Sponsored by: W. K. KELLOGG FOUNDATION · sustainable credit and banking options in ... from other...

12

KIRWAN INSTITUTE FOR THE STUDY OF RACE AND ETHNICITY THE OHIO STATE UNIVERSITY Regional Convening Notes: Austin, TX PRESENTED BY NOVEMBER 6, 2009 Hosted by Green Doors and Kirwan Institute for the Study of Race and Ethnicity FAIR HOUSING and FAIR CREDIT THE FUTURE OF Sponsored by: W. K. KELLOGG FOUNDATION

Transcript of Sponsored by: W. K. KELLOGG FOUNDATION · sustainable credit and banking options in ... from other...

KIRWAN INSTITUTE

FOR THE STUDY OF RACE AND ETHNICITY

THE OHIO STATE UNIVERSITY

Regional Convening Notes:Austin, TX

PRESENTED BY

NOVEMBER 6, 2009Hosted by Green Doors and Kirwan Institute for the Study of Race and Ethnicity

FAIR HOUSING and FAIR CREDIT

THEFUTURE

OF

Sponsored by: W. K. KELLOGG FOUNDATION

The Kirwan Institute for the Study of Race and Ethnicity is a university-wide interdisciplinary research institute. We generate and support innovative analyses that improve understanding of the dynamics that underlie racial marginality and undermine full and fair democratic practices throughout Ohio, the United States, and the global community. Responsive to real-world needs, our work informs policies and practices that produce equitable changes in those dynamics.

1

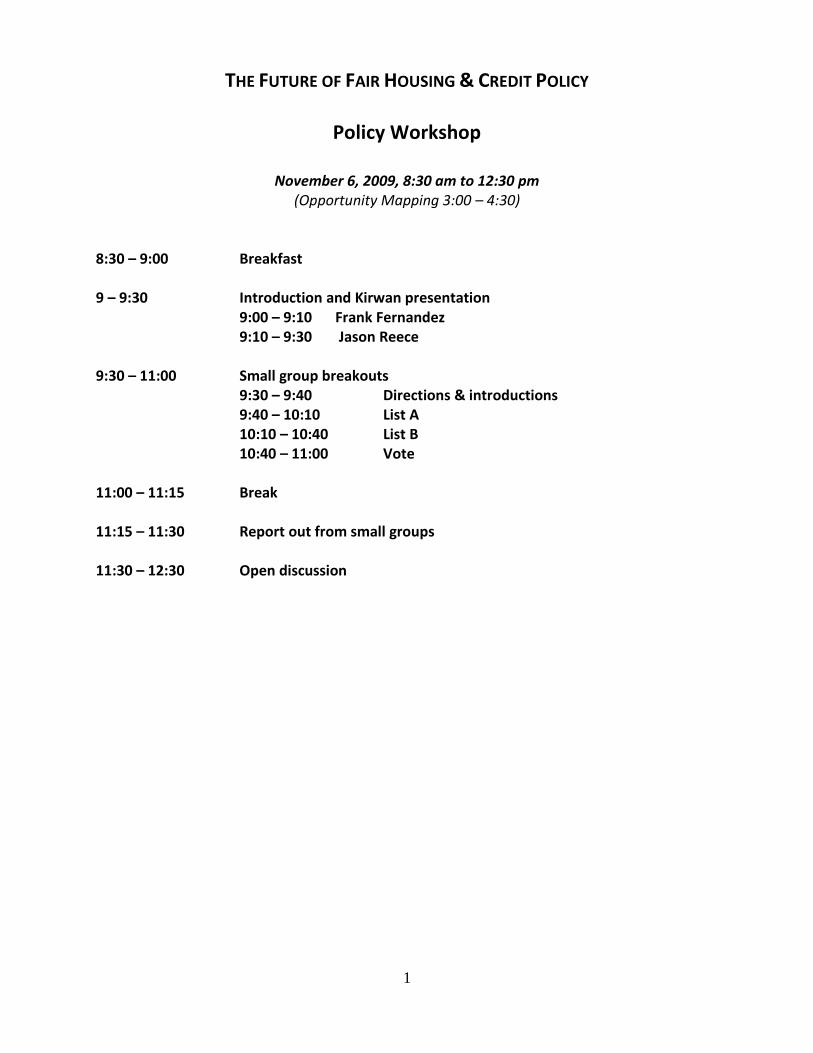

THE FUTURE OF FAIR HOUSING & CREDIT POLICY

Policy Workshop

November 6, 2009, 8:30 am to 12:30 pm (Opportunity Mapping 3:00 – 4:30)

8:30 – 9:00 Breakfast 9 – 9:30 Introduction and Kirwan presentation 9:00 – 9:10 Frank Fernandez 9:10 – 9:30 Jason Reece 9:30 – 11:00 Small group breakouts 9:30 – 9:40 Directions & introductions 9:40 – 10:10 List A 10:10 – 10:40 List B 10:40 – 11:00 Vote 11:00 – 11:15 Break 11:15 – 11:30 Report out from small groups 11:30 – 12:30 Open discussion

2

Directions for small group facilitators: I recommend that before you begin, have people in your small group introduce themselves (name and organization). Group A: Generate Lists On a large sheet(s) of paper, list barriers to fair financial options in Austin. This includes barriers to affordable, sustainable credit (mortgage, auto loan, short term loan, credit card, education, etc.) and banking services (bank accounts, debit cards, etc.). On a separate sheet(s) of paper, generate a list of potential solutions to address the lack of sustainable credit and banking options in Austin. Please indicate if they are aspirational solutions (i.e. “doesn’t exist yet in Austin”) or existing programs/practices, pilot programs, etc. Where you have local promising solutions, try to capture a fairly robust description (i.e. who runs the program, for how long, stable, etc.). Vote Once the two lists are made, have people take two stickers and “vote” for the two most troublesome barriers or challenges to fair credit. People are allowed to use both their stickers for one item if they feel it is clearly the most important. Next, have people take two stickers and “vote” for the two most promising solutions (aspirational or existing). Again, people may vote for two or one solutions. Here’s a simplified example of what you might generate when you’re done: Barriers/Challenges Solutions Consumer culture Community credit unions (i.e. XYZ) ****** Deceptive practices***** Payday lending legislation (just passed) *** Low wages** Financial counseling (run by Austin Legal)* Lack of enforcement of existing regulations*** State legal preemption (aspirational) ** People don’t trust banks**** Higher minimum wage (aspirational) ** Group B: You follow the same process, but your group discusses challenges to (and solutions for) affirmative neighborhood revitalization. Group C: You follow the same process, but your group discusses challenges to (and solutions for) opportunity-based housing.

Future of Fair Housing/Fair Credit

Austin, TX Regional Convening

November 06, 2009

Ranking Index:

Blue highlight: most votes

Red highlight: second-most votes

Yellow highlight: third-most votes

*indicates one vote, 4th

place

Community Revitalization

Barriers

Different context needs different approach

o Historic disinvested neighborhoods, ripe for reinvestment

o Core transit corridors

o New suburban/fringe/urban fringe

No CDC/local infrastructure

o Longitudinal approach, different drivers

City Planning

o Allowing poorly developed designs

o Planning not thinking of wide set of goals

Ex: transit transportation

o Lax planning

o No comprehensive/community vision

o What is the aspiration for the community?

Shared values, missions

No shared goals

No agreement that this is a public purpose

o No integration of plans

o Funding: public/private

Building w/o thinking of quality

Little state support/impact of bad economy

Austin reality

o Rapid population growth

o Attracting people from other places/states

o Cheaper housing but escalating construction

Lack of affordable housing

o Investment coming to transit areas

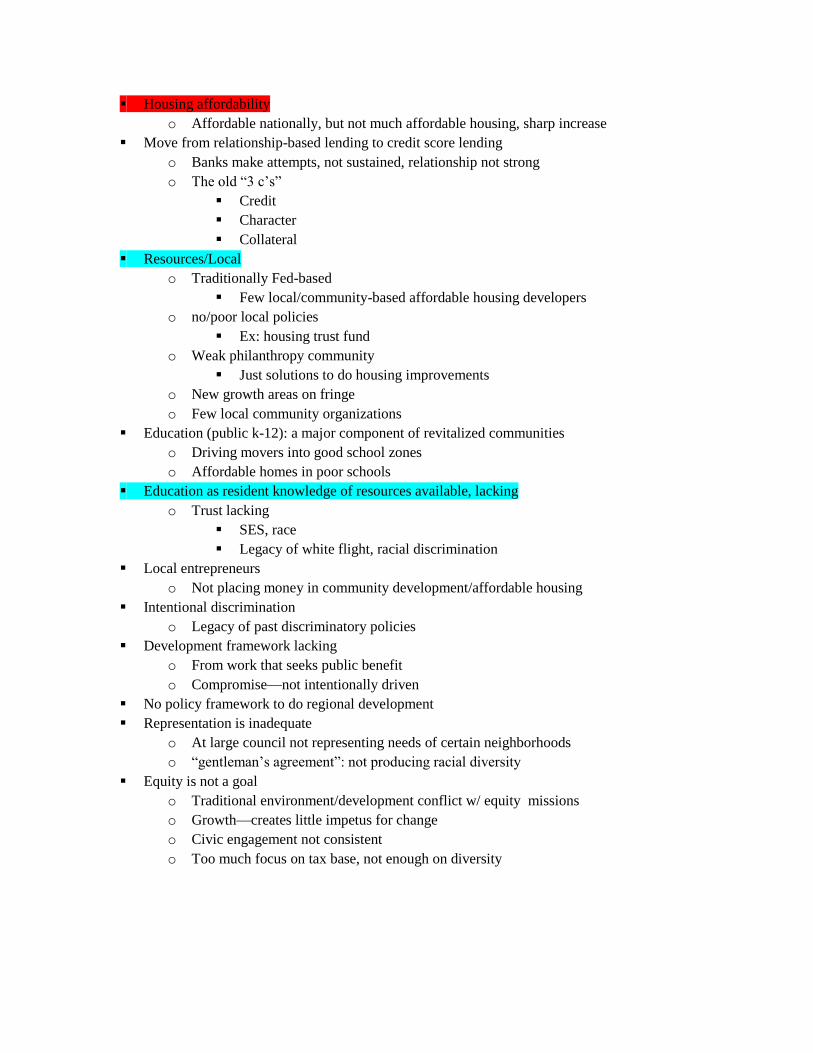

Housing affordability

o Affordable nationally, but not much affordable housing, sharp increase

Move from relationship-based lending to credit score lending

o Banks make attempts, not sustained, relationship not strong

o The old “3 c‟s”

Credit

Character

Collateral

Resources/Local

o Traditionally Fed-based

Few local/community-based affordable housing developers

o no/poor local policies

Ex: housing trust fund

o Weak philanthropy community

Just solutions to do housing improvements

o New growth areas on fringe

o Few local community organizations

Education (public k-12): a major component of revitalized communities

o Driving movers into good school zones

o Affordable homes in poor schools

Education as resident knowledge of resources available, lacking

o Trust lacking

SES, race

Legacy of white flight, racial discrimination

Local entrepreneurs

o Not placing money in community development/affordable housing

Intentional discrimination

o Legacy of past discriminatory policies

Development framework lacking

o From work that seeks public benefit

o Compromise—not intentionally driven

No policy framework to do regional development

Representation is inadequate

o At large council not representing needs of certain neighborhoods

o “gentleman‟s agreement”: not producing racial diversity

Equity is not a goal

o Traditional environment/development conflict w/ equity missions

o Growth—creates little impetus for change

o Civic engagement not consistent

o Too much focus on tax base, not enough on diversity

Solutions

Integrated vision for planning/development

o More district representatives

o Future-oriented but incorporate history/common history

Build common base for community, for kids as well

o Force developers to learn history of community

Needs of existing residents

Robust civic engagement

o Sustainable

o More ways to be included in process

o Show process respects their needs

Inclusive—Equity as a goal

o Building as a formal planning goal

More local funding/resources

o General obligation bonds for affordable housing

o More aligned with vision and comprehensive plan

o Dedicate fair housing trust fund

Education

o Revitalized communities must have good education options

o Link education and planning directly

More robust interactive policy toolbox

o Ex: land trusts

Inclusive housing/smart housing policy

o Useful but not effective

o Not as helpful on rental side

o Sustainable

o Needs to be mandated, how?

o Inclusive housing incentives?

Regional plan-brand

o Set affordable housing goals and link policy to goals

o Feed research continually into process, but also constant dialogue

Leadership/innovation, public/civic

o Education on policy issues

o Dialogue

o Constant leadership engagement

o Lots of info/no process for engagement

Stronger civic organizations

o Funding relationship w/ CDCs to city, hard to make demands

More community development involvement, more CDCs

More successes identified

o Identify mission-sensitive for-profit developers

Credit and Banking

Barriers

Lack of trust in banking

o Negative experiences

Education

o People from different countries not familiar with US system

o Previous negative experiences; knowing how to balance checkbook/maintain accounts

o More conceptual; too many assumptions; no experience

o People not aware of options, think they can‟t qualify for prime

o Confusing the issue? Regulated vs. non-regulated (still framed as “the banks”)

Discrimination

o Credit scoring

o Disproportionate loan denials to certain groups

Lack of alternative options

o “second chance” accounts

o System set up to make profit from fees

o No human-human relationship

Location/access/accessibility*

o Language barriers

o Physical proximity

o Outreach

Predatory targeting

How to make non-customers comfortable going into banks?

Access to information

o Disclosures don‟t give a full snapshot of outcomes from financial decisions

o Financial responsibility

Incentive structure of brokers

What are barriers to banks reaching out?

Solutions

Develop a targeted marketing approach for prime financial institutions

Develop “hybrid” products that combine “comfort” in the “money box” with safety of regulated

institutions*

Regulation for everyone

o But how to do w/o cutting off access?

Regulation on marketing? (outreach/advertising)

Move „point in time‟ before

o Before entering a bank, influencing the decision process at the front end

“Blue book” for banking

Expanded Self-Help model of CRL

Consumer empowerment beyond disclosures

o The bank has to convince me that they‟re giving me the best terms

Intermediary at the community level to ensure equal treatment for similarly situated borrowers

o Financial ombudsman

Change incentive structure of brokers, not tied to rate*

Collaborations

o With City for education

o With NPOs

Partnering with realtors to connect homebuyers to financial education classes

o Or include something on loan apps, asking if have attended a class

Partnerships between health insurers, housing

o Connection btw bankruptcy and health insurance

o Utility assistance programs

o Referral programs among different services—recognizing interconnections

Health bills

Housing/utility

o Comprehensive services can get to cultural differences

Disclosures earlier, not at the point of purchase

Opportunity-Based Housing

Barriers

Low-income pushed out of city

Foreclosures concentrated in “new” suburbs

70% of foreclosures are Latino households

Costs higher in higher-opportunity neighborhoods

NIMBYism

Problems of micro-inflation due to Austin‟s economic success/becoming high-cost area

Affordable housing concentrated in same area or in low-opportunity neighborhoods

Discrimination of different sorts against families, national origin, race

Even some low opportunity neighborhoods are unaffordable

Middle class folks are challenged

Retaining appropriate mix of business and cultural assets

Affordable housing not reaching intended market

Govt housing programs inadequate

o Geographic dispersion

o Need to hit low MFI levels

High opportunity neighborhoods have been given “free ride”

Lack of regionalism

Overemphasis on homeownership

Acceptance of shared equity/CLT

Accounting for student population

Solutions

Come to terms w/ our “gated community/Disneyland” phenomena

o Intellectual capital needs to focus on issue

Aggressive legal methods—sue the city and state, targeted to government programs

o “inclusive communities” example

o Need to foment angst/attention on issue

Affordable housing targets throughout city at neighborhood level

Aggressive PHA that places S8 vouchers in high opportunity neighborhoods

Anti- “income source of origin” discrimination ordinance

Promote more sweat equity models

Opportunity maps guiding affordable housing investments

Willingness to spend more funds in high opportunity areas for affordable housing

Enforce existing fair housing statutes

Educational awareness campaign on integration

Prioritize public-owned lands for affordable housing

Sue the “bastards”

Aggressive affirmative marketing/preference strategies

Better link to job opportunities w/housing opportunities

Better linkages between transportation and housing

Concluding Discussion

Q: If had a magic wand for the federal level?

How can we get PHAs to be more intentional to target/market S8 to high opportunity? How to

incentivize?

Can we incent (funding?) for cities that do have fair share housing targets? Reward them for

achievements of targets?

Federal mandates for transportation to incorporate housing

TX has unfunded mandate for financial education; develop a federal program?

“Fair housing is a joke”: “lack of guts of every administration” to sanction violations. Must

enforce existing law.

Understanding impediments to enforcement & how to tweak so regulations not vulnerable to

unenforcement

o Ensuring analysis of impediments documents are accurate; if not, STOP the money! (for

everything-- housing, roads, etc.)

o Westchester case is an opportunity; cities need a push or things won‟t get done

Cover DesignSamir Gambhir

Sr. GIS/Demographic Specialist

Craig RatchfordGIS/Demographic Assistant

KIRWAN INSTITUTE FOR THE STUDY OF RACE AND ETHNICITYTHE OHIO STATE UNIVERSITY433 MENDENHALL LABORATORY | 125 SOUTH OVAL MALL | COLUMBUS OH 43210Ph: 614.688.5429 | Fax: 614.688.5592Website: www.kirwaninstitute.org

For more information on Kirwan Institute, please contact Barbara Carter | [email protected] more information on this report, please contact Christy Rogers | [email protected]