Speech: Internationalization Of The Capital … of the capital markets: the experience of the u.s....

21

Commission 20549 INTERNATIONALIZATION OF THE CAPITAL MARKETS: THE EXPERIENCE OF THE u.S. SECURITIES AND EXCHANGE COMMISSION A Paper Before The XI Annual Conference of the International Association of Securities Commissions Paris, France July 16, 1986 Charles C. Cox Commissioner Securities and Exchange Washington, D. C. U.S.A. The views expressed herein are those of Commissioner Cox and do not necessarily represent those of the Commission, other Commissioners or the staff.

Transcript of Speech: Internationalization Of The Capital … of the capital markets: the experience of the u.s....

Commission20549

INTERNATIONALIZATION OF THE CAPITAL MARKETS:THE EXPERIENCE OF THE

u.S. SECURITIES AND EXCHANGE COMMISSION

A Paper Before

The XI Annual Conference of theInternational Association of Securities Commissions

Paris, FranceJuly 16, 1986

Charles C. CoxCommissioner

Securities and ExchangeWashington, D. C.

U.S.A.

The views expressed herein are those of Commissioner Cox and donot necessarily represent those of the Commission, otherCommissioners or the staff.

INTERNATIONALIZATION OF THE CAPITAL MARKETS:THE EXPERIENCE OF THE

U.S. SECURITIES AND EXCHANGE COMMISSION

CONTENTS

SUMMARY. • • •

INTRODUCTION .

. . . . . . . . . 1

2

I. International Offerings. . 3

A. Present Registration Procedure. . . . . . 4B. The Multinational Offerings Release • • . 4C. Response to the Release . . .. 5D. Other Initiatives .•. . . 7E. Recommendations. . . . . . . . .. 8

II. International Trading . 8

A. Present Trading Development . . 9

1. Trading and Quotation Linkages . . .. 92. Clearance and Settlement Linkages. . 113. SEC Review of Current Linkages. . . .. 12

B.C.D.E.

The Global Trading Release. . . .Response to the Release .SEC Implementation. . . . . .Recommendations . . . .

12121313

III. International Surveillance and Investigation.. 14

A.B.C.

The Present Enforcement Environment . .Developments in Market Surveillance .Developments in Investigations. .

141515

1. Informal Methods . . . .. .•. 162. Formal Methods. . . . . . . . 163. New Constructive Alternatives. . . . 17

D. Recommendations 18

IV. Implementation. . . 18

• •

•

•

•

• •

•

•

SUMMARY

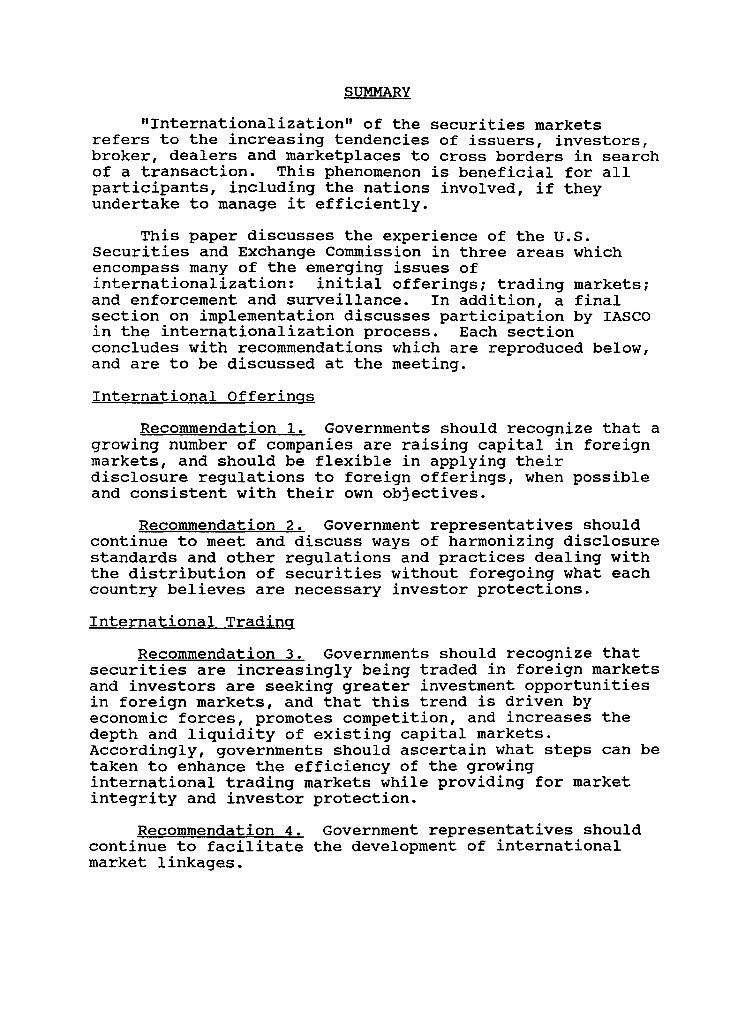

"Internationalization" of the securities marketsrefers to the increasing tendencies of issuers, investors,broker, dealers and marketplaces to cross borders in searchof a transaction. This phenomenon is beneficial for allparticipants, including the nations involved, if theyundertake to manage it efficiently.

This paper discusses the experience of the u.S.securities and Exchange Commission in three areas whichencompass many of the emerging issues ofinternationalization: initial offerings; trading markets;and enforcement and surveillance. In addition, a finalsection on implementation discusses participation by IASCOin the internationalization process. Each sectionconcludes with recommendations which are reproduced below,and are to be discussed at the meeting.

International Offerings

Recommendation 1. Governments should recognize that agrowing number of companies are raising capital in foreignmarkets, and should be flexible in applying theirdisclosure regulations to foreign offerings, when possibleand consistent with their own objectives.

Recommendation 2. Government representatives shouldcontinue to meet and discuss ways of harmonizing disclosurestandards and other regulations and practices dealing withthe distribution of securities without foregoing what eachcountry believes are necessary investor protections.

International Trading

Recommendation 3. Governments should recognize thatsecurities are increasingly being traded in foreign marketsand investors are seeking greater investment opportunitiesin foreign markets, and that this trend is driven byeconomic forces, promotes competition, and increases thedepth and liquidity of existing capital markets.Accordingly, governments should ascertain what steps can betaken to enhance the efficiency of the growinginternational trading markets while providing for marketintegrity and investor protection.

Recommendation 4. Government representatives shouldcontinue to facilitate the development of internationalmarket linkages.

2

International Surveillance and Investigation

Recommendation 5. Governments should recognize theneed for international enforcement of national securitieslaws where violations in one country have harmed investorsin another country. Cooperative arrangements should bedeveloped to enhance international surveillance of marketactivity.

Recommendation 6. Governments should agree to developmechanisms for access by foreign securities enforcementauthorities to regulatory and investigative files.

Recommendation 7. Governments should considernegotiating bilateral and multilateral agreements whichwould provide mutual assistance in securities matters.

Implementation

Recommendation 8. Representatives to the IASCOmeeting should report upon the consideration of thesematters in writing to the IASCO Secretariat prior to thenext annual meeting.

INTRODUCTION

International capital markets are developing rapidly.Orders, paYments and securities can now be transmitted fromone market to another almost instantaneously. Thesedevelopments in capital markets are but one part of thefree flow of goods and services over national borders. Thefree flow of international capital promotes a moreefficient allocation of resources by increasing the depthand liquidity of capital markets and by providing improvedopportunities for corporate planning and investmentdecision making.

International securities trading benefits all of themarket participants: corporations, investors, brokers,dealers and marketplaces. Corporations and other issuersof securities benefit because they can broaden theirownership basis by entering foreign markets. This promotesmarket stability and liquidity, may increase interest inthat issuer's products, and may facilitate foreignacquisitions. International investors benefit because theyhave new opportunities to diversify investment risks and toseek higher returns. Brokers and dealers benefit becausethey can broaden product lines offered to domesticcustomers and can attract new foreign customers or betterservice the needs of existing foreign customers. And

3

marketplaces benefit because transnational trading andclearing linkages can result in increased potential orderflow for both markets, increased price efficiency, morecapital being available for market-making, improved tradeclearances and settlement processing, and increasedvisibility.

Notwithstanding the enormous potential benefits ofinternationalization of capital markets for the globaleconomy, there are obstacles to internationalization. Inaddition to direct obstacles to the free flow of capitalsuch as taxes, exchange controls and investment controls,perhaps greater obstacles result from cultural and historicdifferences in various national approaches to capitalformation. Disclosure, auditing and accounting principles,trade processing, trade and quote dissemination, marketsurveillance and enforcement are all affected by suchdifferences.

This paper discusses these benefits of and obstaclesto internationalization in three specific areas, asexperienced by the u.s. Securities and Exchange Commission(SEC). Part I discusses disclosure requirements for pUblicofferings of securities in more than one country, and therecent SEC proposal on reciprocal and common prospectuses.Part II discusses the development of the internationalsecurities marketplace and recent initiatives, both by theindustry and the SEC, to develop trading, information,clearing and settlement linkages. Part III discussesmarket surveillance and international investigations, andthe methods which the SEC has developed, and newsuggestions which may result, for obtaining informationfrom other nations about securities law violations whichresult in domestic harm. After these areas are discussed,Part IV examines implementation of the recommended actionsand IASCO's potential role in ensuring smoothinternationalization. Each section concludes withrecommendations for discussion at this meeting.

I. International OfferingsRaising capital in international markets is no longer

the novelty it was only a few years ago. Commentators havetitled 1985 a "boom year" in the global capital markets.The total volume outstanding of u.S. commercial paper, u.S.bonds, Eurobonds and Euronotes is up sharply over 1984levels; some individual volume levels have more thandoubled. New issues of Eurobonds totaled a record $133.4billion during 1985. During 1985, foreign investorspurchased $37.9 billion of united States TreasurySecurities, and United States investors purchased roughly

4

$10 billion in foreign government bonds. Innovation anddiversification has produced traditional financialinstruments in new currency denominations and has increasedtrading levels in equity securities and "swaps." It isestimated that 50 percent of 1985 Eurobond offerings werelinked to interest rate and currency swap transactions.

Innovation in the capital markets must be paralleledby innovation in disclosure requirements. The SEC has beendeveloping its disclosure system for international issuers,and plans to continue that development.

A. Present Registration Procedure

In 1977, the SEC began developing a disclosure systemspecifically for foreign private issuers offering andtrading securities in the united States by adopting Form20-F. This form lists the disclosure requirements forforeign companies whose securities are actively traded inthis country and who are sUbject to our continuousdisclosure requirements. Accommodations were made toforeign private issuers in an attempt to harmonize thedisclosure requirements in the united States with therequirements most commonly found in foreign countries.

In 1982, an integrated disclosure system for foreignissuers was first adopted which is similar to the systemfor domestic issuers. This system -- Forms F-1, F-2, F-3and F-4 -- generally requires the same information as Form20-F, and p~rmits issuers to meet some disclosureobligations by referring to previous filings, or"incorporation by reference."

B. The Multinational Offerings Release

In March 1985, the SEC issued a release entitled"Facilitation of Multinational Securities Offerings." Therelease requested pUblic comments about ways to accommodatemultinational offerings and to harmonize the prospectusdisclosure standards and securities distribution systems ofthe United States, the united Kingdom and Canada.

The release discussed two ways to make multinationalsecurities offerings: the reciprocal approach and thecommon prospectus approach. The reciprocal approach wouldresult in an agreement by the three countries that aprospectus accepted in an issuer's domicile which meetscertain standards would be accepted for offerings in eachof the participating countries. The common prospectusapproach would result in agreed disclosure standards for anoffering document that could be used in two or more of the

5

three countries. Under either approach, the same liabilitystandards, discussed in Part III below, would apply toforeign issuers and domestic issuers.

The release asked questions about these approaches,their impact in other areas, and the SEC's role infacilitating such offerings. The united Kingdom and Canadawere chosen for initial consideration in any possibleexperimental implementation because issuers from thosecountries frequently use the united States markets, and thedisclosure and accounting requirements of those countriesare more similar to united States requirements than thoseof other countries.

C. Response to the ReleaseThere were seventy commentators on the release; some

raised additional issues not mentioned in the release. TheSEC's initiative was strongly endorsed by a significantmajority of the commentators. Many indicated that the SECwas the logical entity to assume this leading role.Commentators stressed that the objective of removingbarriers to mUltinational offerings should be balanced withthe statutory mandate to protect United States investors.The opponents of the initiative were concerned about theimpact on the domestic regulatory schemes, or wereconcerned that this initiative would facilitate the spreadof United States disclosure standards to their domicile.The major points raised are discussed in the followingparagraphs.

The Reciprocal Approach. The majority of commentatorsfavored the reciprocal approach. One of the majoradvantages of the reciprocal approach appeared to be theease of implementation. It was also argued that thereciprocal system best respects the different customs,business conduct, and traditions of fairness and disclosurein each jurisdiction. Some believed the reciprocal systemwould result in lower costs by reducing united Statesprinting fees, underwriters' "due diligence" expenses, andfees of experts such as lawyers and accountants.

While there was some support for reciprocity withoutany additional disclosure, many respondents favored amodified reciprocal approach, based upon either aprospectus supplement to be used outside the issuer'sdomicile, or a domestic supplement to a foreign prospectusmeeting minimum disclosure standards.

6

The Common Prospectus Approach. Many persons believedthe common prospectus may be the ideal approach, althoughthey were skeptical about the prospects for achieving thenecessary agreements in the near future.

Accounting Standards. The difference in accountingstandards in the three countries was mentioned by manycommentators. Some asserted that compliance withinternational accounting standards would be an adequatesafeguard, noting that present united States, unitedKingdom and Canadian generally-accepted accountingprinciples are all in conformity with internationalaccounting standards. In contrast, other commentatorsindicated that anything less than compliance with UnitedStates generally-accepted accounting principles andaUditing standards could present various problems withcomparability and independence and could sanction the useof techniques such as hidden reserves. Many of thesecommentators recommended continuing the present requirementof reconciling statements to united states generally-accepted accounting principles. Commentators were sharplydivided on whether to require the full segment reportingnow required for most pUblic offerings in the unitedStates. Half supported full segment reporting and theother half supported modified segment reporting requiringonly disclosure of segment revenues with narrativediscussion of segment income in certain circumstances.

Supplemental Disclosure. Some commentators felt thereshould be minimum disclosure standards or supplementalinformation in other areas such as the description ofbusiness, management's discussion and analysis and riskfactors. Most commentators endorsed the inclusion of alegend stating that the offering is made by a foreignissuer which has met the disclosure requirements of its owncountry but such requirements are not necessarilycomparable to those of the United states.

Impact of the SEC Review Process. Some commentatorswarned that the potential benefits of a reciprocalprospectus approach may be negated if the timing and natureof the SEC's registration statement examination andcontinuous reporting requirements are not modified. withrespect to the timing of initial offerings, commentatorspointed out differences of the distribution system employedin the United Kingdom. United States "gun-jumping" rulesinhibit pre-effective publicity in the United Kingdom, andit is difficult to coordinate effectiveness in the Unitedstates with the United Kingdom issuer's position in theGovernment Brokers queue which mandates the date ofeffectiveness in the united Kingdom. Some of thesuggestions in these areas called for the SEC staff to pre-

7

review filings. on a confidential basis, or to abstain fromreviewing multinational filings by relying entirely on thereview in the issuer's domicile. For periodic reporting,some commentators called for the SEC to accept periodicreports filed in the issuer's domicile as meeting Unitedstates periodic reporting requirements and proxy and tenderoffer rules.

Disproportionate Benefits. Some commentators believedthat foreign issuers would benefit more than United Statesissuers from a reciprocal approach, because United Statesstandards are more strict and comprehensive. othercommentators, however, did not expect such adisproportionate benefit. Similarly, some commentatorsbelieved that United States issuers offering securitiesonly in the United States would be competitivelydisadvantaged; others, however, believed there would be nosuch effect. At least one person projected thatmultinational issuers would tend to SUbstantially complywith United States disclosure standards under a reciprocalapproach, in order to avoid any comparative disadvantage totheir offering which might result from more limiteddisclosure.

Gradual Implementation. Many commentators indicatedthat the reciprocal system should initially be limited to"world-class" or "seasoned" issuers of investment-gradedebt. World-class issuers would be defined by theirassets, revenues, records of profitability, tradingmarkets, or exchange listings.

Incorporation by Reference. The release solicitedcomments on the possibility of incorporation by referenceto reciprocal registration statements, and access to theSEC's Electronic Data Gathering Analysis and RetrievalSystem (EDGAR). Commentators favored incorporation byreference with the qualification that repositories forincorporated documents, such as regulatory agencies orstock exchanges, should be required in each jurisdiction.Access to the EDGAR system was also enthusiasticallyendorsed, with further suggestions that reciprocal benefitsfor any foreign counterpart system be assured and thatother countries given access be encouraged to contribute todevelopment costs of the EDGAR system.

D. Other InitiativesThe SEC is considering similar approaches in

disclosures by mutual funds. A growing number of mutualfunds are providing individuals with the opportunity toinvest indirectly in foreign stocks. There were 41 suchfunds at the end of 1985, ten more than in 1984 and nearly

8

twenty more than in 1983. In addition, united states fundsare increasingly sold to foreign investors. The SEC isconsidering a recent suggestion by the Investment CompanyInstitute that the United states seek an agreement with theEEC allowing r~ciprocal sales, similar to the existingarrangement among EEC members.

E. Recommendations

The SEC hopes that this release and response andother initiatives wlll result in concrete proposals in thenear future. SUkcessful implementation, even on anexperimental basis, would be a significant step forward inthe process of harmonization of international disclosurestandards. Because initial success is important, anyreciprocal or common prospectus system should be graduallyimplemented as indicated above.

Recommendation 1. Governments should recognize that agrowing number of companies are raising capital in foreignmarkets, and should be flexible in applying theirdisclosure regulations to foreign offerings, when possibleand consistent with their own objectives.

Recommendation 2. Government representatives shouldcontinue to meet and discuss ways of harmonizing disclosurestandards and other regulations and practices dealing withthe distribution of securities without foregoing what eachcountry believes are necessary investor protections.

II. International Trading

International securities trading markets aredeveloping in tandem with international pUblic securitiesofferings. Debt instruments, particularly Eurobonds, havebeen the most prominent elements in the internationalmarkets. Total issues of Eurobonds outstanding exceed $300billion, and annual trading volume has increased sevenfoldover the last five years to an estimated $1.5 trillion.International markets also flourish for sovereign debt,most notably United States Treasury securities, BritishGilt instruments, and Japanese Yen bonds. While debt hasbeen the foremost element of the internationalizationprocess, equity securities also are being tradedincreasingly on an international basis. The stock ofapproximately 410 major companies, including over 85 unitedStates corporations, is traded actively in both theissuers' home market and at least one foreign market.Foreign demand for united States equities remained high in1985, with overseas investors effecting more than $108billion in transactions on united states markets in the

9

first nine months of 1985, and additional trading in unitedstates equities occurred on foreign markets. united statesinvestors during the same period traded over $30 billionworth of foreign stocks, and united states institutions nowhold over $16 billion in foreign stocks, compared to about$2 billion in the late 1970s.

A. Present Trading DevelopmentAn active market is developing among dealers away from

organized stock exchanges to meet the demand of investorsfor international trading opportunities. This trading isprimarily by institutional investors or by dealers fortheir own accounts, and involves international securitiesfirms passing orders among their worldwide offices.Brokerage firms and banks are making markets around-the-clock in sovereign debt instruments, particularly Unitedstates Treasury securities, and are using internationalmarkets to execute interest rate and currency swaps.

Global trading of equity securities is alsodeveloping, although the market is not as active as thatfor debt securities. International broker-dealers tradecertain foreign equities around-the-clock. For the mostpart, trading in united states equities remainsconcentrated in the united states securities markets,although intermittent trading in some issues occurs inEurope before the trading day begins in the united states,and some blocks are placed in Japan.

1. Trading and Quotation Linkagessecurities markets are developing linkages to

accommodate international trading of equity securities andoptions. The American stock Exchange (Amex) and Torontostock Exchange and the Boston and Montreal stock Exchangesare currently operating electronic trading linkages andcoordinated market information systems. The Amex-Torontolink is the first between primary markets inside andoutside the United states. Trading through the Amex-Toronto linkage began in late 1985 on a pilot basis in sixdually-listed stocks and will later be expanded to includeall dually-listed issues. Orders in linkage securitiesfrom the Amex and Toronto are transmitted between the twotrading floors using existing automated routing systems.Trades routed from Toronto to the Amex have increased fromfourteen trades totaling 18,500 shares when the programbegan in October 1985 to 78 trades totaling 292,000 sharesin January 1986. Trades routed from the Amex to Torontohave been less frequent, with six trades totaling 9,000shares in January 1986. The Midwest stock Exchange andToronto have developed a similar trading linkage, which

10

began operating in April 1986. Boston and Montreal haveimplemented a linkage that enables Montreal specialists tosend orders for execution by Boston specialists in a smallnumber of Canadian issues listed in the united states andin approximatel~ 200 United states-listed securities.Trading has grown from 150 trades totaling 41,000 shares inJune 1985 to 530 trades totaling 423,000 shares in January1986. The two exchanges also may later allow Boston memberfirms to send orders in canadian national issues directlyto Montreal for execution.

In addition to the operating linkages described above,other market participants are finalizing arrangements tofacilitate the growth of transnational trading. TheNational Association of securities Dealers, Inc. (NASD) andthe London stock Exchange have agreed to a two-year stockquotation sharing pilot program. Under the pilot, theNASD's automated quotation system (NASDAQ) will displayprice quotes from the 100 London stocks included in theFinancial Times-Stock Exchange Index and for 180 non-UnitedKingdom stocks in which there is an active London marketoff the exchange floor. London's international SEAQ systemwill display firm quotes for 200 companies traded on NASDAQand 75 non-United Kingdom companies whose AmericanDepository Receipts (ADRs) are traded on NASDAQ.

The Paris, London, Brussels, and Amsterdam StockExchanges are scheduled to establish the Interbourse DataInterchange System (Idis) in 1986. Idis will provide acommon means for reporting historical non-current pricesamong the linked markets. Idis later will also include theCopenhagen, Madrid, and Milan Stock Exchanges.

There are several other information or tradinglinkages under consideration by the world's securitiesexchanges and information processors. The Philadelphiastock Exchange and London have proposed trading fungiblecontracts on the six foreign currencies on whichPhiladelphia currently trades options. Under thisproposal, quotation and available trade information fromeach exchange would be disseminated on the floor of theother exchange, but no formal trading linkage iscontemplated at this time. The New York and London StockExchanges are discussing possible future joint ventures insecurities trading and reporting of market data. The Amexand European Options Exchange (EOE) in Amsterdam haveannounced a proposal for the EOE to trade fungible optionson Amex's Major Market Index. And Instinet and Reutershave entered into an international marketing agreementgranting Reuters exclusive rights to represent Instinetoutside the united States. Reuters has agreed to purchasea large stake in Instinet in order to make Instinet's

11

automated execution and negotiation services for unitedstates equities, options, and ADRs available to Reuters'foreign customers.

Even where no formal trading or information exchangeis made, exchanges in different countries are using commontechnology. The Paris Exchange, for example, is using thetechnology from Toronto's Computer Assisted Trading System(CATS) for its order routing system. The Zurich Exchangealso is considering using CATS.

2. Clearance and Settlement LinkagesDevelopers of these information and trade sharing

arrangements have realized that a precondition to effectivetrading linkages is the development of efficient clearanceand settlement arrangements. united States clearingagencies have been forming links with foreign clearingagencies and establishing clearing subsidiaries designed toprocess international securities transactions moreefficiently and safely.

National Securities Clearing Corporation (NSCC) hasadmitted the Canadian Depository for Securities to itsmembership. This addition permits processing of bothexchange and over-the-counter transactions between UnitedStates and Canadian broker-dealers, and facilitates theBoston-Montreal and Amex-Toronto exchange linkagesdescribed above. NSCC's new SUbsidiary, Internationalsecurities Clearing Corporation (ISCC), was created tofurther international clearing, initially to develop aclearing linkage with London's "Talisman" fortnightlysettlement system. The ISCC-Talisman linkage will provideunited States investors with access to London's clearingfacilities, and permit united Kingdom investors to cleartrades through NSCC.

The Options Clearing Corporation (OCC) is developingsecurities processing arrangements to enable it to cleartrades in fungible foreign currency options from bothLondon and Philadelphia. OCC proposes to establish aLondon office and a special membership category to ena~leLondon firms to clear foreign currency options tradesthrough OCC's London office. OCC also would establish alinkage with the International Commodities Clearing House(ICCH), which currently issues, guarantees, clears, andsettles transactions in London options, to processtransactions by European firms that elect to continue toclear options trades through ICCH.

12

3. SEC Review of Current Linkages

The SEC has been studying these developments with aview towards seeing what steps, if any, it should take toincrease efficiency in the international securities marketswhile assuring appropriate investor protection. The SECencourages international trading and clearing linkages, butrecognizes that there are few surveillance mechanisms forthis trading. In reviewing rule changes of United Statesnational securities exchanges developing internationallinkages, therefore, the SEC has been careful to insurethat adequate arrangements have been made for marketsurveillance. For the linkages involving Montreal andToronto, for example, the SEC worked closely with theparties and the provincial regulatory authorities todevelop private agreements and other assurances ofcooperation and information-sharing.

B. The Global Trading Release

In addition to" assisting with specific development oftrading, information, clearing and settlement linkages, theSEC is studying generally the growth of transnationaltrading markets to encourage further development. In April1985, the SEC solicited comment on a broad range of issuesconcerning the increasing internationalization of thesecurities markets, including conditions and structures ofinternational trading markets, international consolidatedreporting, quotation and trading linkages. The purpose ofthe SEC survey was to encourage United States and foreignsecurities industries, markets and regulators to considerways of attaining"the fairest and most efficient globaltrading markets possible.

C. Response to the Release

In response, the SEC received thirty letters fromcommentators in six countries. Commentators believed thatinternational trading is a positive development, and thatit would continue to grow in size and importance.Commentators also recognized that the SEC plays animportant role in internationalization, but mostcommentators opined that the SEC should refrain frompremature action in this area, and should permitinternational trading markets to develop further on theirown.

Although commentators agreed that internationaltrading would increase, they disagreed about the futurestructure of the international securities markets. Severalexchanges predicted that future global trading of worldclass securities would occur around-the-clock through a

13

network of interconnected exchanges, while othercommentators asserted that such trading would be morelikely done off the exchange floors, by large securitiesfirms. Commentators believed that greater dissemination ofquotation and trade information would facilitate the growthof global trading markets, although some expressedreservations about the practicability of immediatedevelopment of international consolidated quotation andtransaction reporting systems. They also stronglysupported additional links between central clearing anddepository organizations, and indicated that theincremental development of links between existinginstitutions was preferable to trying to create a centralinternational clearing or depository entity.

D. SEC ImplementationThe SEC discussed these responses in a pUblic meeting

on May 23, 1986. The SEC staff recommended that the SECinformally suggest to the New York Stock Exchange and theNational Association of Securities Dealers that they loosentrading restrictions and increase reporting requirementsfor so-called "after hours" trading. The SEC determinedinstead that the issues needed further study and discussionbefore any recommendations could be made. The SEC staffwas directed to prepare a memorandum on the generalnecessary elements for developing an international marketstructure, looking at characteristics such as fairness,efficiency and flexibility. In particular the staff wasdirected to consult with members of the stock exchanges,self-regulatory organizations, and securities firms. Manyof the principles developed in this process will bediscussed at this conference.

E. RecommendationsInternational securities markets develop in response

to international economic forces. That development shouldbe encouraged and channeled into organized markets in orderto maintain and increase market efficiency.

Recommendation 3. Governments should recognize thatsecurities are increasingly being traded in foreignmarkets and investors are seeking greater investmentopportunities in foreign markets, and that this trend isdriven by economic forces, promotes competition, andincreases the depth and liquidity of existing capitalmarkets. Accordingly, governments should ascertain whatsteps can be taken to enhance the efficiency of the growinginternational trading markets while providing for marketintegrity and investor protections.

14Recommendation 4. Government representatives should

continue to facilitate the development of internationalmarket linkages.

III. International Surveillance and InvestigationThe development of linked world markets combined with

dual listing and registration of securities will create newchallenges for enforcement agencies seeking to policeindividual securities markets. The united Statessecurities laws prohibit market participants, be theyissuers or traders of securities, from deceit, manipulationor fraud in connection with purchases and sales ofsecurities. Disclosure to investors of all informationmaterial to their investment decisions is the cornerstoneof the united States securities laws. These laws apply toall investors and issuers whose transactions are directedtoward the united States market.

A. The Present Enforcement EnvironmentThe SEC enforces the laws by identifying where

violations have occurred, developing evidence of theviolation, and instituting appropriate administrative orjUdicial proceedings against the violators. In a casewhere all of the evidence is located in or controlled fromthe united States, the SEC has the jurisdiction to compelits production. However, where the evidence is locatedabroad, the SEC's investigative power is greatly limited.The SEC's SUbpoena authority is limited to persons withinthe United States. Foreign law often does not allow forany investigative or pretrial discovery, and may frustrateSEC efforts to develop facts where only suspiciouscircumstances are apparent. The SEC has been required toengage in lengthy proceedings and negotiations to obtaininformation regarding transactions through foreign banks orsecurities firms located outside the United States. Nocomprehensive agreements exist for assistance in suchinternational investigative efforts.

While the vast majority of issuers and traders complywith the United states securities laws, multinationaltransactions can be advantageous to securities lawviolators desiring to conceal evidence of their activitiesfrom enforcement authorities. As these multinationaltransactions become more common, each nation seeking toenforce its securities laws will need access to informationfrom outside its borders. The SEC believes that the time

15

has come to discuss ways to improve the gathering ofrelevant information for the enforcement of securitieslaws.

B. Developments in Market SurveillanceElectronic linkage between securities markets will

complicate the surveillance and oversight of marketactivity. Without enhanced surveillance techniques,internationally-linked markets will be more susceptible tofraud.

As discussed in Part II above, the SEC has encouragedthe development of transnational trading. The SECencourages international participation in the IntermarketSurveillance Group, an organization through which many ofthe United States securities exchanges share surveillanceinformation. International participation would allowregulators and stock exchange managers to adequatelyoversee an internationally linked market.

The SEC has already approved several linkages betweenunited States and foreign markets, and is satisfied thatadequate arrangements have been made for marketsurveillance and information sharing regarding theselinkages. For example, the SEC has worked closely withCanadian provincial authorities and the securitiesexchanges involved to assure, in writing, that cooperationin enforcement investigations will be available. Thearrangements developed for the Amex-Toronto and Boston-Montreal linkages are possible models for future linkages.Toronto and Montreal have both agreed to cooperate in theinvestigation of any questioned trades and to transferinformation to their counterparts in the united States.Amex and Boston have made corresponding agreements. Audittrails will be maintained by all exchanges. The ontarioSecurities Commission has opined to the SEC staff that "itis difficult to conceive of an insider trading, marketmanipUlation or other case of improper trading" in whichthe recently-enacted Canadian blocking statute might beexercised to prohibit exchange of information. Thisassurance was especially important to the SEC, as it hasbeen frustrated by foreign blocking statutes in previousinvestigations.

C. Developments in InvestigationsBeyond market surveillance, the SEC's enforcement

program may generate multinational investigations intoalleged violations of the United States securities laws.The SEC has developed good informal relationships withforeign countries, but has otherwise found that resort to

16formal mechanisms -- bilateral and multilateral treatiesand letters rogatory -- often does not bring satisfactoryresults. The SEC is seeking to develop a dialogue withother countries to find effective and efficient methods toassist investigations.

1. Informal MethodsThe SEC has developed excellent informal working

relationships with its counterparts in other foreigncountries. Most recently, on May 23, 1986, the SEC and theSecurities Bureau of the Japanese Ministry of Financesigned a memorandum recognizing the need for internationalsurveillance and investigative assistance, and agreeing "tofacilitate each agency's respective requests forsurveillance and investigatory information on a case-by-case basis." Access to SEC files is available upon requestby foreign authorities, and some foreign securitiescommissions have been able to provide reciprocal or evengreater assistance. For example, the SEC has joined withits Canadian counterparts in investigating some cases whichinvolve both united States and Canadian violations.

2. FOrmal MethodsThe only formal methods for gathering evidence abroad

are multinational agreements such as the Hague convention,bilateral agreements specifically governing assistance incriminal matters, and letters rogatory. None of these isadequate for evidence gathering prior to litigation. Newarrangements for assistance need to be developed to ensurethat all nations can obtain the information necessary toenforce their securities laws and to maintain the integrityof their securities markets.

The Hague Convention/Letters Rogatory. Both the HagueConvention on Evidence Gathering and letters rogatoryprovide useful mechanisms for obtaining evidence fromneutral witnesses. However, they generally are availableto the SEC only after a lawsuit has been filed in a unitedStates District Court. Most often, the SEC needs foreigncooperation to obtain evidence and complete aninvestigation before commencing such a lawsuit. Manynations have agreed to the Hague Convention on thecondition that no "pretrial" discovery may take placepursuant to Convention procedures. The usefulness of theHague Convention is further limited by the requirement thatlitigants follow the procedural rules of the country inwhich the evidence is sought, rather than the rules of thecountry attempting to enforce its laws. In addition, it isoften difficult to obtain evidence pursuant to the HagueConvention where those in possession of the evidence oppose

17

its production. It is also difficult to obtain evidencepursuant to letters rogatory with either speed orcertainty.

Bilateral Agreements. The united states has treatieswith three countries for mutual assistance in criminalmatters and is negotiating with others. Although theunited states securities laws provide criminal penalties,the SEC generally seeks information for use in a civil oradministrative rather than a criminal proceeding. Thus,these treaties, while technically available to the SEC,have limited practical value. Although they provideimportant assistance, they are not optimal models forfuture agreements in the securities enforcement area.

3. New Constructive Alternatives

The SEC sought pUblic comment last year on the "waiverby conduct" concept, which would provide that the purchaseor sale of securities on a united States market wouldconstitute a waiver of the protection that would otherwisebe afforded by foreign secrecy laws. The SEC also invitedpublic consideration of the broader factual, legal andpolicy issues implicated by the increasingly internationalsecurities markets.

Sixty-five comments were received, most of themopposed to a legislative enactment of the "waiver byconduct" concept. The SEC recognizes that this idea waspoorly received and is committed to exploring differentalternatives. Unfortunately, no commentator proposed acomprehensive alternative to "waiver by conduct" other thanthe negotiation of bilateral and multinational arrangementsthat expressly provide the necessary assistance. The SECbelieves that there are other viable non-confrontationalalternatives. Although many countries are understandablyreluctant to allow foreign evidence-gathering rules to beapplied within their borders, flexible arrangements arenecessary to make evidence available to maintain theintegrity of the securities markets and protect investorsfrom fraud. Without such arrangements, wrongdoers will beable to prey on the securities markets of many nations fromoutside the borders of those nations.

Any arrangement for assistance in evidence gatheringmust allow participating nations all the informationnecessary to protect their securities markets againstforeign-based fraud. At the same time, such an arrangementmust not jeopardize the sovereign interests ofparticipating nations in activities occurring within theirborders. For example, a foreign law enforcement agency'srequest for evidence might be required to meet a relevancy

18•standard applied by a court in the country where the

evidence or witness is located. This standard would guardagainst unwarranted "fishing expeditions." The assistancemight also be limited to governmental investigations &ndlitigation, excluding private lawsuits. This would reducefears that the process might be abused. Finally, thearrangement might limit assistance to matters arising underspecified statutes, which would ensure that a participatingnation would not be forced to assist in the enforcement ofa foreign law which is contrary to its policies. The SECis not committed to anyone vehicle for providingassistance, but rather believes that this subject should beexplored in detail by all trading nations to develop anagreement enhancing cooperation among members.

D. Recommendations

As the securities markets become more international,law enforcement problems will become more severe and morewidespread. All nations with securities markets may facethe dilemma of deciding whether to act unilaterally toprotect their markets from foreign-based fraud, or to livewith markets where some participants can defraud otherswith impunity. Neither alternative is acceptable. Theacceptable alternative is to develop ways of sharingsurveillance and investigating information, and toformalize these arrangements in bilateral or multilateralunderstandings.

Recommendation 5. Governments should recognize theneed for international enforcement of national securitieslaws where violations in their country have harmedinvestors in a foreign country. Cooperative arrangementsshould be developed to enhance international surveillanceof market activity.

Recommendation 6. Governments should agree to developmechanisms for access by foreign securities enforcementauthorities to regulatory and investigative files.

Recommendation 7. Governments should considernegotiating bilateral and multilateral agreements whichwould provide mutual assistance in securities matters.

IV. Implementation

Each of the three areas discussed above raises new,emerging issues in the development of the internationalsecurities markets. Coordinated and trouble-freedevelopment of these markets requires continuing andrigorous dialogue among participant nations. The

19

International Association of Securities commissions canplay a leading role in developing and advancing thisdialogue.

Recommendation 8. Representatives at the IASCOmeeting should report upon consideration of these mattersin writing to the Secretariat prior to the next annualmeeting.