication2008

Impact

2012

Impact

Competition:

Fast food brands have

introduced their own

specialty coffee

brands and are

pushing those to

consumers seeking

value for money.

Starbucks in turn has focused its attention on delivering a quality coffee product.

Starbucks has launched a loyalty and promotional programme hoping to retain

customers and increase daily visits. To help attract consumers looking for

convenience the company plans to open more drive-throughs which have been a

success. The alternative value beverage offering from fast food operators will attract

consumers faced with higher food and fuel costs but in the long term Starbucks‟s

premium position will help it maintain a more selective coffee consumer. The

key challenge will be maintaining their interest particularly with an increasing number

of smaller chains and independents emphasising their coffee expertise .

Unhealthy image:

Continued media

scrutiny regarding the

calorie count of

restaurant items in the

US has brought

Starbucks’s high-

calorie menu to the

forefront.

Starbucks built its brand by offering a wide selection of often sweet high-caloric

beverages. With more consumers looking for healthy alternatives Starbucks

has responded with the launch of Vivanno, a fruit-based smoothie and five

new healthy breakfast items. These new products are unlikely to change the

brand’s unhealthy image in the short term but this is not expected to have a great

impact as Americans are expected to continue to indulge. The new products

should also help attract new consumers looking for a non-coffee alternative or

increase the spend of existing customers.

Weakening US

economy:

Consumers have seen

their disposable

incomes shrink as a

result of higher food

and fuel costs.

Once considered an affordable luxury for the masses, Starbucks has been impacted

by the slowdown in the economy and this will continue to put downward

pressure on traffic. Poor US performance has been tied to stores in Florida and

California where consumers have been particularly hurt by the housing downturn.

The company is said to be testing smaller cups of drip coffee with free refills for

US$1; however, this type of tactic is unlikely to reverse the traffic declines. Starbucks

is better off maintaining its premium status and driving traffic through new

product launches or loyalty programmes, initiatives that are more likely to reap

benefits over the long term.

High Impact

Low impact

19

© Euromonitor International >Starbucks – CFSMarket Assessment

International Market Evaluation

Starbucks steadily expands abroad Current hurdles

Following the addition of five new countries in

2006/2007, Starbucks also added new locations

to Argentina and the Czech Republic in 2008 and

plans to expand into Poland, Hungary, Colombia

and India.

In 2008, Starbucks partnered with SSP, the

leading food and beverage brand operator in

travel locations, to open 150 outlets in airports

across Europe concentrating on France,

Germany and the UK. These travel locations can

be extremely profitable because of the semi-

captive, high disposable income and typically

international audience that uses airports.

In some countries, Starbucks faces an existing coffee culture

with competitive local chains; in others, it must create a coffee

culture that does not exist. Starbucks has so far been

successful in entering new markets, with its premium product

and aspirational brand, particularly those where there is a

young, high disposable income consumer base.

However, as consumers are faced worldwide with shrinking

disposable incomes Starbucks will need to justify its high price

or risk becoming a commodity. Already the impact is apparent

with the UK market in 2008 showing a slowdown in traffic as a

result of rising food prices.

Starbucks has had a more challenging time within the Australian

market, with an existing coffee culture and where consumers

have not been drawn into the novelty of the Starbucks brand.

While this does not impact the brand’s global share it is an

indication that the brand is not always going to be met with

open arms, and Starbucks must remain aware of the local

chains and customs inherent to each market.

2008 Starbucks

announced plans to close

61 Australian outlets –

80% of total stores

2006/2007 New Market Entries

Total 2007 Outlets

Brazil - 5

Egypt - 7

Denmark - 2

Romania - 2

Russia - 2

20

© Euromonitor International >Starbucks – CFSMarket Assessment

International Challenges and Opportunities

Starbucks is hedging on international expansion to lessen its

dependence on the US, increase sales and improve shareholder

value.

Global expansion on the surface looks to be promising with a

number of markets projecting outlet expansion influenced in part

by Starbucks’s expansion plans.

While short term the company will face a challenging market

environment, unlike in the US, there is still room for expansion

internationally and value growth can be gained through the

addition of new outlets.

International locations with comfortable seating and a localised

food offering will benefit from consumers looking for a place to

socialise, eat and drink.

China is a major target for Starbucks, where it has

already seen a positive response to the 259 outlets in

2007 and as a result is now focusing on small to medium-

sized Chinese cities.

Favourable demographics make China an obvious target

and is expected to be Starbucks’s second largest market.

The growing number of expatriates and citizens that have

returned to their homeland from abroad is expected to

help fuel an interest in coffee and the “third place”

positioning is increasingly attractive to Chinese people

looking for a place to socialise with friends.

In 2- and 3-tier cities, Starbucks faces strong competition

from local and global cafés/bar chains and independents

and a completely nonexistent coffee culture. Starbucks

has the resources to expand more quickly but its success

will be dependent on the general public’s willingness to

pay a premium for speciality beverages. 12

Starbucks, like others, looks to ChinaFinding growth opportunities abroad

Starbucks % Value Market Share – China

2006 2007

Total Cafés/bars 1.0 1.2

Chained Cafés/bars 4.5 4.7

Chained Specialist coffee shops 39.4 40.0

21

© Euromonitor International >Starbucks – CFS

Strategic Evaluation

Competitive Positioning

Market Assessment

Recommendations

22

© Euromonitor International >Starbucks – CFSRecommendations

Premium Experience and International Expansion

Over saturation may weaken the value of the

brandUnderstanding local preferences crucial for

international expansion in 2-tier cities

As Starbucks expands so will its competitors in both

type and number. The US market has already seen an

increasing number of fast food operators improve their

coffee offering. In international markets, competition will

come from independents and local chains that can

quickly adapt to consumer demand. Starbucks would be

wise to continue responding to these challenges through

promotional campaigns and its loyalty rewards card

programme rather than offering a lower quality product

that threatens the premium positioning of the brand.

Remain mindful of all levels of competition

New food products and non-coffee beverages

launched in the US should help increase store traffic

and attract new consumers; however, this shift in

focus may put off those core coffee consumers that

are an essential part of the company’s success.

Starbucks will benefit from finding ways to improve its

coffee offering and consistency in quality rather than

diversifying its product range. While food and non-

coffee beverages are a great way to increase the

average transaction value if they become a substitute,

coffee enthusiasts will seek out a higher quality

product and experience elsewhere.

New products should not alienate core coffee

consumers

The company’s concentration on international expansion

is wise as it currently remains too dependent on the US

market. While expansion in major cities should continue

to be well-accepted the challenge will be to appeal to a

wider consumer base in smaller cities where consumers

typically have lower incomes and coffee cultures are

often nonexistent. Starbucks would benefit from

remaining culturally attuned to local preferences,

adjusting prices accordingly, localising food and

beverage and adapting stores to consumer demand.

Crucial to Starbucks’s success is its premium brand

positioning. While outlet expansion across the US and

internationally drove value growth and increased the

popularity of speciality coffee there is a point at which

market saturation can dilute a brand’s premium

positioning. In an effort to avoid becoming a sterile fast

food brand, Starbucks should not lose focus on its “third

place” positioning, particularly in International locations

where consumers seek out a place to relax and socialise.

23

© Euromonitor International >Starbucks – CFS

Global Briefings Global Company Profiles Country Market Insight Reports

Interactive Statistical Database Strategy Briefings Learn More

The state of the market globally and regionally, emerging trends and pressing industry issues: timely, relevant insight published every month.

The competitive positioning and strategic direction of the leading companies including uniquely sector-specific sales and share data.

The key drivers influencing the industry in each country; comprehensive coverage of supply-side and demand trends and how they shape the future outlook.

Market sizes, market shares, distribution channels and forecasts; the complete market analysed at levels of category detail beyond any other source.

Executive debate on the global trends changing the consumer markets of the future.

To find out more about Euromonitor International's complete range of business intelligence on industries, countries and consumers please visit www.euromonitor.com or contact your local Euromonitor International office:

London + 44 (0)20 7251 8024

Chicago +1 312 922 1115

Singapore +65 6429 0590

Shanghai +86 21 63726288

Vilnius +370 5 243 1577

Dubai +971 4 609 1340

Experience more...

This research from Euromonitor International is part of a global strategic intelligence

system which offers a complete picture of the commercial environment . Also available

from Euromonitor International: