Socio-Economic Offences:Nature and Dimensions

25

1 Criminology Socio-Economic Offences:Nature and Dimensions TAX EVASION

Transcript of Socio-Economic Offences:Nature and Dimensions

1

Criminology

Socio-Economic Offences:Nature and Dimensions

TAX EVASION

2

DESCRIPTION OF MODULE:

Items Description of Module

Subject Name Criminology

Paper Name Socio-Economic Offences: Nature and

Dimensions

Module

Name/Title

Tax Evasion

Module Id Cri/SEO/

Objectives

Learning Outcome:

i. To understand the meaning and concept

of tax evasion.

ii. To know the reasons and modes for tax

evasion.

iii. To know and understand the impact of tax

evasion

iv. To know the institutions dealing with the

tax evasion

v. To find the measures to contain the tax

Role Name Affiliation

Principal Investigator Prof. (Dr.) G.S. Bajpai Registrar, National Law

University Delhi

Paper Coordinator Dr. Kavita Singh Associate Professor,

WBNUJS, Kolkata

Content Writer/Author Dr. Sanjay Kumar Assistant Professor,

WBNUJS, Kolkata

Content Reviewer Prof. (Dr.) N. K.

Chakraborty

Director, KIIT Law School,

Bhubaneswar, Orissa

3

evasion

Prerequisites

Key words

4

TABLE OF CONTENTS

I. Tax Evasion- Introduction to the concept ............................................................................... 5

V. Causes of Tax Evasion ........................................................................................................... 14

VI. Methods of Tax Evasion ....................................................................................................... 17

VI. Suggestions ............................................................................................................................ 22

5

TAX EVASION

I. TAX EVASION- INTRODUCTION TO THE CONCEPT

Why Taxes?

Over the Course of human history there are quite few things which would have divided human

opinions taxes have. On one side we have luminaries Adam Smith, the father of modern

economics1 saying "It is not very unreasonable that the rich should contribute to the public

expense, not only in proportion to their revenue, but something more than in that proportion.”

and in the other corner we see titans like Mark Twain quipping in with: the "The only difference

between a tax man and a taxidermist is that the taxidermist leaves the skin." meaning that the

taxpayer leaves nothing and takes everything. As citizens of a developing country like ours, we

are always at the dilemma of whether to pay or not to pay tax.

The history of taxation is as old as tale of great civilizations. The Egyptian Pharaoh's tax

collectors were known as scribes and the taxes were imposed and collected stringently.2 In times

of war the Athenians imposed a tax referred to as eisphora and imposed metoikion, a monthly

poll tax on foreigners, on people who did not have both an Athenian Mother and Father, of one

drachma for men and a half drachma for women.3 Rome imposed customs duties on imports and

exports called portoria and the taxation system of Caesar Augustus is mentioned in the bible and

became the corner stone for the development of inheritance taxes. Chanakya , the great Indian

statesman had also endorsed taxation of citizens.

1 L. Davis, William; Figgins, Bob; Hedengren, David; B. Klein, Daniel (May 2011). "Economics Professors'

Favorite Economic Thinkers, Journals, and Blogs (along with Party and Policy Views)" (PDF). Econ Journal Watch.

8 (2): 133 2 History Of Taxation available at http://www.taxworld.org/History/TaxHistory.htm 3 Ibid

6

As citizens of a welfare state we expect the government to provide us with all the facilities, we

expect good roads, subsidized fuels, healthcare at affordable rates, state of the art universities

and above all its the dream of every common Indian to land a government job. Now the

government cannot keep printing currency notes to discharge all the above functions. this is

where the relevance of the taxes come in as the great American jurist Justice Oliver Wendell

Holmes who pointed out “I hate paying taxes. But I love the civilization they give me”. taxes are

the necessary evil by which we gift ourselves health care through Government hospitals (usually

they offer service without any cost), Education (In Municipal and Government schools the fee is

negligible), cooking gas at concessional rate , employ lakhs of employees in various

departments and secure our borders with sufficient arms and ammunitions so that we can live a

happy and peaceful life.

COMPLIANCE WITH TAXATION MEASURES; PLANNING VS AVOIDANCE VS EVASION

Most of the civilised nations, if not all, levy taxes on their citizens to meet their running

expenses. What the government does through legislation is imposition of taxes. Adapting the

popular idiom, government proposes and citizen disposes is the present tax scenario in the

nation. 5.16 crore people which is just 4.1 per cent of the over 125 crore population pays taxes in

India, in contrast, in the U.S., about 45 per cent of the population pays taxes showing the dismal

rate of tax collection and the absence of a tax culture in our country4. In an ideal scenario all the

individuals will be taxed according to their capacity and pay will what is levied on them.

However the law is never a rigid system which has a one size fits all formula.

Tax Planning

Let's admit that government is no Count Dracula who is satisfied only by sucking the poor

citizen dry of all his earnings. The legislation allow deductions and exemptions from payment of

4 'Why should I pay tax? available at www.incometaxindia.gov.in/Charts Tables/Why should I pay tax.htm

7

taxes to incentivise certain priority measures of government, eking out maximum benefit out of

such benevolent provisions is tax planning. Subject to certain limits the government allows

exemption from payment of taxes by non levy of taxes on pension plans, life insurance policy,

medical insurance, home loans, education loans, long term capital gains etc. If one is able to

claim full deductions under all the heads of the Income Tax Act the total non-taxable income is

pegged at 10.75 lakhs.5 An intelligent tax planning lets one of the hook of the tax man, at the

same time complying with the letter and spirit of the law. If the assessee goes for tax planning, it

is win-win situation for everyone including the Stateas planning is both compliance and savings .

Tax Avoidance and Tax Evasion

“The difference between tax avoidance and tax evasion is the thickness of a prison wall.”6, said

Denis Healey the former UK Chancellor of the Exchequer. What the ex-tax man meant was that

the evader goes behind bars whilst avoider manages to stay outside. Tax avoidance, though

seems closer to tax evasion, is rather related to tax planning than the former. Tax avoidance, as

the term suggests is brazen non payment of taxes by exploiting loopholes in the taxation

machinery. Though there is no violation of the letter of the law the but the spirit of law is given a

go by. In short, an assessee essentially exploits the loophole that enables him them to pay tax at

on a lesser amount rate than what was initially due. Since this act merely involves finding and

exploiting a gap in the fiscal provision, it is not usually construed to be strictly illegal because it

usually enables the assessee to be legally exempted from the payment of tax.

5 What is the Maximum Income Tax You can Save for FY 2015-16? available at http://apnaplan.com/max-income-

tax-saving-fy2015/# 6 As quoted by Craig Elliffe, The Thickness of a Prison Wall - When Does Tax Avoidance Become a Criminal

Offence? New Zealand Business Law Quarterly, Vol. 17, No. 4, pp. 441-466, December 2011

8

The Black's Law Dictionary defines tax evasion as "Illegally paying less in taxes than the law

permits; committing fraud in filing or paying taxes"7. The deliberate fraud committed by a

person who is liable to pay taxes by non payment is tax evasion and the evader runs the risk of

prosecution and penalty. In simple terms, tax evasion means suppressing or minimising the tax

liability by using unlawful means. Unlike tax avoidance which is a legal act, tax evasion is illegal

and involves “exploiting a tax advantage that Parliament never intended”8 In the judgment of

CIT v. Raman & Co.9 , the Supreme Court held:

“Avoidance of tax liability by so arranging commercial affairs that charge of tax is distributed is

not prohibited. A taxpayer may resort to a device to divert the income before it accrues or arises

to him. Effectiveness of the device does not depend not upon considerations of morality, but on

the operation of the Income Tax Act. Legislative injunction in taxing statutes may not, except on

peril of penalty, be violated, but it may lawfully be circumvented.”

In the judgment case of Union of India v. Azadi Bachao Andolan10 , the Apex Court has

reaffirmed the right of the assessee to mitigate the payment of tax as long as it is done by

legitimate and legal means and measures. Similarly, in the case of Vodafone International

Holdings v. Union of India & Another11, the Court agreed with the Westminster principle,

evolved in England, stating that every tax payer has the right to manage their tax liability and

consequently, efficient tax management cannot be penalized.

7 Black's Law Dictionary 6th Edn. 1990 8 Ben Chu, David Cameron offshore investment fund: What is the difference between tax avoidance and tax

evasion? (April 8, 2016) available at http://www.independent.co.uk/news/uk/politics/what-difference-between-tax-

avoidance-evasion-david-cameron-offshore-panama-papers-a6974791.html 9 67 ITR 11, 17(SC) 10 (2004) 10 SCC 1 11 (2012) 6 SCC 613

9

In Vodafone International Holdings Case12, the Court held that “whether a transaction is used

principally as a colourable device for the distribution of earnings, profits and gains, is determined

by a review of all the facts and circumstances surrounding the transaction... It is in the above

cases that the principle of lifting the corporate veil or the doctrine of substance over form or the

concept of beneficial ownership or the concept of alter ego arises. Thus it is the facts and

circumstances which decides on whether or not one is found guilty of tax evasion or saves

himself due to gaps in the tax net.

II. Tax Evasion And The Evil Of Black Money

A common saying in the country side which goes like "evil breeds evil", one which is true about

the evil of tax evasion also. The evil of tax evasion breeds greater evil in the form of black

money, economic destabilization measures like this is capable of bringing down entire nations

down, infact the entire economy of the Delhi Sultanate faced severe crisis due to counterfeit

currency that flooded the markets.13 Black money has defined as assets or resources that have

neither been reported to the public authorities at the time of their generation nor disclosed at

any point of time during their possession14. In its 1985 report on Aspects of Black Economy, the

National Institute of Public Finance and Policy (NIPFP). defined ‘black income’ as ‘the

aggregates of incomes which are taxable but not reported to the tax authorities’.15

"Black" Black money and "White" Black Money

12 Ibid 13 Chandra, Satish (2004). Medieval India: From Sultanat to the Mughals-Delhi Sultanat (1206-1526) - Part One.

Har-Anand Publications. ISBN 9788124110645. at p105 14 White Paper on Black Money (the Paper) table by Finance Minister in the Lok Sabha on May 21, 2012 para

2.1.1 15 As cited by White Paper on Black Money (the Paper) table by Finance Minister in the Lok Sabha on May 21,

2012 at para 2.1.2

10

Black money can actually be classified as Black money begotten by legitimate ways and black

money amassed by legitimate means. The first type the "black" black money is that the money

may have been generated through illegitimate activities not permissible under the law, like

crime, drug trade, terrorism, and corruption, all of which are punishable under the legal

framework of the state. The "white" black money on the other hand is begotten by through

perfectly legitimate and otherwise permissible activities under the law of the land but s/he has

failed to report the income so generated, comply with the tax requirements, or pay the dues to

the public exchequer, leading to the generation of this wealth16. The first type is illegal income

gained by illegal means while the second type covers legal income that is concealed from public

authorities. The effect of the former is direct and is quite detrimental to the economy as the

promotion of illegal activities funds terrorism, drug trafficking and the dubious underworld

ecosystem, the latter is an indirect threat as its effect is felt due to the adverse effects on the

economy leading to a dysfunction in the whole system of cash flow.

III. The Tax Payer And The Evader, A Classic Crow - Cuckoo Story.

The Cuckoo is wily bird, it lays the eggs in the crows nest leaving the poor crow to go though all

trails and tribulations of incubating the eggs. Once the cuckoo chick is born it feeds out of the

hard work of the crow to the detriment of the little crows, as a free rider its entire growth is a to

the detriment of the crows on chicks. The tax evader is a free rider like this. He doesn’t

contribute as he is expected to contribute but drains out the precious government resources

funded by the honest tax payer. Since taxes are used for the purpose of providing public benefit

welfare measures, tax evasion by persons implies that these persons the evaders avail of the

general benefits of welfare measures of conferred to them by the government, executed by

making use of the compliant taxpayers’ money, without contributing anything towards the

16 Ibid para 1.3.1

11

exchequer. The classic cuckoo - crow story is repeated in the great Indian stage with the crooked

evader being the cuckoo who raises his offspring solely on the effort of the crow who is the

honest tax payer. while these persons who are evading tax are not complying with it and

nevertheless receiving public benefits

In developing and under-developed economies taxes are a matter of life and death, in such

economies evasion entails there is not just an economic costs but also a social cost associated in

relation to the evil of with tax evasion.17 In the absence of the tax income filling its coffers the

State is unable to foot the bill of its welfare measures resulting in cuts in allocation of funds for

such projects and the honest tax payer is made to pay for such evaders. The social impact of tax

evasion is much like the dejection felt by a crow chick, the evader grows more and more while

the complaint tax payer loses whatever little he had. It is said that the evil in the world is not due

to a few bad men but due to the complacency of the score of good men. The more the commoner

snuggle under this cozy blanket blissful ignorance higher will be the price he pays.

IV. Aam Aadmi And Tax Evasion; The Parable Of The Boiled Frog.

Of the 125 crore people in India only 4.5% pays taxes, the question that the 95.5 % of common

men raises when they hear about tax evasion and black money is the archetypal "chod do, hame

kya? ", as tax laws are of no concern for them. Kids are taught the tale of the frog who enjoyed

the rising warmth of the slowly heated vessel. The warmth felt good, a bit later, it felt like a

steam bath draining away energy and deepening the frog's relaxation while the water is getting

hotter and hotter. By the time the frog realizes its danger, it is too late to take action and the

dumb frog perished in boiling water. The aam aadmi is like the frog and the shadow economy

created by tax evasion and infested with black money is the slowly boiling water. The common

17 Matthew Timms, “The true costs of tax avoidance”, World Finance, available at

http://www.worldfinance.com/strategy/the-true-costs-of-tax-avoidance

12

man though might not feel the pinch of this arcane National Sport of India’18 but he stands to

lose all as its only a matter of time before the field gets too hot to take remedial action.

Impact Of Evasion On State Revenue And Welfare Measures

One of the important function of the tax is the mobilization of resources from rich to poor and

bridging the gap between the rich and the poor. As the tax evasion immediate effect is the loss of

revenue to the State which adversely affect the power to state to spend more on the poor and to

ensure welfare of the people. Though the government might not have delivered us the promised

land flowing with milk and honey we cannot fail to see the governmental initiatives that touch

every phase of our lives. The doctors who touch us the moment we are born are learn their trade

at hugely subsidized prices, the schools run by the government light the lamp of learning in the

minds of lakhs of kids, though the public transport fails to make ends meet they ensure that the

citizen remains unburdened, the doctors, the teachers, the judges, the policemen, the firefighter

and scores of other government servants on whom we rely on in our journey from cradle to grave

are paid by the government. We raise hue and cry when fuel prices increase, we take to streets

when subsidized gas cylinders are capped, we declare bandhs when transport fares are hiked.

What we sometimes opt to forget is that the government needs revenue to provide these

facilities. The expenditure if not recouped by tax revenue will empty the government coffers and

will be the toll the death knell of the government subsidies. It’s the tax payer who gifts himself,

through taxes, all these perks and the day this payment stops we will have to wake to the grim

realty of having killed the golden goose of welfare measures for greed.

Impact Of Evasion Of Public, Peace And Morality

18 Tushar Dhara & Cherian Thomas, ‘ In India, Tax Evasion Is a National Sport’ Bloomberg Business week (July

29, 2011) available at http://www.bloomberg.com/news/articles/2011-07-28/in-india-tax-evasion-is-a-national-sport

13

More direct than expected is the impact of the illegally obtained black money in the everyday

life of the common citizen. Black money arising from illegal activities such as crime and

corruption fosters an underground parallel economy that is anti-social. The black money

amassed by racketeering, trafficking in counterfeit and contraband goods, smuggling, production

and trade of narcotics, forgery, illegal mining, illegal felling of forests, illicit liquor trade,

robbery, kidnapping, human trafficking, sexual exploitation and prostitution, cheating and

financial fraud, embezzlement, drug money, bank frauds, and illegal trade in arms are more than

capable of disturbing the public peace, law and order and morality. The smugglers, the dacoits

and the terrorists who are the beneficiaries of this shadow economy will deliver nightmares to

our country. The ‘corrupt’ component of black money stemming from bribery and illicit

gratification by those holding public office results in an system failure where the citizen must

bribe to get his pound of flesh, despite it being a right vested in him to avail the same.

The Impact Of evasion On Economy.

Currency is but a random piece of paper if it loses its purchasing power. Money unaccounted for

is capable of creating large scale infaltionationary pressure on the economy resulting in loss of

purchasing power of currency. The impact of food inflation and inflation of prices of essential

commodities on the common man is a topic over which much ink is spilt and its always the poor

that suffers due to such market disturbances. A case in point is the real estate sector where the

large scale influx of black money has resulted in property prices shooting through the roof and

pricing the common out of the race to buy property. Another effect of black money is the impact

it causes on the GDP of the country. It causes an adverse impact on the GDP as a huge part of the

14

income is diverted to another economy not being the home economy resulting in deficient GDP,

thereby depicting a faulty picture of the economy and hiding real state of affairs.19

V. CAUSES OF TAX EVASION

There could be various reasons which could possibly be causing tax evasion resulting in the

creation of black money in India. Some of them are-

1. A High Burden Of Taxation:- High tax rates either actual or perceived, provides a

strong temptation to evade taxes and generate black money. Taking a look at the past, the

present marginal income tax rate capped at around 34.6%20 is not substantial when

compared to the astronomical going upto 97.75%21 marginal income tax rate including

surcharge) in seventies. Despite the steep decrease in the tax rates, its ironic that the

perception that is persisting is one of high tax rates. The high rate of taxes creates greater

incentive for non compliance of the tax laws, as high rate adversely affect the disposable

income in their hands. The people evades taxes is because of the high rates of the taxes

and this a phenomenon which is common in almost all kind of taxes whether being

income tax, sales tax, excise duties, custom duties, corporate taxes, etc. Moreover the

increase in the burden of taxation, as well as the burden of complying with the laws is a

strong reason for getting tempted to be a part in tax evasion

2. Culture and social practices : In a society where tax evasion and under-reporting of

activities and income is perceived to be very common or the norm, such activities may be

considered acceptable and honest tax compliance and paying one’s due share to the

public fund may not be considered a virtue.

19 Sukanta Sarkar, “The Parallel Economy In India: Causes, Impacts And Government Initiatives”, Economic

Journal of Development Issues, Vol. 11 & 12 No. 1-2 (2010) 20 Income tax rate 30%, surcharge 12% and Edu. cess 3%. 21 Income tax rate 85%, surcharge 15%. Chathurvedi and Pithisaria Income tax Law 5th edn. Vol I (1998) p 219-

220

15

3. Ineffective enforcement of laws- It is found that more often than not, the enforcement

of laws that regulate taxation- Income Tax Act, Sales Tax, Excise Duty, etc. are not very

efficiently enforced. Due to lukewarm enforcement of such provisions as well as

abundant exploitation of the loopholes and gaps in these creates no deternce and makes

the tax evasion fearless. and thereby creation of parallel economy has become very easy.

4. Unregulated sector or informal economy- Economy can be divided into two sections-

formal and informal. Informal economy is that part of the economy which is largely

unregulated by the enforcement agencies. A large part of the Indian economy comprises

of the informal sector which essentially implies that there is a large area of the Indian

economy which is uncovered by the enforcement agencies mainly because regulating this

sector is extremely difficult and to a certain extent, not even possible. It is primarily in

this section of the economy that most cases of evasion take place. Since it is largely

unregulated, the ease to carry out unscrupulous transactions is in fact quite high. An

example is that of jewelry sector or the real estate sector wherein in most transactions are

done in cash and barely an regulatory mechanism exists to monitor the large volume of

money that flows through these key sectors.

5. Corruption- The corruption leads to tax evasion as the person getting the income by way

of corrupt practice is hardly going to disclose the income and its source to the State. The

disclosure on his part not only invite tax burden but also the punitive action under the

relevant laws and loss of job too. Since most people are aware of the rampant corruption

that exists, according to them evading tax is easier and financially also viable. By paying

a minimal amount in lieu of ensuring that the same is carried out without any hassle.

6. Corrupt Business practices:- With the advent of globalization, liberalization and

privatization the industries started mushrooming in the country along with them came

16

the whole scale bribery to the officials by way of secret commission, speed money, on-

money, pugree etc.22 The cases like Wa

7. Lack of stringent penal provisions. – The tax statute hardly makes the stringent penal

provisons in case of evasion. Since the penalty amounts are also low, evading taxes is

easier and financially lucrative owing to the fact that penalty is much lesser than the tax

they would have paid on the earnings had the same not been evaded.

8. Lack of banking infrastructure and overreliance on cash economy:- The majority of

transactions in India are still made though cash making it an easy route to launder money.

The lack of penetration of effective banking facilities has meant that the people find it

more convenient to transact in cash than through banks where it is easier to trace.

9. Deterioration in moral standards- In the earlier days people owed respect for their

king or ruler and were more governed by fear of getting caught and get punished but with

passage of time both fear and respect have faded away and now people are not any more

transparent or honest and have found out various ways in which they can accumulate and

generate unaccounted money or black money. The people were more united and were

more disciplined as they worked in coordination as a unit, they were honest and

transparent and were not tainted with jealousy and worked for a common goal.They were

willing to share the reaps of their hard labour with every member of the society which is

not the present case in our society. In contrast, the people are now self centered and are

only working for their own good and do not think about the society or the country as a

whole.

10. Evasion of one tax leads to evasion of another tax- Where assessed suppress the

production or manipulate the price , it will lead to evasion of excise duty, sale tax,

income tax and other taxes on the goods.

22 K.N Wanchoo Committee Report chapter 2, para 2.20 (d)

17

11. Non Compliance of general laws:- Sometimes the people do not intend to evade taxes,

however while making non compliance of non tax laws, they evade the taxes unwillingly.

For example to evade payment of other statutory contributions, to evade compliance with

the provisions of industrial laws such as the Industrial Dispute Act 1947, Minimum

Wages Act 1948, Payment of Bonus Act 1936, Factories Act 1948, and Contract Labour

(Regulation and Abolition) Act 1970, and / or to evade compliance with other laws and

administrative procedures.

VI. METHODS OF TAX EVASION

Now that we know that tax evasion is an extremely common phenomenon and is also deliberate

in nature, let us look at the methods that the assesses employ for evading taxes. Evasion could

take place by way of the following methods-

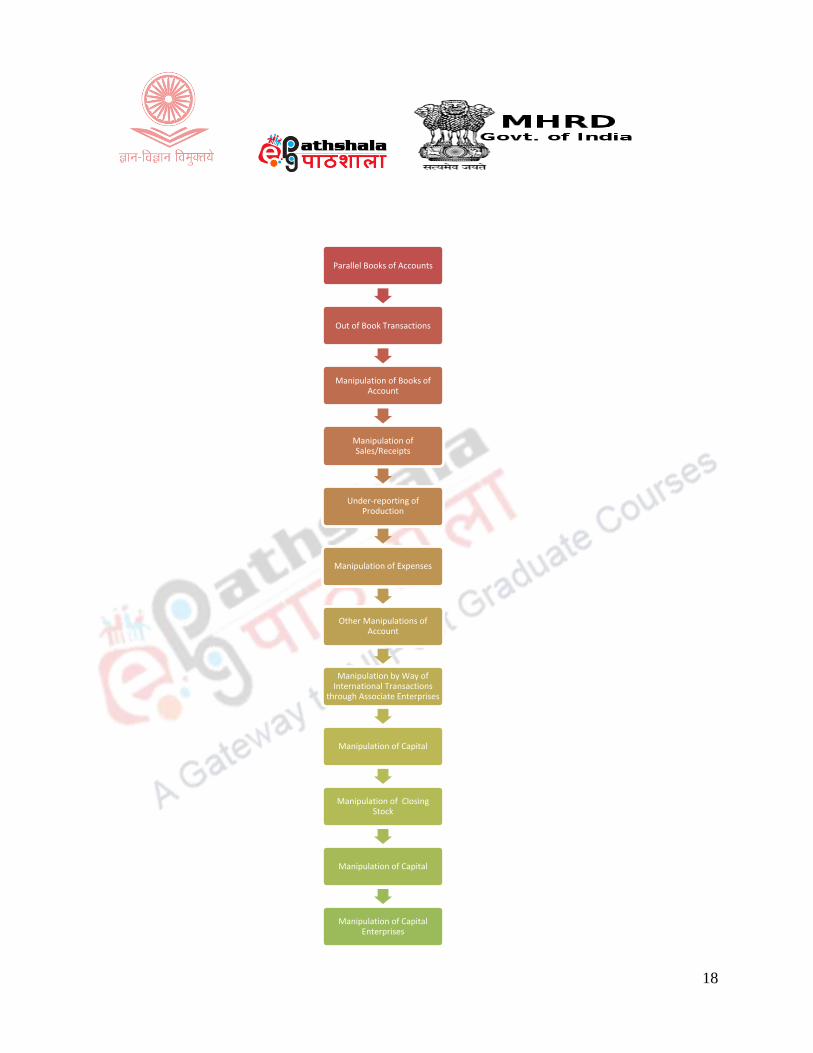

1. Manipulating transactions- This is the most commonly adopted method of evading tax,

owing to the ease in the transaction. The tax payer usually does not maintain a proper

account of income or the receipts which may be subject to taxation and manipultes the

books of accounts through any of the following methods23-

23 White Paper on Black Money (the Paper) table by Finance Minister in the Lok Sabha on May 21, 2012

18

Parallel Books of Accounts

Out of Book Transactions

Manipulation of Books of Account

Manipulation of Sales/Receipts

Under-reporting of Production

Manipulation of Expenses

Other Manipulations of Account

Manipulation by Way of International Transactions

through Associate Enterprises

Manipulation of Capital

Manipulation of Closing Stock

Manipulation of Capital

Manipulation of Capital Enterprises

19

2. Transfer pricing- Apart from manipulating accounts, another method of reducing tax

liability is by way of transfer pricing. This pertains to the manner in which the companies

carry out transactions among their affiliates transcending territorial boundaries. The

companies in this case, essentially, by way of efficient trade planning, shift the proceeds

of their business to countries with lower tax rates, thereby reducing their effective tax

liability. This money which is routed overseas is transferred back to India by way of

Foreign Direct Investment, etc.

3. Share price rigging- Initial Public Offerings (referred to as “IPOs”), offer a lot of scope

for embezzlement of funds resulting in reduction of tax liability. Usually, there is a shell

company created for this purpose which entails investment by offshore companies or

individuals in foreign tax jurisdictions in the shares offered by IPO. Thereafter these

artificially escalate this trading price and sell it off later at the cost of ordinary investors.

4. Tax Havens- While this term lacks a precise definition OECD has previously provided it

as something that is “characterized by no or very low taxes, lack of effective exchange of

information, and lack of transparency about substantial activities.” However, due to lack

of regulation and vigilance that is exercised over these and the almost negligible rate of

taxation imposed in these countries they have come to become ‘offshore financial centers'

(OFCs).

5. Non-profit Sector: Taxation laws confers some benefits for promoting charitable

activities. The lack of proper monitoring in this sector has lead to misuse of the funds

funneled through the non profit sector.

6. Routing through vulnerable sector- Certain sectors of the economy offer ample of

opportunity to indulge in evasion of tax, consequently in the generation of black money

in the economy. Real estate sector, wherein under-reporting of transactions owing to high

market price in the real estate sector and the proportionately high tax incidents, has lately

evidenced undervaluation of transactions to avoid the payment of taxes. Further, gold

20

bullion and jewellery market transactions also provide the space to carry out transactions

which can effectively avoid payment of taxes. Usually in such transactions, buyer has the

scope of legally bringing in black money which was parked safely till now, into the

economy. While the seller can, by way of cash transactions save on tax by not putting the

transaction on record.

Tax Evasion

Manipulation of Accounts

Out of Book/Parallel reporting of transactions

Manipulation of sales/receipts

Under-reporting transactionsTransfer Pricing

Tax Havens

Share Price Rigging

Routing through vulnerable sectors

21

VII. INSTITUTIONS DEALING WITH TAX EVASIONS .

There are many institutions which have been set from time to time under the different laws for

dealing with tax evasion and related issues. The agencies which are directly related with tax

evasion are as under.

1. Central Board Of Excise And Customs

The Central Board of Excise and Customs ( hereinafter referred as CBEC), constituted under the

Central Boards of Revenue Act,1963, is the apex body for the administration of indirect tax laws

enacted by the union government. The Board deals with the work of formulating policy relating

to levy and collection of Customs & Central Excise duties and Service Taxes, preventing

smuggling, and doing work related to administration of matters in the sphere of customs, Central

Excise, Service Tax and narcotics within the ambit and purview of the Board.24

2. Central Board Of Direct Taxes

The Central Board of Direct Taxes (hereinafter referred as CBDT), constituted under the Central

Boards of Revenue Act,1963, is the apex body for administration various direct taxes being

imposed by the union governemnet. The board also lay down the broader policy for the direct

taxes in India. 25

3. Enforcement Directorate:

The Directorate of Enforcement was established in the year 1956, it was initially

established to manage and control the provisions relating to the Foreign Exchange

Regulation Act,1973 but after the Act got repealed and got substituted by the Foreign

Exchange Management Act,1999 (FEMA) which came into effect from 1st June,2000. The

24 White Paper on Black Money (the Paper) table by Finance Minister in the Lok Sabha on May 21, 2012 25 Ibid

22

Enforcement Directorate hereinafter referred as ED is entrusted with the duty of

enforcement of the Foreign Exchange Management Act, 1999 herein after referred as

FEMA and some specific provisions of the Prevention of Money Laundering Act herein after

referred as PMLA , it is under the control of the Department of Revenue for the operational

purposes with regard to administration. At present it is empowered to investigate and

prosecute the offences that are related to money laundering as well to confiscate or attach any

property that has been obtained with the proceeds of the crime as Stated under the Prevention

of Money Laundering Act,2002.26

VI. SUGGESTIONS

The tax evasion leads to black money. The immense growth of black money is having an

adverse effect on the economy, on the society and the person residing in the country. It has also

become a threat to the security of the country as the black money is being used to fund the anti

social entities like terrorism. The persons are evolving various means and ways for evading taxes

and adversely effecting the society, social structure, economic growth and development of the

country as a whole. A few measures that can be adopted to root out the evil of tax evasion are

1. Simplification of the tax laws: "The hardest thing to understand in the world is the

income tax, said Albert Einstein. Sheer complexity of the Tax laws makes it a Herculean

task to understand it and maneuver through its murky currents. The outrageous number of

amendments to tax laws brought year after year makes it even more complex. A simple

system which can easily be communicated and understood will definitely change the

perception that people have towards the tax laws and this positive social perception is

paramount in ensuring revenue through taxes.

26 government of india, ministry of finance department of revenue ,ed(enforcement directorate), available at<

http://dor.gov.in/ed_pml> last accessed 12.6.2016

23

2. To have moderate rate of taxes- Tax rates may be reduced as it may prima facie seem

plausible considering high tax rates are often understood to be on the of the principal

causes behind evasion of taxes. Low tax rates provides incentive for tax compliance and

create heavy disincentive for non compliance coupled with heavy penalty

3. Deterrent Penalty : Law according to Austen is the command of the sovereign with a

sanction behind it. The sanctions under the current tax laws aren't having enough the

expected deterrence to ensure compliance. Lessons can be leant from criminalization of

cheque bouncing which brought out a radical impact.27 The threat of criminal prosecution

and a possible jail term if coupled with astronomic fines can have a deterrent effect in the

minds of prospective evaders.

4. Improvement Of Banking Infrastructure and Promotion of Plastic Money : The

economy of India is still reliant on cash transaction as opposed to plastic money. The

lion's share of cash transactions that take place are untraceable and results in large scale

evasion in vulnerable industries like jewelry , bullion and real estate. By bringing the

entire nation within the banking umbrella is the first step to move away from a cash

economy. Post offices which have reach to each and every nook and corner of the nation

can be made the nodal agency to ensure that every Indian is connected to the banking

system.

Unlike cash which is untraceable, transactions through cards make it sure that money

changing hands is traceable by government and can be taxed appropriately. The current

system of surcharge on card transactions acts as a disincentive to this much useful mode

of efficient tax governance. Promotion of plastic money by incentivizing it can go a long

way in reducing the size of cash economy and widening the tax net.

27 Centre for Civil Society, Criminalizing Cheque Bounce Cases – An effective remedy available at

ccs.in/sites/default/files/research/research-criminalizing-cheque-bounce-cases.pdf

24

5. Promotion of awareness : Awareness of a law leads to compliance with the laws. Tax

and tax laws belong to that part of public mind which is considered murky and unclear. A

genuine lack of awareness about taxation and tax laws prevail in the country. Grass root

level awareness programmes which familiarizes the common citizen with the workings of

the tax machinery can create a better social perception about the taxes that are levied on

them.

Addition of taxation and tax laws as part of the curriculum at the secondary level or any

other appropriate level can being out a generation who knows why and how they are

taxed. Such education will lay foundations in young minds on the importance of taxation,

impact of evasion etc resulting in positive social perception on taxation.

6. Better enforcement of existing laws : we have a large number of laws which aid to

prevent evasion, the sheer number of legislations have not brought the evasion to the

extent that they were expected to. Corruption a major cause of tax evasion is sought to be

tackled through the Prevention of Corruption Act 1988, the Prevention of Money

Laundering Act, 2002 intends to curtail money laundering, The Black Money

(Undisclosed Foreign Income And Assets) And Imposition Of Tax Act, 2015 is aimed

directly at black money. Despite having so many laws, the mischief sough to be remedied

is persistent due to poor enforcement regime. An iron fisted enforcement of existing laws

can ensure that the legislative intention behind current laws is realized.

7. Changing the social perception about taxes : " How is the state mirrored in citizens’

minds? This is the question with which any investigation about the discipline that citizens

exercise over their tax paying behaviour must start. Consciousness about the state leads to

citizens’ civic and tax ‘sentiments’ and to a fundamental attitude with regard to problems

of ‘their’ state." (Schmolders, 1960, p. 38)28. As rightly pointed out, the negative social

28 As quoted by Erich Kirchler, The Economic Psychology of Tax Behaviour 2009, p 29

25

perception about taxes must change and a positive idea of a State's needs being

understood by people must settle in the minds of citizens. The initiative of Indian

Railways to mention the subsidy information on railway tickets is a step in this direction.

When the citizen is told or shown how much the government does for him out of the tax

money, he would be more inclined to pay his taxes. Ensuring that the target group

benefits out of government welfare programmes will also aid in creating a feeling of

contentment resulting in better realization of taxes.

In the end the realization that tax evasion is nothing but daylight robbery is what one should

understand. The temporary gain of today is a seed of destruction which would engulf the

economy tomorrow and would leave the but phantom of a once great nation. As Dwight

Eisenhower, pointed out "… we … must avoid the impulse to live only for today, plundering for

our own ease and convenience the precious resources of tomorrow". Finally, the tax policy

should be oriented to make the life of tax payer comfortable and of tax evader difficult,

miserable and hell. This can be done through the strong political will and zero tolerance policy

as to evasion.