Sovereign Default, Exit and Contagion in a Monetary Union

40

Sovereign Default, Exit and Contagion in a Monetary Union Sylvester Eijffinger, Michal Kobielarz and Burak Uras (Tilburg University) Belgian Macro Workshop Namur, 12th September 2017 Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 1 / 17

Transcript of Sovereign Default, Exit and Contagion in a Monetary Union

Sovereign Default, Exit and Contagionin a Monetary Union

Sylvester Eijffinger, Michal Kobielarz and Burak Uras(Tilburg University)

Belgian Macro WorkshopNamur, 12th September 2017

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 1 / 17

Introduction

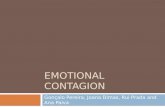

Crisis and Contagion in the Eurozone

2006 2008 2010 2012 2014 2016

0

5

10

15

20

25

30

35

GreecePortugalSpainItaly

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 2 / 17

Introduction

This paper

1 A theoretical framework for analyzing two sovereign decisions:

default on external debt,

exit from a monetary union.

2 Explain contagion within a monetary union:

risk of one country exiting triggers sovereign debt problems in othercountries.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 3 / 17

Introduction

This paper - setup

Small Open Economy dynamic macro model,

SOE issues debt on international financial markets,

SOE is a member of a monetary union.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 4 / 17

Decisions in the Model

Sovereign Default

Government issues bonds on international financial markets,

Each period decision whether to repay debt:

repay - it can issue new bonds,

default - cannot issue:

is banned from international financial markets,suffers an output loss (default penalty).

Government makes the optimal long-run decision, which depends onpast debt and current conditions.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 5 / 17

Decisions in the Model

Sovereign Default

Government issues bonds on international financial markets,

Each period decision whether to repay debt:

repay - it can issue new bonds,

default - cannot issue:

is banned from international financial markets,suffers an output loss (default penalty).

Government makes the optimal long-run decision, which depends onpast debt and current conditions.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 5 / 17

Decisions in the Model

Sovereign Default

Government issues bonds on international financial markets,

Each period decision whether to repay debt:

repay - it can issue new bonds,

default - cannot issue:

is banned from international financial markets,suffers an output loss (default penalty).

Government makes the optimal long-run decision, which depends onpast debt and current conditions.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 5 / 17

Decisions in the Model

Sovereign Default

Government issues bonds on international financial markets,

Each period decision whether to repay debt:

repay - it can issue new bonds,

default - cannot issue:

is banned from international financial markets,suffers an output loss (default penalty).

Government makes the optimal long-run decision, which depends onpast debt and current conditions.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 5 / 17

Decisions in the Model

Monetary Union Exit

There is a nominal friction (wage rigidity) - beneficial to devalue inrecession,

The country is a member of a MU ⇒ fixed exchange rate,

Government may exit the MU and devalue,

but exit is costly, C .

Optimal decision: exit iff

Benefits > Cost

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 6 / 17

Decisions in the Model

Monetary Union Exit

There is a nominal friction (wage rigidity) - beneficial to devalue inrecession,

The country is a member of a MU ⇒ fixed exchange rate,

Government may exit the MU and devalue,

but exit is costly, C .

Optimal decision: exit iff

Benefits > Cost

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 6 / 17

Decisions in the Model

Monetary Union Exit

There is a nominal friction (wage rigidity) - beneficial to devalue inrecession,

The country is a member of a MU ⇒ fixed exchange rate,

Government may exit the MU and devalue,

but exit is costly, C .

Optimal decision: exit iff

Benefits > Cost

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 6 / 17

Decisions in the Model

Monetary Union Exit

There is a nominal friction (wage rigidity) - beneficial to devalue inrecession,

The country is a member of a MU ⇒ fixed exchange rate,

Government may exit the MU and devalue,

but exit is costly, C .

Optimal decision: exit iff

Benefits > Cost

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 6 / 17

Decisions in the Model

Exit cost & benefits

Exit benefits:

relax nominal friction,

debt reduction.

Exit cost in reality - examples:

losses in trade and production,

liquidity issues during transition, potential (domestic andinternational) bank runs,

EMU vs EU membership.

Conclusion: exit cost is unknown!

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 7 / 17

Decisions in the Model

Exit cost & benefits

Exit benefits:

relax nominal friction,

debt reduction.

Exit cost in reality - examples:

losses in trade and production,

liquidity issues during transition, potential (domestic andinternational) bank runs,

EMU vs EU membership.

Conclusion: exit cost is unknown!

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 7 / 17

Decisions in the Model

Exit cost & benefits

Exit benefits:

relax nominal friction,

debt reduction.

Exit cost in reality - examples:

losses in trade and production,

liquidity issues during transition, potential (domestic andinternational) bank runs,

EMU vs EU membership.

Conclusion: exit cost is unknown!

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 7 / 17

Decisions in the Model

Main mechanism - Contagion

Cost of exiting are unknown, C ∈ {CL,CH},

First country exiting reveals the true exit cost,

Exit decisions depend on information available:

With uncertainty ⇒ exit decision against expected cost C e ,After cost revealed ⇒ exit decision with true cost, CL or CH ,

Assumption:CH > C e > Benefits > CL

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 8 / 17

Decisions in the Model

Main mechanism - Contagion

Cost of exiting are unknown, C ∈ {CL,CH},

First country exiting reveals the true exit cost,

Exit decisions depend on information available:

With uncertainty ⇒ exit decision against expected cost C e ,After cost revealed ⇒ exit decision with true cost, CL or CH ,

Assumption:CH > C e > Benefits > CL

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 8 / 17

Decisions in the Model

Main mechanism - Contagion

Rumors about a future exit (of Greece) influence today’s interest rates (forPortugal):

risk of Grexit ⇒ true C revealed before next period decisions,

if C = CL Portugal might exit and devalue,

re-denomination + devaluation = partial default,

investors price it in (today) ⇒ increase in interest rates.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 9 / 17

Decisions in the Model

Main mechanism - Contagion

Rumors about a future exit (of Greece) influence today’s interest rates (forPortugal):

risk of Grexit ⇒ true C revealed before next period decisions,

if C = CL Portugal might exit and devalue,

re-denomination + devaluation = partial default,

investors price it in (today) ⇒ increase in interest rates.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 9 / 17

Decisions in the Model

Main mechanism - Contagion

Rumors about a future exit (of Greece) influence today’s interest rates (forPortugal):

risk of Grexit ⇒ true C revealed before next period decisions,

if C = CL Portugal might exit and devalue,

re-denomination + devaluation = partial default,

investors price it in (today) ⇒ increase in interest rates.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 9 / 17

Decisions in the Model

Main mechanism - Contagion

Rumors about a future exit (of Greece) influence today’s interest rates (forPortugal):

risk of Grexit ⇒ true C revealed before next period decisions,

if C = CL Portugal might exit and devalue,

re-denomination + devaluation = partial default,

investors price it in (today) ⇒ increase in interest rates.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 9 / 17

Decisions in the Model

Main mechanism - Contagion

Rumors about a future exit (of Greece) influence today’s interest rates (forPortugal):

risk of Grexit ⇒ true C revealed before next period decisions,

if C = CL Portugal might exit and devalue,

re-denomination + devaluation = partial default,

investors price it in (today) ⇒ increase in interest rates.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 9 / 17

Model overview & Analysis

Model overview

SOE model a la Schmitt-Grohe & Uribe (JPE, 2016), Na et al. (2017):

SOE issues bonds on international financial markets,

may default on the debt,

downward nominal wage rigidity,

the rigidity may cause involuntary unemployment.

We extend the model with:

SOE is member of a monetary union - fixed exchange rate,

possibility of (costly) exit from the union,

exit allows devaluation and debt reduction.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 10 / 17

Model overview & Analysis

Model overview

SOE model a la Schmitt-Grohe & Uribe (JPE, 2016), Na et al. (2017):

SOE issues bonds on international financial markets,

may default on the debt,

downward nominal wage rigidity,

the rigidity may cause involuntary unemployment.

We extend the model with:

SOE is member of a monetary union - fixed exchange rate,

possibility of (costly) exit from the union,

exit allows devaluation and debt reduction.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 10 / 17

Model overview & Analysis

Quantitative analysis

Benchmark analysis:

Standard calibration - Argentina, calibration

Simulation: 1000 series x 5000 periods,

1 period = 1 quarter

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 11 / 17

Model overview & Analysis

Simulation results more switches

Expectedexit cost

Fraction of simulation serieswith regime switch

EXIT DEFAULT

0.7 99.7% 100%0.8 93.9% 100%1.1 33.0% 100%1.5 3.9% 100%1.9 0.1% 100%2.2 0.0% 100%2.3 0.0% 100%

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 12 / 17

Model overview & Analysis

Quantitative analysis

Benchmark analysis:

Standard calibration - Argentina, calibration

Simulation: 1000 series x 5000 periods,

Contagion experiment:

Take benchmark simulation periods without default/exit,

Introduce a rumors shock - probability that Greece exits before nextperiod (information revelation),

Compare with benchmark simulation.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 13 / 17

Model overview & Analysis

Simulation results - Contagion more

Experiment setup Exit Prob. Additional defaults(%) as % of no-default periods

C e CL CH all periods periods with recessionspositive debt

2.3 0.8 3.8 0 0.78 1.44 4.43

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 14 / 17

Model overview & Analysis

Simulation results - Contagion more

Experiment setup Exit Prob. Additional defaults(%) as % of no-default periods

C e CL CH all periods periods with recessionspositive debt

2.3 0.8 3.8 0 0.78 1.44 4.43

0.78+0.380.38 = 1.44+0.70

0.70 = 4.43+1.001.00 =

Default multipliers: 3.05 3.05 5.43

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 14 / 17

Model overview & Analysis

Simulations - bond prices

-8 -4 0 4 8 120.999

1

1.001

1.002

1.003

1.004Tradable output

-8 -4 0 4 8 120.994

0.996

0.998

1

1.002

1.004

1.006Tradable consumption

-8 -4 0 4 8 12-0.04

-0.035

-0.03

-0.025

-0.02

-0.015Debt level

-8 -4 0 4 8 120.972

0.974

0.976

0.978

0.98

0.982

0.984

0.986Bond prices

baseline simulationsimulation with rumor shockcounterfactual (bond price)

-8 -4 0 4 8 122.1

2.15

2.2

2.25

2.3Nominal Wages

optimal wage (baseline)optimal wage (with shock)

-8 -4 0 4 8 120.074

0.076

0.078

0.08

0.082

0.084Unemployment

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 15 / 17

Model overview & Analysis

Simulations - consumption more

-8 -4 0 4 8 120.999

1

1.001

1.002

1.003

1.004Tradable output

-8 -4 0 4 8 120.994

0.996

0.998

1

1.002

1.004

1.006Tradable consumption

-8 -4 0 4 8 12-0.04

-0.035

-0.03

-0.025

-0.02

-0.015Debt level

-8 -4 0 4 8 120.972

0.974

0.976

0.978

0.98

0.982

0.984

0.986Bond prices

baseline simulationsimulation with rumor shockcounterfactual (bond price)

-8 -4 0 4 8 122.1

2.15

2.2

2.25

2.3Nominal Wages

optimal wage (baseline)optimal wage (with shock)

-8 -4 0 4 8 120.074

0.076

0.078

0.08

0.082

0.084Unemployment

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 16 / 17

Conclusions

Conclusions

Model explaining contagion in a monetary union,

Rumors of a first exit cause debt problems in other countries,

Information friction (uncertainty) generates fragility,

Limiting uncertainty limits space for contagion,

but (potentially) at the cost of more exits.

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 17 / 17

Appendix

Appendix

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 18 / 17

Appendix

Calibration back

Parameter Value Descriptionβ 0.87 Quarterly discount factorr∗ 0.01 Quarterly net world interest rateγ 0.99 Degree of downward nominal wage rigidityδ1 -0.25 Parameters of the output loss functionδ2 0.27CL 0.8 Low exit costCH 3.8 High exit costC e 2.3 Expected cost of exit

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 19 / 17

Appendix

Calibration back

Parameter Value Descriptionσ 2 Inverse of intertemporal elasticity of consumptiona 0.28 Share of tradablesε 0.44 Elasticity of substitution between T and NTα 0.59 Labor share in the non-traded sectorρ 0.932 Serial correlation of ln yT

t

σy 0.037 Standard deviation of innovation to yTt

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 20 / 17

Appendix

Benchmark simulation results back

Expectedexit cost

Consumptionequivalent

Fraction of simulationswith regime switch

EXIT DEFAULT

0.7 8.3% 99.7% 100%0.8 9.4% 93.9% 100%1.1 12.5% 33.0% 100%1.5 16.3% 3.9% 100%1.9 19.8% 0.1% 100%2.2 22.2% 0.0% 100%2.3 23.0% 0.0% 100%

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 21 / 17

Appendix

Benchmark simulation results back

Expectedexit cost

First regime switch

EXIT DEFAULT BOTH

0.7 66.2 33.2 0.60.8 53.5 46.1 0.41.1 22.8 77.1 0.11.5 3.5 96.5 01.9 0 100 02.2 0 100 02.3 0 100 0

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 22 / 17

Appendix

Regime switches in the model

UNION DEFAULT

EXIT AUTARKY

default

default

exit

exit

default &exit

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 23 / 17

Appendix

Simulation results - Contagion back

Experiment setup Exit Prob. Additional defaults(%) as % of no-default periods

C e CL CH all periods periods with recessionspositive debt

2.3 0.8 3.8 0 0.78 1.44 4.43

2.3 0.7 3.9 0 1.20 2.21 6.202.3 1.1 3.5 0 0.42 0.78 1.922.3 1.9 2.7 0 0.25 0.46 0.38

1.5 0.7 2.3 0.00 0.75 1.38 5.061.5 0.8 2.2 0.00 0.43 0.79 4.081.5 1.1 1.9 0.00 0.16 0.30 1.52

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 24 / 17

Appendix

Simulations - unemployment back

-8 -4 0 4 8 120.999

1

1.001

1.002

1.003

1.004Tradable output

-8 -4 0 4 8 120.994

0.996

0.998

1

1.002

1.004

1.006Tradable consumption

-8 -4 0 4 8 12-0.04

-0.035

-0.03

-0.025

-0.02

-0.015Debt level

-8 -4 0 4 8 120.972

0.974

0.976

0.978

0.98

0.982

0.984

0.986Bond prices

baseline simulationsimulation with rumor shockcounterfactual (bond price)

-8 -4 0 4 8 122.1

2.15

2.2

2.25

2.3Nominal Wages

optimal wage (baseline)optimal wage (with shock)

-8 -4 0 4 8 120.074

0.076

0.078

0.08

0.082

0.084Unemployment

Michal Kobielarz (Tilburg) Sovereign Default, Exit & Contagion in MU Namur, 12.09.2017 25 / 17

![Causality and contagion in EMU sovereign debt marketsfirst definition of contagion [(Masson, 1999) and Kaminsky and Reinhart (2000) among others]. Concretely, they examine whether](https://static.fdocuments.in/doc/165x107/5eb86a8c9ce3030c4127be8b/causality-and-contagion-in-emu-sovereign-debt-first-definition-of-contagion-masson.jpg)

![Modelling Long Memory and Default Risk Contagion …fmModelling Long Memory and Default Risk Contagion in Sovereign Bond Markets. Alfonso Mendoza∗ [Early draft] Department of Economics](https://static.fdocuments.in/doc/165x107/5ea002113f565d63a20cd77e/modelling-long-memory-and-default-risk-contagion-fm-modelling-long-memory-and-default.jpg)