Standards Moscow 2013 Derivatives Usage and Reports

38

MT Standards Derivatives: Usage and Reports Moscow, 11 April 2013 Francoise Massin, Business Registration Authority, SWIFT Standards

-

Upload

swift -

Category

Economy & Finance

-

view

904 -

download

1

Transcript of Standards Moscow 2013 Derivatives Usage and Reports

MT Standards Derivatives:

Usage and Reports

Moscow, 11 April 2013

Francoise Massin, Business Registration Authority, SWIFT Standards

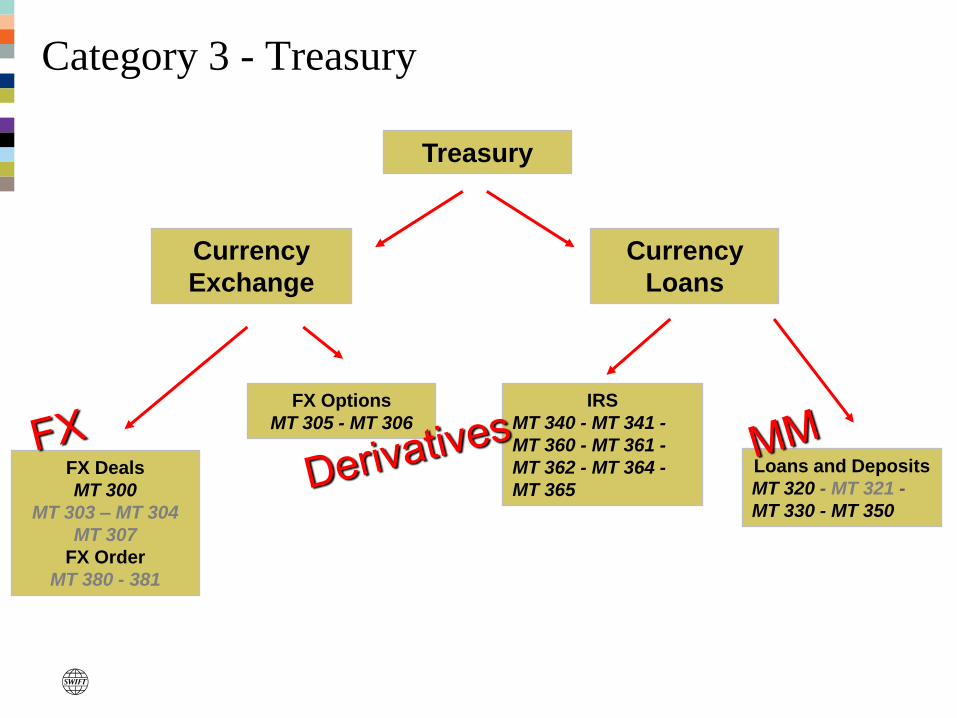

Treasury

Currency

Exchange

Currency

Loans

FX Deals

MT 300

MT 303 – MT 304

MT 307

FX Order

MT 380 - 381

Loans and Deposits

MT 320 - MT 321 -

MT 330 - MT 350

FX Options

MT 305 - MT 306

IRS

MT 340 - MT 341 -

MT 360 - MT 361 -

MT 362 - MT 364 -

MT 365

Category 3 - Treasury

FX Derivatives

MT 300 - Derivatives

Forward

Swap NDF

MT 300 - Derivatives

Forward

Forward

Sequences of MT 300

A - General information

B – Transaction details

C – Optional information

D – Split settlement details

E – Reporting information

Trade Date

Value Date

Exchange Rate

Amount Bought

Currency and Amount

Settlement Instructions

Amount Sold

Currency and Amount

Settlement Instructions

Value Date – Trade Date > 2 Days

MT 300 - Derivatives

Forward

Swap NDF

MT 300 - Derivatives

Swap

Swap Flows

MT 300: Spot

Trade Date

Value Date1

Exchange Rate

Amount Bought

Currency1 and Amount

Settlement Instructions

Amount Sold

Currency2 and Amount

Settlement Instructions

time

Value Date 2 Value Date 1 Trade Date

Swap Flows

MT 300: Spot

MT 300: Forward

Trade Date

Value Date1

Exchange Rate

Amount Bought

Currency1 and Amount

Settlement Instructions

Amount Sold

Currency2 and Amount

Settlement Instructions

Trade Date

Value Date2

Exchange Rate

Amount Bought

Currency2 and Amount

Settlement Instructions

Amount Sold

Currency1 and Amount

Settlement Instructions

time

Value Date 2 Value Date 1 Trade Date

MT 300 - Derivatives

Forward

Swap NDF

MT 300 - Derivatives

NDF

NDF

Sequences of MT 300

A - General information

B – Transaction details

C – Optional information

D – Split settlement details

E – Reporting information

References

Operation Characteristics

Parties

Master Agreement Information

Terms and Conditions

Valuation Date

Settlement Currency

Settlement Rate Source

Fixing Reference (Closing)

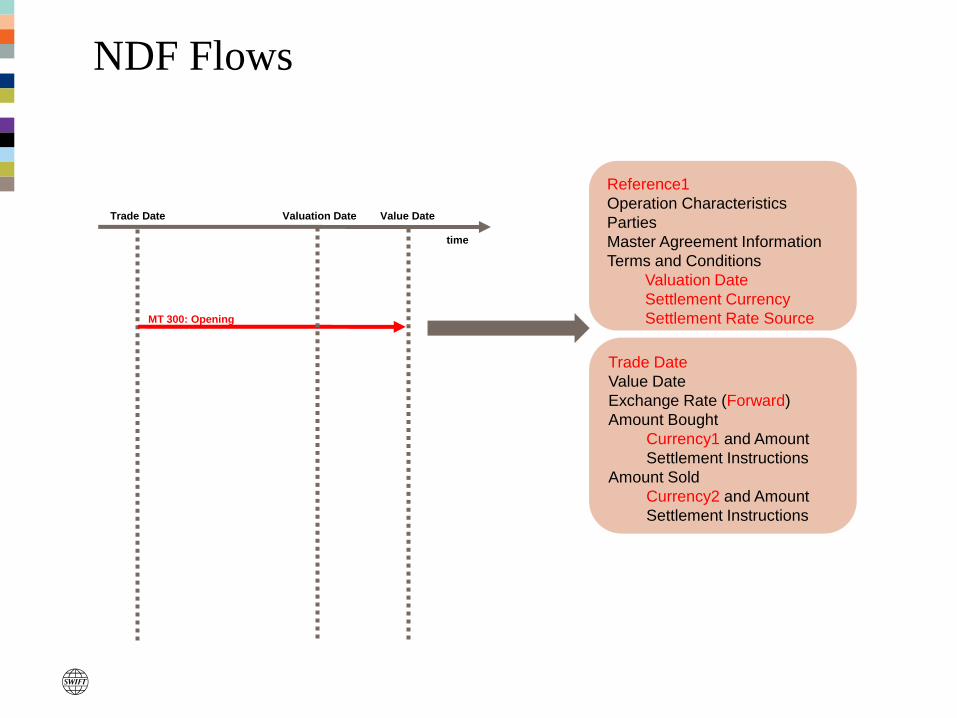

NDF Flows

MT 300: Opening

Trade Date

Value Date

Exchange Rate (Forward)

Amount Bought

Currency1 and Amount

Settlement Instructions

Amount Sold

Currency2 and Amount

Settlement Instructions

time

Value Date Trade Date

Reference1

Operation Characteristics

Parties

Master Agreement Information

Terms and Conditions

Valuation Date

Settlement Currency

Settlement Rate Source

Valuation Date

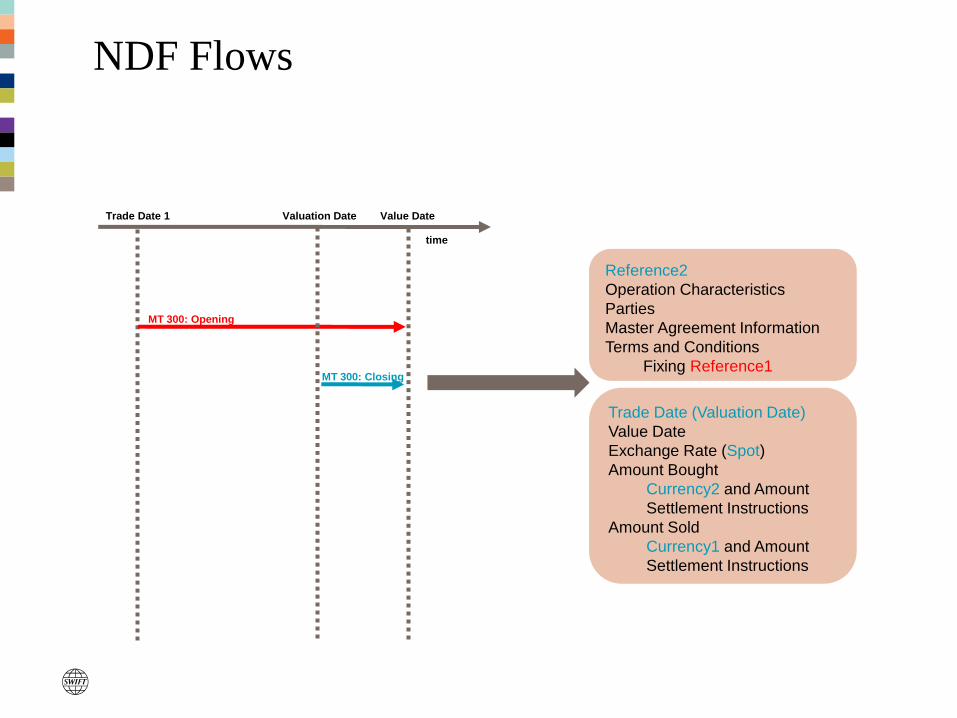

NDF Flows

MT 300: Opening

MT 300: Closing

time

Value Date Trade Date 1 Valuation Date

Trade Date (Valuation Date)

Value Date

Exchange Rate (Spot)

Amount Bought

Currency2 and Amount

Settlement Instructions

Amount Sold

Currency1 and Amount

Settlement Instructions

Reference2

Operation Characteristics

Parties

Master Agreement Information

Terms and Conditions

Fixing Reference1

Options

MT 305 MT 306

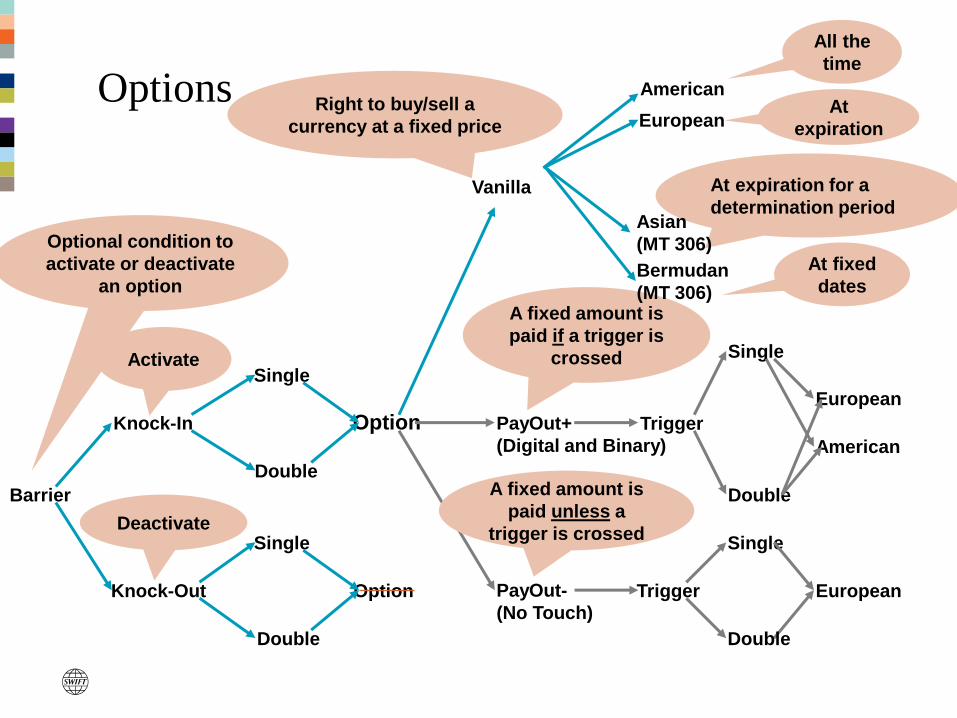

Options

Barrier Knock-In

Knock-Out

Double Option American

Trigger

Vanilla

Bermudan

Knock-Out PayOut- Trigger

Single

Single

European

Double

Double

Knock-In Single

PayOut+ Option

Double

Asian

Options

Vanilla

European

American

Barrier

Knock-Out Option PayOut- Trigger

Single Single

American

European

Single

European

Double Double

Double

Knock-In

Single

PayOut+ Option Trigger

Double

Bermudan

Asian

Options

Barrier

Knock-Out Option PayOut-

(No Touch) Trigger

Single Single

American

European

Single

European

Double Double

Double

Knock-In

Single

PayOut+

(Digital and Binary)

Option Trigger

Double

Optional condition to

activate or deactivate

an option

Activate

Deactivate

Right to buy/sell a

currency at a fixed price

A fixed amount is

paid if a trigger is

crossed

A fixed amount is

paid unless a

trigger is crossed

At fixed

dates

At

expiration

All the

time

Vanilla At expiration for a

determination period

European

American

Bermudan

(MT 306)

Asian

(MT 306)

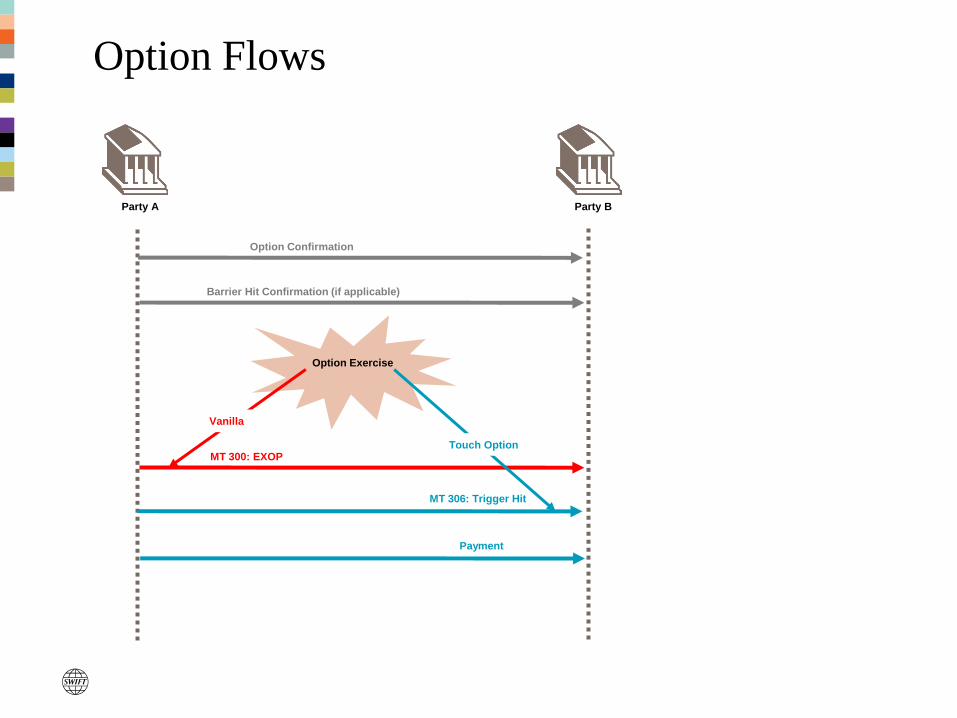

Option Flows

Option Confirmation

Party A Party B

Barrier Hit Confirmation (if applicable)

Option Exercise

MT 300: EXOP

Vanilla

MT 306: Trigger Hit

Touch Option

Payment

Commodities

MT 600 MT 601

Forward

Sequences of MT 600

A – Details of the Contract

B – Commodity Bought

C – Commodity Sold

D – Reporting information

Quantity

Parties

Value Date

Cash Amount

Value Date – Date Contract Agreed > 2 Days

References

Scope of Operation

Parties

Date Contract Agreed

Commodity + Price

Master Agreement

Option

Sequences of MT 601

A – Option

B – Reporting Information

Right to Buy or Sell a quantity

of a Commodity at a price

fixed in advance against a

premium.

PowerPoint Toolkit – 23 October 2008 – Confidentiality: restricted 24

Reporting

FX Derivatives - Reporting

• Collaboration with different repositories

• Mapping with their requirements

• Mapping with other standards

• Updates of the message formats for November 2013

25

Mapping Examples

NDF Examples

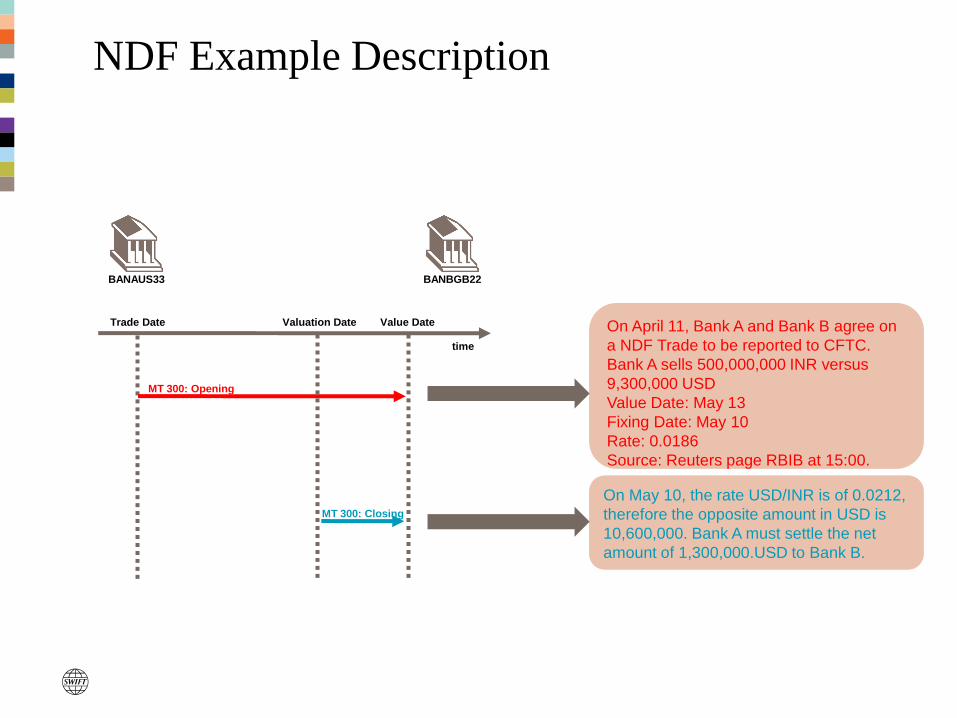

NDF Example Description

MT 300: Opening

On May 10, the rate USD/INR is of 0.0212,

therefore the opposite amount in USD is

10,600,000. Bank A must settle the net

amount of 1,300,000.USD to Bank B.

time

Value Date Trade Date On April 11, Bank A and Bank B agree on

a NDF Trade to be reported to CFTC.

Bank A sells 500,000,000 INR versus

9,300,000 USD

Value Date: May 13

Fixing Date: May 10

Rate: 0.0186

Source: Reuters page RBIB at 15:00.

Valuation Date

BANAUS33 BANBGB22

MT 300: Closing

NDF Example (I)

Tag Name Content

:15A: General Information

:20: Sender's Reference 123

:22A: Type of Operation NEWT

:22C: Common Reference BANA330186BANB22

:82A: Party A BANAUS33

:87A: Party B BANBGB22

:77D: Terms and Conditions

/VALD/ 20130510

/SETC/ USD

/SRCE/ RBIB USD/INR 1500

NDF Example (II)

Tag Name Content

:15B: Transaction Details

:30T: Trade Date 20130411

:30V: Value Date 20130513

:36: Exchange Rate 0.0186

B1 Amount Bought

:32B: Currency and Amount USD9300000,

:57J: Receiving Agent /NETS/

B2 Amount Sold

:33B: Currency and Amount INR500000000,

:57J: Receiving Agent /NETS/

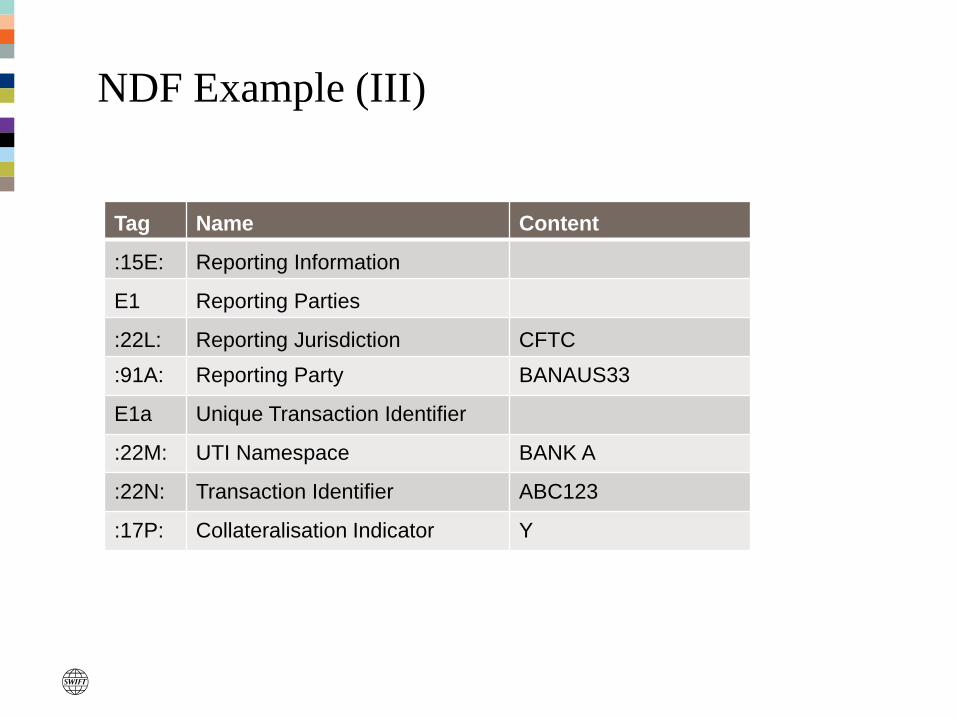

NDF Example (III)

Tag Name Content

:15E: Reporting Information

E1 Reporting Parties

:22L: Reporting Jurisdiction CFTC

:91A: Reporting Party BANAUS33

E1a Unique Transaction Identifier

:22M: UTI Namespace BANK A

:22N: Transaction Identifier ABC123

:17P: Collateralisation Indicator Y

NDF Closing (I)

Tag Name Content

:15A: General Information

:20: Sender's Reference 456

:22A: Type of Operation NEWT

:22C: Common Reference BANA330212BANB22

:82A: Party A BANAUS33

:87A: Party B BANBGB22

:77D: Terms and Conditions

/FIX/ 123

NDF Closing (II)

Tag Name Content

:15B: Transaction Details

:30T: Trade Date 20130510

:30V: Value Date 20130513

:36: Exchange Rate 0.0212

B1 Amount Bought

:32B: Currency and Amount INR500000000,

:57J: Receiving Agent /NETS/

B2 Amount Sold

:33B: Currency and Amount USD10600000,

:57J: Receiving Agent /NETS/

PowerPoint Toolkit – 23 October 2008 – Confidentiality: restricted 34

Option Example

Option Example Description

MT 305: Opening

On May 10, the rate EUR/CHF is of 1.145,

therefore Bank A exercises the option.

time

Value Date Trade Date

On April 11, Bank A and Bank B agree on

a Vanilla European Option Trade to be

reported to CFTC.

Bank A buys the right to sell 1,000,000

EUR versus sells 1,253,000 CHF

Value Date: May 13

Expiry Date May 10

Valuation Date

BANAUS33 BANBGB22

MT 300: Exercise

Option

Example

Tag Name Content

:15A: General Information

:20: Transaction Reference Number 789

:21: Related Reference NEW

:22C: Common Reference NEW/BANA331253BANB22

:23: Further Identification BUY/PUT/E/EUR

:82A: Party A BANAUS33

:87A: Party B BANBGB22

:30: Date Contract Agreed 130411

:31G: Expiry Details 130510/1000/USNY

:31E: Final Settlement Date 130513

:26F: Settlement Type PRINCIPAL

:32B: Underlying Currency and Amount EUR1000000,

:36: Strike Price 1.253

:33B: Counter Currency and Amount CHF1253000,

:37K: Premium Price PCT2.

:34P: Premium Payment EUR2000,

:57A: Account With Institution BANADEFF

Option

Exercise

Tag Name Content

:15A: General Information

:20: Sender's Reference DEF

:22A: Type of Operation EXOP

:22C: Common Reference BANA331253BANB22

:82A: Party A BANAUS33

:87A: Party B BANBGB22

:15B: Transaction Details

:30T: Trade Date 20130510

:30V: Value Date 20130513

:36: Exchange Rate 1.253

B1 Amount Bought

:32B: Currency and Amount CHF1253000,

:57A: Receiving Agent BANACHZH

B2 Amount Sold

:33B: Currency and Amount EUR1000000,

:57J: Receiving Agent BANBLULL

Thank you