Special Education Finance 101...Special Education Finance 101 Nan Records Regional Low Incidence...

91

Special Education Finance 101 Nan Records Regional Low Incidence Facilitator December 2018

Transcript of Special Education Finance 101...Special Education Finance 101 Nan Records Regional Low Incidence...

Special Education Finance 101

Nan Records Regional Low Incidence Facilitator December 2018

Special Education Finance 101

Part B Federal Flow-Through 3-21

Preschool Incentive 3-5

Part C Infants and Toddlers Birth-2

• Part B (3-21 year olds) AKA….419 AKA….Section 611 AKA….Federal Flow Through

• Part C (3-5 year olds) AKA….420 AKA….Section 619 AKA….Preschool Incentive

• Part C (Birth-2 year olds) AKA….422 AKA….Section 619 AKA….Infant and Toddlers

Number of students in special ed (Base)

Total District Enrollment

Total number of students on free and reduced

FEDERAL FLOW-THROUGH 3-21

Total Fin 419 Allocation

Searching for Federal Allocations

Data Center > Data Reports and Analytics > School Finance Spreadsheets > Special Education …

Data Center > Data Reports and Analytics > School Finance Spreadsheets > Special Education … Special Education, Federal Allocations, 2017

Other “optional” sources

Coordinated Early Intervening Services CEIS

Coordinated Early Intervening Services

CEIS LEAs can use up to 15% of their federal $$ (419) to fund programs to prevent students from having to be placed into special education …Providing educational and behavioral interventions services and supports… ….These are NOT additional $$$...it’s an option to use part of your Part B/419 $$$ for this initiative

50% Rule

LEAs can use up to 50% of the increase in their federal $$ from one year to the next to supplant local costs of providing special education services.

Carryover Funds Unspent federal funds will be “carried over”. An LEA has up to 27 months to use federal funds.

Maintenance of Effort (MOE)

Districts must spend same or greater amount of local funds on special education from one year to the next

Maintenance of Effort (MOE)

There are a few exceptions… • Reduction in child count • Retirements • High cost student gone • Elimination of one time expenditure

Maintenance of Effort (MOE)

When directed to make cuts in special ed… Can it be done with MOE? It Depends… • Salary step and lane increase MAY cover the gap of staff being cut • Work closely with Business Manager to ensure MOE is met if making cuts • MOE is currently calculated by Individual Districts and Co-op or Ed District • Educate Superintendents and Board Members on MOE requirements early on so it is not a surprise!

Gen Ed of Foundation Aid

Special Ed Initial Aid

Excess Cost Aid

Homebased Travel Aid

Special Pupil Aid

Court Placed Revenue

Out-of-State Tuition

Tuition Billing

FY 15

Gen Ed of Foundation Aid

Special Ed Initial Aid

Excess Cost Aid

Homebased Travel Aid

Special Pupil Aid

Court Placed Revenue

Out-of-State Tuition

Tuition Billing

FY 15

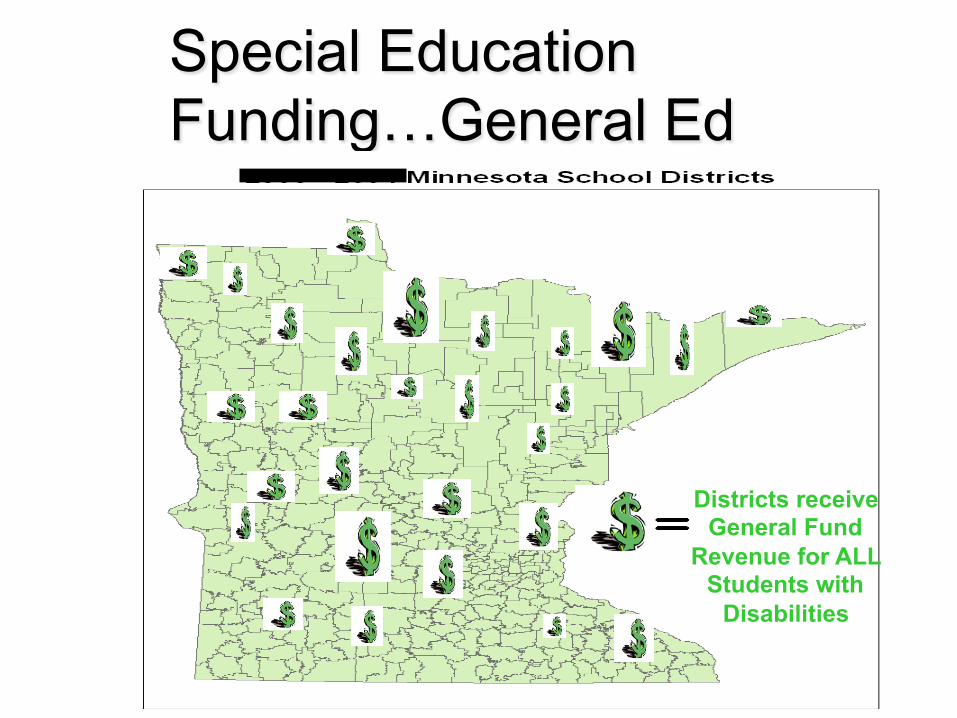

Special Education Funding…General Ed Revenue

Districts receive General Fund

Revenue for ALL Students with

Disabilities

Special Education Funding…General Ed

Amount differs across the

State!!

Gen Ed of Foundation Aid

Special Ed Initial Aid FY 15

Excess Cost Aid

Homebased Travel Aid

Special Pupil Aid

Court Placed Revenue

Out-of-State Tuition

Tuition Adjustments

Base special ed revenue is equal to the sum of the following expenditures regular year and summer special education programs:

Base Special Ed State Aid FY 15

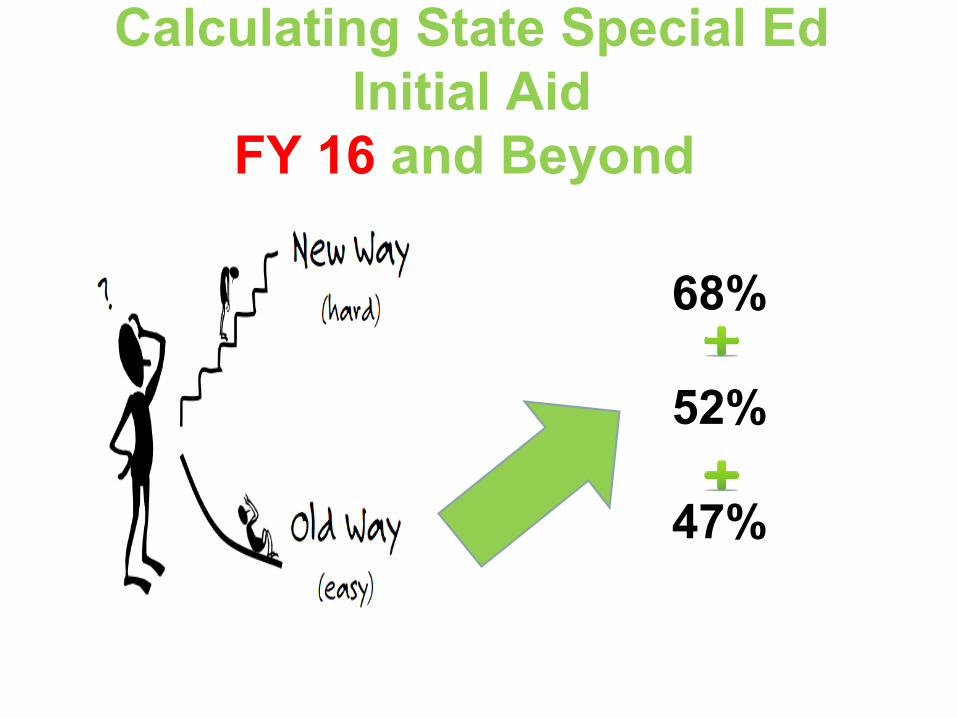

68% Salary for personnel essential to providing services to students with disabilities

52% Contract amount for supplementary special ed services provided

47% of expenditures for special supplies and equipment for educating children with disabilities up to a maximum of $47 per child receiving special education

Special Ed Initial State Aid FY 15

68 % Salary 52% Contracted Services 47% Supplies/Equipment

68% 52% 47%

68% 52% 47%

68% 52% 47%

2003 2002

2001

Program Growth Factor

2004 2005 2006 2007

68% 63% 61% 60%

2004 2005 2006 2007

Program Growth Factor

Special Ed Initial State Aid FY 15

68 % Salary 52% Contracted Services 47% Supplies/Equipment

Statewide Adjustment Factor Total

Total Proration Factor

Special Ed Initial State Aid FY 15

68 % Salary 52% Contracted Services 47% Supplies/Equipment

Statewide Adjustment Factor Total

Total Proration Factor

UNKNOWN

Gen Ed of Foundation Aid

Special Ed Initial Aid FY 16 And Beyond

Excess Cost Aid

Tuition Adjustments

Calculating State Special Ed Initial Aid

FY 16 and Beyond

68% 52% 47%

Calculating State Special Ed Initial Aid FY 16

Ways

FY 16 and Later State Special Education Initial Aid will be the

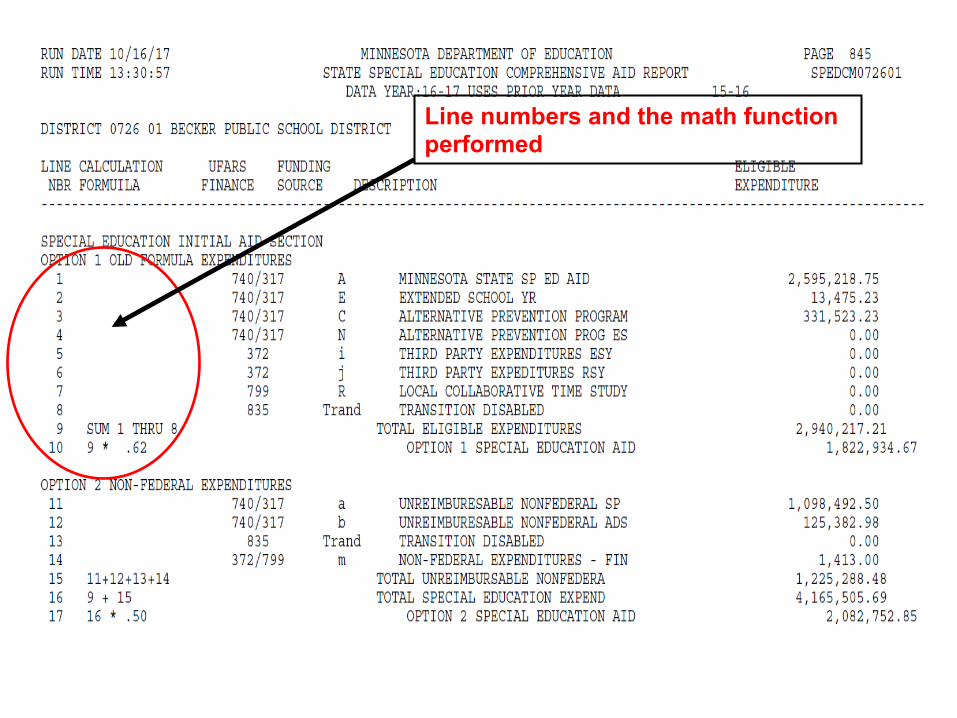

LEAST of …. Option 1. 62% of the district’s old formula sped expenditures, excluding sped transportation expenditures

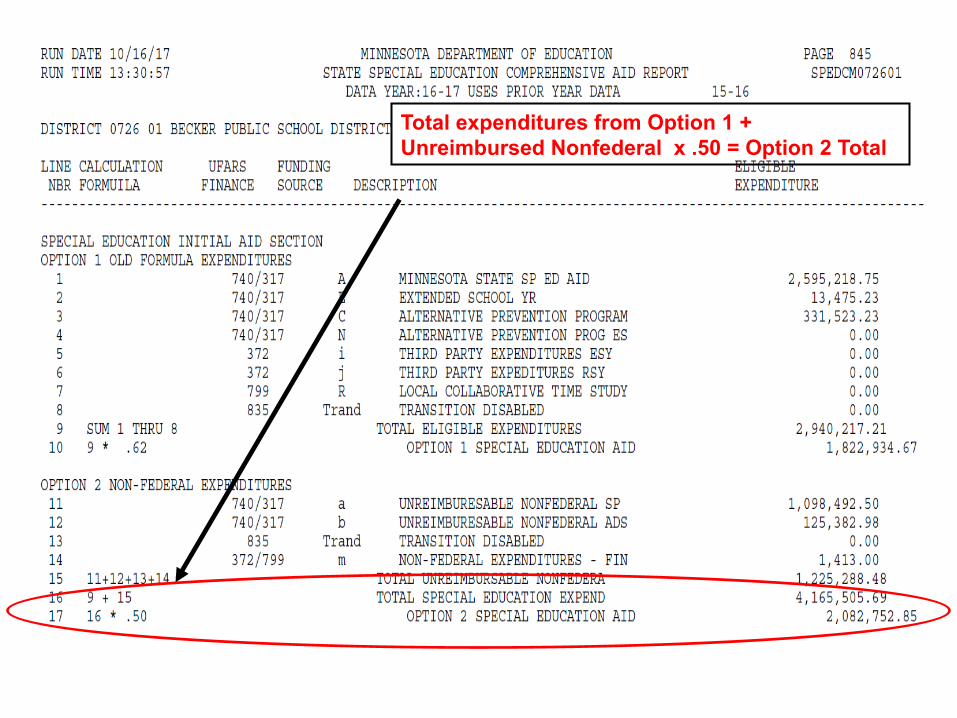

OR Option 2. 50% of the district’s nonfederal special education expenditures, excluding sped transportation expenditures

OR Option 3. 56% of the pupil-based formula calculation

FY 16 and Later

Option 1. 62% of the district’s old formula sped expenditures means…. Expenditures eligible for revenue under 68%+52%+47% formula, plus transition disabled expenditures. You don’t apply the %s for reimbursement… You just add the expenditures you would have used in the old formula and then take 62% of that total.

This calculation uses prior fiscal year expenditures

FY 16 and Later

Option 2. 50% of the district’s nonfederal special education expenditures means… All direct expenditures that are necessary and essential to meet the district’s obligation to provide special instruction and services EXCLUDING expenditures:

• reimbursed with federal funds; • reimbursed with other state aids; • for general ed costs of serving student with a disability; • for facilities; • for pupil transportation; • for postemployment benefits.

Then take 50% of the total for this calculation. This calculation uses prior fiscal year expenditures.

FY 16 and Later

Option 2.

Uses all of the expenditures used in Option 1, plus other expenditures not previously covered (i.e. benefits) Then take 50% of the total for this calculation. This calculation also uses prior fiscal year expenditures.

FY 16 and Later

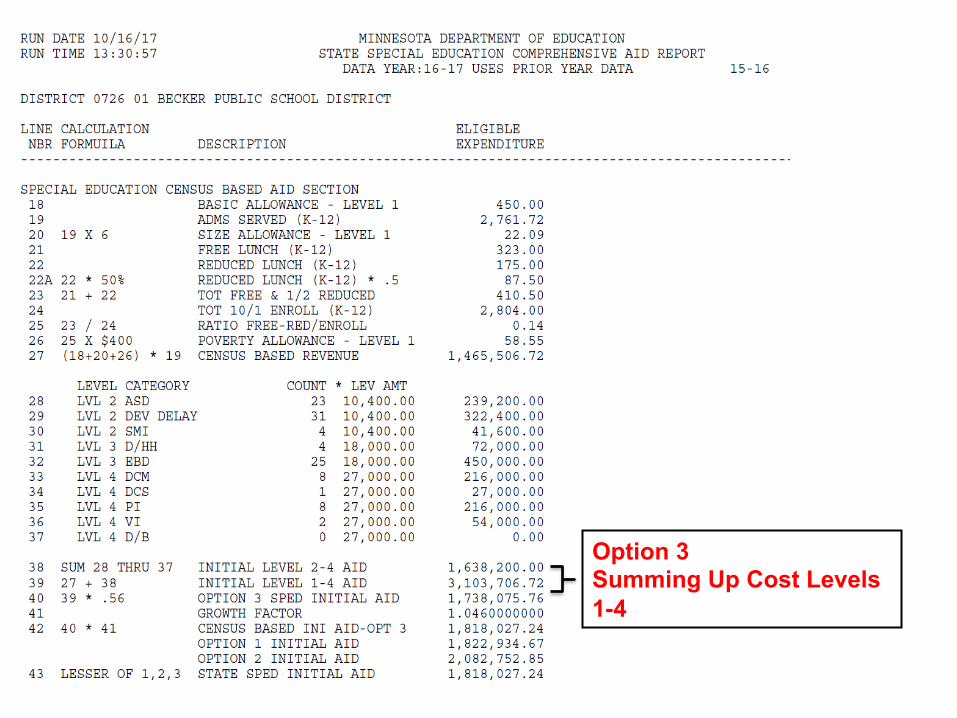

Option 3. 56% of the pupil-based formula calculation.

• Calculations are based on all special education students served in a district. Residency is not considered. • Students’ primary disability area determine what “Cost Level” they are counted in.

Option 3

Cost Level 1 calculation includes various multipliers; ADMs served, Free Lunch Count for (K-12), Half of the Reduced Lunch Count for (K-12) • Various calculations are done with these numbers to get

Cost Level 1 revenue

• Within the ADMs served are ALL students with disabilities SERVED K-12

• This is the ONLY Cost Level in Option 3 that students

served with the primary disability of LD, OHD, TBI, or Speech are counted

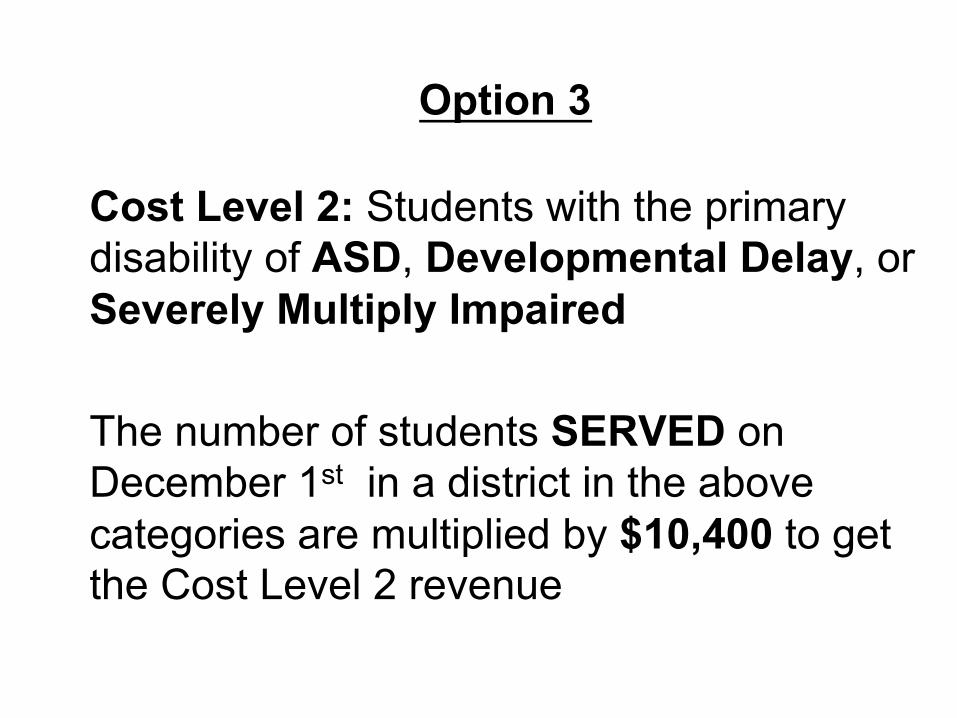

Option 3

Cost Level 2: Students with the primary disability of ASD, Developmental Delay, or Severely Multiply Impaired

The number of students SERVED on December 1st in a district in the above categories are multiplied by $10,400 to get the Cost Level 2 revenue

Option 3

Cost Level 3: Students with the primary disability of DHH or EBD

The number of students SERVED on December 1st in a district in the above categories are multiplied by $18,000 to get the Cost Level 3 revenue

Option 3 Cost Level 4: Students with the primary disability of DCD-Mild, DCD-Severe, Physically Impaired, Visually Impaired, or Deaf/Blind

The number of students SERVED on December 1st in a district in the above categories are multiplied by $27,000 to get the Level 4 revenue

FY 16 and Later State Special Education Aid will be the LEAST of

Option 1. 62% of the district’s old formula sped expenditures

OR Option 2. 50% of the district’s nonfederal sped expenditures

OR Option 3. 56% of the census based formula calculation

Excess Cost Aid

Special Education Transportation Aid

State Special Education Initial Aid

Searching for State Special Ed Aid Reports

Data Center > Data Reports and Analytics > School Finance Reports > Minnesota Funding Reports (MFR)

Data Center > Data Reports and Analytics > School Finance Reports > Minnesota Funding Reports (MFR)

Data Center > Data Reports and Analytics > School Finance Reports > Minnesota Funding Reports (MFR)

ALWAYS Make Copies of Reports… they are NOT archived on MDE’s website

Line numbers and the math function performed

62% of the old formula expenditures

Total expenditures from Option 1 + Unreimbursed Nonfederal x .50 = Option 2 Total

Option 3 Cost Level 1 Calculations

Option 3 Cost Level 2, 3, and 4 Calculations

Option 3 Summing Up Cost Levels 1-4

Growth Factor applied to Cost Level 3

Total Option 3

Lesser of the three options = State Sped Initial Aid

Gen Ed of Foundation Aid

Special Ed Initial Aid FY 16 And Beyond

Excess Cost Aid

Tuition Adjustments

Excess Cost Aid

“A district’s excess cost aid is its initial excess cost aid prorated to the state total excess cost aid by multiplying the district’s initial excess cost aid by the ratio of the state total excess cost aid to initial (uncapped) state total excess cost aid.”

~MN School Finance A Guide for Legislators November 2016

Excess Cost Aid

Provides additional special education funding for districts that have extremely high levels of unreimbursed special education expenses

Excess Cost Aid Changes for FY 16 and Later

The GREATER of: • CALCULATION A: 62% of the difference between the

district’s unreimbursed old formula special education expenditures and 2.5% of the district’s general revenue

OR • CALCULATION B: 56% of the difference between the

district’s unreimbursed nonfederal special ed expenditures and 7.0% of the district’s general revenue

OR

• Zero

Excess Cost Aid Changes for FY 16 and Later

After perfoming the two Calculations, you get the GREATER of the two totals for excess cost aid.

• It is still possible for a district to “not qualify” for excess

cost aid. • The general ed revenue attributed to students in federal

settings greater than 2 will be used in the calculations. Meaning…more revenue is being used to offset the unreimbursed costs!

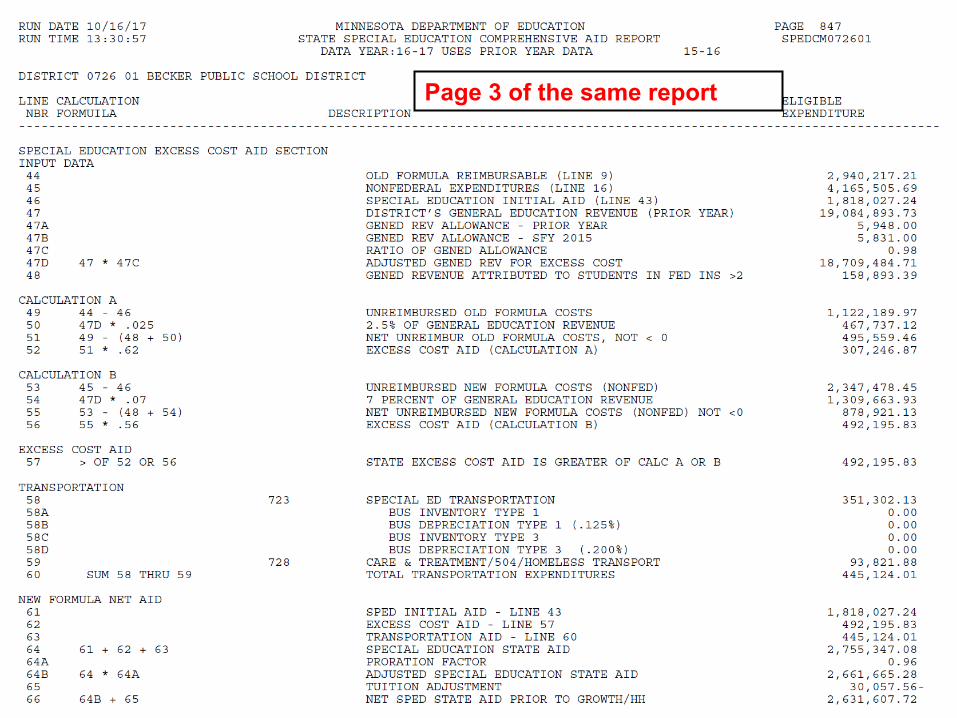

Searching for Excess Cost Aid Reports

Page 3 of the same report

Data to be used in the two calculations

Calculation A

Calculation B

GREATER of A and B = Excess Cost Aid

Page 3

Page 3

Page 3

Page 3

Page 3

Page 3

Page 3

HOLD HARMLESS

GROWTH LIMIT

Page 4

FY 16 (but NOT beyond) MAXIMUM Special Ed Aid must not exceed…

Special ed aid based on old formula

Excess cost aid based on old formula

Tuition Adjustments ADM served $80 (This is referred to as the special ed aid increase limit)

MAXIMUM Special Ed Aid for FY 16

GROWTH LIMIT

GROWTH LIMIT

FY 16 and Later MINIMUM Special Ed Aid must not be less than the lesser…

Special ed aid based on old formula

District’s nonfederal sped OR

expenditures for current FY Excess cost aid based on old formula

Tuition Adjustments

ADM Current Yr ADM FY16

Program Growth Factor *

*1.0 for FY16, 1.046 for FY 17, and the product of 1.046 and the program growth factor for the previous year for FY 18 and later

MINIMUM Special Ed Aid for FY 16 and Later

HOLD HARMLESS

HOLD HARMLESS

FY 17 and Later MAXIMUM Special Ed Aid must not exceed…

ADM served special ed aid increase ($100); add $40 each yr after FY17

Old formula calculation for FY16 (FY stays FY16 for subsequent years)

Excess Cost Aid for FY16 (FY stays FY16 for subsequent years) Tuition Adjustments

Current Year ADM served ADM served FY 16

Program Growth Factor 1.046 (FY 18 1.046 x 1.046) (FY19 is FY18 x 1.046…)

MAXIMUM Special Ed Aid for FY 17 and Later

GROWTH LIMIT

GROWTH LIMIT

• Haven’t had a Minimum and Maximum before • Adjustments are made in February of the

following fiscal year (because it uses current year CY figures)

• Make sure you consider Growth Factor and Hold

Harmless and aren’t surprised with big adjustments!