Supply chains and the internationalization of SMEs · Supply chains and the internationalization of...

49

Supply chains and the internationalization of SMEs Evidence from Italy Connecting Local Enterprises to Global Markets Geneva, October 8 th , 2014 Giorgia Giovannetti Robert Schuman Centre for Advanced Studies, European University Institute, and University of Florence

Transcript of Supply chains and the internationalization of SMEs · Supply chains and the internationalization of...

Supply chains and the

internationalization of SMEs Evidence from Italy

Connecting Local Enterprises to Global Markets

Geneva, October 8th, 2014

Giorgia Giovannetti Robert Schuman Centre for Advanced Studies,

European University Institute,

and University of Florence

The context

• Huge changes in the last 20 years: ICT & falling

costs led to emergence of GVC (production

networks; fragmentation; trade in tasks; etc) &

increasing globalization, with emerging actors

and different challenges.

• Structure of different countries remains different

• Many small and not very internationalized firms

(especially in developing countries, but also in

EU,e.g Italy)

– Africa, smaller and less internationalized

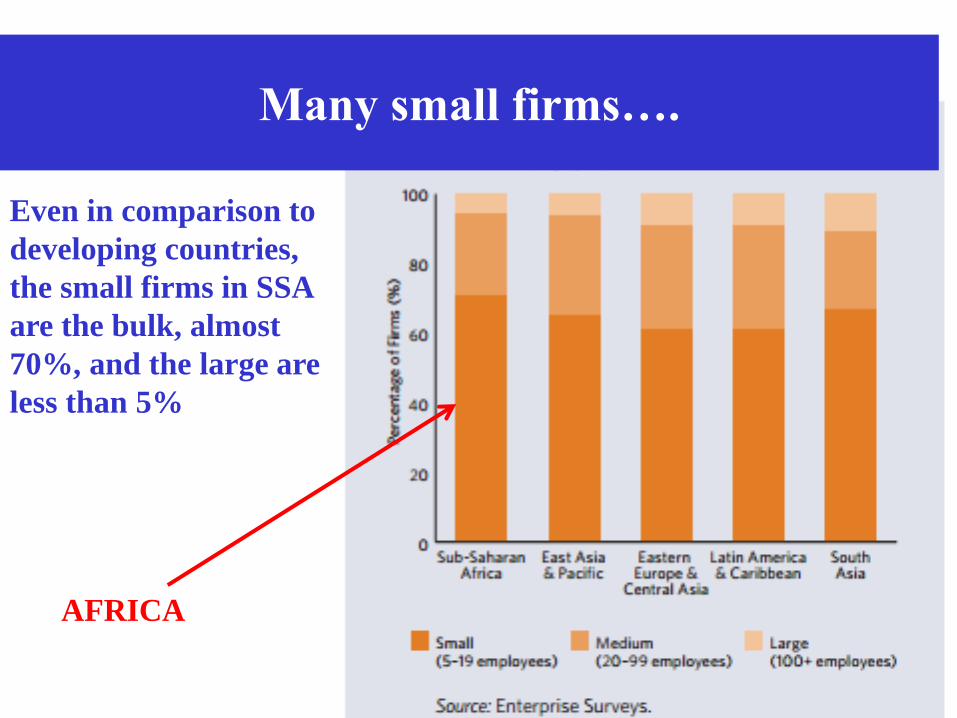

Many small firms….

Even in comparison to

developing countries,

the small firms in SSA

are the bulk, almost

70%, and the large are

less than 5%

AFRICA

Also in EU

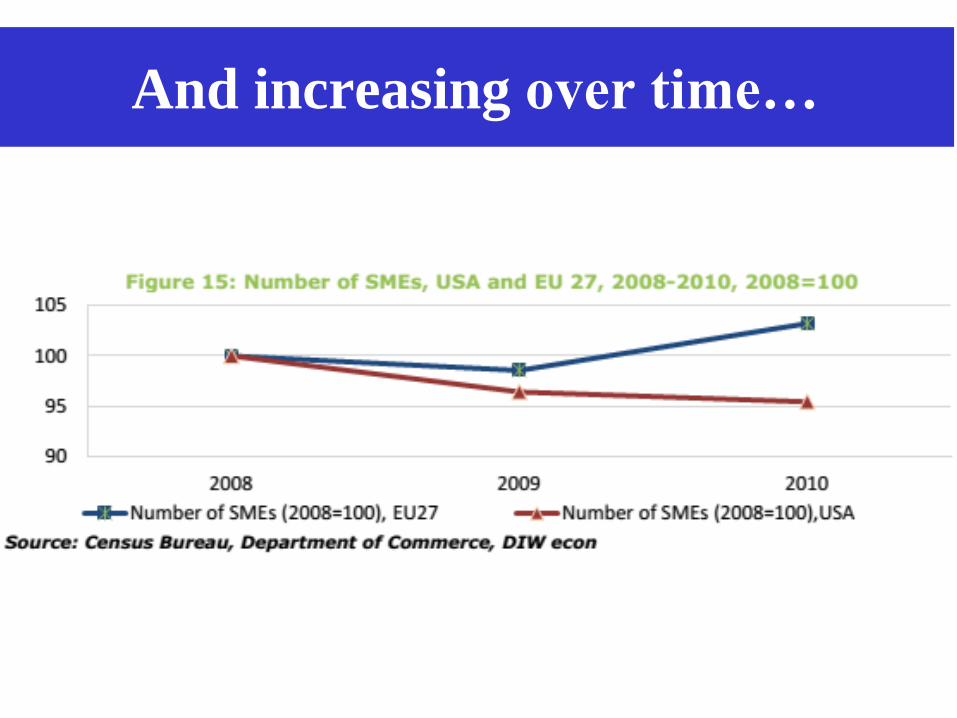

And increasing over time…

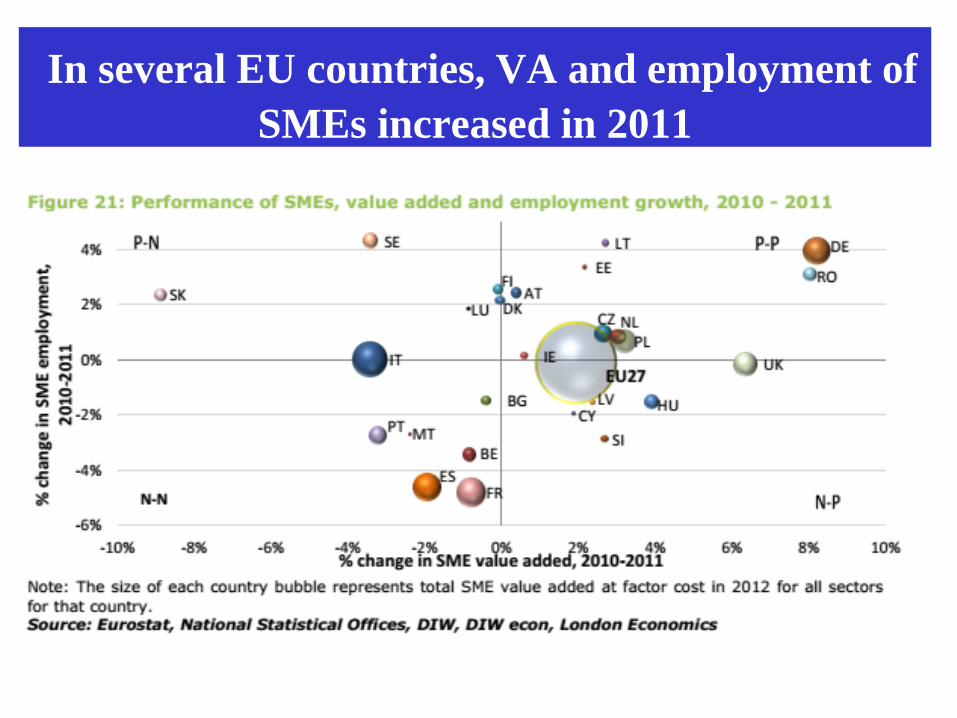

In several EU countries, VA and employment of

SMEs increased in 2011

0

200

400

600

800

1000

1200

1400

1600

1800

Micro/Small (<20 employees) Medium

(20-99 employees)

Large

(100+ employees)

Size distribution: Africa, Entreprise Survey, by country, last av. year

«Formal»

In Africa, most firms are micro or small

184 126

226 77

249

84

377

299

368

333

45

250

208

306 87

1461

114

409

111

361

483 422 437

232

131

97

108 54

68

51

103

206

94

240

54

98

132

142

52

386

90

75

27

376

186 169 225

221

45 45 60 19 42 16 46

139

32

140

51

12

58

31 11 44

37

22 12

200

54 49 58

146

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Micro/Small (<20 employees) Medium

(20-99 employees)

Large

(100+ employees)

Size distribution, %: Africa, by country, last av. Year, Ent. Survey

Formal=100

Firm size distribution by region

The size distribution in Africa peaks

at 7 employees per firm; the density

of larger firms is lower than

elsewhere

Outline

• The goals of the presentation

• The operative definition of Supply chain (and a

comparison with the alternatives); the empirical

issue of how to proxy participation to a supply

chain and lack of appropriate data.

• The case of Italy: use of a detailed survey with

specific questions on supply chain, networks and

position along the chain

• A focus on the agro value chain, in Italy

• Some general conclusion (can we learn any

lessons from the Italian case study?)

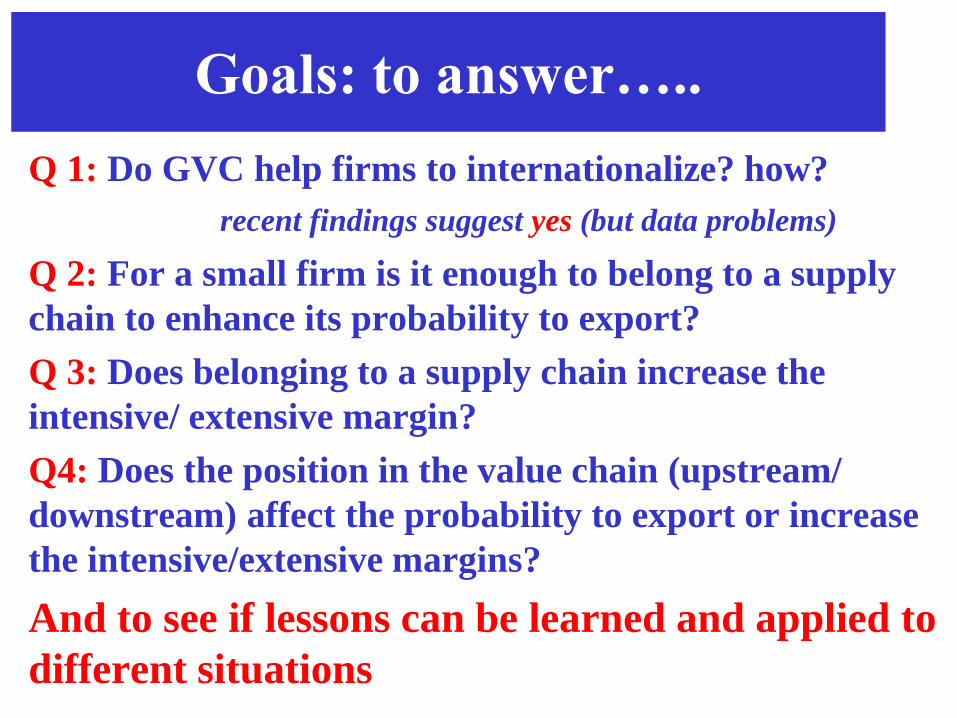

Goals: to answer…..

Q 1: Do GVC help firms to internationalize? how?

recent findings suggest yes (but data problems)

Q 2: For a small firm is it enough to belong to a supply

chain to enhance its probability to export?

Q 3: Does belonging to a supply chain increase the

intensive/ extensive margin?

Q4: Does the position in the value chain (upstream/

downstream) affect the probability to export or increase

the intensive/extensive margins?

And to see if lessons can be learned and applied to

different situations

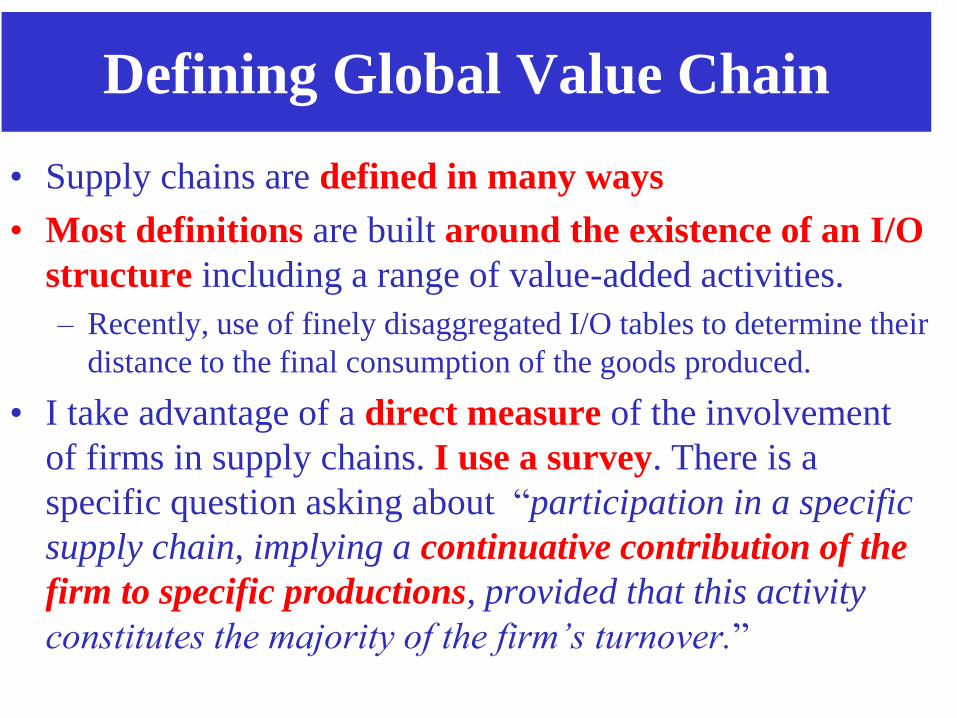

Defining Global Value Chain

• Supply chains are defined in many ways

• Most definitions are built around the existence of an I/O

structure including a range of value-added activities.

– Recently, use of finely disaggregated I/O tables to determine their

distance to the final consumption of the goods produced.

• I take advantage of a direct measure of the involvement

of firms in supply chains. I use a survey. There is a

specific question asking about “participation in a specific

supply chain, implying a continuative contribution of the

firm to specific productions, provided that this activity

constitutes the majority of the firm’s turnover.”

• … is based on a direct answer from a firm’s

representative.

• It captures the specialization of the firm in specific

tasks within a well-defined production process.

• Thanks to specific information on firms’ upstream and

downstream activities, it also allows to control for the

role of firms within the production process.

• The involvement in a specific production process is

identified in the survey with a firm’s identification with a

specific supply chain, which is different from the sector

they belong to.

Our definition…..

Partecipation in supply chains….

• …. may enhance the internationalization of firms through complex

and highly interrelated mechanisms. A major one has to do with

incomplete contract theory and specialization.

• Heterogeneous firms deciding whether and how to fragment their

production (domestically and/or internationally) are likely to

undertake a relationship-specific investment in an incomplete

contracts environment. An example of such a situation is the

decision on where to position themselves along the supply chain,

according to their specialization.

• Since inputs are often customized to the buyers’ needs, trust

between agents becomes key. By «relationship-specific» we mean

that the value of assets or investments is higher inside a particular

relationship than outside of it.

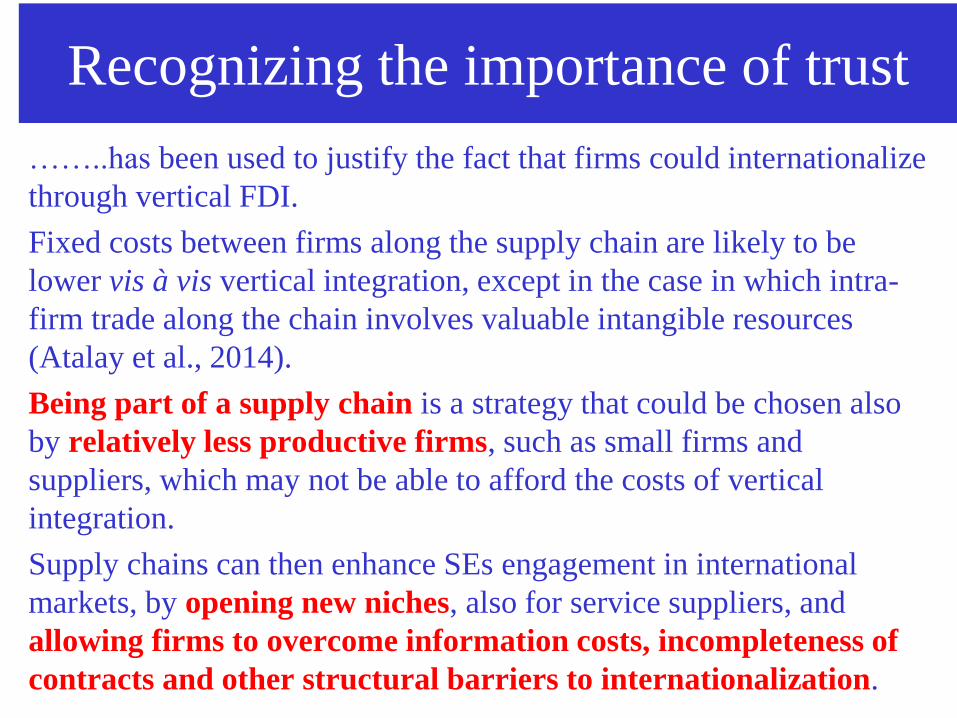

Recognizing the importance of trust

……..has been used to justify the fact that firms could internationalize

through vertical FDI.

Fixed costs between firms along the supply chain are likely to be

lower vis à vis vertical integration, except in the case in which intra-

firm trade along the chain involves valuable intangible resources

(Atalay et al., 2014).

Being part of a supply chain is a strategy that could be chosen also

by relatively less productive firms, such as small firms and

suppliers, which may not be able to afford the costs of vertical

integration.

Supply chains can then enhance SEs engagement in international

markets, by opening new niches, also for service suppliers, and

allowing firms to overcome information costs, incompleteness of

contracts and other structural barriers to internationalization.

I exploit an original dataset….

• ….. based on a survey conducted by MET

(Monitoraggio Economia e Territorio) on over

25000 Italian firms, which include direct

information on their involvement in supply

chains.

• I rely on a direct measure of supply chain: the

answer to an ad-hoc question included in the

survey

The survey

• 25,090 Italian firms, of which 86.2% SMEs

• Merged and matched with balance sheets data

(AIDA) and ICE Reprint data for FDI.

• Final dataset has 7,590 firms (loss mainly due to

micro-small firms)

• 40% of firms export; 16% are in a supply chain;

6% are in a foreign network

• In Italy, large literature on importance of imports

(what, from where), networks and supply chain

integration (especially for SMEs)

• The supply chains variable includes firms that buy

and/or sell intermediate inputs and at the same time

have some degree of participation in the design of the

final product, which is likely to signal the “contribution

of the firm to specific productions.

• According to our definition, in Italy (with our dataset)

firms belonging to a supply chain are 15.7 percent of

the sample, a majority (82.3 percent) being

manufacturers.

• NB: in the empirical exercise we have also run all the

regressions using a “traditional” proxy for supply chain

Supply chains in our dataset (Italy)

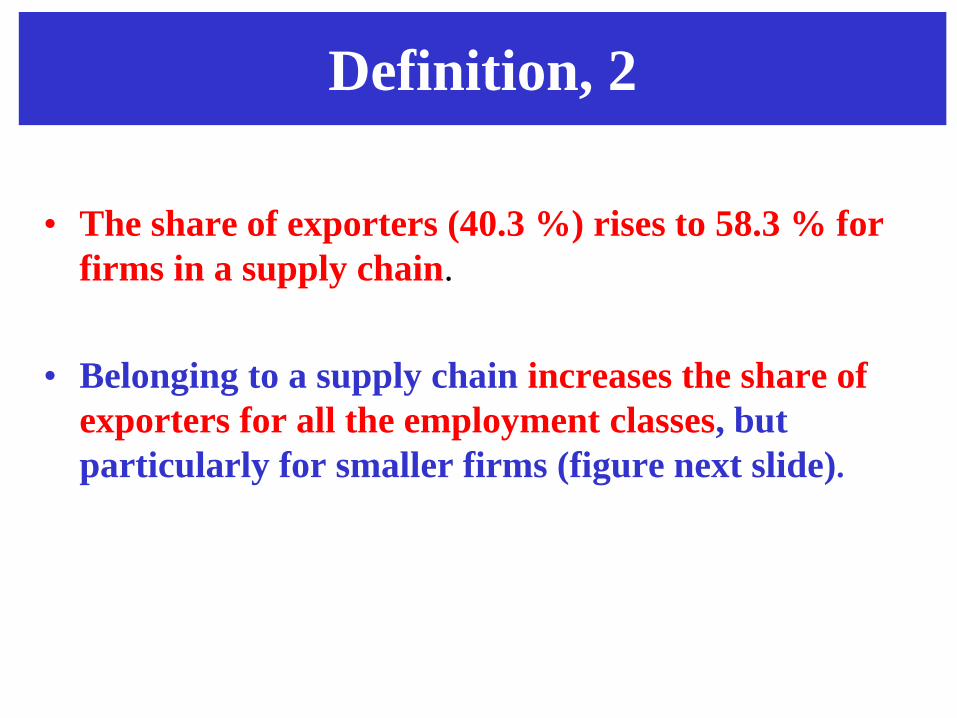

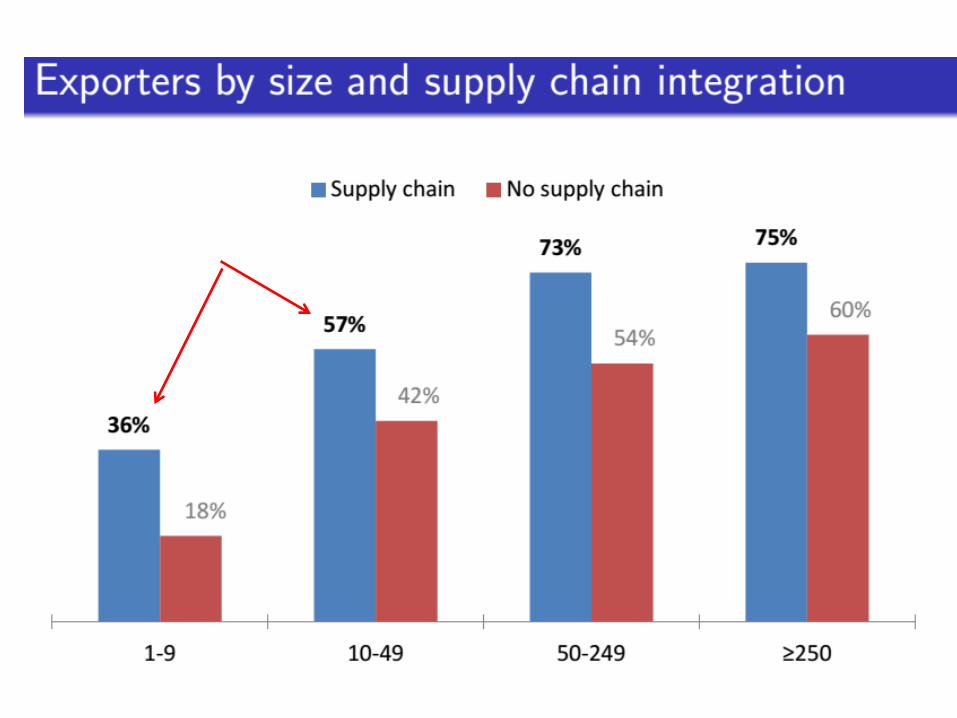

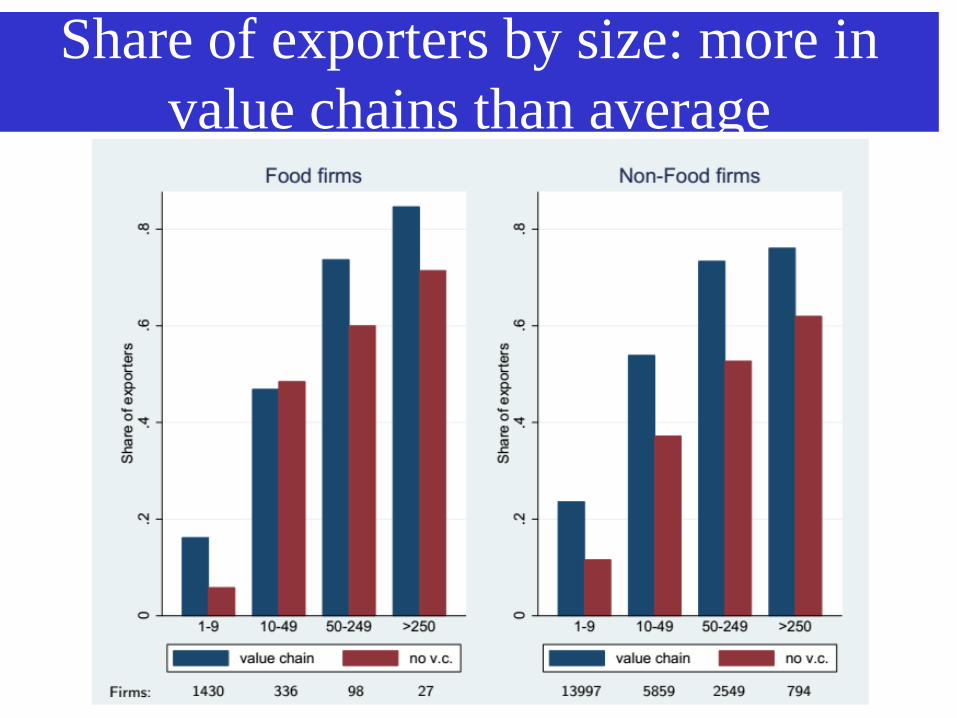

• The share of exporters (40.3 %) rises to 58.3 % for

firms in a supply chain.

• Belonging to a supply chain increases the share of

exporters for all the employment classes, but

particularly for smaller firms (figure next slide).

Definition, 2

Complex degree of international

involvement:

• About 9.5 % of firms are both exporting and

involved in FDIs; this corresponds to 24 % of

FDI firms among exporters and to 73.8 % of

exporters among FDI firms.

• Our TFP estimates are in line with the

findings of the literature, and show that

productivity premia are different for different

internationalization modes

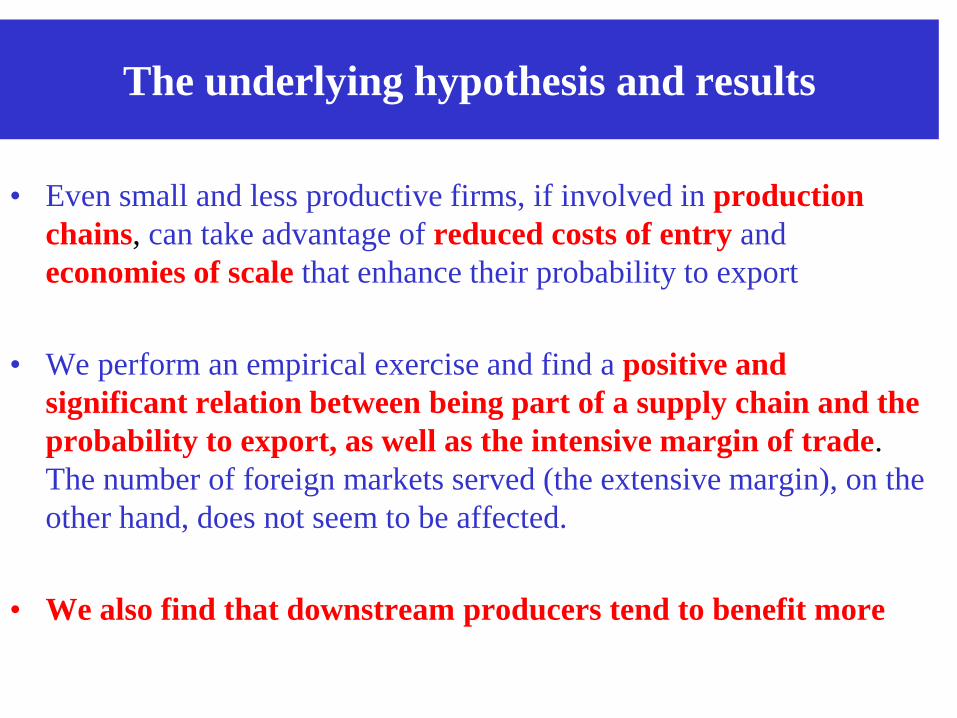

The underlying hypothesis and results

• Even small and less productive firms, if involved in production

chains, can take advantage of reduced costs of entry and

economies of scale that enhance their probability to export

• We perform an empirical exercise and find a positive and

significant relation between being part of a supply chain and the

probability to export, as well as the intensive margin of trade.

The number of foreign markets served (the extensive margin), on the

other hand, does not seem to be affected.

• We also find that downstream producers tend to benefit more

Italy peculiar specialization

• Italy’s sectorial specialization and industrial

structure triggered a high division of labor

among firms, many of which often work as

specialized suppliers

• Traditional small suppliers can take advantage

from the international fragmentation of

production to engage in more complementary

activities with final firms and improve their

performance

Networks

• Italian SMEs often engage in formal and informal

networking at the local level, involving

cooperation among specialized firms, to achieve

collective efficiency and better performance

compared to firms outside industrial districts.

• The survey also has direct information on whether

a firm belongs to a “local” , “domestic” o

“international” network.

• “local” are the industrial districts (clusters), very

common in Italy in traditional sectors

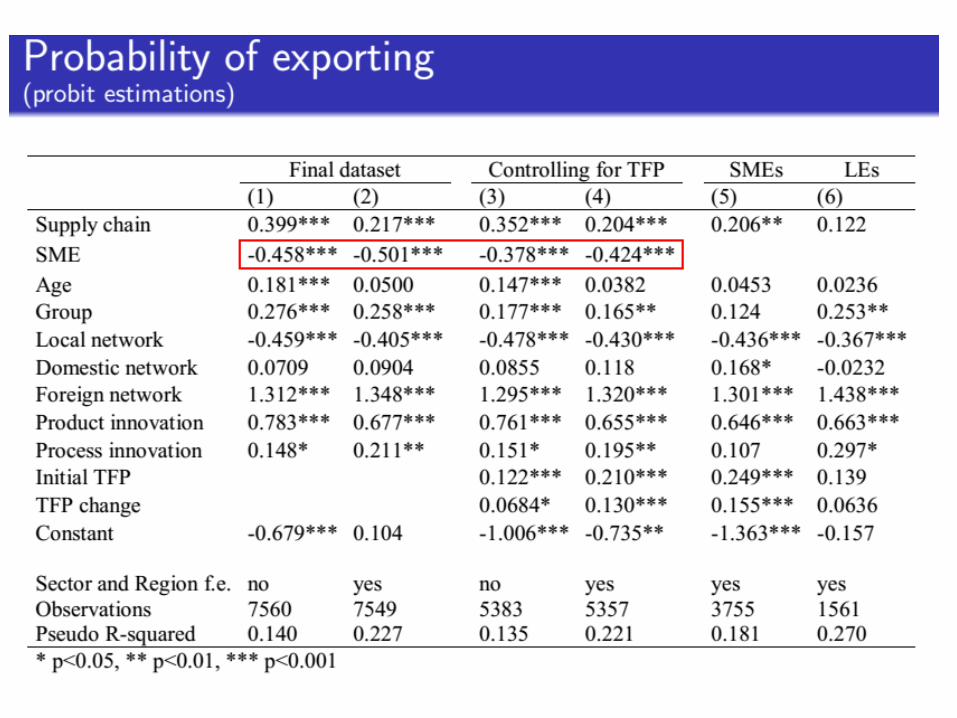

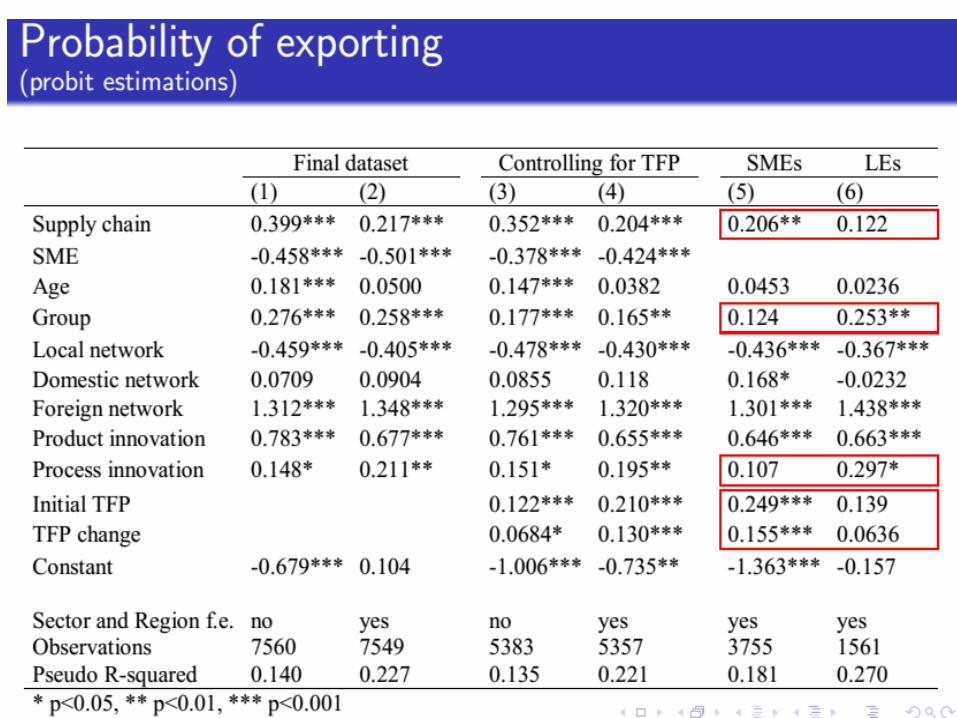

Our Results….

• show that belonging to a supply chain helps offsetting

some of the competitive disadvantages of SEs (e.g. lower

levels of productivity), as it is positively correlated to (i)

their probability to export and (ii) the intensive margin of

export (measured as share of total exports on turnover).

• Supply chain participation does not seem to affect the

extensive margin, measured as the number of foreign

markets served, in line with the view that structural limits

linked to the size matter for international expansion of SEs.

• Firms involved in downstream activities benefit more

from being part of a supply chain.

… and suggest some important

implications

• ….. especially for countries like Italy

characterized by a high number of small firms

and a fragmented production system

• only a small fraction of domestic firms is able

to autonomously integrate in supply chains

• Need for specific policies supporting the

inclusion in more organized, domestic and

global, production processes.

The marginal effects are significant for

small firms…

-.4-.2

0.2

<=5 <=15 <=30 <=50 >=50 >=100 >=200 >=300n. of employees

Supply chain marginal effect 95% c.i.

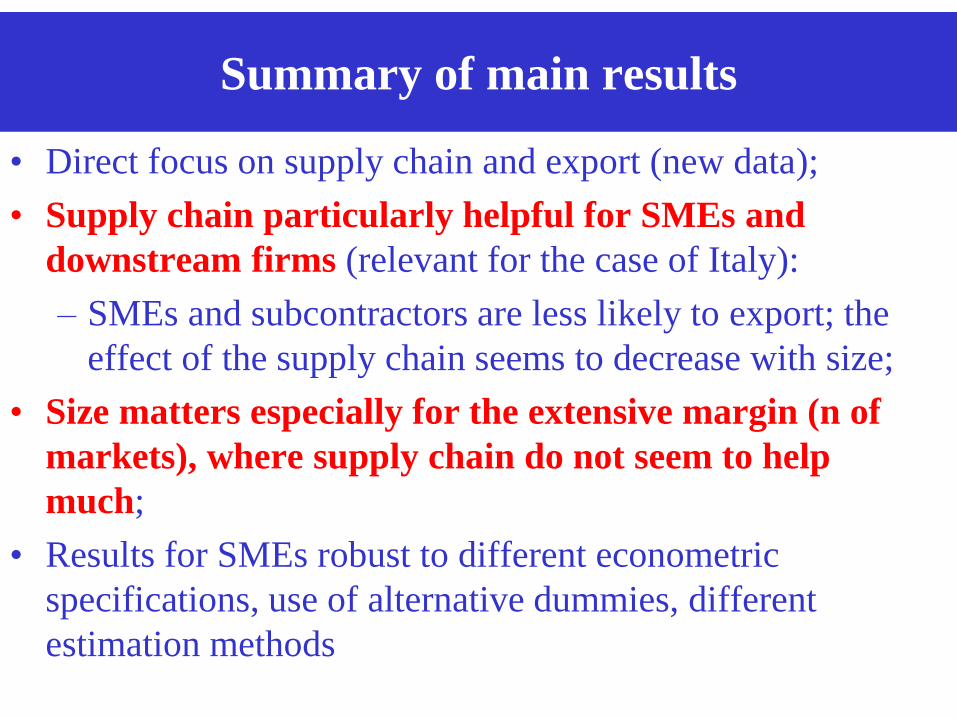

Summary of main results

• Direct focus on supply chain and export (new data);

• Supply chain particularly helpful for SMEs and

downstream firms (relevant for the case of Italy):

– SMEs and subcontractors are less likely to export; the

effect of the supply chain seems to decrease with size;

• Size matters especially for the extensive margin (n of

markets), where supply chain do not seem to help

much;

• Results for SMEs robust to different econometric

specifications, use of alternative dummies, different

estimation methods

An application to agrifood value chain

• An interesting sector (for Africa for instance) is

agri-food

• We performed a specific analysis for agro value

chains in Italy

• Using the same dataset (a subsample) and getting

very similar results in general and interesting

results on quality

• The agrifood firms in the sample are 1080, 7,5% of

the total, most small and integrated in supply

chains

Firms’ distribution by size: in

agrifood firms are smaller

Share of exporters by size: more in

value chains than average

Share of exporters by firm’s size and

type of value chain: the role of quality

Food value chain (only relevant

coefficients)

AgriFood Value Chain coefficients

Summing up

• Results very similar to the general case, but also

interesting insights into the issue of quality

• Value Chains allow to enhance quality of small

producers

• Agri food value chain can be very relevant for

developing countries (Italian case could be

considered as an example)

Can we extend results or policy implications

to other countries?

• We assessed the importance of GVC, especially for

small domestic firms: what about developing countries

(Q1)?

• How to improve SMEs positioning in GVC and reap

benefits (Q2)?

• The case of Ethiopia (Q3) (Sutton survey, better

information; example of leather GVC, Bruatigham)

• Are there links between SME and FDI (Q4)?

• Best practices and policy options

1. Share in Global Value Chain income

1. What really matters is where the value added is created….

Yarn Raw

Cotton

Textile

Finishing Garment

production

11.3% 16.0% 6.9% 54.5% 11.3%

2. GVCs (or RVCs?) today: stylized facts

• US+EU27 share is getting decreasing; developing & emerging countries’ share increasing

• This is driven by just few countries, most of them in Asia.

• Nevertheless, developed countries still take the majority of

income generated in GVCs

Two issues:

• Many developing countries do not (yet?) participate in GVCs

• If and when they do participate, they are at the low end of the value chain.

2.UPGRADING IN GLOBAL VALUE CHAINS

How?

– Improving Process

– Improving Products

– Specialising in new

functions

– Moving to a new VC

Introduction of better quality control systems or new production equipment.

A footwear producer shifts from mass produced low-cost shoes to more fashion-intensive footwear sold for higher prices

Moving from a manufacturing to a design function.

Move from TV to computer monitor production

New role of SMES in a globalizing

industry

• On the one hand, SMEs are well adapted to the new conditions of competition: flexibility, innovation and strong presence in and understanding of local markets.

• On the other hand, they are isolated from and have limited understanding of the opportunities and challenges of globalization. These weaknesses are particularly important in developing countries

• The policy challenge for developing and in particular African countries is not to protect them from global competition but to help entrepreneurs and small companies to address the challenges and opportunities by improving their links to global value chains and to improve their access to information, technology, finance and skills.

Global transformations have a strong impact on the role of

SMEs in sustainable industrialization:

06/10/2011

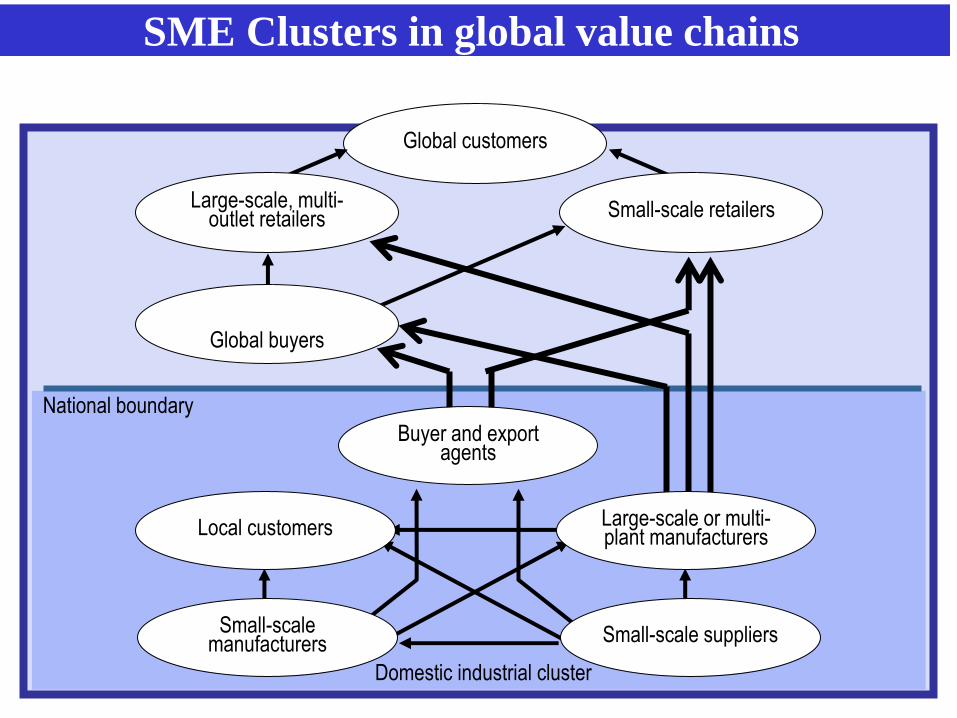

SME Clusters in global value chains

National boundary

Domestic industrial cluster

Global customers

Large-scale, multi-outlet retailers Small-scale retailers

Global buyers

Buyer and export agents

Local customers Large-scale or multi-plant manufacturers

Small-scale manufacturers

Small-scale suppliers

Where is SSAfrica in the global value chain?

• Lead firms are primarily from developed

countries

• Several first-tier suppliers are from developed

or emerging economies such as HK, Malaysia,

India etc

• African companies are second, third or fourth-tier

suppliers

• Global value chains (which operate in a transparent and accountable way) can be engines for economic growth and sustainable development

• They can support export propensity for SMEs

• Indeed they are key for sustainable development and SME support

• (It is important to include in the Aid for trade initiative the enterprise dimension in building productive capacities, to unleash enterpreneurial talents and skills in developing countries)

• (Dynamics effects of regional integration and South-South co-operation)

• Public Private Partnerships deliver good results (to be further explored)

Summing up

In conclusion

• GVC help firms internationalization; but it is important to

be «on the right point»

• Value added is not created all along

• Also clusters and network help (technological clusters, e.g

case of shoes industry in Spain)

• GVC support SMEs in complying with intl standards. This

is key in the agro-food industry (e.g. salmon case in

Chile);

• Experiment with new forms of private-public partnerships

(participatory systems for setting research agendas,

intermediary organizations linking small firms with

universities) (the wine case in Chile and SA).

Thanks!